s3.eu-west-2.amazonaws.com · Web view8.20. Mr Arul Kanda also informed during 1MDB Board Meeting...

495

Auditor general report on 1MDB CONTENTS Introduction executive summary Page 2 CHAPTER 1 INTRODUCTION Page 12 CHAPTER 2 ISLAMIC MEDIUM TERM NOTES, EQUITY Page 22 INVESTMENT, MURABAHAH NOTES AND PORTFOLIO FUNDS CHAPTER 3 INVESTMENT IN THE SRC GROUP Page 65 CHAPTER 4 1MDB GROUP PROPERTY Page 78 INVESTMENT CHAPTER 5 INVESTMENTS IN 1MDB GROUP Page 165 ENERGY SECTOR CHAPTER 6 1MDB GROUP FINANCIAL Page 273 CONFERENCE CHAPTER 7 CORPORATE GOVERNANCE AND Page 354 INTERNAL CONTROL CHAPTER 8 SUMMARY Page 382

Transcript of s3.eu-west-2.amazonaws.com · Web view8.20. Mr Arul Kanda also informed during 1MDB Board Meeting...

Auditor general report on 1MDB

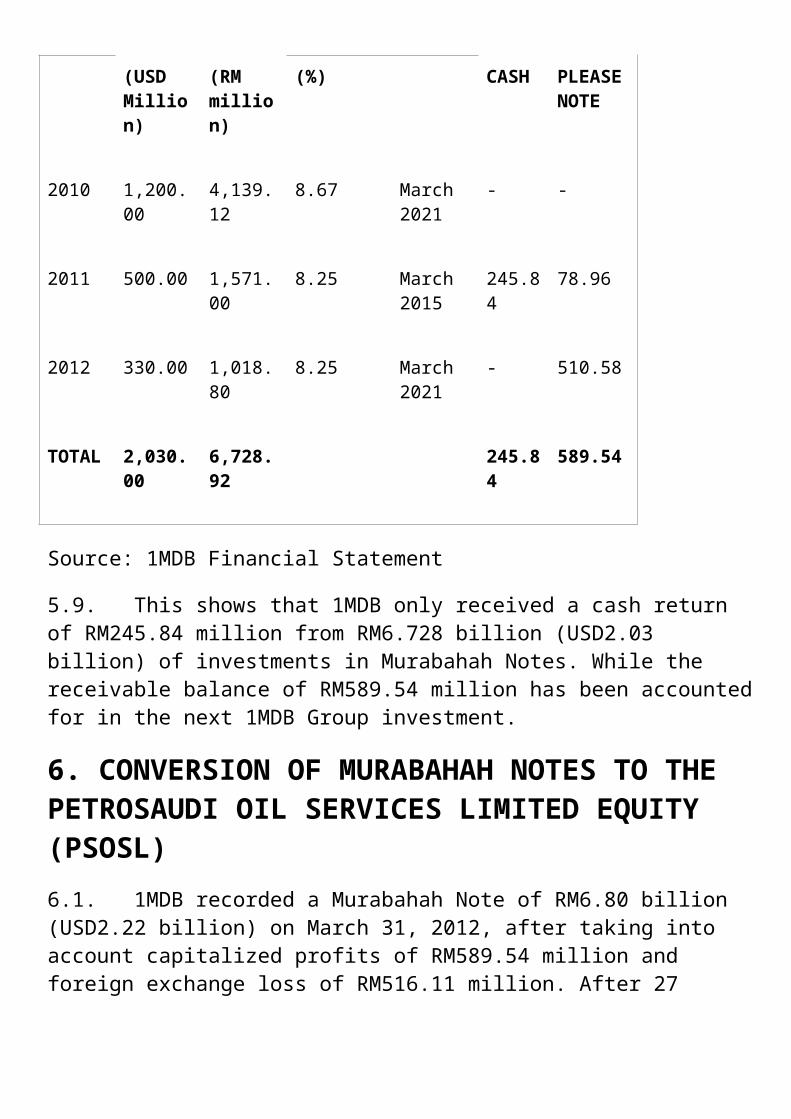

CONTENTS

Introduction executive summary Page 2

CHAPTER 1 INTRODUCTION Page 12

CHAPTER 2 ISLAMIC MEDIUM TERM NOTES, EQUITY Page 22INVESTMENT, MURABAHAH NOTES AND PORTFOLIO FUNDS

CHAPTER 3 INVESTMENT IN THE SRC GROUP Page 65

CHAPTER 4 1MDB GROUP PROPERTY Page 78INVESTMENT

CHAPTER 5 INVESTMENTS IN 1MDB GROUP Page 165ENERGY SECTOR

CHAPTER 6 1MDB GROUP FINANCIAL Page 273CONFERENCE

CHAPTER 7 CORPORATE GOVERNANCE AND Page 354INTERNAL CONTROL

CHAPTER 8 SUMMARY Page 382

Auditor general report executive summary14 July 2016

This is the translated Executive Summary.To see the full report in Malay click on this link.

1. Introduction1.1 BackgroundCabinet had decided on March 4, 2015 that the National Audit Department (JAN) were to verify the accounts of 1Malaysia Development Bhd (1MDB) and its relevant report ought to be handed to the Public Accounts Committee (PAC). Prior to this, on Feb 27, 2015 PAC had also made a request to the JAN to perform an audit on 1MDB.

With regard to this, JAN initiated an audit on March 10, 2015. The audit that took place between March 10 and June 15, 2015 was an interim audit and the relevant report was submitted to the PAC on July 9 and July 10, 2015. This interim report discussed the analysis of the financial statements and investments in a joint-venture with PetroSaudi; the issuance of Murabahah Notes and the Segregated Portfolio Company (SPC).

Following this, the audit was continued until Jan 31, 2016 and a final report was prepared, containing the analysis of the financial statements and financial position of the 1MDB Group based on financial statements ending March 31, 2014 and financial information received up until Oct 31, 2015.

Apart from this, an analysis was also performed on the performance of the equity investments, Murabahah notes, financial portfolio / Portfolio of Funds / Fund Portfolio, SRC Group, real estate sector and energy sector. This final report includes issues covered in the interim report and discussions at the PAC level.

1.2 Audit ObjectivesThis audit was performed based on the mandate from the Cabinet and PAC to verify the financial statements of the 1MDB Group, which have been audited, and to evaluate the financial performance and activities of the 1MDB Group in order to determine if the objectives of establishing the company had been achieved.

1.3 Scope and MethodologyJAN’s had performed checks on the 1MDB Group’s audited financial statements for the financial period ending March 31, 2010 until March 31, 2014. The financial statements for the year ending March 31, 2015 was not prepared by 1MDB for this audit. However, JAN was able to perform an audit based on documents obtained from 1MDB including discussions with (1MDB’s) management. JAN faced limitations while performing this audit in view of the fact that some original or important documents were either submitted late or were not provided by 1MDB for the purpose of verifying transactions or as evidence for the audit.

1.4 Limitations

The limitations resulted in a significant impact on the audit process in terms of verification of the actual financial position, operations and related transactions. Among important documents that were not submitted were the 1MDB Group’s Management Account for the year ending March 31, 2015 and bank statements from foreign lenders. [The audit team] was unable to access computers, notebooks and servers at 1MDB in order retrieve data and information for cross reference and analysis.

1.5 Formation of 1MDBFinance Ministry Incorporated (MKD) has taken over Terengganu Investment Authority Berhad (TIA) which was established by Menteri Besar Terengganu Incorporated (MBI Terengganu) on Feb 27, 2009. The original objective of establishing TIA was to create a sovereign wealth fund with a capital of RM11 billion. The funds were to be obtained from oil royalty owed (to Terengganu) amounting to RM6 billion and bond issuance from the local and foreign financial markets with a proposal for the Federal Government to provide a guarantee of RM5 billion based on Terengganu’s future oil revenue. The Federal Government decided to take over TIA and this process was completed on July 31, 2009 and the company was renamed 1MDB on Sept 25, 2009. After the takeover, 1MDB was no longer a sovereign wealth fund but a strategic development company wholly- owned by MKD with an approved capital of RM1 billion and paid-up capital of RM1,000,002. Subsequently, 1MDB was involved in the following investments:

1. JV with PetroSaudi Holdings (Caymans) Ltd;

2. Investment in Segregated Portfolio Company (SPC);

3. Investment in SRC Group;

4. Investment in real estate sector; and,

5. Investment in energy sector.

1.6 Management Structure and Organisation in 1MDB1.6.1. The management structure was divided into three levels – Advisory Board, Board of Directors and Senior Management. The Advisory Board was tasked with providing guidance and advice on investments and business.

1.6.2. In 2009 and 2010, 1MDB had only one subsidiary and was involved in equity and real estate investments. 1MDB Group’s structure expanded following its involvement in the energy sector through the acquisition of three independent power producers with local and foreign networks, following which the amount of companies in the 1MDB Group had increased to 96 in 2014.

