Rus Telecoms Report 2012 Otkritiye

26

Important disclosures are found at the Disclosures Appendix. This investment research is produced by Otkritie S ecurities Ltd, authorised and regulated by the Financial Services Authority (FSA), and has been prepared by non-US research analysts who are not FINRA registered/qual ified as research analysts. UPDATE Russian Telecoms 2012 Expecting recovery Sector ratings Company Rating TP upside/ downside MTS BUY $22.8 36% VimpelCom BUY $14 33% Rostelecom SELL RUB117 -21% Sistema BUY $33.9 74% Sources: Bloomberg, Otkritie Capital estimates Telecoms 2011 performance -40% -30% -20% -10% 0% Rostelecom RTS Index MTS Sistema VimpelCom Sources: Otkritie Capital estimates Telecoms YtD performance 0% 5% 10% 15% 20% Sistema MTS RTS Index VimpelCom Rostelecom Sources: Otkritie Capital estimates We expect the Russian telecom sector to rebound in 2012. This follows in the wake of its underperformance of all major indices in 2011, mainly due to margins erosion and questionable M&A activity. This year we are very positive on mobile telecoms (MTS and VimpelCom), where we expect margins to start recovering, and we still dislike Rostelecom, which should continue facing sluggish top-line growth. MTS is our top pick among Russian telecoms, which also benefits Sistema, a direct exposure to MTS. Sistema core assets growth is also expected to be combined with further value accretive acquisitions of assets in agriculture and petrochemic als. Data services to drive top-line growth. We expect Russia‘s telecom sector to benefit from data services growth in 2012. We believe that a significant portion of the investment that is considered prerequisite to capture this growth has already been made, hence going forward the operators will need to invest less in the development of 3G data networks. Margins turnaround for mobile operators. We expect a reversal of the negative trends of declining EBITDA margins among the Russian mobile operators. Margin growth should be fuelled by an increasing share of data revenue, completion of the rollout of monobrand retail networks, and a focus on a strategy of increasing ARPU from existing customers rather than acquiring new ones. Dividend stories to remain the same. Mobile operators remain high dividend payers. We expect MTS and VimpelCom to pay out dividend yield s of 6% and 8% in 2012, respectively, while Rostelecom is expected to spend most of its operating cash flow on capex and M&A. We anticipate Rostelecom‘s dividend yield at 1.8%. Sistema‘s dividend yield is expected to be limited by extensive M&A activity, we project only 1% dividend yield for the company. MTS is our top pick amongst Russian telecoms, while Rostelecom is our least preferred stock in the sector. We continue to prefer MTS thanks to its high dividend yield, low leverage, and clear growth story. Sistema should also benefit as a direct exposure to MTS. We still like VimpelCom, but the stock has high leverage, lacks short-term positive triggers, and consists of too many moving parts that could limit its short-term upside. Rostelecom‘s major revenue source is fixed-line voice, which is projected to decrease at 2% CAGR in the next 5 years. The acquisition of Skylink provides the necessary 3G licenses for development of mobile business, though we think the major risks lie in its execution strategy. The ‗new‘ Rostelecom was recently combined from 9 separate companies and we think that in 2012 its management will struggle to effect significant changes within the company. Figure 1. Valuation table P/E EV/EBITDA EV/Sales Name 2011E 2012E 2013E 2011E 2012E 2013E 2011E 2012E 2013E MTS 11.0 8.9 7.5 4.6 4.3 3.8 1.9 1.7 1.6 VimpelCom 7.7 6.4 5.8 4.3 3.7 3.4 1.7 1.5 1.3 Rostelecom 11.8 11.7 10.9 5.1 4.5 4.6 2.0 1.8 1.7 Sistema 9.3 17.9 13.2 1.9 1.9 1.5 0.3 0.3 0.2 Sources: Bloomberg, Otkritie Capital estimates EQUITY | Russia Telecom 1 February 2011 Research analysts Alexander Vengranovich [email protected]+ 7 (495) 2131830

-

Upload

victor-funkin -

Category

Documents

-

view

220 -

download

0

Transcript of Rus Telecoms Report 2012 Otkritiye

8/3/2019 Rus Telecoms Report 2012 Otkritiye

http://slidepdf.com/reader/full/rus-telecoms-report-2012-otkritiye 1/26

Important disclosures are found at the Disclosures Appendix.This investment research is produced by Otkritie Securities Ltd, authorised and regulated by the Financial Services Authority (FSA),

and has been prepared by non-US research analysts who are not FINRA registered/qualified as research analysts.

