Savings in Transition (Final) - Sanlam Shared Documents... · Savings in Transition ... Birla...

24

Savings in Transition UBS Financial Services Conference 2007 Johan van Zyl Savings in Utopia y Savings in Utopia ~ Insights into the following questions: | Where does Sanlam see the future growth potential in respect of the various savings markets in which it operates? | What is the group’s associated strategies to penetrate these markets, and grow its market share? | And lastly, what are the associated opportunities and risks? y At Sanlam, we see the current savings environment in transition, and are gearing up our capabilities to make the most of these anticipated changes y To understand our outlook for savings, and answers to the above- mentioned questions, one needs to understand our strategy…

Transcript of Savings in Transition (Final) - Sanlam Shared Documents... · Savings in Transition ... Birla...

Savings in TransitionUBS Financial Services Conference 2007

Johan van Zyl

Savings in Utopia

Savings in Utopia ~ Insights into the following questions:Where does Sanlam see the future growth potential in respect of the various savings markets in which it operates? What is the group’s associated strategies to penetrate these markets, and grow its market share?And lastly, what are the associated opportunities and risks?

At Sanlam, we see the current savings environment in transition, and are gearing up our capabilities to make the most of these anticipated changes

To understand our outlook for savings, and answers to the above-mentioned questions, one needs to understand our strategy…

Agenda

Strategy — Client centricity

Changing savings environment

Retail Savings SolutionsLower-income market (NSSS)Middle-income MarketAffluent Market

Institutional Savings Solutions

Conclusion

1. Client Centricity

Strategy: Client Centricity

Client centricity:-Know who our clients are,Understand their needs,Design solutions to meet their needs (confirm appropriateness of particular solution set)Continue to satisfy expectations (through operational efficiencies and continuous advice)

Strategically, we do not intend to grow market share predominantly through product superiority, but mainly through client centricity

However, if we focus on the client, innovation in respect of superior products/solutions will surely follow

Understanding and adapting to the clientUnderstanding and adapting to the client’’s needs,s needs, through a broader through a broader distribution network, supported by a wider array of service/proddistribution network, supported by a wider array of service/product uct

offerings and capable talent, and offerings and capable talent, and ‘‘statestate--ofof--thethe--artart’’ technology systemstechnology systems

Understanding and adapting to the clientUnderstanding and adapting to the client’’s needs,s needs, through a broader through a broader distribution network,distribution network, supported by a wider array of service/product supported by a wider array of service/product

offerings and capable talent, and offerings and capable talent, and ‘‘statestate--ofof--thethe--artart’’ technology systemstechnology systems

Understanding and adapting to the clientUnderstanding and adapting to the client’’s needs, through a broader s needs, through a broader distribution network,distribution network, supported by a wider array of service/product supported by a wider array of service/product

offerings and capable talent,offerings and capable talent, and and ‘‘statestate--ofof--thethe--artart’’ technology systemstechnology systems

Understanding and adapting to the clientUnderstanding and adapting to the client’’s needs, through a broader s needs, through a broader distribution network, supported by a wider array of service/proddistribution network, supported by a wider array of service/product uct

offerings and capable talent,offerings and capable talent, and and ‘‘statestate--ofof--thethe--artart’’ technology systemstechnology systems

Wealth Management

Life-style

PersonalCover

FinancialEducation

Sanlam Personal FinanceElsewhere in Sanlam Group

Edu-cation provi-sion

Savings & Invest-

ment

Home loan

Car & house-hold cover

Banking / Trans-

actionalMedium

term credit

Finan-cial

Educa-tion

Wills & trusts

Medical

Risk cover

Retirement

ClientClient

Competitive advantage:Interact with clientsUnderstand their needsProvide adviceDesign solutionsFeedback - Maintain relationship

Comprehensive offering:

Client focus also provides various cross-sell opportunitiesThereby enhancing overall value proposition for client

Cross-sell Potential at SPF: Clients with a Single Provider and % Untapped

56%51%

44%

36%41%

30%

77%

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

SPF (Life only) SCI Santam Wills Glacier SPL Home Loans

mil

lion

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

no. of clients with a single provider - lhs As a % of provider's base (ie untapped potential) - rhs

SPF’s life clients have the largest untapped potential of 1.4m clients

Despite Significant Future Potential, our Progress to Date

Accelerated success towards providing a wide range of client-centric solutions

Group net operating profit (Rm)

