Ruth Smith, CPS/CAP 2011-2012 Kansas Division Treasurer Leadership Workshop August 13, 2011.

21

Fiduciary Responsibility Ruth Smith, CPS/CAP 2011-2012 Kansas Division Treasurer Leadership Workshop August 13, 2011

-

date post

19-Dec-2015 -

Category

Documents

-

view

215 -

download

0

Transcript of Ruth Smith, CPS/CAP 2011-2012 Kansas Division Treasurer Leadership Workshop August 13, 2011.

Fiduciary Responsibility

Ruth Smith, CPS/CAP2011-2012 Kansas Division Treasurer

Leadership WorkshopAugust 13, 2011

August 13, 2011 2

Responsible for all funds for your respective chapters and for keeping records current

Responsible for complete and accurate record of chapter membership

Generally a member of your Finance/Ways and Means Committee (depending on your chapter bylaws and standing rules)

Responsible for preparing annual budget and event budgets as needed

File tax reports as required• Form 990-N is due November 15

Treasurer Duties

August 13, 2011 3

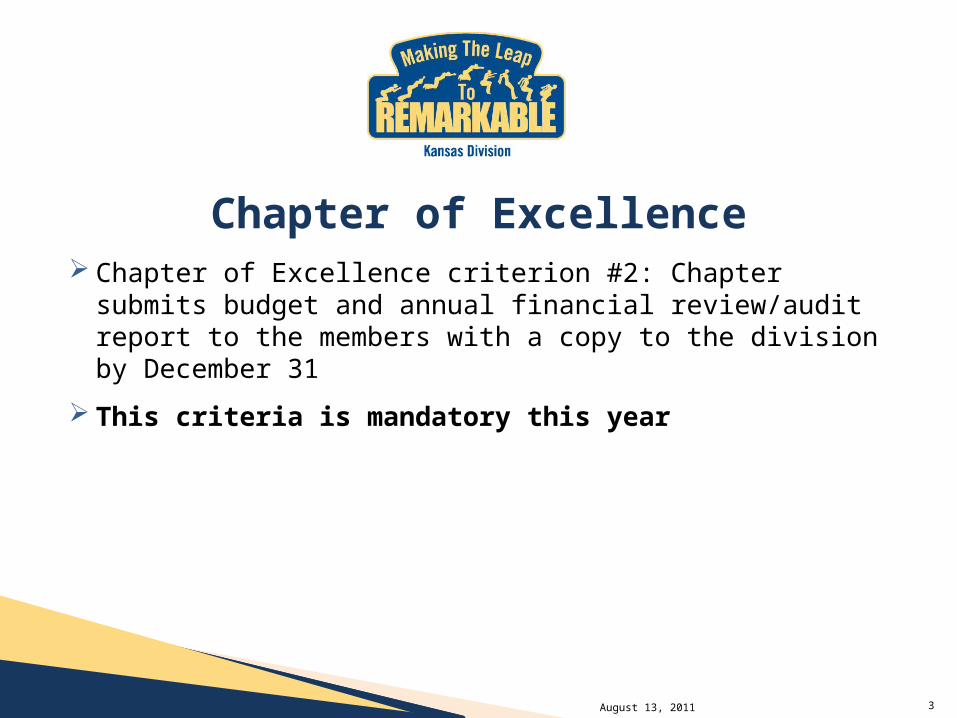

Chapter of Excellence criterion #2: Chapter submits budget and annual financial review/audit report to the members with a copy to the division by December 31

This criteria is mandatory this year

Chapter of Excellence

August 13, 2011 4

Keep board discussions confidential and agree to disagree.

Support a decision once it is made.

Confidentiality

August 13, 2011 5

These are based on IAAP Core Values of Integrity, Respect, Adaptability, Communication, Commitment and include Ethical Business Conduct for IAAP Members for Trust and Behavior.

NOTE: These standards were approved by the International Board of Directors on November 1, 2008.

