Russian Energy: investment opportunities -...

20

Russian Energy: investment opportunities Alexey Teksler First Deputy Minister of Energy of the Russian Federation МАКЕТ MINISTRY OF ENERGY OF THE RUSSIAN FEDERATION 2017

Transcript of Russian Energy: investment opportunities -...

Russian Energy: investment opportunities

Alexey Teksler First Deputy Minister of Energy

of the Russian Federation

М А К Е Т

MINISTRY OF ENERGY OF THE RUSSIAN FEDERATION

2017

2 MINISTRY OF ENERGY OF THE RUSSIAN FEDERATION

Ministry of Energy of the Russian Federation, Center for Energy Research, CDU TEK

RUSSIA – one of the most attractive Emerging Market for investments

MACRO

• FXstabilization

•Recoveringeconomy

•Deceleratinginflation

•Decreasinginterestrates

RUSSIAN OIL

• Lowcostoil&largereserves

• Flexibletaxation

•Cheapvaluation

•Highdividendsandhealthyleverage

RUSSIAN GAS

•Vastmonetizablereserves

•MostcompetitivesuppliertoEurope

• EmergingsuppliertoAsia

• SignificantLNGpotential

RUSSIAN RENEWABLE ENERGY

• FavorableRESregulation

•Ownadvancedtechnologies

•Potentialfortechnologicalcooperation

•RussiasignedParisagreementin2016

3 MINISTRY OF ENERGY OF THE RUSSIAN FEDERATION

Ministry of Energy of the Russian Federation, Center for Energy Research, CDU TEK

Economic growth is back

After recession in 2015 Russian economy has adapted to new reality and is set to grow: Aftera2.8%declinein2015theeconomyiscurrentlyrecovering,withGDPgrowth-0.2%in2016andexpected+2%in2017

Stabilizing FXConsistent monetary policy and oil price recovery helps to stabilize FX and improves predictability. Predictablecentralbankpolicy,slowinginflationandimprovingcommoditymarketsaremakingtheroublemorestable

Inflation is lowInflation reached historical lows. Determinedpolicyfromthegovernmentstabilizingmarketsbroughtinflationdownto5,4%y/yinDecember.(CBRtargetof4%)

Russian economy – on the way to recovery

$

$

4 MINISTRY OF ENERGY OF THE RUSSIAN FEDERATION

Ministry of Energy of the Russian Federation, Center for Energy Research, CDU TEK

KEY TRENDS RUSSIA`S STRATEGIC POSITIONING

Economic growth significantly increases energy demand in developing countries

Russiaisgeographicallywellpositionedtowardsmarketsthatwilldriveenergydemandinthefuture

Gas is aggressively substituting coal in global fuel mix

Russiahasthelargest commercialreserves of natural gas(~20trillionm3)

Global warming concerns affect energy policy

Russia’s energy mix is among the «greenest» among the world’s top economies with the share of gas and renewables standing at over 50 % and 20 % respectively

Russian energy sector is well positioned to help the world overcome future energy challenges

5 MINISTRY OF ENERGY OF THE RUSSIAN FEDERATION

Ministry of Energy of the Russian Federation, Center for Energy Research, CDU TEK

