SANTA CLARA COUNTY OFFICE OF EDUCATION AUDIT REPORT …

87

SANTA CLARA COUNTY OFFICE OF EDUCATION AUDIT REPORT For the Fiscal Year Ended June 30, 2013

Transcript of SANTA CLARA COUNTY OFFICE OF EDUCATION AUDIT REPORT …

SANTACLARACOUNTYOFFICEOFEDUCATION

AUDITREPORT

FortheFiscalYearEndedJune30,2013

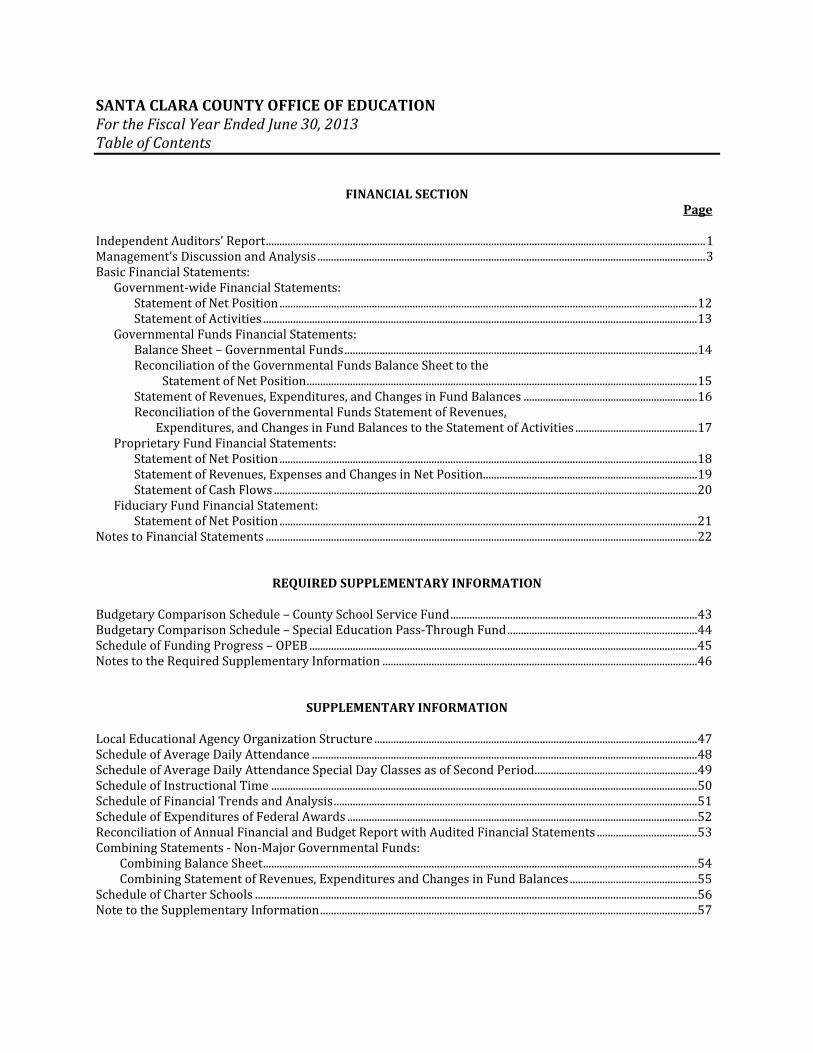

SANTACLARACOUNTYOFFICEOFEDUCATIONFortheFiscalYearEndedJune30,2013TableofContents

FINANCIALSECTION Page

IndependentAuditors’Report..................................................................................................................................................................1Management’sDiscussionandAnalysis...............................................................................................................................................3BasicFinancialStatements:

Government‐wideFinancialStatements:StatementofNetPosition..........................................................................................................................................................12StatementofActivities................................................................................................................................................................13

GovernmentalFundsFinancialStatements:BalanceSheet–GovernmentalFunds..................................................................................................................................14ReconciliationoftheGovernmentalFundsBalanceSheettothe StatementofNetPosition................................................................................................................................................15StatementofRevenues,Expenditures,andChangesinFundBalances................................................................16ReconciliationoftheGovernmentalFundsStatementofRevenues,

Expenditures,andChangesinFundBalancestotheStatementofActivities.............................................17ProprietaryFundFinancialStatements:

StatementofNetPosition..........................................................................................................................................................18StatementofRevenues,ExpensesandChangesinNetPosition...............................................................................19StatementofCashFlows............................................................................................................................................................20

FiduciaryFundFinancialStatement:StatementofNetPosition..........................................................................................................................................................21

NotestoFinancialStatements...............................................................................................................................................................22

REQUIREDSUPPLEMENTARYINFORMATIONBudgetaryComparisonSchedule–CountySchoolServiceFund...........................................................................................43BudgetaryComparisonSchedule–SpecialEducationPass‐ThroughFund......................................................................44ScheduleofFundingProgress–OPEB...............................................................................................................................................45NotestotheRequiredSupplementaryInformation....................................................................................................................46

SUPPLEMENTARYINFORMATIONLocalEducationalAgencyOrganizationStructure.......................................................................................................................47ScheduleofAverageDailyAttendance..............................................................................................................................................48ScheduleofAverageDailyAttendanceSpecialDayClassesasofSecondPeriod............................................................49ScheduleofInstructionalTime.............................................................................................................................................................50ScheduleofFinancialTrendsandAnalysis......................................................................................................................................51ScheduleofExpendituresofFederalAwards.................................................................................................................................52ReconciliationofAnnualFinancialandBudgetReportwithAuditedFinancialStatements.....................................53CombiningStatements‐Non‐MajorGovernmentalFunds:

CombiningBalanceSheet................................................................................................................................................................54CombiningStatementofRevenues,ExpendituresandChangesinFundBalances...............................................55

ScheduleofCharterSchools...................................................................................................................................................................56NotetotheSupplementaryInformation...........................................................................................................................................57

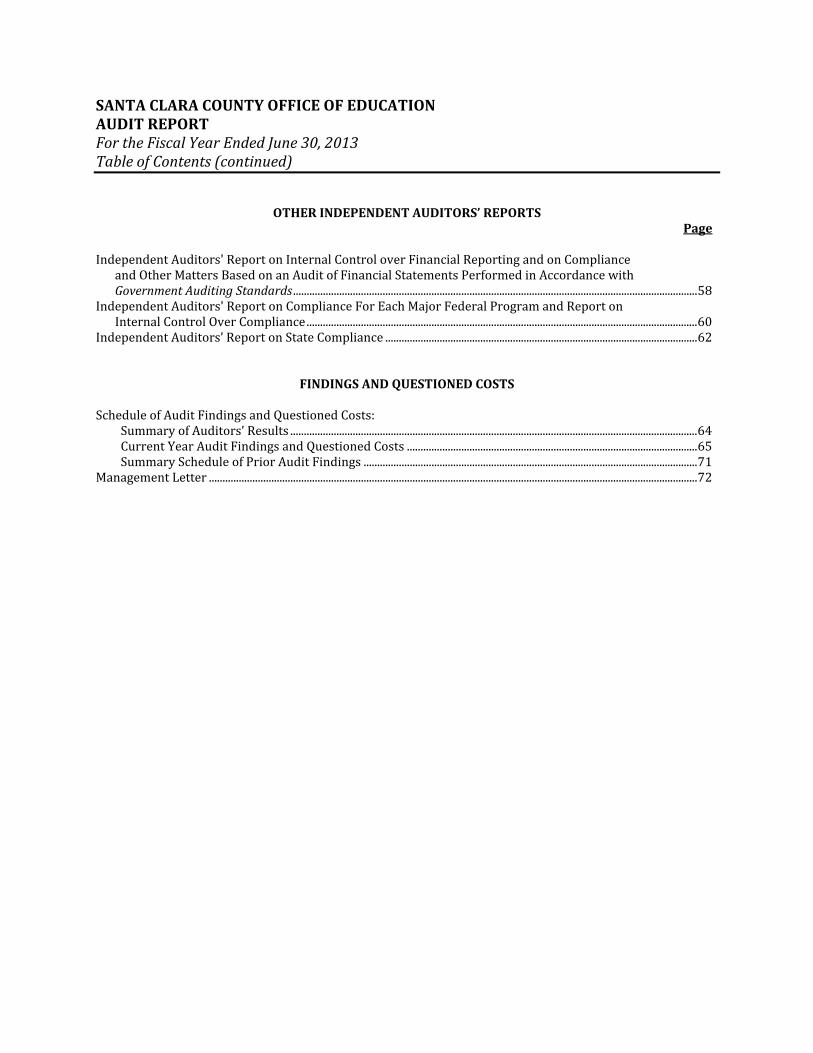

SANTACLARACOUNTYOFFICEOFEDUCATIONAUDITREPORTFortheFiscalYearEndedJune30,2013TableofContents(continued)

OTHERINDEPENDENTAUDITORS’REPORTS Page

IndependentAuditors'ReportonInternalControloverFinancialReportingandonCompliance andOtherMattersBasedonanAuditofFinancialStatementsPerformedinAccordancewith GovernmentAuditingStandards.....................................................................................................................................................58IndependentAuditors'ReportonComplianceForEachMajorFederalProgramandReporton InternalControlOverCompliance................................................................................................................................................60IndependentAuditors’ReportonStateCompliance...................................................................................................................62

FINDINGSANDQUESTIONEDCOSTSScheduleofAuditFindingsandQuestionedCosts: SummaryofAuditors’Results......................................................................................................................................................64 CurrentYearAuditFindingsandQuestionedCosts...........................................................................................................65 SummaryScheduleofPriorAuditFindings...........................................................................................................................71ManagementLetter....................................................................................................................................................................................72

FinancialSection

(Thispageintentionallyleftblank)

1

INDEPENDENTAUDITORS’REPORTBoardofEducationSantaClaraCountyOfficeofEducationSanJose,CaliforniaWehaveauditedtheaccompanyingfinancialstatementsofthegovernmentalactivities,eachmajorfund,andtheaggregateremaining fund informationofSantaClaraCountyOfficeofEducation,asofandfor the fiscalyearendedJune30,2013,andtherelatednotestothefinancialstatements,whichcollectivelycomprisetheCounty'sbasicfinancialstatementsaslistedinthetableofcontents.Management’sResponsibilityfortheFinancialStatementsManagement is responsible for the preparation and fair presentation of these financial statements inaccordancewithaccountingprinciplesgenerallyaccepted in theUnitedStatesofAmerica; this includes thedesign,implementation,andmaintenanceofinternalcontrolrelevanttothepreparationandfairpresentationoffinancialstatementsthatarefreefrommaterialmisstatement,whetherduetofraudorerror.Auditors'ResponsibilityOurresponsibilityistoexpressopinionsonthesefinancialstatementsbasedonouraudit.WeconductedourauditinaccordancewithauditingstandardsgenerallyacceptedintheUnitedStatesofAmerica,thestandardsapplicabletofinancialauditscontainedinGovernmentAuditingStandards,issuedbytheComptrollerGeneralof theUnited States, andStandardsandProcedures forAuditsofCaliforniaK‐12LocalEducationalAgencies2012‐13. Thosestandardsrequirethatweplanandperformtheaudittoobtainreasonableassuranceaboutwhetherthefinancialstatementsarefreefrommaterialmisstatement.Anauditinvolvesperformingprocedurestoobtainauditevidenceabouttheamountsanddisclosuresinthefinancialstatements.Theproceduresselecteddependontheauditor’sjudgment,includingtheassessmentoftherisksofmaterialmisstatementofthefinancialstatements,whetherduetofraudorerror.Inmakingthoserisk assessments, the auditor considers internal control relevant to the entity’s preparation and fairpresentation of the financial statements in order to design audit procedures that are appropriate in thecircumstances,butnot for thepurposeofexpressinganopinionontheeffectivenessoftheentity’s internalcontrol. Accordingly,we express no suchopinion.An audit also includes evaluating the appropriatenessofaccountingpoliciesusedandthereasonablenessofsignificantaccountingestimatesmadebymanagement,aswellasevaluatingtheoverallpresentationofthefinancialstatements.Webelievethattheauditevidencewehaveobtainedissufficientandappropriatetoprovideabasisforourauditopinions.OpinionsInouropinion,thefinancialstatementsreferredtoabovepresentfairly,inallmaterialrespects,therespectivefinancial position of the governmental activities, each major fund, and the aggregate remaining fundinformation of Santa Clara County Office of Education, as of June 30, 2013, and the respective changes infinancialpositionand,whereapplicable,cashflowsthereofforthefiscalyearthenendedinaccordancewithaccountingprinciplesgenerallyacceptedintheUnitedStatesofAmerica.