2. 1MDB Group’s Investments

2.1. Islamic Medium Term Notes2.1.1. TIA had proposed to issue Islamic Medium Term Notes (IMTN) amounting to RM5 billion as initial funding. On April 1, 2009, the Federal Government agreed to act as guarantor for TIA to raise the RM5 billion from the domestic and foreign financial markets through IMTN for investment purposes in accordance to the Loans Guarantee (Bodies

Corporate) Act 1965. This guarantee encompasses the repayment of the principle and interest for a period of 30 years. This was followed by an approval from the TIA’s Board of Directors on April 15, 2009. The agreement was signed on May 15, 2009 between TIA (issuer) and AmInvestment Bank Bhd (AmBank) as the lead arranger, lead manager and facility agent. On the same day, the Federal Government provided a guarantee for the issuance of the IMTN.

2.1.2. However, the signing of the agreement and facilitation of the government guarantee was not in accordance to the terms and plans by MBI Terengganu and this had dissatisfied MBI Terengganu as the TIA shareholder. The TIA Board of Directors through a resolution dated May

22, 2009 ordered the suspension of the issuance of the IMTN until a corporate management structure and best practices were realised. The TIA chief executive officer was instructed to take immediate action to terminate and suspend all actions involving the issuance of the IMTN. However, he had already signed the Subscriber Agreement with AmBank on May 25, 2009 and the Aqad Agreement, Murabahah Purchase Agreement and Murabahah Sales Agreement on May 26, 2009. [Hal

2.1.3. The TIA CEO’s act of pursuing the issuance of the IMTN resulted in him being removed as a company director through a shareholders resolution dated May 27, 2009. On the same date, a TIA Board of Directors resolution signed by Datuk Ismee and Shahrol Azral [Halmi] to proceed with the issuance of the IMTN and reappoint Shahrol Azral as a TIA director. The issuance of the IMTN […] had resulted in MBI Terengganu issuing a written warning to AmBank on May 29, 2009. The bank was accused of malpractice and non-compliance by issuing the IMTN. Moreover, Cabinet was informed on June 3, 2009 that the DYMM Sultan of Terengganu had sought a report on the “Unauthorised Issuance of IMTN by TIA”.

2.1.4. On May 29, 2009, TIA received the net amount from the IMTN totalling RM4.385 billion from the full value of RM5 billion, which is at a price of RM87.92 for every RM100 in nominal value with a discount rate of 12.08% in view of AmBank as the lead arranger to ensure the issuance of the IMTN was fully subscribed. The coupon rate is 5.75% per annum with effective rate of returns to be 6.68% annually.

2.1.5. During the 1MDB Board meeting on Oct 10, 2009, the chief executive officer informed that the IMTN was issued based on the urgings of the TIA special advisor for the purpose of developing Pulau Bidong in cooperation with Mubadala (a company). Apart from this, in June 2015, the former 1MDB CEO said the issuance of the IMTN had proceeded because the agreement signed on May 15, 2009 was a “bought deal” in which AmBank as the lead arranger and primary subscriber had obtained secondary market subscribers for the issuance of the bond.

2.2 Equity Investments, Murabahah Note and Fund Portfolio

2.2.1. 1MDB Group’s joint-venture with foreign companies began in 2009 with the goal of pioneering investment opportunities abroad. The first JV

project was finalised between 1MDB, PetroSaudi Holdings (Cayman) Ltd. and 1MDB PetroSaudi Ltd. (joint-venture compay) on Sept 28, 2009. 1MDB held 40% equity with a contribution of USD1 billion while PetroSaudi Holdings (Cayman) Ltd. held 60% equity in form of assets worth approximately USD1.5 billion. The decision to invest in this JV company was made in a period of eight days, without a detailed evaluation process and before issues/conditions raised by the 1MDB Board of Directors were resolved. There were four different companies registered with the name PetroSaudi but the investment proposal paper tabled to the 1MDB Board of Directors did not state this fact.

2.2.2. The assets valuation report prepared by Edward L Morse was presented on Sept 29, 2009, which is the same date that he was confirmed in his appointment to perform the job by the 1MDB CEO, and the report was received one day after the JV was signed. The valuation report took into consideration the exploration rights and oil production in Turkmenistan and Argentina. The valuation was conducted on assets owned by PetroSaudi International Ltd although the JV agreement clearly states that the company which owned all rights and interests on the agreed assets for the JV project was PetroSaudi International Cayman.

2.2.3. In addition, the JV agreement includes clauses which insufficiently provides for the interest of the company [1MDB]. Among others, the loan received by 1MDB PetroSaudi Ltd. amounting to USD700 million from its parent company, PetroSaudi Holdings ( Cayman) Ltd. on Sept 25, 2009 must be paid back in full on or before Sept 30, 2009. On Sept 30, 2009, a total of USD1 billion (RM3.487 billion) was transferred by 1MDB to two separate accounts – USD300 million to the account of the JV company and USD700 million to the account of another company for the purpose of repaying the loan received by the JV company. The payment of USD700 million to the other company was performed without the approval of the 1MDB Board of Directors.

2.2.4. Six months after the JV was signed, 1MDB disposed all of its 40% equity stake amounting to USD1 billion in the JV company in return received USD1.20 billion through the subscription of Murabahah Notes. The Murabahah Notes provide returns of 8.67% annually and mature on March 31, 2021 and were supported by a corporate guarantee by PetroSaudi International Ltd. On Sept 14, 2010, an additional subscription of Murabahah Notes amounting to USD500 million (RM1.57 billion) was

made and a total of USD330 million (RM1.02 billion) was paid between May 20 and Oct 25, 2011. A portion of the funds to finance the additional subscription of Murabahah ntoes were made through loans from financial institutions.

2.2.5. After investing 27 months in the Murabahah Notes, on June 1, 2012, 1MDB redeemed the Murabahah Note, including profits yet to be received, amounting to USD2.22 billion (RM6.8 billion) through an asset swap arrangement in which 1MDB’s subsidiary, 1MDB International Holdings Ltd (1MDB-IHL), acquired a 49% equity stake in PetroSaudi Oil Services Ltd (PSOSL), a PetroSaudi International Ltd subsidiary. 1MDB-IHL also ratified a “call and put option” with PetroSaudi International Ltd to acquire the remaining 51% stake in PSOSL at an option price of USD10. The swapping of Murabahah Notes for equity in PSOSL was performed without detailed study to determine (PSOSL’s) liability, ability to generate funds and its past financial performance. Although knowledge of PSOSL’s operations in Venezuelan waters was subjected to restrictions/sanctions by the US and drilling contracts were expiring, the decision to invest in PSOSL was continued. Moreover, the approval by the Board of Directors and 1MDB shareholders to swap the Murabahah Notes for equity in PSOSL was signed on June 20, 2012, but the 1MDB CEO had signed five documents regarding the deal on June 1, 2012. This shows that the 1MDB CEO took action even before seeking the board’s approval.

2.2.6. 45 days after 1MDB swapped the Murabahah Note for an equity stake in PSOSL, the 1MDB CEO had sought to dispose of the equity stake in PSOSL because Venezuela was facing sanctions by the US. In relation to this, the 1MDB Board of Directors approved the disposal of 1MDB-IHL’s 49% equity stake in PSOSL to Bridge Partners International Investment Ltd (Bridge Partners) for a consideration of not less than USD2.22 billion which to be managed by a licensed fund manager. This decision was made through a resolution by the Board of Directors and 1MDB shareholders.

2.2.7. On Sept 12, 2012 the sale and purchase agreement to dispose of 1MDB-IHL’s entire stake (in PSOSL) was ratified between 1MDB and Bridge Partners. In return, Bridge Partners issued six promissory notes, without interest, valued at USD2.318 billion, which must be paid in one month. On the same date, 1MDB, through its fully-owned subsidiary Brazen Sky Ltd, ratified an “Investment Management Agreement” with

Bridge Global Absolute Return Fund SPC (Bridge Global SPC) and Bridge Partners Investment Management (Cayman) Ltd. to invest the USD2.318 billion. This investment was funded through promissory notes in lieu of cash and was later invested in various investment portfolios through a Segregated Portfolio Company (SPC) in the Cayman Islands. This Investment was made through Bridge Global Absolute Return Fund SPC (Bridge Global SPC), which was a month-old company, without a fund managing license and without experience in managing large sum of funds.

2.2.8. The Board of Directors on May 20, 2013 agreed that the investment be redeemed in stages in order to improve public perception on the credibility of 1MDB’s investments. The Board of Directors had issued nine instructions between May 2013 and August 2014 to the management to prepare a plan, schedule and redemption of portfolio funds from the SPC either through stages or as a whole. However, no immediate action was taken by the 1MDB management.

2.2.9. On Dec 20, 2014 the Board of Directors was informed that the latest funds to have been redeemed from the SPC portfolio stood at USD1.392 billion and the balance of USD939.87 million would be redeemed at the end of December 2014. From this amount, USD993 million was paid to Aabar to terminate options. In reality, all of those remaining funds from the SPC portfolio were used as collateral for Beutsche Bank for a loan amounting to USD975 million, for which an approval from the Board of Directors was not obtained. Apart from this, the USD1.392 billion which had been transferred to the account of Brazen Sky Ltd was forwarded to 1MDB Global Investment Limited (1MDB GIL). This act contravened the instructions of the Board of Directors who demanded that the SPC portfolio funds be brought back to Malaysia.