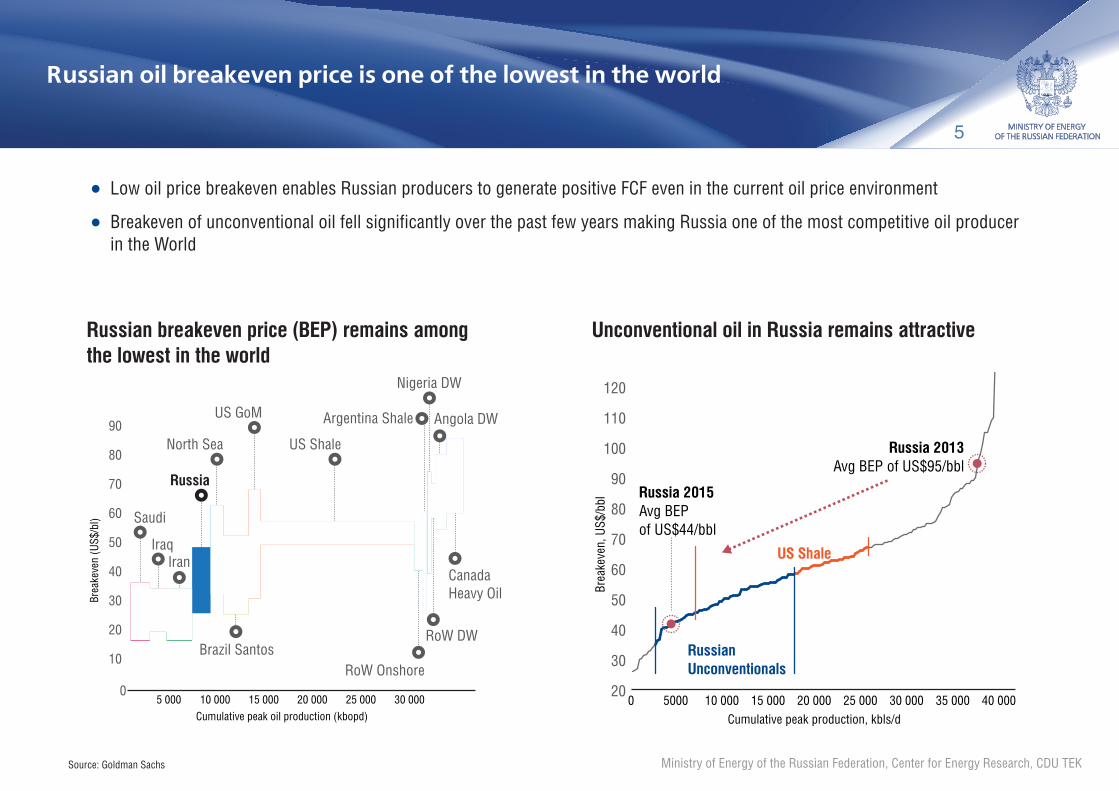

Russian oil breakeven price is one of the lowest in the world

• LowoilpricebreakevenenablesRussianproducerstogeneratepositiveFCFeveninthecurrentoilpriceenvironment

• BreakevenofunconventionaloilfellsignificantlyoverthepastfewyearsmakingRussiaoneofthemostcompetitiveoilproducerintheWorld

Russian breakeven price (BEP) remains among the lowest in the world

Unconventional oil in Russia remains attractive

0

10

20

30

40

50

60

70

80

90

5 000 10 000 15 000 20 000 25 000 30 000

Brea

keve

n (U

S$/b

l)

Cumulative peak oil production (kbopd)

Saudi

IraqIran

Russia

North Sea

Brazil SantosRoW DW

Angola DW

CanadaHeavy Oil

Argentina ShaleUS GoM

US Shale

RoW Onshore

Nigeria DW

20

30

40

50

60

70

80

90

100

110

120

Russia 2015Avg BEPof US$44/bbl

US Shale

RussianUnconventionals

Russia 2013Avg BEP of US$95/bbl

5000 40 00035 00030 00025 00020 000

Cumulative peak production, kbls/d

Brea

keve

n, U

S$/b

bl

15 00010 0000

Source:GoldmanSachs

6 MINISTRY OF ENERGY OF THE RUSSIAN FEDERATION

Ministry of Energy of the Russian Federation, Center for Energy Research, CDU TEK

Russia enjoys attractive positioning on the global cost curve

Biofuels20

Proccessing Gain20

Other NGLs20

Saudi Arabia39 Iran

42Russia

41

Onshore OPEC57

Iraq39

Conventional US (lower 48)68 Onshore

non-OPEC57

ShallowwaterOPEC

78

Deepwaternon-OPEC

86Shallow water

non-OPEC72

US (lower 48)tight oil

64

Canada(oil sands)

91

Deepwater OPEC 89

Oil Shale95

1 3 5 7 9 11 13 15 17 19 21 23 25 27 29 31 33 35 37 39 41 43 45 47 49 51 53 55 57 59 61 63 65 67 69 71 73 75 77 79 81 83 85 87 89 91 93 95 97 99 101

103

105

107

mmbd

$/bb

l

GTL65

Global cost curve

7 MINISTRY OF ENERGY OF THE RUSSIAN FEDERATION

Ministry of Energy of the Russian Federation, Center for Energy Research, CDU TEK