2

OtherMattersRequiredSupplementaryInformationAccounting principles generally accepted in the United States of America require that the management’sdiscussionandanalysisonpages3through11,budgetarycomparisoninformationonpages43and44,andschedule of fundingprogress onpage45bepresented to supplement thebasic financial statements. Suchinformation,althoughnotapartofthebasicfinancialstatements,isrequiredbytheGovernmentalAccountingStandardsBoard,whoconsidersittobeanessentialpartoffinancialreportingforplacingthebasicfinancialstatements in anappropriateoperational, economic, orhistorical context. Wehaveapplied certain limitedprocedures to the required supplementary information in accordance with auditing standards generallyacceptedintheUnitedStatesofAmerica,whichconsistedofinquiriesofmanagementaboutthemethodsofpreparing the informationandcomparing the information forconsistencywithmanagement’s responses toourinquiries,thebasicfinancialstatements,andotherknowledgeweobtainedduringourauditofthebasicfinancialstatements.Wedonotexpressanopinionorprovideanyassuranceontheinformationbecausethelimitedproceduresdonotprovideuswithsufficientevidencetoexpressanopinionorprovideanyassurance.OtherInformationOur auditwas conducted for the purpose of forming opinions on the financial statements that collectivelycomprise Santa Clara County Office of Education’s basic financial statements. The other supplementaryinformation listed in the table of contents is presented for purposes of additional analysis and is not arequiredpartofthebasicfinancialstatements.Theothersupplementaryinformationlistedinthetableofcontents,includingtheScheduleofExpendituresofFederal Awards, is the responsibility of management and was derived from and relates directly to theunderlyingaccountingandotherrecordsusedtopreparethebasicfinancialstatements.Suchinformationhasbeensubjected to theauditingproceduresapplied intheauditof thebasic financialstatementsandcertainadditional procedures, including comparing and reconciling such information directly to the underlyingaccounting and other records used to prepare the basic financial statements or to the basic financialstatements themselves, and other additional procedures in accordance with auditing standards generallyacceptedintheUnitedStatesofAmerica.Inouropinion,theothersupplementaryinformationisfairlystated,inallmaterialrespects,inrelationtothebasicfinancialstatementsasawhole.OtherReportingRequiredbyGovernmentAuditingStandardsInaccordancewithGovernmentAuditingStandards,wehavealsoissuedourreportdatedDecember13,2013on our consideration of the County's internal control over financial reporting and on our tests of itscompliancewithcertainprovisionsof laws,regulations,contracts,andgrantagreementsandothermatters.Thepurposeofthatreportistodescribethescopeofourtestingofinternalcontroloverfinancialreportingandcomplianceandtheresultsofthattesting,andnottoprovideanopiniononinternalcontroloverfinancialreporting or on compliance. That report is an integral part of an audit performed in accordance withGovernment Auditing Standards in considering the County's internal control over financial reporting andcompliance.

December13,2013

3

FigureA‐1.OrganizationofSantaClaraCountyOfficeofEducation’sAnnualFinancialReport

SANTACLARACOUNTYOFFICEOFEDUCATIONManagement’sDiscussionandAnalysis(Unaudited)FortheFiscalYearEndedJune30,2013This discussion and analysis of SantaClaraCountyOffice ofEducation’s financial performanceprovides anoverview of the County’s financial activities for the fiscal year ended June 30, 2013. Please read it inconjunctionwiththeCounty’sfinancialstatements,whichimmediatelyfollowthissection.FINANCIALHIGHLIGHTS The County’s financial status increased overall as a result of this year’s operations. Net position of

governmentalactivitiesincreasedby$13.9million,or12.4%. Governmentalexpenseswereabout$244.2million.Revenueswereabout$258.1million. TheCountyspentover$3.8millioninnewcapitalassetsduringtheyear. The County increased its outstanding long‐term debt by $0.4 million. This was primarily due to an

increaseintheotherpostemploymentbenefitsliability. Averagedailyattendance(ADA)decreasedby64,or3.2%.OVERVIEWOFTHEFINANCIALSTATEMENTSThis annual report consists of three parts – management discussion and analysis (this section), the basicfinancial statements, and required supplementary information. The basic financial statements include twokindsofstatementsthatpresentdifferentviewsoftheCounty: Thefirsttwostatementsarecounty‐widefinancialstatementsthatprovidebothshort‐termandlong‐term

informationabouttheCounty’soverallfinancialstatus. The remaining statements are fund financial statements that focus on individual parts of the County,

reportingtheCounty’soperationsinmoredetailthantheCounty‐widestatements. Thegovernmental fundsstatementstellhowbasicservices likeregularandspecialeducationwere

financedintheshorttermaswellaswhatremainsforfuturespending. Short and long‐term financial information about the activities of the County that operate like

businesses(self‐insurancefunds)areprovidedintheproprietaryfundsstatements. Fiduciary funds statement provides information about the financial relationships in which the

Countyactssolelyasatrusteeoragentforthebenefitofotherstowhomtheresourcesbelong.Thefinancialstatementsalsoinclude notes that explainsome of the information inthe statements and providemore detailed data. FigureA‐1 shows how the variousparts of this annual reportare arranged and related tooneanother.

Management’sDiscussionandAnalysis

BasicFinancial

Information

RequiredSupplementaryInformation

FundFinancialStatements

County‐WideFinancialStatements

NotestoFinancialStatements

SUMMARY DETAIL

4

SANTACLARACOUNTYOFFICEOFEDUCATIONManagement’sDiscussionandAnalysis(Unaudited)FortheFiscalYearEndedJune30,2013

OVERVIEWOFTHEFINANCIALSTATEMENTS(continued)FigureA‐2summarizesthemajorfeaturesoftheCounty’sfinancialstatements,includingtheportionoftheCounty’sactivitiestheycoverandthetypesofinformationtheycontain.FigureA‐2.MajorFeaturesoftheCounty‐WideandFundFinancialStatements

TypeofStatements

County‐Wide

GovernmentalFunds

ProprietaryFunds

FiduciaryFunds

Scope Entirecounty,exceptfiduciaryactivities

TheactivitiesoftheCountythatarenotproprietaryorfiduciary,suchasspecialeducationandbuildingmaintenance

ActivitiesoftheCountythatoperatelikeabusiness,suchasself‐insurancefunds

InstancesinwhichtheCountyadministersresourcesonbehalfofsomeoneelse,suchasscholarshipprogramsandstudentactivitiesmonies

Requiredfinancialstatements

StatementofNetPosition

StatementofActivities

BalanceSheet

StatementofRevenues,Expenditures&ChangesinFundBalances

StatementofNetPosition

StatementofRevenues,Expenses,&ChangesinNetPosition

StatementofCashFlows

StatementofNetPosition

Accountingbasisandmeasurementfocus

Accrualaccountingandeconomicresourcesfocus

Modifiedaccrualaccountingandcurrentfinancialresourcesfocus

Accrualaccountingandeconomicresourcesfocus

Accrualaccountingandeconomicresourcesfocus

Typeofasset/liabilityinformation

Allassetsandliabilities,bothfinancialandcapital,short‐termandlong‐term

Onlyassetsexpectedtobeusedupandliabilitiesthatcomedueduringtheyearorsoonthereafter;nocapitalassetsincluded

Allassetsandliabilities,bothshort‐termandlong‐term;TheCounty’sfundsdonotcurrentlycontainnonfinancialassets,thoughtheycan

Allassetsandliabilities,bothshort‐termandlong‐term;TheCounty’sfundsdonotcurrentlycontainnonfinancialassets,thoughtheycan

Typeofinflow/outflowinformation

Allrevenuesandexpensesduringyear,regardlessofwhencashisreceivedorpaid

Revenuesforwhichcashisreceivedduringorsoonaftertheendoftheyear;expenditureswhengoodsorserviceshavebeenreceivedandpaymentisdueduringtheyearorsoonthereafter

Allrevenuesandexpensesduringtheyear,regardlessofwhencashisreceivedorpaid

Allrevenuesandexpensesduringtheyear,regardlessofwhencashisreceivedorpaid

5

SANTACLARACOUNTYOFFICEOFEDUCATIONManagement’sDiscussionandAnalysis(Unaudited)FortheFiscalYearEndedJune30,2013

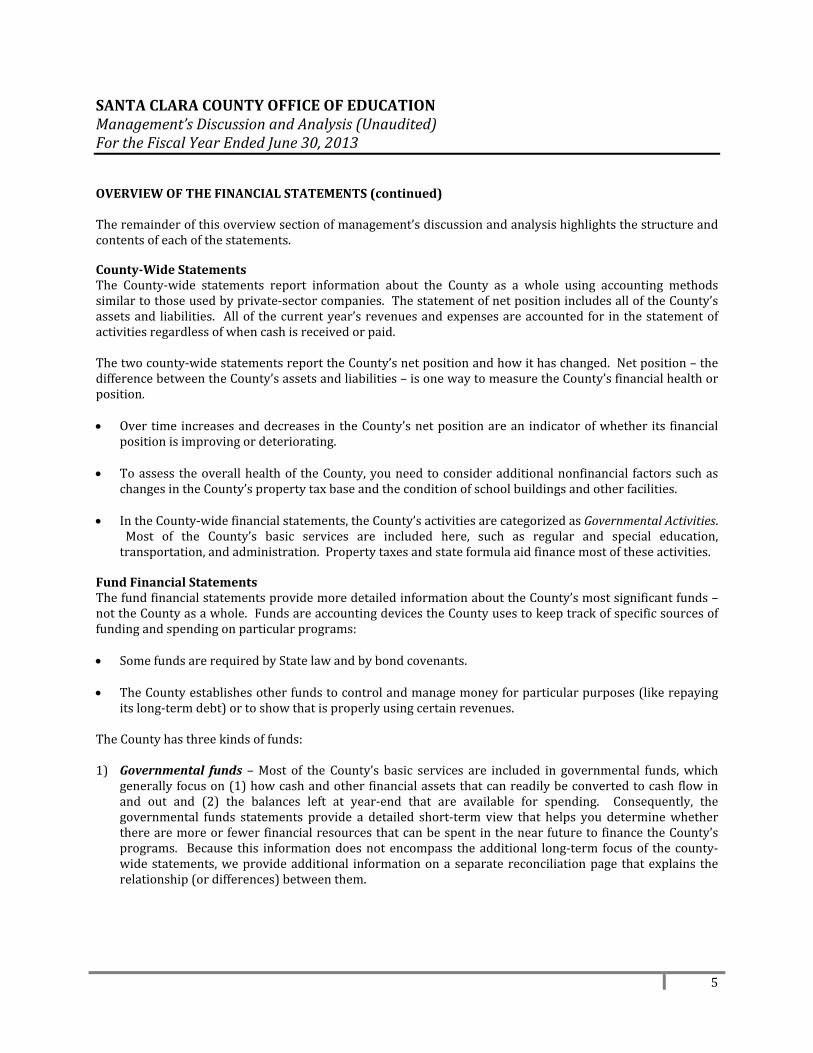

OVERVIEWOFTHEFINANCIALSTATEMENTS(continued)Theremainderofthisoverviewsectionofmanagement’sdiscussionandanalysishighlightsthestructureandcontentsofeachofthestatements.County‐WideStatementsThe County‐wide statements report information about the County as a whole using accounting methodssimilartothoseusedbyprivate‐sectorcompanies.ThestatementofnetpositionincludesalloftheCounty’sassetsand liabilities. Allof thecurrentyear’srevenuesandexpensesareaccountedfor inthestatementofactivitiesregardlessofwhencashisreceivedorpaid.Thetwocounty‐widestatementsreporttheCounty’snetpositionandhowithaschanged.Netposition–thedifferencebetweentheCounty’sassetsandliabilities–isonewaytomeasuretheCounty’sfinancialhealthorposition. Overtime increasesanddecreases intheCounty’snetpositionarean indicatorofwhether its financial

positionisimprovingordeteriorating. Toassess theoverallhealthof theCounty,youneedtoconsideradditionalnonfinancial factorssuchas

changesintheCounty’spropertytaxbaseandtheconditionofschoolbuildingsandotherfacilities. IntheCounty‐widefinancialstatements,theCounty’sactivitiesarecategorizedasGovernmentalActivities.