2.2.10. An Asset Sale Agreement was signed on Jan 2, 2015 between Brazen Sky Ltd and Aabar Investments PJS Limited (Aabar Ltd) to ensure the balance of the SPC portfolio funds amounting to USD939.87 could be redeemed before March 31, 2015, as sought by the Board of Directors. However, the agreement was signed without the knowledge of the Board of Directors and 1MDB shareholders. In relations to this, the Board of Directors agreed on March 25, 2015 to terminate the Asset Sale Agreement and replaced it with a Share Sale Agreement in which the all equity in Brazen Sky Ltd was to be sold to Aabar Ltd at a consideration

price of USD1.20 billion. However, the Share Sale Agreement was never finalised.

2.2.11. On May 28, 2015, a Term Sheet for Settlement Arrangements (Binding Term Sheet) was signed between 1MDB Group, Finance Ministry Incorporated (MKD), International Petroleum Investment Company (IPIC) and Aabar Investments PJS Groups (Aabar). Among the important terms in the Binding Term Sheet is that IPIC will pay 1MDB USD1 billion before or on June 4, 2015 and takeover the payment obligations for the interest and principle for two USD Notes which respectively amounts to USD1.75 billion. As for 1MDB, during a meeting on June 14, 2015, the Board of Directors was informed that among assets which would be transferred to IPIC/Aabar was the balance from the SPC portfolio amounting to USD939.87.

2.2.12. In conclusion, for the period of four years since 1MDB was established, the initial investment by 1MDB through funds from the issuance of IMTN amounted to RM5 billion and this investment instrument was changed four times. This started with the investment of USD1 billion (RM3.49 billion) in 2009 in a JV with a subsidiary of PetroSaudi International Ltd, followed by the investment of Murabahah Note amounting to USD830 million (RM2.59 billion) in 2011 and 2012 until it was transformed into investment in the SPC Portfolio amounting to USD2.318 billion (RM7.18 billion) in Cayman Islands in September 2012. The repatriation of a portion of the investment in the SPC Portfolio in 2014 was used to fund various company commitments and investments. In the end,

the investment was left with a balance of USD939.87 in the form of investment units in the SPC Portfolio on March 31, 2015.

3. Investments in SRC Group3.1. An early proposal for the establishment of a Strategic Resource Company was presented by 1MDB to the prime minister on Aug 24, 2010. The Economic Planning Unit (EPU) had studied the proposal and approved the establishment of the company after several conditions were fulfilled. Based on the Memorandum and Articles of Association (M&A), SRC’s objective was to identify and invest in projects involving drilling, extraction, processing and trade in conventional energy, renewable natural resources and minerals, including the acquisition of company shares, stocks and securities. According to SRC’s business plan for 2011 to 2015,

SRC will supply coal for the long term needs of the country by the fourth year of operation (2014).

3.2. As a subsidiary of 1MDB, SRC received funds from a government development grant amounting to RM15 million from the RM20 million approved by the EPU and a loan of RM2 billion from Retirement Fund Incorporated (KWAP). The RM2 billion was received on Aug 29, 2011 which was meant to be repaid over 10 years. The loan was guaranteed by the Government which includes principle and interest, amounting to RM2.902 billion.

3.3. A JV project between SRC’s subsidiary SRC International (Malaysia) Ltd (SRCI) and Aabar Investments PJS (Aabar) on Nov 3, 2011 resulted in the establishment of Aabar-SRC Strategic Resources Limited (ASRC). ASRC’s initial capital amounts to USD120 million, with each side providing USD60 million. The SRCI board had approved USD45.50 million for investment in the coal industry in Mongolia without providing a feasibility study on the matter which will be undertaken by ASRC through Gobi Coal & Energy Limited (GCE). SRC also invested in PT ABM Investama TBK, Indonesia amounting to USD120 million (RM366.68 million) through published share prices listed on the Indonesian Stock Exchange. During a meeting on Feb 14, 2012, the SRC CEO had reported that the estimated gains on the investment was USD4 million.

3.4. On Feb 15, 2012 1MDB’s ownership of SRC was relinquished to Finance MInistry Incorporated (MKD) by means of share transfer through dividend-in-specie interim payments. The transfer of SRC shares also reduced 1MDB Group’s operational loss from RM25 million to RM16.2 million, reduced the 1MDB’s gearing ratio from 12 times to 9.5 times and reduced the government’s guarantee by RM2.902 million to 1MDB Group.

4. Real Estate Investments

5. Energy Sector Investments

6. Financial Position of 1MDB Group

6.1 Based on the financial statements for the year ending March 31, 2014, 1MDB Group’s outstanding debt, both foreign and domestic, stood at RM33.71 billion. This does not include inherited loans. Eight of the loans involve domestic lenders and three from foreign lenders. Apart from this,

1MDB had 11 inherited loans, from two independent power producers in 2012 and 2014, involving RM8.15 billion which must be serviced. Thus 1MDB’s position in loan balance up until financial year ending March 31, 2014 stands at RM41.86 billion.

6.2 In terms of asset positions, a 363% rise (in value), from RM9.53 billion in 2012 to RM44.14 billion in 2013, was recorded. This increase resulted from the acquisition of two independent power producers, revaluation of real estate investments, an increase in cash on hand, deposits to Aabar Ltd, concession agreements and leases which have not been received. According to the 2014 financial statements, the value of assets increased by another 16% to RM51.41 billion following the acquisition of another IPP and investment in a portfolio fund manager.

6.3 An analysis of the cash flow on the financial statements from year 2010 to 2014 have shown that 1MDB’s paid-up capital was only RM1 million. This small amount showed that the company was not (financially) stable because it required to borrow for its activities. Throughout financial year 2010 until 2014, 1MDB obtained 17 loans (not inclusive of inherited loans) at a nominal value of RM42.88 billion but received cash amounting to RM39.17 billion. However, (the company’s) activities which were funded by loans did not generate the necessary cash flow to repay the loans.

6.4. Up until Oct 31, 2015, the total amount repayable by 1MDB Group stood at RM55 billion while its assets were valued at RM58.60 billion. Government guaranteed or assisted loans stood at RM20.31 billion.

6.5. Based on the assumption that the rationalisation plan is implemented and no new loans are taken after Oct 2015, it is estimated that RM42.26 billion is required to repay the loans which will mature between November 2015 and May 2039. 1MDB needs to prepare large sums to fulfil its obligations – RM4.88 billion in 2016, RM14.74 in 2023 and RM5.14 billion in 2039. 1MDB also requires to have at least RM1.52 billion annually from Nov 2015 to May 2024 to repay its loans.

6.6 For the period of 2016 until 2023, the borrowing cost which must be borne by 1MDB Group amounts to RM9.08 billion. The IMTN issued in 2009 will mature in 2039 with coupon payments amounting to RM287.50 per annum. 1MDB Group’s commitment for the IMTN from November 2015

until 2039 amounts to RM11.90 billion – RM5 billion principle and RM6.90 billion in interest.

7. Corporate management and Internal Controls

[…] Overall, the management and internal controls in 1MDB Group was “less than satisfactory”. Some management decisions and decisions by the Board of Directors were made without due process. Among others:

1.Between 2009 and 2015, several important investment decisions involving large sums were made through written resolutions by the Board of Directors without any discussion and proper detailed valuation. Several investments were decided on short notice and were high risk. However, the Board of Directors have told the PAC on Jan 19, 2016 that discussions were held before approvals were given through written resolutions.

2.In several situations, the 1MDB management had presented incomplete or inaccurate information to the Board of Directors before an important decision was to be made. In fact, the management sometimes took action without approval from the Board.

3.There were also situations in which the 1MDB management had presented information that was inaccurate or did not correlate with other interested parties.

4.The 1MDB management took actions which were against, or did not fully comply with, Board/shareholder decisions.

1MDB’s record keeping and filing methods were not systematic and less than satisfactory.

CHAPTER 1

INTRODUCTION 14 July 2016

1. AUDITING TO 1MALAYSIA DEVELOPMENT BERHAD1.1. The Cabinet meeting on 4 March 2015 has decided that the National Audit Department (JAN) verify the 1MDB company's account and the relevant report should be submitted to the National Accounts Committee (PAC). Accordingly, the audit of the 1Malaysia Development Berhad (1MDB) company was conducted by JAN from March 10, 2015.

1.2. Prior to this, on 27 February 2015, the PAC had requested JAN to conduct auditing of 1MDB by focusing on five aspects as follows:

Source of funds amounting to RM2 billion obtained by 1MDB in settling its loan to several local banks; The injection of new financial funds from the Ministry of Finance amounted to RM3 billion; 1MDB investment agreement in PetroSaudi company;

The 1MDB investment money in the Cayman Islands has either been brought back to Malaysia; and International auditing firm to approve 1MDB accounts.

1.3. Interim ReportThe Interim Report was tabled to the National Accounts Committee (PAC) on 9 and 10 July 2015 for reporting audits conducted between 10 March and 15 June 2015. The Interim Report is limited to deliberating on the analysis of financial statements and investments in joint venture companies PetroSaudi, a murabahah note and Segregated Portfolio Company (SPC). PA has requested JAN to review some additional aspects to take into account in preparing the Final Report.

