SANLAM 1 · 2019. 12. 10. · SANLAM 5 on the Statement of Financial Position as set on these...

56

Transcript of SANLAM 1 · 2019. 12. 10. · SANLAM 5 on the Statement of Financial Position as set on these...

SANLAM 1

ANNUAL FINANCIAL STATEMENTS 2018 2

Contents

Director’s report 2-4Statement of directors’ responsibilities 6Report of the independent auditors 7-9

Financial Statements

Statement of comprehensive income 10Statements of financial position 11Statement of changes in equity 12Statement of cash flows 13Notes to the financial statements 14-55

SANLAM 3

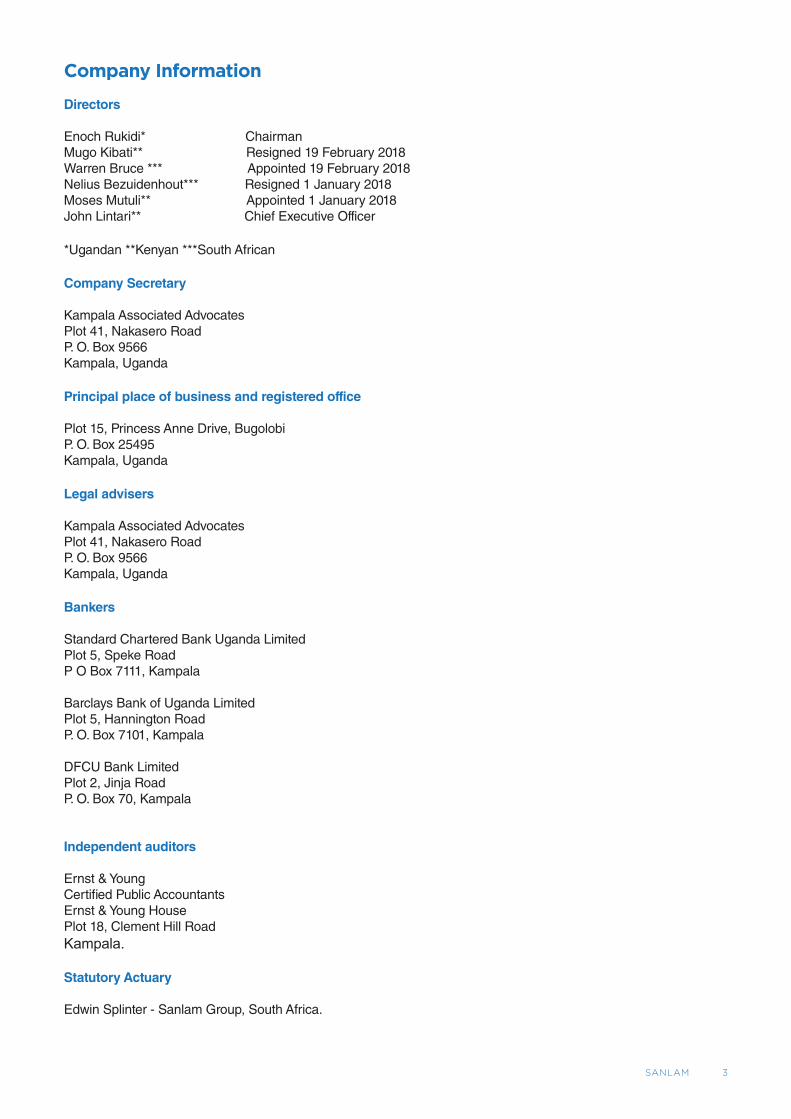

Company Information

Directors

Enoch Rukidi* Chairman Mugo Kibati** Resigned 19 February 2018 Warren Bruce *** Appointed 19 February 2018 Nelius Bezuidenhout*** Resigned 1 January 2018Moses Mutuli** Appointed 1 January 2018John Lintari** Chief Executive Officer *Ugandan **Kenyan ***South African

Company Secretary

Kampala Associated AdvocatesPlot 41, Nakasero RoadP. O. Box 9566Kampala, Uganda

Principal place of business and registered office

Plot 15, Princess Anne Drive, BugolobiP. O. Box 25495Kampala, Uganda

Legal advisers

Kampala Associated AdvocatesPlot 41, Nakasero RoadP. O. Box 9566 Kampala, Uganda

Bankers

Standard Chartered Bank Uganda LimitedPlot 5, Speke RoadP O Box 7111, Kampala

Barclays Bank of Uganda LimitedPlot 5, Hannington RoadP. O. Box 7101, Kampala

DFCU Bank LimitedPlot 2, Jinja RoadP. O. Box 70, Kampala

Independent auditors

Ernst & Young Certified Public AccountantsErnst & Young HousePlot 18, Clement Hill RoadKampala.

Statutory Actuary

Edwin Splinter - Sanlam Group, South Africa.

ANNUAL FINANCIAL STATEMENTS 2018 4

Directors’ Report

The Directors present their report together with the audited financial statements for the year ended 31 December 2018, which discloses the state of affairs of Sanlam Life Insurance (Uganda) Limited (“the company”).

Incorporation and principal activity

Sanlam Life Insurance (Uganda) Limited was incorporated on 03 November 2009 as a private limited liability company.

The principal activity of the company is to provide various classes of long term insurance business as defined in the Insurance Act (Cap 213) including the re-insurance of any such business. The company also obtained approval from the Insurance Regulatory Authority of Uganda to provide a medical product, Sancare Medical Insurance.

Results

The company reported a net profit of Ushs 882 million (2017: Ushs 554 million) which has been offset against the accumulated losses.

Dividends

The directors do not recommend the payment of a dividend in 2018 (2017: Nil).

Reserves

Contingency reserve

Under section 5 (b) of the Insurance Regulations, 2002, the company is required to annually credit an amount equal to 1 percent of premiums to contingency reserves.

An amount of Ushs 311 million (2017: Ushs 248 million) has been transferred to the contingency reserve to comply with Section 5 (b) of the Insurance Regulations, 2002.

Capital reserve

The Insurance laws and regulations require the company to transfer from its profits for the year, before any dividend is declared and after provision has been made for taxation, a sum of 5 percent of the profits to capital reserves to facilitate capital base growth.

An amount of Ushs 91.2 million (2017: Ushs 27.7 million) has been transferred to the capital reserve to comply with insurance laws and regulations.

Statutory requirements

Share capital

Under Section 37 of the Insurance Act, 2017, the Company is required to have a minimum paid up capital of Ushs. 3,000 million (Three billion Uganda shillings). This requirement has been met by the Company at 31 December 2018 and 31 December 2017.

Issued and paid up share capital

The issued and paid up share capital is Ushs 21,714 million (2017: 18,690 million) which is divided into 21,714 (2017: 18,690) ordinary shares of Ushs 1,000,000 each.

Statutory deposit

Security deposits with Bank of Uganda (the Central Bank)

Under the Ugandan Insurance laws and regulations, the Company is required to make and maintain a security deposit with the Bank of Uganda of at least 10% of the prescribed paid-up capital. The Company has fulfilled this requirement by making a deposit of Ushs 2,698 million (2017: Ushs 2,325 million) with the Bank of Uganda.

Financial risk management and objective

The Company’s activities expose it to a variety of financial risks, including underwriting risk, equity market prices, foreign currency exchange rates and interest rates. The Company’s overall risk management programme focuses on the identification and management of risks and seeks to minimize potential adverse effects on its financial performance and position.

The Company’s risk management policies include the use of underwriting guidelines and capacity limits, reinsurance planning, policy governing the acceptance of clients, and defined criteria for the approval of intermediaries and reinsurers. Investment policies are in place, which help manage liquidity, and seek to maximize return within an acceptable level of interest rate risk.

Related party transactions

Transactions with related parties during the year were in the normal course of business. Details of transactions and balances with related parties are included in note 22 to the financial statements.

Solvency

The Directors consider the Company’s solvency position

SANLAM 5

on the Statement of Financial Position as set on these financial statements to be satisfactory based on the fact that the Company’s solvency margin at 31 December 2018, and as at 31 December 2017, exceeded the minimum requirements of the Insurance Act, 2017.

Employee welfare

The Company’s employment terms are reviewed annually to ensure that they meet statutory and market conditions. The Company has a medical scheme that caters for medical needs of employees and their immediate dependents.

In order to improve the motivation of employees, the Company provides training and holds regular meetings with employees to elicit their views on the promotion of customer service and working conditions.

Directors

The directors who held office during the year up to the

date of this report are set out on page 1.

Auditors

In accordance with Section 108 of the Insurance Act, 2017, an insurance company’s auditors are required to rotate upon completion of audit for a continuous period of four years.

The auditors, Ernst & Young, who were appointed during the year, have expressed willingness to continue in office in accordance with section 167 (2) of the Companies Act, 2012 of Uganda and the Insurance Act, 2017.

By Order of the Board

Secretary

Date: ………….…………………2019

ugsl0061

Typewritten text

01st April

ANNUAL FINANCIAL STATEMENTS 2018 6

Statement of Directors’ Responsibilities

The Company’s directors are responsible for the preparation and fair presentation of these financial statements in accordance with International Financial Reporting Standards, the Companies Act of Uganda and, Ugandan Insurance Act and for such internal control as the directors determine is necessary to enable the preparation of financial statements that are free from material misstatement, whether due to fraud or error.

The director’s responsibilities include: designing implementing and maintaining internal control relevant to the preparation and fair presentation of these financial statements that are free from material misstatements whether due to fraud or error; selecting and applying appropriate accounting policies and making accounting estimates that are reasonable in the circumstances. They are also responsible for safe guarding the assets of the company.

