SaaS in NYC: 2015 Overview, Primary Venture Partners

20

1 SaaS in NYC June 2015

-

Upload

brad-svrluga -

Category

Software

-

view

4.058 -

download

3

Transcript of SaaS in NYC: 2015 Overview, Primary Venture Partners

1

SaaS in NYC

June 2015

2015-2025: The NYC SaaS Decade?

2

As the enterprise SaaS market continues to mature, and as we watch a blossoming of SaaS activity in New York City, we believe NYC is poised to become a true leader in the formation of companies leading the next wave of enterprise transformation, ultimately challenging even the Bay Area for SaaS leadership. Primary Venture Partners took a deep look at the existing NYC SaaS landscape, seeking a clear understanding of the reality behind our anecdotal sense of our home market’s strengths. What we found is exciting and bodes awfully well for Primary and our friends who are focused on NYC SaaS investing. There is much more to come! Key Findings: 9 SaaS company formation and investing has been rapidly accelerating in recent years,

and growing much more quickly than in the Bay Area

9 We’ve already seen a bunch of early exit successes, but with a growing pipeline of extremely well-funded, high growth successes, we can expect many, many more

9 NYC is particularly well positioned to lead as vertical SaaS applications continue to grow in importance vs. the historic horizontal paradigm

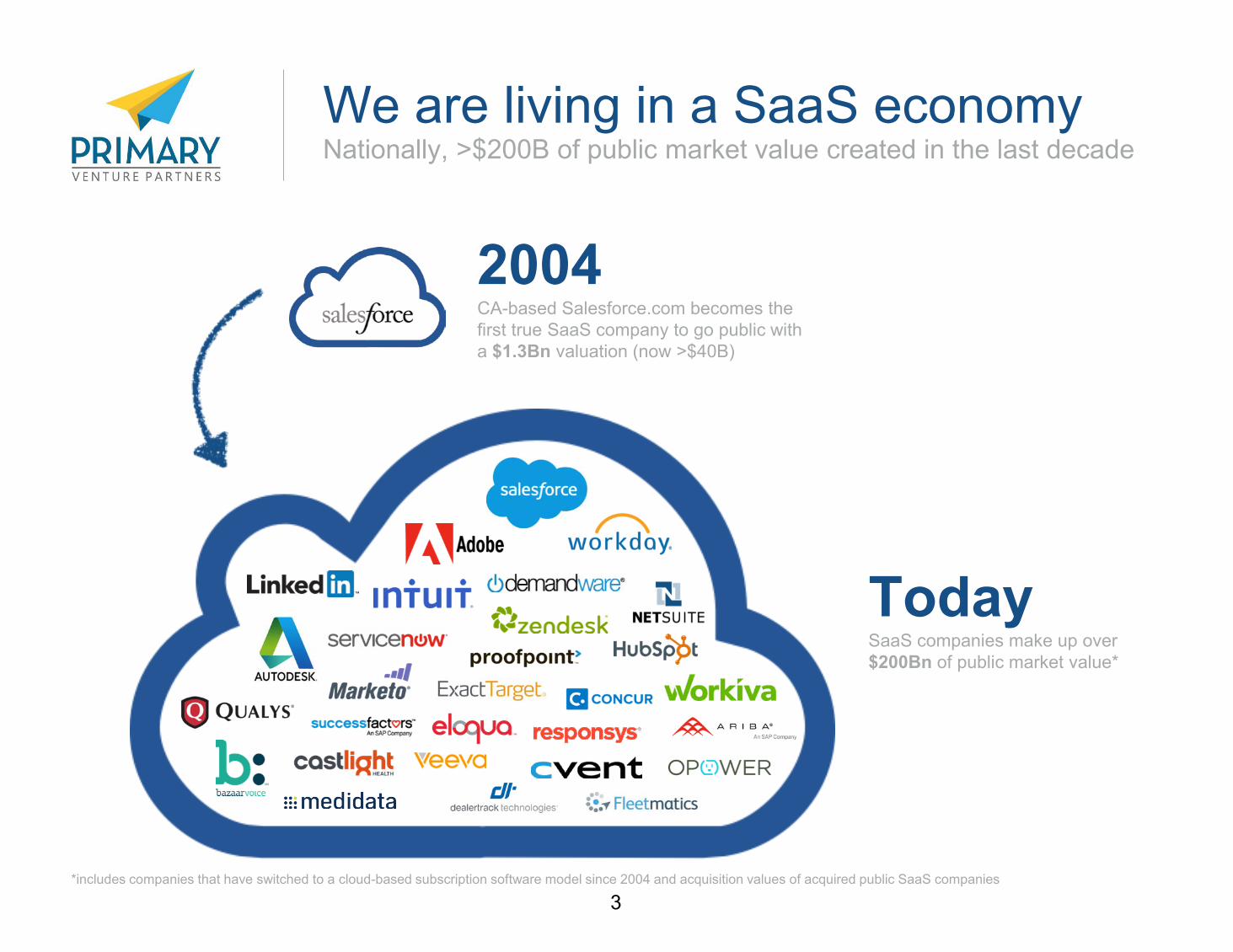

We are living in a SaaS economy

3

Nationally, >$200B of public market value created in the last decade

2004 CA-based Salesforce.com becomes the first true SaaS company to go public with a $1.3Bn valuation (now >$40B)

Today SaaS companies make up over $200Bn of public market value*

*includes companies that have switched to a cloud-based subscription software model since 2004 and acquisition values of acquired public SaaS companies