1.4. Final Report

This Final Report contains an analysis of the financial statements and financial position of the Group 1MDB until the financial year ending 31 March 2014 and its investment performance in equity, murabahah notes, portfolio funds, SRC groups, property and energy sectors. This Final Report takes into account the issues that have been reported in the Interim Reports and have been updated according to documents received until October 31, 2015.

2. OBJECTIVES OBJECTIVESThe audit is conducted on the mandate of the Cabinet and the PAC to verify the audited financial statements of the 1MDB Group and to evaluate the financial performance and activities of the 1MDB Group whether or not they meet the objectives of the establishment.

3. SCOPE AND AUDITING METHODOLOGY3.1. The revised JAN is conducted on the audited financial statements of the 1MDB Group for the financial period ended 31 March 2010 until the financial year ended 31 March 2014. The financial statements for the year ended 31 March 2015 have not been submitted to JAN as it has not been prepared by 1MDB for auditing. However, JAN has conducted audits based on the relevant documents and records.

3.2. An audit was carried out using the following methods: Review of the Memorandum and Articles of Association of the Company, minutes of Board meetings and related documents of incorporation of the company; Revisions to documents relating to policies and procedures, business models used and the laws and regulations established by Terengganu Investment Authority Berhad (TIA) and 1MDB; Review of agreements, contracts and related financial documents; Interviews with the Board of Directors and the management of the company and the previous and current auditors at the company and its subsidiaries level; Financial analysis is based on the audited financial statements of the Company and its subsidiaries from 2010 to 2014;

Reviewing and analyzing auditing papers of private audit firms; Review of the evidence of PAC proceedings related to 1MDB; Site visit to several 1MDB real estate investment projects and projects; Financial analysis based on the financial statements for the period ended 31 March 2012 Group SRC

International Sdn. Bhd. (SRC), which is from the date of its establishment on 7 January 2011 until the date of transfer to the Minister of Finance Incorporated (MKD) on 15 February 2012. Validation of investments made prior to the transfer was taken into account until the date of the response on 3 December 2015; and Collaboration with Bank Negara Malaysia (BNM) for financial and investment transactions involving domestic and foreign financial institutions.

4. LIMITATION OF EXPERIENCE4.1. JAN faces limitations when conducting audits where part of the original and important document is passed on or not submitted by 1MDB for the purposes of transaction validation and as audit evidence. This limitation has a significant impact on the audits carried out in terms of verifying the financial position and operations of the company as well as related transactions. Some important documents that are not submitted are as in the following table:

TABLE 1.1 DOCUMENTS NOT UNDERSTANDING BY 1MDB

INFORMATION

i. 1MDB Group's financial position for financial year 2015:

a. Management Account (Management Account); and

b. Group Financial Statement 1MDB

II. Statement / Confirmation of bank from external financial institution:

a. Singapore

BSI Bank-Brazen Sky

Deutsche Bank -1MDB Energy Holding Ltd.

b. Hong Kong

Falcon Private Bank Ltd.

1MDB Energy Ltd.

1MDB Energy (Langat) Ltd.

c. Switzerland

BSI Bank, Lugano

o 1MDB Global Investments Ltd.

d. United Kingdom

Bank of New York Melon

o 1MDB Energy Ltd.

o 1MDB Energy (Langat) Ltd.

o MDB Global Investments Ltd.

4.2. No access can be made to computers, notebooks and servers at 1MDB to obtain data and information for cross referrals and analysis during auditing.

4.3. JAN also did not receive a 1MDB Management / Operations Meeting Minutes from 2009 to October 31, 2015 and Minutes of Board of Directors of the joint venture / subsidiary company as follows:

1MDB PetroSaudi Ltd.

1MDB International Holdings Ltd.

1MDB Global Investments Ltd.

Brazen Sky Ltd.

SRC-Aabar Resources Ltd.

1MDB Energy Holdings Ltd.

1MDB Energy Ltd.

1MDB Energy (Langat) Ltd.

5. ESTABLISHMENT OF 1MALAYSIA DEVELOPMENT BERHAD5.1. The Finance Minister Incorporated (MKD) has taken over Terengganu Investment Authority Berhad (TIA) set up by Terengganu Incorporated Menteri Besar (MBI Terengganu) on 27 February 2009. The original purpose of the TIA establishment was to create a sovereign wealth fund with an initial fund of RM11 billion. The fund will be derived from a total of RM6 billion worth of oil royalty revenues and funds from bond issues on local and overseas financial markets with the Federal Government's proposal to provide a guarantee of RM5 billion based on Terengganu's future oil revenues.

5.2. The Cabinet meeting on April 1, 2009 approved the TIA application so the Federal Government guaranteed TIA to borrow up to RM5 billion from local and overseas financial markets through Islamic Medium Term Notes (IMTN) for investment. Guarantee issued is in accordance with the Loan

Guarantee (Corporations Incorporation) Act 1965 covering principal and interest repayments for a period of 30 years.

5.3. On May 15, 2009, a program agreement was signed between TIA and AmInvestment Bank Berhad for the issue of IMTN issues amounting to RM5 billion. However, the TIA plan was rejected by MBI Terengganu. Subsequently, the Federal government decided to take over the TIA. The acquisition was completed on 31 July 20009 and the name TIA was changed to 1Malaysia Development Berhad (1MDB) on 25 September 2009.

5.4. Once taken over by the Federal Government, 1MDB is no longer a sovereign wealth fund but as a strategic development company that becomes a wholly-owned company of MKD with authorized capital of RM1 billion and paid-up capital of RM1,000,002. In line with the 1MDB vision to become a strategic catalyst to help bring new ideas and sources of growth and enhance the country's competitiveness in the economy especially in the global environment, 1MDB is given the key mandates among them:

Invest in projects that can help drive strategic initiatives for long-term sustainable development and encourage inflows of foreign direct investment into the country.

Use the existing sovereign wealth fund network in the Middle East and China to bring in foreign direct investment that corresponds to national projects.

5.5. Since its inception, 1MDB has been involved in the investment as follows: Joint venture with PetroSaudi Holdings (Cayman) Ltd .; Investments in Segregated Portfolio Company (SPC); Investment in SRC Group; Investment in real estate sector; and Investment in the energy sector. The description of the investment made by 1MDB is described in the next chapters.

6. GOVERNMENT STRUCTURE AND GROUP ORGANIZATION STRUCTURE 1MDB6.1 Based on 1MDB Company Memorandum and Articles of Incorporation (M & A), the 1MDB governance structure is divided into three levels namely the Advisory Board, the Board and the Top Management. The Advisory Board is

responsible for providing guidance and investment advice as well as business. Article 117 of M & A has outlined some of the decisions needing written permission from the Honorable Prime Minister that includes the following: Any change in M & A of the company, whether in whole or in part;

Any appointment and termination of any director (including the Managing Director and Alternate Director) and the Company's Supreme Management; and any financial commitments (including investments), restructuring or security matters issued by the Federal Government of Malaysia for the interests of the company, national interest, national security or any Federal Government policy of Malaysia. For this purpose, the determination of the meaning of 'national interest', 'national security' and 'policy of the Federal Government of Malaysia' shall be finalized by the Federal Government of Malaysia.

6.2. Membership rating of Advisory Board, Board of Directors and Top Management 1MDB on 31 October 2015 and list of Board Members from 2009 to 2014 are as follows:

TABLE 1.2 LIST OF 1MDB ADVISORY LIST ON OCTOBER 2015

NAME POSITION

YAB Dato 'Sri Mohd Najib Tun Abdul Razak Prime Minister and Minister of Finance of Malaysia (Chairman)

Sheikh Hamad bin Jassim Bin Jabr Al-Thani Former Prime Minister and Qatar's Foreign Minister (Special Adviser)

Tan Sri Mohd Sidek Hassan Petronas chairman

Tan Sri Dato 'Nor Mohamed Yakcop Deputy Chairman Khazanah Nasional Berhad

Tan Sri Dr. Ali Hamsa chief Secretary

Tan Sri Dr. Mohd Irwan Serigar Abdullah Treasury Secretary General

Khaldoon Khalifa Al Mubarak Chairman of the Abu Dhabi Executive Affair Board; and Chief Executive Officer & Managing Director, Mubadala Development Company

Chang Zhenming Chairman and President, CITIC Group China

Source: 1MDB Website

TABLE 1.3 1MDB DIRECTOR LIST ON OCTOBER 2015

NAME POSITION APPOINTMENT OF DATE

Tan Sri Dato 'Seri Che Lodin Wok Kamaruddin

Chairman October 20, 2009

Non - Executive Director 11 August 2009

Tan Sri Dato 'Paduka Ismee Ismail Non - Executive Director March 23, 2009 *

Datuk Shahrol Azral Ibrahim Halmi Non - Executive Director March 23, 2009 *

Tan Sri Dato 'Ong Gim Huat Non - Executive Director 12 January 2010

Ashvin Jethanand Valiram Non - Executive Director February 2, 2010

Arul Kanda Kandasamy President and Executive Director January 5, 2015

Source: Website 1MDB Note: (*) Appointment On TIA Name (TIA Changed Name To 1MDB On September 25, 2009)