Under the Companies Act of Uganda, the directors are required to prepare financial statements for each year that give a true and fair view of the state of affairs of the Company as at the end of the financial year and of the operating results of the Company for that year. It also requires the directors to ensure the Company keeps proper accounting records that disclose with reasonable accuracy the financial position of the Company. The directors accept responsibility for the financial statements, which have been prepared using appropriate accounting policies supported by reasonable and prudent judgments and estimates, in conformity with International Financial Reporting Standards, Ugandan Companies Act and Ugandan Insurance Act. The directors are of the

opinion that the financial statements give a true and fair view of the state of the financial affairs and the profit for the year ended 31 December 2018. The directors further accept responsibility for the maintenance of accounting records that may be relied upon in the preparation of financial statements, as well as adequate systems of internal financial control.

The directors have made an assessment of the Company’s ability to continue as a going concern and have no reason to believe the business will not be a going concern for the next twelve months from the date of this statement.

Approval of the Financial Statements

The financial statements, as indicated above, were approved by the Board of directors on …………..…….2019 and were signed on its behalf by:

ugsl0061

Typewritten text

01st April

SANLAM 7

Report of the Independent Auditors to the members of Sanlam Life Insurance Uganda Limited

Report on the audit of the financial statements

Opinion

We have audited the financial statements of Sanlam Life Insurance Uganda Limited (“the Company”) set out on pages 11 to 75, which comprise the statement of financial position as at 31 December 2018, and the statement of comprehensive income, statement of changes in equity and statement of cash flows for the year then ended, and notes to the financial statements, including a summary of significant accounting policies and other explanatory information.

In our opinion the accompanying financial statements present fairly in all material respects, the financial position of Sanlam Life Insurance Uganda Limited as at 31 December 2018 and of its financial performance and its cash flows for the year then ended in accordance with International Financial Reporting Standards (IFRS), the Ugandan Companies Act and the Ugandan Insurance Act.

Basis of Opinion

We conducted our audit in accordance with International Standards on Auditing (ISAs). Our responsibilities under those standards are further described in the Auditors’ Responsibilities for the Audit of the Financial Statements section of our report. We are independent of the Company in accordance with the International Federation of Accountants’ Code of Ethics for Professional Accountants

(IFAC code) and other independence requirements applicable to performing audits of Sanlam Life Insurance Uganda Limited. We have fulfilled our other ethical responsibilities in accordance with the IFAC Code, and in accordance with other ethical requirements applicable to performing the audit of Sanlam Life Insurance Uganda Limited. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our opinion.

Key Audit Matters

Key audit matters are those matters that, in our professional judgement, were of most significance in our audit of the financial statements of the current period. These matters were addressed in the context of our audit of the financial statements as a whole, and in forming our opinion thereon, and we do not provide a separate opinion on these matters. For each matter below, our description of how our audit addressed the matter is provided in that context.

We have fulfilled the responsibilities described in the Auditor’s Responsibilities for the Audit of the Financial Statements section of our report, including in relation to these matters. Accordingly, our audit included the performance of procedures designed to respond to our assessment of the risks of material misstatement of the financial statements. The results of our audit procedures, including the procedures performed to address the matters below, provide the basis for our audit opinion on the accompanying financial statements.

ANNUAL FINANCIAL STATEMENTS 2018 8

Key Audit Matter How the matter was addressed in the audit

Insurance contract liabilities

As stated in note 27, Insurance Contract Liabilities amounted to Ushs 14.4 billion. The life business policy liabilities and income recognition for the period is determined by actuarial valuations which are done by the Company’s designated actuarial expert.

The determination of insurance contract liabilities requires significant judgment in the determination of policyholders’ benefits that represent the estimated future benefit liability for traditional life insurance policies and include the value of accumulated declared bonuses or interest that have vested to the policy holders.

The reserves for life benefits for participating traditional life insurance policies are calculated using a gross level premium valuation method.

The calculation of reserves depends on the type of profit participation and is based on actuarial assumptions, such as guaranteed mortality benefits, interest rates, persistency, expenses and investment return, plus a margin for adverse deviations.

We reviewed the procedures/accounting policies around recognition of insurance contract liabilities and the application thereof to check that these are in compliance with IFRS.

We tested the models used in developing these balances, reviewing management’s assumptions in light of current market conditions, industry developments and policyholder behavior, and obtaining comfort over the completeness and accuracy of underlying data used in the calculations. We examined the biometric assumptions, such as mortality and disability and additional assumptions, such as investment return in light of the current market environment, the expected development within the industry as well, as the behavior of insurers.

The future life policyholder benefits are calculated using a discount rate. We have reviewed significant assumption changes made during the year with a focus on the interest rate used in the traditional life insurance policies. In assessing the interest rate used, we confirmed that the interest rates are supported by the anticipated economic performance of the assets backing the liability when considering any planned changes in asset strategy and reinvestment. In particular, we assessed the different components of the discount rate on a portfolio level (“individual life” and “group life”).

We verified the consistency of the assumptions made by management with assumptions made elsewhere (for example in the determination of the market consistent embedded value (MCEV), and

We reviewed the methodology for determining the selected discount rate, based on the above input parameters.

Other information

The directors are responsible for the other information. The other information comprises the information included in the Annual Report and Financial Statements, but does not include the financial statements and our auditors’ report thereon.

Our opinion on the financial statements does not cover the other information and we do not express any form of assurance conclusion thereon.

In connection with our audit of the financial statements, our responsibility is to read the other information and, in doing so, consider whether the other information is materially inconsistent with the financial statements or our knowledge obtained in the audit, or otherwise appears to be materially misstated. If, based on the work we have performed, we conclude that there is a material misstatement of this information, we are required to report that fact. We have nothing to report in this regard.

Directors’ responsibilities for the financial statements

The directors are responsible for the preparation and fair presentation of the financial statements in accordance with International Financial Reporting Standards and the requirements of the Companies Act of Uganda, 2012 and the Insurance Act, 2017, and for such internal control as the directors determine is necessary to enable the preparation of financial statements that are free from material misstatement, whether due to fraud or error.

In preparing the financial statements, the directors are responsible for assessing the Company’s ability to continue as a going concern, disclosing, as applicable, matters related to going concern and using the going concern basis of accounting unless the directors either intend to liquidate the company or to cease operations, or have no realistic alternative but to do so. The directors are responsible for overseeing the Company’s financial reporting processes.

SANLAM 9

Auditor’s Responsibilities for the audit of the financial statements

Our objectives are to obtain reasonable assurance about whether the financial statements as a whole are free from material misstatement, whether due to fraud or error, and to issue an auditor’s report that includes our opinion. Reasonable assurance is a high level of assurance, but is not a guarantee that an audit conducted in accordance with ISAs will always detect a material misstatement when it exists. Misstatements can arise from fraud or error and are considered material if, individually or in the aggregate, they could reasonably be expected to influence the economic decisions of users taken on the basis of these financial statements. As part of an audit in accordance with ISAs, we exercise professional judgement and maintain professional scepticism throughout the audit. We also:

• Identify and assess the risks of material misstatement of the financial statements, whether due to fraud or error, design and perform audit procedures responsive to those risks, and obtain audit evidence that is sufficient and appropriate to provide a basis for our opinion. The risk of not detecting a material misstatement resulting from fraud is higher than for one resulting from error, as fraud may involve collusion, forgery, intentional omissions, misrepresentations, or the override of internal control.

• Obtain an understanding of internal control relevant to the audit in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Company’s internal control.

• Evaluate the appropriateness of accounting policies used and the reasonableness of accounting estimates and related disclosures made by the directors.

• Conclude on the appropriateness of the directors’ use of the going concern basis of accounting and based on the audit evidence obtained, whether a material uncertainty exists related to events or conditions that may cast significant doubt on the Company’s ability to continue as a going concern. If we conclude that a material uncertainty exists, we are required to draw attention in our auditor’s report to the related disclosures in the financial statements or, if such disclosures are inadequate, to modify our opinion. Our conclusions are based on the audit evidence obtained up to the date of our auditor’s report. However, future events or conditions may cause the Company to cease to continue as a going concern.

• Evaluate the overall presentation, structure and content of the financial statements, including the disclosures, and whether the financial statements represent the underlying transactions and events in a manner that achieves fair presentation.

We communicate with the directors regarding, among other matters, the planned scope and timing of the audit and significant audit findings, including any significant deficiencies in internal control that we identify during our audit.

We also provide the directors with a statement that we have complied with relevant ethical requirements regarding independence, and to communicate with them all relationships and other matters that may reasonably be thought to bear on our independence, and where applicable, related safeguards.

From the matters communicated with the directors, we determine those matters that were of most significance in the audit of the financial statements of the current year and are therefore the key audit matters. We describe these matters in our auditor’s report unless law or regulation precludes public disclosure about the matter or when, in extremely rare circumstances, we determine that a matter should not be communicated in our report because the adverse consequences of doing so would reasonably be expected to outweigh the public interest benefits of such communication.

Report on other legal requirements

As required by the Companies Act of Uganda, 2012, we report to you based on our audit, that:

i. We have obtained all the information and explanations which to the best of our knowledge and belief were necessary for the purposes of our audit;

ii. In our opinion, proper books of account have been kept by the Company so far as appears from our examination of those books; and

iii. The Bank’s statement of financial position and statement of comprehensive income are in agreement with the books of account

The engagement Partner on the audit resulting in this independent auditor’s report is CPA Michael Kimoni – P0248.

