Russia – Europe's Most Attractive Future Market? · Russia – Europe's Most Attractive Future...

39

Russia – Europe's Most Attractive Future Market? Tim Armstrong Director, Emerging Markets

Transcript of Russia – Europe's Most Attractive Future Market? · Russia – Europe's Most Attractive Future...

Russia – Europe's Most Attractive Future Market?

Tim Armstrong

Director, Emerging Markets

Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE 2

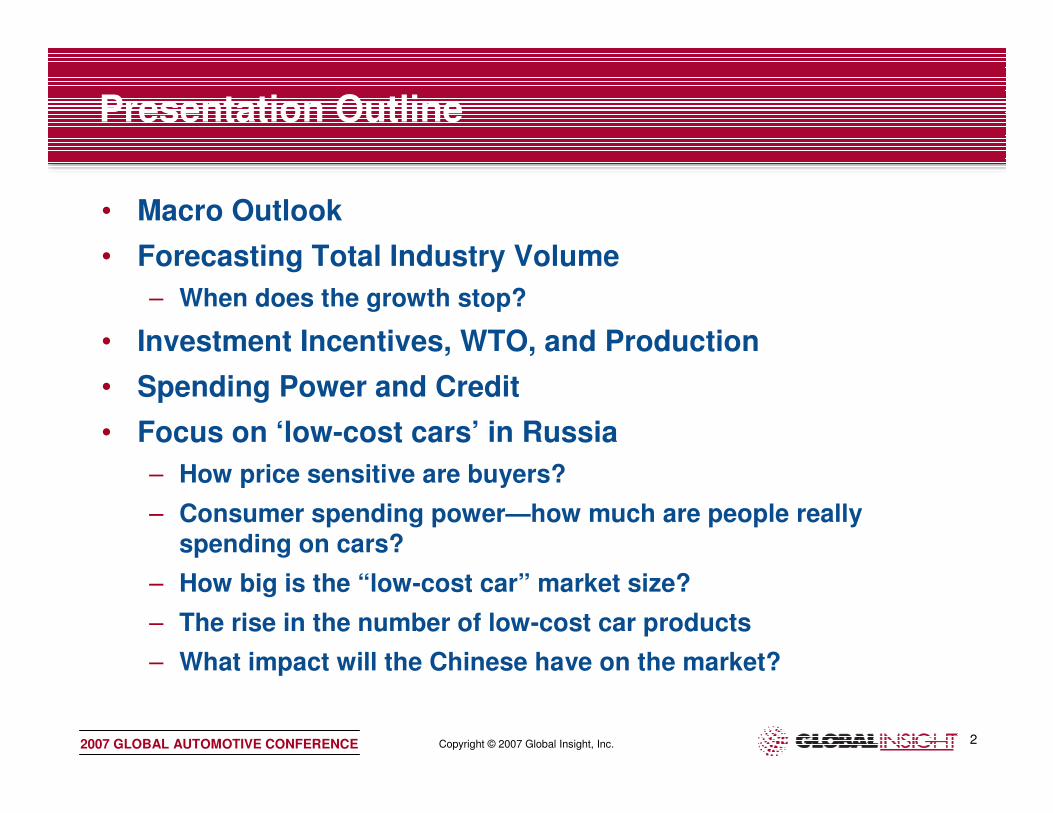

Presentation Outline

• Macro Outlook

• Forecasting Total Industry Volume

– When does the growth stop?

• Investment Incentives, WTO, and Production

• Spending Power and Credit

• Focus on ‘low-cost cars’ in Russia

– How price sensitive are buyers?

– Consumer spending power—how much are people really spending on cars?

– How big is the “low-cost car” market size?

– The rise in the number of low-cost car products

– What impact will the Chinese have on the market?

Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE 3

Russia Is the Best Performing Market in the World…Almost

635

419

130

127

78

69

47

35

-59

-76

-150

-230

-239

1320

412

226

255

100

69

59

31

108

30

-201

-7

-92

147

-129

-401

132

1,166

59

-600 -400 -200 0 200 400 600 800 1000 1200 1400 1600

CHINA

RUSSIA

BRAZIL

INDIA

ITALY

IRAN

ARGENTINA

CANADA

UKRAINE

KOREA

INDONESIA

SPAIN

TURKEY

GERMANY

JAPAN

USA

ThousandsIncremental Change in Vehicle Demand

Change in LV Sales 2005-06

and 2006-07 ranked by 2007

20062007

Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE 4

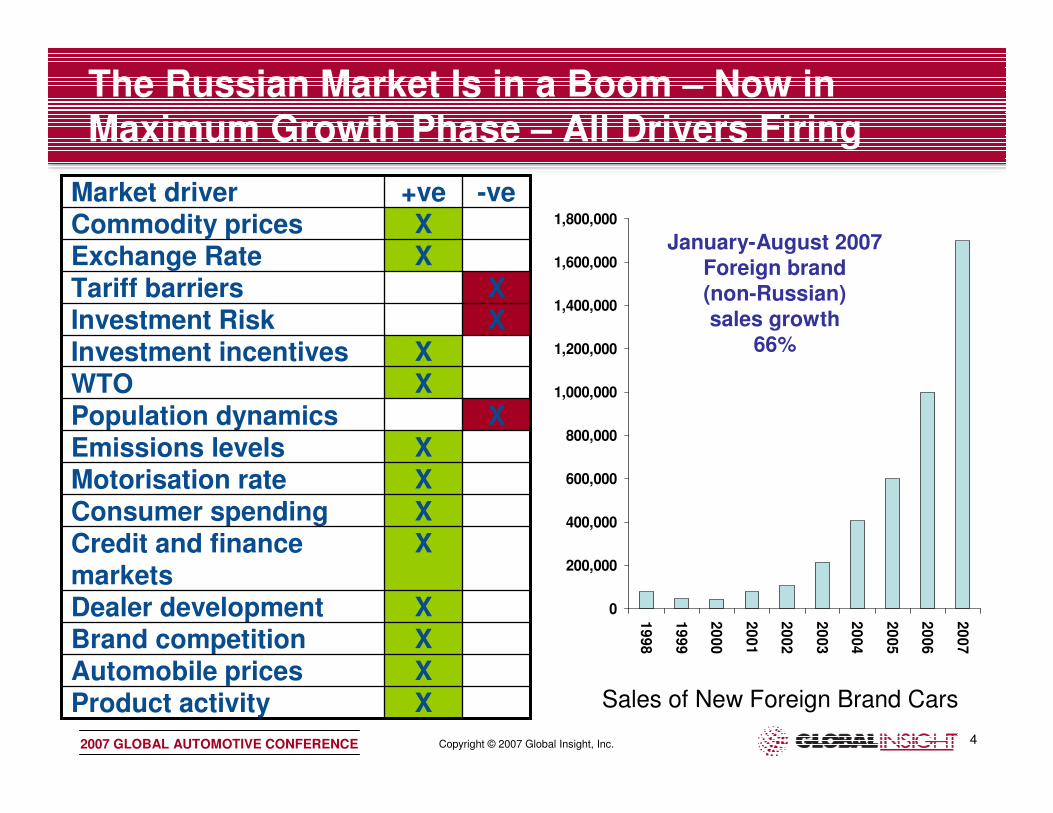

The Russian Market Is in a Boom – Now in Maximum Growth Phase – All Drivers Firing

XPopulation dynamics

XProduct activityXAutomobile pricesXBrand competitionXDealer development

XCredit and finance markets

XConsumer spendingXMotorisation rateXEmissions levels

XWTOXInvestment incentives

XInvestment RiskXTariff barriers

XExchange RateXCommodity prices

-ve+veMarket driver

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

1,800,000

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

Sales of New Foreign Brand Cars

January-August 2007Foreign brand (non-Russian)sales growth

66%

Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE 5

Russia: From Crisis To Boom – Key Indicators

32.636.858.4Total External Debt (as % of GDP)

394.8237.1111.7Average Wage (US$)

7.52.12.3Fiscal Balance (% of GDP)

303.7124.540.3Forex Reserves (US$ bn)

304.5183.5105.3Total Exports (bop US$ bn)

27.228.828.8RBL/US$ exchange rate (avg.)