Russian upstream profitability is supported by low and stable production costs

•Russianoilindustryenjoyslowproductioncostscomparedtootheroilproducers,notaccountingfortheMiddleEastproducers

• LiftingcostswerestableduringthelastdecadepointingtotheefficiencyofRussianoilcompanies

Finding and development costs by region Russian lifting cost progression supported by localization and currency devaluation

QatarSaudiArabia

RussianFederation

VenezuelaCanadaUnitedStates

Europe 0

2

4

6

8

10

12

14

Capex/bbl

$/bb

l

Opex/bbl(incl/transportation)

LUKOIL

GazpromneftBashneft

Rosneft

0

2

4

6

8

10

$/bb

l

Average weighted

3Q161Q163Q151Q153Q141Q143Q131Q133Q121Q123Q111Q113Q101Q103Q091Q093Q081Q083Q071Q07

8 MINISTRY OF ENERGY OF THE RUSSIAN FEDERATION

Ministry of Energy of the Russian Federation, Center for Energy Research, CDU TEK

Russian gas is competitive in Europe

• Inaweakgrowingdemandenvironment,gainofmarketshareofoneimportermeansalossofmarketsharebysomeoneelse

•Gazpromhasthesparecapacityandlowcostbasetocompeteformarketshare

Full-cycle commercial breakeven cost curve

0

2

4

6

8

10

50 100 150 200 250 300 350 400 450 500 550 600 650 700 750 800 850 900 950

NetherlandsIranLibya

Algeria

Other EuropeUK base$/

mcf

bcm

Norway base Russia legacyIraq

UK new

Azerbaijan (SD II)

Norway new

Russia new

Source:CreditSuisse

9 MINISTRY OF ENERGY OF THE RUSSIAN FEDERATION

Ministry of Energy of the Russian Federation, Center for Energy Research, CDU TEK

0

1500

3000

Prel

ude

FLN

G

Ango

la L

NG

Snoh

vit

Whe

atst

one

LNG

Gorg

on

Petro

nas

FLN

G 1

QCL

NG

Trai

n 2

Plut

o

Petro

nas

FLN

G 2

Icht

hys

Yam

al L

NG

US$

/mm

tpa

Russian LNG projects – looking beyond pipelines

• TheSakhalin-2projectisthefirstonstreamLNGprojectinRussiawithtotalcapacityof10,8mlnt

• YamalLNG(Novatek)iswellontrackandthefirsttrainshouldbelaunchedinOctoberthisyear

• TheProjectconsistsofconstructionofthreetrainswithanoutputcapacityofaround16.5mlntonsperyear

• ThetwogiantgascondensatefieldsintheremoteGydanpeninsula,SalmanovskoyeandGeofizicheskoyeshouldbethenextpotentialsourceofLNGproductionforArcticLNG

LNG project implementation costs to first gas

Russian LNG production prospects

0

25

50

75

100

32.3

57.362.3

80.0

16.321.8

27.3

10.8

2035E2022E2021E2020E2019E2018E2017E2016

Other probable projectsVladivostok LNGBaltiyskiy LNGYamal LNGCurrent Capacity

mln

tons

10 MINISTRY OF ENERGY OF THE RUSSIAN FEDERATION

Ministry of Energy of the Russian Federation, Center for Energy Research, CDU TEK

Russian electricity sector

Electricity consumption Capacity additions

+18.1 (+1.7%)

1037.5 1031.31040.4 1036.4

1054.5

20162015201420132012actual

TWh

6289.8

4019.2

7597.0

4852.5 4293.9

3575

.1

1926

.5

4969

.6

2952

.8

1792

.5

2714

.7

2092

.7

2627

.4

1899

.7

2501

.4

20162015201420132012actual

additions through CSC (thermoelectric power plants)other additions

MW

• ElectricityconsumptionandproductioninRussiahasgrownby1.7%and2.1%respectivelyin2016

•Duringnexttwentyyearselectricityproductionisexpectedtogrowbyanother30-38%drivenbyinternalconsumptionandexportopportunities