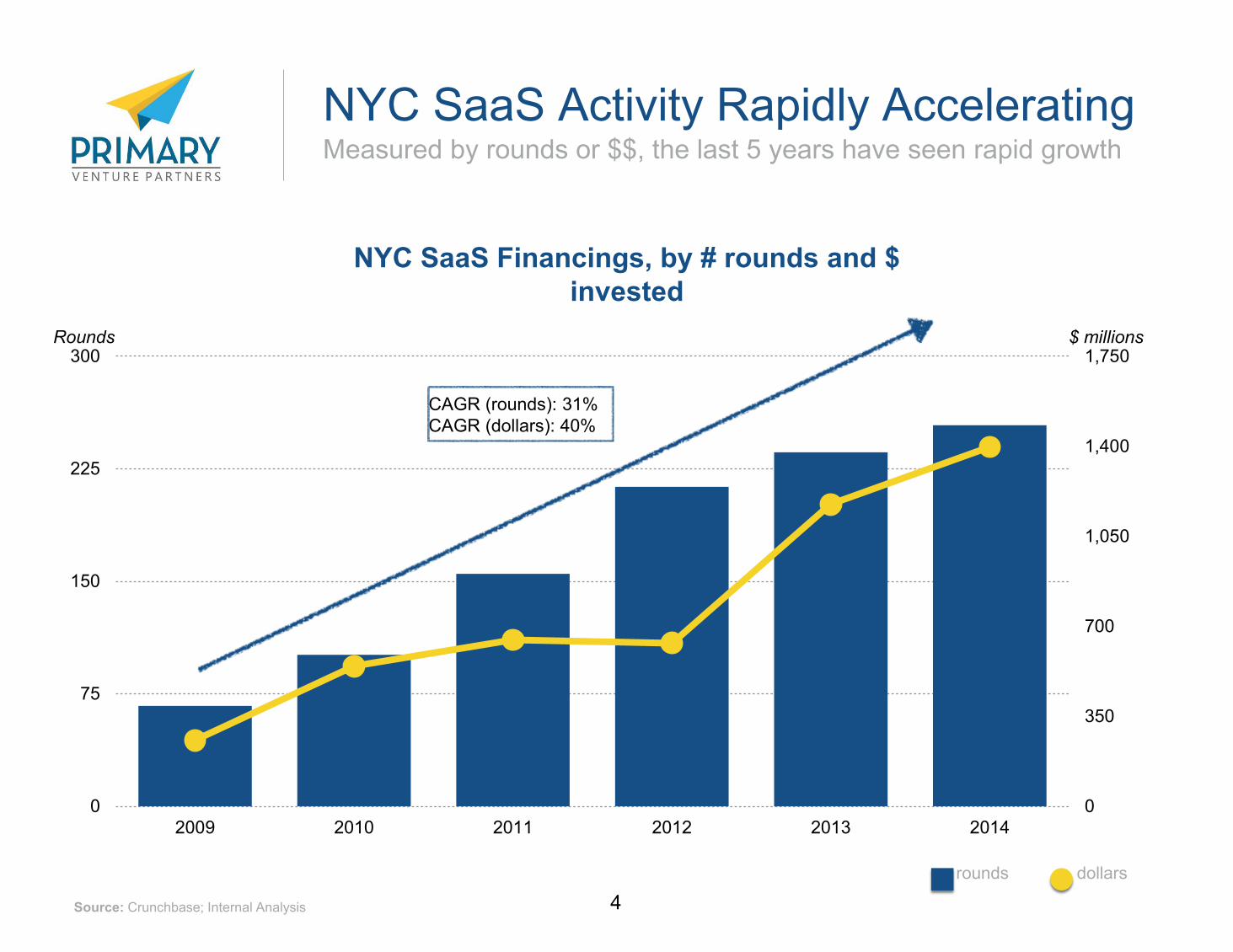

NYC SaaS Activity Rapidly Accelerating

4

Measured by rounds or $$, the last 5 years have seen rapid growth

0

350

700

1,050

1,400

1,750

0

75

150

225

300

2009 2010 2011 2012 2013 2014

rounds dollars

Source: Crunchbase; Internal Analysis

Rounds

CAGR (rounds): 31% CAGR (dollars): 40%

$ millions

NYC SaaS Financings, by # rounds and $ invested

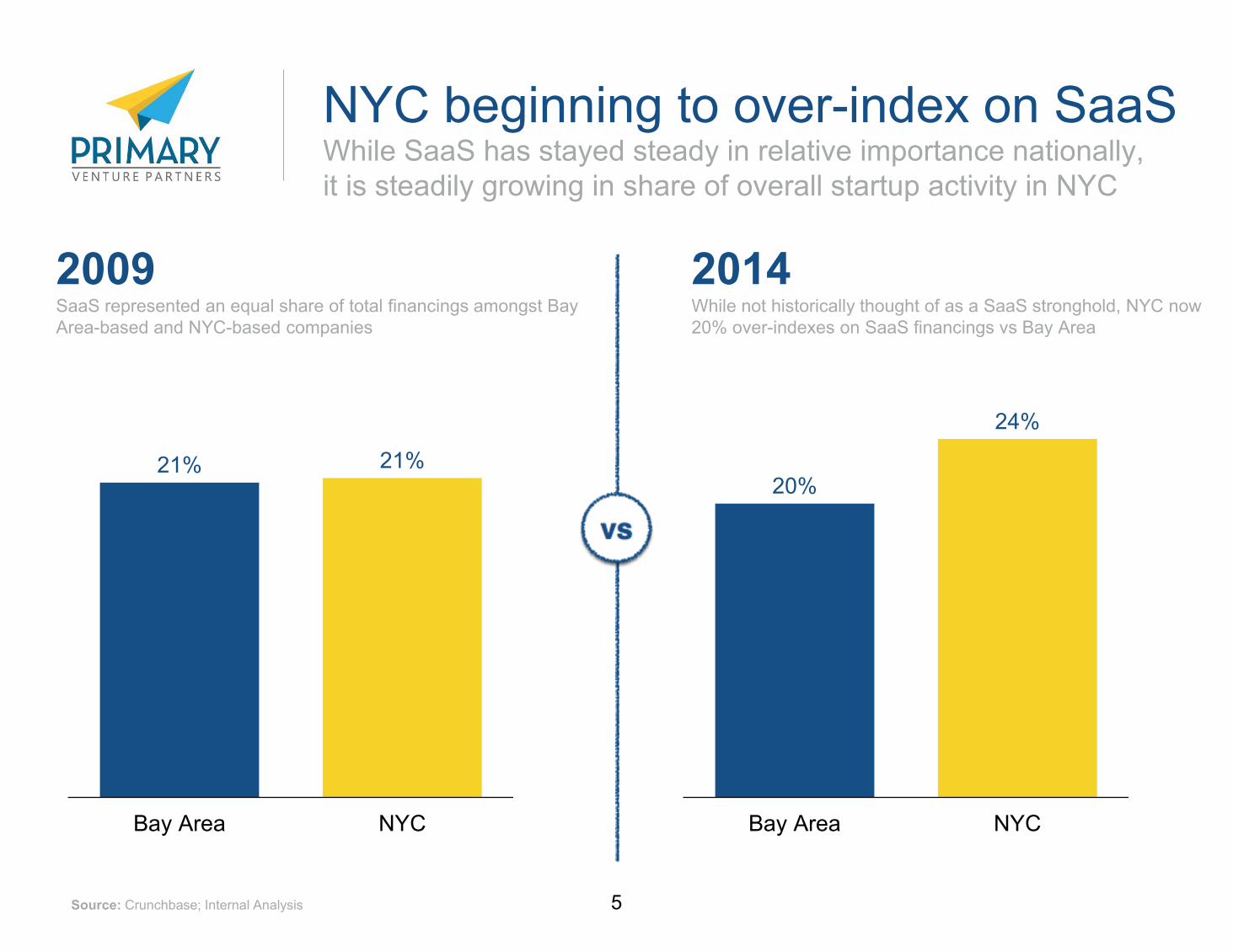

NYC beginning to over-index on SaaS

5

While SaaS has stayed steady in relative importance nationally, it is steadily growing in share of overall startup activity in NYC