Most of the County’s basic services are included here, such as regular and special education,transportation,andadministration.Propertytaxesandstateformulaaidfinancemostoftheseactivities.

FundFinancialStatementsThefundfinancialstatementsprovidemoredetailedinformationabouttheCounty’smostsignificantfunds–nottheCountyasawhole.FundsareaccountingdevicestheCountyusestokeeptrackofspecificsourcesoffundingandspendingonparticularprograms: SomefundsarerequiredbyStatelawandbybondcovenants. TheCountyestablishesotherfundstocontrolandmanagemoneyforparticularpurposes(likerepaying

itslong‐termdebt)ortoshowthatisproperlyusingcertainrevenues.TheCountyhasthreekindsoffunds:1) Governmental funds –Most of the County’s basic services are included in governmental funds,which

generallyfocuson(1)howcashandotherfinancialassetsthatcanreadilybeconvertedtocashflowinand out and (2) the balances left at year‐end that are available for spending. Consequently, thegovernmental funds statements provide a detailed short‐term view that helps you determinewhethertherearemoreorfewerfinancialresourcesthatcanbespentinthenearfuturetofinancetheCounty’sprograms. Because this informationdoesnotencompass theadditional long‐term focusof thecounty‐widestatements,weprovideadditional informationonaseparatereconciliationpage thatexplains therelationship(ordifferences)betweenthem.

6

SANTACLARACOUNTYOFFICEOFEDUCATIONManagement’sDiscussionandAnalysis(Unaudited)FortheFiscalYearEndedJune30,2013

FundFinancialStatements(continued)2) Proprietary funds –When the County charges other County funds for the services it provides, these

services are reported in proprietary funds. Proprietary funds are reported in the same way that allactivitiesarereportedintheStatementofNetPositionandStatementofActivities. Infact,theCounty’sinternal service fund is included within the governmental activities reported in the County‐widestatementsbutprovidemoredetailandadditionalinformation,suchascashflows.TheCountyusestheinternal service fund to report activities that relate to the County’s self‐insured program for workerscompensationclaims.

3) Fiduciary funds – TheCounty is the trustee, or fiduciary, for assets that belong to others, such as thestudentactivities funds. TheCounty isresponsible forensuringthattheassetsreportedinthesefundsareusedonly for their intendedpurposesandbythosetowhomtheassetsbelong. Allof theCounty’sfiduciary activities are reported in a separate statement of fiduciary net position. We exclude theseactivities from the County‐wide financial statements because the County cannot use these assets tofinanceitsoperations.

FINANCIALANALYSISOFTHECOUNTYASAWHOLENetPosition.TheCounty’scombinednetpositionwashigheronJune30,2013,thanitwastheyearbefore–increasing12.4%to$126.1million(SeeTableA‐1).TableA‐1

VarianceIncrease

2013 2012* (Decrease)Currentassets 114.4$ 104.0$ 10.4$Noncurrentassets 0.4 0.5 (0.1)Capitalassets 68.3 67.7 0.6Totalassets 183.1 172.2 10.9Currentliabilities 37.5 40.9 (3.4)Long‐termliabilities 19.5 19.1 0.4Totalliabilities 57.0 60.0 (3.0)NetpositionNetinvestmentincapitalassets 57.9 56.7 1.2Restricted 15.1 22.0 (6.9)Unrestricted 53.1 33.5 19.6

Totalnetposition 126.1$ 112.2$ 13.9$

*Asrestated

GovernmentalActivities(Inmillions)

7

SANTACLARACOUNTYOFFICEOFEDUCATIONManagement’sDiscussionandAnalysis(Unaudited)FortheFiscalYearEndedJune30,2013

FINANCIALANALYSISOFTHECOUNTYASAWHOLE(continued)Changes innetposition,governmentalactivities. TheCounty’s totalrevenues increased3.4%to$258.1million(SeeTableA‐2).Theincreaseisdueprimarilytoanincreaseinrevenuelimitsources.The total cost of all programs and services decreased 4.2% to $244.2million. The County’s expenses arepredominantlyrelatedtoeducatingandcaringforstudents,59%.ThepurelyadministrativeactivitiesoftheCountyaccountedforjust10%oftotalcosts.Asignificantcontributortothedecreaseincostswasadecreaseintransferstootheragenciesandplantservices.TableA‐2

VarianceIncrease

2013 2012 (Decrease)TotalRevenues 258.1$ 249.5$ 8.6$TotalExpenses 244.2 254.9 (10.7)Increase(decrease)innetposition 13.9$ (5.4)$ 19.3$

GovernmentalActivities(Inmillions)

FINANCIALANALYSISOFTHECOUNTY’SFUNDSThe financial performance of the County as awhole is reflected in its governmental funds aswell. As theCountycompletedthisyear,itsgovernmentalfundsreportedacombinedfundbalanceof$66.7million,whichisabovelastyear’sendingfundbalanceof$56.1million.Theprimarycauseoftheincreasedfundbalanceisincreasedstatefunding.CountySchoolServicesFundBudgetaryHighlightsOverthecourseoftheyear,theCountyrevisedtheannualoperatingbudgetseveraltimes.Themajorbudgetamendmentsfallintothesecategories:

Revenues–increasedby$6.1millionprimarilytoreflectfederalandstatebudgetactions. Salariesandbenefitscosts–decreased$3.5millionduetochangesinstaffingestimates. Other non‐personnel expenses – increased $14.0 million to re‐budget carryover funds and revise

operationalcostestimates.

WhiletheCounty’s finalbudgetfortheCountySchoolServiceFundanticipatedthatrevenueswouldexceedexpendituresbyabout$3.0million,theactualresultsfortheyearshowthatrevenuesexceededexpendituresby roughly $18.4million. Actual revenueswere $4.8million less than anticipated, but expenditureswere$20.1million less thanbudgeted. Thatamount consistsprimarilyof restrictedcategoricalprogramdollarsthatwerenotspentasofJune30,2013thatwillbecarriedoverintothe2013‐14budget.

8

SANTACLARACOUNTYOFFICEOFEDUCATIONManagement’sDiscussionandAnalysis(Unaudited)FortheFiscalYearEndedJune30,2013

CAPITALASSETANDDEBTADMINISTRATIONCapitalAssetsBytheendof2012‐13theCountyhadinvested$3.8millioninnewcapitalassets.(Moredetailedinformationaboutcapitalassetscanbe foundinNote6tothefinancialstatements). Totaldepreciationexpensefortheyearexceeded$3.2million.TableA‐3:CapitalAssetsatYear‐End,NetofDepreciation

VarianceIncrease

2013 2012 (Decrease)Land 5.5$ 5.5$ ‐$Buildingsandimprovements 58.6 50.3 8.3Furnitureandequipment 3.5 4.0 (0.5)Constructioninprogress 0.7 7.9 (7.2)Total 68.3$ 67.7$ 0.6$

GovernmentalActivities(Inmillions)

Long‐TermDebtAt year‐end the County had $19.5 million in certificates of participation and employment benefits – anincreaseof1.9%fromlastyear–asshowninTableA‐4.(MoredetailedinformationabouttheCounty’slong‐termliabilitiesispresentedinNote7tothefinancialstatements).TableA‐4:OutstandingLong‐TermDebtatYear‐End

VarianceIncrease

2013 2012* (Decrease)Certificatesofparticipation 10.4 11.0 (0.6)Compensatedabsences 1.3 1.4 (0.1)Otherpostemploymentbenefits 7.8 6.7 1.1Total 19.5$ 19.1$ 0.4$

*Asrestated

GovernmentalActivities(Inmillions)

9

SANTACLARACOUNTYOFFICEOFEDUCATIONManagement’sDiscussionandAnalysis(Unaudited)FortheFiscalYearEndedJune30,2013

FACTORSBEARINGONTHECOUNTY’SFUTUREBudgetOverviewThe finalbudgetpackagewas signedby theGovernoron June27,2013. Notably,aside fromoneaction tocorrect a technical error in the Franchise Tax Board budget, the Governor did not use his line–item vetoauthority to reduce or eliminate non–Proposition 98General Fund spending. TheGovernor did, however,reducespendingfromotherfundsby$5.6million.The state spending plan assumes total budget expenditures of $138.3 billion from the General Fund andspecialfunds,anincreaseof3percentover2012–13.Thisconsistsof$96.3billionfromtheGeneralFundandEducationProtectionAccountcreatedbyProposition30(2012),aswellas$42billionfromspecialfunds.Thebudget estimates that spending from federal funds in 2013–14 will total $87.6 billion, an increase of 7.7percentover2012–13.Theadministration’sMayRevisionestimatesof2012–13revenueswereabout$2.3billionhigherthanwhenthe2012–13spendingplanwasadoptedlastyear.Thesehigherrevenuesresultin$2.5billioninadditionalexpendituresundertheProposition98minimumfundingguaranteeforK–14education.Inaddition,higherexpendituresinotherareascontributedtotheestimated2012–13GeneralFundendingbalancebeingabout$694millionlowerthanwasassumedinthe2012–13spendingplan.Nevertheless,underthespendingplan2012–13wouldendwitha$254millionreserve,thefirstsuchyear–endpositivebalanceinthereservesince2007–08.The spending plan assumesGeneral Fund andEducation ProtectionAccount revenues of $97.1 billion andexpendituresof$96.3billion. Theresulting$817millionoperatingsurpluscombinedwiththe$254millionpositiveendingbalancefor2012–13produceanestimated$1.1billionreservefor2013–14.MajorSpendingChangesForK–12education, the largest2013–14augmentation ($2.1billion) is for implementing theLocalControlFundingFormula(LCFF)forschooldistricts.Othermajor2013–14K–12augmentationsinclude$406millioningrantsandloansforenergyprojects,anadditional$250milliononaone–timebasisfortheCommonCoreStateStandardsinitiative,$250milliononaone–timebasisforanewCareerPathwaysprogram,$50millionto augment the mandate block grant, $32 million to implement the LCFF for county offices of education(COEs),and$10milliontoestablishtheCaliforniaCollaborativeforEducationalExcellence(CCEE)toprovidelow–performingschooldistrictswithacademicassistance.ThebudgetalsofurtherpaysdownK–12deferrals.Additionally,thebudgetincludesa1.57percentcost–of–living adjustment (COLA) for certain K–12 categorical programs. The budget includes a slight increase toreflect0.2percentgrowthinK–12ADA. Thebudgetalsoprovidesa$26million(5percent)increasetothepart–day/part–yearStatePreschoolprogramtosupportapproximately7,100newpreschoolslots.In 2013–14, despite fewer overall resources compared to 2012–13, much less funding is designated forpayingdowndeferrals. This frees up funds in 2013–14 that canbe used for otherpurposes. In total, thebudgetincludesa$2.6billionincreaseinK–12ongoingfunding.Ongoingfundingperstudent(asmeasuredbyADA)increasesfrom$7,590in2012–13to$8,005in2013–14—anincreaseof$415(5.5percent).

