Saikat.iip Report

445

INSTITUTE FOR TECHNOLOGY AND MANAGEMENT INDUSTRIAL INTERNSHIP PROGRAM REPORT A STUDY ON “EQUITY AND DERIVATIVES- OPTIONS & FUTURES” Submitted in partial fulfillment of

-

Upload

saikat-das -

Category

Documents

-

view

11 -

download

4

description

great report. helpful!

Transcript of Saikat.iip Report

INSTITUTE FOR TECHNOLOGY AND

MANAGEMENT

INDUSTRIAL INTERNSHIP PROGRAM REPORT

A STUDY

ON

“EQUITY AND DERIVATIVES- OPTIONS & FUTURES”

Submitted in partial fulfillment of

POST GRADUATE DIPLOMA IN MANAGEMENT (PGDM-

FINANCE)

Submitted by

Saikat Das

PGDM 1720

Academic Year (2013-2015)

Under the guidance of

Dr. Latha Sreeram Mr. Abhishek Kumar Consultant – Finance Department Deputy Manager

Institute for Technology and Management, Kharghar Karvy

Stock Broking Limited, Vashi

DECLARATION

This project entitiled “A study on Equity and Derivatives (options & futures)” in Karvy Stock Broking Limited, is a benefited work done by me in partial fulfillment of my PGDM Finance course Management from Institute for Technology and Management, Kharghar.

I further state that this report entirely stand original in its

concepts ideology and genuine in its presentation.

I declare that this report has not been submitted to any other University/Institute for the award of any Degree/Diploma.

Saikat Das

PGDM Finance – 2013-15

Institute for Technology and Management

Kharghar.

CERTIFICATE OF APPROVAL

This is to certify that the

Summer Internship Project “A study on

Equity and Derivatives (options & futures)” submitted by Saikat

Das, a student of Institute for Technology and Management, as a

part of the curriculum of PGDM – Finance has

been approved.

___________________ ________________

Faculty Guide Dean

Dr. Latha Sreeram Prof. AS Adhikari

Consultant ITM BS Kharghar

Finance Department

ITM BS Kharghar

Shop no. A 43/44, Vashi Plaza

Sector-17, Vashi, Navi Mumbai-400703

CERTIFICATE

This is to certify that the project titled “Study on equity and Derivatives- options and

futures” is a bonafide research work carried out by Mr.

Saikat Das (PGDM 1720) under our guidance. This

dissertation has not formed the basis for the award previously

of any Degree/Diploma, or any other similar titles of any

Institution/University.

Mr. Abhishek Kumar

Deputy Manager

Karvy Stock Broking Ltd

Vashi Branch

Navi Mumbai

ACKNOWLEDGEMENT

I take this opportunity to thank all, whose able guidance and kind co-operation helped me complete my internship & study On “A study on Equity and Derivatives (options &

futures)” successfully.

I am particularly indebted to Karvy Stock Broking Ltd, for providing me the opportunity to complete my project successfully. Employees of Karvy always extended their cooperation and provided me with valuable information regarding the organization in spite of their busy schedule.

I would like to thank and express my gratitude towards Mr. Abhishek Kumar (deputy Manager) my project guide, who has been a constant source of inspiration and encouragement for me during this project.

I extend my gratitude to ITM Business School for giving me this opportunity.

I extend my sincere gratitude to my Head of the Institute Dr. Ganesh

Raja, for giving me the privilege to do the Summer Internship Program. I am greatly obliged to my Faculty Guide Dr. Latha Sreeram (Chief consultant, Finance Department) for her complete guidance and also for his valuable insights on the project.

Last but not the least, I would extend a special word of thanks to all my well-wishers for giving me a helping hand whenever needed and for making the project a success.

Place: Kharghar, Navi Mumbai

Signature:

Date:

Saikat Das

EXECUTIVE SUMMARY:-

The Summer Project at “KARVY STOCK BROKING LIMITED” has given an exposure into the investment scenario in India. The project while working at “KARVY STOCK BROKING LIMITED” includes advisory services i.e. educating the existing and potential investors about stock market as an alternative source to investment. This involves catering to the

queries of the investors about the concept of stock market, the various options that an investor can invest his money into, funds management of investors.

This internship report consists of overall experience of working as a part of KARVY STOCK BROKING LTD. This experience helped me to understand the functioning of a stock broking company. My training consisted of observing how the trading is done in live financial market and also learning about the various sectors of investment like shares, futures, options, etc. Analyzing the investors’ behavior includes understanding the concerns a person has towards Stock Market, his stages in life and wealth cycle, the effect of the investments made by the peer groups, effect of the profession he/she is in, education

qualification, importance of tax benefits, the most preferred saving tool etc. and this all is analyzed with the help of a schedule prepared. Understanding the significance of Equity and Derivatives market, types of instruments present in the Indian Stock Market such as Shares, Futures, Options and Forwards. The various techniques used to identify the trend of the market and analysing the scrip before investing.

Through the systematic investment plan invest a specific amount for a continuous period, at regular intervals. By doing this, the investor get the advantage of rupee cost averaging which means that by investing the same amount at regular intervals, the average cost per unit remains lower than the average market price.

During my internship, I also came to know the various tactics and strategies of trading in the financial markets. I started from the very basics of stock market and earned a very good knowledge by observing the portfolios of different investors which indicated their investing behaviors in various sectors and various segments. The study is limited to Equity and derivatives, with special reference to Futures and Options in Indian context. The study can’t be said as totally perfect. The study has only made a humble attempt to compare between equity and derivatives market in respect to its risk and return to investors, only in Indian context.

CONTENT

1. OBJECTIVES OF THE STUDY

2. MODUS OPERANDI3. INDUSTRY PROFILE4. COMPANY PROFILE5. INTRODUCTION TO

STOCK MARKET.6. INTRODUCTION TO BSE7. INTRODUCTION TO NSE8. FUNDAMENTAL

ANALYSIS9. TECHNICAL ANALYSIS10. INTRODUCTION TO

DERIVATIVES11. STRATEGIES IN

OPTIONS12. OPTION GREEKS13. PORTFOLIO

MANAGEMENT SERVICE AND CREATION

14. TRANSMISSION AND TRANSPOSITION OF SHARE CERTIFICATE.

15. LEARNINGS16. SUGGESTIONS17. CONCLUSIONS18. BIBLIOGRAPHY

Objectives of the Study

To study the movements in stocks in equity market.

To understand the Indian stock market and its various concepts.

To study in detail the role of futures and options market.

To study the role of derivatives in the Indian financial

market.

To study the various strategies in derivative market.

To study the product in equity market and derivative market (options & Future)

Modus Operandi of the project

With the help of our company

guide, we were given knowlwdge

about equity and derivative market

in depth and its mechanism. I have

also read some other similar reports

online to get some knowledge.

Moreover we are given individual

PCs to work on getting more

knowledge about fundamentals and

technicals of market.

The next task was given to keep an

eye on the daily changes that occurs

in Stock market with respect to

economic conditions as well as due

to changes in government policies

To complete this report, there is

more use of secondry source of

information i.e. moneycontrol,

calloptionputoption, nse.com and

some more and further primary

source as well i.e. clients of Karvy

stoc broking ltd. Information will

be taken with the help of

questionnaire method as well as

telephonic survey technique (only

to Active Karvy Clients). This data

will be mainly used to check their

investment patterns in equity and

derivative market. Moreover since

the title is on comparative analysis

of equity and derivative, it will also

help in understanding investor's

why they choose equity over

options and future and vice versa. I

have already started the survey

method over phone by calling

clients of Karvy. Moreover the

clients who visit the office are also

my part in achieving my goals in

the report. Finally meeting the

prospective clients helps a lot in

finding more information.

INDUSTRY PROFILE

INTRODUCTION

Stock exchanges to some extent play an important role as indicators, reflecting the performance of the country’s economic state of health. Stock market is a place where securities are bought and sold. It is exposed to a high degree of volatility; prices fluctuate within minutes and are determined by the demand and supply of stocks at a given time. Stock brokers are the ones who buy and sell securities on behalf of individuals and institutions for some commission.

The Securities and Exchange Board of India (SEBI) is the authorized body, which regulates the operations of stock exchanges, banks and other financial institutions. The past performances in the capital markets especially the securities scam by ‘Harshad Mehta’ has led to tightening of the operations by SEBI. In addition the international trading and investment exposure has made it imperative to better operational efficiency. With the view to improve, discipline and bring greater transparency in this sector, constant efforts are being made and to a certain extent improvements have been made.

HISTORY OF THE STOCK BROKING INDUSTRY

Indian Stock Markets are one of the oldest in Asia. Its history dates back

to nearly200 years ago. The earliest records of security dealings in India are meager and obscure. By 1830's business on corporate stocks and shares in Bank and Cotton presses took place in Bombay. Though the trading list was broader in 1839, there were only half a dozen brokers recognized by banks and merchants during 1840 and 1850. The1850's witnessed a rapid development of commercial enterprise and brokerage business attracted many men into the field and by 1860 the number of brokers increased into 60.In 1860-61 the American Civil War broke out and cotton supply from United States of Europe was stopped; thus, the 'Share Mania' in India begun. The number of brokers increased to about 200 to 250. However, at the end of the American Civil War, in1865, a disastrous slump began (for

example, Bank of Bombay Share which had touched Rs 2850 could only be sold at Rs. 87). At the end of the American CivilWar, the brokers who thrived out of Civil War in 1874, found a place in a street (nowappropriately called as Dalal Street) where they would conveniently assemble andtransact business.In 1887, they formally established in Bombay, the "Native Share and Stock Brokers'Association" (which is alternatively known as "The Stock Exchange"). In 1895, theStock Exchange acquired a premise in the same street and it was inaugurated in1899. Thus, the Stock Exchange at Bombay was consolidated.Thus in the same way, gradually with the passage of time number of exchangeswere increased and at currently it reached to the figure of 24 stock exchanges.