9.721.638.1CPI (annual average in %)

6,9254,1242,068Per Capita GDP (market rates in US$)

6.77.21.6GDP Growth (annual in %)

20062004Avg.

1996-2000

Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE 6

0

2

4

6

8

10

12

14

16

18

20

2000 2002 2004 2006

GDP Consumption Investment

(Annual growth in percent)

• 2006 growth bettered 2005 performance at 6.7%. Pace to moderate in 2007 to 6.5% as sliding net exports drag on growth. Domestic demand continues to surge

• Enterprise profits up strongly, sustaining capital spending boom; rapidly rising real incomes boosting private consumption

• Aggregate demand has a very substantial import component; Imports outpace exports which face capacity constraints, moderating prices, and a strengthening ruble

Domestic Demand Drives Growth, Aided by High Energy Prices

Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE 7

Higher Base Oil Price Forecast

0

10

20

30

40

50

60

70

80

90

1996 1999 2002 2005 2008 2011 2014 2017

Mar-07 Sep-07

• Oil is $15 higher long term than last forecast or around 25%

• Stronger economic outlook

• Greater capacity for government fiscal support and wealth diversification

• Pump prices low in Russia with low taxation rates—little impact at the pump

• No significant negative shift in segmentation—income effects could move segmentation upwards

Brent, US$ per barrel

Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE 8

Per capita income

Incom

e e

lasticity

of

ow

ne

rsh

ip

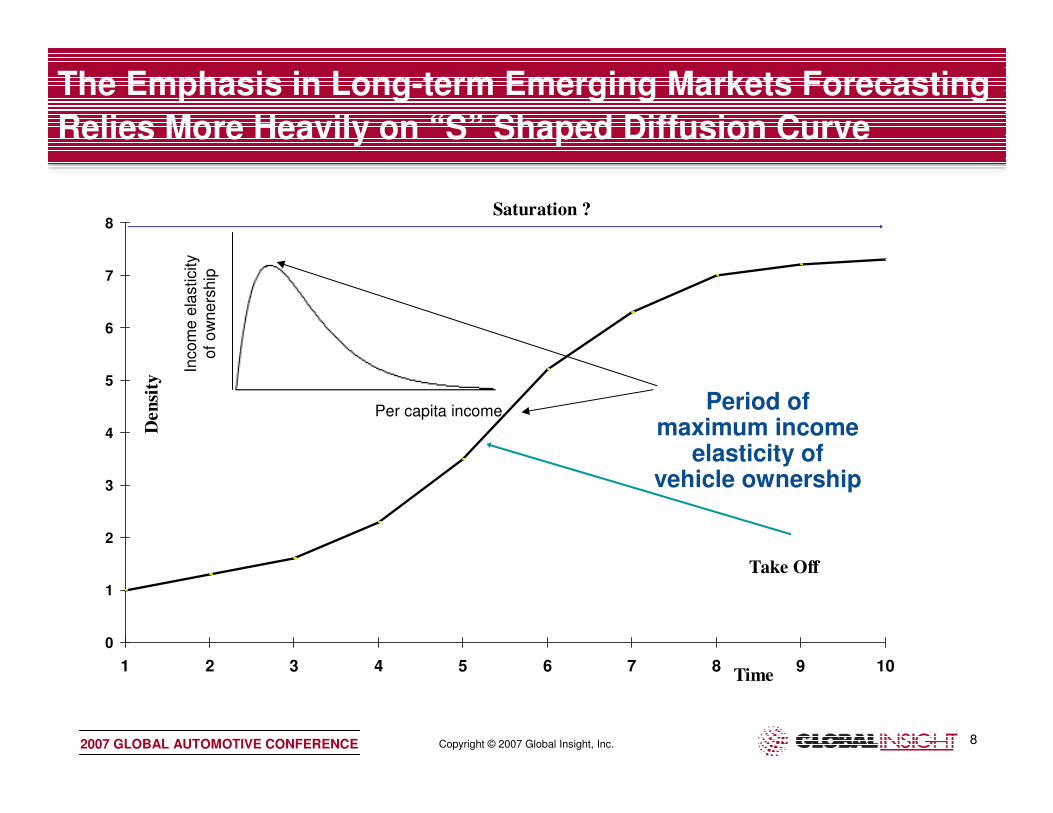

The Emphasis in Long-term Emerging Markets Forecasting

Relies More Heavily on “S” Shaped Diffusion Curve

0

1

2

3

4

5

6

7

8

1 2 3 4 5 6 7 8 9 10

Den

sity

Take Off

Saturation ?

Time

Period of maximum income

elasticity of vehicle ownership

Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE 9

There are Similarities in S-Curve Development Across Emerging Markets - Stages of Industry Growth

• Pre take-off: Incomes under c. $3000–$5000

– Low incomes, closed financial markets, poor road conditions, low local model quality, public transport system, imports restricted, structural under-supply resolved by waiting lists

• Take off: commonly around income of $6000 pa

– Restructuring well underway, incomes rise, access to credit, open to imports, tariff barriers decline, interest rates fall and exchange rates stabilize, investment in road infrastructure, product mix

• Maturity: can be around $13,000–30,000 pa

– Market reaching long-term equilibrium as determined by geographical, political, social factors

• Income Distribution Analysis: Stability Ratio Method e.g. Car sales per household with >$20,000 income, current or ppp adjusted

– This requires forecasts of number of households by income bands for all emerging markets over the forecast horizon

(Source: Global Insight, Consumer Markets Forecast databases)

Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE 10

Income Take-off Started in 2003 (Number of Households by $US Nominal Income Bracket)