20%

24%

Bay Area NYC

2014 While not historically thought of as a SaaS stronghold, NYC now 20% over-indexes on SaaS financings vs Bay Area

21% 21%

Bay Area NYC

2009 SaaS represented an equal share of total financings amongst Bay Area-based and NYC-based companies

Source: Crunchbase; Internal Analysis

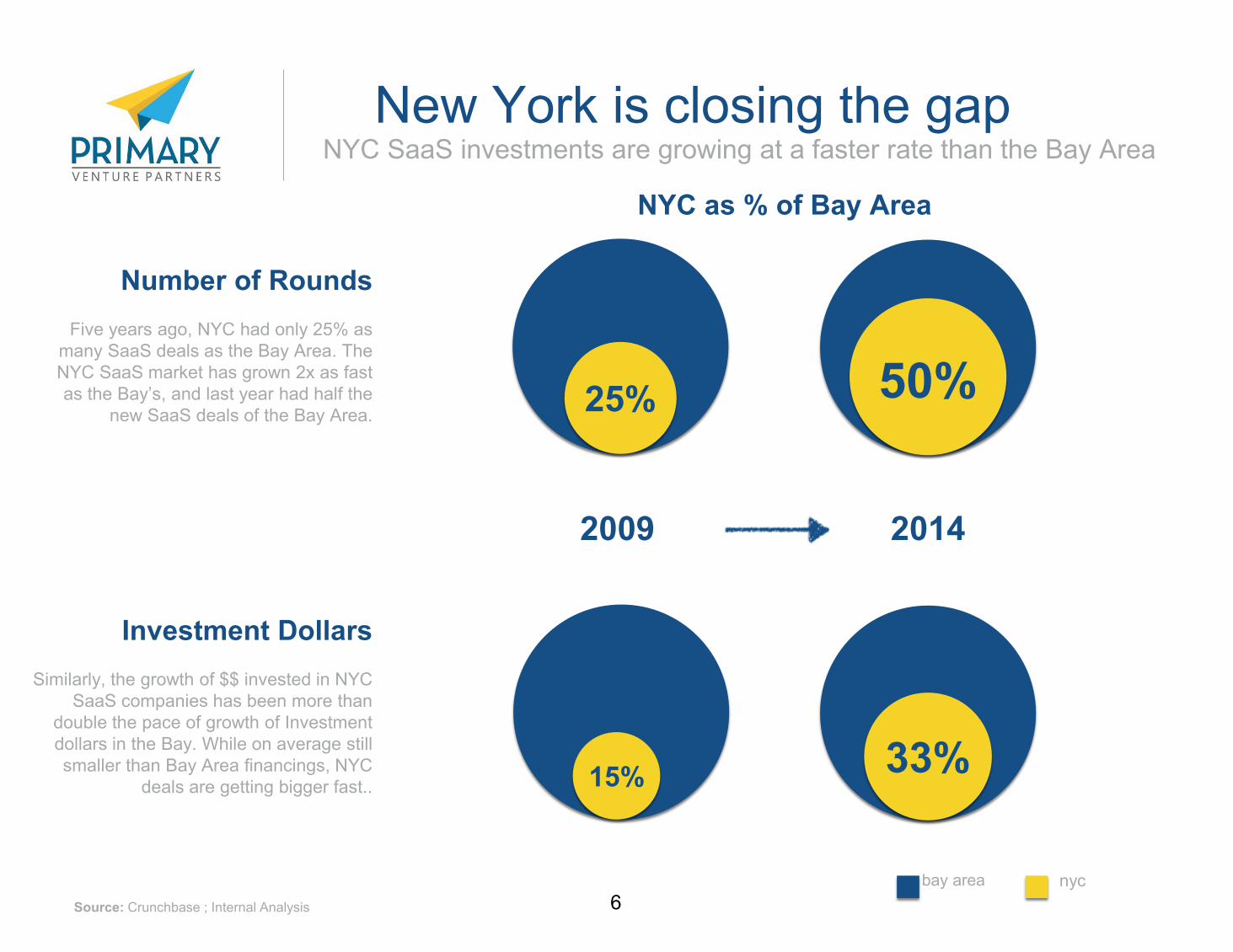

New York is closing the gap

6

NYC SaaS investments are growing at a faster rate than the Bay Area

Investment Dollars

Similarly, the growth of $$ invested in NYC SaaS companies has been more than

double the pace of growth of Investment dollars in the Bay. While on average still smaller than Bay Area financings, NYC

deals are getting bigger fast..

Number of Rounds

Five years ago, NYC had only 25% as many SaaS deals as the Bay Area. The NYC SaaS market has grown 2x as fast as the Bay’s, and last year had half the

new SaaS deals of the Bay Area.

Source: Crunchbase ; Internal Analysis

2009 2014

50%

15% 33%

25%

bay area nyc

NYC as % of Bay Area

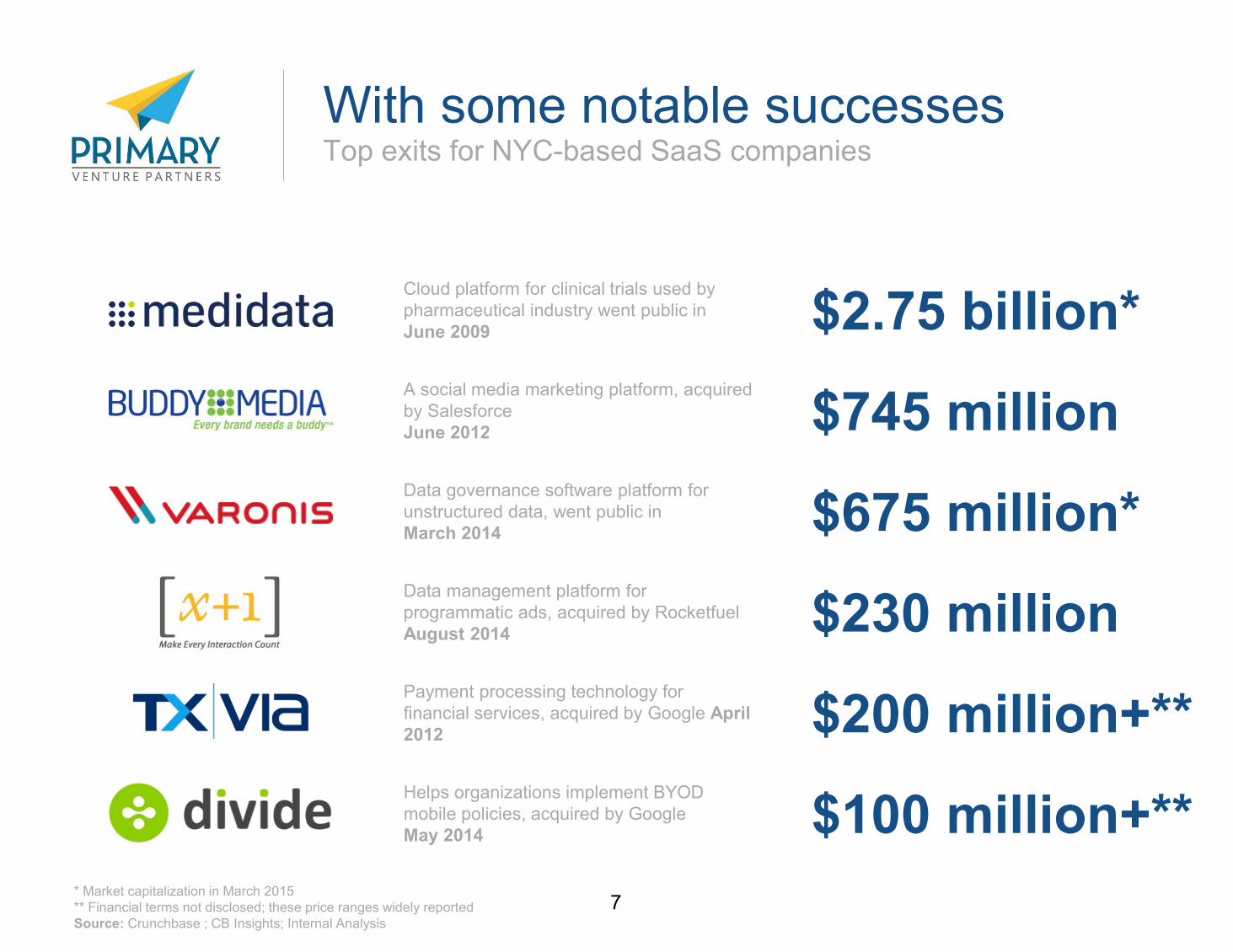

With some notable successes

7

Top exits for NYC-based SaaS companies

$745 million A social media marketing platform, acquired by Salesforce June 2012

$675 million*

$2.75 billion*

$230 million

$100 million+**

$200 million+**

Data governance software platform for unstructured data, went public in March 2014

Cloud platform for clinical trials used by pharmaceutical industry went public in June 2009

Data management platform for programmatic ads, acquired by Rocketfuel August 2014

Helps organizations implement BYOD mobile policies, acquired by Google May 2014

Payment processing technology for financial services, acquired by Google April 2012

* Market capitalization in March 2015 ** Financial terms not disclosed; these price ranges widely reported Source: Crunchbase ; CB Insights; Internal Analysis

and more potential in the pipeline

8

Recent large financings suggest a pipeline of potential future unicorns

Platform enabling SMBs to sell their services online $77 million funding

Monitoring service producing unified metrics and events from IT infrastructure $53 million funding

Modular desktop and API products for integrating datasets / back-testing services $180 million funding

Simple and fast cloud hosting service built for developers $90 million funding

Cloud-based technology platform dedicated to improving cancer care $140 million funding

Equity trading platform for mutual funds, hedge funds and family offices $100 million funding

SaaS-based recruiting technology solutions to the Global Fortune 1000 $41 million funding

Next-generation database technology for enterprise customers $311 million funding

Automated patient check-in process for healthcare providers $73 million funding

Aggregates and analyzes disparate user data to provide personalized marketing $48 million funding

Cloud-based translation management platform $63 million funding

Complete social media management platform for enterprise brands $123 million funding

Low-latency market data and exchange connectivity solutions for financial firms $53 million funding

Small business digital presence management platform $116 million funding

Automated platform for managing online offers, reviews and email campaigns $40 million funding

Source: Crunchbase ; Internal Analysis *includes NYC enterprise / SaaS companies that have raised over $40 million

9

Leveraging New York City Why will NYC lead the next generation of SaaS?