TABLE 1.4 1MDB HIGHEST MANAGEMENT LIST ON OCTOBER 2015

NAME POSITION

Arul Kanda Kandasamy President and Group Executive Director

Azmi Tahir Chief Financial Officer

Ivan Chen General Counsel

Vincent Koh Beng Huat Chief Investment Officer

Badrul Hisham Abdul Karim Executive Director of Business Development

Terence Geh Choh Heng Executive Director of Finance

Source: 1MDB Website

TABLE 1.5 POSITION OF 1MDB BOARD OF DIRECTORS FROM 2009 TO 2014

NAME

FINANCIAL YEAR

31.3.2010 31.3.2011 31.3.2012 31.3.2013 31.3.2014

Tan Sri Mohd Bakke Bin Salleh *

(appointed on 27.02.2009 and 11.08.2009 and resigned on 07.04.2009 and 19.10.2009) **

✓ X X X X

Tan Sri Azlan Mohd Zainol *(appointed on 11.08.2009 and resigned on 11.01.2010)

✓ X X X X

Christophor Lee Sian Teik *(appointed on 27.02.2009 and resigned on 23.03.2009)

✓ X X X X

Datuk Shahrol Azral Bin Ibrahim Halmi * (appointed on 23.03.2009) ✓ ✓ ✓ ✓ ✓

Tan Sri Dato 'Paduka Ismee Bin Haji Ismail * (appointed on 23.03.2009) ✓ ✓ ✓ ✓ ✓

Tan Sri Dato 'Seri Che Lodin Bin Wok Kamaruddin *(appointed on 11.08.2009)

✓ ✓ ✓ ✓ ✓

Tan Sri Dato 'Ong Gim Huat(appointed on 12.01.2010) ✓ ✓ ✓ ✓ ✓

Ashvin Jethanand Valiram(appointed on 02.02.2010) ✓ ✓ ✓ ✓ ✓

Mohd. Hazem Bin Abd. Rahman(appointed on 15.03.2013 and resigned on 01.01.2015)

X X X ✓ ✓

Source: 1MDB Document

Note: (*) Appointment of TIA (TIA changed name to 1MDB on 25 September 2009) (**) Appointed Position and Reappointed

6.3. In 2009 and 2010, 1MDB only had one subsidiary, namely 1MDB Real Estates Sdn. Bhd. formerly known as City Streams Sdn Bhd. and a sub-subsidiary, Raintree Summit Sdn. Bhd. as in Appendix A. Beginning in 2011, 1MDB's activities have grown into three sectors, namely investment holding, real estate and energy related. In line with this, the number of companies in the 1MDB Group has increased to 10 companies as in Appendix B. In 2012, the 1MDB Group restructured its organizational structure to increase its number to 18 companies as in Appendix C.

6.4. Subsequently in 2013, the 1MDB Group has grown rapidly as companies began to invest in the energy sector by taking over the independent power producers. The largest acquisition was made by the acquisition of Powertek Energy Sdn. Bhd. which has 57 existing companies. The development of the 1MDB Group structure is shown in detail in Appendix D.

6.5. In 2014, the Group's 1MDB structure continued to grow with the acquisition of Jimah O & M Sdn. Bhd. Dan Jimah Teknik Sdn. Bhd. which operates in the energy sector, makes the entire 1MDB Group company to 96 companies. The development of the 1MDB Group's organizational structure is detailed in Appendix E.

CHAPTER 2

ISLAMIC MEDIUM TERM NOTES, EQUITY INVESTMENT, MURABAHAH NOTES AND PORTFOLIO FUNDS

16 July 2016

1. ISLAMIC MEDIUM TERM NOTES ISSUE (IMTN)1.1. TIA was incorporated on 27 February 2009 under the auspices of His Majesty the Sultan of Terengganu who supported the idea of establishing it as a state sovereign wealth fund with an initial fund of RM11 billion. The fund will be sourced from bond issues on local and overseas financial markets with the Federal Government's proposal to provide a guarantee of RM5 billion on Terengganu's future oil revenues. The fund is expected to be derived from a total of RM6 billion worth of oil royalty revenue and the issuance of Islamic Medium Term Notes (IMTN) of RM5 billion.

1.2. On 25 March 2009, the TIA Board of Directors has authorized Mr Shahrol Azral (TIA's Chief Executive Officer) to confirm the appointment of AmInvestment Bank Berhad (AmBank) as lead arranger and / or lead manager and primary subscriber for the proposed RM5 billion IMTN issue and to hold consultation on the terms of the appointment of AmBank, to be recommended to the TIA Board of Directors.

1.3. The Cabinet meeting on April 1, 2009 approved the TIA application so that the Federal Government assured the TIA to borrow up to RM5 billion from local and overseas financial markets through IMTN for investment in accordance with the Loan Guarantee Act (Bodybuilding) Act 1965. These guarantees include refunds principal and interest for a period of 30 years.

1.4. The first meeting of the TIA Board on April 15, 2009 has agreed with the proposal to issue a RM5 billion IMTN syariah-compliant bond with a 3-year term to secure funds for general investment and working capital. The TIA Board also agrees that there is no need to create the Due Diligence Working Group and provide the Due Diligence Planning Memorandum as the information on IMTN does not need to be submitted to the Securities

Commission before being offered to prospective investors. This is because the bonds are guaranteed by Government.

1.5. Terengganu Menteri Besar through a letter dated 13 May 2009 to the YAB Minister of Finance state the State Government's support for the issuance of IMTN amounting to RM5 billion by the TIA with certain terms.

1.6. On May 15, 2009, the program agreement was signed between TIA (issuer) and AmBank as lead arranger, lead manager and facility agent . On the same date, the Federal Government has issued Government guarantees for the issuance of IMTN amounting to RM5 billion.

1.7. However, the signing of a government guarantee and program agreement without the terms and plans of Terengganu Menteri Besar Incorporated (MBI Terengganu) as a TIA shareholder has caused dissatisfaction and objection from MBI Terengganu. Accordingly, pursuant to Article 94 of the Articles of Association of the Company, the Board of TIA approved three resolutions dated 22 May 2009, directing the suspension of the IMTN issues until the structure of corporate governance and best practice was established including the establishment of the Company's Advisory Board and Investment Panel and appointing the Board of Directors representing all the special shareholders. The TIA Board of Directors at that time was YAM Tengku Rahimah Puteri Ibni Almarhum Sultan Mahmud, Datuk Ismee Ismail and Mr Shahrol Azral.

1.8. The TIA Board of Directors through a resolution dated 22 May 2009 has also decided that Mr Shahrol Azral take immediate action on an urgent basis to inform the IMTN issue advisor to terminate and suspend all affairs relating to the issuance of IMTN and to ensure that no IMTN issues are made. The TIA Board of Directors also decides to suspend the powers conferred on Encik Shahrol Azral or any other director in connection with the issuance of IMTN.

1.9. However, the Chief Executive Officer and Company Secretary of TIA have signed a Subscription Agreement with AmBank on 25 May 2009, three days after the resolution of the TIA Board which directs the postponement of the IMTN issue and any affairs related to the IMTN program. The TIA Chief Executive Officer's actions are against the directives of the TIA Board.

1.10. On May 26, 2009, aqad agreement for the sale of assets by AmIslamic Bank Berhad to TIA was signed by TIA Chief Executive Officer. On the same date, a Murabahah Purchase Agreement amounting to RM4.396 billion and a

Murabahah Sales Agreement amounting to RM13.625 billion has also been signed by the TIA Chief Executive Officer.

1.11. Mr Shahrol Azral's acting as TIA Chief Executive Officer continued his affairs related to IMTN had caused him to be dropped as a director of the company as decided on a TIA shareholders resolution dated 27 May 2009 pursuant to Section 152A of the Companies Act 1965. This action is also in accordance with Article 73 of the Memorandum and The Articles of Association of the Company which permit the abatement of any company directors by a written resolution. The action was supported by the letter of Terengganu MBI dated 29 May 2009 to the Honorable Minister of Finance. MBI Terengganu has raised serious weaknesses and stating the stance that disagrees with the method of derivative of IMTN which does not follow the terms and plans of Terengganu MBI. Terengganu MBI's representative on the TIA Board of Directors,

1.12. On May 29, 2009, TIA received net IMTN proceeds of RM4.385 billion from the full value of RM5 billion. This is because IMTN is issued at RM87.92 for every RM100 nominal value, at a discount of 12.08%. The TIA Board of Directors at the meeting on 20 August 20009 was informed that the bonds were issued at such discount rates based on AmBank's recommendation as lead arrangerto ensure that IMTN issues get full subscription. In addition, the interest rate charged is 5.75% per annum with an effective return rate of 6.68% per annum. The JAN revised the total cost of the IMTN issues up to the maturity of RM13.625 billion comprising RM5 billion for principal payments (lump sum payable in 2039) and RM8.625 billion for profit payments to IMTN bond holders over a period of 30 years. Transaction costs amounting to RM11.25 million have been paid to AmBank as arranger fee . In addition, a trustee fee and agency fee of RM7.14 million are also payable, at a rate of RM238,000 per annum for 30 years.

1.13. MBI Terengganu has also written a warning letter dated 29 May 2009 to AmBank allegedly involved in misconduct and incompatibility during the issuance of IMTN.