0

10

20

30

40

50

60

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

H'holds w / Income $150K and over

H'holds w / Income $100 to 150K

H'holds w / Income $90 to 100K

H'holds w / Income $80 to 90KH'holds w / Income $70 to 80K

H'holds w / Income $60 to 70K

H'holds w / Income $50 to 60K

H'holds w / Income $40 to 50K

H'holds w / Income $30 to 40K

H'holds w / Income $20 to 30KH'holds w / Income $15 to 20K

H'holds w / Income $10 to 15K

H'holds w / Income $0- to $10k

Millions of Households

Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE 11

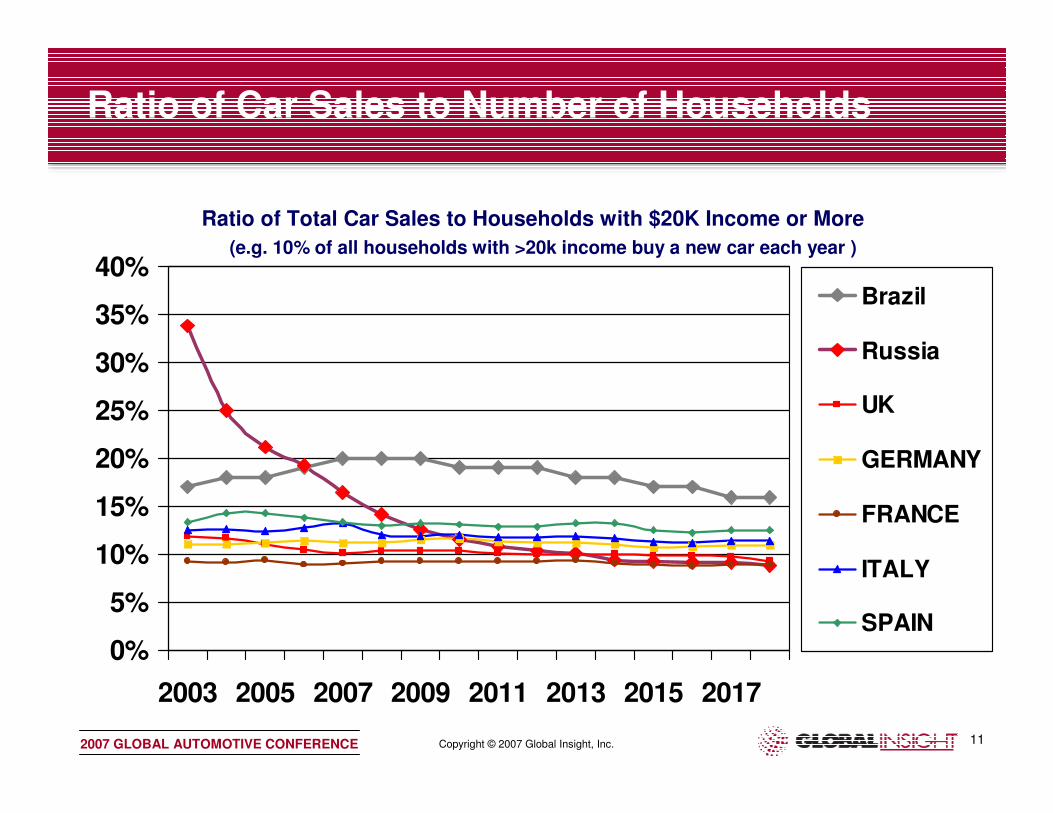

Ratio of Car Sales to Number of Households

0%

5%

10%

15%

20%

25%

30%

35%

40%

2003 2005 2007 2009 2011 2013 2015 2017

Brazil

Russia

UK

GERMANY

FRANCE

ITALY

SPAIN

Ratio of Total Car Sales to Households with $20K Income or More

(e.g. 10% of all households with >20k income buy a new car each year )

Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE 12

Russia Is Fast Becoming the Most Attractive Market in Europe – Light Vehicle Sales

0

500

1000

1500

2000

2500

3000

3500

4000

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Th

ou

sa

nd

s

DEU ITA GBR FRA ESP RUS

Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE 13

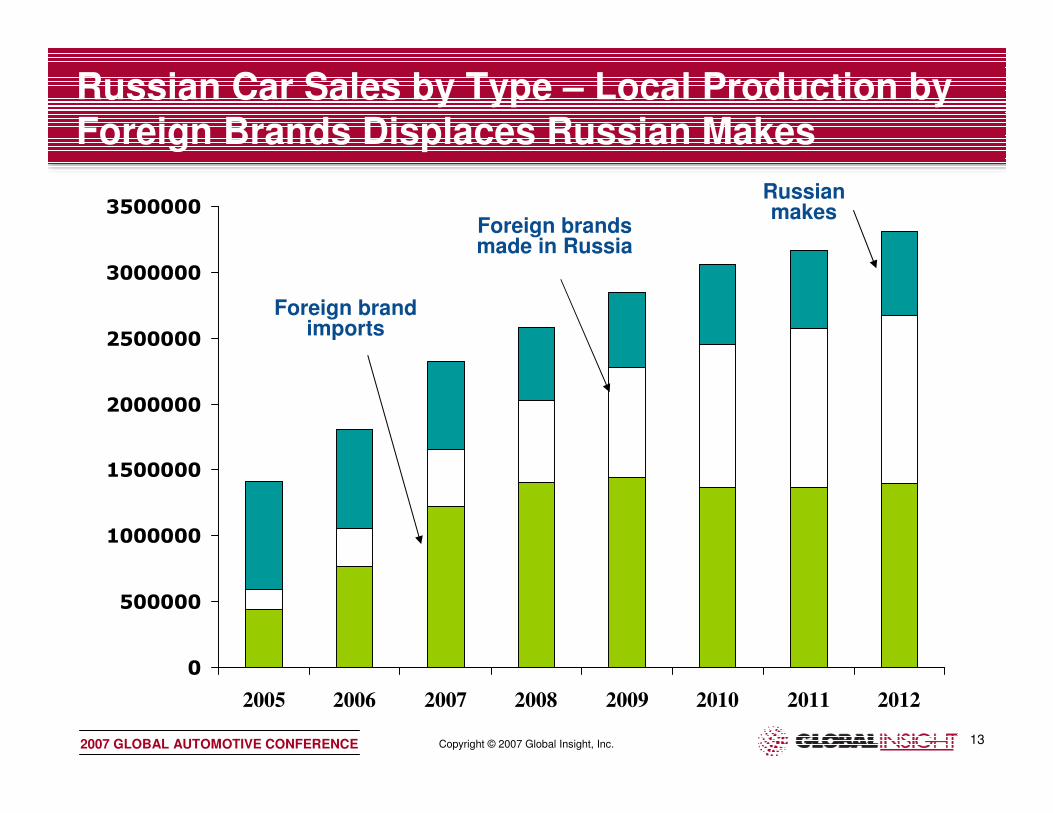

Russian Car Sales by Type – Local Production by Foreign Brands Displaces Russian Makes

0

500000

1000000

1500000

2000000

2500000

3000000

3500000

2005 2006 2007 2008 2009 2010 2011 2012

Russian makes

Foreign brands made in Russia

Foreign brand imports

Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE 14

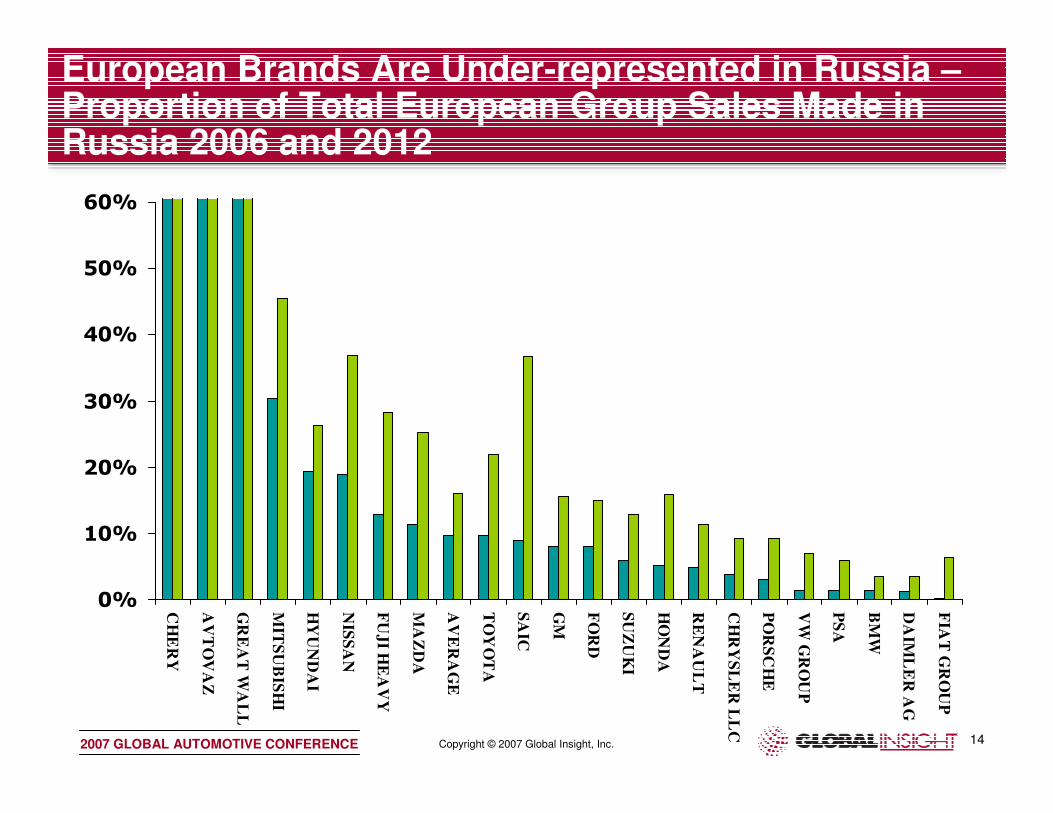

European Brands Are Under-represented in Russia –Proportion of Total European Group Sales Made in Russia 2006 and 2012

0%

10%

20%

30%

40%

50%

60%

CH

ER

Y

AV

TO

VA

Z

GR

EA

T W

AL

L

MIT

SU

BIS

HI

HY

UN

DA

I

NIS

SA

N

FU

JI H

EA

VY

MA

ZD

A

AV

ER

AG

E

TO

YO

TA

SA

IC

GM

FO

RD

SU

ZU

KI

HO

ND

A

RE

NA

UL

T

CH

RY

SL

ER

LL

C

PO

RS

CH

E

VW

GR

OU

P

PS

A

BM

W

DA

IML

ER

AG

FIA

T G

RO

UP

Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE 15

Decree 135 (since 1998) or similar

• Failed to attract widespread investment

• Too hard to achieve localisation levels

Decree 166 Was the Turning Point in Investment Legislation

Decree 166 (since 2005)