UPDATE

Russian Telecoms 2012Expecting recovery

Sector ratings

Company Rating TPupside/

downside

MTS BUY $22.8 36%

VimpelCom BUY $14 33%

Rostelecom SELL RUB117 -21%

Sistema BUY $33.9 74%

Sources: Bloomberg, Otkritie Capital estimates

Telecoms 2011 performance

-40% -30% -20% -10% 0%

Rostelecom

RTS Index

MTS

Sistema

VimpelCom

Sources: Otkritie Capital estimates

Telecoms YtD performance

0% 5% 10% 15% 20%

Sistema

MTS

RTS Index

VimpelCom

Rostelecom

Sources: Otkritie Capital estimates

We expect the Russian telecom sector to rebound in 2012. Thisfollows in the wake of its underperformance of all major indicesin 2011, mainly due to margins erosion and questionable M&Aactivity. This year we are very positive on mobile telecoms (MTSand VimpelCom), where we expect margins to start recovering,and we still dislike Rostelecom, which should continue facingsluggish top-line growth. MTS is our top pick among Russian

telecoms, which also benefits Sistema, a direct exposure toMTS. Sistema core assets growth is also expected to becombined with further value accretive acquisitions of assets inagriculture and petrochemicals.

Data services to drive top-line growth. We expect Russia‘s telecom sector tobenefit from data services growth in 2012. We believe that a significant portion ofthe investment that is considered prerequisite to capture this growth has alreadybeen made, hence going forward the operators will need to invest less in thedevelopment of 3G data networks.

Margins turnaround for mobile operators. We expect a reversal of thenegative trends of declining EBITDA margins among the Russian mobileoperators. Margin growth should be fuelled by an increasing share of datarevenue, completion of the rollout of monobrand retail networks, and a focus on

a strategy of increasing ARPU from existing customers rather than acquiring newones.

Dividend stories to remain the same. Mobile operators remain high dividendpayers. We expect MTS and VimpelCom to pay out dividend yields of 6% and8% in 2012, respectively, while Rostelecom is expected to spend most of itsoperating cash flow on capex and M&A. We anticipate Rostelecom‘s dividendyield at 1.8%. Sistema‘s dividend yield is expected to be limited by extensiveM&A activity, we project only 1% dividend yield for the company.

MTS is our top pick amongst Russian telecoms, while Rostelecom is ourleast preferred stock in the sector. We continue to prefer MTS thanks to itshigh dividend yield, low leverage, and clear growth story. Sistema should alsobenefit as a direct exposure to MTS. We still like VimpelCom, but the stock hashigh leverage, lacks short-term positive triggers, and consists of too manymoving parts that could limit its short-term upside. Rostelecom ‘s major revenuesource is fixed-line voice, which is projected to decrease at 2% CAGR in the next5 years. The acquisition of Skylink provides the necessary 3G licenses fordevelopment of mobile business, though we think the major risks lie in itsexecution strategy. The ‗new‘ Rostelecom was recently combined from 9separate companies and we think that in 2012 its management will struggle toeffect significant changes within the company.

Figure 1. Valuation table

P/E EV/EBITDA EV/Sales

Name 2011E 2012E 2013E 2011E 2012E 2013E 2011E 2012E 2013E

MTS 11.0 8.9 7.5 4.6 4.3 3.8 1.9 1.7 1.6

VimpelCom 7.7 6.4 5.8 4.3 3.7 3.4 1.7 1.5 1.3

Rostelecom 11.8 11.7 10.9 5.1 4.5 4.6 2.0 1.8 1.7

Sistema 9.3 17.9 13.2 1.9 1.9 1.5 0.3 0.3 0.2

Sources: Bloomberg, Otkritie Capital estimates

EQUITY | Russia

Telecom

1 February 2011

Research analysts

Alexander [email protected]+7 (495) 2131830

8/3/2019 Rus Telecoms Report 2012 Otkritiye

http://slidepdf.com/reader/full/rus-telecoms-report-2012-otkritiye 2/26

Russian telecoms 2012 | UPDATE | Russia | 1 February 2011

Otkritie Capital 2

Table of Contents

Russian Telecoms peer comparison .......................................................... 3