Development

An important early event in the development of the stock market in India was the formation of the Native Share and Stock Brokers’ Association at Bombay in 1875, the precursor of the present-day Bombay Stock Exchange. This was followed by the formation of associations /exchanges in Ahmedabad (1894), Calcutta (1908) and Madras (1937). In addition, a large number of ephemeral exchanges emerged mainly in buoyant periods to recede into oblivion during depressing times subsequently. In order to check such aberrations and promote a more orderly development of the stock market, the central government introduced a legislation called the Securities Contracts (Regulation) Act, 1956. Under this legislation, it

is mandatory on the part of a stock exchanges to seek government recognition. As of January 2002 there were 23 stock exchanges recognized by the central Government. They are located at Ahemdabad, Bangalore, Baroda, Bhubaneshwar, Calcutta, Chenni,(the Madrasstock Exchanges ), Cochin, Coimbatore, Delhi, Guwahati, Hyderbad, Indore, Jaipur,Kanpur, Ludhiana, Mangalore, Mumbai(the National Stock Exchange or NSE),Mumbai (The Stock Exchange), papularly called the Bombay Stock Exchange,Mumbai (OTC Exchange of India), Mumbai (The Inter-connected Stock Exchange of India), Patna, Pune, and Rajkot. Of course, the principle courses are the National Stock Exchange and The Bombay Stock Exchange , accounting for the bulk of the business done on the Indian stock market. While the recognized

stock exchanges have been accorded a privileged position,they are subject to governmental supervision and control. The rules of a recognized stock exchanges relating to the managerial powers of the governing body, admission, suspension, expulsion, and re-admission of its members, appointment of authorized representatives and clerks, so on and so forth have to be approved by the government. These rules can be amended, varied or rescinded only with the prior approval of the government

COMPANY PROFILE

KARVY Stock Broking Limited

KARVY Stock Broking Limited, one of the cornerstones of the KARVY edifice, flows freely towards attaining diverse goals of the customer through varied

services. It creates a plethora of opportunities for the customer by opening up investment vistas backed by research-based advisory services. Here, growth knows no limits and success recognizes no boundaries. Helping the customer create waves in his portfolio and empowering the investor completely is the ultimate goal. KARVY Stock Broking Limited is a member of:

National Stock Exchange (NSE)

Bombay Stock Exchange (BSE)

Hyderabad Stock Exchange (HSE)

Karvy Investor Services Limited

Deepening of the Financial Markets and an ever-increasing sophistication in corporate transactions, has made the role of Investment Bankers indispensable to organizations seeking

professional expertise and counselling, in raising financial resources through capital market apart from Capital and Corporate Restructuring, Mergers & Acquisitions, Project Advisory and the entire gamut of Financial Market activities.

Our quality professional team and our work-oriented dedication have propelled us to offer value-added corporate financial services and act as a professional navigator for long term growth of our clients, who include leading corporates, State Governments, Foreign Institutional Investors, public and private sector companies and banks, in Indian and global markets. We have also emerged as a trailblazer in the arena of relationships, both at the customer and trade levels because of our unshakable integrity, seamless service and innovative solutions that are tuned to meet

varied needs. Our team of committed industry specialists, having extensive experience in capital markets, further nurtures this relationship.

Credentials

• Emerging as a leading Investment Banker with a strong support from its Group entities in Research, Stock Broking, Institutional Sales and Retail Distribution.

• Strong team of more than 25 qualified professionals operating from six cities; Hyderabad, Mumbai, Delhi, Kolkata, Chennai, and Bangalore apart from two overseas offices at New York (USA) and Dubai.

• One of the largest retail distribution networks with over 584 branches in over 389 cities/towns.

• Excellent Institutional Sales Division.

MISSION STATEMENT

“To Bring Industry, Finance and People together.”

VISION STATEMENT

“To be pioneering financial services company. And continue to grow at a healthy pace, year after year, decade after decade.”

VALUES

Trust

Integrity

Dedication

Commitment

Transparency

Enterprise

Hard work and team play

Learning & innovation

Empathy and humility

REGLATORY BODIES

MINISTRY OF FINANCE

a) SEBI (Stock Brokers, R & T Agent, Mtual Fund)

b) RBI (Commercial Banks, NBFCs)

c) Department of IT (PAN, TAN, e-TDS)

INVESTOR SERVICE - KEY FACTS

IPO’s handled - 720

financial transaction processed - 100 mn

number of investor accounts services - 16 mn

corporate clents as r&t agents - 300

asset mgmt,companies services - 11

mutual fund scheme services – 72

KARVY STOCK BROKING OFFERS

Personalized Service

Professional Advice

Long Term Relationship

Access to Research Report

Transparency and confidentiality

SERVICES

1.Stock broking

2. Demat services

3. Investment product distribution

4. Investment advisory services

5. Corporate finance & Merchant banking

6. Insurance

7. Mutual fund services

8. IT enabled services

9. Registrars & Transfer agents

10. Loans

Competitive Advantage - KARVY

Market Power

Brand Preference

Customer Value

SWOT ANALYSIS

Strength

Good research team.

Dedicated employees.

Strong customer relationship.

Strong brand name.

Wide spread branches and brokers network..

Weakness

Technology need to be upgraded.

Not enough advertisement

Opportunity

Growing IPO issues.

Positive outlook of people towards financial products.

Growing consumer awareness about equity related product.

Threat

Market uncertainty.

Galloping competition.

Broad economic factors like inflation etc

OBJECTIVES

Market Positioning

Market positioning statements of Karvy are “At Karvy we give you single window service” and “We

also ensure your comfort”. So, Karvy focus on the consumers who prefer almost all investment activities at same place by providing number of various financial services. At Karvy a person can purchase or sell shares, debentures etc. and at the same place also demat it. Karvy also provides other investment option to the same person at same place like Mutual Fund, Insurance, Fixed Deposit, and Bonds etc. and help the person in designing his portfolio. By this way Karvy provides comfort to its customers. Karvy is also positioned according to Ries and Trout. Karvy is promoted as a no. 1 investment product distributor and R & T agent of India.

Target Market

Karvy uses demographic segmentation strategy and segment people based on their occupation. Karvy uses selective specialization strategy for market targeting. Target person for the Karvy Stock Broking and Karvy Investment Service are persons who can work as sub-broker for the companies. Companies focus on Advisors of Insurance and post office, Tax consultants and CAs for making sub-broker.

Marketing channel System

Karvy uses one level marketing channel for investment product distribution. Sub-brokers work as intermediary between consumer and company. Company has both forward and backward flow of activity through channel. Company

distributes stationery, brokerage, and information forward to its sub-broker. The sub-brokers send filled forms, queries, amount of investment etc. back to the company.

Training Channel Members

Karvy provides training to the sub-brokers because they will be viewed as the company by the investors. The executives of Karvy explain various new schemes of investment to the sub-brokers with its objective, risk factors and expected return. Company also periodically arrange seminar to guide sub-brokers.

Advertising and Promotion:

The objective of advertising of Karvy is to create awareness about

services of Karvy among investors and sub-brokers and increase sub-brokers of Karvy. Company doesn’t give advertisement in media like TV, Newspapers, and Magazines etc. Karvy’s advertisement is made indirectly by the companies associate with it. Karvy is R & T agent of around 700 companies. They publish name, address and logo of Karvy on their annual report.Karvy also publish its weekly Stock Market Newsletter ‘Karvy Bazaar Baatein’ and monthly magazine ‘The Finapolis’ to guide investors and sub-brokers about market.

STRATEGIES

Karvy believes that foremost ingredient for success in the has been the co-operation ability to continously evolve both

organizational strcture and product offerings, thereby remaining on the cutting financial services. Karvy believes taht three capital viz., financial, human and technology, would drive the financial services sector in the future and draw the boundaries for achieving leadership. Karvy believes that the customized solutions are now the key drivers for market share and profit margins.

ACHIEVEMENTS1. Among the top 9 stock

brokers in India (4% of NSE volumes)

2. India's No. 1 Registrar & Securities Transfer Agents

3. Every 20th trade is done by KARVY Stock Broking Ltd.

4. Among the top 3 Depository Participants

5. Largest Network of Branches & Business

Associates6. ISO 9002 certified

operations by DNV7. Among top 10 Investment

bankers8. Largest Distributor of

Financial Products9. Adjudged as one of the top

50 IT uses in India by MIS Asia

10. Full Fledged IT driven operations trade is done by KARVY Stock Broking Ltd.

INTRODUCTION TO STOCK MARKET

What is a stock ?

A stock is a partial ownership in a

company or an industry, with rights to share in its profits. When an investor buys a stock of a company, he is called a shareholder or a stockholder of that company. The benefit of buying a share is that when the company profits, the shareholders also profit. The company distributes the profit among its shareholders, which is called the ‘dividend‘.

How do you make profits with stocks ?

But many traders make real profit in stocks using the market price of the stocks. Stocks are traded in the stock markets. The face value is the nominal value of the stock that is determined by the issuer of the stock. ‘Market price‘ of a stock is the price at which currently a stock is traded in the market. This price may be at premium or lesser than the ‘face value’ of the stock,

depending on the company’s performance and prospects, investors’ interests in the company and a lot of other factors.

Market price of a stock keeps varying as traders trade the stock in the market. Traders often make money using these variations in the market price of the stock. Stocks are bought at lower market prices and sold at higher prices later. This is referred to as ‘long‘ positions in market terms. Similarly stocks can be sold at a higher market price and bought at a lower price later. Thiis is referred to as ‘short‘ positions in market terms. In these cases, the difference in the market prices at the time of buying and selling will be seen as profit by the traders.

What is the Demat Account ?

Like opening a bank account for doing your personal financial

transactions, you have to open a Demat account to trade in the stock market. Demat account refers to Dematerialized account. This account helps you to buy and sell stocks without the need for physical paper shares.

A Demat Account is a must for trading the stocks these days. To open a demat account, you should select a Depository Participant (DP). These days most of the banks are also DPs. So you can contact any of the DPs with your identity, address proof and PAN documents for opening a demat account for a prescribed fee by the DP. The registered DPs are also listed in NSDL and CDSL.

Who is the Stock Broker ?

Stock Brokers are members of the Stock Exchanges. Only these members can conduct transactions in the exchange on behalf of the individuals and companies. So if you want to buy or sell shares in the exchange, you have to contact a stock broker for doing so. This normally requires the individuals to open an account with the Stock Broker. So the individual becomes a client for the stock broker.

Once the client wishes to buy a stock, the broker would place the order in the stock exchange on behalf of the client. When the transaction is done, the broker places the price to the client. The client pays for the stocks he bought and the broker transfers the stocks into the demat account of the client by following the transaction and settlement procedures.

Stock Markets:

Stock Market is a market where the trading of company stock, both listed securities and unlisted takes place. It is different from stock exchange because it includes all the national stock exchanges of the country. For example, we use the term, "the stock market was up today" or "the stock market bubble."

Stock Market Conditions

There are two ways to describe the general conditions of the stock market:

1)BULL MARKET

2)BEAR

MARKET

Bull Market

A Bull Market indicates the constant upward movement of the stock market. A particular stock that seems to be increasing in value is described to be bullish.

Bear Market

A bear market indicates the continuous downward movement of the stock market. stock that seems to be decreasing in value is described to be bearish.