Date.........................................2019

Young Certified Public Accountants of Uganda Kampala, Uganda

……………………......... Ernst &

ugsl0061

Typewritten text

01st April

ANNUAL FINANCIAL STATEMENTS 2018 10

Statement of comprehensive income

for the year ended 31 December 2018

2018 2017

Notes Ushs ‘000 Ushs ‘000

Gross written premiums 4 35,185,474 24,803,785

Reinsurance gross premium ceded 4 (6,769,196) (323,265)

Net change in provision for unearned premium - Sancare (293,012) (689,293)

Net written premiums 28,123,266 23,791,227

Interest income using the EIR 5(a) 3,086,278 1,753,916

Other investment income 5(b) 194,557 108,347

Commission income 253,045 171,312

Other operating income 6 265,168 298,189

Fair value movement on quoted shares and unquoted shares 19 & 21 81,561 55,149

Net fair value losses on debt instruments at fair value through profit or loss (277,917) -

Other income 3,602,692 2,386,913

Total income 31,725,958 26,178,140

Claims incurred and policy holders’ benefits 7 (10,322,931) (10,654,750)

Claims ceded to reinsurers 2,488,196 273,820

Net change in insurance contract liabilities 8 (5,329,137) (1,671,241)

Net claims incurred (13,163,872) (12,052,171)

Finance Costs 9 - (68,176)

Expected credit losses on financial instruments 10(a) 20,347 -

Operating and administrative expenses 10(b) (12,914,102) (9,027,465)

Commissions expense (4,248,202) (4,439,191)

Total expenses (17,141,957) (13,534,832)

Total benefits, claims and other expenses (30,305,829) (25,587,003)

Profit before tax 1,420,129 591,137

Income tax charge 12(a) (538,251) (37,272)

Net profit for the year 881,878 553,865

Total comprehensive income 881,878 553,865

SANLAM 11

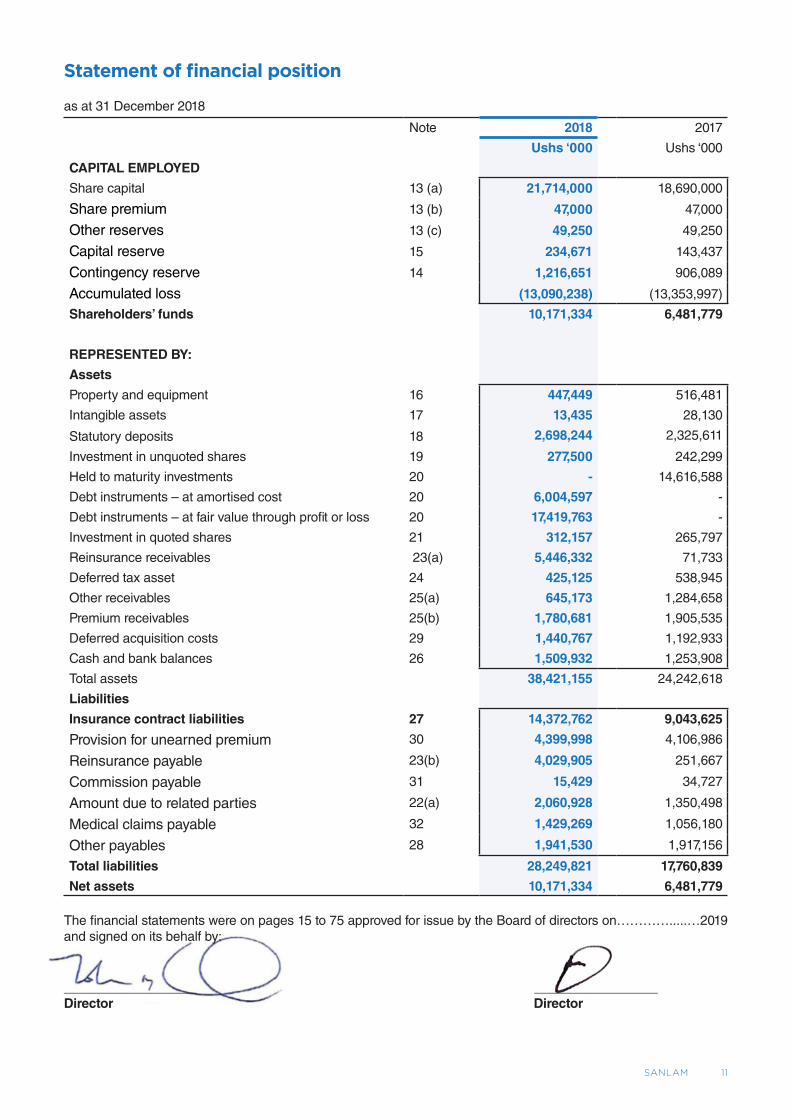

Statement of financial position

as at 31 December 2018

Note 2018 2017

Ushs ‘000 Ushs ‘000

CAPITAL EMPLOYED

Share capital 13 (a) 21,714,000 18,690,000

Share premium 13 (b) 47,000 47,000

Other reserves 13 (c) 49,250 49,250

Capital reserve 15 234,671 143,437

Contingency reserve 14 1,216,651 906,089

Accumulated loss (13,090,238) (13,353,997)

Shareholders’ funds 10,171,334 6,481,779

REPRESENTED BY:

Assets

Property and equipment 16 447,449 516,481

Intangible assets 17 13,435 28,130

Statutory deposits 18 2,698,244 2,325,611

Investment in unquoted shares 19 277,500 242,299

Held to maturity investments 20 - 14,616,588

Debt instruments – at amortised cost 20 6,004,597 -

Debt instruments – at fair value through profit or loss 20 17,419,763 -

Investment in quoted shares 21 312,157 265,797

Reinsurance receivables 23(a) 5,446,332 71,733

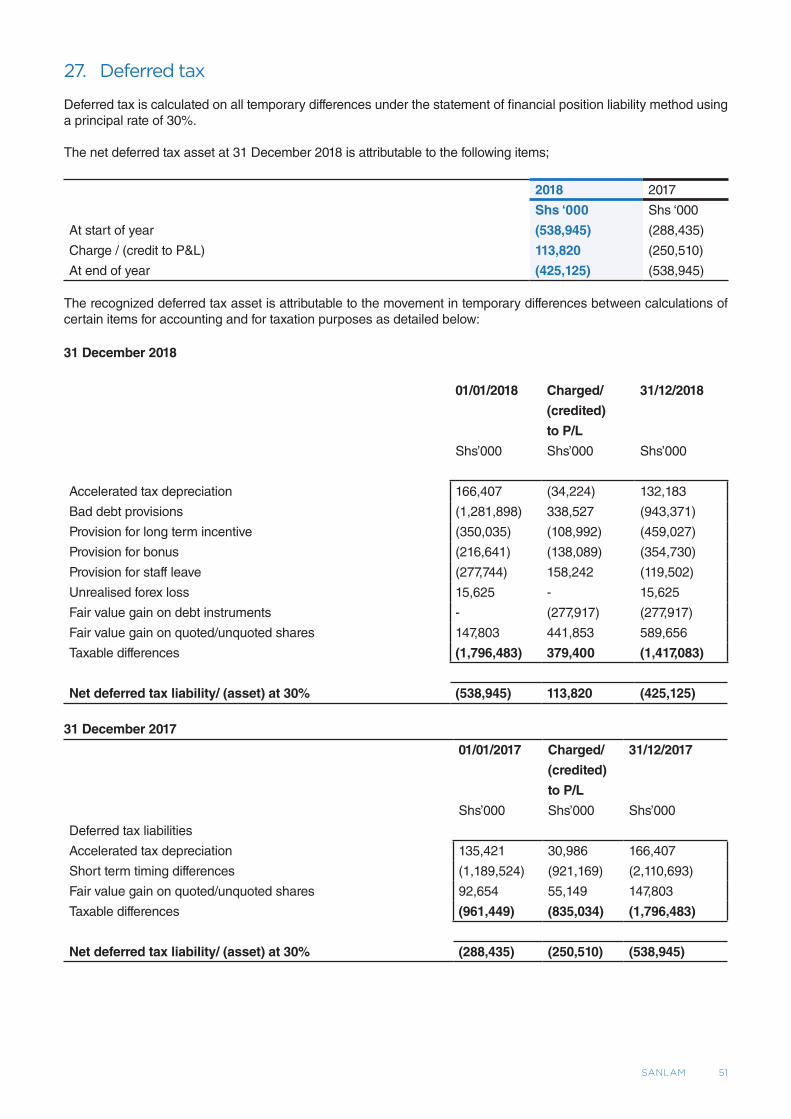

Deferred tax asset 24 425,125 538,945

Other receivables 25(a) 645,173 1,284,658

Premium receivables 25(b) 1,780,681 1,905,535

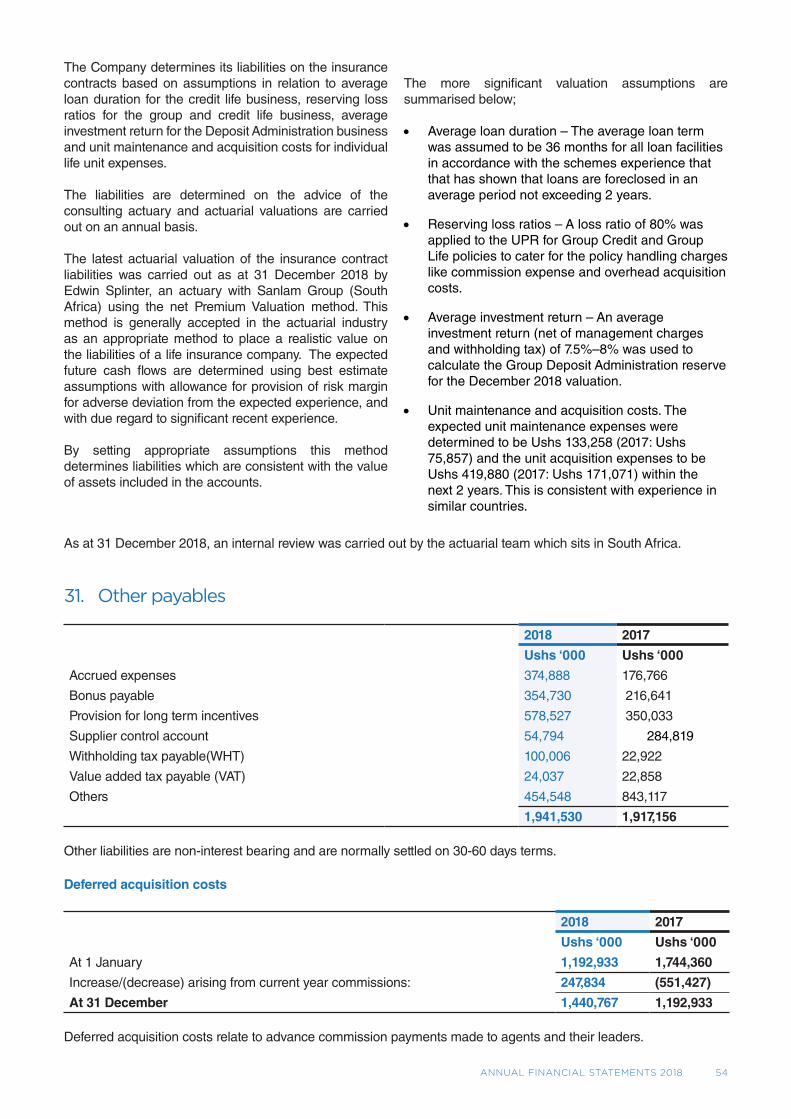

Deferred acquisition costs 29 1,440,767 1,192,933

Cash and bank balances 26 1,509,932 1,253,908

Total assets 38,421,155 24,242,618

Liabilities

Insurance contract liabilities 27 14,372,762 9,043,625

Provision for unearned premium 30 4,399,998 4,106,986

Reinsurance payable 23(b) 4,029,905 251,667

Commission payable 31 15,429 34,727

Amount due to related parties 22(a) 2,060,928 1,350,498

Medical claims payable 32 1,429,269 1,056,180

Other payables 28 1,941,530 1,917,156

Total liabilities 28,249,821 17,760,839

Net assets 10,171,334 6,481,779

The financial statements were on pages 15 to 75 approved for issue by the Board of directors on………….....…2019 and signed on its behalf by:

__________________ _________________Director Director

ANNUAL FINANCIAL STATEMENTS 2018 12

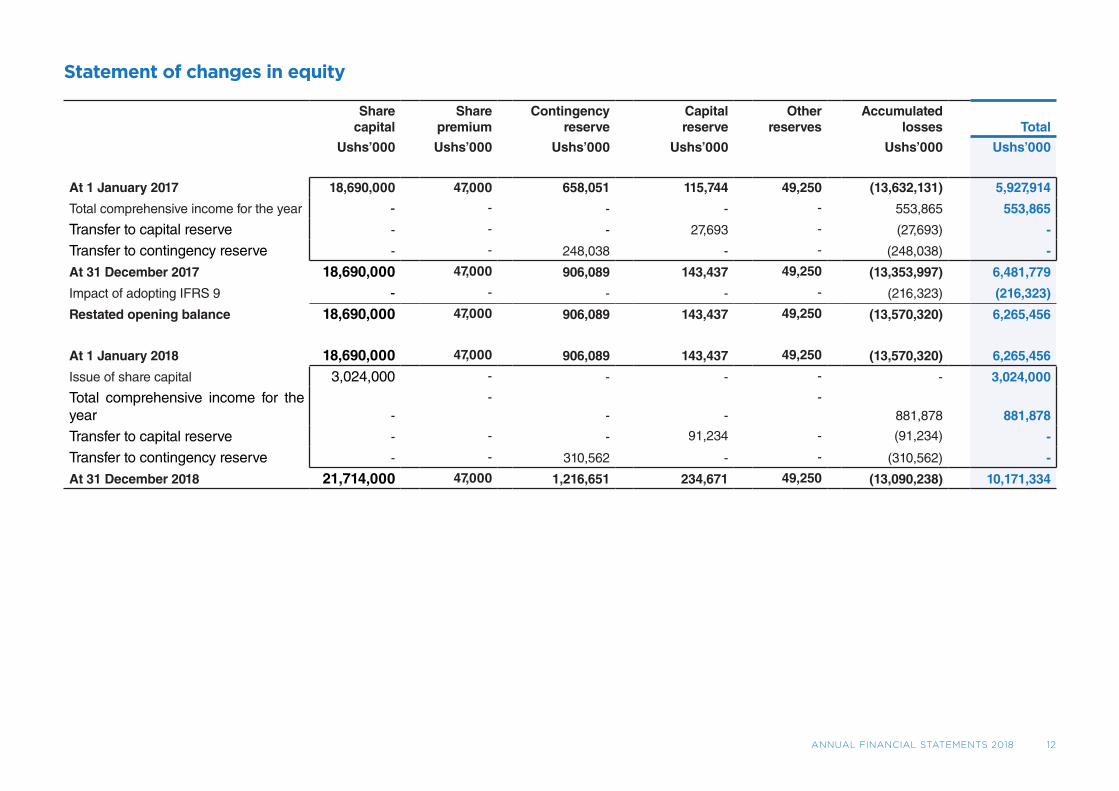

Statement of changes in equity

Share capital

Share premium

Contingency reserve

Capital reserve

Other reserves

Accumulated losses Total

Ushs’000 Ushs’000 Ushs’000 Ushs’000 Ushs’000 Ushs’000

At 1 January 2017 18,690,000 47,000 658,051 115,744 49,250 (13,632,131) 5,927,914

Total comprehensive income for the year - - - - - 553,865 553,865

Transfer to capital reserve - - - 27,693 - (27,693) -

Transfer to contingency reserve - - 248,038 - - (248,038) -

At 31 December 2017 18,690,000 47,000 906,089 143,437 49,250 (13,353,997) 6,481,779

Impact of adopting IFRS 9 - - - - - (216,323) (216,323)

Restated opening balance 18,690,000 47,000 906,089 143,437 49,250 (13,570,320) 6,265,456

At 1 January 2018 18,690,000 47,000 906,089 143,437 49,250 (13,570,320) 6,265,456

Issue of share capital 3,024,000 - - - - - 3,024,000

Total comprehensive income for the year -

-- -

-881,878 881,878

Transfer to capital reserve - - - 91,234 - (91,234) -

Transfer to contingency reserve - - 310,562 - - (310,562) -

At 31 December 2018 21,714,000 47,000 1,216,651 234,671 49,250 (13,090,238) 10,171,334

SANLAM 13

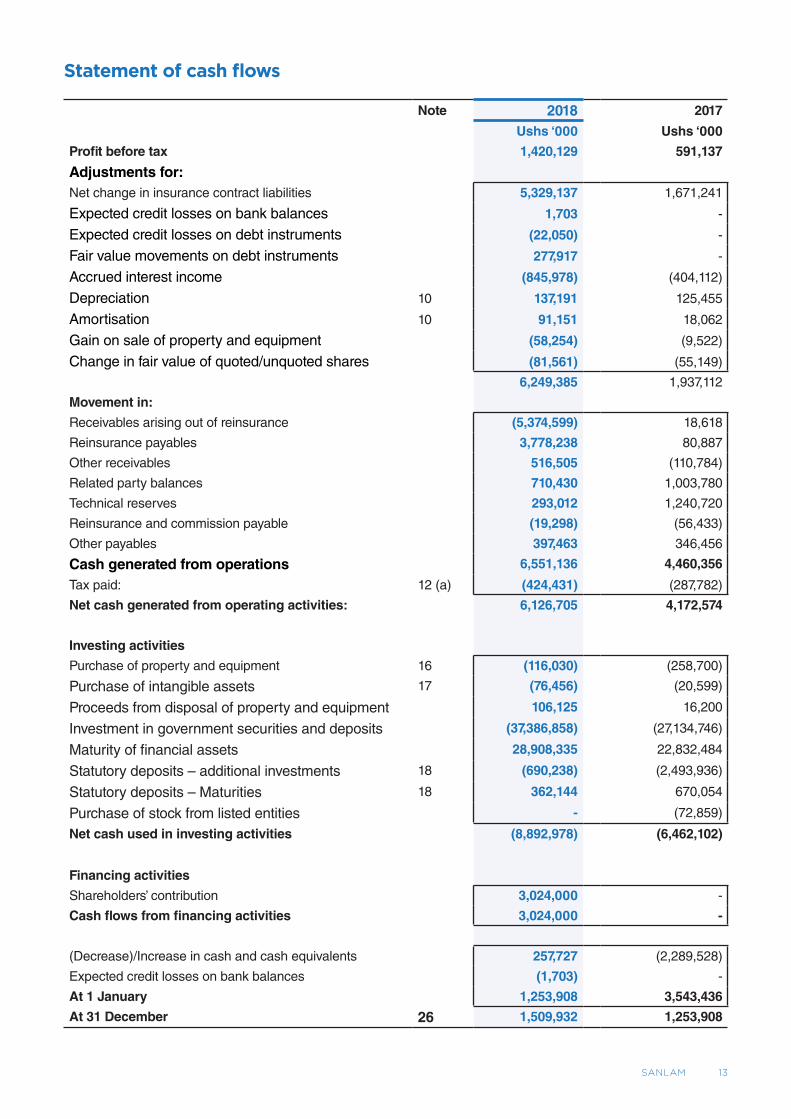

Statement of cash flows

Note 2018 2017

Ushs ‘000 Ushs ‘000

Profit before tax 1,420,129 591,137

Adjustments for:Net change in insurance contract liabilities 5,329,137 1,671,241

Expected credit losses on bank balances 1,703 -

Expected credit losses on debt instruments (22,050) -

Fair value movements on debt instruments 277,917 -

Accrued interest income (845,978) (404,112)

