Effects of Nitrogen Fertilizer Rate, Timing, and Herbicide ...

Russian Nitrogen Fertilizer Marketg

TFI’s Outlook and Technology ConferenceCharleston South Carolina U S A

LONDON | RALEIGH | WASHINGTON | BEIJING

Charleston, South Carolina, U.S.A.11-13 November, 2008

31 Mount Pleasant, London WC1X 0AD UK Tel +44 20 7903 2132 Fax +44 20 7833 4973

www.crugroup.com

Presentation Overview

� Country Profile: Natural Gas Reserves

� Nitrogen Industry: Overview and Recent Developments

� Agriculture� Agriculture

� Fertilizer Consumption� Breakdown by Regions and Products

Hi t d F t

� Domestic Fertilizer Trading

� History and Forecast� Agricultural Equipment for Fertilizer Application

� Key Domestic Players in Nitrogen Fertilizer Segment

� Overview of Russian Biofuel: Market of Future

� Domestic Market Overview� Domestic Market Overview

� Conclusion

� Drivers for Growth� Threats for Stagnation

2

Country Profile: Natural Gas Reserves (I)Russia’s Position in Global Ranking by Gas Reserves and Production, 2006

Reserves Production

RussiaIran

QatarS di A bi

RussiaUSA

CanadaI

(26%) (21%)

Saudi ArabiaU.A.E.

USANigeria

IranNorwayAlgeria

UKAlgeria

VenezuelaIraq

Kazakhstan

IndonesiaSaudi Arabia

TurkmenistanNetherlands

0 10 20 30 40 50

Other (>35 countries)

Trillion cubic meters

0 250 500 750 1000

Other (>35 countries)

Billion cubic meters

Source: BP (Reserves: Proved Reserves at end of 2006)

Country Profile: Natural Gas Reserves (II)Structure of Gas Reserves in Russia by Ownership in 2006, % and trillion cubic meters

Undistributed/Non-licensed Fund

16%

Gazprom

7.8RosneftLukoil

Novatek Gazprom(controlledreserves)

63%29.8510.2

IndependentProducers

21%

NovatekNorthgas

SurgutneftegazTNK-BP

Itera, etc.

Total Volume of Gas Reserves in Russia: 48 t illi bi t48 trillion cubic meters

4Source: Gazprom (Reserves as per 31.12.2006)

Russian Nitrogen Industry: Overview (I)Nitrogen industry of Russia is an export oriented industry: it is the 1st or 2nd leadingexporter in the world for all straight nitrogen products Domestic market is rather a exporter in the world for all straight nitrogen products. Domestic market is rather a strategic or balancing profit issue.