Russian telecom market update ................................................................. 4 Mobile communications .................................................................................. 4 Broadband Internet ......................................................................................... 6 Capex ............................................................................................................. 8 Retail chains ................................................................................................... 9

MTS .............................................................................................................. 11 Valuation ....................................................................................................... 12 Appendix: Financial forecasts ....................................................................... 13

Sistema ........................................................................................................ 14 Valuation ....................................................................................................... 15

Appendix: Financial forecasts ....................................................................... 17

Rostelecom ................................................................................................. 18 Valuation ....................................................................................................... 19 Appendix: Financial forecasts ....................................................................... 20

VimpelCom .................................................................................................. 21 Valuation ....................................................................................................... 22 Appendix: Financial forecasts ....................................................................... 23

Disclosures appendix ................................................................................ 24

8/3/2019 Rus Telecoms Report 2012 Otkritiye

http://slidepdf.com/reader/full/rus-telecoms-report-2012-otkritiye 3/26

Russian telecoms 2012 | UPDATE | Russia | 1 February 2011

Otkritie Capital 3

Russian Telecomspeer comparison

Figure 2. Peers valuation

P/E EV/EBITDA EV/Sales

Ticker Name 2011E 2012E 2013E 2011E 2012E 2013E 2011E 2012E 2013E

Eastern Europe peers 14.9 15.9 14.2 4.9 5.3 5.1 1.9 1.9 2.0

SPTT CP Equity TELEFONICA CZECH REPUBLIC AS 15.1 14.8 14.7 5.7 6.3 5.9 2.3 2.4 2.4

MTEL HB Equity MAGYAR TELEKOM TELECOMMUNICA 13.4 11.9 9.7 4.4 4.4 4.3 1.5 1.5 1.6

TPS PW Equity TELEKOMUNIKACJA POLSKA SA 16.3 20.9 18.3 4.6 5.2 5.2 1.8 1.9 1.9

South East Asia 29.3 19.1 14.5 7.0 6.6 6.2 2.5 2.3 2.2

941 hk Equity CHINA MOBILE 12.7 12.4 11.9 5.4 5.2 5.0 2.6 2.4 2.3

762 HK Equity CHINA UNICOM HONG KONG 62.1 32.8 20.5 6.2 5.4 4.6 2.0 1.7 1.5

ST SP Equity SINGAPORE TELECOM 13.0 12.0 11.0 9.4 9.2 9.2 2.9 2.9 2.8

AXIATA MK Equity AXIATA GROUP BERHAD 14.9 13.4 12.2 6.1 5.8 5.5 2.8 2.6 2.4

BHARTI IN Equity BHARTI AIRTEL 21.4 14.9 11.5 8.4 6.9 6.0 2.9 2.6 2.3

RCOM IN Equity RELIANCE COMMUNICATIONS 15.3 10.4 8.0 6.8 6.1 5.6 2.2 2.0 1.9

South Africa 11.9 10.5 9.6 4.7 4.4 4.1 1.7 1.6 1.5

TKG SJ Equity TELKOM 10.0 8.8 7.6 2.6 2.5 2.4 0.7 0.7 0.7MTN SJ Equity MTN GROUP 12.0 10.5 9.6 4.6 4.2 4.0 2.1 1.8 1.7

