The Right to Survive Survive - Oxfam International | Working

Upload

alicia-craigCategory

view

215download

0

SAVING : INVESTING : PLANNING

EXPERTISEHow to Prepare For and Survive a 403(b) Plan Audit

Joseph S. Kendy IIISenior Counsel

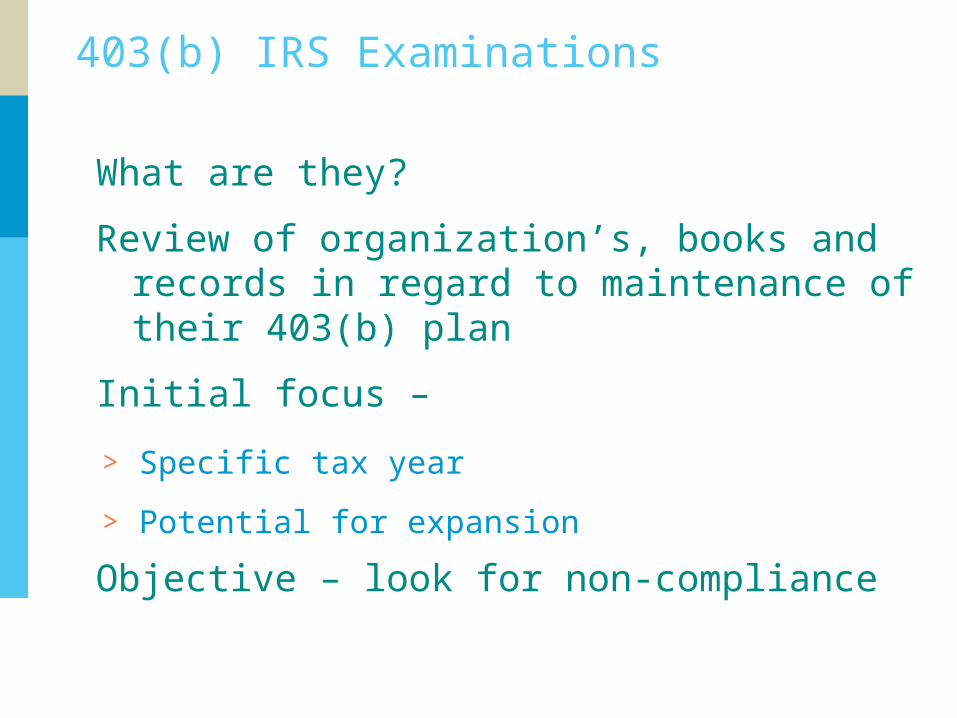

403(b) IRS Examinations

What are they?

Review of organization’s, books and records in regard to maintenance of their 403(b) plan

Initial focus –

> Specific tax year

> Potential for expansion

Objective – look for non-compliance

What is the basis of the exam?

It could be any Code Section 403(b) compliance matter:

> Timely plan adoption

> Form compliance

> Operating in accordance with plan terms

> Universal Availability

> Plan terminations

> Form 5500 and internal audit – not applicable to public schools

Who is examined? & How are they selected?

Education

> Public & Private

> K-12 & Higher Education

Healthcare

> Public & Private−Tax-exempt only (501(c)(3))

Other 501(c)(3)s

Selection process

> National Plan

> Local Selection

What is the process?Step 1: They’re coming!

> Phone call or letter

Step 2: They’re here!

> The importance of the initial meeting− Assemble the right team− HR / Payroll / Counsel− Have them in the room

Step 3: Information Document Requests (IDRs)

> Identifies:− What documents− What timeline− Negotiating Scope & Requests

> Count on additional IDRs

Gathering IDR Documents & Records

Employer’s Records

Investment Provider Records

Other service providers records

>Compliance service provider,

>TPA, etc.

Negotiate scope and delivery

How is the exam resolved?

Examiner’s initial findings

Plan sponsor team review of initial findings

Discussion, modification, & negotiation

Final findings

Closing Agreement (Audit CAP)

Generally involves correction & sanction

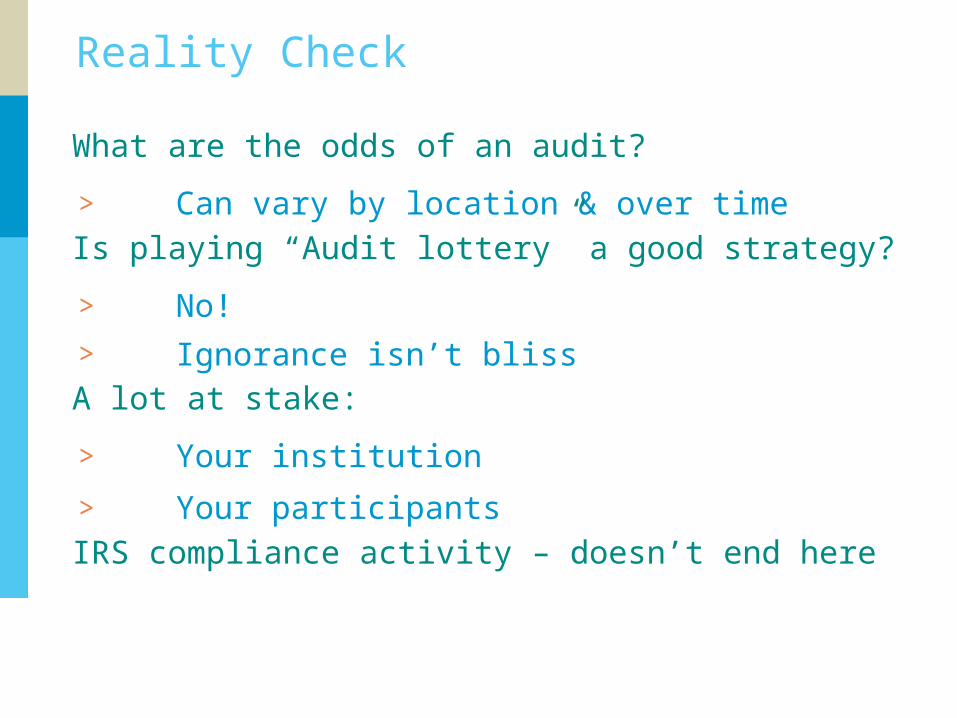

Reality Check

What are the odds of an audit?