AMMONIA UREA AN UAN

17 plants 12 plants 11 plants 4 plantsNumber of Plants

8% 4% 21% 7%

Plants

Share in World’sProduction

19% 13% 39% 22%Share in World’sExports

�2 �2 � 1 � 1Rank in World’sExports

5

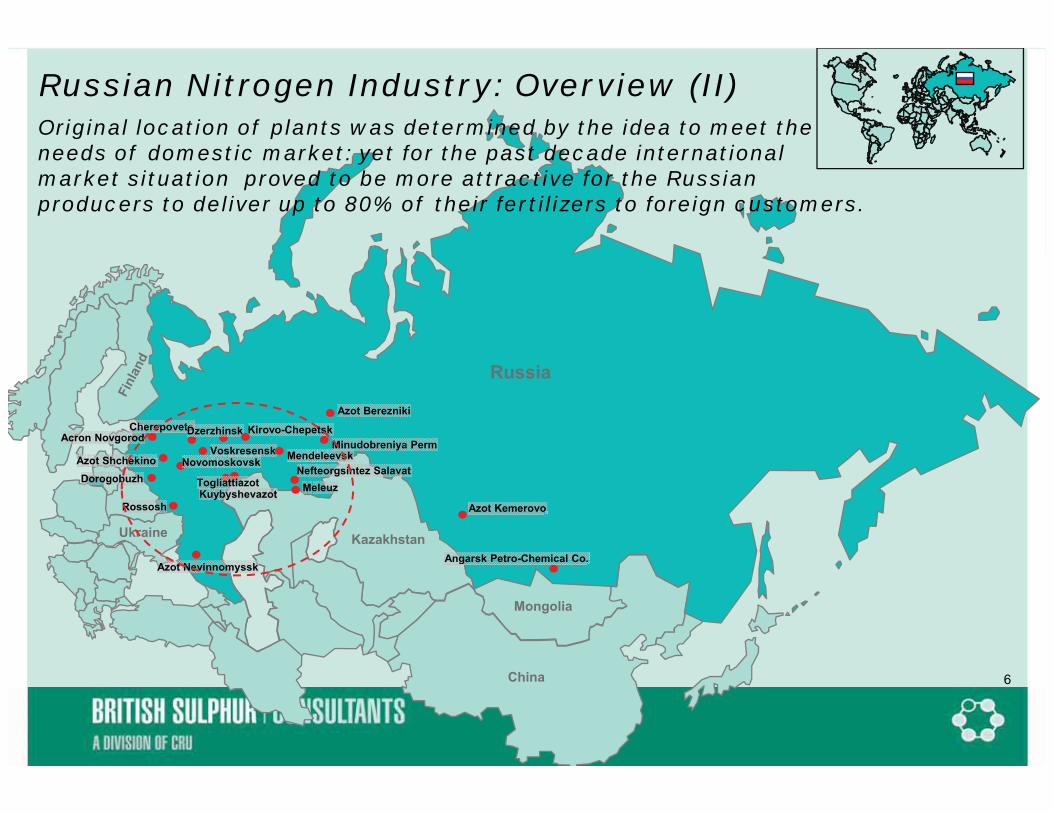

Russian Nitrogen Industry: Overview (II)Original location of plants was determined by the idea to meet the needs of domestic market: yet for the past decade international needs of domestic market: yet for the past decade international market situation proved to be more attractive for the Russian producers to deliver up to 80% of their fertilizers to foreign customers.

Acron Novgorod

Azot BereznikiCherepovets

A t Sh h kiVoskresensk Minudobreniya Perm

Kirovo-ChepetskDzerzhinsk

Mendeleevsk

Russia

Angarsk Petro-Chemical Co.

Azot Kemerovo

NovomoskovskAzot Shchekino

KuybyshevazotDorogobuzh

Nefteorgsintez SalavatTogliattiazot

Rossosh

Meleuz

Mendeleevsk

KazakhstanUkraine

Angarsk Petro Chemical Co.Azot Nevinnomyssk

Mongolia

6China

Russian Nitrogen Industry: Recent Developments (I)

7

Major Events Inside the Industry and General Impact of Other Related Domestic Factors Russian Nitrogen Industry: Recent Developments (II)

Developmentand expansion

New gas trading “5+5 system” launched

Marketing

Managementfocus on long-term strategies and IPOs ideas

of domestic distributionnetworks

launched

New

Marketingstructurechange:FCA/FOB to CFR/CIF/DAFsales

2004 2006

HoldingAgroprodmir

82004-2006

New projects announcements driven by increasing margins from international sales.

Russian Nitrogen Industry: Recent Developments (III)

Newexporttariffs

Quotarestrictions

to follow (?)

2007 2008 92007-2008Note: VSGC = Vostochno-Sibirskaya Gasochemical Company

Russian Agriculture: Global Indicators� � 1 in the global ranking of barley, sunflower seed, rye, and oats producers in the world.� � 2 th ld t t t d ft Chi � � 2 among the world top potato producers after China.� � 4 among the world’s largest wheat producers after China, India, and the USA. � One of the world leaders in sugar beets, buckwheat, carrots and cabbages production.� Among the top 10 leading exporters of wheat in the world.

C

World WHEAT Producers' Ranking: Top 10 Countries

by Output in 2005 (mln. t)

World BARLEY Producers' Ranking: Top 10 Countries

by Output in 2005 (mln. t)

World OATS Producers' Ranking: Top 10 Countries

by Output in 2005 (mln. t)

96.3

72.0

57.1

47.6

36 9

China

India

USA

Russia

France

15.8

12.1

11.7

10.4

9 0

Russia

Canada

Germany

France

Ukraine

4.6

3.3

1.7

1.3

1 2

Russia

Canada

USA

Poland

Finland36.9

25.5

24.1

23.6

21.6

France

Canada

Australia

Germany

Pakistan

9.0

9.0

6.6

5.5

4.6

Ukraine

Turkey

Australia

UK

USA

1.2

1.1

1.0

0.8

0.8

Finland

Australia

Germany

China

Belarus

21.0

0 20 40 60 80 100

Turkey mln t 4.4

0 4 8 12 16

Spain mln t 0.7

0 1 2 3 4 5

Sweden mln t

10Source: FAO (2005, latest year available)