Stock Exchanges:

Stock Exchanges are an organized marketplace, either corporation or

mutual organization, where members of the organization gather to trade company stocks or other securities. The members may act either as agents for their customers, or as principals for their own accounts.

Stock exchanges also facilitates for the issue and redemption of securities and other financial instruments including the payment of income and dividends. The record keeping is central but trade is linked to such physical place because modern markets are computerized. The trade on an exchange is only by members and stock broker do have a seat on the exchange.

History of Indian Stock Market:

Indian stock market marks to be

one of the oldest stock market in Asia. It dates back to the close of 18th century when the East India Company used to transact loan securities. In the 1830s, trading on corporate stocks and shares in Bank and Cotton presses took place in Bombay. Though the trading was broad but the brokers were hardly half dozen during 1840 and 1850.

An informal group of 22 stockbrokers began trading under a banyan tree opposite the Town Hall of Bombay from the mid-1850s, each investing a (then) princely amount of Rupee 1. This banyan tree still stands in the Horniman Circle Park, Mumbai. In 1860, the exchange flourished with 60 brokers. In fact the 'Share Mania' in India began with the American Civil War broke and the cotton supply from the US to Europe stopped. Further the brokers

increased to 250. The informal group of stockbrokers organized themselves as the The Native Share and Stockbrokers Association which, in 1875, was formally organized as the Bombay Stock Exchange (BSE).

BSE was shifted to an old building near the Town Hall. In 1928, the plot of land on which the BSE building now stands (at the intersection of Dalal Street, Bombay Samachar Marg and Hammam Street in downtown Mumbai) was acquired, and a building was constructed and occupied in 1930.Premchand Roychand was a leading stockbroker of that time, and he assisted in setting out traditions, conventions, and procedures for the trading of stocks at Bombay Stock Exchange and they are still being followed.

The following is the list of some of the initial members of the exchange, and who are still running their respective business:

D.S. Prabhudas & Company (now known as DSP, and a joint venture partner with Merrill Lynch)

Jamnadas Morarjee (now known as JM)

Champaklal Devidas (now called Cifco Finance)

Brijmohan Laxminarayan

In 1956, the Government of India recognized the Bombay Stock Exchange as the first stock exchange in the country under the Securities Contracts (Regulation) Act.

The most decisive period in the

history of the BSE took place after 1992. In the aftermath of a major scandal with market manipulation involving a BSE member named Harshad Mehta, BSE responded to calls for reform with intransigence. The foot-dragging by the BSE helped radicalise the position of the government, which encouraged the creation of the National Stock Exchange (NSE), which created an electronic marketplace. NSE started trading on 4 November 1994. Within less than a year, NSE turnover exceeded the BSE. BSE rapidly automated, but it never caught up with NSE spot market turnover. The second strategic failure at BSE came in the following two years. NSE embarked on the launch of equity derivatives trading. BSE responded by political effort, with a friendly SEBI chairman (D. R. Mehta) aimed at blocking equity derivatives

trading. The BSE and D. R. Mehta succeeded in delaying the onset of equity derivatives trading by roughly five years. But this trading, and the accompanying shift of the spot market to rolling settlement, did come along in 2000 and 2001 - helped by another major scandal at BSE involving the then President Mr. Anand Rathi. NSE scored nearly 100% market share in the runaway success of equity derivatives trading, thus consigning BSE into clearly second place. Today, NSE has roughly 66% of equity spot turnover and roughly 100% of equity derivatives turnover.

Capital Market: The capital market is divided into two segments viz:

Primary Market

Secondary Market

Primary Market:

Most companies are usually started privately by their promoters. However the promoters‘ capital and the borrowed capital from banks or financial institutions might not be sufficient for running the business over the long term. That is when corporate and the government looks at the primary market to raise long term funds by issuing securities such as debt or equity.

These securities may be issued at face value, at premium or at discount. Let us understand the meaning of these terms:

Face Value: Face value is the original cost of the security as shown in the certificate/instrument. Most equity shares have a face value of Rs. 1, Rs. 5, Rs. 10 or Rs. 100 and do not have much bearing on the actual market price of the stock. When issuing securities, they may be offered at a discount or at a premium.

Premium: When the security is offered at a price higher than the face value it is called a premium

Discount: When the security is offered at a price lower than the face value it is called a discount.

Secondary Market :

The secondary market provides liquidity to the investors in the primary market. Today we would not invest in any instrument if there was no medium to liquidate our position. The secondary markets provide an efficient platform for trading of those securities initially offered in the primary market. Also those investors who have applied for shares in an IPO may or may not get allotment. If they don‘t then they can always buy the shares (sometimes at a discount or at a premium) in the secondary market.

Trading in the secondary market is done through stock exchange. The Stock exchange is a place where the buyers and sellers meet to trade in shares in an organized manner. The stock exchange performs the

following functions:

Provide trading platform to investors and provide liquidity

Facilitate Listing of securities

Registers members - Stock Brokers, sub brokers

Make and enforce by-laws

Manage risk in securities transactions

Provides Indices

There are two leading stock exchanges in India which help us trade are:

National Stock Exchange: National Stock Exchange incorporated in the year 1992 provides trading in the equity as well as debt market. Maximum volumes take place on NSE and hence enjoy leadership position in the country today

Bombay Stock Exchange: BSE on the other hand was set up in the year 1875 and is the oldest stock exchange in Asia. It has evolved in to its present status as the premier stock exchange.

INTRODUCTION TO BSE:

As we read in the history of Indian stock exchange; the stock exchange, Mumbai, popularly known as

"BSE". BSE was established in 1875 as "The Native Share and Stock Brokers Association". It is the oldest one in Asia, even older than the Tokyo Stock Exchange, which was established in 1878. It is a voluntary non-profit making Association of Persons (AOP) and has converted itself into demutualised and corporate entity. It has evolved over the years into its present status as the Premier Stock Exchange in the country. It is the first Stock Exchange in the Country to have obtained permanent recognition in 1956 from the Govt. of India under the Securities Contracts (Regulation) Act, 1956.

The Exchange, while providing an efficient and transparent market for trading in securities, debt and derivatives upholds the interests of the investors and ensures redressal of their grievances whether against

the companies or its own member-brokers. It also strives to educate and enlighten the investors by conducting investor education programmes and making available to them necessary informative inputs.

A Governing Board having 20 directors is the apex body, which decides the policies and regulates the affairs of the Exchange. The Governing Board consists of 9 elected directors, who are from the broking community (one third of them retire every year by rotation), three SEBI nominees, six public representatives and an Executive Director & Chief Executive Officer and a Chief Operating Officer.

The Executive Director as the Chief Executive Officer is responsible for the day-to-day administration of the Exchange and he is assisted by the Chief Operating Officer and other

Heads of Department

INTRODUCTION TO NSE :

The National Stock Exchange (NSE) is India's leading stock exchange covering 364 cities and towns across the country. NSE was set up by leading institutions to provide a modern, fully automated screen-based trading system with national reach. The Exchange has brought about unparalleled transparency, speed & efficiency, safety and market integrity. It has set up facilities that serve as a model for the securities industry in terms of systems, practices and procedures. NSE has played a catalytic role in reforming the Indian securities market in terms of microstructure, market practices and trading volumes. The market today uses state-of-art information

technology to provide an efficient and transparent trading, clearing and settlement mechanism, and has witnessed several innovations in products & services viz. demutualisation of stock exchange governance, screen based trading, compression of settlement cycles, dematerialisation and electronic transfer of securities, securities lending and borrowing, professionalisation of trading members, fine-tuned risk management systems, emergence of clearing corporations to assume counterparty risks, market of debt and derivative instruments and intensive use of information technology.

The National Stock Exchange of India Limited has genesis in the report of the High Powered Study Group on Establishment of New Stock Exchanges, which

recommended promotion of a National Stock Exchange by financial institutions (FIs) to provide access to investors from all across the country on an equal footing. Based on the recommendations, NSE was promoted by leading Financial Institutions at the behest of the Government of India and was incorporated in November 1992 as a tax-paying company unlike other stock exchanges in the country. On its recognition as a stock exchange under the Securities Contracts (Regulation) Act, 1956 in April 1993, NSE commenced operations in the Wholesale Debt Market (WDM) segment in June 1994. The Capital Market (Equities) segment commenced operations in November 1994 and operations in Derivatives segment commenced in June 2000.

NSE's mission is setting the agenda for change in the securities markets in India. The NSE was set-up with the following objectives:

1 establishing a nation-wide trading facility for equities, debt instruments and hybrids,

2 ensuring equal access to investors all over the country through an appropriate communication network,

3 providing a fair, efficient and transparent securities market to investors using electronic trading systems,

4 enabling shorter settlement cycles and book entry settlements systems, and

5 meeting the current international standards of

securities markets.

One of the objectives of NSE was to provide a nationwide trading facility and to enable investors spread all over the country to have an equal access to NSE. NSE has made it possible for an investor to access the same market and order book, irrespective of location, at the same price and at the same cost. NSE has been promoted by leading financial institutions, banks, insurance companies and other financial intermediaries

Trading schedule

Trading on the equities segment takes place on all days of the week (except Saturdays and Sundays and holidays declared by the Exchange

in advance). The market timings of the equities segment are:

1. Pre-open session

Order entry & modification Open: 09:00 hrsOrder entry & modification Close: 09:08 hrs**with random closure in last one minute.

Pre-open order matching starts immediately after close of pre-open order entry.

2. Regular trading session

Normal/Retail Debt/Limited Physical Market Open: 09:15 hrsNormal/Retail Debt/Limited Physical Market Close: 15:30 hrsBlock deal session is held between 09:15 hrs and 09:50 hrs.

3. The Closing Session is held

between 15.40 hrs and 16.00 hrs.

The Exchange may however close the market on days other than the above schedule holidays or may open the market on days originally declared as holidays. The Exchange may also extend, advance or reduce trading hours when it deems fit and necessary.

SENSEX

An abbreviation of the Bombay Exchange Sensitive Index (Sensex) - the benchmark index of the Bombay Stock Exchange (BSE). It is composed of 30 of the largest and most actively-traded stocks on the BSE. Initially compiled in 1986, the Sensex is the oldest stock index in India.

Method for Calculation of Sensex

The method adopted for calculating Sensex is the market capitalization weighted method in which weights are assigned according to the size of the company. Larger the size, higher the weight age.

The base year chosen for calculation of sensex is 1978-79 and the base index value is set to 100 for this period.

The total value of shares in the market at the time of index construction is assumed to be ’100′ in terms of ‘points’. This is for the purpose of ease of calculation and to logically represent the change in terms of percentage. So, next day, if the market capitalization moves up 10%, the index also moves 10% to 110.