1.14. The Cabinet has been notified on 3 June 2009 that DYMM Sultan Terengganu has requested a report prepared on the Unauthorized Issuance of IMTN by TIA and Report of Managing Oil Royalty of the state of Terengganu as a Sovereign Wealth Fund with the Best Corporate Governance Practice and Transparency.

1.15. During the meeting on June 30, 2009 chaired by the Treasury Secretary General, Shahrol Azral explained that a letter from the State Government of Terengganu (letter dated 27 May 20009 directs the issuance of IMTN deferred), only received after the marketing process which started one week earlier, and the subscription was closed on May 29, 2009. IMTN issuance is continued due to a brief period of instruction and to maintain TIA's credibility if the issue is deferred. While during the JAN interview with Datuk Shahrol Azral in June 2015, the former TIA Chief Executive Officer admitted that the IMTN bond issue had to be continued as the program agreement signed on May 15, 2009 was a buy deal where AmBank waslead arranger and primary subscriber have received secondary market subscriptions for the issuance of the bond.

1.16. JAN's review found at the Board of Directors' Meeting on 10 October 2009, Mr Shahrol Azral informed the IMTN issue to be expedited upon the request of TIA's special adviser with the intention of developing Bidong Island in collaboration with Mubadala's company in 2009. The AmBank (who was also present at the meeting) confirming that TIA's special advisers have called on the issuance of bonds secured. However, through a press statement on May 23, 2009, Mubadala denied its involvement in Malaysia other than the project in the Iskandar Development Region. JAN's review found that TIA special advisor appointed on April 8, 2009 was Dato 'Abdul Aziz bin Mohd Akhir and Mr Low Taek Jho.

2. TIA RECEIVING OF FEDERAL GOVERNMENT AND CHANGE OF NAME TO 1MDB2.1. Following TIA's action continued the issue of RM5 billion IMTN and ignored the Terengganu MBI order to delay the program, the Terengganu Government sought to separate its entitlement from TIA, by submitting the TIA and IMTN program to be taken over by the Federal Government. The TIA meeting chaired by the Treasury Secretary General on 16 June 2009 and 30 June 2009 has discussed and agreed that the Minister of Finance Incorporated (MKD) takes over control and equity in TIA which will be released by MBI Terengganu.

2.2. On July 20, 2009, the Minister of Finance informed the Cabinet on the decision of the Federal Government through the MKD taking over the TIA from Terengganu MBI. Among the considerations to consider are as follows:

a. MKD bought all the ordinary shares owned by MBI Terengganu and paid back the paid-up capital involving a total payment of RM1,000,002.

b. The Federal Government will continue to be the guarantor for IMTN bonds of RM5 billion.

c. IMTN issuance is estimated at RM5 billion to be used for investments in strategic development areas.

d. The financial implications of the Federal Government for the TIA takeover process are estimated at RM1,550,002.

e. TIA loan receipts are retained in fixed deposits at AmBank and RHB Bank with interest payments of 2.0% only. This means that the TIA experienced an interest loss of 3.75% during the period of May 29, 2009 until the TIA fund could be fully invested.

f. Total interest loss in the period from 29 May 20009 to 15 September 2009 amounted to RM56 million. Profit payment to bondholders is once every six months and the first payment of RM143.75 million on 30 November 2009. The principal repayment amounted to RM5 billion at the same time in 2039.

2.3. On July 31, 2009, TIA was taken over by the Federal Government. On 11 August 2009, three new Board of Directors were appointed to make the Board a total of five, namely. Shahrol Azral bin Ibrahim Halmi. On August 20, 2009, Mr. Shahrol Azral bin Ibrahim Halmi (former Chief Executive Officer of TIA Berhad) was appointed as the Managing Director of the company with immediate effect.

2.4. On 4 September 2009, the TIA Board of Directors approved the change of TIA name to 1MDB. This name was officially approved by the Companies Commission of Malaysia (SSM) only on 25 September 20009. The JAN found that the new name was used earlier in some cases where the name 1MDB was used for the appointment letter of the Board of Directors and the Chief Executive Officer dated 17 September 2009. The JAN found that the letter of appointment took effect backdated from 11 August 2009. According to the Attorney-General, this act is permissible in terms of communication and no legal issues .

2.5. While letters from PetroSaudi International Ltd. (Saudi Arabia) and Prince Turkey dated 28 August 2009 have proposed a long-term partnership with 1MDB. This shows that 1MDB's management has unofficially

communicated with PetroSaudi International Ltd. and used the name 1MDB before the Board approved the adoption of the 1MDB name on 4 September 2009.

3. BUSINESS PROJECTS SAME WITH PETROSAUDI INTERNATIONAL LIMITED

3.1. Proposed Establishment of Joint Venture Project3.1.1. This joint venture project began with the letter of Prince Turki dated 28 August 2009 to the Honorable Prime Minister of Malaysia (YAB PM) accompanying letter from Encik Tarek Obaid (Chief Executive Officer of PetroSaudi International Ltd.) who also dated 28 August 2009 to introduce PetroSaudi International Ltd . to YAB PM. The letter was later extended to 1MDB management for further action.

3.1.2. Mr Tarek Obaid's Letter contains a proposed USD1 billion 1MDB shareholding of 1MDB in a joint venture between 1MDB and PetroSaudi International Ltd. While PetroSaudi International Ltd will contribute assets in the USD2 billion energy sector into the joint venture. The letter also states PetroSaudi International Ltd. agreeing to provide a goodwill valuation discount making its asset contribution valued at USD1.50 billion.

3.1.3. The proposed set of shareholding ratios, cash flow of USD1 billion, asset value and goodwilldiscountassets not rated as stated in Mr. Tarek Obaid's letter indicate that the project has been planned earlier. However, the JAN review found no information about the letter of PetroSaudi International Ltd. and Prince Turkey in connection with this joint venture proposal are tabled to the 1MDB Board during a special meeting discussing the investment. The Chairman of 1MDB Board stated that the ratio of cash assets to joint venture companies has not been finalized at 1MDB Board meeting on September 18, 2009. If the joint venture proposal has been finalized and identified from the early stage, the 1MDB Board should be briefly described by the management regarding the decision on this joint venture proposal,

3.2. Special Meeting of the 1MDB Board on 18 September 20093.2.1. The proposed project proposal paper under an initiative between the Government of Malaysia and the Government of Saudi Arabia (provided by

the Investment Division officer, reviewed by Executive Director of Business Development and supported and approved by 1MDB Chief Executive Officer) has been submitted for consideration by the Board of 1MDB during a meeting at 18 September 2009. The three main objectives of the joint venture project are to invest in and outside Malaysia; to support long-term economic development in Malaysia; as well as to enhance relations and cooperation between Malaysia and Saudi Arabia.

3.2.2. At the special meeting, Mr Casey Tang (Executive Director of Business Development 1MDB) during a briefing on this joint venture project to the Board requested the cooperation of all parties to ensure that the joint venture agreement was concluded on the planned date of 28 September 2009. The date which is too short should not happen because the investment decision involves a large amount but no specific project that requires immediate investment.

3.2.3. The 1MDB Board of Directors has been informed that this project is an affair between the Government of Malaysia and the Kingdom of Saudi Arabia (G2G). Mr. Casey Tang also informed that PetroSaudi International Ltd. is owned by King Abdullah and the Kingdom of Saudi Arabia and has been in existence since 2000. The acknowledgment by Mr Casey Tang is also acknowledged by several Board members and former Board of Directors of 1MDB during a JAN interview with them in June 2015. The JAN can not verifying the actual status of this company's registration whether PetroSaudi International Ltd. owned by King Abdullah or Kingdom of Saudi Arabia. Review of PetroSaudi International Ltd.'s website found that the company was only established in 2005, privately owned and has no ownership link with the Kingdom of Saudi Arabia. JAN's review also found Mr Tarek Obaid is the sole director of PetroSaudi International Ltd. based on documentsWritten Resolution of the Sole Director of the Company . Therefore, the statement made by Mr. Casey Tang was found to be inaccurate.

3.2.4. On September 18, 2009, a foreign company, PetroSaudi Holdings (Cayman) Limited, has registered a company under the name of 1MDB PetroSaudi Limited in British Virgin Island (BVI). The company is then used as a joint venture between 1MDB and PetroSaudi Holdings (Cayman) Ltd. Joint venture with PetroSaudi International Ltd. was only informed to the 1MDB Board for the first time in the meeting on September 18, 2009. Registration of 1MDB PetroSaudi Ltd. (BVI) shows that 1MDB's management has decided ahead of time to work with PetroSaudi International Ltd. and the

1MDB Board of Directors are only informed later. No record showing the 1MDB Board has been notified of the special purpose vehicle, namely 1MDB PetroSaudi Ltd. (BVI) has been registered or established.

3.2.5. The JAN's review of several documents related to this project found that there are four different companies registered under the name of PetroSaudi, as in the following table:

TABLE 2.1

LIST OF COMPANIES LISTED HISTORY OF PETROSAUDICOMPANY NAME

PLACE OF REGISTRATION

DATE OF REGISTRATION

PetroSaudi International Ltd.

Saudi Arabia Year 2005

PetroSaudi International

Cayman Islands 24 February 2009

PetroSaudi Holdings (Cayman) Ltd.

Cayman Islands 18 September 2009

PetroSaudi International Ltd.