Russian Agriculture: Domestic Indicators

� The share of rural population is 27% of total country’s population of 143 million people.p p y p p p p

� The largest part – slightly less than 60% - of total area under agricultural crops in Russia in 2007 was used for the production of grains (wheat, barley, oats, rye, and others). Oil crops accounted for about 10%.

Structure of Grains Output by Crop Types in Russia in 2007

(in farms of all types; percentage of the total gross harvest)

Maize for grain5%

Rye5%

Groats2% Grain legumes

2%

( yp p g g )

Barley

Oats7%

Wheat60%

Barley19%

11Source: Federal State Statistics Service of Russia, 2008

Russian Fertilizer (N+P+K) Consumption in Agriculture:Breakdown by Regions (FD = Federal Districts)

Central FD (33%)

Far-Eastern FD (1%)

Volga FD (28%)

Southern FD (27%)

Siberian FD (4%)

88%

12Source: Rosstat (2006), Azotecon, BSC

Russian Fertilizer Deliveries to Agriculture: Breakdown by Products (share estimates in nutrient N value), 2007

AS

MAP5%

DAP1%

Other7%

Urea8%

2%

AN77%

The bulk of N consumed in Russian agriculture is Ammonium Nitrate.The bulk of N consumed in Russian agriculture is Ammonium Nitrate.

AN is the most popular nitrogen fertilizer among Russian farmers and the product is forecast to retain its dominant position in the Russian agriculture in the future.

13Source: BSC estimates, Azotecon // Note: data excludes the amount of fertilizer consumed in industrial sector

Russian Fertilizer Consumption: History and Forecast

kg/ha +74%

19 19 21 21 23 25 2733

14

21

28

35nutrients

Use of Mineral

Fertilizers in Agriculture,

74%

0

7

2000 2001 2002 2003 2004 2005 2006 2007

g ,kg/ha

Use of 2 2

2.5 2.73.0

2 53

3.5

mln t nutrients

+12% CAGR

+2.5% CAGRMineral

Fertilizers in Agriculture,

mln t nutrients

1.4 1.3 1.5 1.3 1.4 1.4 1.5 1.72.0 2.2

00.5

11.5

22.5

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Government’s Target Growth**Acc. to the State Program for the Development of Agribusiness and Regulation

f A i lt l G d ’ R M t i l ’ d F d’ M k t f 2008 2012 14Source: Federal State Statistics Service of Russia, Russian Ministry of Agriculture

of Agricultural Goods’, Raw Materials’ and Food’s Markets for 2008-2012

Russian Fertilizer Consumption: Agricultural Equipment for Fertilizer Application

2830

'000 units

- 35%24

2220

19 181820

25 Scattering/Spreadingmachines for solid mineral fertilizers

M hi f i1513

1110 99

87

6

10

15Machines for organicfertilizer application (solid)

Machines for organic fertilizer application6 5 5

0

5

2002 2003 2004 2005 2006 2007

fertilizer application(liquid)

While old agricultural equipment wears down and fails to function, it is being replaced by the new modern machines for fertilizer application, which are more efficient and long-lasting.

15Source: Federal State Statistics Service of Russia

Domestic Fertilizer Trading: 2006 - 2008Fertilizer Exchange trading in Russia was recently introduced for the following reasons:

� to make fertilizer market more transparent;� to develop competitiveness of domestic fertilizer sales; � to diversify sourcing opportunities for export deliveries;� to provide alternative options for supply of raw materials .

Moscow Stock Exchange (MSE) Two platforms for fertilizer exchange trading in RussiaUniversal Mercantile Exchange

“UMEX” i St P t b“UMEX” in St. Petersburg

Fertilizer producers involved in fertilizer trading as suppliers of products:� Balakovskiye Mineral Fertilizers, Balakovo� Ammophos Cherepovets� Ammophos, Cherepovets� Azot, Cherepovets� Silvinit� Uralkali� Kuybyshevazot� Kuybyshevazot� Rossosh� Meleuz

Range of fertilizers includes AN, NPK, DAP, MAP, NP, MCP, apatite concentrate, MOP, urea phosphoric acid etc The products are offered as bulk in bags or big bags 16urea, phosphoric acid, etc. The products are offered as bulk, in bags or big bags.

