S- Sustainability Resources: Budgeting and Cost. Agenda 1. Discuss readings- Brooks Chapters 6, 7...

49

S- Sustainability Resources: Budgeting and Cost

-

Upload

gregory-logan -

Category

Documents

-

view

216 -

download

2

Transcript of S- Sustainability Resources: Budgeting and Cost. Agenda 1. Discuss readings- Brooks Chapters 6, 7...

S- Sustainability

Resources:

Budgeting and Cost

Agenda

1. Discuss readings- Brooks Chapters 6, 7 Brainstorm sources of cost and income

2. Hands On Activity – Work as a team to Fill in Parameters for First Place Fund for Youth (p.96)

Once you have established Community Need

developed a Logic Model and formed and Assessment Plan, the next question is, how you will pay

for or SUSTAIN your program.Needs Assessment

CostLogic Model

Mobilizing Resources

1. Define the Capabilities Needed

2. Devise a Human Resource Outline to meet each capability need

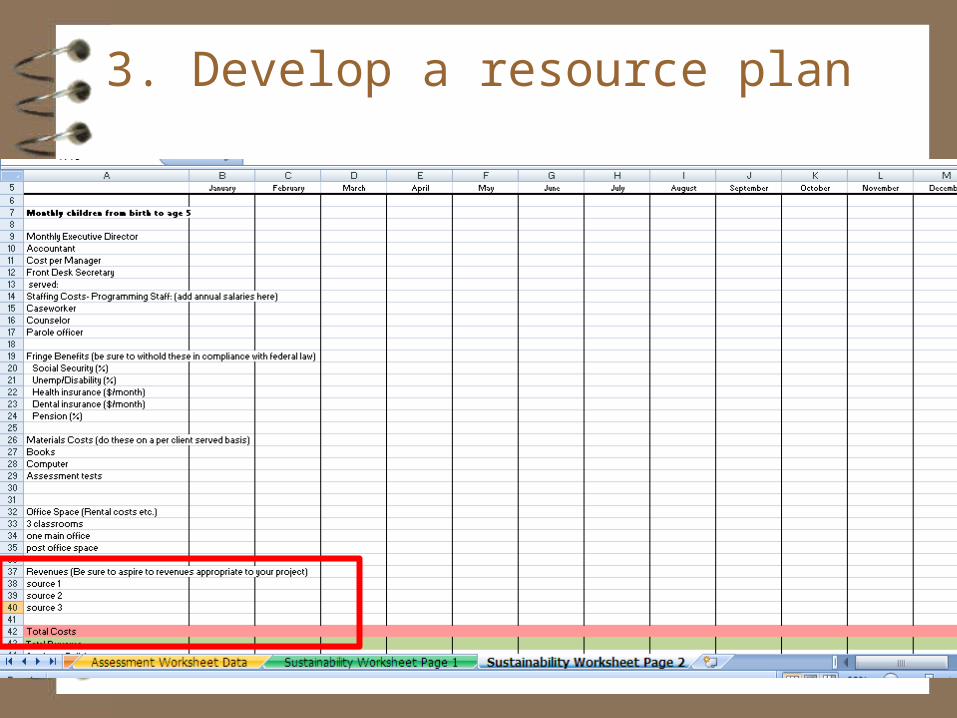

3. Develop a resource plan

4. Put on the Numbers

Brooks Ch 6 p 86

1. Define the Capabilities Needed

Start by reflecting on the activities and who will

do them.

Figure 6.1 The Capabilities – Resource Model

Core ventures functionsAdministration

Technical supportLegal advice

.

.

What capabilities do we need?

Social entrepreneurHired help

SubcontractorsVolunteers

.

.

Who will provide them?

MoneyHuman effort

Expertise..

How will we meet the capabilities?

Earned revenuesBorrowed funds

Donated money and timeGovernment funds

.

.

Where will the resources come from?

Core ventures functionsAdministration

Technical supportLegal advice

.

.

What capabilities do we need?

Social entrepreneurHired help

SubcontractorsVolunteers

.

.

Who will provide them?

MoneyHuman effort

Expertise..

How will we meet the capabilities?

Earned revenuesBorrowed funds

Donated money and timeGovernment funds

.

.

Where will the resources come from?

Figure 6.1 The Capabilities – Resource Model

Core ventures functionsAdministration

Technical supportLegal advice

.

.

What capabilities do we need?

Social entrepreneurHired help

SubcontractorsVolunteers

.

.

Who will provide them?

MoneyHuman effort

Expertise..

How will we meet the capabilities?

Earned revenuesBorrowed funds

Donated money and timeGovernment funds

.

.

Where will the resources come from?

Core ventures functionsAdministration

Technical supportLegal advice

.

.

What capabilities do we need?