Otherfinancialservices

0

200

400

600

800

1 000

1 200

1 400

1 600

1H03 1H04 1H05 1H06 1H07

SPF SDM SEB SIM SCM SNT IFS

Life

CAGR: 19%pa

2. Savings Environment

South Africa, a Country of Rapid Change

Increased freedom ↔ increased personal responsibility:

Catalyst behind changing realities in South AfricaSocio-economic realities

Transparency / Access to informationConsumerism / Protection of the individual → Increased regulationEmpowerment

Economic realitiesLow inflation environmentIncreased market volatilityShorter time horizons → Flexibility and mobility

Other influencesProliferation of technologyExpectations created by other industriesExpectations from Government (FAIS, FICA, SOI, NSSS)

Current Savings Environment in SA

Overall a strong improvement in household wealth, driven by:Strong growth in disposable income (CAGR of 11% over past 3 yrs)Increasing tax reliefLower inflationary environmentStrong GDP growthHigher stock market levelsEscalating house prices

However, not reflected in the official macro statistics (-0.5% savings rate of personal disposable income - PDI) due to aggregation impacts (ie unemployed and lower wage earners)

Despite a sharp rate of growth in household consumption expenditure, a recent survey commissioned by Credit Suisse Standard Securities (TNS Survey — March 2007) paints a very different picture…

Current Savings Environment in SA — Higher Savings Rate

After stripping out aggregation impacts, survey showed a higher propensity to save amongst households (savings from 4%-10% of PDI)

Suggests higher income households are not consuming out of savings

Savings as a % of Disposable Income (by household income groupinSavings as a % of Disposable Income (by household income grouping)g)

0%

2%

4%

6%

8%

10%

12%

7000-7999 8000-8999 9000-10999

11000-13999

14000-19999

20000-24999

25000-41999

>42000

Source : CSSS

Current Savings Environment in SA — Savings Diversified

63% of households use more than one savings productLower income groups typically use a large number of funeral plansHigher income households use a larger array of savings products

Savings products usedSavings products used

0%

20%

40%

60%

80%

100%

7000-7999

8000-8999

9000-10999

11000-13999

14000-19999

20000-24999

25000-41999

>42000

other

shares on the stock exchange

Money marke t account o r 30/60 daynot ice accountsInvestment in o ther your own orsomeone e lse 's businessUnit t rusts

Stokve ls o r o ther savings c lubs o rburia l soc ie t iesEducat ion po licy/s

Endowment po licy/s

Pension or provident fund/s o rre t irement annuity/sFunera l po l icy/s

Source : CSSS

Current Savings Environment in SA — Black Diamonds

Number of people in the middle market will grow by approximately37% from 2006 to 2011

Blacks and Indians have a growth rate of more than 50% (Coloureds —72%), whereas the White population has a mere 19% growth rate

0

200

400

600

800

1 000

1 200

1 400

1 600

1 800

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

'00

0

B lack Co loured Indian WhiteSource : AMPS 2006

Growth in race groups Growth in race groups —— Middle income marketMiddle income market

3. Retail Businesses — Savings Solutions

3. Retail Savings Solutions - Summary

Low incomeCurrently low savings penetration, limited mainly to risk solutionsRoll-out of NSSS should fill the gap (limited private sector opportunities)RoA, India and other emerging markets provide the biggest savings-related opportunities in the lower-income market

Middle incomeHigher level of savings penetrationOpportunities in respect of new distribution models

Affluent marketNew commission dispensation will change structure of marketRelaxation (or abolishment) of foreign exchange controlsCapturing share of ‘Baby Boomers’ marketAddressing trend of backward integration by IFAs

Lower Income Market

Regulatory Environment in SA

National Social Security Scheme (NSSS):Supportive of government’s initiative for a collective scheme with its resultant cost advantages and compulsory participation

We expect a (at least a partially) funded scheme:Funded schemes give people a greater sense of control over theirown financial positions (rather than feeling that they are cross-subsidizing)The amount of assets available for investment will be substantial —difficult to manage without splitting up assets / partnering with the private sector

We see the NSSS as meeting only a very specific need for our clients:Still exists a wide array of ‘other’ financial services which we can offer this market (e.g. there will still be a need for shorter-term savings)A focus on direct marketing channels, also provides a lower-cost avenue to tap into this market

Overview — Rest of Africa

OverviewSanlam operates in African countries with under-developed investment marketsLife insurance products give clients access to participate in these investment marketsLeverage off our existing expertise to expand into otherwise unavailable products (e.g. annuities)