Key Domestic Players in Nitrogen Fertilizer SegmentDomestic Product

Fertilizer sales to domestic market

% of fertilizer sales to Russia in Company’s Company

distribution Portfolio (N)to domestic market

in 2007to Russia in Company s

total fertilizer salesCompany

EuroChem“EuroChem-Agronetwork”includes 23 distributing

centres in Russia

AN, CAN, Urea, UAN, MAP, DAP,

NPK, NP, NK

> Onemilliontonnes

15% in total fertilizer

sales

AcronEstablished in 2005 “Agronova” network

includes 20 distributing

centres in Russia

AN, Urea, UAN, NPK

0.8milliontonnes

22% in total fertilizer

sales

UralchemOne of the new

holdings in Russia:two N plants

Kirovo-Chepetsk and Azot Berezniki

AN, SAN, CAN, Urea,

NPK

0.9milliontonnes

28% in total fertilizer

sales

RossoshSales via the trading house

“Rosagrotrade”AN, NPK

0.52milliontonnes

30% in total fertilizer

sales

KUAZSales via own agrochemical centres,

representativesor dealers

AN, Urea, AS, UAN

0.5milliontonnes

44% in N fertilizer sales of KUAZ

17

Overview of Russian Biofuel: Market of Future

Russian Biofuels Association suggests the development of Russian biofuels’ Russian Biofuels Association suggests the development of Russian biofuels’ market in two stages:

(1) The development of bioethanol for export(2) The development of domestic consumption of bioethanol

R d P d ti i R i

The targeted production growth of rapeseed (one of the bio-crops) in Russia by 2012 is a five-fold increase from the current level.

Rapeseed Production in Russia(gross harvest, mln tonnes)

3.03 0

mln t+400%

0 3 0 30.5 0.6

0.961.30

1.68

2.18

1.0

2.0

3.0 400%

+200%

0.2 0.2 0.2 0.10.3 0.3

0.02000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Government’s Target Growth*18

gSource: Federal State Statistics Service of Russia, Russian Ministry of Agriculture

Russian Domestic Market: Drivers for Growth Strategies focused on domestic market developmentExpansion of distribution networks

FERTILIZERPRODUCERS

GOVERNMENTINTER-

NATIONAL

Decline of international prices Anti-dumping measures’ tighteningPressure of low-cost nitrogen

National priority projects Federal target programsGOVERNMENTNATIONAL

MARKETproducers

Involuntary diversion of some of the traditionally exporting products to domestic consumers.

ede a ta get p og a sFinancial, banking systemExport tariffs and quotas

FOREIGNINDUSTRIAL FOREIGNINVESTMENTS

INDUSTRIALSEGMENT

Foreign investments in Russian agribusinesses developing food processing industry

Biofuel crops segment developmentIncreasing demand for technical purposes

19processing industry

Russian Domestic Market: Threats for Stagnation

� L ft i i l i f tili li ti� Leftover principle in fertilizer applicationapproach in Russian agricultural sector

� Decline of working age population in rural areas� Underdeveloped storage infrastructure for fertilizers

FARMING SECTOR

GOVERN-PRICES

�Inefficiency of governmental support�Lack of systematic�Rising production costs

�Hi h l i i MENTPRICES yimplementation in governmental programs at a regional level

�High logistics costs

20

Conclusion

� Domestic market development is of high strategic value formost fertilizer manufacturers

�In the short-to-medium term the export share will retain itsdominance in Russian nitrogen industry: the country has beenand will remain the major player and exporter in the globalinternational nitrogen trade

� However, domestic market leaves vast opportunities with al t ti l d l t f l l d t tili th ilarge potential development for local producers to utilize theirnitrogen products

� As hedging from more pressure in the global trade at the bottom� As hedging from more pressure in the global trade at the bottomof the cycle the development of the domestic market might be asolution for surplus of products for Russian manufacturers

21

Thank You!

SMarina Simonova

British Sulphur Consultants 22British Sulphur Consultants