10

SANTACLARACOUNTYOFFICEOFEDUCATIONManagement’sDiscussionandAnalysis(Unaudited)FortheFiscalYearEndedJune30,2013

FACTORSBEARINGONTHECOUNTY’SFUTURE(continued)LCFFforSchoolDistrictsandCharterSchoolsThe budget package includes a major restructuring of the state’s funding system for school districts andcharter schools. The new LCFF system replaces existing funding formulas for revenue limits and mostcategoricalprogramswithaweightedstudentfundingformula.Overthecourseofimplementation,districtswillreceiveadditionalfundingtoreducethesameshareofthegapbetweentheirexistingper–pupilfundingratesandtheirtargetsundertheLCFF.FullimplementationoftheLCFFisexpectedtotakeeightyears(withfull implementation in2020–21)andcost$18billion(notaccounting for futureCOLAcosts). The2013–14BudgetActprovidesfirst–yearfundingof$2.1billion. Thisisexpectedtoclose12percentofeachdistrict’sgap.LCFFforCOEsThebudgetpackagealsoreplacestheexistingCOErevenuelimitandcategoricalfundingsystemwithanewtwo–partfundingformula.Thenewformulahas(1)onepartrelatingtofundingforoperationalservicesthatCOEsprovidetolocaleducationalagencieswithintheirrespectivecountiesand(2)asecondpartrelatingtothe alternative education services COEs directly provide to students. Similar to the approach for schooldistricts,theformulaestablishesafundingtargetforeachCOE,countsexistingfundstowardthetarget,andusesnewfundingtoclosethesameproportionalshareofeachCOE’sgapbetweenitsexistingfundinglevelandtargetfundinglevel.FullimplementationofthenewCOEsystemisexpectedtotaketwoyears(withfullimplementationin2014–15)andcost$50million.The2013–14BudgetActprovidesfirst–yearfundingof$32million—almosttwo–thirdsofthefundingneededtobringCOEsuptotheirtargetlevels.DeferralPaydownsAfter four consecutive years of increasing the amount of deferrals for schools and community colleges—reachinga totalof$10.4billion inoutstandingdeferralsby theendof2011–12—the2012–13budgetplanprovided$2.2billiontoreducetheamountofoutstandingdeferrals.Therecentlyenactedbudgetplanmakesan additional $1.8 billion in 2012–13deferral paydowns aswell as $272million inpaydowns in2013–14.Underthebudgetpackage,$6.2billioninoutstandingdeferralsremainasoftheendof2013–14.CommonCoreImplementationThebudgetplanprovides$1.25billion inone–time funding toschools for implementationof theCCSS. (Ofthisamount,thebudgetplancounts$1billiontowardsmeetingthe2012–13minimumguaranteeand$250milliontowardsmeetingthe2013–14guarantee.)TheCCSSarenationallydevelopedstandardsformathandEnglish/Language Arts that the state adopted in 2010. Under current law, schools are required to aligninstructiontotheCCSSbeginningin2014–15.The$1.25billioninCCSSfundingmustbespentin2013–14or2014–15forprofessionaldevelopment,instructionalmaterials,andtechnologythatassistschoolsinaligninginstruction to theCCSS. Local governingboardsare required in a seriesofpublicmeetings todiscuss andadoptaplanforspendingthefundsandmustreporthowthefundswerespenttotheCaliforniaDepartmentofEducation(CDE)byJuly1,2015.Proposition39PassedbythevotersinNovember2012,Proposition39increasesstatecorporatetaxrevenuesandrequiresfor a five–year period, starting in 2013–14, that a portion of these revenues be used to improve energyefficiencyandexpandtheuseofalternativeenergyinpublicbuildings.

11

SANTACLARACOUNTYOFFICEOFEDUCATIONManagement’sDiscussionandAnalysis(Unaudited)FortheFiscalYearEndedJune30,2013

FACTORSBEARINGONTHECOUNTY’SFUTURE(continued)AdultEducationIn an effort to improve coordination among adult education providers, the budget provides $25 million(Proposition 98 General Fund) for a new Adult Education Consortium Program. School districts andcommunitycollegesthatformaregionalconsortiumareeligibletoapplyforthesefunds.Inarelatedaction, thebudgetpackageeliminatesschooldistricts’adulteducationcategoricalprogramandconsolidatesallassociatedannualfunding($635millionProposition98GeneralFund)intotheschooldistrictLCFF.Thebudgetpackage,however,containsarequirementforschooldistricts(throughtheiradultschools)tomaintainatleasttheir2012–13levelofstatespendingonadulteducationin2013–14and2014–15.NewCareerPathwaysProgramThebudgetprovides$250millioninone–timeProposition98fundingtocreatea“CaliforniaCareerPathwaysTrust.” The primary purpose of the new program is to improve linkages between career technical(vocational) programs at schools and community colleges as well as between K–14 education and localbusinesses.Theprogramauthorizesseveraltypesofactivities,suchascreatingnewtechnicalprogramsandcurriculum.SpecialEducationThebudgetpackagemakesthreenotablechangestospecialeducationfunding.First,thepackagesimplifiesthestate’sapproachtodistributingfundingtospecialeducationlocalplanareas(SELPAs)bydelinkingstateand federal special educationallocation formulas. A conforming change revises the “statewide target rate”used to fund new students to the updated statewide average per–pupil funding rate. Second, the budgetprovides $2.6 million in Proposition 98 funds to fully offset federal sequestration funding cuts forpreschoolers and infants/toddlerswith disabilities and provides $2.1million in federal carryover funds topartiallymitigate federalsequestrationfundingcuts forK–12studentswithdisabilities. Third, thepackageconsolidates11specialeducationcategoricalgrantsinto5largergrants.Allof these factorswereconsidered inpreparing theSantaClaraCountyOfficeofEducationbudget for the2013‐14fiscalyear.CONTACTINGTHESANTACLARACOUNTYOFFICEOFEDUCATION'SFINANCIALMANAGEMENTThisfinancialreportisdesignedtoprovideourcitizens,taxpayers,customers,investorsandcreditorswithageneraloverviewoftheSantaClaraCountyOfficeofEducation’sfinancesandtodemonstratetheSantaClaraCountyOfficeofEducation‘saccountabilityforthemoneyitreceives.Ifyouhavequestionsaboutthisreportor need additional financial information, contact Ted O, Director‐Internal Business Services via email [email protected].

Thenotestofinancialstatementsareanintegralpartofthisstatement. 12

SANTACLARACOUNTYOFFICEOFEDUCATIONStatementofNetPositionJune30,2013

TotalGovernmental

ASSETS ActivitiesCurrentassets:

Cash 74,057,352$Accountsreceivable 39,849,060Inventories 327,110Prepaidexpenses 219,309

Totalcurrentassets 114,452,831Non‐currentassets:

Debtissuancecosts 438,336Capitalassets:

Non‐depreciableassets 6,229,631Depreciableassets 86,417,220Lessaccumulateddepreciation (24,371,073)

Totalcapitalassets,netofdepreciation 68,275,778Totalassets 183,166,945

LIABILITIESCurrentliabilities:

Accountspayable 24,304,720Claimliabilities 10,679,000Deferredrevenue 2,520,966

Totalcurrentliabilities 37,504,686Long‐termliabilities:

Dueorpayablewithinoneyear 670,000Dueorpayableafteroneyear 18,848,182

Totallong‐termliabilities 19,518,182Totalliabilities 57,022,868

NETPOSITIONNetinvestmentincapitalassets 57,875,778Restrictedfor:

Capitalprojects 3,890,972Debtservice 1,171,250Categoricalprograms 10,148,055

Unrestricted 53,058,022

Totalnetposition 126,144,077$

Thenotestofinancialstatementsareanintegralpartofthisstatement. 13

SANTACLARACOUNTYOFFICEOFEDUCATIONStatementofActivitiesFortheFiscalYearEndedJune30,2013

Net(Expense)Operating Capital Revenueand

Chargesfor Grantsand Grantsand ChangesinExpenses Services Contributions Contributions NetPosition

GovernmentalActivities:InstructionalServices:

Instruction 90,546,094$ 1,048,418$ 53,432,785$ (348,995)$ (36,413,886)$Instruction‐RelatedServices:

Supervisionofinstruction 14,418,278 2,786,221 6,726,930 ‐ (4,905,127)Instructionallibrary,mediaandtechnology 1,186,565 6 9,057 ‐ (1,177,502)Schoolsiteadministration 10,911,101 532,503 5,149,382 ‐ (5,229,216)

PupilSupportServices:Home‐to‐schooltransportation 1,169,169 ‐ 879,272 ‐ (289,897)Foodservices 1,988,175 126,628 1,603,455 ‐ (258,092)Allotherpupilservices 24,342,272 275,544 14,532,333 ‐ (9,534,395)

GeneralAdministrationServices:Dataprocessingservices 6,063,953 267 78 ‐ (6,063,608)Othergeneraladministration 17,500,895 736,736 7,073,085 ‐ (9,691,074)

Plantservices 5,918,306 176,130 3,181,082 ‐ (2,561,094)

Ancillaryservices 3,280,108 2,525,904 739,067 ‐ (15,137)Communityservices 6,000 4,743 1,383 ‐ 126Enterpriseactivities 12,565 8,488 2,475 ‐ (1,602)Transfersbetweenagencies 65,732,061 ‐ 48,729,855 ‐ (17,002,206)Interestonlong‐termdebt 526,400 ‐ ‐ ‐ (526,400)Otheroutgo 556,128 110,343 ‐ ‐ (445,785)

TotalGovernmentalActivities 244,158,070$ 8,331,931$ 142,060,239$ (348,995)$ (94,114,895)

GeneralRevenues:

Propertytaxes 85,708,740Federalandstateaidnotrestrictedtospecificpurpose 13,060,166Interestandinvestmentearnings 289,548Interagencyrevenues 3,714,417Miscellaneous 5,284,539

Totalgeneralrevenues 108,057,410

Changeinnetposition 13,942,515

Netposition‐July1,2012,asoriginallystated 108,555,179

Adjustmentsforrestatements(Note15) 3,646,383

Netposition‐July1,2012,restated 112,201,562

Netposition‐June30,2013 126,144,077$

Functions/Programs

ProgramRevenues

Thenotestofinancialstatementsareanintegralpartofthisstatement. 14

SANTACLARACOUNTYOFFICEOFEDUCATIONBalanceSheet–GovernmentalFundsJune30,2013

CountySchoolServiceFund

SpecialEducation

Pass‐ThroughFund

Non‐MajorGovernmental

Funds

TotalGovernmental

FundsASSETS

Cash 45,876,222$ 107,650$ 6,931,670$ 52,915,542$Accountsreceivable 20,880,281 18,251,214 677,217 39,808,712Duefromotherfunds 53,900,490 47,450,527 383,316 101,734,333Inventories 327,110 ‐ ‐ 327,110Prepaidexpenditures 2,309 ‐ ‐ 2,309

TotalAssets 120,986,412$ 65,809,391$ 7,992,203$ 194,788,006$

LIABILITIESANDFUNDBALANCES

LiabilitiesAccountspayable 9,217,090$ 13,173,250$ 1,434,312$ 23,824,652$Duetootherfunds 48,113,719 52,630,812 1,009,021 101,753,552Deferredrevenue 2,322,934 ‐ 198,032 2,520,966

TotalLiabilities 59,653,743 65,804,062 2,641,365 128,099,170

FundBalancesNonspendable 354,419 ‐ ‐ 354,419Restricted 9,854,110 5,329 5,350,838 15,210,277Assigned 43,240,891 ‐ ‐ 43,240,891Unassigned 7,883,249 ‐ ‐ 7,883,249

TotalFundBalances 61,332,669 5,329 5,350,838 66,688,836

TotalLiabilitiesandFundBalances 120,986,412$ 65,809,391$ 7,992,203$ 194,788,006$

Thenotestofinancialstatementsareanintegralpartofthisstatement. 15

SANTACLARACOUNTYOFFICEOFEDUCATIONReconciliationoftheGovernmentalFundsBalanceSheettotheStatementofNetPositionJune30,2013Totalfundbalances‐governmentalfunds 66,688,836$

68,275,778

(124,798)

438,336

Certificatesofparticipationpayable (10,400,000)Compensatedabsencespayable (1,300,028) (11,700,028)

2,565,953

Totalnetposition‐governmentalactivities 126,144,077$

Amountsreportedforgovernmentalactivities inthestatementofnetpositionaredifferentbecausecapitalassetsusedforgovernmentalactivitiesarenotfinancialresourcesandthereforearenotreportedasassetsingovernmentalfunds.Thecostoftheassetsis$92,646,851,andtheaccumulateddepreciationis($24,371,073).