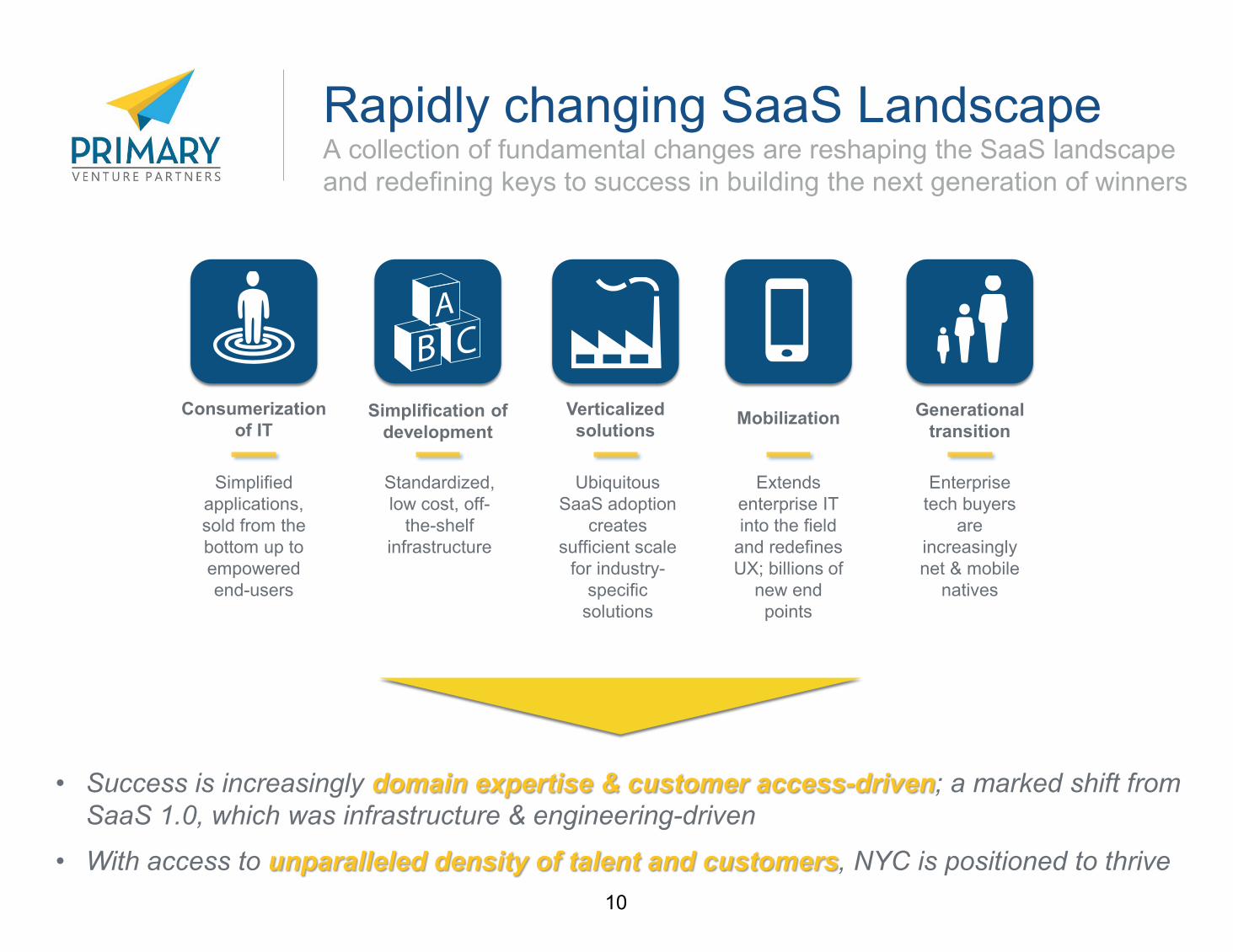

Rapidly changing SaaS Landscape

10

A collection of fundamental changes are reshaping the SaaS landscape and redefining keys to success in building the next generation of winners

Consumerization of IT

Simplification of development

Verticalized solutions Mobilization Generational

transition

Simplified applications, sold from the bottom up to empowered end-users

Standardized, low cost, off-

the-shelf infrastructure

Ubiquitous SaaS adoption

creates sufficient scale

for industry-specific

solutions

Extends enterprise IT into the field

and redefines UX; billions of

new end points

Enterprise tech buyers

are increasingly net & mobile

natives

• Success is increasingly domain expertise & customer access-driven; a marked shift from SaaS 1.0, which was infrastructure & engineering-driven

• With access to unparalleled density of talent and customers, NYC is positioned to thrive

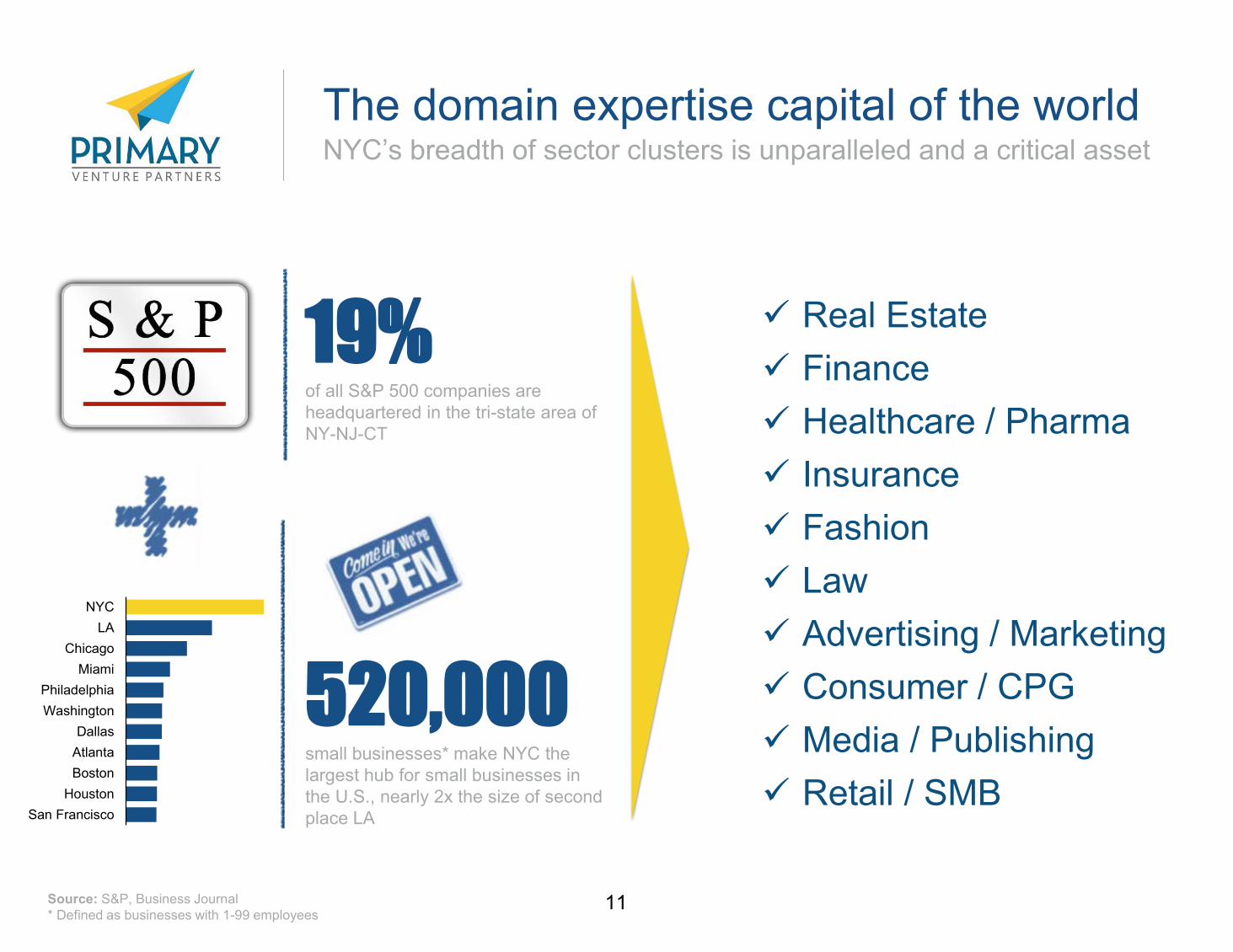

The domain expertise capital of the world

11

NYC’s breadth of sector clusters is unparalleled and a critical asset

520,000 small businesses* make NYC the largest hub for small businesses in the U.S., nearly 2x the size of second place LA