Seychelles No information

Source: Company Document of Establishment

3.2.6. Under a joint venture agreement between 1MDB and PetroSaudi Holdings (Cayman) Ltd. dated 28 September 2009, PetroSaudi Holdings (Cayman) Ltd. has been referred to in the abbreviation 'PSI' whilst based on the Written Resolution of the Sole Director of the Companywhich was signed by Mr. Tarek Obaid, PetroSaudi Holdings (Cayman) Ltd. has been referred to as 'PHS'. A media statement dated September 30, 2009 also announced the signing of a joint venture between 1MDB and PetroSaudi International

Ltd. (PSI), while the actual joint venture agreement was signed with PetroSaudi Holdings (Cayman) Ltd. In most cases, abbreviations for PSI are always used for PetroSaudi International Ltd. (Saudi Arabia). This shows that the PSI brief name used in this joint venture agreement seems to imply that PetroSaudi Holdings (Cayman) Ltd. is the same entity as PetroSaudi International Ltd. (Saudi Arabia). The Board also does not realize that PSI refers to PetroSaudi Holdings (Cayman) Ltd. Therefore,

3.2.7. The 1MDB Board of Directors during the meeting on 18 September 2009 has decided that three directors are appointed and two of them have professional qualifications as 1MDB's representatives in the joint venture. However, no evidence indicates that the proposal was implemented.

3.2.8. The 1MDB Board directs management to ensure PetroSaudi International Ltd. contributed its share of the joint venture through 50% in cash or at least USD1 billion and another 50% in the form of assets to a joint venture company. However, the management of 1MDB did not execute the directive of the Board but had implemented Mr Tarek Obaid's proposal in a letter dated 28 August 2009.

3.2.9. The Board also does not have detailed information on PetroSaudi International Ltd. and one of the Board members has been directed to obtain further information and profile of PetroSaudi International Ltd. This profile is not submitted and has been informed by management that information is being obtained. However, based on JAN's interview with 1MDB Board member, the profile was never presented to the Board until the joint venture agreement was signed. This is unusual for a joint venture deal involving a large cash investment at an instant.

3.2.10. On 18 September 2009, the 1MDB Board has asked the management to further consult with PetroSaudi International Ltd. and finalize some important things before concluding the agreement as follows:

a. Make a deal with PetroSaudi International Ltd. to resolve issues raised by the 1MDB Board to get better terms of negotiation. This should be re-reported to the Board.

b. Appoint Dato 'Mohd Bakke and Encik Shahrol Azral as corporate representatives in each joint venture company meeting once the 1MDB company is registered as a shareholder of the joint venture. The JAN review further found that the appointment of Dato 'Mohd Bakke was replaced by Mr. Casey Tang.

c. The company's seal must be sealed on any document pertaining to joint venture with PetroSaudi International Ltd.

3.2.11. This clearly shows that the 1MDB Board has provided conditional approval to the management to establish a joint venture with PetroSaudi International Ltd. because they are unaware of the existence of other subsidiaries of nearly identical names, namely PetroSaudi International and PetroSaudi Holdings (Cayman) Ltd. This was confirmed by several Board and former Board of Directors of 1MDB during the JAN interview in June 2015.

3.3 Special Meeting of 1MDB Board on 26 September 20093.3.1. The Special Meeting of the 1MDB Board was held on 26 September 2009, two days before the joint venture project was signed. During this meeting, the Board is still discussing whether to continue investing in this joint venture.

3.2.2. However, the 1MDB Board has approved the participation in a joint venture project with PetroSaudi International Ltd. with a subscription of one billion ordinary shares in 1MDB PetroSaudi Ltd. subject to the following conditions:

a. Appointing independent professional valuers to assess the assets of a joint venture;

b. Appoint three members representing 1MDB in the Board of Directors of joint venture companies including those who are experienced in the appropriate sector; and

c. As a wind up option , one party will offer shares to other shareholders at fair market value or at a value agreed upon by both governments who have an interest in the agreement.

3.3.3. Letter from Edward L. Morse's rating dated 20 September 2009 informed 1MDB management that he would be appointed by 1MDB and 1MDB PetroSaudi Ltd. to implement independent assessments of PetroSaudi International Ltd.'s hydrocarbon assets and its subsidiaries. However, until the meeting on 26 September 2009, the 1MDB Board of Directors was not informed.

3.3.4. The joint venture agreement states that 1MDB is eligible to appoint two directors in the composition of the Board of Directors of this joint venture. This shows the terms set by the Board of 1MDB to appoint three members representing 1MDB on the Board of Directors of the joint venture company are not complied with.

3.3.5. In view of this, the 1MDB Board has approved the use of common seal on all joint-venture documents with PetroSaudi International Ltd. This shows that the Board approves participation in a joint venture project only with PetroSaudi International Ltd. and not with other companies.

3.4 Joint Venture Agreement dated 28 September 20093.4.1. On September 28, 2009, a joint venture agreement was signed between 1MDB, PetroSaudi Holdings (Cayman) Ltd. and 1MDB PetroSaudi Ltd. in Kuala Lumpur. PetroSaudi Holdings (Cayman) Ltd. and 1MDB PetroSaudi Ltd. represented by Mr. Tarek Obaid, while 1MDB was represented by Mr. Shahrol Azral. The ceremony was also witnessed by YAB Prime Minister of Malaysia and Prince Turki. The objectives of the joint venture company as stated in the joint venture agreement are:

a. "To seek, explore, enter into and participate in business and economic opportunities within and outside of Malaysia; and

b. To enhance, strengthen and promote the future prosperity and economic development of Malaysia, to the extent that achievement of above-mentioned objectives would maximize the profits of the Company. "

3.4.2. Under this joint venture agreement, 1MDB will invest USD1 billion in cash (40% equity stake) while PetroSaudi Holdings (Cayman) Ltd. contributing in the form of assets valued at not less than USD1.50 billion (60% equity stake) in this joint venture company.

3.4.3. JAN's review of the joint venture agreement found some questions and contradictions in the information in the agreement. This joint venture company, 1MDB PetroSaudi Limited, was registered on September 18, 2009 in the British Virgin Island by PetroSaudi Holdings (Cayman) Limited. Based on the Cayman Islands Registry of Companies search reports, PetroSaudi Holdings (Cayman) Limited was established on September 18, 2009. This shows that the two companies were set up on the same date.

3.4.4. In a joint venture agreement clause states 1MDB PetroSaudi Ltd. (established on September 18, 2009) has received a USD700 million advance loan on September 25, 2009 from its parent company, PetroSaudi Holdings (Cayman) Ltd. The advance loan is repayable in full on or before 30 September 2009. The existence of a USD700 million advance loan for this five-day period raises the question. JAN's review found no minutes or documents indicating that the 1MDB Board was informed of the USD700 million advance loan before the joint venture agreement was signed. In addition, JAN interviews with the 1MDB Board (former and current) in June 2015 found that the advance loan was never disclosed or discussed by 1MDB management before the joint venture project was finalized. A copy of USD700 million loan agreement between 1MDB PetroSaudi Limited and PetroSaudi Holdings (Cayman) Limited signed by Mr. Tarek Obaid representing both companies has been submitted by 1MDB management but the JAN can not confirm it with original documents.

3.4.5. Although the draft agreement was discussed during the meeting on 18 September 2009 but the draft agreement was also not allowed by 1MDB to JAN. JAN's review of documents submitted by Datuk Shahrol Azral to JAN on 5 June 2015 found Mr Brian Chia (Messrs Wong & Partners) via email dated September 30, 2009 questioned the letter requesting a repayment of USD700 million advance loan using PetroSaudi International Ltd. letterhead which gives the advance loan is PetroSaudi Holdings (Cayman) Ltd. The e-mail dated September 30, 2009 while the transfer of money for the repayment of the loan was also made on the same date.

3.4.6. This agreement dated 28 September 2009 also stipulates that the subscription of one billion shares by 1MDB in the joint venture amounted to USD1 billion is payable fully on or before September 30, 2009. This shows that 1MDB is only given a very short period (two days) to make payment USD1 billion to 1MDB PetroSaudi Ltd. The 1MDB Board of Directors at a meeting dated 26 September 2009 approved a transfer of USD1 billion to the bank account of the joint venture company for the purpose of subscription of shares in 1MDB PetroSaudi Ltd.

3.4.7. As at 30 September 2009, Bank Negara Malaysia (BNM) granted approval for funds transfer into joint venture accounts at JP Morgan SA and RBS Coutts Bank Ltd. (Geneva). As of September 30, 2009, a total of USD300 million has been transferred to the 7619400 account at JP Morgan (Suisse) SA, namely 1MDB PetroSaudi Ltd. However, the remaining USD700 million has been transferred to the 11116073 account at RBS Coutts Bank

Ltd., owned by another company that is not involved with this joint venture project. Based on the document submitted by Datuk Shahrol Azral on June 5, 2015 and his statement at the National Accounts Committee meeting on November 25, 2015, the account belongs to Good Star Limited, a subsidiary of the PetroSaudi Group since 1 September 2009.