Social entrepreneurHired help

SubcontractorsVolunteers

.

.

Who will provide them?

MoneyHuman effort

Expertise..

How will we meet the capabilities?

Earned revenuesBorrowed funds

Donated money and timeGovernment funds

.

.

Where will the resources come from?

2. Devise a Human Resource Outline to meet each capability need

3. Develop a resource plan

Figure 6.2 Sources of income for American nonprofits*

Government funding, 33%

Private donations, 20%

Fee income, 47%

* Salamon 2002

Figure 6.3 Types of earned income for social enterprises

Commercial endeavors Other activities

Direct programs TransactionsSeparately-incorporated

ventures

Earned income

Licensing Joint-issue ventures

Table 6.3 The Product Profile Map

Source: James & Young (2006)

High mission impact

Low mission impact

Positive profit Stars Cash cowsLoss-making Saints Dogs

Income sources

Three main sources of nonprofit revenue– Fee income, which is about half of the total– Donations, which are about one fifth– Government, which provides the balance

Different nonprofits rely on different types– Social welfare: 52% government, <1/3 earned– Health: less than 6% is donated– But arts groups are half funded by private giving– Religious institutions are not government funded

Figure 6.2 shows income sources for all nonprofits Figure 6.3 shows social enterprise earned income types

Table 6.4 Revenues from membership dues for various nonprofit enterprises, 2003

Enterprise typePercentage of income

from dues

Labor organizations 66.02%

Social clubs 59.61%

Business leagues 40.27%

Public charities (all 501(c)(3)) 0.90%

Source: Steinberg (2006)

Table 7.1 Source of donations to American nonprofits, 2005

Living individuals 76.5%Foundations 11.5%Bequests 6.7%Corporations 5.3%

Figure 7.1 Average annual contributions to various types of causes and charities among those making positive contributions, 2003

Average annual gift size among givers

$1,825$1,735

$418

$247$359

$167 $198$125 $155

$230$394

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

$1,800

$2,000

Av

era

ge

an

nu

al g

ift

am

on

g t

ho

se

ma

kin

g p

os

itiv

e

co

ntr

ibu

tio

ns

Raising funding is connected to being able to demonstrate effectiveness

http://www.socialresearchmethods.net/kb/pecycle.php

Utilizing results includes for publicity and fund raising for non profits: http://www.9wsyr.com/news/local/story/More-parents-

reading-to-their-kids/MCwPYPKY20SPNrUHf1p0Pw.cspx

4. Put on the Numbers

Activity: p 96 First Place Fund for Youth

Use the CLASS project planning tool to walk through the above 4 steps as a group for “First Place Fund for Youth”

Novel Approaches to Raise Money

Dan Pallota – 1st 10 minutes

To accompany Brooks Ch 8 Entrepreneurial Fundraising and

Marketing

For Discussion: Dan Pallotta: The way we think about charity is dead wrong

http://www.youtube.com/watch?v=bfAzi6D5FpM

Inspirational Stories from Students For Final Project

http://www.localsyr.com/bridge-street/video/d/video/jennifer-

nadler-lemoyne-speaker-bridge-street-3271/5011371

Soc Club Events on Video

Local grad to pedal cross country for area's homeless

http://www.localsyr.com/mostpopular/story/Local-grad-to-pedal-cross-country-for-areas/d/story/UpgtCu_Jf0yzmb3zHuVUKQ

Father and daughter continue mission for special needs playground near Phoenix

http://www.youtube.com/watch?v=w6lx18ubmyo

First list all of your assumptions in a sheet/tab called parameters

Crucial for Final Project

This exercise will help you complete the S portion of your final project

For your final project DO NOT just tweak your Imagination Library budget- it will likely lead to many mistakes.

Instead start from scratch and build a new smaller budget for your program just like we will practice today – Use the last 2 tabs of your Project Planning Tool in Excel