Depreciation 10 137,191 125,455

Amortisation 10 91,151 18,062

Gain on sale of property and equipment (58,254) (9,522)

Change in fair value of quoted/unquoted shares (81,561) (55,149)

6,249,385 1,937,112

Movement in:

Receivables arising out of reinsurance (5,374,599) 18,618

Reinsurance payables 3,778,238 80,887

Other receivables 516,505 (110,784)

Related party balances 710,430 1,003,780

Technical reserves 293,012 1,240,720

Reinsurance and commission payable (19,298) (56,433)

Other payables 397,463 346,456

Cash generated from operations 6,551,136 4,460,356

Tax paid: 12 (a) (424,431) (287,782)

Net cash generated from operating activities: 6,126,705 4,172,574

Investing activities

Purchase of property and equipment 16 (116,030) (258,700)

Purchase of intangible assets 17 (76,456) (20,599)

Proceeds from disposal of property and equipment 106,125 16,200

Investment in government securities and deposits (37,386,858) (27,134,746)

Maturity of financial assets 28,908,335 22,832,484

Statutory deposits – additional investments 18 (690,238) (2,493,936)

Statutory deposits – Maturities 18 362,144 670,054

Purchase of stock from listed entities - (72,859)

Net cash used in investing activities (8,892,978) (6,462,102)

Financing activities

Shareholders’ contribution 3,024,000 -

Cash flows from financing activities 3,024,000 -

(Decrease)/Increase in cash and cash equivalents 257,727 (2,289,528)

Expected credit losses on bank balances (1,703) -

At 1 January 1,253,908 3,543,436

At 31 December 26 1,509,932 1,253,908

ANNUAL FINANCIAL STATEMENTS 2018 14

Notes to Financials

1. Reporting entity

Sanlam Life Insurance (Uganda) Limited is a limited liability company incorporated under the Companies Act of Uganda and domiciled in Uganda. The principal activity of the company is to carry on any class of long term insurance business and to provide a medical insurance product, as defined in the Insurance Act, 2007 including the re-insurance of any such business. The Company is also licensed to provide a medical product, Sancare Medical Insurance.

2. Basis of preparation

The financial statements are prepared in accordance with and comply with International Financial Reporting Standards. Except for policy holder investments, investments in quoted and unquoted shares measured at fair value through profit or loss (FVTPL), the financial statements are prepared under the historical cost convention, as modified by the carrying of impaired assets at their recoverable amounts, and actuarially determined liabilities at their present value. The financial statements are presented in Uganda Shillings (Ushs), rounded to the nearest thousand.

The preparation of financial statements in conformity with generally accepted accounting principles requires the use of estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. Although these estimates are based on the directors’ best knowledge of current events and actions, actual results ultimately may differ from those estimates. The areas involving a higher degree of judgment or complexity, or where assumptions and estimates are significant to the financial statements, are disclosed in Note 3.3

3. Summary of significant accounting policies

The principal accounting policies adopted in the preparation of these financial statements are set out below. These policies have been consistently applied to all years presented, unless otherwise stated;

» Classification of contracts

A contract is classified as insurance where the company accepts significant insurance risk by agreeing with the policyholder to pay benefits if a specified uncertain

future event (the insured event) adversely affects the policyholder or other beneficiary. Significant insurance risk exists where it is expected that for the duration of the policy or part thereof, policy benefits payable on the occurrence of the insured event will significantly exceed the amount payable on early termination, before allowance for expense deductions at early termination. Once a contract has been classified as an insurance contract, the classification remains unchanged for the remainder of its lifetime, even if the insurance risk reduces significantly during this period.

» Life insurance contract liabilities

Life insurance liabilities are recognized when contracts are entered into and premiums are charged. These liabilities are measured by using the gross premium method. The liability is determined as the sum of the discounted value of the expected future benefits, claims handling and policy administration expenses, policyholder options and guarantees and investment income from assets backing such liabilities, which are directly related to the contract, less the discounted value of the expected premiums that would be required to meet the future cash outflows based on the valuation assumptions used. The liability is either based on current assumptions or calculated using the assumptions established at the time the contract was issued, in which case, a margin for risk and adverse deviation is generally included. A separate reserve for longevity may be established and included in the measurement of the liability. Furthermore, the liability for life insurance contracts comprises the provision for unearned premiums and premium deficiency, as well as for claims outstanding, which includes an estimate of the incurred claims that have not yet been reported to the company.

In line with IFRS 4, the company assesses the adequacy of the recognised insurance contract liabilities using current estimates of future cash flows. If the assessment shows that the carrying amount of the insurance contract liabilities is inadequate in the light of related future cash flows, the entire deficiency is recognised in profit or loss.

The insurance contract provisions are valued using realistic expectations of future experience, with margins for prudence and deferral of profit emergence. The provision, estimation techniques and assumptions are periodically reviewed, with changes in estimates reflected in the profit or loss as they occur. Whilst the Directors consider that the insurance contract provisions and the related reinsurance recovery are fairly stated on the basis of the information currently available to them, the ultimate liability will vary as a result of subsequent information and events and may result in significant adjustments to the amount provided.The insurance contract liabilities are determined through an actuarial valuation done on an annual basis.

SANLAM 15

Group credit liabilities

For personal loans, unearned premium reserve (UPR) is calculated as a reducing balance of the single premium received over the term of the loan. A loss ratio of 80% (2017: 80%) is then applied to the UPR. An Incurred But Not Reported (IBNR) reserve equivalent to one month of earned premium is also maintained.

Group life liabilities

This is annually renewable business with cover restricted to the period covered by premiums.For this business, the company holds an Unearned Premium Reserve (UPR), which represents the element of premiums already received where cover has not yet been provided. A loss ratio of 80% (2017: 80%) is then applied to the UPR.

Individual life liabilities

Two reserves are considered for this valuation, the unit reserve and the shillings reserve (or non-unitized reserve). The unit reserve is the reserve held in respect of the investment account component for the investment products. It represents the total value of investment funds held in respect of policyholders and is calculated as the number of units times the unit price as at the valuation date. For the shillings reserve (or non-unitized reserve), all policies are valued on a policy-by-policy Financial Soundness Valuation (FSV) method. The shilling reserves is calculated by subtracting the present value of the future projected income to the company (predominantly premiums and investment income) from the present value of the future projected outflow of the company (predominantly claims and expenses). The estimates of projected income and outflows are based on a set of realistic assumptions (best estimate assumptions) with an added margin for prudence. In addition, the statutory actuary may choose to strengthen these margins by applying an additional layer of what is known as discretionary margins. Thus, the valuation basis results in a larger reserve than would be required on a true best estimate basis. The degree of conservatism in the results depends on the extent of the discretionary margins.

Group Deposit Administration Liabilities

The Deposit Administration business was introduced in 2015. This is a with-profit arrangement where Sanlam Uganda is responsible for collecting contributions; investing them appropriately and managing the individual member accounts. Interest added to each account in the first three years from the date of joining the scheme is guaranteed to be 7.5% to 8% per annum. The reserve is calculated as the build-up of actual member contributions at a prudent rate of investment return, less charges and claims. An average investment return (net of management charges and withholding tax) of 8.5% (2017: 9.0%) was used to calculate the reserve for the December 2018 valuation.

Medical

Medical insurance contract liabilities include the outstanding claims provision, the provision for unearned premium and the provision for premium deficiency. The outstanding claims provision is based on the estimated ultimate cost of all claims incurred but not settled at the reporting date, whether reported or not, together with related claims handling costs and reduction for the expected value of salvage and other recoveries. The cost of outstanding claims is estimated by using a range of standard actuarial claims projection techniques. The main assumption underlying these techniques is the company’s past claims development experience.

The provision for unearned premiums represents that portion of premiums received or receivable that relates to risks that have not yet expired at the reporting date. The portion of premiums received on in-force contracts that relates to unexpired risks at the statement of financial position date is reported as an unearned premium liability.

Adjustments to the liabilities at each reporting date are recorded in the statement of comprehensive income in ‘gross change in contract liabilities’. The liability is derecognised when the contract expires, is discharged or is cancelled. Refer to Note 27 for the actuarial findings. When the present value of expected future cash flows, results in an asset, the asset is recognized on the statement of financial position.

» Reinsurance

The company cedes insurance risk in the normal course of business. Outward reinsurance premiums are accounted for in the same period as the related premiums for the direct or inwards reinsurance business being reinsured. Reinsurance liabilities comprise premiums payable for outwards reinsurance contracts. Reinsurance assets include balances due from reinsurance companies relating to the portion of the insurance liability that is recoverable from the reinsurer. Reinsurance assets are measured in accordance with the terms of the reinsurance contract.

Gains or losses on buying reinsurance are recognised in the statement of comprehensive income immediately at the date of purchase and are not amortised.

Ceded reinsurance arrangements do not relieve the company from its obligations to policyholders.Reinsurance liabilities represent balances due to reinsurance companies. Amounts payable are estimated in a manner consistent with the related reinsurance contract.Claims are presented on a gross basis for ceded reinsurance.

Reinsurance liabilities are derecognised when the contractual rights are extinguished or expire or when the contract is transferred to another party.

ANNUAL FINANCIAL STATEMENTS 2018 16

» Revenue recognition

Premium income

Gross premiums

Gross recurring premiums on life are recognised as revenue when payable by the policyholder. For single premium business, revenue is recognised on the date on which the policy is effective. Monthly premiums in respect of certain products are accounted for in accordance with the terms of their policy contracts. Cover only commences when premiums are received.