Ingovernmentalfunds,interestonlong‐termdebtisnotrecognizeduntiltheperiodinwhichitmaturesandispaid.Inthegovernment‐widestatementofactivities,itisrecognizedintheperiodthatitisincurred.Theadditionalliabilityforunmaturedinterestowingattheendoftheperiodwas:

Ingovernmentalfunds,debtissuecostsarerecognizedasexpendituresintheperiodtheyareincurred.Inthegovernment‐widestatements,debtissuecostsareamortizedoverthelifeofthedebt.Unamortizeddebtissuecostsincludedonthestatementofnetpositionare:

Ingovernmentalfunds,onlycurrentliabilitiesarereported.Inthestatementofnetposition,allliabilities,includinglong‐termliabilities,arereported.Long‐termliabilitiesrelatingtogovernmentalactivitiesconsistof:

Internalservicefundsareusedtoconductcertainactivitiesforwhichcostsarechargedtootherfundsonafullcost‐recoverybasis.Becauseinternalservicefundsarepresumedtooperateforthebenefitofgovernmentalactivities,assetsandliabilitiesofinternalservicefundsarereportedwithgovernmentalactivitiesinthestatementofnetposition.Netpositionforinternalservicefundsis:

Thenotestofinancialstatementsareanintegralpartofthisstatement. 16

SANTACLARACOUNTYOFFICEOFEDUCATIONStatementofRevenues,Expenditures,andChangesinFundBalances–GovernmentalFundsFortheFiscalYearEndedJune30,2013

REVENUESCountySchoolServiceFund

SpecialEducation

Pass‐ThroughFund

Non‐MajorGovernmental

Funds

TotalGovernmental

FundsRevenuelimitsources 93,205,078$ ‐$ ‐$ 93,205,078$Federalsources 40,987,170 20,633,360 2,302,143 63,922,673Otherstatesources 22,809,363 38,960,839 2,573,007 64,343,209Otherlocalsources 34,882,982 1,282,354 464,289 36,629,625

TotalRevenues 191,884,593 60,876,553 5,339,439 258,100,585EXPENDITURES

Current:Instruction 84,870,626 ‐ 3,558,811 88,429,437Instruction‐relatedservices:

Supervisionofinstruction 13,642,488 ‐ 436,161 14,078,649Instructionallibrary,mediaandtechnology 1,152,612 ‐ ‐ 1,152,612Schoolsiteadministration 10,101,330 ‐ 568,459 10,669,789

Pupilsupportservices:Home‐to‐schooltransportation 1,128,176 ‐ ‐ 1,128,176Foodservices 273,766 ‐ 1,671,346 1,945,112Allotherpupilservices 23,733,141 ‐ 140,756 23,873,897

Ancillaryservices 3,198,511 ‐ ‐ 3,198,511Communityservices 6,000 ‐ ‐ 6,000Enterpriseactivities 10,737 ‐ ‐ 10,737Generaladministrationservices:

Dataprocessingservices 6,017,116 ‐ ‐ 6,017,116Othergeneraladministration 18,219,968 ‐ 125 18,220,093

Plantservices 5,890,660 ‐ 408,693 6,299,353Transfersofindirectcosts (506,192) ‐ 506,192 ‐

Intergovernmentaltransfers 4,859,235 60,872,825 ‐ 65,732,060Capitaloutlay 918,357 ‐ 2,703,359 3,621,716Debtservice:

Principal ‐ ‐ 640,000 640,000Interest ‐ ‐ 526,400 526,400

TotalExpenditures 173,516,531 60,872,825 11,160,302 245,549,658

Excess(Deficiency)ofRevenuesOver(Under)Expenditures 18,368,062 3,728 (5,820,863) 12,550,927

OTHERFINANCINGSOURCES(USES)Interfundtransfersin 148,376 ‐ 3,417,778 3,566,154Interfundtransfersout (5,406,554) ‐ (148,376) (5,554,930)

TotalOtherFinancingSourcesandUses (5,258,178) ‐ 3,269,402 (1,988,776)

NetChangeinFundBalances 13,109,884 3,728 (2,551,461) 10,562,151

48,222,785 1,601 7,902,299 56,126,685

FundBalances,June30,2013 61,332,669$ 5,329$ 5,350,838$ 66,688,836$

FundBalances,July1,2012

Thenotestofinancialstatementsareanintegralpartofthisstatement. 17

SANTACLARACOUNTYOFFICEOFEDUCATIONReconciliationoftheGovernmentalFundsStatementofRevenues,Expenditures, andChangesinFundBalancestotheStatementofActivitiesFortheFiscalYearEndedJune30,2013

Totalnetchangeinfundbalances‐governmentalfunds 10,562,151$

Amountsreportedforgovernmentalactivities inthestatementofactivitiesaredifferentbecause:

Expendituresforcapitaloutlay 3,840,681Depreciationexpense (3,246,521)

Net: 594,160

640,000

(36,526)

(15,249)

6,800

71,308

2,119,871

Changeinnetpositionofgovernmentalactivities 13,942,515$

Capitaloutlaysarereportedingovernmentalfundsasexpenditures.However,inthestatementofactivities,thecostofthoseassetsisallocatedovertheirestimatedusefullivesasdepreciationexpense.Thedifferencebetweencapitaloutlayexpendituresanddepreciationexpensefortheperiodis:

Ingovernmentalfunds,repaymentsoflong‐termdebtarereportedasexpenditures.Inthegovernment‐widestatements,repaymentsoflong‐termdebtarereportedasreductionofliabilities.Expendituresforrepaymentoftheprincipalportionoflong‐termdebtwere:

Theinternalservicefundisusedbymanagementtochargethecostofself‐insuranceactivities.Thenetrevenue(expense)oftheinternalservicefundisreportedwithgovernmentalactivities.

Ingovernmentalfunds,debtissuancecostsarerecognizedasexpendituresintheperiodtheyareincurred.Inthegovernment‐widestatements,debtissuancecostsareamortizedoverthelifeofthedebt.Debtissuancecostsamortizedfortheperiodwere:

Ingovernmentalfunds,interestonlong‐termdebtisrecognizedintheperiodthatitbecomesdue.Inthegovernment‐widestatementofactivities,itisrecognizedintheperiodthatitisincurred.Unmaturedinterestowingattheendoftheperiod,lessmaturedinterestpaidduringtheperiodbutowingfromthepriorperiod,was:

Inthestatementofactivities,compensatedabsencesaremeasuredbytheamountsearnedduringtheyear.Inthegovernmentalfunds,however,expendituresfortheseitemsaremeasuredbytheamountoffinancialresourcesused(essentially,theamountsactuallypaid.)

Ingovernmentalfunds,theentireproceedsfromdisposalofcapitalassetsarereportedasrevenue.Inthestatementofactivities,onlytheresultinggainorlossisreported.Thedifferencebetweentheproceedsfromdisposalofcapitalassetsandtheresultinggainorlossis:

Thenotestofinancialstatementsareanintegralpartofthisstatement. 18

SANTACLARACOUNTYOFFICEOFEDUCATIONStatementofNetPosition–ProprietaryFundJune30,2013

GovernmentalActivities:

InternalServiceFund

ASSETSCash 21,141,810$Otherreceivables 40,348Prepaidexpenses 217,000Duefromotherfunds 283,389

TotalAssets 21,682,547

LIABILITIESClaimliabilities 10,679,000OPEBliability 7,818,154Accountspayable 355,270Duetootherfunds 264,170

TotalLiabilities 19,116,594

NETPOSITIONRestricted 2,565,953$

Thenotestofinancialstatementsareanintegralpartofthisstatement. 19

SANTACLARACOUNTYOFFICEOFEDUCATIONStatementofRevenues,ExpensesandChangesinNetPosition–ProprietaryFundFortheFiscalYearEndedJune30,2013

GovernmentalActivities:

InternalServiceFund

OPERATINGREVENUESChargestootherfunds 8,815,291$Otherlocalrevenues 360,957

Totaloperatingrevenues 9,176,248

OPERATINGEXPENSESClassifiedsalaries 217,380Employeebenefits 74,969Booksandsupplies 19,787Servicesandotheroperatingexpenditures 8,827,429

Totaloperatingexpenses 9,139,565

OperatingIncome 36,683

NON‐OPERATINGREVENUESInterestincome 94,412

Incomebeforetransfers 131,095

Interfundtransfersin 1,988,776

Changeinnetposition 2,119,871

Netposition,July1,2012,asoriginallystated 7,180,857

Adjustmentforrestatement(Note15) (6,734,775)

Netposition,July1,2012,restated 446,082

Netposition,June30,2013 2,565,953$

Thenotestofinancialstatementsareanintegralpartofthisstatement. 20

SANTACLARACOUNTYOFFICEOFEDUCATIONStatementofCashFlows–ProprietaryFundFortheFiscalYearEndedJune30,2013

GovernmentalActivities:

InternalServiceFund

CASHFLOWSFROMOPERATINGACTIVITIESCashreceivedfromassessmentsmadetootherfunds 9,726,649$Cashreceivedfromretireepremiumpayments 361,921Cashpaymentsforpayroll,insuranceandoperatingcosts (8,286,318)

Netcashprovided(used)byoperatingactivities 1,802,252

CASHFLOWSFROMNON‐INVESTINGACTIVITIESOperatingtransfersin 1,988,776

CASHFLOWSFROMINVESTINGACTIVITIESInterestoninvestments 105,538

Netincrease(decrease)incash 3,896,566

Cash,July1,2012 17,245,244

Cash,June30,2013 21,141,810$

Operatingincome(loss) 36,683$

(Increase)Decreaseinoperatingassets:Duefromotherfunds 647,188Accountsreceivable 964Prepaidexpenses 158,748

Increase(Decrease)inoperatingliabilities:Duetootherfunds 264,170Claimliabilities (441,000)OPEBliability 1,083,379Accountspayable 52,120

Netcashprovided(used)byoperatingactivities 1,802,252$

byoperatingactivities:Reconciliationofoperatingincome(loss)tonetcashprovided(used)