3.5 Rating Report by Edward L. Morse dated 29 September 20093.5.1. Edward L. Morse's valuation through its letter dated 20 September 2009 informed his company to be appointed by 1MDB and 1MDB PetroSaudi Ltd. to implement independent assessments of PetroSaudi International Ltd.'s hydrocarbon assets and its subsidiaries. The appointment letter was signed by Mr Shahrol Azral on September 29, 2009 which was on the same day that Edward L. Morse's assessment report dated 29 September 2009, a day after the joint venture agreement was signed on 28 September 2009. Given the complexities of assets to be evaluated, Edward L. Morse can issue the assessment report within eight days.

3.5.2. Assessment by Edward L. Morse Energy Advisory Services has been implemented on PetroSaudi International Ltd.'s assets (oil exploration and production rights). While the joint venture agreement clearly states that the company owning all rights and interests of the agreed assets for this joint venture project is PetroSaudi International Cayman, a company other than PetroSaudi International Ltd. The joint venture agreement also states that on the date of the agreement, PetroSaudi Holdings (Cayman) Ltd. has transferred all issued shares of PetroSaudi International Cayman (which owns all rights and interests in assets with a value of USD2.70 billion) to 1MDB PetroSaudi Ltd. The report also can not verify the assets owned by PetroSaudi Turkmenistan 1 Limited (Jersey company) and Petro Saudi Ltd. Inc. (Panama company). The actual ownership of the assets involved in this joint venture project can not be confirmed as no documents were submitted to 1MDB or JAN auditors to prove the exact date that PetroSaudi International Cayman assets have been transferred to 1MDB PetroSaudi Ltd.

3.5.3. This report is relevant to the exploration and production rights of various locations in Argentina and Turkmenistan. In accordance with item 1.1 of the Overview of Assets in the appraisal report states, valuers only review project economics without assessing geological resources, property rights, including contractual rights to the field . This indicates that oil production rights for Block 3 areas in Turkmenistan and Argentina have not

yet been confirmed. This is because the area has long been a dispute between various parties. This limited information is a constraint on the appraisal report.

3.5.4. In this report it was also explained that the block was originally owned by Buried Hill Energy, a company registered in Panama through a sale and purchase agreement with the Turkmen Government. However, current ownership of the rights to the block is not disclosed. Therefore, the consent to accepting an asset as equity in a joint venture investment may be considered unrealistic and at high risk.

3.5.5. The report also noted many constraints, including PetroSaudi International Ltd. unable to provide cash flow capital that can be used for comparison with assets in Turkmenistan because it does not have the ability to evaluate the evolution of royalty and fiscal regimes as well as check the value comparison procedures. This shows PetroSaudi International Ltd. have no expertise to deal with complex assets. While paragraph 4 of the appraisal report states that assets in Argentina are non-tradable and non-transactional assets. However, assets have been valued based on high and low estimates ( high & low estimates) which shows a high risk of assets in Argentina. This shows that 1MDB failed to evaluate the assumptions used by valuers relating to production, petroleum prices, discount rates and capital and operating expenses. This valuation report only assesses the rights to assets only rather than the value of the company owning these assets. Therefore, the net value of this company is also not disclosed. All such constraints are the risks to the accuracy of the assessment report.

3.5.6. At a meeting on October 3, 2009, the 1MDB Board expressed their concern about the reliability of the appraisal report as it had been prepared for a short period as previously it was informed that the evaluation report would take several months and could only be made available in March 2010. Clause in agreement a joint venture that stipulated 1MDB should appoint an independent valuer to assess the assets of PetroSaudi Holdings (Cayman) Ltd. and the report must be submitted on or before September 30, 2009 is an unreasonable determination. The 1MDB Board of Directors at the meeting also asked the management to obtain an evaluation report and arrange an explanation by Edward L. Morse at the next meeting.

3.6. 1MDB Board of Directors' Meeting on 3 October 2009

3.6.1. At this meeting, the 1MDB Board of Directors expressed dissatisfaction when their orders were omitted and the use of funds was channeled to others without their knowledge. The views of the Board are as follows:

a. The Board of Directors is not informed of the change of plans to transfer a total of USD700 million from 1MDB into an account that is not a joint venture company.

b. The Board of Directors is also not advised on the conversion of a bank account of a joint venture company from BSI-SA (Geneva) to JP Morgan (Suisse) Geneva. This raises the question as the revision of JAN obtains approval for the transfer of this bank account is made by a resolution dated September 30, 2009 (ie on the same date the transfer was made), but the JAN interview with some former Board members found they were unaware of the existence of this resolution despite their signature at the resolution.

c. The Board is also less clear about the status of ownership of assets held by joint venture companies and the quality of assets transferred to joint venture companies including inherent / potential risks inrelation to the assets.

d. The Board also notes that this amount of investment requires a thorough and detailed consideration and needs to undergo due diligence .

e. The Board is of the opinion that all actions have taken place in a very short period of time and have compromised with key controls and checks and balances that are essential to safeguarding the interests of 1MDB. The Board is also puzzled by the speed of appraisal reports provided by Edward L. Morse.

f. The Board has given firm orders to 1MDB's Chief Executive Officer and management not to deviate from the instructions given and to adhere to the agreed procedures.

g. The Board is of the view that the management has ignored the company's core thrust to focus on attracting foreign investment into Malaysia.

3.6.2. In this regard, the 1MDB Board directs the management to take corrective action as follows:

a. Determine whether a total of USD700 million from PetroSaudi Holdings (Cayman) Ltd. can be reinstated so that the funds can be channeled according to the original resolution;

b. Obtain written confirmation from JP Morgan on the approval of the use of funds kept in the joint account;

c. Obtain written confirmation that the assets injected by PetroSaudi Holdings (Cayman) Ltd. was owned by a joint venture company and obtained a copy of the appraisal report by Edward L. Morse as well as legal views for Board considerations;

d. Arrange meetings with Edward L. Morse appraisers and legal counsel to brief the Board at the next Board meeting.

e. Obtain written confirmation of the quality of the assets (including the quality and lifetime of oil wells, political risks and other potential risks relating to assets placed in a joint venture); and

f. The Board is still dissatisfied and directs the management to appoint an independent valuer to re-evaluate the assets in a joint venture.

3.6.3. Based on documentary evidence and interviews with the former 1MDB Board, the JAN review found that the directives of the Board were not complied with by 1MDB's management. It is observed that the approval given by the Board is for cooperation with PetroSaudi International Ltd. and not with its subsidiary, PetroSaudi Holdings (Cayman) Ltd.

3.6.4. It is arguable that 1MDB's management has repeatedly disobeyed the specific instructions given by the Board. Among them are as follows:

a. Signing a joint venture agreement on 28 September 2009 before taking action on the matters required by the Board. This led to the 1MDB Chief Executive Officer and management being reprimanded and warned at 1MDB Board meeting dated 3 October 2009.

b. Not performing a second assessment of the assets of a joint venture as directed by the Board on 3 October 2009.

3.6.5. Although 1MDB's CEO was found to be inconsistent with directives, guidelines and corporate governance, the 1MDB Board of Directors still did not take any action against him.

3.7. 1MDB Board of Directors' Meeting on 10 October 2009

3.7.1. During this meeting, the Board of Directors of 1MDB raised the asset valuation requirements in which the management was asked to obtain 10 reputable valuer names for shortlist and obtain the approval of the Chairman of the Advisory Board. As such, management can discuss with PetroSaudi Holdings (Cayman) Ltd. for the appointment of the second valuer.

3.7.2. Furthermore, the 1MDB Board has instructed 1MDB's Chief Executive Officer to provide a comprehensive summary paper to the Chairman of the Advisory Board which contains the chronological events of the joint venture agreement, funding status and Board of Directors 1MDB's discrepancies on PetroSaudi Holdings (Cayman) Ltd. assets valuation report However, during the 1MDB Board of Directors' meeting on November 7, 2009, Mr Shahrol Azral made no second assessment on the assets of the joint venture as the Chairman of the Advisory Board disagreed with the proposal, but directed the 1MDB Board to appoint a consulting company to assess the ownership of the company joint venture. However, JAN's review found no document that could prove the appointment of the consultation had been made.

3.7.3. JAN's review finds that the joint venture agreement has a clause stipulating that all financial reports, accounts and operations need to be submitted to shareholders on a quarterly basis. However, the documents can not be submitted by 1MDB for the revision of JAN. During the joint venture project period, the 1MDB Board was not informed where the fund was invested by joint venture companies although Mr. Shahrol Azral and Mr. Tang Keng Chee were appointed as 1MDB's representatives in the joint venture. The JAN also did not submit any documents to prove the investment made by this joint venture company.

3.7.4. Nonetheless, although the 1MDB Board is dissatisfied with some of the 1MDB's management actions, JAN finds no evidence that this matter has been referred to the Chairman of the 1MDB Advisory Board in writing. Meanwhile, 1MDB Board Chairman during the PAC meeting on 19 January 2015 informed that the Board of Directors of 1MDB was completely dissatisfied with the way the management handled the affairs related to the joint venture project but agreed to further clarification and confirmation given by 1MDB's management.

3.7.5. JAN's analysis summarizes the decision to make equity investments in the joint venture, namely 1MDB PetroSaudi Limited is an action without strategic planning for being made within eight days, without detailed assessment and prior to resolving the issues raised by the Board

earlier. Joint venture agreements also contain clauses that do not care for the interests of the company