VOD SJ Equity VODACOM GROUP 13.7 12.4 11.5 6.9 6.4 6.0 2.4 2.2 2.1

Middle East 9.8 8.2 8.1 4.3 4.3 4.2 1.4 1.4 1.3

CEL IT Equity CELLCOM ISRAEL 5.9 7.1 7.4 3.0 3.2 3.3 1.0 1.0 1.0

PTNR IT Equity PARTNER COMMUNICATIONS 5.8 6.4 6.6 3.7 4.1 4.0 1.1 1.2 1.2

Tcell ti Equity TURKCELL ILETISIM HIZMET 17.6 11.0 10.3 6.2 5.6 5.3 2.0 1.8 1.7

orte ey Equity ORASCOM TELECOM HOLDING 7.0 8.0 6.5 4.2 4.2 4.1 1.9 1.9 1.8

ETISALAT UH Equity EMIRATES TELECOM CORPORATION 10.7 10.1 9.3 4.3 4.1 3.9 2.1 2.0 1.9

TTKOM TI Equity TURK TELEKOMUNIKASYON 13.2 10.2 9.8 6.1 5.9 5.6 2.6 2.5 2.4

QTEL QD Equity QATAR TELECOM 9.6 8.8 8.4 3.3 3.2 3.1 1.6 1.5 1.4

EM peers 15.2 12.5 10.8 5.4 5.1 4.9 2.0 1.9 1.8

TEF SM Equity Telefonica 9.7 8.6 8.3 5.4 5.0 4.9 1.8 1.8 1.8

Tel2b ss Equity TELE 2 12.1 10.7 9.5 5.6 5.0 4.6 1.5 1.4 1.4

DTE GR Equity DEUTSCHE TELEKOM 11.3 12.4 11.5 4.3 4.5 4.5 1.4 1.4 1.4

FTE FP Equity FRANCE TELECOM 7.3 7.7 7.9 4.1 4.3 4.4 1.4 1.4 1.4

BT/A LN Equity BT 9.1 8.5 8.1 4.2 4.1 4.1 1.3 1.3 1.3

VOD LN equity VODAFONE 10.8 10.4 10.0 8.0 8.1 7.9 2.5 2.5 2.5

TIT IM Equity TELECOM ITALIA 5.9 6.0 5.9 3.9 3.9 3.9 1.6 1.6 1.6

TEL NO Equity TELENOR 13.6 11.3 9.4 5.8 5.3 4.9 1.8 1.7 1.6

BELG BB Equity BELGACOM 10.5 11.1 11.4 5.0 5.1 5.2 1.5 1.5 1.5

PTC PL Equity PORTUGAL TELECOM 7.3 7.1 6.5 2.4 2.2 2.2 0.9 0.8 0.8

T US Equity AT&T 12.4 11.7 11.3 5.5 5.3 5.2 1.8 1.8 1.8

VZ US Equity VERIZON COMMUNICATIONS 15.0 13.4 12.1 4.0 3.7 3.6 1.3 1.3 1.2

DM peers 10.4 9.9 9.3 4.8 4.7 4.6 1.6 1.5 1.5

Sources: Otkritie Capital estimates, Bloomberg

Figure 3. Russian Telecoms valuation comparison

P/E EV/EBITDA EV/Sales

Name 2011E 2012E 2013E 2011E 2012E 2013E 2011E 2012E 2013E

MBT US Equity MTS

Current multiples 11.0 8.9 7.5 4.6 4.3 3.8 1.9 1.7 1.6

vs EM Peers -28% -29% -31% -14% -17% -21% -8% -9% -15%

vs DM Peers 6% -10% -20% -5% -9% -17% 19% 14% 4%

vs VimpelCom 43% 38% 30% 7% 15% 14% 9% 18% 18%

vs Rostelecom -6% -24% -31% -9% -6% -17% -7% -2% -7%

VIP US Equity VimpelCom

Current multiples 7.7 6.4 5.8 4.3 3.7 3.4 1.7 1.5 1.3

vs EM Peers -50% -48% -47% -20% -27% -31% -16% -23% -28%

vs DM Peers -26% -35% -38% -11% -21% -27% 9% -4% -12%

vs MTS -30% -28% -23% -6% -13% -12% -8% -16% -16%

vs Rostelecom -35% -45% -47% -15% -18% -27% -14% -17% -22%

RTKM rx equity Rostelecom

Current multiples 11.8 11.7 10.9 5.1 4.5 4.6 2.0 1.8 1.7

vs EM Peers -23% -6% 1% -6% -12% -5% -1% -7% -8%

vs DM Peers 13% 18% 17% 5% -4% 0% 28% 16% 12%

vs MTS 6% 32% 46% 10% 6% 20% 7% 2% 8%

vs VimpelCom 53% 82% 89% 18% 21% 37% 17% 21% 28%

Sources: Otkritie Capital estimates, Bloomberg

8/3/2019 Rus Telecoms Report 2012 Otkritiye

http://slidepdf.com/reader/full/rus-telecoms-report-2012-otkritiye 4/26

Russian telecoms 2012 | UPDATE | Russia | 1 February 2011

Otkritie Capital 4

Russian telecom marketupdate

Mobile communicationsCompetition to diminish further. Both MTS and VimpelCom have moved theirfocus away from the acquisition of new subscribers, while Megafon continues toconcentrate on bolstering its leadership in the acquisition of new subscribers forthe past 4 months. We expect the competition to diminish further in 2012,especially since in 3Q11 both VimpelCom and MTS began to focus onincreasing ARPUs from existing subscribers.