The stocks are selected based on a lot of qualitative and quantitative criteria’s.

The construction technique of index is quite easy to understand if we assume that there is only one stock in the market. In that case, the base value is set to 100 and let’s assumes that the stock is currently trading at 200. Tomorrow the price hits 260 (30% increase in price) so, the index will move from 100 to 130 to indicate that 30% growth. Now let’s assume that on day 3, the stock finishes at 208. That’s a 20% fall from 260. So, to indicate that fall, the Sensex will be corrected from 130 to 104(20%fall).

CNX NIFTY

CNX stands for the Credit Rating Information Services of India

Limited (CRISIL) and the National Stock Exchange of India (NSE). These two bodies own and manage the index within a joint venture called the India Index Services and Products Ltd. (IISL). Without the additional abbreviation to S&P CNX, the index name would be S&P CRISIL NSE Index.

Quick Clearing and Settlement

NSE has introduced a full range of clearing house facilities; a pan of securities is processed at the regional clearing centers (Delhi, Chennai and Calcutta). The inter region clearing facility provided at present, reduced that risk of the members because of not getting timely delivery of shares or loss of shares in transit. The facility is also expected to boost delivery based trading.

So the nifty index is a bit broader than the Sensex which is constructed using 30 actively traded stocks in the BSE.

Nifty is calculated using the same methodology adopted by the BSE in calculating the Sensex – but with three differences. They are:

The base year is taken as 1995 The base value is set to 1000 Nifty is calculated on 50 stocks actively traded in the NSE 50 top stocks are selected from 23 sectors.The selection criteria for the 50 stocks are also similar to the methodology adopted by the Bombay stock exchange.

IPO PROCESS

Conditions

1. Net Asset of Rs. 3 crore in each preceding year.

2. Distribution Profit at least 3 out of 5 preceding year.

3. Networth of 1 crore in preceding 3 years.

4. Issue size less than 5 times of pre issue.

The IPO process in India consists of the following steps: -

1) Appointment of merchant banker and other intermediaries

2) Registration of offer

document

3) Marketing of the issue

4) Post- issue activities

5) Appointment of Merchant Banker and Other Intermediaries

One of the crucial steps for successful implementation of the IPO is the appointment of a merchant banker. A merchant banker should have a valid SEBI registration to be eligible for appointment.

A merchant banker can be any of the following – lead manager, co-manager, underwriter or advisor to the issue. Certain guidelines are laid down in Section 30 of the SEBI Act, 1992 on the maximum limits of intermediaries associated with the issue:

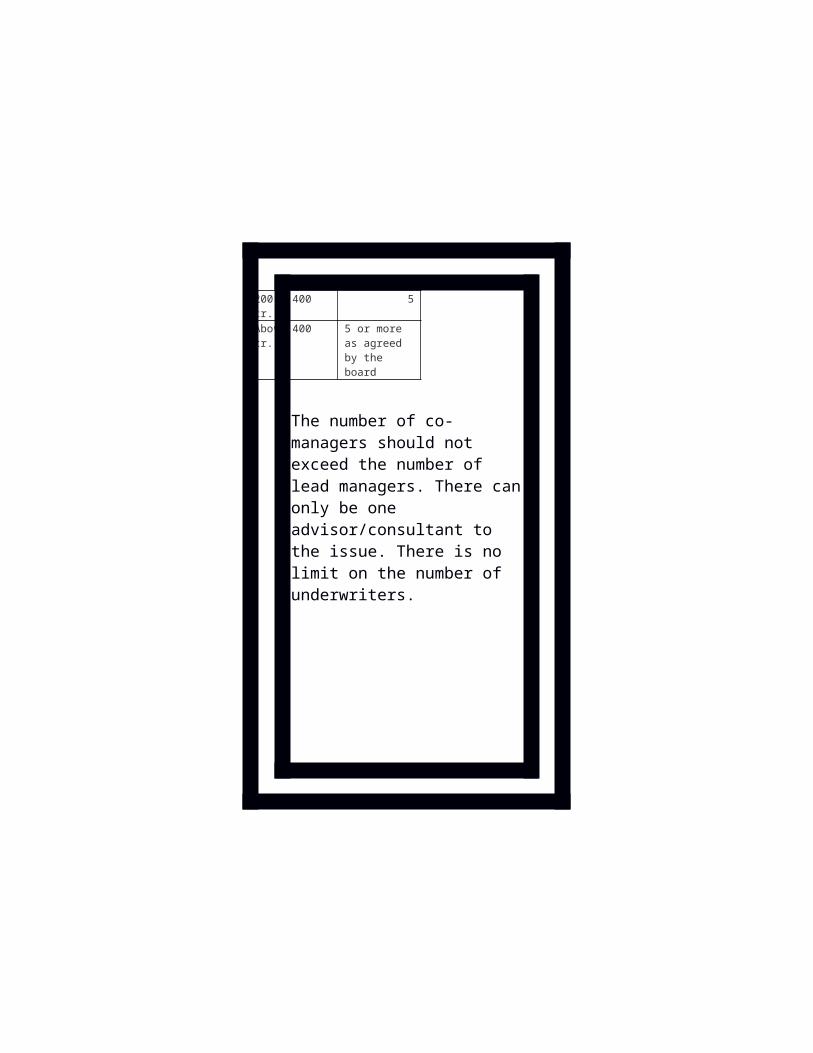

Size of the Is-sue

No. Of lead Managers

50 cr. 2

50 – 100 cr. 3

100 – 200 cr. 4

200 - 400 cr. 5

Above 400 cr. 5 or more as agreed by the board

The number of co- managers should not exceed the number of lead managers. There can only be one advisor/consultant to the issue. There is no limit on the number of underwriters.

Other Intermediaries

Registrar to the Issue:

Registration with SEBI is mandatory to take on responsibilities as a registrar and share transfer agent. The registrar provides administrative support to the issue process. The registrar of the issue assists in everything from helping the lead manager in the selection of Bankers to the Issue and the Collection Centres to preparing the allotment and application forms, collection of application and allotment money, reconciliation of bank accounts with application money, listing of issues and grievance handling.

Bankers to the Issue:

Any scheduled bank registered with SEBI can be appointed as the banker to the issue. There are no

restrictions on the number of bankers to the issue. The main functions of bankers involve collection of application forms with money, maintaining a daily report , transferring the proceeds to the share application money account maintained by the controlling branch, and forwarding the money collected with the application forms to the registrar.

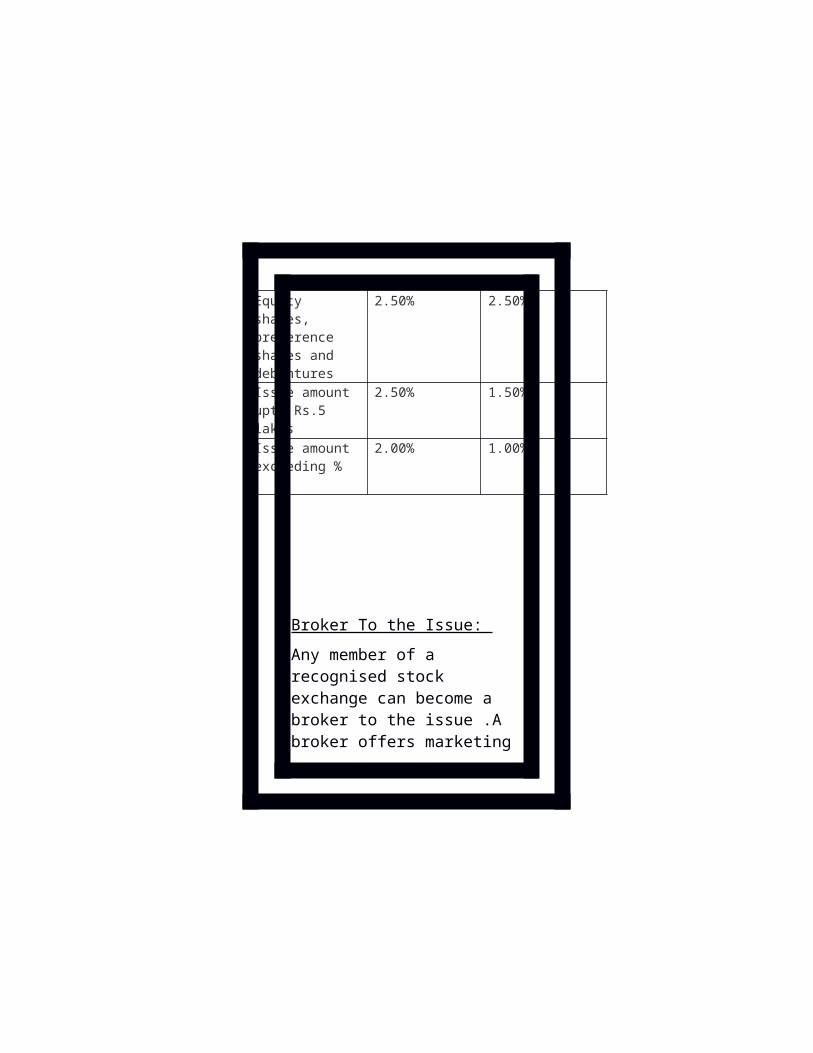

Underwriters to the Issue:

Underwriting involves a commitment from the underwriter to subscribe to the shares of a particular company to the extent it is under subscribed by the public or existing shareholders of the corporate. An underwriter should have a minimum net worth of 20 lakhs, and his total obligation at any time should not exceed 20 times the underwriter’s net worth. A

commission is paid to the writers on the issue price for undertaking the risk of under subscription.

The maximum rate of underwriting commission paid is as follows:

Nature of Issue On amount Devolving On Underwriters

On amounts subscribed by public

Equity shares, preference shares and debentures

2.50% 2.50%

Issue amount upto Rs.5 lakhs

2.50% 1.50%

Issue amount exceeding %

2.00% 1.00%

Broker To the Issue:

Any member of a recognised stock exchange can become a broker to the issue .A broker offers marketing support, underwriting support, disseminates information to investors about the issue and distributes issue stationery at retail investor level.

Registration Of The Offer Document

For registration,10 copies of the draft prospectus should be filed with SEBI. The draft prospectus filed is treated as a public document. The lead manger also files the document with all listed stock exchanges. Similarly, SEBI uploads the document on its website www.sebi.com. Any amendments to be made in the prospectus should be done within 21days of filing the

offer document. Thereafter the offer document is deemed to have been cleared by SEBI.