• Everybody joins or switches to Decree 166 by 2006

• But applications closed on 15 September 2007

• Not applicable to suppliers

New entrants/adopters

Switchers

Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE 16

Moscow

Izhevsk

Togliatti

Nab. Chelny

Elabuga

Kaluga

St. Petersburg

Kaliningrad

Taganrog

OEMs Are Rushing to Invest in Russia—in Special Economic Zones

Novouralsk

Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE 17

0

5

10

15

20

25

30

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

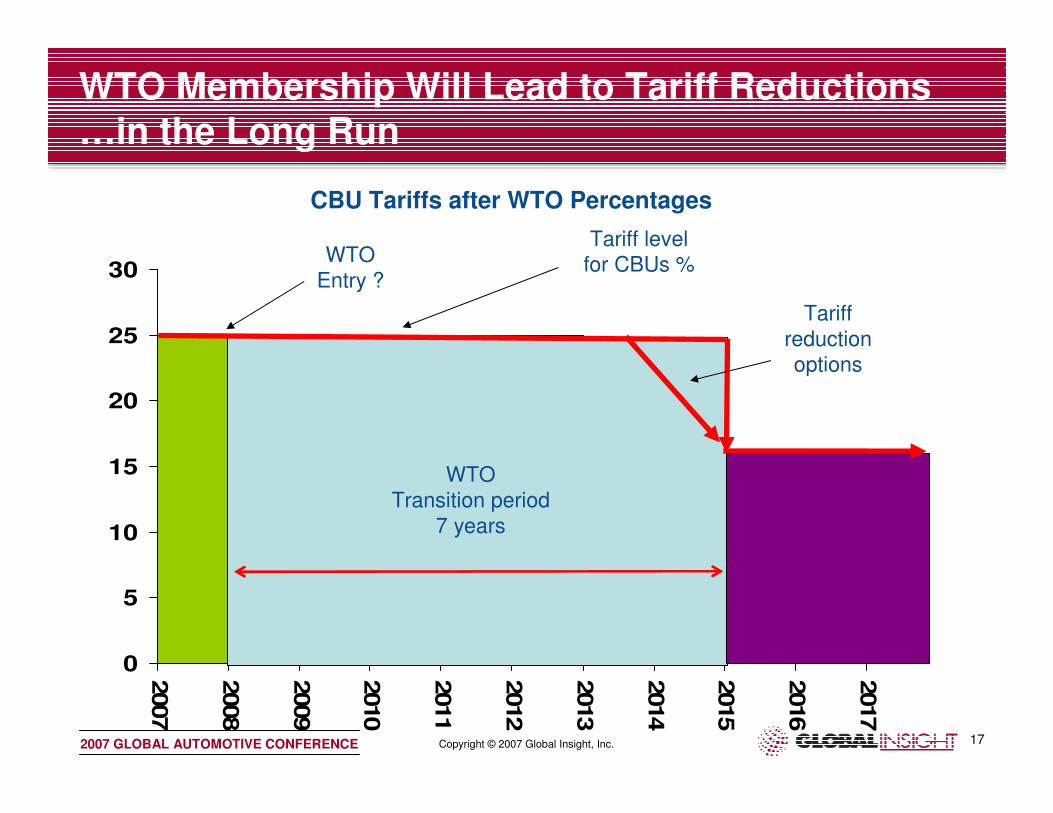

WTO Transition period

7 years

WTO Membership Will Lead to Tariff Reductions …in the Long Run

Tariff level for CBUs %WTO

Entry ?

Tariff reduction options

CBU Tariffs after WTO Percentages

Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE 18

0

200

400

600

800

1000

1200

1400

1600

2004

2005

2006

2007

2008

2009

2010

2011

2012

Thousands

YUEJINVWTOYOTASUZUKISSANGYONGSKODA

RENAULTPEUGEOTNISSANMITSUBISHILDVKIAHYUNDAIHUMMERHEBEI ZHONGXINGGREAT WALLGEELYFORD

FIATCITROENCHEVROLETCHERYCADILLACBMW

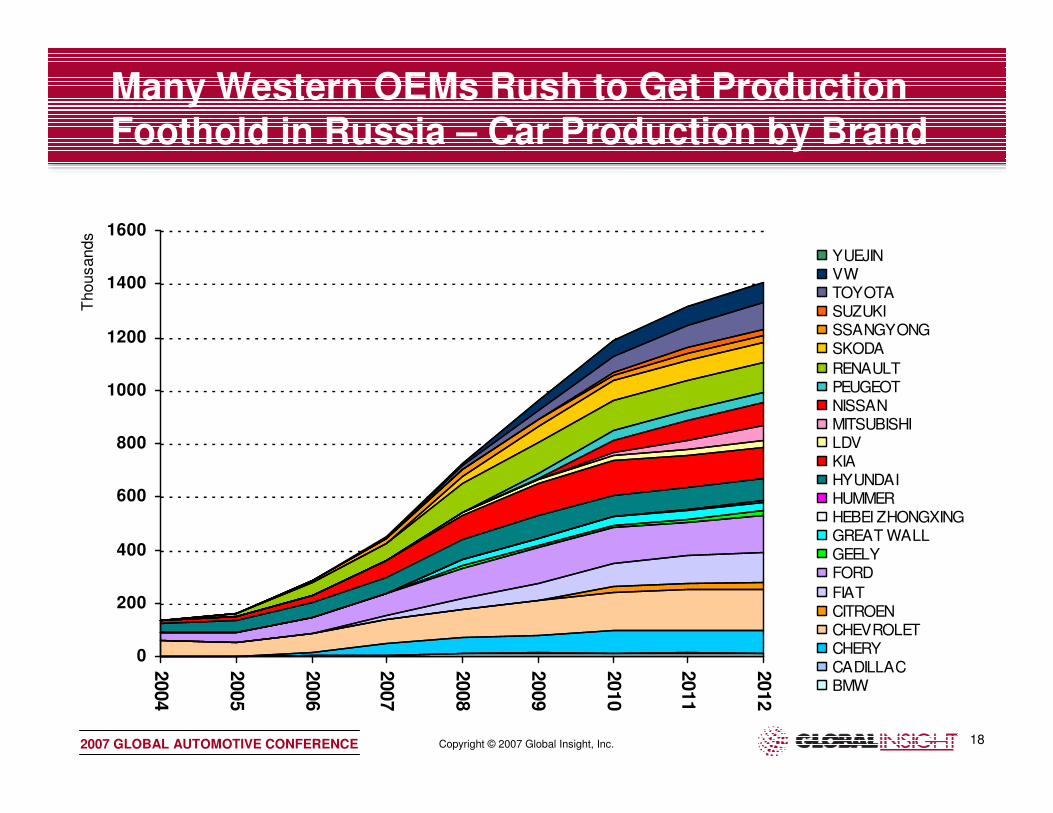

Many Western OEMs Rush to Get Production Foothold in Russia – Car Production by Brand

Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE 19

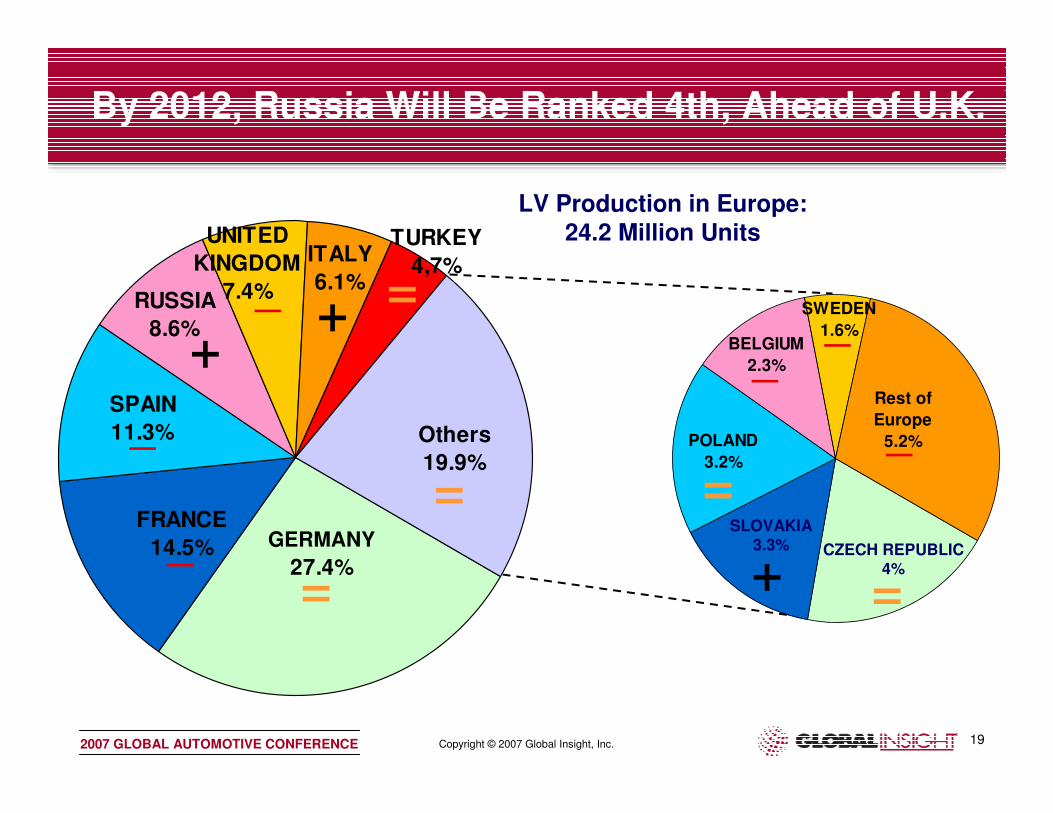

By 2012, Russia Will Be Ranked 4th, Ahead of U.K.

SPAIN

11.3%

GERMANY

27.4%

FRANCE

14.5%

Others

19.9%

TURKEY

4,7%ITALY

6.1%

UNITED

KINGDOM

7.4%RUSSIA

8.6%

POLAND

3.2%

Rest of

Europe

5.2%

SWEDEN

1.6%BELGIUM

2.3%

SLOVAKIA3.3% CZECH REPUBLIC

4%

=

= =

=+

__

_

_

+

_+

_

LV Production in Europe:24.2 Million Units

=

Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE 20

0 50 100 150 200 250 300 350 400 450 500

AB

C1C2

CDV

D1D2

E1E2

MPV-C

MPV-DSUV-B

SUV-CSUV-DSUV-E

Thousands

Russia Car Production by Segment 2007 and 2012

Toyota Small CarLogan, Nissan 1 litre

Focus, Linea, Spectra, Accent

Jetta & OctaviaDoblo

Mondeo, Sonata, Epica

Camry, 3 Series

5- Series, Teana

Rezzo

Rodius, CowrySX4

Chevy Niva, Captiva, Sportage, Tiggo

Rexton, Sorento, Santa Fe, Kyron

Escalade, H2

Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE 21

Spending Power and Credit

Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE 22

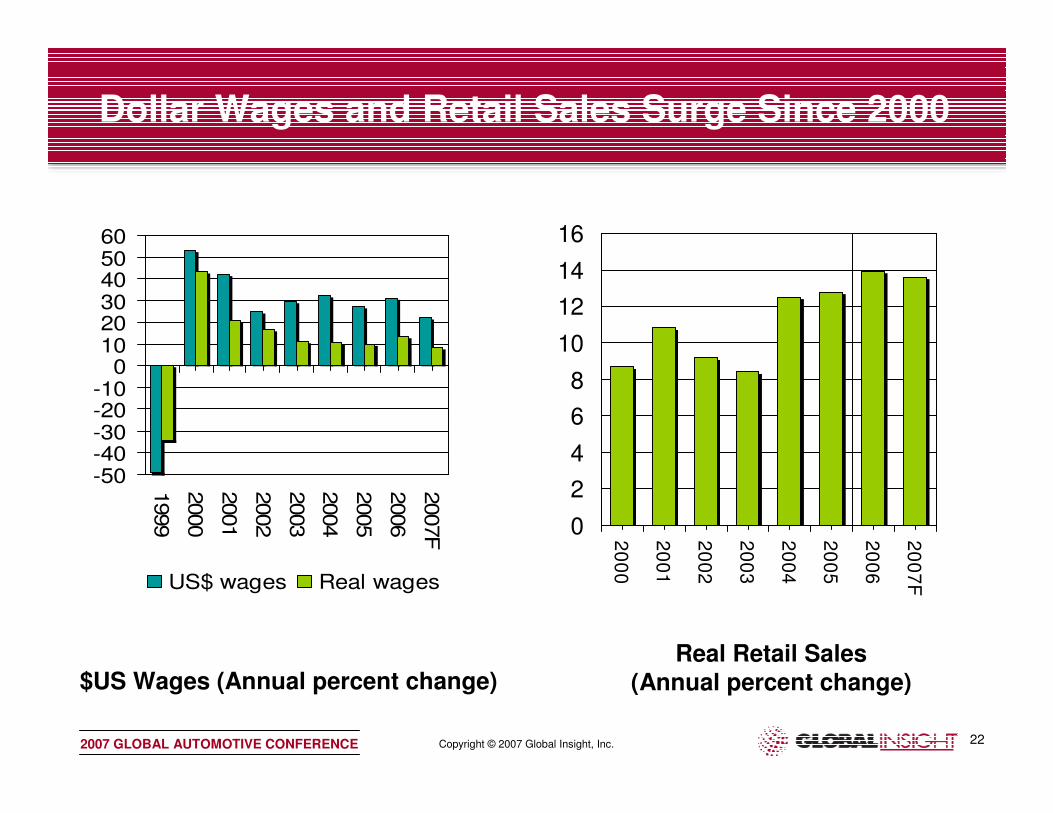

Dollar Wages and Retail Sales Surge Since 2000

-50-40-30-20-10

0102030405060

1999

2000

2001

2002

2003

2004

2005

2006

2007F

US$ wages Real wages

$US Wages (Annual percent change)

0

2

4

6

8

10

12

14

16

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

F

Real Retail Sales(Annual percent change)

Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE 23

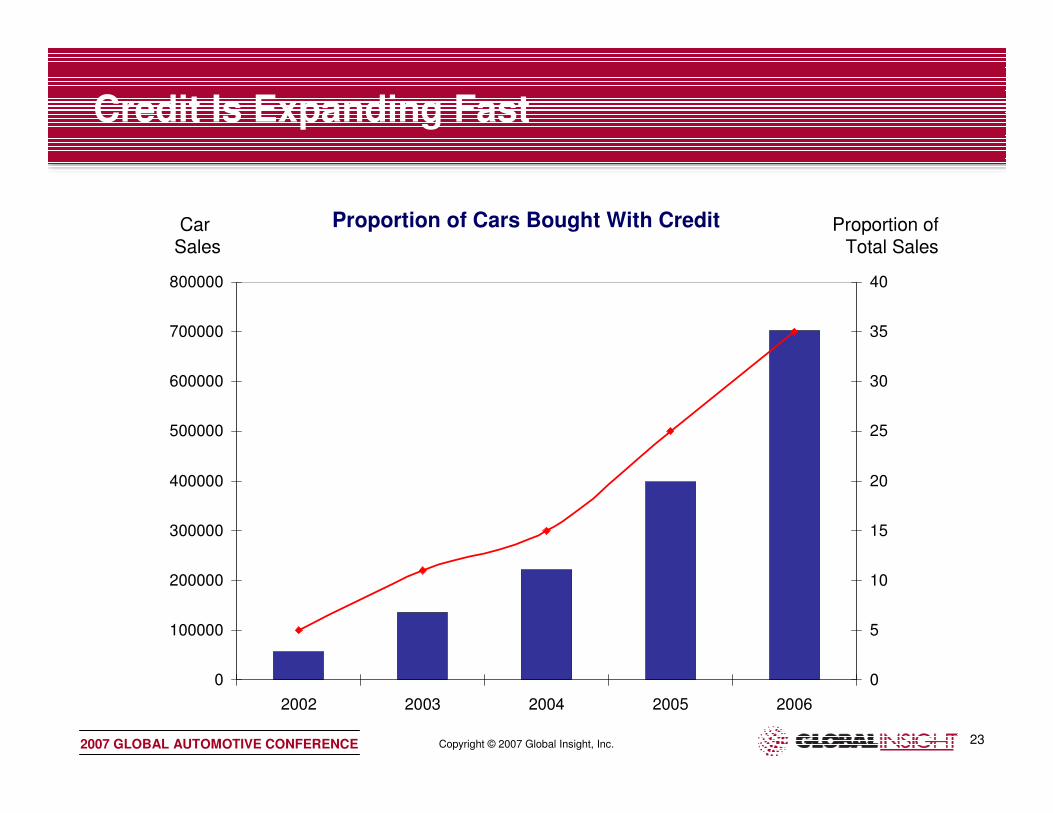

Credit Is Expanding Fast

0

100000

200000

300000

400000

500000

600000

700000

800000

2002 2003 2004 2005 2006

0

5

10

15

20

25

30

35

40

Proportion of Cars Bought With CreditCarSales

Proportion of Total Sales

Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE 24

Features of Credit in Russia

• Credit is dominated by banks rather than specialised consumer lending institutions

– Banks have developed direct ties with importers, dealers, and insurance companies

• Most car loan business occurs around Moscow and St Petersburg

– Strong potential to unlock credit in the regions

• Most loans are still denominated in hard currency

– This will shift towards rouble denominated credit as the importance of the regions increases

• Terms are getting easier

– The minimum acceptable salary was reduced in November 2006 to 100,000 roubles

– 70% of households could potentially qualify

– Average loan value rose from $10k in 2005 to $12.4k in 2006

• Foreign OEMs are moving to set up their own financing arms

– GM, Ford, Toyota, Nissan, Renault, BMW, and Mercedes Benz are all looking into setting up their own finance networks

– Mercedes-Benz and BMW will set up their own banking by late 2007 and early 2008 respectively

• Corporate and fleet sales are growing

– Influx of foreign companies who prefer foreign brands

– Ford sold 25% of its cars to corporate buyers in 2005

• Risks of a credit crisis are building

– Fast lending and lack of credit history

– Risk controls are still to be put in place

– Exchange rate risk probably not factored in by consumers

– A credit crunch already occurred during the Russian mini banking crisis in the summer of 2004

Copyr

ight

©200

7 G

lob

al In

sig

ht,

Inc.

2007 G

LO

BA

L A

UT

OM

OT

IVE

CO

NF

ER

EN

CE

25

Gro

wth

in

Fo

reig

n C

ar

Pa

rc,

To

p 1

5 R

eg

ion

s i

n

20

06

(%

Gro

wth

on

20

05

)

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Moscow

Moscow Oblast

St Petersburg

Primorsky Krai

Kalinningrad Oblast

Krasnodarsk Krai

Svedlovsok Oblast

Krasnoyarsk Krai

Irkutsk Oblast

Novosibirsk Oblast

Rostov Oblast

Cheliabink Oblast

Kemrovsky Oblast

Kanti-Mansi AO

Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE 26

Low-Cost Cars in Russia:Is the Market Evolving Too Fast?

Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE 27

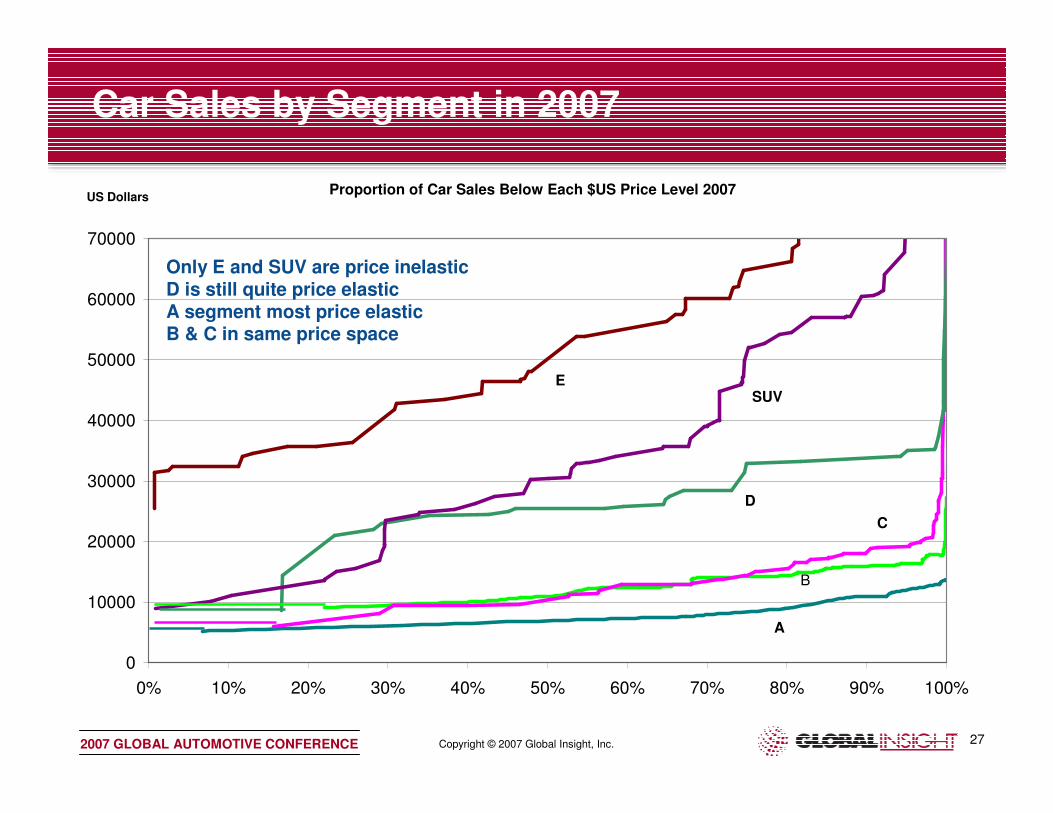

Car Sales by Segment in 2007

Proportion of Car Sales Below Each $US Price Level 2007

0

10000

20000

30000

40000

50000

60000

70000

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

US Dollars

A

B

C

D

SUVE

Only E and SUV are price inelasticD is still quite price elasticA segment most price elasticB & C in same price space

Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE 28

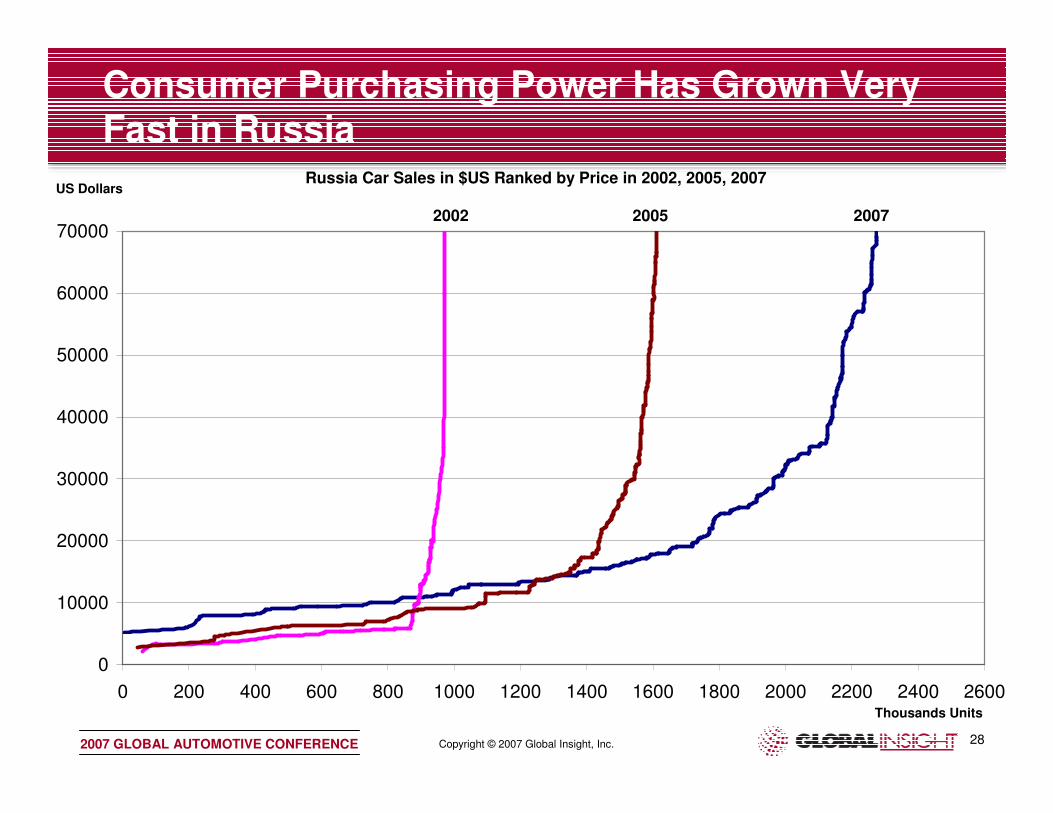

Consumer Purchasing Power Has Grown Very Fast in Russia

Russia Car Sales in $US Ranked by Price in 2002, 2005, 2007

0

10000

20000

30000

40000

50000

60000

70000

0 200 400 600 800 1000 1200 1400 1600 1800 2000 2200 2400 2600Thousands Units

US Dollars

2002 2005 2007

Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE 29

0

500

1000

1500

2000

2500

2002 2005 2007

The Proportion of Low Price Cars Is Falling

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2002 2005 2007

Proportion of Sales

$11–20k

$11k & under

Over $20k

Car Sales Volume 000s

Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE 30

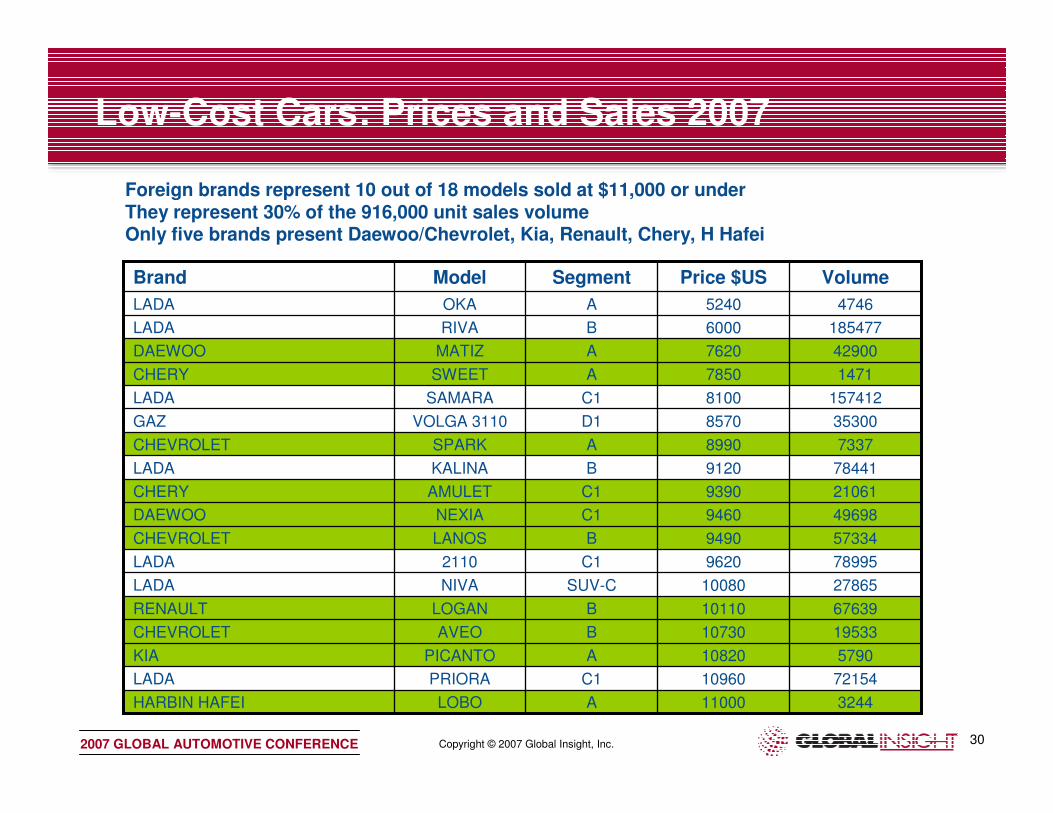

Low-Cost Cars: Prices and Sales 2007

324411000ALOBOHARBIN HAFEI

7215410960C1PRIORALADA

PICANTO

AVEO

LOGAN

NIVA

2110

LANOS

NEXIA

AMULET

KALINA

SPARK

VOLGA 3110

SAMARA

SWEET

MATIZ

RIVA

OKA

Model

A

B

B

SUV-C

C1

B

C1

C1

B

A

D1

C1

A

A

B

A

Segment

579010820KIA

1953310730CHEVROLET

6763910110RENAULT

2786510080LADA

789959620LADA

573349490CHEVROLET

496989460DAEWOO

210619390CHERY

784419120LADA

73378990CHEVROLET

353008570GAZ

1574128100LADA

14717850CHERY

429007620DAEWOO

1854776000LADA

47465240LADA

VolumePrice $USBrand

Foreign brands represent 10 out of 18 models sold at $11,000 or underThey represent 30% of the 916,000 unit sales volume Only five brands present Daewoo/Chevrolet, Kia, Renault, Chery, H Hafei

Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE 31

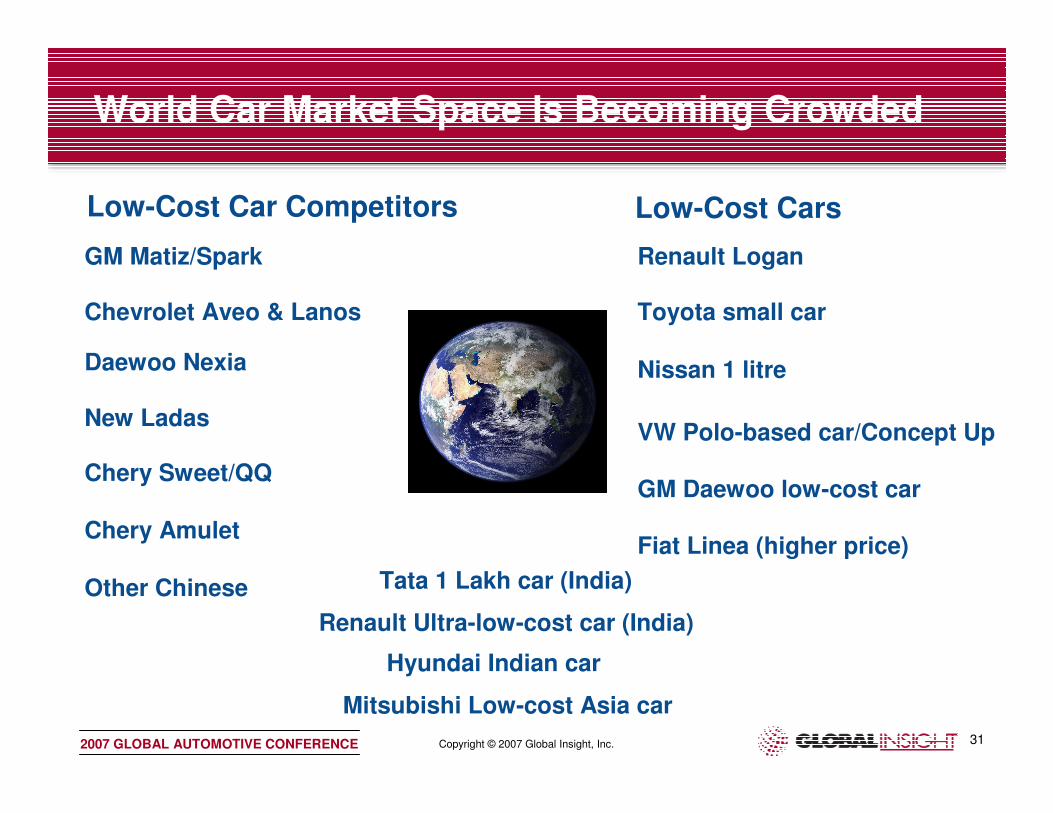

World Car Market Space Is Becoming Crowded

GM Matiz/Spark

Chevrolet Aveo & Lanos

Daewoo Nexia

New Ladas

Renault Logan

Toyota small car

Nissan 1 litre

VW Polo-based car/Concept Up

Mitsubishi Low-cost Asia car

Tata 1 Lakh car (India)