Figure 4. Russia mobile subscribers, mn Figure 5. Russia mobile subscribers QoQdynamics, %

50

55

60

65

70

75

1Q10 2Q10 3Q10 4Q10 1Q11 2Q11 3Q11 Nov-11

MTS VimpelCom MegaFon

-4%

-2%

0%

2%

4%

6%

8%

10%

1Q10 2Q10 3Q10 4Q10 1Q11 2Q11 3Q11 Nov-11

MTS VimpelCom MegaFon

Sources: AC&M Sources: AC&M

EBITDA margins for mobile operators to see slow recovery in 2012.Competition had a negative effect on EBITDA margins in 2011, and itsdeceleration in terms of the rational behaviour of market players shouldpositively affect the EBITDA margins of mobile operators in 2012. The initialimpact was already seen in the 3Q11 financials of MTS.

Figure 6. Russia mobile EBITDA margin quarterlydynamics

Figure 7. Russia mobile EBITDA margin annualforecast

30%

35%

40%

45%

50%

55%

1Q10 2Q10 3Q10 4Q10 1Q11 2Q11 3Q11

MTS VimpelCom Megafon

40%

42%

44%

46%

48%

50%

52%

54%

2008 2009 2010 2011E 2012E

MTS VimpelCom Megafon

Sources: Otkritie Capital estimates Sources: Otkritie Capital estimates

8/3/2019 Rus Telecoms Report 2012 Otkritiye

http://slidepdf.com/reader/full/rus-telecoms-report-2012-otkritiye 5/26

Russian telecoms 2012 | UPDATE | Russia | 1 February 2011

Otkritie Capital 5

We believe that the increase in EBITDA margins will come from 2 factors:

1. Selling expenses. As the EBITDA margin is substantially driven by theoperator activity designed to acquire new subscribers, we expect that thetrend of shifting focus away from the acquisition of new subscribers shouldpositively impact EBITDA margins. Moreover, during 2011 mobileoperators moved to deferred dealer compensation schemes as another

way to decrease marketing expenses (based on the principle of revenue-sharing). This implies no upfront payment for the acquisition ofsubscribers. In addition, in order to decrease subscriber acquisition coststhe operators developed their own retail networks in 2011.

2. Value-added services (VAS) share in revenues. The share of VAS inmobile revenues is the major driver of improving profitability for mobileoperators. Value-added services have EBITDA margins in the 70-80%range, so the operators are focusing on increasing its share in revenues.

Data usage growth is the primary driver of the VAS share increase. The marketgrew 50% YoY in 2011, though we think that growth will decelerate to singledigits in 2012 according to MTS management guidance. Meanwhile, messagingrevenue is sliding on the back of user migration to Internet messengers such as

Skype, ICQ, and Mail Agent. We expect this trend to continue, but do not thinkthis will lead to substantial decrease in messaging revenues and will becompensated by accelerated growth in other VAS. Content revenue is alsofalling due to the improved popularity of mobile internet, which is a cheaperoption for customers vis-a-vis other multimedia content.

Figure 8. Russia VAS revenues by segment, RUBmn

0

5,000

10,000

15,000

20,000

25,000

1Q10 2Q10 3Q10 4Q10 1Q11 2Q11 3Q11Messaging Content Data Other

Sources: AC&M, Otkritie Capital estimates

VAS revenue is highly dependent upon the capacity of the 3G network. Megafon, which invested heavily in 3G rollout in 2010, is the leader in terms ofVAS share. In 2011 Megafon continued to be the leader in the number of 3Gbase stations in Russia, while MTS made substantial progress in 2011 by nearlyquadrupling the number of its base stations in operation. VimpelCom is growingslower in this respect, which is confirmed by the lower proportion of VAS sharein revenues. We expect that this year Big3 operators will reduce their activity inexpansion of 3G networks, the additions of new base stations will be morefocused on big cities, where most high-ARPU clients are located.