> Can vary by location & over time

Is playing “Audit lottery” a good strategy?

> No!

> Ignorance isn’t blissA lot at stake:

> Your institution

> Your participants

IRS compliance activity – doesn’t end here

Compliance through correspondence (The non-exam)

Employee Plans Correspondence Unit (EPCU)

> An Employee Plans activity

> Not to be confused with Exempt Organizations

Extends the reach of limited IRS Resources

> Beware the innocent inquiry from the IRS

The EPCU Process

> Targeted initiatives

> Initial questionnaire and follow-up

EPCU 403(b) Initiatives

K-12 Universal Availability

> Phase I - completed 2009

> Over 5,500 letters sent out: −11 exams −1,000 identified for potential issues.

Other 403(b) initiatives possible

Main Issues for IRS Activity

Universal Availability

>Potentially significant tax consequences to plan & participants

Contribution Dollar Limitations

>Records are data driven

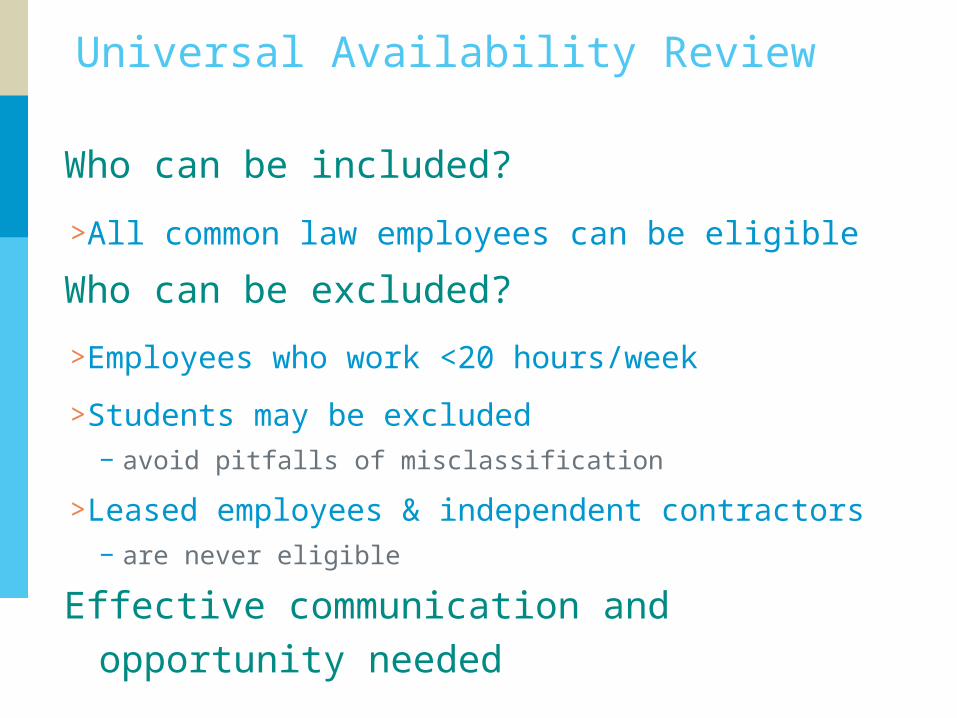

Universal Availability Review

Who can be included?

>All common law employees can be eligible

Who can be excluded?

>Employees who work <20 hours/week

>Students may be excluded−avoid pitfalls of misclassification

>Leased employees & independent contractors−are never eligible

Effective communication and opportunity needed

Review of 403(b) 2013 and 2014 Contribution Dollar Limits

Overall DC limit: $52,000 for 2014, $51,000 for 2013

Includes elective deferrals (unchanged for 2014)

> Basic: $17,500

> Long term Employer Catch-up, up to: $3,000

> Age 50 catch-up: $5,500

2013 Updates

403(b) prototype program

>Currently found in Revenue Procedure 2013-22

Update to Employee Plans Compliance Resolution System (EPCRS)

>Currently found in Revenue Procedure 2013-12

>Voluntary Correction Program

>Self Correction

Resources

Published IRS guidance

> Regulations

> Notices

> Revenue Procedures

> Revenue Rulings

Individual rulings and determinations

> Relied on only by recipient

IRS website (www.irs.gov)

DOL website (for ERISA plans) www.dol.gov

Legal Counsel, Investment Providers, Other Service Providers

QUESTIONS ?

SAVING : INVESTING : PLANNING

THANK YOU

Securities and investment advisory services are offered by VALIC Financial Advisors, Inc., member FINRA and an SEC-registered investment advisor.

The information in this presentation is general in nature and may be subject to change. Neither VALIC nor its financial advisors or other representatives give legal or tax advice. Applicable laws and regulations are complex and subject to change. Any tax statements in this material are not intended to suggest the avoidance of U.S. federal, state or local tax penalties. For legal or tax advice concerning your situation, consult your attorney or professional tax advisor.

VALIC represents The Variable Annuity Life Insurance Company and its subsidiaries, VALIC Financial Advisors, Inc. and VALIC Retirement Services Company.

Copyright © The Variable Annuity Life Insurance Company. All rights reserved.VALIC.comTemplate (04/2009) J73125 EE

For Plan Sponsor Use Only