Promoters Contribution:

In the public issue of an unlisted company, the promoters shall contribute not less than 20% of the post issue capital as given in Chapter- IV of the SEBI Act, 1992.The entire contribution should have been made before theopening of the issue.

Lock-in Requirement

The minimum promoters contribution will be locked in for a period of 3 years. The lock-in period commences from the date of allotment or from the date of commencement of commercial production, whichever is earlier.

Marketing of the Issue

• Timing of the Issue

• Retail distribution

• Reservation of the Issue

• Advertising Campaign

Timing of the Issue

An appropriate decision regarding the timing of the IPO should be made, keeping in mind the general sentiments prevailing in the investor market. For example, if recession is prevailing in the economy (the investors are pessimistic in their approach), then the firm will not be able to get a good pricing for its IPO, as investors may not be willing to put their money in stocks.

Retail distribution:

Retail distribution is the process through which an attempt is made to increase the subscription. Normally, a network of brokers undertakes retail distribution. The issuer company organises road shows in which conferences are held, which are attended by high networth investors, brokers and sub-brokers. The company makes presentations and solves queries raised by participants. This is one of the best ways to raise subscription.

Reservation in the Issue

Sometimes reservations are tailored to a specific class of investors. This reduces the amount to be issued to the general public. The following are the classes of investors for whom reservations are made:

• Mutual Funds

• Banks and Financial Institutions; Non-resident Indians (NRI) and Overseas Corporate Bodies (OCB) The total reservation for NRI/OCB should not exceed 10% of the post-issue capital, and individually it should not exceed 5% of the post issue capital.

• Foreign Institutional Investors (FII): The total reservation for FII cannot exceed 10% of the post-issue capital, and individually it should not exceed 5% of the post issue capital.

• Employees: Reservation under this category should not exceed 10% of the post issue capital.

• Group Shareholders: Reservation in this category should not exceed 10% of the post issue capital. The net offer made to the public should not be less then the 25% of the total issue at any point of time.

Post-Issue Activities

• Principles of Allotment: After the closure of the subscription list, the merchant banker should inform, within 3 days of the closure, whether 90% of the amount has been subscribed or not. If it is not subscribed up to 90%, then the underwriters should bring the shortfall amount within 60 days. In case of over subscription, the shares should be allotted on a pro-rata basis, and the excess amount should be refunded with interest to the shares holders within 30 days from the date of closure.

• Formalities Associated With Listing:

The SEBI lists certain rules and regulations to be followed by the issuing company. These rules and

regulations are laid down to protect the interests of investors. The issuing company should disclose to the public its profit and loss account, balance sheet, information relating to bonus and rights issue and any other relevant information.

SEBI

Securities Exchange Board of India (SEBI) was set up in 1988 to regulate the functions of securities market. SEBI promotes orderly and healthy development in the stock market but initially SEBI was not able to exercise complete control over the stock market transactions. It was left as a watch dog to observe

the activities but was found ineffective in regulating and controlling them. As a result in May 1992, SEBI was granted legal status. SEBI is a body corporate having a separate legal existence and perpetual succession.

Reasons for Establishment of SEBI:

With the growth in the dealings of stock markets, lot of malpractices also started in stock markets such as price rigging, ‘unofficial premium on new issue, and delay in delivery of shares, violation of rules and regulations of stock exchange and listing requirements. Due to these malpractices the customers started losing confidence and faith in the stock exchange. So government of India decided to set up an agency or

regulatory body known as Securities Exchange Board of India (SEBI).

Purpose and Role of SEBI:

SEBI was set up with the main purpose of keeping a check on malpractices and protect the interest of investors. It was set up to meet the needs of three groups.

1. Issuers:

For issuers it provides a market place in which they can raise finance fairly and easily.

2. Investors:

For investors it provides protection and supply of accurate and correct information.

3. Intermediaries:

For intermediaries it provides a

competitive professional market.

Objectives of SEBI:

The overall objectives of SEBI are to protect the interest of investors and to promote the development of stock exchange and to regulate the activities of stock market. The objectives of SEBI are:

1. To regulate the activities of stock exchange.

2. To protect the rights of investors and ensuring safety to their investment.

3. To prevent fraudulent and malpractices by having balance between self regulation of business and its statutory regulations.

4. To regulate and develop a code of conduct for intermediaries such as

brokers, underwriters, etc.

P/E Ratio

P.E ratio ( price to earning ratio ) is one of the most important and common stock valuation ratio. It is a ratio of company’s current market share price compared to its annual earning per share.

Example-

Suppose a company is trading at 500. It’s earning per share is 10 for the last 12 months then it’s P.E ratio will be 50(500/10) Generally earning per share is calculated for last 12 months so this ratio is often called trailing P.E ratio

Significance of price to earning ratio

Price to earning ratio indicates how cheaper or expensive a stock is. If P.E ratio of a stock is 10 then it

tells that investors are willing to pay 10 times of company’s earning to buy that stock.

Stocks with P.E ratio less than 10 are quite cheaper.These types of stocks often provide a good opportunity for buying. High Price to earning ratio indicates that investors are expecting high earning growth in future. But while investing don’t consider P.E ratio as a standalone parameter.

If all other things remain same then a 500 stock with P.E ratio 12 is cheaper than a 20 stock with P.E ratio 18.

FACTORS TO LOOK FOR BEFORE BUYING STOCK

Management

Project Undertaken

Goodwill

Past Performance

Debt Level

Dividend Declared

P/E Ratio

Volume Traded/Deliverable Quantity

Reasons For or Advantages in Investing In equity

High Intraday Margin

High Return

High Liquidity

Direct Investment

Charges (easy)

Tax Benefits

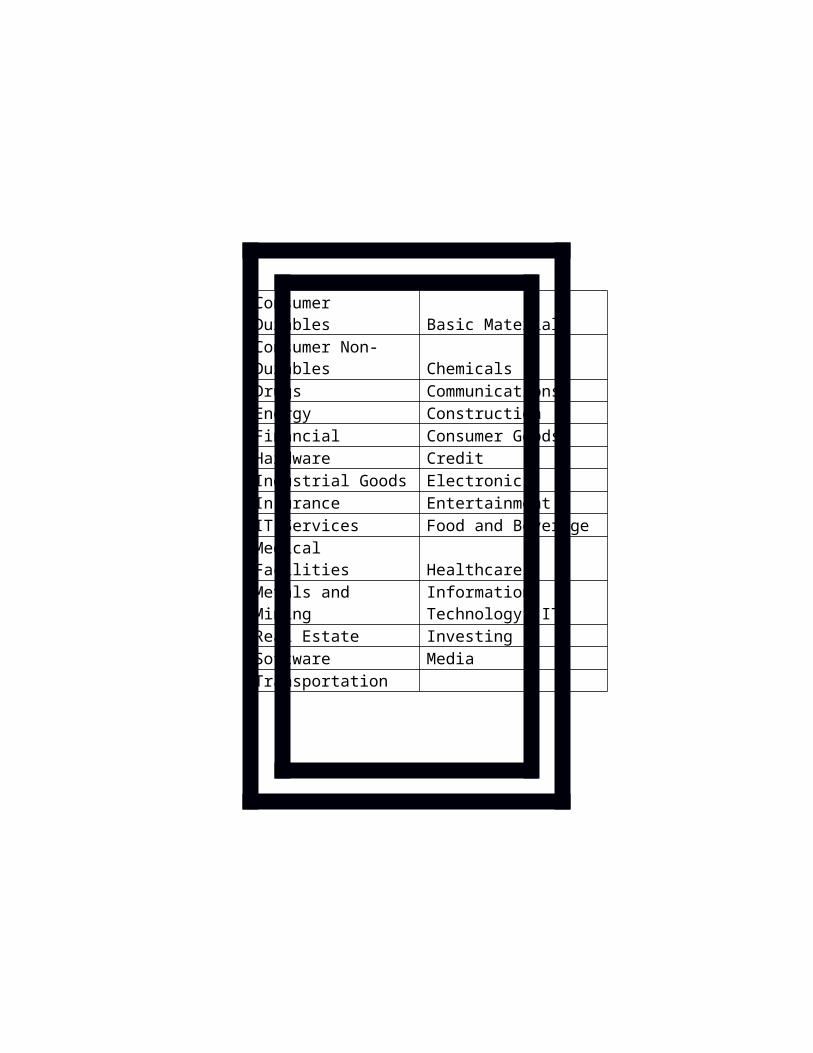

Sectors

Banking ServicesCapital Goods TechnologyClothing UtilitiesConglomerates AgricultureConsumer Durables Basic MaterialsConsumer Non-Durables ChemicalsDrugs CommunicationsEnergy ConstructionFinancial Consumer GoodsHardware CreditIndustrial Goods ElectronicsInsurance EntertainmentIT Services Food and BeverageMedical Facilities Healthcare

Metals and MiningInformation Technology (IT)

Real Estate InvestingSoftware MediaTransportation

FUNDAMENTAL ANALYSIS

Fundamental analysis is the examination of the underlying forces that affect the well being of the economy, industry groups and companies. As with most analysis, the goal is to develop a forecast of future price movement and profit from it. At the company level, fundamental analysis may involve examination of financial data, management, business concept and competition. At the industry level, there might be an examination of supply and demand forces of the

products.

Some of the Fundamental factors that should be kept in mind while analyzing the company that will help in deciding whether to invest in that company or not, are as follows:-

Market overview Market capitalization Goodwill Past performance Future prospect Management Dividend distribution Attrition rate

THREE PHASES OF FUNDAMENTAL ANALYSIS

1) Understanding of the macro-economic environment and developments (Economic

Analysis)

2) Analyzing the prospects of the industry to which the firm belongs (Industry Analysis)

3) Assessing the projected performance of the company (Company Analysis)

This three phase examination of fundamental analysis is also called EIC(Economy-Industry-Company Analysis) framework or a top-down approach.

Here the financial analyst first makes forecasts for the economy, then for industries and finally for companies. The industry forecasts are based on the forecasts for the economy and in turn, the company forecasts are based on the forecasts for both the industry and the economy. Also in this approach, industry groups are compared

against other industry groups and companies against other companies. Usually, companies are compared with others in the same group.For example, a telecom operator (Spice) would be compared to another telecom operator not to an oil company.

TECHNICAL ANALYSIS

Technical analysis takes a completely different approach; it doesn't care one bit about the "value" of a company or a commodity.

Technicians are only interested in the price movements in the market. Technical Analysis is the forecasting of future financial price movements based on an examination of past price movements.