9 Real Estate 9 Finance 9 Healthcare / Pharma 9 Insurance 9 Fashion 9 Law 9 Advertising / Marketing 9 Consumer / CPG 9 Media / Publishing 9 Retail / SMB

Source: S&P, Business Journal * Defined as businesses with 1-99 employees

19% of all S&P 500 companies are headquartered in the tri-state area of NY-NJ-CT

NYCLA

ChicagoMiami

PhiladelphiaWashington

DallasAtlantaBoston

HoustonSan Francisco

12

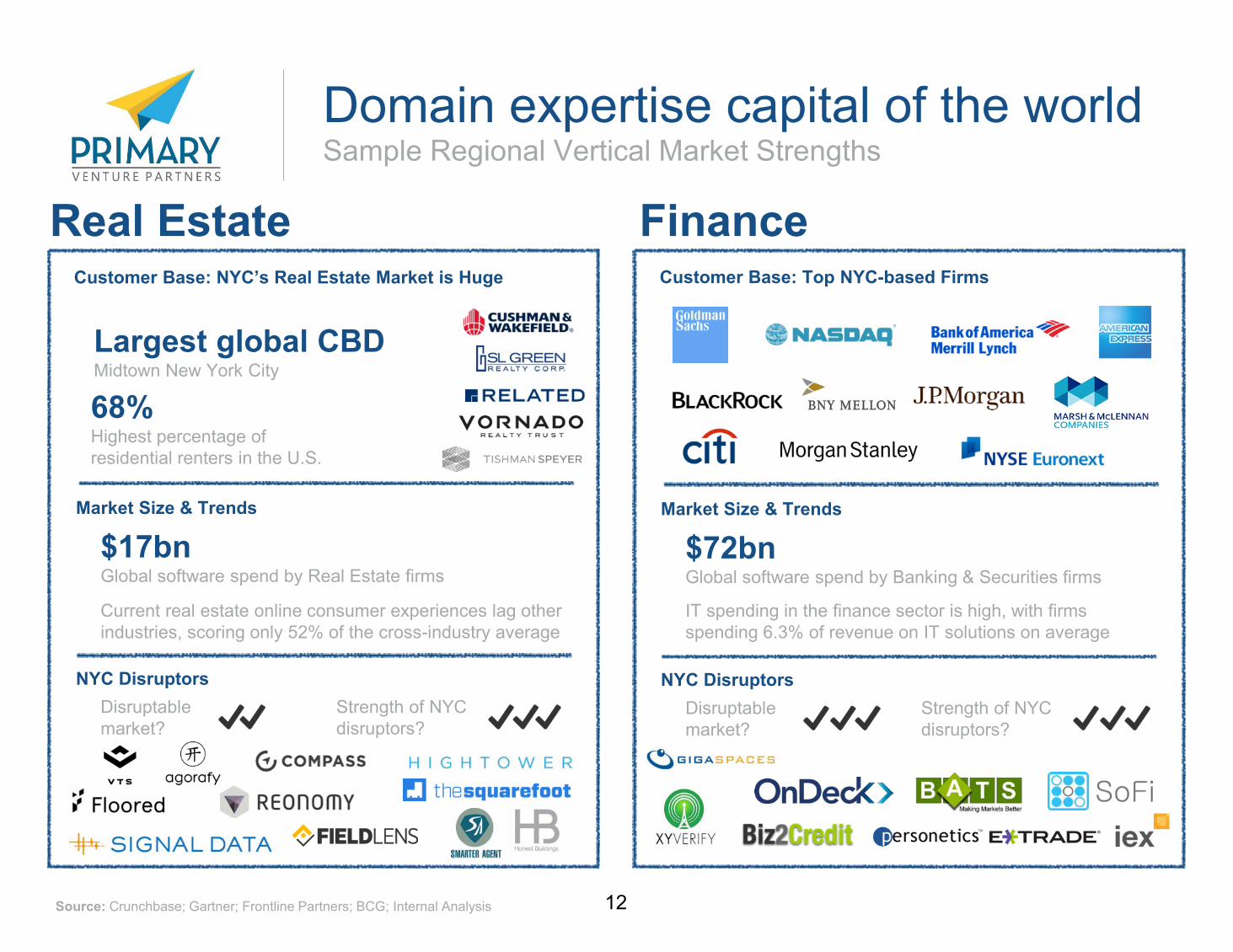

Sample Regional Vertical Market Strengths

Real Estate Finance Customer Base: Top NYC-based Firms

Market Size & Trends

NYC Disruptors

$72bn Global software spend by Banking & Securities firms

IT spending in the finance sector is high, with firms spending 6.3% of revenue on IT solutions on average

Disruptable market?

Strength of NYC disruptors?

Source: Crunchbase; Gartner; Frontline Partners; BCG; Internal Analysis

Customer Base: NYC’s Real Estate Market is Huge

Market Size & Trends

NYC Disruptors

$17bn Global software spend by Real Estate firms

Disruptable market?

Strength of NYC disruptors?

Largest global CBD Midtown New York City

68% Highest percentage of residential renters in the U.S.

Current real estate online consumer experiences lag other industries, scoring only 52% of the cross-industry average

Domain expertise capital of the world

13

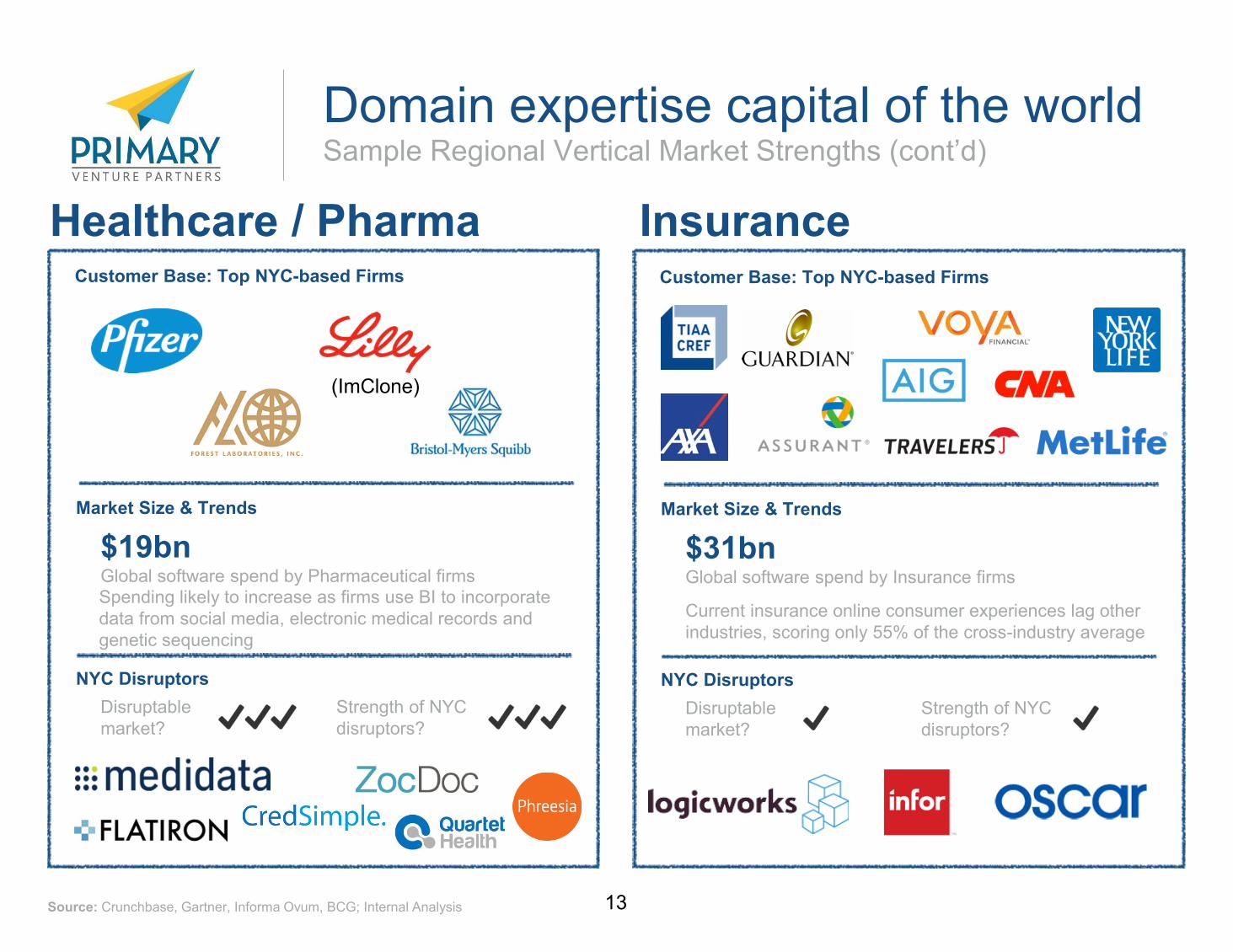

Sample Regional Vertical Market Strengths (cont’d)

Healthcare / Pharma Insurance Customer Base: Top NYC-based Firms

Market Size & Trends

NYC Disruptors

$31bn Global software spend by Insurance firms

Current insurance online consumer experiences lag other industries, scoring only 55% of the cross-industry average

Disruptable market?