8/3/2019 Rus Telecoms Report 2012 Otkritiye

http://slidepdf.com/reader/full/rus-telecoms-report-2012-otkritiye 6/26

Russian telecoms 2012 | UPDATE | Russia | 1 February 2011

Otkritie Capital 6

Figure 9. VAS share in mobile revenues, % Figure 10. 3G base stations in Russia

0%

5%

10%

15%

20%

25%

30%

35%

1Q10 2Q10 3Q10 4Q10 1Q11 2Q11 3Q11

MTS Vimpelcom Megafon

0

5,000

10,000

15,000

20,000

25,000

30,000

MTS VimpelCom Megafon

2010 2011E

Sources: Otkritie Capital estimates, AC&M, Company data Sources: Otkritie Capital estimates, Company data

Broadband InternetThe number of broadband Internet users in Russia has increased 13%YtDin June 2011 and 51% since the beginning of 2010. The growth came mostlyfrom regions other than Moscow and St. Petersburg, where marketing activitiesand increased spending on building fiber lines attracted stimulated a shift awayfrom dial-up internet usage to broadband connections.

Figure 11. Russia Broadband users monthly dynamics, mnhouseholds

0

2

4

6

8

10

12

14

16

18

20

Russia Moscow St Petersburg

Sources: Otkritie Capital estimates, AC&M

Competition on the broadband market across almost Russia’s major citiesis becoming ever more severe as internet penetration increases. Althoughthere are still areas within Russia with unsaturated demand, the big playersfocus on the cities with populations exceeding 100,000, which is moreeconomically efficient. The competition in big cities is already tough, whichmakes it difficult to grow market share without acquiring local competitors.

The Russian broadband market is still dominated by Rostelecom, which hasmore than 7mn households using its services. While MTS and VimpelCom aremuch smaller, they are rapidly growing their subscriber bases via M&A activityand greenfield projects. There is still a large share of independent providers on

the market, the biggest of which is ER-Telecom, which operates in 42 cities inCentral, Northwest, Urals, South, and Siberia regions.

MTS has the biggest share of the lucrative Moscow market with over 900,000households subscribed, although VimpelCom and Akado have both been

8/3/2019 Rus Telecoms Report 2012 Otkritiye

http://slidepdf.com/reader/full/rus-telecoms-report-2012-otkritiye 7/26

Russian telecoms 2012 | UPDATE | Russia | 1 February 2011

Otkritie Capital 7

present on the market for a long time and have solid portions of it. By contrast,Rostelecom and Megafon entered the market Moscow only in 2011 viaacquisitions of NTK and NetbyNet, respectively.

The share of local players on St. Petersburg market is almost 44%. The marketis dominated by Rostelecom —VimpelCom and Megafon have only limitedmarket shares while Megafon has presence at all.

Figure 12. Russia broadbandmarket breakdown by users,1H11

Figure 13. Moscow broadbandmarket breakdown by users,1H11

Figure 14. St. Petersburgbroadband market breakdownby users, 1H11

Rostelecom41%

MTS11%

VimpelCom

9%

ER-Telecom

9%

AKADO4%

Other26%

MTS28%

VimpelCom20%

AKADO20%

Megafon11%

Rostelecom7%

Other14%

Rostelecom

45%

InterZet17%

P&NTelecom

12%

VimpelCom9%

Skynet7%

MTS2%

Other8%

Sources: Otkritie Capital estimates, AC&M Sources: Otkritie Capital estimates, AC&M Sources: Otkritie Capital estimates, AC&M

We expect M&A activity to remain the main theme for the broadbandinternet access market in Russia in 2012. We expect Rostelecom‘s marketshare to decline over the time since most of the Rostelecom lines are copperlines — such lines enable users to have only a limited-speed Internet access.Meanwhile, MTS, VimpelCom, Megafon, and often local providers offer opticfiber lines, which are able to ensure higher speeds. As a measure to stem themigration in that direction Rostelecom needs to acquire local providers in theregions or build new fiber lines. According to the new Rostelecom strategy, thecompany considers M&A as a preferred path to increase market share in the big

cities. But as the Big-3 operators are also highly engaged in competition forregional players, this has effectively increased valuations for the targetcompanies, a process that we already observed in 2011.