For medical insurance, written premiums comprise the total premiums receivable for the whole period of cover provided by contracts entered into during the accounting period. They are recognised on the date on which the policy commences, and adjusted for, by recognition of the unearned premium reserve (UPR).

Unearned premiums are those proportions of premiums written in a year that relate to periods of risk after the reporting date. The unearned portion of accrued premiums is included within long-term policy liabilities.

Reinsurance premiums

Gross reinsurance premiums on life contracts are recognised as an expense on the earlier of the date when premiums are payable or when the policy becomes effective.

Investment income

Interest income (including income on DAP funds) is recognised in the statement of comprehensive income as it accrues and is calculated by using the effective interest rate method. Fees and commissions that are an integral part of the effective yield of the financial asset or liability are recognised as an adjustment to the effective interest rate of the instrument. Dividend income is recognised in the statement of comprehensive income when authorised by the counterparty, and the Company has an unconditional right to receipt of the amount due.

» Benefits, claims and expenses recognition

Gross benefits and claims for life insurance contracts include the cost of all claims arising during the year, including internal and external claims handling costs that are directly related to the processing and settlement of claims.

Death claims and surrenders are recorded on the basis of notifications received. Maturities and annuity payments are recorded when due.

Medical claims include all claims occurring during the year, whether reported or not, related internal and

external claims handling costs that are directly related to the processing and settlement of claims.

» Share capital

Share capital is classified as equity where the company has no obligation to deliver cash or other assets to shareholders.

» Property and equipment

Property and equipment is stated at cost, excluding the costs of day-today servicing, less accumulated depreciation and accumulated impairment losses.

Depreciation is provided for on a straight-line basis over the useful lives of the following classes of assets:

Computer equipment 33%

Furniture, fittings and other equipment 10%

Motor vehicles 25%

Leasehold improvements 10%

The assets’ residual values, and useful lives and method of depreciation are reviewed at each financial year end and adjusted prospectively, if appropriate.Impairment reviews are performed when there are indicators that the carrying value may not be recoverable. Impairment losses are recognised in the statement of comprehensive income as an expense.An item of property and equipment is derecognised upon disposal or when no further future economic benefits are expected from its use or disposal. Any gain or loss arising on derecognition of the asset (calculated as the difference between the net disposal proceeds and the carrying amount of the asset) is included in the statement of comprehensive income in the year the asset is derecognised.

» Financial assets

Initial recognition and measurement

On 1 January 2018, the Company adopted IFRS 9 financial instruments using the modified retrospective method of adoption. The cumulative effect of initially adopting IFRS 9 is recognised as an adjustment to the opening balance of retained earnings. Therefore, the comparative information has not been restated and continues to be reported under IAS 39 as follows:Financial assets within the scope of IAS 39 are classified as financial assets at fair value through profit or loss, loans and receivables, held-to-maturity investments, or as derivatives designated as hedging instruments in an effective hedge, as appropriate. The company determines the classification of its financial assets at initial recognition. All financial assets are recognised initially at fair value plus transaction costs, except in the case of financial assets recorded at fair value through profit or loss.

SANLAM 17

Purchases or sales of financial assets that require delivery of assets within a time frame established by regulation or convention in the market place (regular way trades) are i.e., the date that the company commits to purchase or sell the asset.

Subsequent measurement

The subsequent measurement of financial assets depends on their classification as follows:

i. Financial assets at fair value through profit or loss

Financial assets at fair value through profit or loss include financial assets designated upon initial recognition at fair value through profit or loss. Financial assets at fair value through profit or loss are carried in the statement of financial position at fair value with net changes in fair value presented as losses (negative net changes in fair value) or gains (positive net changes in fair value) in the statement of comprehensive income. Financial assets designated upon initial recognition at fair value through profit or loss are designated at their initial recognition date and only if the criteria under IAS 39 are satisfied.

ii. Held-to-maturity investments

Non-derivative financial assets with fixed or determinable payments and fixed maturities are classified as held to maturity when the company has the positive intention and ability to hold them to maturity. After initial measurement, held to maturity investments are measured at amortised cost using the effective interest rate, less impairment. Amortised cost is calculated by taking into account any discount or premium on acquisition and fees or costs that are an integral part of the effective interest rate. The effective interest rate amortisation is included as finance income in the statement of comprehensive income. The losses arising from impairment are recognised in the statement of comprehensive income in finance costs. On adoption of IFRS 9, these instruments are now classified at amortised cost, as disclosed later.

iii. Other assets and amounts due from related parties

The above financial assets are financial assets with fixed or determinable payments and fixed maturities that are not quoted in an active market. They are not entered into with the intention of immediate or short-term resale and are not classified as ‘Financial assets held for trading’, designated as ‘financial Investments-available for sale’ or ‘financial assets designated at fair value through profit or loss’. After initial measurement, these financial assets are subsequently measured at amortised cost, using the effective interest rate method, less allowance for impairment. On adoption of IFRS 9, these instruments are now classified at amortised cost. Amortisation is calculated by taking into account any discount or premium on acquisition fees and costs that are an integral part of the effective interest rate. The amortization is included

in the statement of comprehensive income. The losses arising from impairment are included in the statement of comprehensive income.

Derecognition of financial assets

A financial asset (or, where applicable a part of a financial asset or part of a group of similar financial assets) is derecognised when:

The rights to receive cash flows from the asset have expired; andThe company has transferred its rights to receive cash flows from the asset or has assumed an obligation to pay the received cash flows in full without material delay to a third party under a ‘pass-through’ arrangement; and either

(a) the company has transferred substantially all the risks and rewards of the asset, or (b) the company has neither transferred nor retained substantially all the risks and rewards of the asset, but has transferred control of the asset.

Impairment of financial assets

The company assesses at each reporting date whether a financial asset or group of financial assets is impaired. A financial asset or a group of financial assets is deemed to be impaired if, and only if, there is objective evidence of impairment as a result of one or more events that has occurred after the initial recognition of the asset (an incurred ‘loss event’) and that loss event has an impact on the estimated future cash flows of the financial asset or the group of financial assets that can be reliably estimated.

Evidence of impairment may include indications that the debtors or a group of debtors is experiencing significant financial difficulty, default or delinquency in interest or principal payments, the probability that they will enter bankruptcy or other financial reorganisation and where observable data indicate that there is a measurable decrease in the estimated future cash flows, such as changes in arrears or economic conditions that correlate with defaults.

Financial assets carried at amortised cost

For financial assets carried at amortised cost, the company first assesses whether objective evidence of impairment exists individually for financial assets that are individually significant, or collectively for financial assets that are not individually significant. If the company determines that no objective evidence of impairment exists for an individually assessed financial asset, whether significant or not, it includes the asset in a group of financial assets with similar credit risk characteristics and collectively assesses them for impairment. Assets that are individually assessed for impairment and for which an impairment loss is, or continues to be, recognised are not included in a collective assessment of impairment.

ANNUAL FINANCIAL STATEMENTS 2018 18

If there is objective evidence that an impairment loss has been incurred, the amount of the loss is measured as the difference between the asset’s carrying amount and the present value of estimated future cash flows (excluding future expected credit losses that have not yet been incurred). The present value of the estimated future cash flows is discounted at the financial asset’s original effective interest rate. If a loan has a variable interest rate, the discount rate for measuring any impairment loss is the current effective interest rate.

The carrying amount of the asset is reduced through the use of an allowance account and the loss is recognised in the statement of comprehensive income. Interest income continues to be accrued on the reduced carrying amount and is accrued using the rate of interest used to discount the future cash flows for the purpose of measuring the impairment loss. The interest income is recorded as finance income in the statement of comprehensive income. Loans together with the associated allowance are written off when there is no realistic prospect of future recovery and all collateral has been realised or has been transferred to the company.

If, in a subsequent year, the amount of the estimated impairment loss increases or decreases because of an event occurring after the impairment was recognised, the previously recognised impairment loss is increased or reduced by adjusting the allowance account. If a write-off is later recovered, the recovery is credited to finance costs in the statement of comprehensive income.

Financial liabilities – initial recognition and subsequent measurement

Financial liabilities within the scope of IAS 39 are classified as financial liabilities at fair value through profit or loss, loans and borrowings, or as derivatives as appropriate. The company determines the classification of its financial liabilities at initial recognition. All financial liabilities are recognised initially at fair value. The company’s financial liabilities include reinsurance and other payables and amounts due to related parties.

The financial liabilities are subsequently measured at amortised cost, using the effective interest rate (EIR) method. The EIR amortisation is included in finance costs in the statement of comprehensive income.

Derecognition of financial liabilities

A financial liability is derecognised when the obligation under the liability is discharged or cancelled or expires.When an existing financial liability is replaced by another from the same lender on substantially different terms, or the terms of an existing liability are substantially modified, such an exchange or modification is treated as a derecognition of the original liability and the recognition of a new liability, and the difference in the respective carrying amounts is recognised in the statement of comprehensive income.

Offsetting of financial instruments

Financial assets and financial liabilities are offset and the net amount is reported in the statement of financial position if, and only if, there is a currently enforceable legal right to offset the recognised amounts and there is an intention to settle on a net basis, or to realise the assets and settle the liabilities simultaneously. Income and expense will not be offset in the statement of comprehensive income unless required or permitted by any accounting standard or interpretation, as specifically disclosed in the accounting policies of the company.

i. Impact of adoption of IFRS 9

On 29 July 2014, the IASB issued the final IFRS 9 Financial Instruments Standard which bring together the classification and measurement, impairment and hedge accounting phases of the IASB’s project to replace IAS 39 Financial Instruments: Recognition and Measurement.

On 1 January 2018, the Company adopted IFRS 9 on its effective date of 1 January 2018.