Thenotestofinancialstatementsareanintegralpartofthisstatement. 21

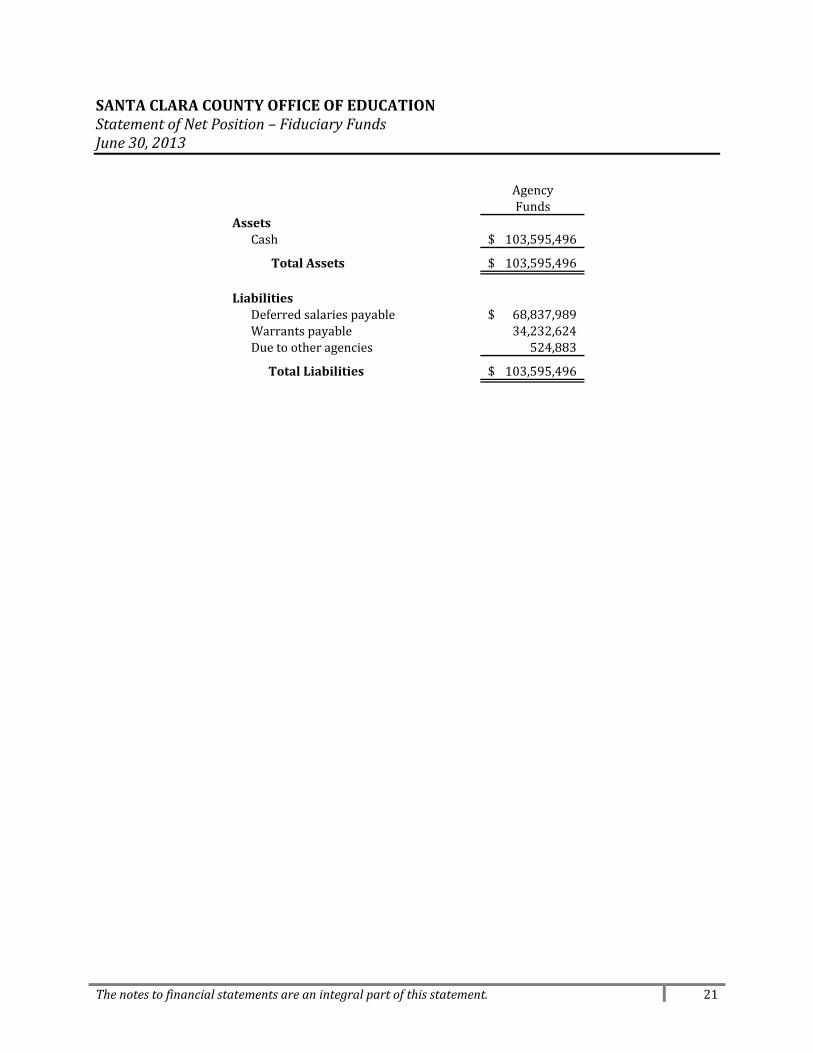

SANTACLARACOUNTYOFFICEOFEDUCATIONStatementofNetPosition–FiduciaryFundsJune30,2013

AgencyFunds

AssetsCash 103,595,496$

TotalAssets 103,595,496$

LiabilitiesDeferredsalariespayable 68,837,989$Warrantspayable 34,232,624Duetootheragencies 524,883

TotalLiabilities 103,595,496$

22

SANTACLARACOUNTYOFFICEOFEDUCATIONNotestoFinancialStatementsJune30,2013NOTE1‐SIGNIFICANTACCOUNTINGPOLICIESA. ReportingEntity

Theaccompanying financial statementspresent theactivitiesofSantaClaraCountyOfficeofEducationand itscomponentunits, legallyseparateorganizations forwhich theCounty is financiallyaccountable.Thesecomponentunitsareso intertwinedwiththeCountythat theyare, insubstance, thesameastheCountyand,therefore,areblendedandreportedasiftheywerepartoftheCounty.TheCountyBoardofEducation also serves as the governing board for the Santa Clara County Board of Education FinanceCorporation. Although the board members of the Santa Clara County Board of Education FinanceCorporationareappointedby theCountyBoard, thecorporationexistssolelyto financetheacquisitionandconstructionofequipmentandfacilitiesfortheCounty.

ComponentUnit

IncludedintheReportingEntityBecause:

SeparateFinancialStatements

Santa Clara County Board ofEducation Finance Corporationwas formedonFebruary2, 1995 forthe sole purpose of providingfinancial assistance to the County byacquiring, constructing, financing,selling and leasing public facilities,land, personal property andequipment for theuseandbenefitofthe County. The County leasescertain school facilities from thecorporation under a lease‐purchaseagreementdatedMay1,2007.

BoardofEducationcomposesboardofFinanceCorporation

AvailablebycontactingtheCounty.

B. BasisofPresentation,BasisofAccounting

1. BasisofPresentationGovernment‐WideFinancialStatementsThestatementofnetpositionandthestatementofactivitiesdisplayinformationabouttheprimarygovernment(theCounty)anditscomponentunits. Thesestatementsincludethefinancialactivitiesoftheoverallgovernment,exceptforfiduciaryactivities. Eliminationshavebeenmadetominimizethedouble‐countingof internal activities. These statementsdistinguishbetween thegovernmentaland business‐type activities of the County. Governmental activities generally are financed throughtaxes,intergovernmentalrevenues,andothernonexchangetransactions.ThestatementofactivitiespresentsacomparisonbetweendirectexpensesandprogramrevenuesforeachfunctionoftheCounty'sgovernmentalactivities.Directexpensesarethosethatarespecificallyassociatedwithaprogramorfunctionand,therefore,areclearlyidentifiabletoaparticularfunction.Program revenues include (a) fees, fines, and charges paid by the recipients of goods or servicesoffered by the programs and (b) grants and contributions that are restricted to meeting theoperational or capital requirements of a particular program. Revenues that are not classified asprogramrevenues,includingalltaxes,arepresentedasgeneralrevenues.

23

SANTACLARACOUNTYOFFICEOFEDUCATIONNotestoFinancialStatementsJune30,2013NOTE1‐SIGNIFICANTACCOUNTINGPOLICIES(continued)B. BasisofPresentation,BasisofAccounting(continued)

1. BasisofPresentation(continued)

FundFinancialStatementsThe fund financial statementsprovide informationabout theCounty's funds, including its fiduciaryfunds (andblendedcomponentunits). Separatestatements foreach fundcategory ‐governmental,proprietary, and fiduciary ‐ are presented. The emphasis of fund financial statements is onmajorgovernmental funds, each displayed in a separate column. All remaining governmental funds areaggregatedandreportedasnonmajorfunds.Proprietaryfundoperatingrevenues,suchaschargesforservices,resultfromexchangetransactionsassociatedwith the principal activity of the fund. Exchange transactions are those inwhich eachpartyreceivesandgivesupessentiallyequalvalues. Nonoperatingrevenues,suchassubsidiesandinvestmentearnings,resultfromnonexchangetransactionsorancillaryactivities.MajorGovernmentalFundsTheCountymaintainsthefollowingmajorgovernmentalfunds:

CountySchoolServicesFund:ThisfundisthegeneraloperatingfundoftheCounty.Itisusedtoaccountforallfinancialresourcesexceptthoserequiredtobeaccountedforinanotherfund.SpecialEducationPass‐ThroughFund:ThisfundisusedbytheAdministrativeUnitofamulti‐district Special Education Local Plan Area (SELPA) to account for Special Education revenuepassedthroughtoothermemberdistricts.

Non‐MajorGovernmentalFundsTheCountymaintainsthefollowingnon‐majorgovernmentalfunds:

SpecialRevenueFunds:

ChildDevelopmentFund: This fund isused to account for resources committed to childdevelopmentandpreschoolprogramsmaintainedbytheCounty.CafeteriaFund:ThisfundisusedtoaccountforrevenuesreceivedandexpendituresmadetooperatetheCounty'sfoodserviceoperations.

CapitalProjectsFunds:

County School Facilities Fund: This fund is used to account for state apportionmentsprovidedformodernizationofschoolfacilitiesunderSB50.

DebtServiceFund:

DebtServiceFund:Thisfundisusedtoaccountfortheaccumulationofresourcesfor,andthe payment of, long‐term debt principal, interest, and related costs on the certificates ofparticipation.

24

SANTACLARACOUNTYOFFICEOFEDUCATIONNotestoFinancialStatementsJune30,2013NOTE1‐SIGNIFICANTACCOUNTINGPOLICIES(continued)B. BasisofPresentation,BasisofAccounting(continued)

1. BasisofPresentation(continued)

ProprietaryFundsProprietary fund reporting focuses on the determination of operating income, changes in netposition,financialposition,andcashflows.Proprietaryfundsareclassifiedasenterpriseorinternalservice.TheCountyhasthefollowingproprietaryfund:

InternalServiceFunds:ThesefundsmaybeusedtoaccountforanyactivityforwhichservicesareprovidedtootherfundsoftheCountyOfficeofEducationonacostreimbursementbasis.TheCounty Office of Education operates a self‐insurance program for workers compensation,propertyand liability,otherpostemploymentbenefits,dental, vision, andmedicalbenefits thatareaccountedforinoneinternalservicefundwithmultiplesub‐funds.

FiduciaryFundsFiduciary fund reporting focuses onnet position and changes in net position. Fiduciary funds areusedtoreportassetsheldinatrusteeoragencycapacityforothersandthereforecannotbeusedtosupport the County's own programs. The fiduciary fund category includes pension (and otheremployeebenefit)trustfunds,investmenttrustfunds,private‐purposetrustfunds,andagencyfunds.TheCountymaintainsthefollowingfiduciaryfunds:

Agency Funds: The County maintains a DFS account for clearing funds which are holdingaccountsforCountywarrants,payroll,taxeswithheld,TRANS,andcharterschoolclearing.

2. MeasurementFocus,BasisofAccounting

Government‐Wide,Proprietary,andFiduciaryFundFinancialStatementsThe government‐wide, proprietary, and fiduciary fund financial statements are reported using theeconomicresourcesmeasurementfocusandtheaccrualbasisofaccounting.Revenuesarerecordedwhenearnedandexpensesarerecordedat thetime liabilitiesare incurred,regardlessofwhentherelated cash flows take place. Nonexchange transactions, inwhich the County gives (or receives)valuewithoutdirectlyreceiving(orgiving)equalvalue inexchange, includepropertytaxes,grants,entitlements,anddonations. Onanaccrualbasis,revenuefrompropertytaxes isrecognizedinthefiscalyearinwhichalleligibilityrequirementshavebeensatisfied.GovernmentalFundFinancialStatementsGovernmental fundsarereportedusingthecurrent financialresourcesmeasurement focusandthemodifiedaccrualbasisofaccounting.Underthismethod,revenuesarerecognizedwhenmeasurableandavailable.TheCountyconsidersallrevenuesreportedinthegovernmentalfundstobeavailableif the revenues are collectedwithin 60 days after year‐end. Expenditures are recordedwhen therelatedfundliabilityis incurred,exceptforprincipalandinterestongenerallong‐termdebt,claimsandjudgments,andcompensatedabsences,whicharerecognizedasexpenditurestotheextenttheyhave matured. Capital asset acquisitions are reported as expenditures in governmental funds.Proceedsofgenerallong‐termdebtandfinancingfromcapitalleasesarereportedasotherfinancingsources.

25

SANTACLARACOUNTYOFFICEOFEDUCATIONNotestoFinancialStatementsJune30,2013NOTE1‐SIGNIFICANTACCOUNTINGPOLICIES(continued)C. BudgetsandBudgetaryAccounting

Annualbudgets areadoptedonabasis consistentwithgenerallyacceptedaccountingprinciples forallgovernmentfunds.Bystatelaw,theCounty'sgoverningboardmustadoptabudgetnolaterthanJuly1.A public hearingmust be conducted to receive comments prior to adoption. The County's governingboardsatisfiedtheserequirements.

These budgets are revised by the County's governing board during the year to give consideration tounanticipated income and expenditures. The final adopted and revised budgets are presented for theGeneralFundandtheSpecialEducationPass‐ThroughFundintherequiredsupplementaryinformationsection.

Formal budgetary integration was employed as a management control device during the year for allbudgeted funds. TheCounty employs budget control byminor object andby individual appropriationaccounts.Expenditurescannotlegallyexceedappropriationsbymajorobjectaccount.

D. EncumbrancesEncumbranceaccounting isused inallbudgeted funds toreserveportionsofapplicableappropriationsforwhichcommitmentshavebeenmade.Encumbrancesarerecordedforpurchaseorders,contracts,andother commitmentswhen they arewritten. Encumbrances are liquidatedwhen the commitments arepaid.AllencumbrancesareliquidatedasofJune30.

E. Assets,Liabilities,andNetPosition

1. DepositsandInvestments

ThecashbalancesofsubstantiallyallfundsarepooledandinvestedbytheCountyTreasurerforthepurposeofincreasingearningsthroughinvestmentactivities.Thepool'sinvestmentsarereportedatfairvalueatJune30,2013,basedonmarketprices.Theindividualfunds'portionsofthepool'sfairvalue are presented as "Pooled Cash and Investments". Earnings on the pooled funds areapportionedandpaidorcreditedtothefundsquarterlybasedontheaveragedailybalanceofeachparticipatingfund.