Following are some technical factors that should be studied:-

Charts Ratio Resistance & Support

ASSUMPTIONS OF TECHNICAL ANALYSIS

The market value of a security is solely determined by the interaction of demand and supply factors operating in the market.

The demand and supply factors of a security are surrounded by numerous factors; these factors are

both rational as well as irrational.

The security prices move in trends or waves which can be both upward or downward depending upon the sentiments, psychology and emotions of operators or traders.

The present trends are influenced by the past trends and the projection of future trends is possible by an analysis of past price trends.

Except minor variations, stock prices tend to move in trends which continue to persist for an appreciable length of time.

Changes in trends in stock prices are caused whenever there is a shift in the demand and supply factors.

TOOLS IN TECHNICAL ANALYSIS

Line charts

Point and Figure Chart

Bar Graph

Candle Stick Chart

Line Chart with Volume

Moving Average

Line Chart

A chart that shows a security’s price over a period of time, such as a day, a month, or a year. A linechart is con-structed by placing points representing the price at different points in time, and then connecting the pointswith lines. It is useful in showing a security's trend over time. However, it does nothing to indicate the security's high, low,open, or close.

Point And Figure Chart

A chart pattern, peculiar to securities, in which only the significant value changes of a security, a futures contract, or a market average are recorded. The vertical axis represents price, but, unlike nearly all other charts, no variable, including time, is plotted on the horizontal axis. Entries on a point-and figure chart are made onlywhen a variable changes by a predetermined amount, for example, by one point or twopoints. A period of days may pass before an entry is recorded. Point and figure (P&F) is a charting technique used in technical analysis. Point and figure charting is unique in that it does not plot price against time as all other techniques do. Instead it plots price against changes in direction by

plotting a column of Xs as the price rises and a column of Os as the price falls.

Bar Chart

A style of chart used by

some technical analysts, on which, as illustrated below, the top of the vertical line indicates the highest price a security traded at during the day, and the bottom represents the lowest price. The closing price is displayed on the right side of the bar, and the opening price is shown on the left side of the bar. A single bar like the one below represents one day of trading.

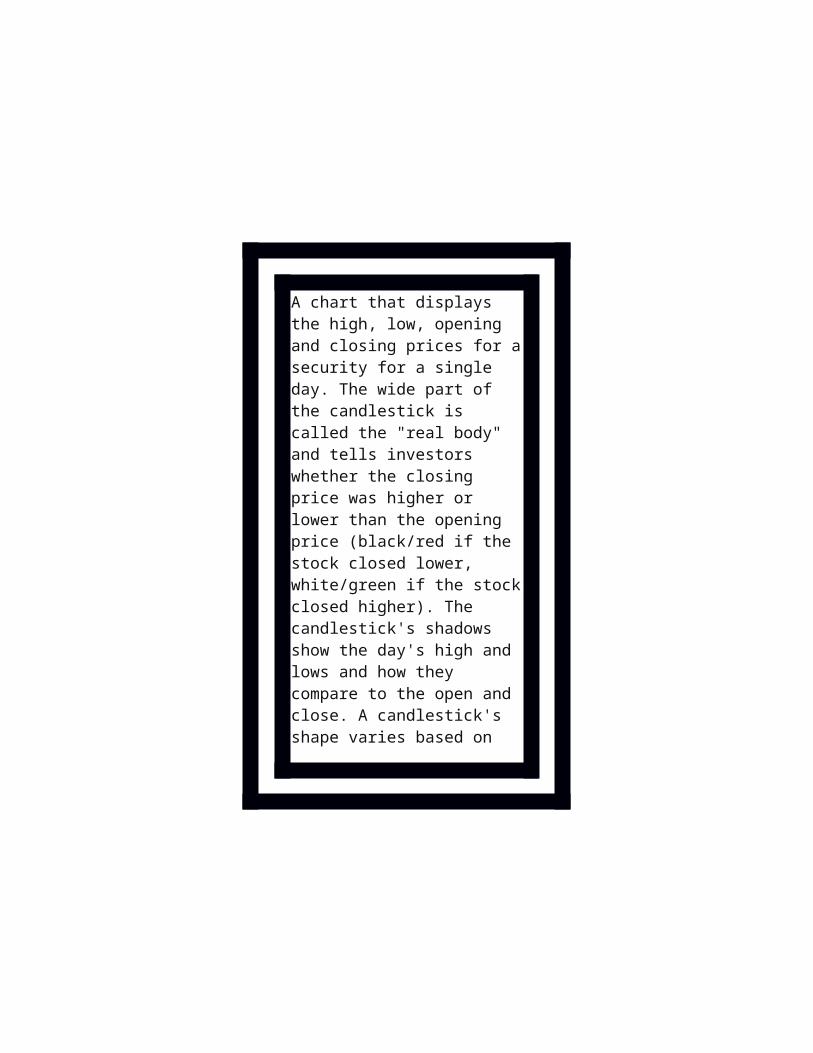

Candle Stick Chart

A chart that displays the

high, low, opening and closing prices for a security for a single day. The wide part of the candlestick is called the "real body" and tells investors whether the closing price was higher or lower than the opening price (black/red if the stock closed lower, white/green if the stock closed higher). The candlestick's shadows show the day's high and lows and how they compare to the open and close. A candlestick's shape varies based on the relationship between the day's high, low, opening and closing prices.

Line Chart With Volume

There are many different types of stock charts: line, bar, OHLC (open-high-low-close), candlestick, mountain, point-and-figure, and others, which are viewable in different time frames: most commonly, daily, weekly, monthly, and intraday charts. Each style and time frame has its advantages and disadvantages, but they all reveal valuable price and volume information that you can use to

make profitable investing decisions

Moving Average

Moving averages are plotted on stock charts to help smooth out volatility and point out the direction a stock may be trending. It may also help provide context for the price or volume movements during a given period as it makes it easier to spot divergences from an established price trend. The red line cutting through the price bars is the 50-day moving average. It represents the average price over the previous 50 trading sessions and is calculated by summing the closing price over the last 50 trading sessions and dividing by 50. The black line is the 200-day moving average. It represents the average price over the previous 200 trading sessions and is calculated by summing the closing price over the

last 200 trading sessions and divid-ing by 200.

MARKET CAPITALIZATION

When understanding how to allocate funds for investing in equities, it is important to understand both your expectation of return and also your risk appetite. Once you are clear on these, it will be a lot easier for you to allocate money between the various categories of stocks.

There are three main classifications when it comes to stocks -

Large Cap stocks;

Mid Cap stocks; and

Small Cap stocks.

Here, the term 'cap' simply refers to the 'market capitalisation' of the stock.

And what is market capitalisation?

It is the value of the stock that you arrive at by multiplying the stock price by the company's outstanding number of equity shares.

Market Capitalisation = Current Stock Price x Number of Shares outstanding

For a better understanding, let us see an example:

Company XYZ has 10,000,000 shares outstanding and its current share price is Rs 8. Based on the above formula, we can calculate that Company XYZ's market

capitalisation is Rs 8 crore, or 1,00,00,000 shares x Rs 8 per share.

Market capitalization is the aggregate valuation of the company based on its current share price and the total number of outstanding stocks.

Definition: Market capitalization is the aggregate valuation of the company based on its current share price and the total number of outstanding stocks. It is calculated by multiplying the current market price of the company's share with the total outstanding shares of the company.

Description: Market capitalization is one of the most important characteristics that helps the investor determine the returns and the risk in the share. It also helps

the investors choose the stock that can meet their risk and diversification criterion.

For instance, a company has 2 crore outstanding shares and the current market price of each share is Rs100. Market capitalization of this company will be 200,00,000 x 100=Rs 200 crore.

Stocks of companies are of three types. The stocks with a market cap of Rs 10,000 crore or more are large cap stocks. Company stocks with a market cap between Rs 2 crore and 10 crore are mid cap stocks and those less than Rs 2 crore market cap are small cap stocks.

STOCK, SECTOR, SENSEX MOVEMENT

Movement In Stocks

Movement of a particular stock depends upon the following things:

Weightage of that particular company in its sector.

P/E Ratio of that company Any good/bad news relating

that company or its sector Good financial results of a

particular company. Movement of other

companies’ stocks in that sector.

Fundamental factors of that company.

Sector movement

Sector movements can be caused when

Stocks ( for eg. I.T stocks) can move the sector I.e internal.

External factors

economy

government laws

currency depreciation (exchange rate fluctuations)

If P.E ratio is less than 10 then it can move the market. Companies with high demand of shares their P.E ratio will also be high.

An another reason for sector movements is that when FII

's invest money into the market it causes sector movements and on the vice versa when they withdraw their money from the market like in the month of July when it is their year end the markets becomes slow.

FII's cause more sector movements than the DII's.

The major sectors in SENSEX are I.T sector, Banking sector, Oil and Gas sector, Steel sector, FMCG sector. When exchange rate changes it affects two sectors namely oil and gas and the I.T sector. Each sector has certain weightage or impact on the SENSEX. There can be certain external factors that can affect only 1 sector solely.

Bank and finance sectors have the highest weightage in SENSEX, so when the external factor that is when RBI changes its interest rates (repo and reverse repo rates) it can pull down the finance or bank sector which can affect the sector movements and in turn result in the fall of NIFTY or SENSEX.

Movement in SENSEX

Movement of SENSEX depends upon the following factors:

External factors affecting two or more sectors and their weightage in SENSEX

Movement of one sector

having a high weightage can move other sectors with it, which in turn will cause the movement of the SENSEX

CIRCUIT:-

Circuit is the maximum percentage change allowed in the share price in a particular day. The circuit is a upper and lower limit beyond which the trading is not allowed. Different stocks have different circuit limits. Usually they are 5%, 10% and 20%.

There are two types of circuits: 1. Buyer Circuit or Upper Circuits and 2. Seller circuit or lower circuit.

The purpose of circuit is to regulate the price and prevent any malpractise by traders or brokers/oprators. If the shares are traded in the options market also then there will not be any restrictions like the circuit breakers for the shares.

WHAT HAPPENS TO ORDERS DURING CIRCUIT LIMITS?

If the market hits the upper or lower circuits, trading is halted and you cannot place orders until the market re-opensIf you have pending orders with the broker at the time of circuit break, such orders can be modified or cancelled only once the trading re-opens.