Strength of NYC disruptors?

Customer Base: Top NYC-based Firms

Market Size & Trends

NYC Disruptors

$19bn Global software spend by Pharmaceutical firms

Disruptable market?

Strength of NYC disruptors?

(ImClone)

Source: Crunchbase, Gartner, Informa Ovum, BCG; Internal Analysis

Spending likely to increase as firms use BI to incorporate data from social media, electronic medical records and genetic sequencing

Domain expertise capital of the world

14

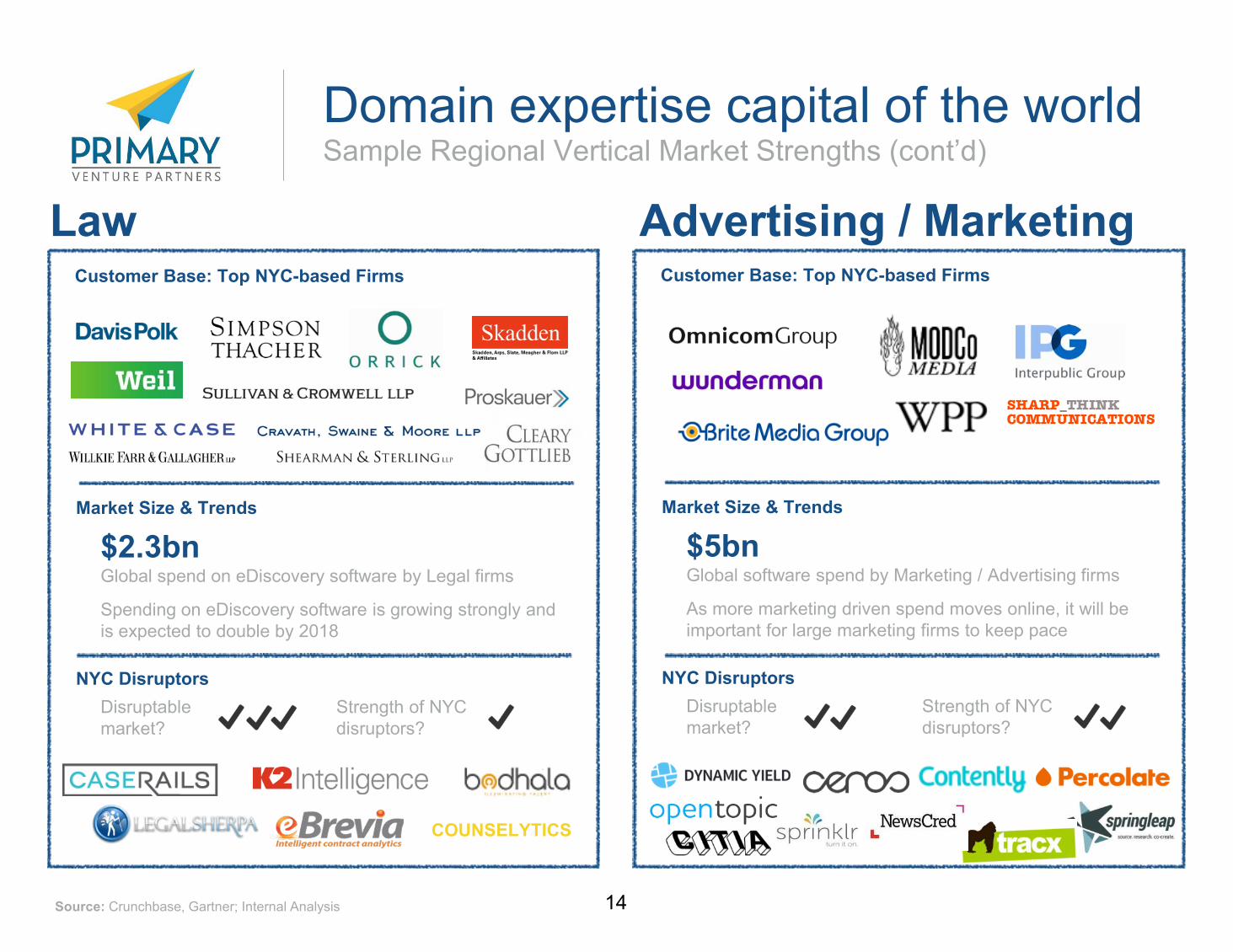

Law Advertising / Marketing

Source: Crunchbase, Gartner; Internal Analysis

Customer Base: Top NYC-based Firms

Market Size & Trends

NYC Disruptors

$2.3bn Global spend on eDiscovery software by Legal firms

Spending on eDiscovery software is growing strongly and is expected to double by 2018

Disruptable market?

Strength of NYC disruptors?

Customer Base: Top NYC-based Firms

Market Size & Trends

NYC Disruptors

$5bn Global software spend by Marketing / Advertising firms

As more marketing driven spend moves online, it will be important for large marketing firms to keep pace

Disruptable market?

Strength of NYC disruptors?

COUNSELYTICS

Domain expertise capital of the world Sample Regional Vertical Market Strengths (cont’d)