DriversHuge drive in Africa for education - since educated people can take better advantage of developing economiesDemand for savings products is primarily driven by educational savings, which we see as a huge growth area

Growth Potential — Presence in Rest of Africa

Why we should be in rest of Africa?Low industry penetration + competitionStrong economic growthHigher margins availableDoes not consume excessive management time

5 00036 million2005Tanzania

24 00010 million2002Zambia

45 00020 million2000Ghana

85 00032 million2000Kenya

200 0001.7 million1995Botswana

810 00045 million1930South Africa (ELM)

PoliciesPopulationCommencedKey

Rest of Africa — Key Risks & Challenges

Restore image of industry — legacy of state insurance companies

Skill shortages — management, technical, operational

Premium collection capabilities — many countries cash driven

Evolution of legislation — revision of Insurance Acts

Increase in competition — more appetite for Africa

But opportunity to help shape the industries…

Rest of Africa — Key Focus Areas

Maintain dominant market position in Botswana, but:More focus on bancassurance / group businessBenefits from annuity matchingUtilization of excess capital

Focus on operational efficienciesDistribution capabilitiesQuality of business (lapses, NTU’s)Cost efficiencies

Partnerships with other credit providers

Improved support out of South Africa

Further expansion into Africa — Nigeria?

Growth Potential — India

The country is looking at an annual GDP growth of 9.2%

Insurance penetration of 3,1% following entry of foreign players

High expected growth in personal income and aspirations

Need for strong financial planning

Markets in most developed countries have saturated

This makes the Indian market more attractive for global insurance majors

Huge opportunity to tap semi-urban and rural markets

There exists a strong urban and rural divide with regard to savings

Over 1 Billion Indians – Strong economic growth

Majority of the population does not have adequate financial protection

Example : The advantage of India — Insurance linkages

Shriram — New Business Premium YTD growth (Sorted by APE Growth)

30%26%Tata AIG22/%24%Aviva

24%32%ING Vysya42%42%ICICI Prudential48%56%Kotak Mahindra Old Mutual71%60%SBI Life55%60%Birla Sunlife91%63%Max New York61%78%HDFC Standard

117%106%Met Life48%106%Bajaj Allianz

120%140%Reliance Life342%187%Shriram Life253%610%Sahara Life1391%1356%Bharti Axa Life55%64%Total Private9%41%LIC19%48%Grand Total

Unweighted GrowthYTD F2008

APE GrowthYTD

Life Insurer

Source : IRDA, JP Morgan* unweighted as data for single premiums were not available prior to Feb06

Middle Income Market

Some of our Challenges

Need for better communication between parties involved in solution:ClientIntermediaryProvider

Providers differentiate through “product innovation” (difficult to answer to a call for simplification)

Difficult to introduce technology into the entire process

Advice increasingly provided only to the wealthy

International experience — UKDesertion of the middle marketInterventions so far failed — protection gap

Existing Distribution Space

Experimental / NewOpportunities

% o

f bus

ines

s →

Exis

ting

mod

el%

of business →N

SSS

Lower Income Middle Income Higher Income

Existing distribution models

NSSS

Shift towards Higher Average Recurring Premiums

Unit costs of sale too high: FAIS, FICA and new commission dispensation likely to push advisors up-market

Since 2005, average recurring premium file-sizes grew by 14%pa in SFA and 18%pa in broker channel (vs. inflation of 4.8%)

Cumulative growth in gross average recurring premiun size vs inflation (indexed)