IAAP Standards of Integrity

August 13, 2011 6

Not-for-Profit 501(c)(6) Nonprofit Business League Tax Status

Contributions to IAAP are NOT tax-deductible• Exceptions are RTF and Research & Education Foundations which

are 501(c)(3) entities• Contributions from Vendors could be considered marketing expense

Tax Status

August 13, 2011 7

Your chapter should have an Employer Identification Number.

Your chapter is exempt from income tax, but not exempt from sales tax – Not eligible for nonprofit postal discounts.

You should provide 1099-MISC form for payments greater than $600 to individuals (not corporations). This includes speakers, entertainment, etc.

Tax Status

August 13, 2011 8

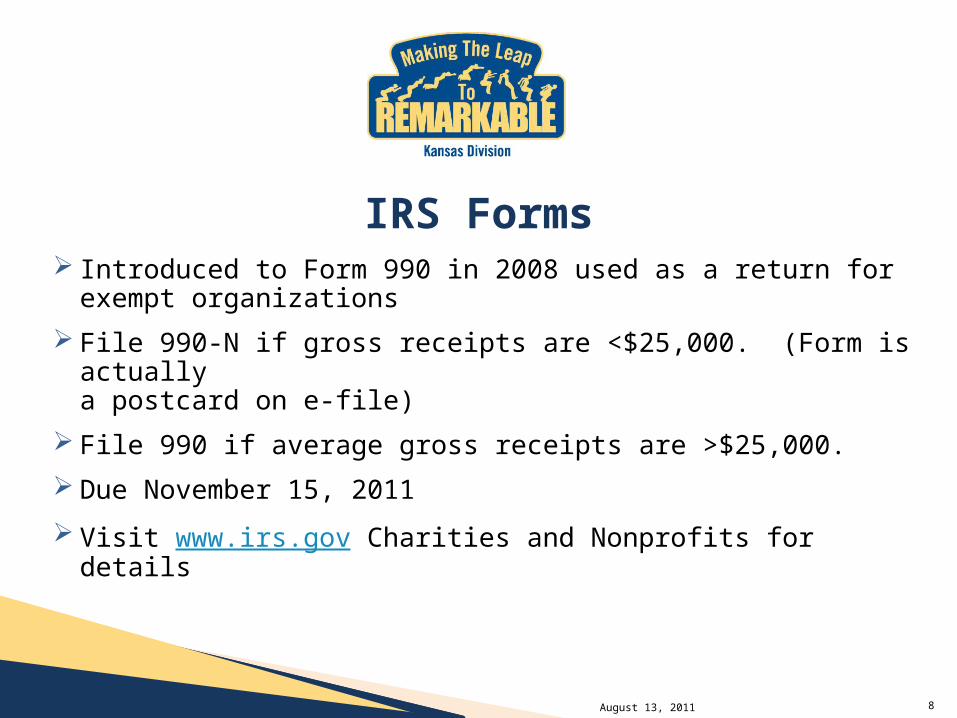

Introduced to Form 990 in 2008 used as a return for exempt organizations

File 990-N if gross receipts are <$25,000. (Form is actually a postcard on e-file)

File 990 if average gross receipts are >$25,000.

Due November 15, 2011

Visit www.irs.gov Charities and Nonprofits for details

IRS Forms

August 13, 2011 9

501(c)(6) status prohibits inurement (financial advantage) to any member.• Distribution must be equitable to all.• Awards must be for actions that benefit entire group

(i.e., recruiting new members) and be in proportion to action.• Should not be donated for member hardship (do individual

collections).

Scholarships are based on academic merit and financial need; all other payments should be termed awards.

Inurement

August 13, 2011 10

Surety Bond• Position bond protects the position; not the individual.

(Office of Treasurer must be bonded and all officers with access to funds should be bonded (usually treasurer and president).

• Coverage is based on average funds handled in the fiscal year, increasing as needed.

• Can be purchased through any insurance, but HQ has competitive rates through Tallman Insurance.

• Bonds only available in 3-year increments and expire April 2019

Third-Party Liability insurance protects chapter assets against lawsuits.