• Capacitysupplycontracts(CSC)introducedbyRussiangovernmenthaveprovedthemselvesasaneffectiveinvestmentsupportmeasureprovidinginvestorswithastablereturnandleadingtonewcapacitiesbeinginstalledeveryyearthatinitsturncreatesroomfordecommissioningobsoleteones

11 MINISTRY OF ENERGY OF THE RUSSIAN FEDERATION

Ministry of Energy of the Russian Federation, Center for Energy Research, CDU TEK

Russian Energy Strategy implies renewable capacity increase

•Shareofrenewableswillincreaseinpowerbalanceupto2,5%by2024fromlessthan1%in2016

•Additional5.9GWofrenewablecapacityarebeingselectedthroughauctionsduringthesameperiod

• 899MWofwind,55MWofsolarand305MWofsmall-scaleHPPcapacitiesaretobeauctionedinthecomingyears

Installed renewable capacity in 2016 Renewable capacity selected for construction through auctions

21%

12%

0.13%4%4%

59%

Solar

Wind

Biogas

GPP

Small-scale HPP

Biomass

2.4 GW

0

500

1000

1500

2000

2500

3000

335

399 505280

520

55

21 50

50

305

105 51 35610

1651

899

Municipal solid waste

Solar

Small-scale HPP

Wind

To beauctioned

20172016201520142013

SolarMunicipal solid waste

Small-scale HPPWind

MW

12 MINISTRY OF ENERGY OF THE RUSSIAN FEDERATION

Ministry of Energy of the Russian Federation, Center for Energy Research, CDU TEK

Russian renewables offer favorable environment for investors

Effective regulatory and financial framework: Examples of Success:

Renewable capacity additions

0

20

40

60

80

100

120

140

35.0

90.0

57.070.0

2017E20162015

SolarWind

MW

•Wholesaleelectricitypowermarketcapacitysupplycontracts(CSC)whichhaveprovedthemselveseffectiveinconventionalgenerationguaranteestableROIforinvestorsinrenewables

•Regulatedtariffsatretailelectricitymarketsprovideforrenewableelectricitytradeatspecialpricesinisolatedareas

•Nearly130MWofsolarpowercapacityhavebeeninstalledduring2015-2016

• 125MWofrenewablepowercapacity–90MWfromsolarand35MWfromwind–expectedtobeinstalledthisyear

•HevelSolarcompanyin2017havemodernizeditssolarcellfactoryonthebasisofitsowndevelopedheterojunctiontechnologythatprovidesfor22-24%cellefficiencyandraisedfactorycellproductioncapacityfrom100to160MWayearwithapotentialoffurtherincreaseupto470MWayear

•During2016-2017majorplayerssuchasRosatom,Rosnano,FortumandEnelenteredthewindpowersectorusingCSCwithstrategiesaimedatequipmentmanufacturingsetupinRussia

13 MINISTRY OF ENERGY OF THE RUSSIAN FEDERATION

Ministry of Energy of the Russian Federation, Center for Energy Research, CDU TEK

Constant technological development of Russian energy sector is the top priority

COALOIL AND GAS ELECTRIC ENERGY RENEWABLE ENERGY

• Increaseinoilrecoveryratio

• Technologicalsolutionsfortightoilandoffshoreoilproduction

• LNGproductionandtransportation

• Technologicalconcepts«smartoilwell»and«smartoilfield»

• Petrochemicalsegmentdevelopment

• Newtechnologicalsolutionsforundergroundminingmethod

• Newtechnologicalsolutionsforcoalupgrading

• Productionofhydrophobicpeatbrickswithhighvalueadded

• Smartgrids

• «Energynet»concept

• Computerizedprotectionandmanagementsystemsforelectricpowersubstation

• Newtechnologicalsolutionsforelectricandelectronicmachinery

• Newtechnologicalsolutionsforconstructionmaterials,includingcomposite

• Newtechnologicalsolutionsforcablemanufacturing

• Hightemperaturesuperconductivity

• Newtechnologicalsolutionsforsmallscaledistributedgenerationbasedonrenewableenergy

• Newtechnologicalsolutionsforphotoelectrictransducer

• Newtechnologicalsolutionsfornetworkstorage

• Hydrogenenergetics

KEY PRIORITIES FOR TECHNOLOGICAL DEVELOPMENT OF RUSSIAN ENERGY SECTOR

14 MINISTRY OF ENERGY OF THE RUSSIAN FEDERATION

Ministry of Energy of the Russian Federation, Center for Energy Research, CDU TEK