90100110120130140150160170180190200

2000 2001 2002 2003 2004 2005 2006 2007

Ave CPIX SFA (incl wealth) Broker

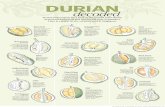

Our Opportunity in the Future Distribution Space

Experimental / NewOpportunities

% o

f bus

ines

s →

Exis

ting

mod

el%

of business →N

SSS

Lower Income Middle Income Higher Income

NSSS

Outlook for Existing distribution

models

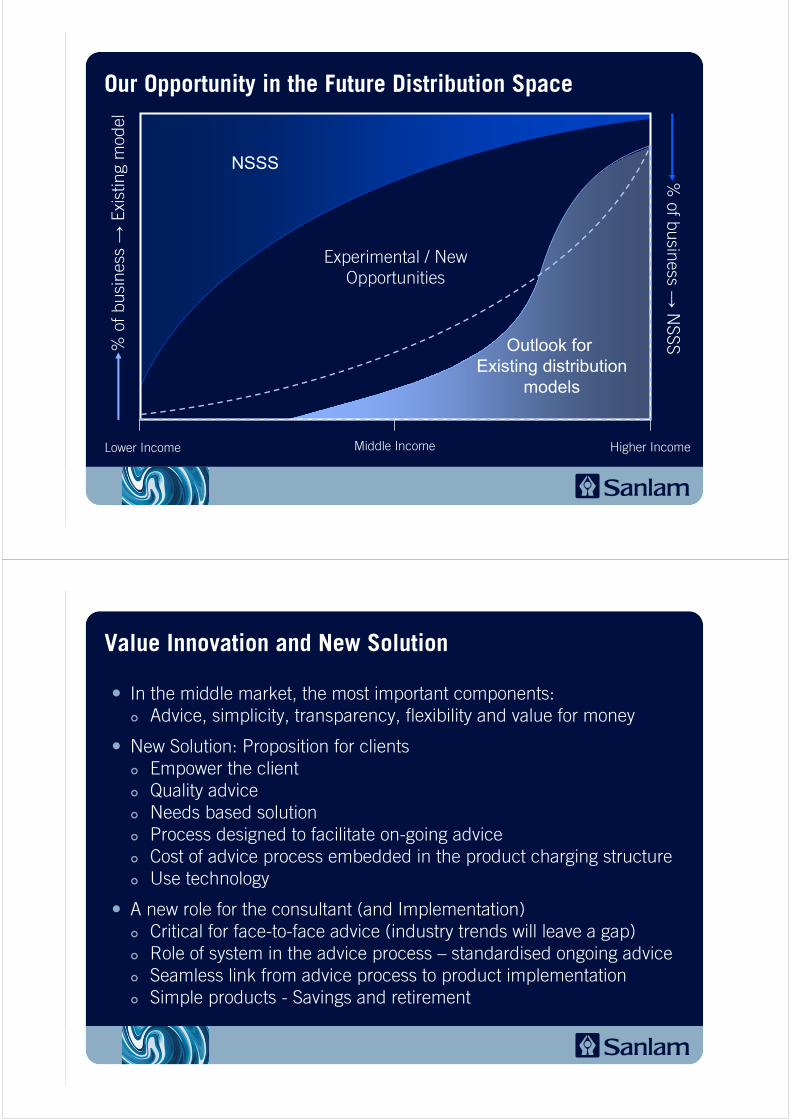

Value Innovation and New Solution

In the middle market, the most important components:Advice, simplicity, transparency, flexibility and value for money

New Solution: Proposition for clientsEmpower the clientQuality adviceNeeds based solutionProcess designed to facilitate on-going adviceCost of advice process embedded in the product charging structureUse technology

A new role for the consultant (and Implementation)Critical for face-to-face advice (industry trends will leave a gap)Role of system in the advice process — standardised ongoing adviceSeamless link from advice process to product implementationSimple products - Savings and retirement

Benefits to Sanlam

Consistent with brand proposition

New growth opportunities (target new clients and grow market share)

Tight control over legal liabilities arising from the provision of advice

In line with thought process of National Treasury

Pro-active initiative against potential fall-out of traditional business model

Improved client retention

Reduced acquisition cost — improved margins and value for moneyImproved productivity (FC)Reduced new business support per financial plan (automated)Reduced management requirements

A streamlined, high-volume process

Affluent Market

Funds under management

Building on a very successful LISP Business

79

12

16

23

30

35

0

5

10

15

20

25

30

35

40

2001 2002 2003 2004 2005 2006 2007

R b

'n

0

50

100

150

200

250

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

'000

65+ yrs 50 - 64 yrs 35 - 49 yrs 25 - 34 yrs 16 - 24 yrs

Growth in age groups — Affluent Market

Future growth profile of Affluent Market

Population size of affluent market will grow by 59% from 2006 to 2011

The 16-24 age group will show the highest growth rate over the period of 63%, but growth from all the age groups will >50%

By 2011, age group 35-49 will make up half of the Affluent market

All race groups will grow by between 53% (Whites) and 86% (Coloureds)

Source : AMPS 2006

Changing Market Conditions

Commoditisation of LISP business

Arrival of new competitors (Coronation, Allan Gray and Discovery)

Increased competition from existing players

LISPs increasingly competing on price

Relaxation (abolishment) of foreign exchange controls provides opportunities for offshore long-only asset management opportunities