Protecting Your Chapter

August 13, 2011 11

Review revenues, expenses and in-kind donations for the past 2-3 years.

Solicit input from board and committee chairs regarding planned programs for the year.

Present budget to board and membership for approval and adoption.

Regularly compare actual income/expenses to budget. Should have budget for general funds and additional

budgets for special events (i.e., APW events)

Budgets

August 13, 2011 12

Drawing is the correct term for use of tickets, entry slips, etc.

Raffles are specifically those which use entry forms with detachable stubs and require a permit from city and/or state.

Games of chance held only during chapter meetings may be acceptable, but you need to check local laws.

Fundraising

August 13, 2011 13

Work with your membership chair for member transfers, reinstatements, etc. • Remind members that renewing on time is a mandatory

Member of Excellence criteria and avoids reinstatement fee.

Membership

August 13, 2011 14

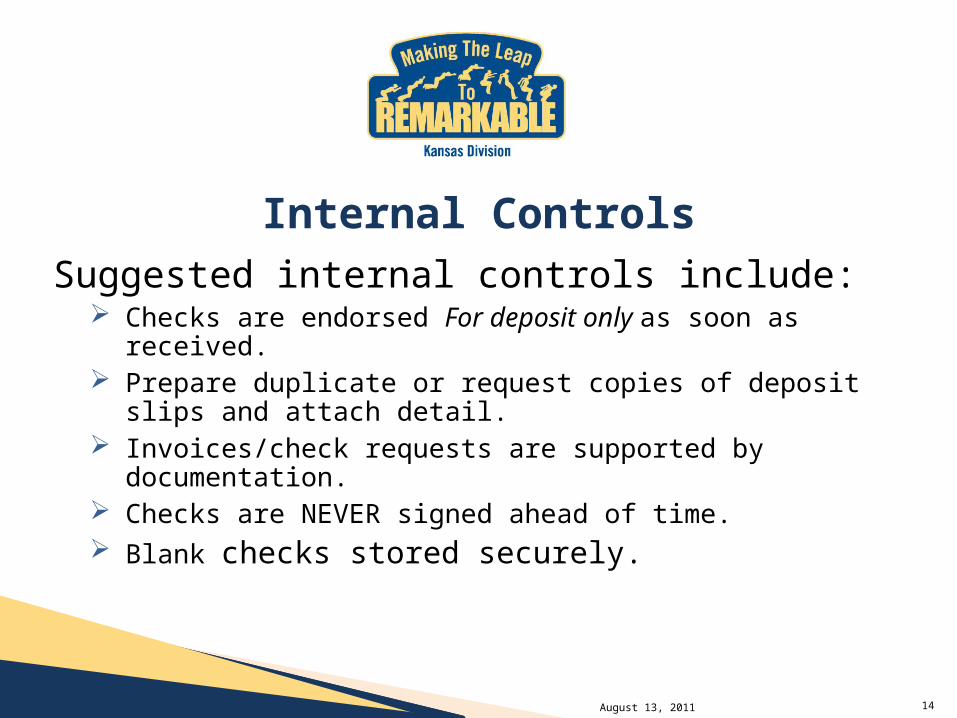

Suggested internal controls include: Checks are endorsed For deposit only as soon as received. Prepare duplicate or request copies of deposit slips and

attach detail. Invoices/check requests are supported by documentation. Checks are NEVER signed ahead of time. Blank checks stored securely.

Internal Controls

August 13, 2011 15

Financial Review Internal Review

• Members assigned to provide an evaluation and/or monitor the reporting and financial practices; or,

• Accounting professional will review records to assess the validity of numbers and speak with appropriate officers.

Audit External Review

• Accounting professional will obtain independent evidence of the numbers, plus look at the internal controls. The accounting professional offers an opinion.

Financial Review vs. AuditWhat’s the Difference?