Russia already enjoys considerable interest from foreign long term investors

PROJECT INVESTORS DESCRIPTION

Gaspipelines:

Nord Stream 1&2

NS 1 Russian: GazpromForeign:BASF/Wintershall,E.ON,Gasuine,ENGIE

AnoffshorenaturalgaspipelinefromVyborg(Russia)toGreifswald(Germany)since2011Yearlycapacity—55blnm3

NS 2 Russian: GazpromForeign: E.ON,Shell,BASF/Wintershall,OMV,ENGIE

ExpansionofNordStream,fromUst-Luga(Russia)toGreifswald(Germany),yearlycapacity–55blnm3

Operationsareplannedtostartin2019

LNGprojects:

Sakhalin 2Yamal LNG

Sakhalin 2 Russian: GazpromForeign:Shell,Mitsui,Mitsubishi

OilandgasdevelopmentinSakhalinIslandsince1994Outputcapacity—9,6mlntperyear,5mlnadditionalcapacityisplannedtorunin2018

Yamal LNG Russian: NovatekForeign: Total,CNPC,SilkRoadFund

LocatedontheYamalPeninsula,abovetheArcticCircleOutputcapacity—16.5milliontofLNGOperationsareplannedtostartin2017

Oildevelopment:

Investment projects

Investment projects Foreign: Shell,BP,Total,ExxonMobil,ONCGVidesh

BPhasseveralprojectsinRussiawithRosneftTotalwithZarubezhneftoperateKharyagafieldandalsootheroilprojectsinRussiaONCGVideshownsVankorneftcompany(alsoownedbyRosneft)

Powergeneration:

Huadian Teninskaya plantInvestment projects

HT Plant Russian: TGC-2Foreign: ChinaHuadianCorporation

Gas-steamcombinedcycleplantlocatedinYaroslavlPlannedcapacity–450MWh

Investment projects Foreign: Enel,Uniper,Fortum

Enelowns56%ofEnelRussiawhichmanages9,4GWofpowercapacityinRussiaUniperowns82%ofUnipro(11,2GWinRussia)Fortumowns29,5%ofTGC-1(4,2GWofpower,10,1heatcapacityinRussia)

15 MINISTRY OF ENERGY OF THE RUSSIAN FEDERATION

Ministry of Energy of the Russian Federation, Center for Energy Research, CDU TEK

In particular, a number of successful projects with Italian investors

PROJECT INVESTORS DESCRIPTION

Enel Russia electricity plants and renewable energy

Foreign:Enel(marketcapitalization-48bln,revenue–75blneuro)

• Enelowns56%ofEnelRussiawhichmanages9,4GWofpowercapacity,2,4GWofheatcapacityinRussia

• EnelRussiaisalsoconstructingwindturbineswithacapacityof291MW,whichshouldstartoperationsin2020-2021(withinvestmentsof400mlneuro)

Plants:

Transneft Oil PumpsRussian Electric Motors

TOP Russian: Transneft,KonarForeign:TermomecanicaPompe

• TransneftOilPumpswasestablishedin2016forthepurposeoflocalizationofproductionofhorizontalandverticalpumpsandunitslocatedinChelyabinsk

• Plannedproductionconsistsof180pumpsperyear

REM Russian: Transneft,KonarForeign: NidecASI

• Operationsareplannedtostartin2018

• Plannedoutputofelectricmotorsis300,capacityofeachmotorcanreach8000kW

Gaspipelines:

Blue StreamNorth Stream

BS Russian: GazpromForeign: Eni

• GaspipelinebetweenRussiaandTurkey(396km)since2003

NS Russian: GazpromForeign: SaipemEnergyServices

• AnoffshorenaturalgaspipelinefromVyborg(Russia)toGreifswald(Germany)since2011

• Yearlycapacity–55blnm3

Oil projects Russian: RosneftForeign: Eni

• EnihasseveralprojectswithRosneft,inparticular,offshorefieldsinRussia

HeliVert JV Russian: Rosneft,RussianHelicoptersForeign: Leonardo-Finmeccanica

• Agreementinvolvesdeliveryof150coptersfromHeliVerttoRosneftuntil2025

• LocalizationlevelofproductioninRussiaisplannedtoreach70%

MINISTRY OF ENERGY OF THE RUSSIAN FEDERATION

THANK YOU FOR YOUR ATTENTION!