The Company has taken advantage of the exemption that allows it not to restate comparative information for prior periods with respect to classification and measurement, including impairment changes, in the scope of IFRS 9.

Differences in the carrying amounts of financial assets and financial liabilities resulting from the adoption of IFRS 9 have been recognized in retained earnings and reserves as at 1 January 2018. Therefore, the comparative information for 2017 is reported under IAS 39 and is not comparable to the information presented for 2018.

Changes to classification and measurement

IFRS 9 introduces a principles-based approach to the classification of financial assets. All financial instruments, except equity instruments and derivatives, including hybrid contracts are measured at fair value through profit or loss (FVTPL), fair value through comprehensive income (FVOCI) or amortized cost, based on the (i) their business model and (ii) the instrument’s contractual cash flow characteristics.

These categories replace the IAS 39 classifications of FVTPL, available for sale (AFS), loans and receivables, and held to maturity.

Equity instruments are measured at FVTPL, unless they are not held for trading purposes, in which case an irrevocable election can be made on initial recognition to measure them at FVOCI with no subsequent reclassification to profit or loss.

For financial liabilities, most of the pre-existing requirements for classification and measurement previously included in IAS 39 were carried forward unchanged into IFRS 9 other than the provisions relating

SANLAM 19

the recognition of changes in own credit risk for financial liabilities designated at fair value through profit or loss, as permitted by IFRS 9. The table below summarizes the changes in classification of financial instruments recognized in accordance with IAS 39, after the adoption of IFRS 9:

As at 1 January 2018, the Company classified its financial instruments at amortized cost, if both of the following conditions were met:

i. The financial assets are held within a business model with the objective to hold financial assets in order to collect contractual cash flows (business model test)

The contractual terms of the financial asset give rise on specified dates to cash flows that are solely payments of principal and interest (SPPI) on the principal amount outstanding (SPPI test)

Instruments at fair value through profit or loss

The Company has designated certain financial assets that would otherwise meet the requirements to be measured at amortized cost, as at fair value through profit or loss (FVTPL), to significantly reduce an accounting mismatch that would have arisen, since the underlying liabilities (insurance contract liabilities) are assessed by actuarial techniques based on fair valuation assumptions. The instruments include fixed deposits, treasury bills and treasury bonds that are directly attributable to policy holders. The following methodologies applied in the valuation of insurance contract liabilities, are based on fair valuation techniques:

Individual Life Liabilities:

• The unit reserve, which relates to the savings component of Dreambuilder policies is calculated as the number of units multiplied by a unit price (less a surrender penalty for inactive policies).

• A bonus stabilization reserve for the Dreambuilder product which is assessed an accumulation for past over-/ under declarations of bonuses relative to the actual investment return earned on the funds, and:

• Non-unit reserves are also calculated by projecting all future outgoes less all future income and discounting these reserving cash flows back to the valuation date.

Group Life Liabilities

• An Unearned Premium Reserve is calculated to represent the element of premiums already received where cover has not yet been provided. Upfront costs equal to the commission rate paid per scheme are then subtracted from the UPR.

• For personal loans, an Unearned Premium Reserve, an INBR equivalent to earned premiums is held. A run-down of the UPR takes into account, changes in sum assured over the loan term, therefore a reducing sum assured UPR is adopted

Financial Instrument Classification under IAS 39

Classification under IFRS 9

Measurement

Cash and balances with banks

1 Loans & receivablesCash and cash equivalents

Amortized cost

Treasury bills and bonds, and fixed deposits – shareholder funds

2 Loans & receivablesDebt instruments at amortized cost

Amortized cost

Statutory deposits 2 Loans & receivablesDebt instruments at amortized cost

Amortized cost

Treasury bills and bonds, and fixed deposits – policy holder funds

2 Loans & receivablesFair value through profit or loss

Amortized cost

Investment in quoted/unquoted shares

3Fair value through profit or loss

Fair value through profit or loss

Fair value

Reinsurance receivables 4 Not in scope** Not in scope** Not in scope**Premium receivables 4 Not in scope** Not in scope** Not in scope**Other receivables 5 Loans & receivables Amortized cost Amortized cost

**In accordance with IFRS 9, rights and obligations arising from insurance contracts are not in the scope of IFRS 9 and therefore the measurement criteria for premium receivables remains unchanged, after the adoption of IFRS 9. The change in carrying amounts relates to additional impairment allowances and fair values losses amounting to Ushs 216 million.

ANNUAL FINANCIAL STATEMENTS 2018 20

for credit life polices where the data is available. Upfront costs equal to the actual commission rate paid per scheme are then subtracted from the UPR.

• Under the Deposit Administration business, Sanlam Uganda collects contributions and invests them. Interest is added to each account in the first three years from the date of joining the scheme, with a guaranteed rate ranging from 7.5% to 8% per annum. The total reserve held is the market value of the fund.

The market value of the fund refers to the underlying assets of the deposit administration portfolio and is an accumulation of the net contributions at the actual investment returns earned, which can be positive or negative. A portion is allocated to member accounts representing the guaranteed benefit payable and is an accumulation of the net contributions at the bonus rates declared. A bonus stabilization reserve (BSR), which is the difference between the market value (the total reserve) and the book value (member accounts) is continually assessed.

Transition disclosures

The following pages set out the impact of adopting IFRS 9 on the statement of financial position and retained earnings including the effect of replacing IAS 39’s incurred credit loss calculations with IFRS 9’s ECLs:

IAS 39 Category

IFRS 9Category

IAS 39 measurement

Re-measurement (ECL/Fair value changes)

IFRS 9 measurement

Amount (Ushs’000)

Amount (Ushs’000)

Amount (Ushs’000)

Financial assets

Cash and balances with banks L & R AC1 1,253,908 (14,678) 1,239,230

Staff debtors L & R AC 45,932 - 45,932

Statutory deposits L & R AC1 2,698,244 (25,443) 2,672,801

Financial investments held to maturity L & R

AC1 4,838,043 (90,790) 4,747,253

FVTPL2 9,778,545 (85,412) 9,693,133

Investments in quoted and unquoted shares FVTPL FVTPL 508,096 - 508,096

19,122,768 (216,323) 18,906,445

Financial liabilities

Amount due to related parties L & R AC 1,350,498 - 1,350,498

Other payablesL & R AC 1,362,939 - 1,362,939

2,713,437 - 2,713,437

Total change in equity due to adopting IFRS 9: (216,323)

1The company has assessed expected credit losses on these instruments, held at amortized cost, as at 1 January 2018. The expected credit loss computations indicated that a higher provision should have been recognized. There were no loss provisions recognized on these financial instruments as at 31 December 2017.

2On initial recognition (under IAS 39), these instruments were classified as held to maturity. Under IFRS 9, these instruments have been reclassified to fair value through profit or loss (FVPL) to significantly reduce an accounting mismatch, since the underlying liabilities, are measured at fair value. The re-measurement relates to the fair value loss that was recognized on 1 January 2018.

SANLAM 21

Business model test

The Company determines its business model at the level that best reflects how it manages groups of financial assets to achieve its business objective.

The Company’s business model is not assessed on an instrument-by-instrument basis, but at a higher level of aggregated portfolios and is based on observable factors such as:

• How the performance of the business model and the financial assets held within that business model are evaluated and reported to the entity’s key management personnel

• The risks that affect the performance of the business model (and the financial assets held within that business model) and, in particular, the way those risks are managed

• How managers of the business are compensated (for example, whether the compensation is based on the fair value of the assets managed or on the contractual cash flows collected)

• The expected frequency, value and timing of sales are also important aspects of the Company’s assessment. The business model assessment is based on reasonably expected scenarios without taking ‘worst case’ or ‘stress case’ scenarios into account. If cash flows after initial recognition are realised in a way that is different from the Company’s original expectations, the Company does not change the classification of the remaining financial assets held in that business model, but incorporates such information when assessing newly originated or newly assessed financial assets going forward.

After initial measurement, debt issued and other borrowed funds are subsequently measured at amortised cost.

Amortised cost is calculated by taking into account any discount or premium on issue funds, and costs that are an integral part of the Effective Interest Rate (EIR). A compound financial instrument which contains both a liability and an equity component is separated at the issue date.

The accounting for financial liabilities has remained largely the same as it was under IAS 39.

SPPI test

As a second step of its classification process the Company assesses the contractual terms of the financial assets to identify whether they meet the SPPI test.

‘Principal’ for the purpose of this test is defined as the fair value of the financial asset at initial recognition and may

change over the life of the financial asset (for example, if there are repayments of principal or amortisation of the premium/discount).

The most significant elements of interest within a lending arrangement are typically the consideration for the time value of money and credit risk. To make the SPPI assessment, the Company applies judgement and considers relevant factors such as the currency in which the financial asset is denominated, and the period for which the interest rate is set.

In contrast, contractual terms that introduce a more than de minimis exposure to risks or volatility in the contractual cash flows that are unrelated to a basic lending arrangement do not give rise to contractual cash flows that are solely payments of principal and interest on the amount outstanding. In such cases, the financial asset is required to be measured at FVPL. From 1 January 2018, the Company does not reclassify its financial assets subsequent to their initial recognition, apart from the exceptional circumstances in which the Company acquires, disposes of, or terminates a business line.

Financial liabilities are never reclassified. The Company did not reclassify any of its financial assets or liabilities in 2018.

Changes to the impairment calculation The adoption of IFRS 9 has fundamentally changed the Company’s accounting for credit losses by replacing IAS 39’s incurred loss approach with a forward-looking expected credit loss (ECL) approach. The impairment model is applied to all financial assets except for financial assets classified as at FVTPL and equity securities designated as at FVOCI, which are not subject to impairment assessment.