1. Daycare Budget than explore the full flexible spreadsheet

- Use digital handout parameter sheet, run scenarios as a class

The Scenario: Use this to complete the Parameters

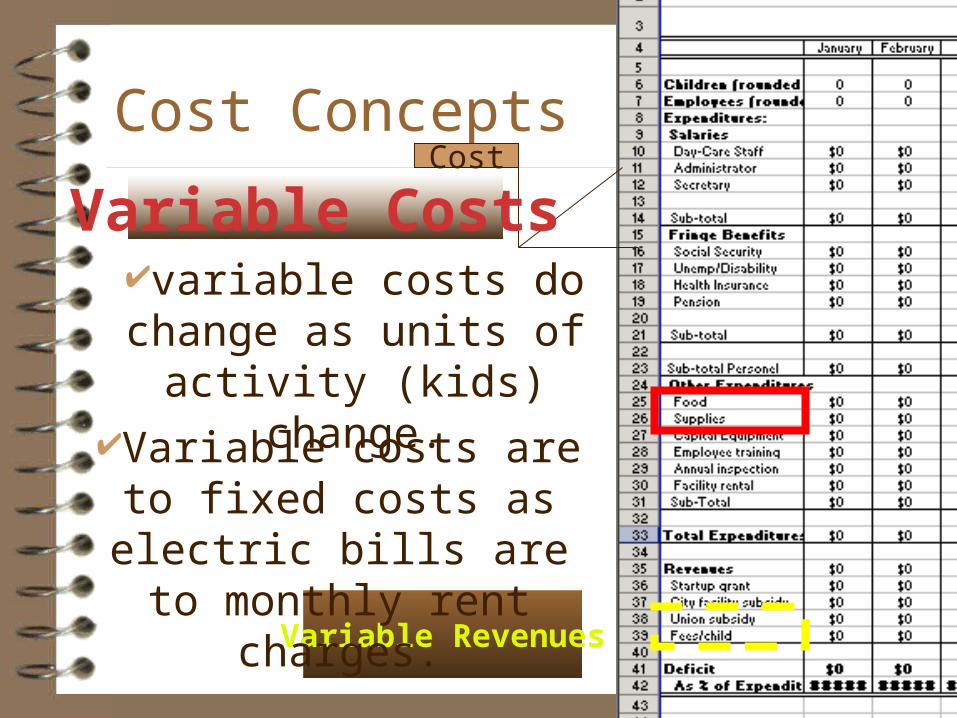

Cost ConceptsCost

OutputVariable Costs

Semi-Variable

Step Costs

Fixed CostsKey question: how does each change

as the cost unit (or unit of activity your agency performs – visits miles,

packages, clients) changes

Cost ConceptsCost

Output

Fixed Costs

Fixed costs do not change as units of

activity (kids) change.

Sheet A-1,cell C 27 is the proportion of the monthly salary we are responsible for (remember we are only one of

the 4 childcare sites see assumption 5 in parameters)

A-1, C25 is _____

Administrator salary/month

Cost DefinitionsFixed vs. Variable

Fixed Costs (do not vary with output):– Top administrators and resources they use.– Financial, legal and other services provided organization.

Variable costs (vary directly with output):– Consumables: materials , supplies, gas used in transportation– Printing/postage/communication– Part time personnel providing service directly– Legal, financial and other services tied directly to output– Equipment (and O&M) used directly in service provision

Semi-variable costs (fixed cost + variable cost per unit):– Phones, utility rates.

Step costs (vary in lump with output):– FT personnel– Facilities/utilities/equipment (and O&M) tied to personnel

Source: Bretschneider

Cost ConceptsCost

OutputVariable Costs

Variable Revenues

Variable costs are to fixed costs as electric bills are to

monthly rent charges.

variable costs do change as units of activity (kids)

change.

Sheet A-1 is a quick clue that it is a parameter. then look for cell C 20

(in sheet a-1)(it is “Food

costs/day/child”)

B6 is the number of children in the

daycare (see previous slide)

A-1, another parameter, C20 is “Work days/month”

Cost ConceptsCost

Output

Semi-variable

Secretary paid by hours of work required, but may require standard

benefits package such as health benefits.

Semi-variable costs do change as units of activity (kids) change but they start

off with a fixed cost.

http://www.labor.ny.gov/stats/lswage2.asp

http://www.labor.state.ny.us/workforceindustrydata/descriptor.asp

http://www.labor.state.ny.us/workforceindustrydata/descriptor.asp

Not needed herebut would be like…=flat cost + (# clients*($5.00))

Cost ConceptsCost

OutputStep Costs

change only when units of activity (kids) reach steps (i.e. by law need one staff member for every 5 kids)

Sheet A-1,cell C 20 is “Work days/month”

B7 is the number of employees

A-1, C 21 is Hours/day/employee (i.e. 8 hours a

day)

A-1, C 24 is Hourly wage--daycare worker (i.e. $6.50/hr)

Share literacy letter as an exemplary solicitation letter – example of where a liberal arts edu can help!

Estimating Personnel Costs

How do I assess the value of volunteers? http://www.independentsector.org/programs/

research/volunteer_time.html Summary: The estimated dollar value of

volunteer time is $19.51 per hour for 2007.

Cost ConceptsCost

OutputVariable Costs

Cost ConceptsCost

Output

Semi-variable

Phone and utilities included in Rental

Cost ConceptsCost

Output

Step Costs

![Budgeting Process [Cost & Management Accounting]](https://static.fdocuments.in/doc/165x107/55a0b1d41a28ab6b5d8b45cf/budgeting-process-cost-management-accounting.jpg)