Ministry of Energy of the Russian FederationCenter for Energy ResearchCentral Dispatching Department of the Fuel and Energy Complex (CDU TEK)

APPENDIX

18 MINISTRY OF ENERGY OF THE RUSSIAN FEDERATION

Ministry of Energy of the Russian Federation, Center for Energy Research, CDU TEK

Russia demonstrates steady growth in liquids, gas, coal and energy production

323.5

584.0

258.4

518.1

654.5

354.6

1054.0

20122000

862.8

534.2

635.5

2015

1049.9

374.0

2015

547.5

640.2

1071.8

385.7

2016

2016

526.7

641.9

359.0

2014

1047.4

20142012

523.4

668.2

352.1

2013

1045.0

20132000

12,4%

17,7%

5,3%

4,3%

Share of global, 2016

RussiaSaudi ArabiaUSAIraqChina

USARussiaIranQatarCanada

56

ChinaIndiaUSAAustraliaIndonesiaRussia

123

3

6

41

2

4

5

ChinaUSAIndiaJapanRussia

2

1

1 1

2

23

3

3 4

4

4

5

5

5

12345

12345

5

3

12 4

WORLD RANK

1

2WORLD RANK

66

55

WORLD RANK

WORLD RANK

Crude oil production and condensate recovery

Gas production

Coal production

Electricity generation

mln

tonn

esbc

mm

ln to

nnes

bln

kWh

19 MINISTRY OF ENERGY OF THE RUSSIAN FEDERATION

Ministry of Energy of the Russian Federation, Center for Energy Research, CDU TEK

Oil and gas condensate production is growing, as well as oil exports, drilling activity and upstream investments

Oil and gas condensate production

Upstream capital expenditures of oil majors

Liquids exports Drilling

Growth in oil reserves

450

500

550

600

518.1 523.4 526.7 534.2547.5

20162015201420132012actual

+13.3 (+2.5%)+13.3 (+2.5%)

mnt

0

10

20

30

40

27.7 28.125.6

17.6 18.0

20162015201420132012

+0.4 (+2.3%)

actual

$ bl

n

0

100

200

300

400

239.7 235.0 221.3 241.8 254.2

20162015201420132012

+12.4 (+5.1%)

actualm

nt0

8000

16000

24000

32000

40000

20293 21262 1982522168

24857

894 914 994 819 932

20162015201420132012

Production drilling

Exploration drilling

+2689 (+12.1%)+2689 (+12.1%)+113 (+13.8%)+113 (+13.8%)

actual

th. m

eter

s

500

570

640

710

780

850

742.0713.4

775.9

726.0

574.8

20162015201420132012actual

-151.2 (-20.8%)

mnt

20 MINISTRY OF ENERGY OF THE RUSSIAN FEDERATION

Ministry of Energy of the Russian Federation, Center for Energy Research, CDU TEK

Russian gas production keeps stable while gas exports is growing

Gas production

Gas consumption as motor fuel

Gas exports (incl. LNG) Domestic gas supplies*

Russian territory covered by infrastructure for gas supply

450

500

550

600

650

700

654.5668.2

641.9 635.5 640.2

20162015201420132012actual

+4.7 (+0.7%)+4.7 (+0.7%)

bcm

+16.1 (+8.4%)

100

140

180

220

260

186.2203.3

181.1192.5

208.6

20162015201420132012actual

bcm

300

350

400

450

500

550

460.0 456.9 458.4 444.3 456.7

20162015201420132012actual

+12.4 (+2.8%)+12.4 (+2.8%)

bcm

*Includingextraction(injection)from(to)undergroundstorages

+51 (+10.5%)+51 (+10.5%)

0

175

350

525

700

390 400453 487

538

20162015201420132012actual

bcm

60%

65%

70%

64.4%65.1% 65.4%

66.2%67.2%

20162015201420132012

+1.0 п.п.

actual