2. CashandCashEquivalents

TheCountyconsiderscashandcashequivalentsinproprietaryfundstobecashonhandanddemanddeposits.Inaddition,becausetheTreasuryPoolissufficientlyliquidtopermitwithdrawalofcashatanytimewithoutpriornoticeorpenalty,equityinthepoolisalsodeemedtobeacashequivalent.

3. PropertyTaxCalendar

TheCountyisresponsiblefortheassessment,collection,andapportionmentofpropertytaxesforalljurisdictionsincludingtheschoolsandspecialdistrictswithintheCounty.TheBoardofSupervisorsleviespropertytaxesasofSeptember1onpropertyvaluesassessedonJuly1.Securedpropertytaxpaymentsaredueintwoequalinstallments.ThefirstisgenerallydueNovember1andisdelinquentwithpenaltiesonDecember10,andthesecondisgenerallydueonFebruary1andisdelinquentwithpenaltiesonApril10.SecuredpropertytaxesbecomealienonthepropertyonJanuary1.

4. InventoriesandPrepaidItemsInventoriesarevaluedatcostusingthefirst‐in/first‐out(FIFO)method.Thecostsofgovernmentalfund‐typeinventoriesarerecordedasexpenditureswhenconsumedratherthanwhenpurchased.Certainpaymentstovendorsreflectcostsapplicabletofutureaccountingperiodsandarerecordedasprepaiditems.

26

SANTACLARACOUNTYOFFICEOFEDUCATIONNotestoFinancialStatementsJune30,2013NOTE1‐SIGNIFICANTACCOUNTINGPOLICIES(continued)E. Assets,Liabilities,andNetPosition(continued)

5. CapitalAssets

Purchased or constructed capital assets are reported at cost or estimatedhistorical cost. Donatedfixed assets are recorded at their estimated fair value at thedateofdonation. The costofnormalmaintenanceandrepairs thatdonotaddtothevalueof theassetormateriallyextendassets' livesarenotcapitalized.Capital assets are depreciated using the straight‐line method over the following estimated usefullives:

Description EstimatedLivesBuildingsandImprovements 20‐30yearsFurnitureandEquipment 4‐25years

6. CompensatedAbsences

The liability for compensated absences reported in the government‐wide statements consists ofunpaid,accumulatedannualandvacationleavebalances.Theliabilityhasbeencalculatedusingthevestingmethod, inwhich leave amounts for both employeeswho currently are eligible to receivetermination payments and other employees who are expected to become eligible in the future toreceivesuchpaymentsuponterminationareincluded.

7. FundBalancesThefundbalanceforgovernmentalfundsisreportedinclassificationsbasedontheextenttowhichthegovernment isboundtohonorconstraintsonthespecificpurposesforwhichamounts inthosefundscanbespent.Nonspendable: Fund balance is reported as nonspendable when the resources cannot be spentbecausetheyareeitherinanonspendableformorlegallyorcontractuallyrequiredtobemaintainedintact.Resourcesinnonspendableformincludeinventoriesandprepaidassets.Restricted: Fund balance is reported as restricted when the constraints placed on the use ofresourcesareeitherexternallyimposedbycreditors,grantors,contributors,orlawsorregulationsofothergovernments;orimposedbylawthroughconstitutionalprovisionorbyenablinglegislation.Committed:TheCounty'shighestdecision‐makinglevelofauthorityrestswiththeCounty'sBoard.Fund balance is reported as committed when the Board passes a resolution that places specifiedconstraints on how resources may be used. The Board can modify or rescind a commitment ofresourcesthroughpassageofanewresolution.Assigned:ResourcesthatareconstrainedbytheCounty'sintenttousethemforaspecificpurpose,but are neither restricted nor committed, are reported as assigned fund balance. Intent may beexpressedbyeithertheBoard,committees(suchasbudgetorfinance),orofficialstowhichtheBoardhasdelegatedauthority.Unassigned: Unassigned fund balance represents fund balance that has not been restricted,committed,orassignedandmaybeutilizedbytheCountyforanypurpose.Whenexpendituresareincurred,andbothrestrictedandunrestrictedresourcesareavailable,itistheCounty'spolicytouserestrictedresourcesfirst,thenunrestrictedresourcesintheorderofcommitted,assigned,andthenunassigned,astheyareneeded.

27

SANTACLARACOUNTYOFFICEOFEDUCATIONNotestoFinancialStatementsJune30,2013NOTE1‐SIGNIFICANTACCOUNTINGPOLICIES(continued)F. UseofEstimates

The preparation of financial statements in conformity with generally accepted accounting principlesrequiresmanagementtomakeestimatesandassumptionsthataffectthereportedamountsofassetsandliabilitiesanddisclosureofcontingentassetsandliabilitiesatthedateofthefinancialstatementsandthereportedamountsofrevenuesandexpendituresduringthereportedperiod. Actualresultscoulddifferfromthoseestimates.

G. NewGASBPronouncements

Duringthe2012‐13fiscalyear,thefollowingGASBPronouncementsbecameeffective:GASBStatementNo.60,AccountingandFinancialReportingforServiceConcessionArrangements:TheobjectiveofthisStatement isto improvefinancialreportingbyaddressingissuesrelatedtoserviceconcessionarrangements(SCAs),whichareatypeofpublic‐privateorpublic‐publicpartnership.Asusedin this Statement, an SCA is an arrangement between a transferor (a government) and an operator(governmentalornongovernmentalentity)inwhich(1)thetransferorconveystoanoperatortherightand related obligation to provide services through the use of infrastructure or another public asset (a"facility") inexchangeforsignificantconsiderationand(2)theoperatorcollectsandiscompensatedbyfeesfromthirdparties. TherequirementsofthisStatementimprovefinancialreportingbyestablishingrecognition,measurement,anddisclosurerequirementsforSCAsforbothtransferorsandgovernmentaloperators, requiringgovernments toaccount forandreportSCAs in thesamemanner,which improvesthecomparabilityoffinancialstatements.GASB Statement No. 61, The Financial Reporting Entity: Omnibus ‐ An Amendment of GASBStatementsNo.14andNo.34: Theobjectiveof thisStatement is to improve financial reporting foragovernmentalfinancialreportingentity.TherequirementsofStatementNo.14,TheFinancialReportingEntity,andtherelatedfinancialreportingrequirementsofStatementNo.34,BasicFinancialStatements‐andManagement'sDiscussion andAnalysis ‐ for State and LocalGovernments, were amended to bettermeet user needs and to address reporting entity issues that have arisen since the issuance of thoseStatements.ThisStatementmodifiescertainrequirementsforinclusionofcomponentunitsinthefinancialreportingentity.Fororganizationsthatpreviouslywererequiredtobeincludedascomponentunitsbymeetingthefiscal dependency criterion, a financial benefit or burden relationship also would need to be presentbetweentheprimarygovernmentandthatorganizationforittobeincludedinthereportingentityasacomponent unit. Further, for organizations that do not meet the financial accountability criteria forinclusion as component units but that, nevertheless, should be included because the primarygovernment’s management determines that it would be misleading to exclude them, this Statementclarifies the manner in which that determination should be made and the types of relationships thatgenerallyshouldbeconsideredinmakingthedetermination.ThisStatementalsoamendsthecriteriaforreportingcomponentunitsasiftheywerepartoftheprimarygovernment(thatis,blending)incertaincircumstances.Forcomponentunitsthatcurrentlyareblendedbased on the “substantively the same governing body” criterion, it additionally requires that (1) theprimary government and the component unit have a financial benefit or burden relationship or (2)management (below the level of the elected officials) of the primary government have operationalresponsibility(asdefinedinparagraph8a)fortheactivitiesofthecomponentunit.Newcriteriaalsoareadded to require blending of component units whose total debt outstanding is expected to be repaidentirely or almost entirely with resources of the primary government. The blending provisions areamended to clarify that funds of a blended component unit have the same financial reportingrequirementsasafundoftheprimarygovernment.

28

SANTACLARACOUNTYOFFICEOFEDUCATIONNotestoFinancialStatementsJune30,2013NOTE1‐SIGNIFICANTACCOUNTINGPOLICIES(continued)G. NewGASBPronouncements(continued)

GASBStatementNo.62,CodificationofAccountingandFinancialReportingGuidanceContained inPre‐November 30, 1989 FASB and AICPA Pronouncements: The objective of this Statement is toincorporate into theGASB’s authoritative literature certain accounting and financial reporting guidancethatisincludedinthefollowingpronouncementsissuedonorbeforeNovember30,1989,whichdoesnotconflictwithorcontradictGASBpronouncements:

1. FinancialAccountingStandardsBoard(FASB)StatementsandInterpretations2. AccountingPrinciplesBoardOpinions3. AccountingResearchBulletinsoftheAmericanInstituteofCertifiedPublicAccountants’(AICPA)

CommitteeonAccountingProcedure.Hereinafter,thesepronouncementscollectivelyarereferredtoasthe“FASBandAICPApronouncements.”This Statement also supersedes Statement No. 20, Accounting and Financial Reporting for ProprietaryFunds and Other Governmental Entities That Use Proprietary Fund Accounting, thereby eliminating theelection provided in paragraph 7 of that Statement for enterprise funds and business‐type activities toapplypost‐November30,1989FASBStatementsandInterpretationsthatdonotconflictwithorcontradictGASBpronouncements.However,thoseentitiescancontinuetoapply,asotheraccountingliterature,post‐November30,1989FASBpronouncementsthatdonotconflictwithorcontradictGASBpronouncements,includingthisStatement.Statement No. 63, Financial Reporting of Deferred Outflows of Resources, Deferred Inflows ofResources,andNetPosition:ThisStatementprovidesfinancialreportingguidancefordeferredoutflowsof resources and deferred inflows of resources. Concepts Statement No. 4, Elements of FinancialStatements,introducedanddefinedthoseelementsasaconsumptionofnetassetsbythegovernmentthatis applicable to a future reporting period, and an acquisition of net assets by the government that isapplicabletoafuturereportingperiod,respectively.Previousfinancialreportingstandardsdonotincludeguidanceforreportingthosefinancialstatementelements,whicharedistinctfromassetsandliabilities.Concepts Statement 4 also identifies net position as the residual of all other elements presented in astatementoffinancialposition.ThisStatementamendsthenetassetreportingrequirementsinStatementNo. 34, Basic Financial Statements—and Management’s Discussion and Analysis—for State and LocalGovernments, and other pronouncements by incorporating deferred outflows of resources and deferredinflows of resources into the definitions of the required components of the residual measure and byrenamingthatmeasureasnetposition,ratherthannetassets.

29

SANTACLARACOUNTYOFFICEOFEDUCATIONNotestoFinancialStatementsJune30,2013NOTE2–CASHCashatJune30,2013isreportedatfairvalueandconsistedofthefollowing:

GovernmentalFunds

ProprietaryFund Total

FiduciaryFunds

PooledFunds:Cashincountytreasury 51,719,292$ 21,003,828$ 72,723,120$ 103,595,496$Cashwithfiscalagent 1,171,250 ‐ 1,171,250 ‐

TotalPooledFunds 52,890,542 21,003,828 73,894,370 103,595,496

Deposits:Cashonhandandinbanks ‐ 137,982 137,982 ‐Cashinrevolvingfund 25,000 ‐ 25,000 ‐

TotalDeposits 25,000 137,982 162,982 ‐

TotalCash 52,915,542$ 21,141,810$ 74,057,352$ 103,595,496$

GovernmentalActivities

PooledFundsIn accordancewith Education Code Section 41001, the Countymaintains substantially all of its cash in theCounty Treasury. The County pools and invests the cash. These pooled funds are carried at cost whichapproximatesfairvalue. Interestearnedisdepositedannuallytoparticipatingfunds. Anyinvestmentlossesareproportionatelysharedbyallfundsinthepool.