Backward integration from advisors:Likely to put further pressure on marginsLose independence from the client’s perspectiveIFA’s will increasingly compete directly against private banksHowever, appears to be a bull-market trend

ProductProductPackagesPackages

IFAIFA

Asset Asset ManagerManager

Bac

kwar

dB

ackw

ard

Inte

grat

ion

Inte

grat

ion

C L I E N T S

50 — 75 bps 50 bps

85 bps65 — 150 bps

75 — 100 bps 100 bps

Current Future

Affluent Market — Strategic Outlook

Offering a wider set of financial solutions to affluent clients, as well as assisting intermediaries to diversify their practices across a wider solution set

Diversify income streams away from pure administrative profits

Partnering with key intermediaries in the market

New commission proposals and early termination proposals likely to push more IFAs up-market

Establishing a relationship with clients earlier in their life

Scale advantages are still important in this business

Potential for IFA aggregation opportunities both locally and abroad

Sustainable superior investment returns is key to playing across the value chain

4. Institutional Businesses — Savings Solutions

Sanlam Adapting to Changing Consumer Demands

1310 11 11 14

7

18

27

43

51

66

38

1.41

2.72

3.81

4.554.74

5.26

0

10

20

30

40

50

60

70

80

90

100

2002 2003 2004 2005 2006 1H07

Rb

n

-0.5

0.5

1.5

2.5

3.5

4.5

5.5

tim

es

Life Non-life Ratio of non-life to life

Grow alternative revenue sources: Sanlam Group New business flowsCAGR 2002-2007 (+24%)

Following off-balance sheet trend & Countering Disintermediation

Making sure that Sanlam has the capabilities in place to capture the shift in savings off-balance sheetDiversification strategy: In part, a response to an increasing trend of disintermediation in the savings industry

New product providers and platforms “eating” into the existing value chain

ClientProduct

platformsDistribution

Network

Traditional LT savings firms

Asset managers

Unit Trusts, LISPs, Multi-

managers

“If you can’t beat them – then join them” (or own them)!

Profile of Sanlam Investments — Available Capacity

Sanlam Sanlam Investment Investment

ManagementManagement

OctaneOctaneHoldingsHoldingsLimitedLimited

Sanlam Sanlam Collective Collective

InvestmentsInvestments

SanlamSanlamPrivatePrivateEquityEquity

Sanlam Asset Sanlam Asset Management Management

(Ireland)(Ireland)

Sanlam MultiSanlam Multi--Managers Managers

InternationalInternational

Sanlam Sanlam PropertiesProperties

Sanlam Sanlam InvestmentsInvestments

SanlamSanlamPrivate Private

InvestmentsInvestments

SIM Emerging SIM Emerging Markets Markets

SanlamSanlamCapitalCapitalMarketsMarkets

SIM GlobalSIM Global Hedgehog Hedgehog CapitalCapital

Sanlam Sanlam Structured Structured SolutionsSolutions

SimekaSimeka

Sanlam Sanlam Employee Employee BenefitsBenefits

Increased Diversity (leads to Increased Focus)

209227

286

327

406430

150

200

250

300

350

400

450

500

2002 2003 2004 2005 2006 Jun-07

SIM - AUM (Rbn)CAGR 2002-2007 (+16%)

SCI - AUM (Rbn)55

22 2631

41

53

0

15

30

45

60

2002 2003 2004 2005 2006 Jun-07

Retail InstitutionalWhite Label

CAGR 2002-2007 (+20%)

Multi-Manager - AUM (Rbn)

25 2338

59

97

0

20

40

60

80

100

120

2002 2003 2004 2005 2006

Consulting SADiscretionary GlobalDiscretionary SA

CAGR 2002-2006 (+40%)

0

200

400

600

800

1,000

1,200

2002 2003 2004 2005 2006 Jun-07

InternationalSA

CAGR 2002-2007 (+36%)

Profit before tax (Rm)

243 270419

699

1 077

560

Conclusion

The current savings market in South Africa is healthier than expected, and is continuing to grow

There is also sizeable growth potential in the savings market in the rest of Africa as well as other emerging markets

We see the need for alternative distribution models in the middle-income market which offers a needs based solution, with (or without) on-going advice. Cost of advice could be embedded in the product charging structure

We see a strong underpin to growth in savings in the form of the black emerging market (black diamond), as well as the unwind of the ‘Baby Boomers’ phenomenon

Increased regulation will continue to shift the IFAs up-market

Given the current success in diversification of the group, Sanlam is well placed to capture these savings trends

Thank You