Renault Ultra-low-cost car (India)

Hyundai Indian car

GM Daewoo low-cost car

Fiat Linea (higher price)

Low-Cost CarsLow-Cost Car Competitors

Chery Sweet/QQ

Chery Amulet

Other Chinese

Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE 32

• One bodystyle available: sedan

• Three trim levels

• Two petrol powertrains – Euro 2 emissions standards

• Prices stretch well above base model

• 1.4 Authentique $10,200

• 1.4 Expression $10,900

• 1.6 Expression $11,800

• 1.6 Privilege $12,700

• 1.6 Prestige $13,700

The Logan in Russia

• Renault brought production at its AvtoFramos plant to full capacity during 2006, when a third shift was added. Production rose to 48,545 units in 2006

• In 2007, output will be extended to 80,000 units. In February, it announced a further investment of US$150 million to expand the facility to 160,000 units. This will take place by the middle of 2009

• In addition, a second model based on the Logan platform is likely to be launched

• Local content levels are being increased. In 2006, local content stood at 30%. In 2008, local content will increase to 40% and to 50% by 2009 by expanding the number of local suppliers from 18 to 30

• Renault will add 30 dealers to its network during 2008 and 2009. In 2007, it had 71 dealers operating 91 outlets

Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE 33

0

50

100

150

200

250

2005

2006

2007

2008

2009

2010

2011

2012

HEBEI

ZHONGXING

BYD

NANJING-MG

HARBIN HAFEI

GEELY

FAW

GREAT WALL

CHERY

Here Come the Chinese—Chinese Brand Car Sales in Russia

Positive Drivers

• Price competitive

• Quality rivals or beats Russian brands

• Explicit export mandate from Chinese government

• Meet Russian Euro 2 emissions levels

• Fewer safety requirements in Russia

Negative Factors

• Russian government reluctant to grant industrial assembly status under Decree 166

• Piecemeal dealer networks with dealers representing several brands

• Incomes rising rapidly and low-cost cars coming from Western OEMS

• Lack of brand and residual value could be issue in future

Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE 34

Chery

• Currently producing at Avtotor in Kalinningrad

– 18,600 units made in H1 2007

– Amulet (A15/Flagcloud)

– Tiggo

– Fora (A21)

– QQ and Kima A1 cars coming by end of 2007

• Expansion plans include large scale production with Avtotor

Amulet (Cowin/ A15)$9,390

Tiggo 3$16,950

Sweet (QQ3)$7850

Oriental Son (Eastar B11)

$21,700

Kimo A1

Fora (A5)$14,390

Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE 35

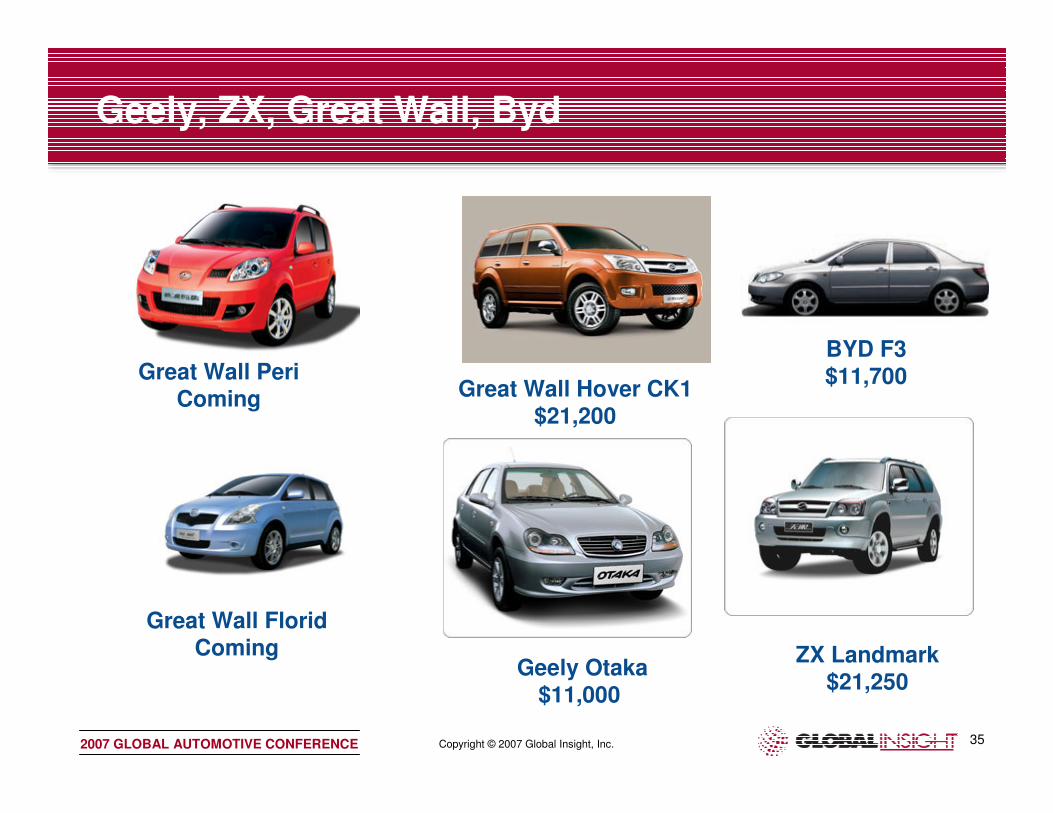

Geely, ZX, Great Wall, Byd

Great Wall Hover CK1$21,200

Great Wall FloridComing

Geely Otaka$11,000

ZX Landmark$21,250

BYD F3$11,700Great Wall Peri

Coming

Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE 36

Low-Cost (BRICs) Cars in Russia - Summary

• Smaller market segments are still very price sensitive in Russia– There is still a substantial demand for low-ish cost cars– Low-cost cars will still sell well—but this segment is no longer the potential

bonanza it once was

• Limited overlap in BRICs segmentations—Russia is closer to China and moving away from India/Brazil

– Little scope for Ultra-Low-Cost cars in Russia

• Spending power is increasing fast– Low base price is becoming less important– Don’t sacrifice functionality or size for a low price

• Tastes moving up scale from Russian, to Chinese, to “Western”– No longer relevant to target Russian brands

• The product space is already getting crowded—Just “low cost” is not enough

– “Me too” models may fail to attract consumers– Differentiate between competitors and within own model– Stretch equipment levels above base model– Several powertrains and manual/automatic– Bodystyle variants will become important

Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE 37

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

LADA CHEVROLET FORD TOYOTANISSAN HYUNDAI RENAULT DAEWOOMITSUBISHI KIA OPEL

Car Sales Volumes by BrandThose Offering Low-Cost Cars Will Do Better

Copyright © 2007 Global Insight, Inc.2007 GLOBAL AUTOMOTIVE CONFERENCE 38

Summary

• Russia is in maximum growth phase now

• Sales “should” stabilise around 3.5 million units

• Investment and wage growth have driven demand

• OEMs not producing in Russia will lose market share

• Europeans will remain under-represented

• Credit expansion has lots more potential—but with risks

• ‘Low-cost cars’ are still attractive, but will not unlock another explosion in market growth