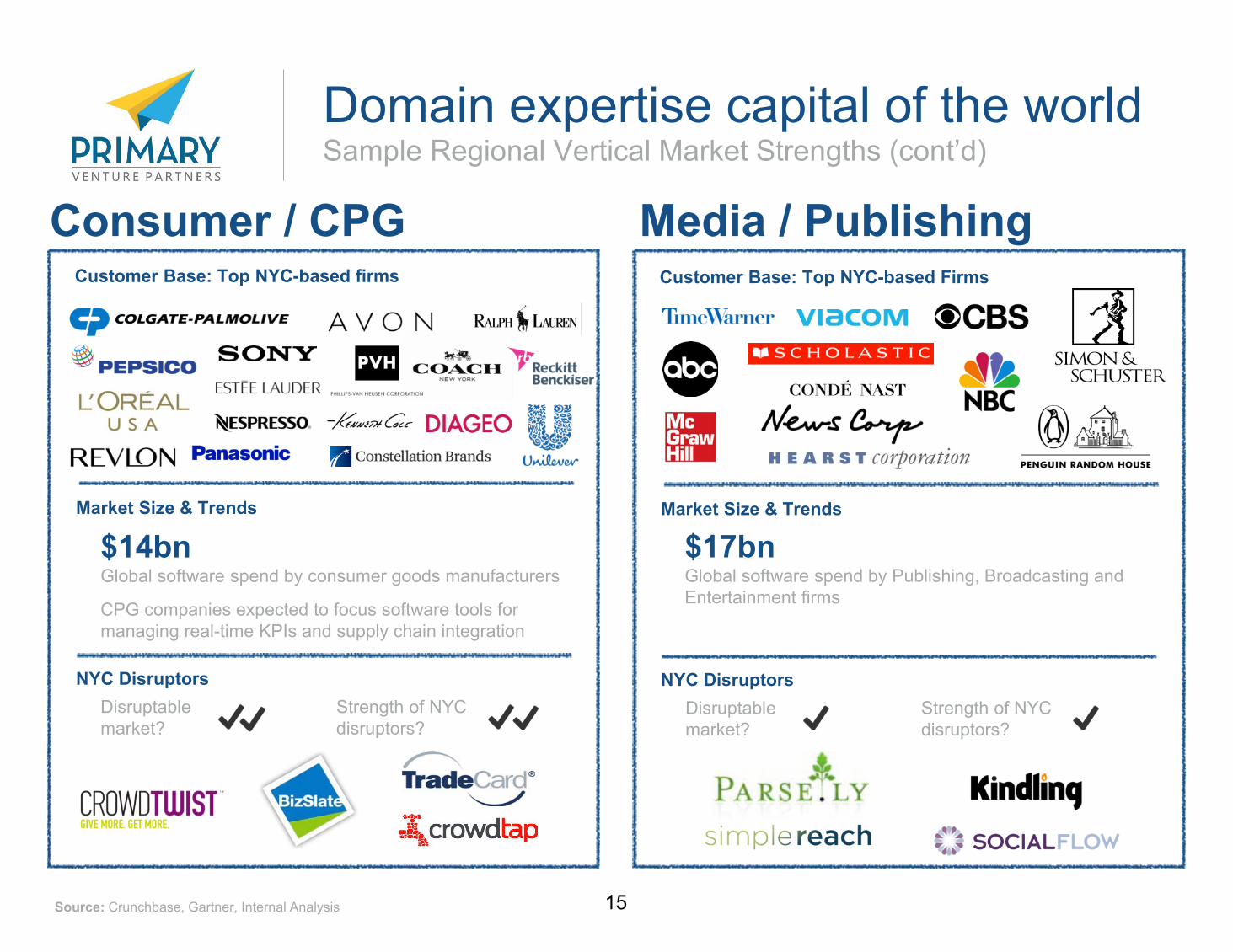

15

Media / Publishing

Source: Crunchbase, Gartner, Internal Analysis

Customer Base: Top NYC-based Firms

Market Size & Trends

NYC Disruptors

$17bn Global software spend by Publishing, Broadcasting and Entertainment firms

Disruptable market?

Strength of NYC disruptors?

Domain expertise capital of the world

Consumer / CPG Customer Base: Top NYC-based firms

Market Size & Trends

NYC Disruptors

$14bn Global software spend by consumer goods manufacturers

Disruptable market?

Strength of NYC disruptors?

CPG companies expected to focus software tools for managing real-time KPIs and supply chain integration

Sample Regional Vertical Market Strengths (cont’d)

16

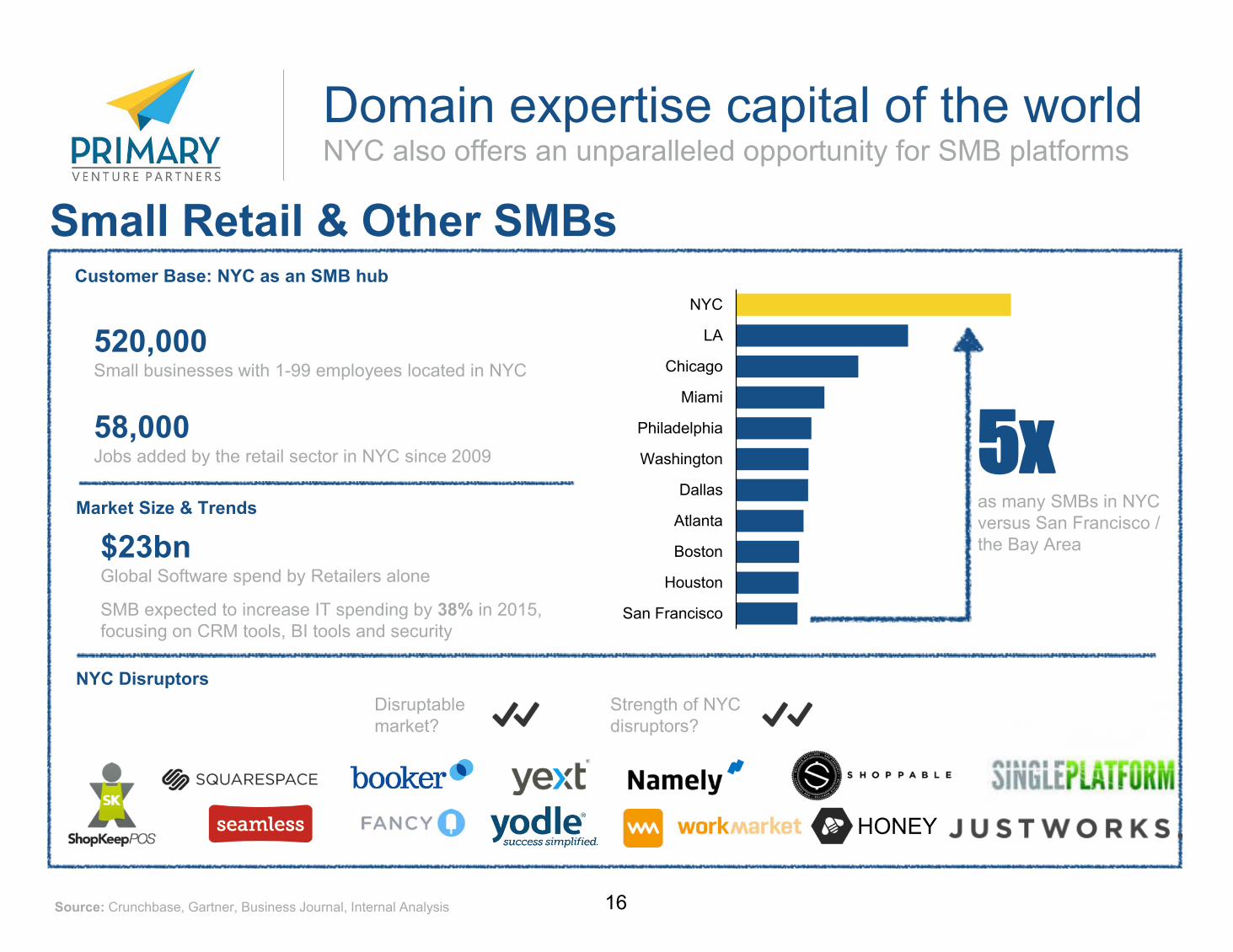

Small Retail & Other SMBs

Source: Crunchbase, Gartner, Business Journal, Internal Analysis

Customer Base: NYC as an SMB hub

Market Size & Trends

NYC Disruptors

$23bn Global Software spend by Retailers alone

SMB expected to increase IT spending by 38% in 2015, focusing on CRM tools, BI tools and security

Disruptable market?

Strength of NYC disruptors?