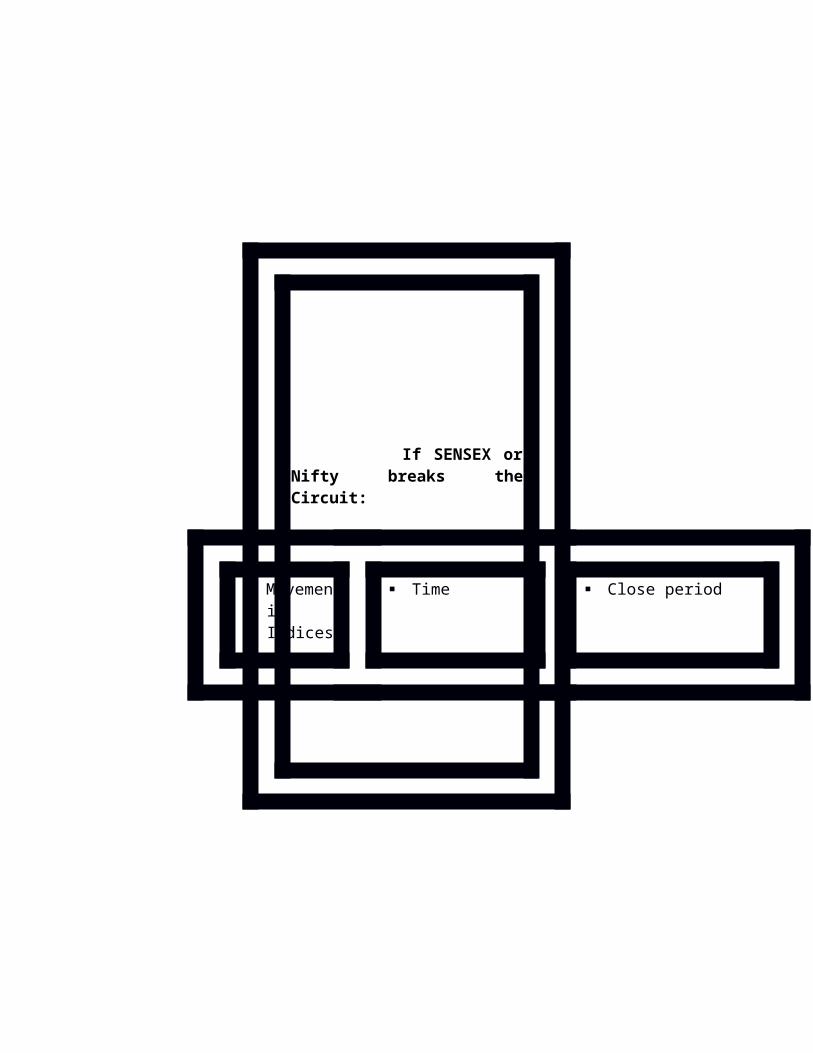

If SENSEX or Nifty breaks the Circuit:

Movement in Indices

Time Close period

10 per cent Before 1.00 pm 1 hour

1.00 pm to 2.30 pm ½ hour

After 2.30 pm Does not close

15 per cent Before 1.00 pm 2 hour

1.00 pm to 2.30 pm 1 hour

After 2.30 pm Close for the rest of the day

20 per cent Any time Close for the rest of the day

RESISTANCE & SUPPORT:-Support and resistance is a concept in technical analysis that the movement of the price of a security will tend to stop and reverse at certain predetermined price levels.

A support level is a price level where the price tends to find support as it is going down. This means the price is more likely to "bounce" off this level rather than break through it. However, once the price has passed this level, by an

amount exceeding some noise, it is likely to continue dropping until it finds another support level.A resistance level is the opposite of a support level. It is where the price tends to find resistance as it is going up. This means the price is more likely to "bounce" off this level rather than break through it. However, once the price has passed this level, by an amount exceeding some noise, it is likely that it will continue rising until it finds another resistance level.Support and resistance levels can be identified by trend lines (technical analysis). Some traders believe in using pivot point calculations.The more often a support/resistance level is "tested" (touched and bounced off by price), the more significance given to that specific level.

If a price breaks past a support level, that support level often

becomes a new resistance level. The opposite is true as well, if price breaks a resistance level, it will often find support at that level in the future.

The Importance of Support and Resistance

Support and resistance analysis is an important part of trends because it can be used to make trading decisions and identify when a trend is reversing. For example, if a trader identifies an important level of resistance that has been tested several times but never broken, he or she may decide to take profits as the security moves toward this point because it is unlikely that it will move past this level.

Support and resistance levels both test and confirm trends and need to be monitored by anyone who uses

technical analysis. As long as the price of the share remains between these levels of support and resistance, the trend is likely to continue. It is important to note, however, that a break beyond a level of support or resistance does not always have to be a reversal. For example, if prices moved above the resistance levels of an upward trending channel, the trend has accelerated, not reversed. This means that the price appreciation is expected to be faster than it was in the channel.

Being aware of these important support and resistance points should affect the way that you trade a stock. Traders should avoid placing orders at these major points, as the area around them is usually marked by a lot of volatility. If you feel confident about making a trade near a support or resistance level, it is

important that you follow this simple rule: do not place orders directly at the support or resistance level. This is because in many cases, the price never actually reaches the whole number, but flirts with it instead. So if you're bullish on a stock that is moving toward an important support level, do not place the trade at the support level. Instead, place it above the support level, but within a few points. On the other hand, if you are placing stops or short selling, set up your trade price at or below the level of support.

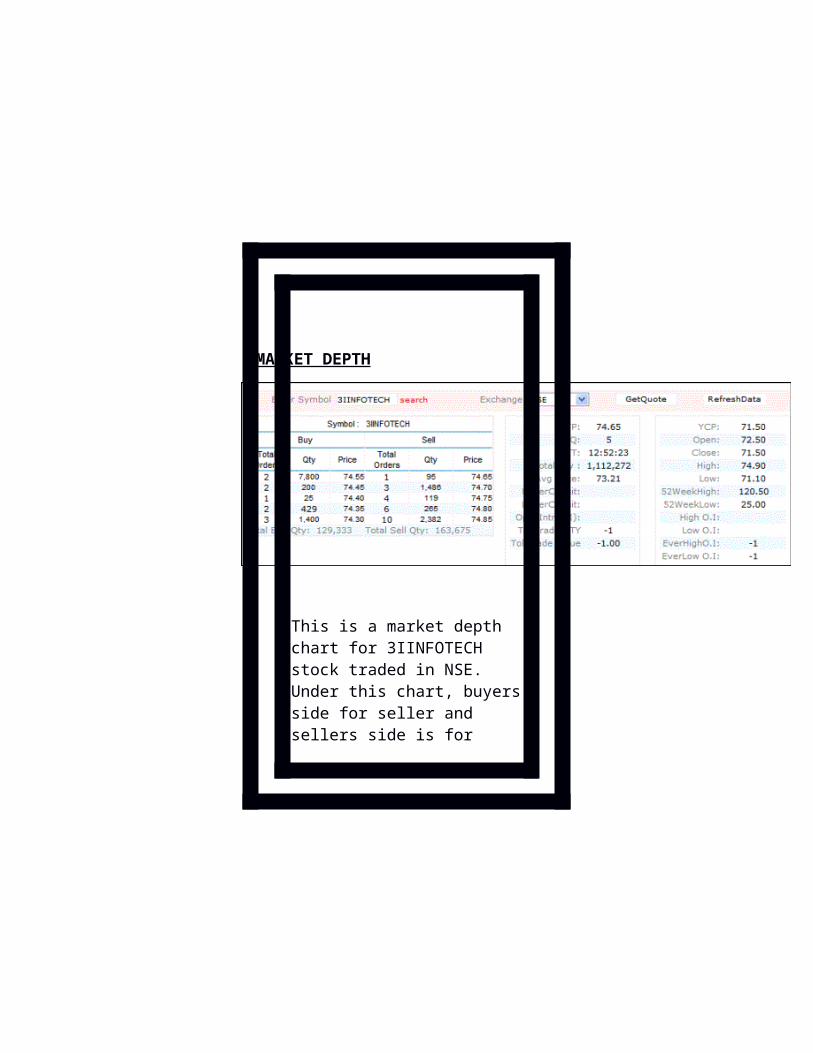

INTRADAY AND DELIVERY TRADING:-

Intraday

Intraday trading refers to the practice of buying and selling financial instruments within the same trading day such that all positions will usually but not necessarily always be closed before the market close of the trading day that is from 9.15am to 3.07pm.

If an intraday trader is suffering loss and he feels tomorrow that particular stock will give him profit than if he can convert thr trade in T+5 days upto the money he has in his account. And if he has no cash in his account than company allows/gives margins upto 2 times to settle in 5 days.

In Intraday Trading,

company provides the trader with some amount of margin in addition to his initial margin to trade in the market

Intraday Trading involves taking a position in the markets with a view of squaring that position before the end of that day.

A day trader typically trades several times a day looking for fractions of a point to a few points per trade, but who close out all their positions by day's end.

The goal of a day trader is to capitalize on price movement within one trading day.

Unlike investors, a day

trader may hold positions for only a few seconds or minutes, and never overnight

This Intraday margin differs with the company. Karvy provides a trader with 10 times of his initial margin. For example, a trader has initial margin of Rs.50, 000, Karvy will allow him to take position for stock of worth Rs.5,00,000 for trading in Intraday.

The brokerage charged by Karvy in Intraday trading is 0.05% which is very low as compared to the delivery brokerage rates.

Why was Intraday Trading Introduced?

Intraday trading was introduced to increase the volume in the market.

Because where a trader was buying 100 stocks due to his limited margin, now he will be able to buy 1000 stocks because of his new margin (which is 10 times of his initial margin). Also the Brokerage amount is less in Intraday Trading as there is no procedure to hold the stocks for more than a day.

Increase the risk appetite of customers

Benefit to brokers as they will now receive brokerage on sale of 1000 shares

instead of 100 shares

Encourages the customers to trade as it serves as extra income apart from the income from business or salaried jobs.

Advantages Of Intraday Trading

In day trading you can buy stocks without paying for the full price of the stocks. The market makers allow you pay only a part of the price to hold the shares. So, you can gain more by investing less.

In day trading you can always short sell the stocks that means you can always sell the stocks before buying

them and then buy the stocks before the closing of the market. This is one benefit that can give you profit even when the price of the stock is sure to fall.

The brokerage of the intraday trading is always lower than the delivery trading.

In day trading you are getting the profit on the very day. So, you investment is for a few hours only. Therefore, even if the stock price rises, a little your profit percentage is significant.

You get back the money each day after the market closes and hence you can

always start afresh the next morning.

Disadvantages Of Intraday Trading:-

The biggest disadvantage of intraday trading is the time frame. You have to sell the stocks within a day. So, if the stock loses price you are sure to lose money.

Short Sell:-

Short selling is the selling of a stock that the seller doesn't own. More specifically, a short sale is the sale of a security that isn't owned by

the seller, but that is promised to be delivered.