Under IAS 39, impairment losses are recognized, if and only if, there is objective evidence of impairment as a result of one or more loss events that have occurred after initial recognition of the asset and that loss event has a detrimental impact on the estimated future cash flows of the asset that can be reliably estimated. If there is no objective evidence of impairment for an individual financial asset, that financial asset is included in a group of assets with similar credit risk characteristics and collectively assessed for impairment losses incurred but not yet identified.

Under IFRS 9, ECLs are recognized in profit or loss before a loss event has occurred, which could result in earlier recognition of credit losses compared to the IAS 39 model.

Under IAS 39, incurred losses are measured by incorporating reasonable and supportable information about past events and existing conditions. Under IFRS 9, the ECL model, which is forward-looking. In

ANNUAL FINANCIAL STATEMENTS 2018 22

addition, IFRS 9 requires that forecasts of future events and economic conditions be used when determining significant increases in credit risk and when measuring expected losses.

Therefore, from 1 January 2018, the Company has been recording the allowance for expected credit losses for all debt financial assets held at amortized cost.

The ECL allowance is based on the credit losses expected to arise over the life of the asset (the lifetime expected credit loss or LTECL), unless there has been no significant increase in credit risk since origination, in which case, the allowance is based on the 12 months’ expected credit loss (12mECL).

The 12mECL is the portion of LTECLs that represent the ECLs that result from default events on a financial instrument that are possible within the 12 months after the reporting date.Changes to the impairment calculation (continued)

Both LTECLs and 12mECLs are calculated on either an individual basis or a collective basis, depending on the nature of the underlying portfolio of financial instruments.

The Company has established a policy to perform an assessment, at the end of each month, of whether a financial instrument’s credit risk has increased significantly since initial recognition, by considering the change in the risk of default occurring over the remaining life of the financial instrument.

Based on the above process, the Company groups its financial instruments into Stage 1, Stage 2, Stage 3 and POCI, as described below:

Stage 1: When loans are first recognised, the Company recognises an allowance based on 12mECLs. Stage 1 loans also include facilities where the credit risk has improved and the loan has been reclassified from Stage 2. Sanlam Life InsurLimited has included relative and absolute thresholds in the definition of significant increase in credit risk and a backstop of 8 days past due. All financial instrument that are 30 days past due are migrated to stage 2.

Stage 2: When a loan has shown a significant increase in credit risk since origination, the COMPANY records an allowance for the LTECLs. Stage 2 loans also include facilities, where the credit risk has improved and the loan has been reclassified from Stage 3.

Stage 3: Loans considered credit-impaired. The Company records an allowance for the LTECLs.

POCI: Purchased or originated credit impaired (POCI) assets are financial assets that are credit impaired on initial recognition. POCI assets are recorded at fair value at original recognition and interest income is subsequently recognised based on a credit-adjusted EIR. ECLs are only recognised or released to the extent that there is a

subsequent change in the expected credit losses.

For financial assets for which the Company has no reasonable expectations of recovering either the entire outstanding amount, or a proportion thereof, the gross carrying amount of the financial asset is reduced. This is considered a (partial) derecognition of the financial asset.

Calculation of ECL

The Company calculates ECLs by measuring the expected cash shortfalls, discounted at an approximation to the EIR. A cash shortfall is the difference between the cash flows that are due to an entity in accordance with the contract and the cash flows that the entity expects to receive.The mechanics of the ECL calculations are outlined below and the key elements are, as follows:

PD The Probability of Default is an estimate of the likelihood of default over a given time horizon. A default may only happen at a certain time over the assessed period, if the facility has not been previously derecognised and is still in the portfolio.

EAD The Exposure at Default is an estimate of the exposure at a future default date, taking into account expected changes in the exposure after the reporting date, including repayments of principal and interest, whether scheduled by contract or otherwise, expected drawdowns on committed facilities, and accrued interest from missed payments.

LGD The Loss Given Default is an estimate of the loss arising in the case where a default occurs at a given time. It is based on the difference between the contractual cash flows due and those that the lender would expect to receive, including from the realisation of any collateral. It is usually expressed as a percentage of the EAD.

Under stage 1, The 12mECL is calculated as the portion of LTECLs that represent the ECLs that result from default events on a financial instrument that are possible within the 12 months after the reporting date. The Company calculates the 12mECL allowance based on the expectation of a default occurring in the 12 months following the reporting date. These expected 12-month default probabilities are applied to a forecast EAD and multiplied by the expected LGD and discounted by an approximation to the original EIR. This calculation is made for each of the four scenarios, as explained above.

When a financial instrument has shown a significant increase in credit risk since origination (stage 2), the PDs and LGDs are estimated over the lifetime of the instrument. The expected cash shortfalls are discounted by an approximation to the original EIR. For financial instruments considered credit-impaired, the Company recognises the lifetime expected credit losses for these loans. POCI assets are financial assets that are credit impaired on initial recognition. The COMPANY only recognises the cumulative changes in lifetime ECLs since

SANLAM 23

initial recognition, discounted by the credit adjusted EIR.

The company applies the simplified model applies for staff debtors and other receivables with maturities of less than 12 months.

ECL models

In its ECL models, the Company relies on a broad range of forward-looking information as economic inputs, such as:• GDP growth

• Unemployment rates

• Central Bank base rates

• Inflation rates

• Interest rates

• Exchange rates

• Domestic borrowing

• Credit to private sector

The inputs and models used for calculating ECLs may not always capture all characteristics of the market at the date of the financial statements. To reflect this, qualitative adjustments or overlays are occasionally made as temporary adjustments when such differences are significantly material.

Impairment of investments and bank balances

Investments in treasury bills, treasury bonds, investments in fixed deposits and bank balances are impaired by applied the following:

A probability of default determined from a credit rating from Fitch. A probability of default is assigned to the credit rating obtained. When a credit from Fitch is not available, Standard & Poor and Fitch are used. The loss given default is assigned at 45% based on Basel specifications.

Definition of Default

IFRS 9 does not define default but requires the definition to be consistent with the definition used for internal credit risk management purposes. IFRS 9 contains a rebuttable presumption that default does not occur later than when a financial asset is 90 days past due. Under IFRS 9, the Company will consider a financial asset as credit impaired when one or more events that have a detrimental impact on the estimated future cash flows of a financial asset have occurred or when contractual payments are 90 days and above past due.

Write-offs

The Company’s accounting policy under IFRS 9 remains the same as it was under IAS 39. Financial assets are

written off either partially or in their entirety only when the Company has stopped pursuing the recovery. If the amount to be written off is greater than the accumulated loss allowance, the difference is first treated as an addition to the allowance that is then applied against the gross carrying amount. Any subsequent recoveries are credited to profit or loss.

Hedging accounting

The company had no hedging relationships as at 1 January 2018, hence no impact on transition to IFRS 9.

Other adjustments

In addition to the adjustments described above, upon adoption of IFRS 9, other items of the primary financial statements such as deferred taxes, income tax expense and retained earnings were adjusted as necessary.

» Impairment of non-financial assets

The company assesses at each reporting date whether there is an indication that an asset may be impaired. If any such indication exists, or when annual impairment testing for an asset is required, the company estimates the asset’s recoverable amount. An asset’s recoverable amount is the higher of an asset’s or cash-generating unit’s (CGU) fair value less costs to sell and its value in use. The recoverable amount is determined for an individual asset, unless the asset does not generate cash inflows that are largely independent of those from other assets or groups of assets.

Where the carrying amount of an asset or CGU exceeds its recoverable amount, the asset is considered impaired and is written down to its recoverable amount. In assessing value in use, the estimated future cash flows are discounted to their present value using a pre-tax discount rate that reflects current market assessments of the time value of money and the risks specific to the asset.

In determining fair value less costs to sell, recent market transactions are taken into account, if available. If no such transactions can be identified, an appropriate valuation model is used. These calculations are corroborated by valuation multiples, quoted share prices for publicly traded subsidiaries or other available fair value indicators.

Impairment losses of continuing operations are recognised in the statement of comprehensive income in those expense categories consistent with the function of the impaired asset.

For assets, an assessment is made at each reporting date as to whether there is any indication that previously recognised impairment losses may no longer exist or may have decreased. If such indication exists, the company makes an estimate of the asset’s or CGU recoverable amount. A previously recognised impairment loss is reversed only if there has been a change in the estimates

ANNUAL FINANCIAL STATEMENTS 2018 24

used to determine the asset’s recoverable amount since the last impairment loss was recognised. If that is the case, the carrying amount of the asset is increased to its recoverable amount. That increased amount cannot exceed the carrying amount that would have been determined, net of depreciation, had no impairment loss been recognised for the asset in prior years. Such reversal is recognised in the statement of comprehensive income unless the asset is carried at revalued amount, in which case the reversal is treated as a revaluation increase.

» Cash and cash equivalents

Cash and cash equivalents comprise cash at bank and in hand and short-term deposits with an original maturity of three months or less in the statement of financial position. Cash and cash equivalents are valued at amortised cost.For the purpose of the statement of cash flows, cash and cash equivalents consist of cash and cash equivalents as defined above.

» Taxes

Current income tax

Current income tax is provided for in the statement of comprehensive income on the basis of the results included therein adjusted in accordance with the provisions of the Income Tax Act (Cap. 340).Current income tax assets and liabilities for the current and prior periods are measured at the amount expected to be recovered from or paid to the tax authorities. The tax rates and tax laws used to compute the amount are those that are enacted or substantively enacted, by the reporting date.Revenues, expenses and assets are recognised net of the amount of Value Added Tax (VAT) except:

• Where the VAT incurred on a purchase of goods and services is not recoverable from Uganda Revenue Authority, in which case the VAT is recognized as part of the cost of the acquisition of the asset or as part of the expense for the item as applicable; and