520,000 Small businesses with 1-99 employees located in NYC

58,000 Jobs added by the retail sector in NYC since 2009

Domain expertise capital of the world

NYC

LA

Chicago

Miami

Philadelphia

Washington

Dallas

Atlanta

Boston

Houston

San Francisco

5x as many SMBs in NYC versus San Francisco / the Bay Area

HONEY

NYC also offers an unparalleled opportunity for SMB platforms

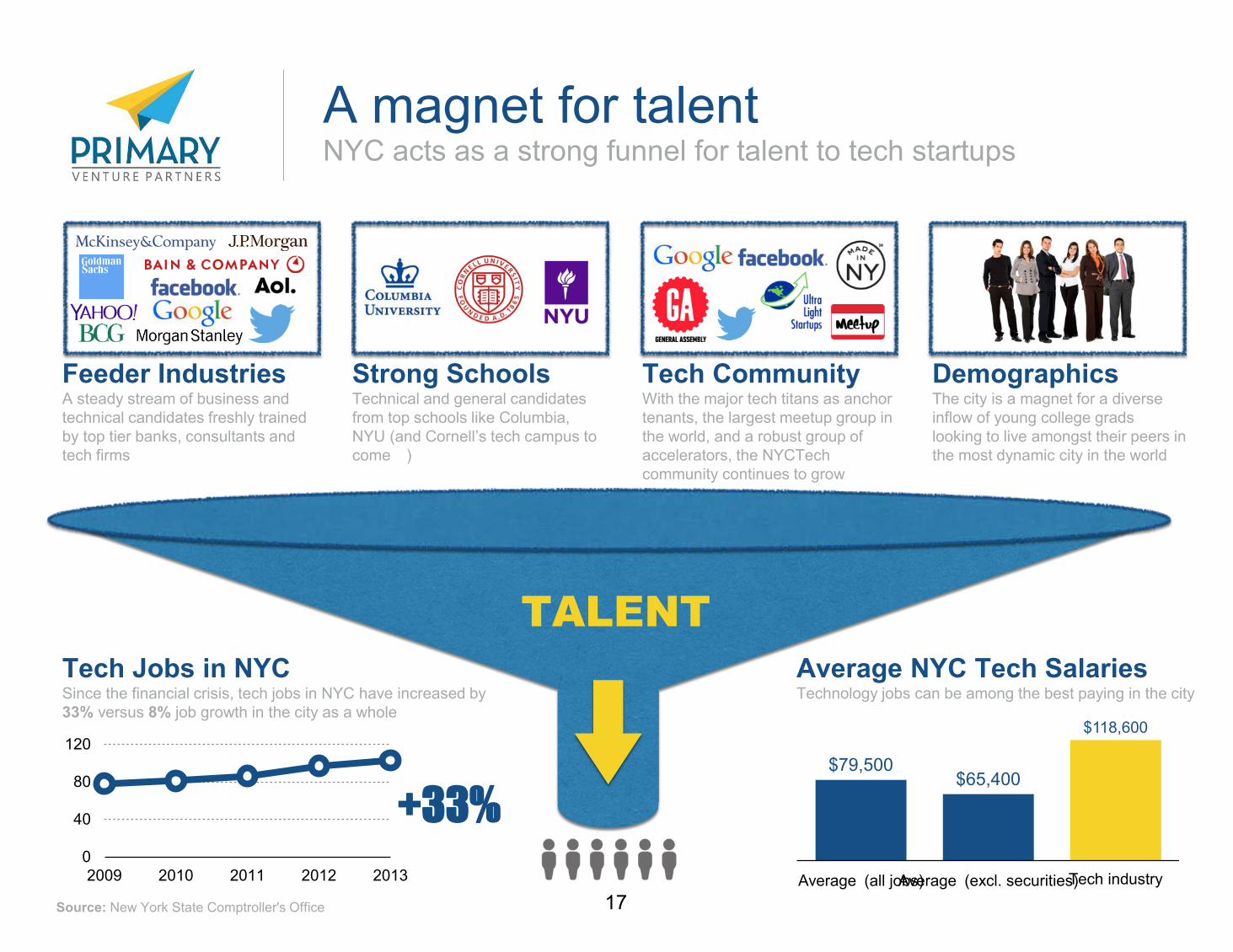

A magnet for talent

17

NYC acts as a strong funnel for talent to tech startups

Feeder Industries A steady stream of business and technical candidates freshly trained by top tier banks, consultants and tech firms

Strong Schools Technical and general candidates from top schools like Columbia, NYU (and Cornell’s tech campus to come )

Tech Community With the major tech titans as anchor tenants, the largest meetup group in the world, and a robust group of accelerators, the NYCTech community continues to grow

Demographics The city is a magnet for a diverse inflow of young college grads looking to live amongst their peers in the most dynamic city in the world

TALENT

0

40

80

120

2009 2010 2011 2012 2013

Tech Jobs in NYC Since the financial crisis, tech jobs in NYC have increased by 33% versus 8% job growth in the city as a whole

+33%

Average NYC Tech Salaries Technology jobs can be among the best paying in the city

$79,500 $65,400

$118,600

Average͒(all jobs) Average͒(excl. securities) Tech industry

Source: New York State Comptroller's Office

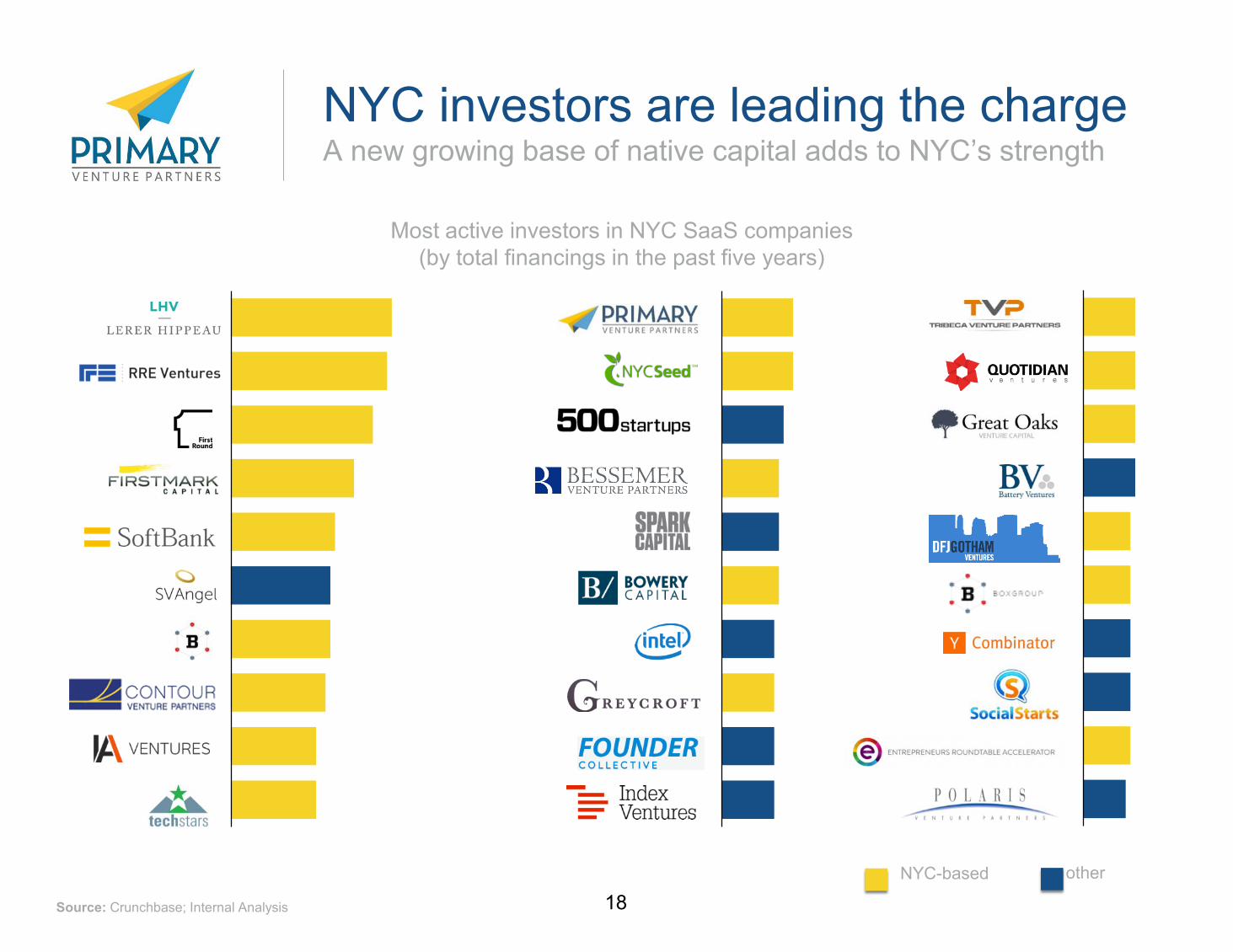

NYC investors are leading the charge

18

A new growing base of native capital adds to NYC’s strength

Source: Crunchbase; Internal Analysis

other NYC-based

Most active investors in NYC SaaS companies (by total financings in the past five years)

What Next?

19

NYC’s SaaS ecosystem has arrived, and is poised for growth. So what now?

9We are catching up to the Bay Area, and the growing importance of vertical SaaS should help us further close the gap in the coming years

9With a strong and growing pipeline of budding unicorns, we can expect Medidata to have plenty of company in the NYC SaaS Unicorn Club by 2020

9 Look for a couple of sectors to really flourish – early promising candidates are real estate, finance, healthcare/pharma, and small business

9The big question: will we build standalone, anchor tenants in the community, or a steady stream of M&A fodder for the big SaaS titans?

Thank You Brad Svrluga, Co-Founder & General Partner [email protected] @bradsvrluga