BecausetheCounty'sdepositsaremaintainedinarecognizedpooledinvestmentfundunderthecareofathirdpartyandtheCounty'sshareofthepooldoesnotconsistofspecific,identifiableinvestmentsecuritiesownedby the County, no disclosure of the individual deposits and investments or related custodial credit riskclassificationsisrequired.In accordancewith applicable state laws, the CountyTreasurermay invest in derivative securitieswith theState of California. However, at June 30, 2013, the County Treasurer has represented that the PooledInvestmentFundcontainednoderivativesorotherinvestmentswithsimilarriskprofiles.CustodialCreditRisk–DepositsCustodialcreditriskistheriskthatintheeventofabankfailure,theCounty’sdepositsmaynotbereturnedtoit. TheCountydoesnothaveapolicy forcustodialcreditrisk fordeposits. Cashbalancesheld inbanksareinsuredupto$250,000bytheFederalDepositoryInsuranceCorporation(FDIC)andarecollateralizedbytherespective financial institutions. In addition, the California Government Code requires that a financialinstitutionsecuredepositsmadebyStateor localgovernmentalunitsbypledgingsecurities inanundividedcollateralpoolheldbyadepositoryregulatedunderState law(unlesssowaivedby thegovernmentalunit).Themarketvalueof thepledgedsecurities inthecollateralpoolmustequalat least110percentof thetotalamount deposited by the public agencies. California law also allows financial institutions to secure publicdeposits by pledging first trust deed mortgage notes having a value of 150 percent of the secured publicdepositsand lettersof credit issuedby theFederalHomeLoanBankofSanFranciscohavingavalueof105percent of the secured deposits. As of June 30, 2013, none of the County’s bank balance was exposed tocustodialcreditriskbecauseitwasinsuredbytheFDIC.

30

SANTACLARACOUNTYOFFICEOFEDUCATIONNotestoFinancialStatementsJune30,2013NOTE3–ACCOUNTSRECEIVABLEAccountsreceivableasofJune30,2013consistedofthefollowing:

CountySchoolServiceFund

SpecialEducationPass‐ThroughFund

Non‐MajorGovernmental

Funds

Self‐InsuranceFund Totals

FederalGovernment:Categoricalaidprograms 10,684,457$ ‐$ 299,353$ ‐$ 10,983,810$

StateGovernment:Revenuelimit 3,108,961 17,825,118 ‐ ‐ 20,934,079Lottery 294,106 ‐ ‐ ‐ 294,106Specialeducation 4,729,184 ‐ ‐ ‐ 4,729,184Childnutrition ‐ ‐ 6,332 ‐ 6,332Categoricalaidprograms 1,514,685 ‐ 147,439 ‐ 1,662,124

Local:Interest 57,264 657 6,004 15,799 79,724Other 491,624 425,439 218,089 24,549 1,159,701

Total 20,880,281$ 18,251,214$ 677,217$ 40,348$ 39,849,060$

NOTE4‐INTERFUNDTRANSACTIONSA. BalancesDueTo/FromOtherFunds

Balancesdueto/fromotherfundsatJune30,2013consistedofthefollowing:

CountySchool SpecialEducation Non‐MajorService Pass‐Through Governmental ProprietaryFund Fund Funds Fund Total

CountySchoolServiceFund ‐$ 47,450,527$ 379,840$ 283,352$ 48,113,719$SpecialEducationPass‐ThroughFund 52,630,812 ‐ ‐ ‐ 52,630,812Non‐MajorGovernmentalFunds 1,005,705 ‐ 3,279 37 1,009,021ProprietaryFund 263,973 ‐ 197 ‐ 264,170

Total 53,900,490$ 47,450,527$ 383,316$ 283,389$ 102,017,722$

DueFromOtherFunds

The$52,630,812duetotheGeneralFundfromtheSpecialEducationPass‐ThroughFundisfortheexcessproperty taxes due from the County. The balance of $47,450,527 due to the Special Education Pass‐Through Fund from the General Fund is for the County's share of the excess property taxes due fromSantaClaraCounty.

31

SANTACLARACOUNTYOFFICEOFEDUCATIONNotestoFinancialStatementsJune30,2013

NOTE4‐INTERFUNDTRANSACTIONS(continued)

B. TransfersTo/FromOtherFundsTransfersto/fromotherfundsforthefiscalyearendedJune30,2013consistedofthefollowing:

CountySchool Non‐MajorService Governmental ProprietaryFund Funds Fund Total

CountySchoolServiceFund ‐$ 3,417,778$ 1,988,776$ 5,406,554$Non‐MajorGovernmentalFunds 148,376 ‐ ‐ 148,376

Total 148,376$ 3,417,778$ 1,988,776$ 5,554,930$

CountySchoolServiceFundtransfertoChildDevelopmentFundforreimbursementsfromtheHeadStartprogram 1,540,958$CountySchoolServiceFundtransfertoCafeteriaFundforcontributionsandindirectcosts 228,056CountySchoolServiceFundtransfertoCountySchoolFacilitiesFundforcontributionsfortheMcCollumProjectandaccruedinterest 482,364CountySchoolServiceFundtransfertoDebtServiceFundforcertificatesofparticipationpayment 1,166,400CountySchoolServiceFundtransfertoSelf‐InsuranceFundforcontributionsfordental,vision,andmedicalinsurance 1,988,776CafeteriaFundtransfertoCountySchoolServiceFundforprioryearcarryover 148,376

Total 5,554,930$

InterfundTransfersIn

NOTE5–FUNDBALANCESMinimumFundBalancePolicyTheCountyhasnotadoptedaformalminimumfundbalancepolicy,asrecommendedbyGASBStatementNo.54;however,theCountyfollowstheguidelinesrecommendedintheCriteriaandStandardsofAssemblyBill(AB)1200,whichrecommendaReserveforEconomicUncertaintiesconsistingofunassignedamountsequaltonolessthantwopercentoftotalGeneralFundexpendituresandotherfinancinguses.When an expenditure is incurred for purposes for which both restricted and unrestricted fund balance isavailable,theCountyconsidersrestrictedfundstohavebeenspentfirst.Whenanexpenditureisincurredforwhichcommitted,assigned,orunassignedfundbalancesareavailable,theCountyconsidersamountstohavebeenspentfirstoutofcommittedfunds,thenassignedfunds,andfinallyunassignedfunds,asneededunlessthegoverningboardhasprovidedotherwiseinitscommitmentorassignmentactions.

32

SANTACLARACOUNTYOFFICEOFEDUCATIONNotestoFinancialStatementsJune30,2013NOTE5–FUNDBALANCES(continued)

AtJune30,2013,fundbalancesoftheCounty’sgovernmentalfundsareclassifiedasfollows:

SpecialEducation Non‐Major

CountySchool Pass‐Through GovernmentalServiceFund Fund Funds Total

Nonspendable:Revolvingcash 25,000$ ‐$ ‐$ 25,000$Storesinventories 327,110 ‐ ‐ 327,110Prepaidexpenditures 2,309 ‐ ‐ 2,309

TotalNonspendable 354,419 ‐ ‐ 354,419Restricted:

Categoricalprograms 6,693,071 ‐ ‐ 6,693,071Specialeducation ‐ 5,329 ‐ 5,329Childdevelopmentprograms ‐ ‐ 288,616 288,616Schoolfacilities ‐ ‐ 3,890,972 3,890,972Debtservice ‐ ‐ 1,171,250 1,171,250Otherlocal 3,161,039 ‐ ‐ 3,161,039

TotalRestricted 9,854,110 5,329 5,350,838 15,210,277Assigned:

Excesstaxes 9,914,841 ‐ ‐ 9,914,841Districtloansforcashflowissues 5,000,000 ‐ ‐ 5,000,000Carryoverunspentfunds 2,243,797 ‐ ‐ 2,243,797Facilities 6,846,069 ‐ ‐ 6,846,069Redevelopmentfunds 332,126 ‐ ‐ 332,126Technologyservices 8,454,774 ‐ ‐ 8,454,774Deferredmaintenance(FMP) 5,789,404 ‐ ‐ 5,789,404Vacationliability 1,300,028 ‐ ‐ 1,300,028COPpayoff 2,000,000 ‐ ‐ 2,000,000SEIUone‐timenegotiatedagreements 1,359,852 ‐ ‐ 1,359,852

TotalAssigned 43,240,891 ‐ ‐ 43,240,891Unassigned:

Reserveforeconomicuncertainties 7,156,923 ‐ ‐ 7,156,923Remainingunassignedbalances 726,326 ‐ ‐ 726,326

TotalUnassigned 7,883,249 ‐ ‐ 7,883,249

Total 61,332,669$ 5,329$ 5,350,838$ 66,688,836$

33

SANTACLARACOUNTYOFFICEOFEDUCATIONNotestoFinancialStatementsJune30,2013NOTE6–CAPITALASSETSANDDEPRECIATIONCapitalassetactivityfortheyearendedJune30,2013wasasfollows:

Balance Balance,

July1,2012 Additions Deletions June30,2013Capitalassetsnotbeingdepreciated:

Land 5,533,399$ ‐$ ‐$ 5,533,399$Constructioninprogress 7,916,602 3,500,232 10,720,602 696,232

Totalcapitalassetsnotbeingdepreciated 13,450,001 3,500,232 10,720,602 6,229,631Capitalassetsbeingdepreciated:

Buildingsandimprovements 63,454,812 10,720,602 32,638 74,142,776Furnitureandequipment 12,071,648 340,449 137,653 12,274,444

Totalcapitalassetsbeingdepreciated 75,526,460 11,061,051 170,291 86,417,220Accumulateddepreciationfor:

Buildingsandimprovements (13,203,482) (2,371,747) (32,638) (15,542,591)Furnitureandequipment (8,076,112) (874,774) (122,404) (8,828,482)

Totalaccumulateddepreciation (21,279,594) (3,246,521) (155,042) (24,371,073)Totalcapitalassetsbeingdepreciated,net 54,246,866 7,814,530 15,249 62,046,147

Governmentalactivitycapitalassets,net 67,696,867$ 11,314,762$ 10,735,851$ 68,275,778$

Depreciationexpensewaschargedtogovernmentalfunctionsasfollows:

GovernmentalActivites:Instruction 1,542,730$Supervisionofinstruction 283,359Instructionallibrary,media,andtechnology 31,485Schoolsiteadministration 188,906Hometoschooltransportation 31,485Foodservices 31,485Allotherpupilservices 409,296Ancillaryservices 62,969Allothergeneraladministration 444,417Dataprocessingservices 94,453Plantservices 125,936

Total 3,246,521$

34

SANTACLARACOUNTYOFFICEOFEDUCATIONNotestoFinancialStatementsJune30,2013NOTE7–GENERALLONG‐TERMDEBTChangesinlong‐termdebtfortheyearendedJune30,2013wereasfollows:

Balance, Balance,July1,2012 July1,2012 Balance, AmountDue

asoriginallystated Restatments asrestated Additions Deductions June30,2013 WithinOneYearCertificatesofParticipation 11,040,000$ ‐$ 11,040,000$ ‐$ 640,000$ 10,400,000$ 670,000$CompensatedAbsences 5,017,719 (3,646,383) 1,371,336 ‐ 71,308 1,300,028 ‐OtherPostemploymentBenefits 6,734,775 ‐ 6,734,775 1,083,379 ‐ 7,818,154 ‐

Totals 22,792,494$ (3,646,383)$ 19,146,111$ 1,083,379$ 711,308$ 19,518,182$ 670,000$

PaymentsforcertificatesofparticipationaremadebytheCountySchoolServiceFund.Accumulatedvacationandotherpostemploymentbenefitswillbepaidforbythefundforwhichtheemployeeworked.

CertificatesofParticipationOnJuly1,2002theCountyissued$15,895,000ofcertificatesofparticipationthroughtheSantaClaraBoardofEducation Financing Corporation. The certificateswere issuedwith stated interest rates ranging between3.0% and 5.0%. The certificateswere issued to advance refund certificates thatwere originally issued in1995.AtJune30,2013theprincipalbalanceoutstandingwas$10,400,000.The annual requirements to amortize certificates of participation outstanding as of June 30, 2013 are asfollows:

FiscalYear Principal Interest Total