The short seller was introduced because investor were not willing to invest in bearish market. First they used to wait for the market/stock price to come down and then they bought shares which reduced the volume of shares being traded. So this helped in motivating investors to earn even when the market is bearish.

For example, if a person A wants to buy 100 stocks of XYZ ltd, and B knows that the price of this stock will go down, then he will sell these 100 stocks to A virtually and after selling the stocks he must buy the

stocks from another seller in the market and for this, he will look for a seller who is ready to sell the same quantity of stocks at a lower price. If B is able to find a seller who will sell the stocks at a lower price, then B will gain profit and if not then he will have to buy the stocks from the seller who might sell at a higher price, to complete the contract but he will incur loss.

PROFIT BOOKING (Short)

Buying back borrowed securities in order to close an open short position. Profit Booking refers to the purchase of the exact same

security at a lower price that was initially sold short. So the short-sale process involved borrowing the security and selling it in the market and thus book profit in market. This will bring the market down as cash is being etracted out of the market by booking profit.

From the above example, we can understand the concept of short covering. When B short 100 stocks at the rate of Rs.20 to A and he finds a seller at Rs.17 in the market for same quantity of stocks, then B will buy these stocks and deliver it to A to complete the contract and he will gain the profit of Re.3 per share, this is called Profit Booking.

For instance - let's say that a trader decided to short 1,000

shares of XYZ at Rs.30. The stock has weakened considerably since then, and is now trading for just Rs.25 per share. The trader decides to take his Rs.5,000 profit (5 points x Rs.1,000 per point). To do this, he must close out his position by purchasing 1,000 shares of XYZ shares in order to exit his short position. By purchasing the 1,000 shares of XYZ, the trader returns the borrowed shares and is now out of the position.

SHORT COVERING

This concept is more or less same as profut booking under short sell but there investors do not earn profit. In short they fail in their strategy badly and thus to avoid much loss, they start buying at higher rates and thus faces loss. This concept makes the maket bullish or to go higher as people's money or losses enter into the market.

DELIVERY TRADING

Delivery based trading is the most common form share trading done by most of the stock market investors throughout the world. In this type of trading the investors have to pay the full price of the stock and the stocks are

deposited in their Demat account. There is no predefined time limit in case of the delivery based trading for selling the stocks.

The brokerage charged by Karvy for trading in Delivery is 0.50%.

The brokerage charged in Delivery is more than that of Intraday because in Delivery you have to hold the stocks in Demat account, whereas in Intraday, you get the stocks virtually.

The settlement in Delivery trading is done on T+2 basis .i.e. when you buy or sell the stocks, then the settlement is done on the second day after the trade has been done.

When an investor buys a stock in Intraday, he can convert that stock in Delivery before the closure of the Intraday market which is at 3.07pm. If the stock is converted to Delivery from Intraday then the investor can hold the stock for T+5 days.

In Karvy, when the investor trades in Delivery, he is allowed to take the position of twice of its initial margin. For example, if the initial margin of a person is Rs.50,000 then he is allowed to take position of Rs.1,00,000 for trading in Delivery.

This additional margin provided by the company differs in various companies.

Advantages Of Delivery Trading

The biggest advantage of delivery based trading is that you are not bound with time for selling the stock. You can hold the stocks for as long as you want. So, you can always hold a stock until you are getting a significant profit from the investment. Therefore, with delivery based trading you can always take your time to take a decision and reduce the risk of losses.

When you are making a long term investment with delivery based trading, you can also benefit from other

things like dividends, split of stocks, bonus shares and so on. These are benefits that the companies offer to their shareholders from time to time and you can make significant profit from these offers if you are holding the stocks for long period.

In delivery trading, the ownership of the share lies with the person who has purchased the share because he purchases the share with his own money.

Disadvantages of Delivery Trading

The biggest disadvantage of delivery based trading is the higher brokerage rate. The

brokerage rate for delivery based trading is relatively higher than the intraday trading.

You have to pay the full price of the stock for delivery based trading, whereas; in case of intraday trading you can buy stocks by paying only a part of the stock price. So, in case of intraday trading you can buy more stocks by investing less.

In delivery based trading you can never benefit from short selling. That means you have to hold the shares before you actually sell them.

These are the benefits and

disadvantages of delivery based trading. Whether you invest through delivery based trading or not solely depends on your financial capacity and willingness to take risks.

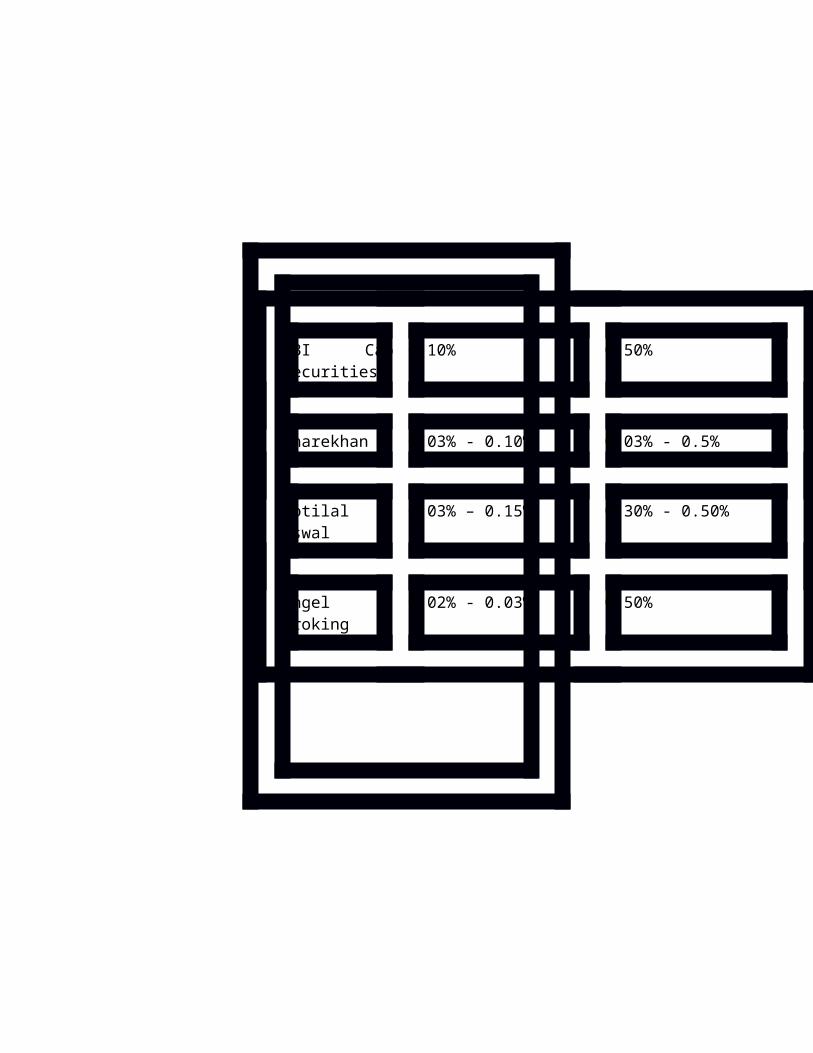

Brokerage Charges Of Different Broking Firms:-

Company Intraday charges Delivery charges

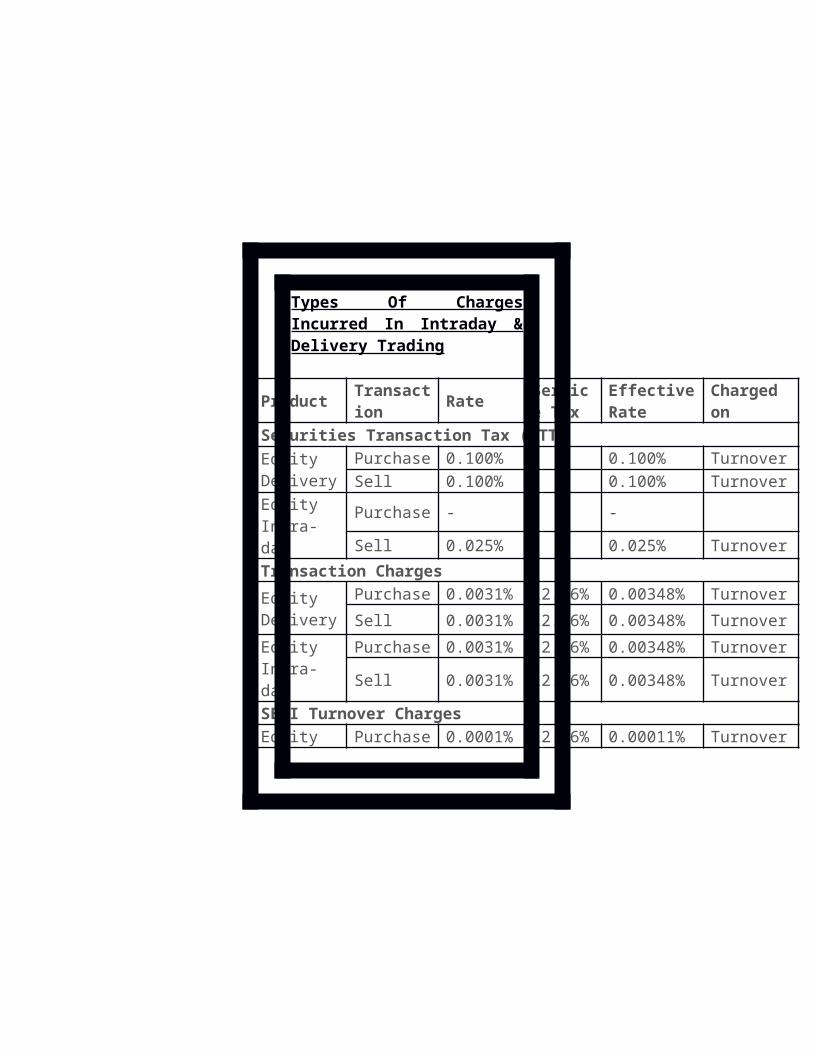

Types Of Charges Incurred In Intraday & Delivery Trading

ProductTransaction

RateService Tax

Effective Rate

Charged on

Securities Transaction Tax (STT)

Equity Delivery

Purchase 0.100% - 0.100% Turnover

Sell 0.100% - 0.100% Turnover

Equity Intra-day

Purchase - - -

Sell 0.025% - 0.025% TurnoverTransaction Charges

Equity Delivery

Purchase 0.0031% 12.36% 0.00348% Turnover

Sell 0.0031% 12.36% 0.00348% Turnover

Equity Intra-day