Figure 15. Selected deals on the Russian broadband market, 2011

Byuer Target Stake price Valuation multiple Subscribers Region Date

Rostelecom NTK 71.8% $1,325mn 8.7x 2010 EV/EBITDA 215,000 broadband. 3.2mn Pay-TV Moscow Feb-11

Megafon NetByNet 100% $270mn 6.8x 2010 EV/EBITDA 245,000 Moscow Jun-11

MTS Altair 100% $23mn 9.3x 2010 EV/EBITDA 20,000 Tula Aug-11

MTS TVT 100% $162.9mn 10.5x 2010 EV/EBITDA 600,000 broadband, 500,000 Pay-TV Tatarstan Oct-11

Sources: Otkritie Capital estimates, Company data

Some potential deals were already discussed in the media. Kommersantreported in October 2011 that CNT, which has approximately 200,000broadband subscribers in Moscow (6% share) and operates under the Qwertybrand, could be acquired by Rostelecom. CNT is 51% owned by Svyazinvest.The media has also reported that Rostelecom is in negotiations to acquireGorcom, another Moscow broadband provider. According to AC&M consulting,Gorcom has 78,000 subscribers and 2% of Moscow‘s broadband market. 100%of the company is owned by Oleg Zaporozhec. If Rostelecom manages to closethese 2 deals its share of the Moscow market could reach 15%. Considering theprice per subscriber paid by Megafon for the same size business of NetbyNet,together Qwerty and Gorcom could be valued at around $300mn.

Megafon‘s attempt to acquire Akado (20% of the Moscow market, 686,000subscribers) continues. The shareholders of both companies are still in theprocess of negotiating a final deal parameters. Meanwhile, FAS has approved arequest by MTS to acquire 100% of Skynet (7% market share in St. Petersburg,75,000 subscribers).

8/3/2019 Rus Telecoms Report 2012 Otkritiye

http://slidepdf.com/reader/full/rus-telecoms-report-2012-otkritiye 8/26

Russian telecoms 2012 | UPDATE | Russia | 1 February 2011

Otkritie Capital 8

CapexWe expect a gradual decrease in the capex/revenue ratio for mobileoperators in 2012. We use the ratio of capex to revenue in order to comparecapex efficiency and the activity of operators. After high spending on 3G basestations for mobile operators in 4Q10, we observed more balanced capex

during 9M11, as the bulk of the increase in the number of 3G base stations isover, we expect a gradual decrease in the capex/revenue ratio for operators in2012.

Both MTS and VimpelCom guide for a gradual decrease in the capex/revenueratio in 2012. VimpelCom targets for that ratio to drop to 15% by 2014.

Megafon expects some slowdown of the capex/revenue ratio in 2012, fromalready the highest level of more than 30% in 2011. Megafon‘s Board ofDirectors has approved RUB64bn of spending in 2012, which represents 27%of its RUB237bn 2012 revenue guidance.

For Rostelecom we expect a substantial increase in capex in 2012 on the backof its newly-acquired elections broadcasting project (to be finished by March2012). We4 estimated this project to bear an equipment cost of around

RUB20bn (a figure that comprises 6% of Rostelecom 2012E revenue).

Figure 16. Capex/revenue quarterly dynamics, % Figure 17. Capex/revenue annual dynamics, %

0%

10%

20%

30%

40%

50%

60%

70%

1Q10 2Q10 3Q10 4Q10 1Q11 2Q11 3Q11 4Q11E

MTS VimpelCom Megafon Rostelecom

0%

5%

10%

15%

20%

25%

30%

35%

2008 2009 2010 2011E 2012E

MTS VimpelCom Megafon Rostelecom

Sources: Otkritie Capital estimates Sources: Otkritie Capital estimates

We do not incorporate 4G network rollout expenditures in our models dueto the lack of clarity regarding the timing and cost of the 4G licenses. Weexpect that auctions for 4G frequencies could be delayed beyond the initially settime horizon of 1Q12. As the March 2012 presidential elections approach, theprobability of a delay rises owing to uncertainty surrounding the identity of apossible new Minister of Telecommunications in the event that Igor Schegolev