August 13, 2011 16

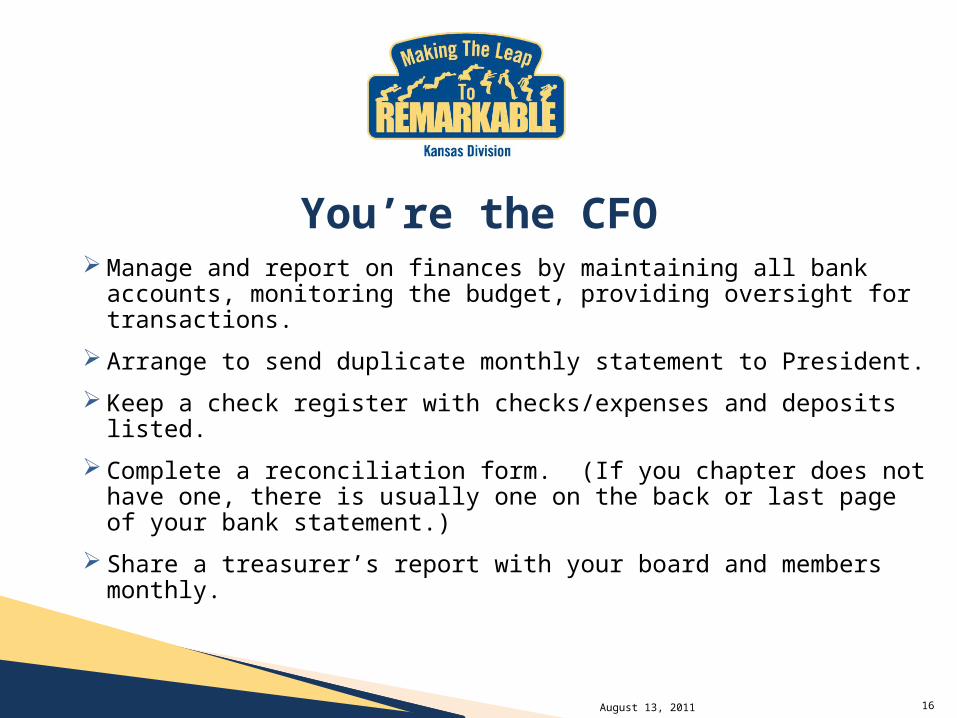

Manage and report on finances by maintaining all bank accounts, monitoring the budget, providing oversight for transactions.

Arrange to send duplicate monthly statement to President.

Keep a check register with checks/expenses and deposits listed.

Complete a reconciliation form. (If you chapter does not have one, there is usually one on the back or last page of your bank statement.)

Share a treasurer’s report with your board and members monthly.

You’re the CFO

August 13, 2011 17

Know and understand your financials.

Monitor expenses to maintain the budget.

Keep your eye on investment rates and adjust accordingly.

All members should know and understand their chapter’s policies and procedures related to their budget.

Having complete knowledge or expertise on financials is not a requirement, but common sense is essential.

“A strategic plan without a solid financial plan is just spending.” Rob Batarla in Associations Now. January 2011 issue.

How to be a Good Fiduciary Steward

August 13, 2011 18

Q: According to Fenton Crackshell, who is the richest individual in the world?

Fun Financial Facts

August 13, 2011 19

A: Scrooge McDuck or Uncle Scrooge, is a Scottish anthropomorphic duck created by Carl Barks that first appeared inFour Color Comics #178, Christmas on Bear Mountain, published by Dell Comics in December 1947.

Fun Financial Facts

August 13, 2011 20

A: Scrooge McDuck or Uncle Scrooge, is a Scottish anthropomorphic duck created by Carl Barks that first appeared inFour Color Comics #178, Christmas on Bear Mountain, published by Dell Comics in December 1947.

Q: What is his net worth?

Fun Financial Facts

August 13, 2011 21

A: Trick question. It’s the same as yoursand mine. Net worth = Assets minus liabilities

Fenton Crackshell (Scrooge's accountant) notes that McDuck's money bin contains 607 tillion 386 zillion 947 trillion 522 billion dollars and 36 cents.

In 2007, Forbes estimated his wealth at $28.8 billion; in 2011, it rose to $44.1 billion due to the rise in gold prices.[

Fun Financial Facts