is replaced in the new Cabinet. The current state position assumes that as a result of the auctions theBig-4 operators should obtain equal parts of the spectrum suitable for 4Grollout in Russia. This is based on a September 2011 decision of the StateComission on Wireless Frequences to distribute 4 equal parts of the spectrum.The Commission fixed the range of 791-862MHz, 2.5-2.7GHz and 2.3-2.4GHzas available for 4G rollout. According to the Commission‘s resolution the first 4parts of 791-862MHz frequency range will be distributed at the 1

ststage of the

auction, while in the future the winners of the 1st

stage will get frequencies in2.5-2.7GHz range for free. The main difficulty is that the range of frequenciesdesignated for the auctions is currently occupied by the Ministry of Defense,which requires additional conversion costs to be incurred by the winners. Thecost estimates of the conversion of the full range of the spectrum vary from$2bn to $3bn.

8/3/2019 Rus Telecoms Report 2012 Otkritiye

http://slidepdf.com/reader/full/rus-telecoms-report-2012-otkritiye 9/26

Russian telecoms 2012 | UPDATE | Russia | 1 February 2011

Otkritie Capital 9

Rostelecom could benefit if the auctions are delayed. Before the auctionsare held, some operators could already start providing 4G services since theyalready have the necessary licenses. Skartel (Yota brand) has a part of the 2.5-2.7GHz range, while Osnova Telecom and Rostelecom have the right to build a4G network based on 2.3-2.4GHz frequencies (Rostelecom has licenses for 39regions).

Another option to avoid total frequency conversion is the introduction oftechnological neutrality which could bolster faster 4G rollout and enableoperators to create network unions. Technological neutrality is the ability to useany frequencies that are suitable for the provision of telecom services. This isthe chief prerequisite for joint use of base stations by operators, as it wouldallow a base station to operate using different frequencies simultaneously.Technological neutrality is mainly supported by Tele2 and regional players,since it would enable them to build 4G networks on existing frequencies. Untilnow, the Ministry of Telecommunications has been reluctant to consider anyproposals in this respect.

Retail chains

In 2011 mobile operators took a big step forward in rolling out brandedretail chains. Owning a retail chain is another way to increase margins, as thisdecreases dealer and payment commissions and allows better access toclients, which helps to hasten the impact of marketing initiatives.

MTS has the biggest operational retail chain, which comprises more than 2,200stores. Theoretically Rostelecom has the biggest chain (3,000 stores), but manyare old-fashioned and inefficient (only selling 2-3 mobile phones a month insome stores). The fact that the stores are not separated from the core businessmakes it almost impossible for management to track their performance. Onlyonce they are transformed into a special subsidiary is it clear which negativeeffect on the financials they may have.

Figure 18. Russia mobile retail networks, # of stores

0

1,000

2,000

3,000

4,000

5,000

6,000

Euroset MTS Megafon Rostelecom VimpelCom Svyaznoy

Own Franchise

Sources: Otkritie Capital estimates, company data, Kommersant

The higher number of monobrand stores leads to a higher proportion of MTSsales generated through its own network.

8/3/2019 Rus Telecoms Report 2012 Otkritiye

http://slidepdf.com/reader/full/rus-telecoms-report-2012-otkritiye 10/26

Russian telecoms 2012 | UPDATE | Russia | 1 February 2011

Otkritie Capital 10

Figure 19. New revenue generation breakdown by type of distributionchannel

50%

30%

20%

32%

30%38%

0%

20%

40%

60%

80%

100%

120%

MTS VimpelCom

Own network National dealers Regional dealers & street retail

Sources: Otkritie Capital estimates, company data

We expect to see some increase for MTS and VimpelCom in terms of thenumber of monobrand stores in 2012. These operators will focus more onimproving existing networks, which we think should have a minor positive effecton their financials. Rostelecom is expected to modernize its retail network,which could mean some additional SG&A expenses that are currently notincluded in our model.

8/3/2019 Rus Telecoms Report 2012 Otkritiye

http://slidepdf.com/reader/full/rus-telecoms-report-2012-otkritiye 11/26

Otkritie Capital 11

UPDATE

MTSTop pick among Russian telecoms

BUYTicker MBT US

Target price, $ 22.8

Last price of ADRs, $ 16.7

Upside 36%

Number of ADRs, mn 1,008.5

Market cap, $mn 16,882

Net debt, $mn 6,360EV, $mn 23,243

Free float 47%

52-week min, $ 11.9

52-week max, $ 21.5

Sources: Bloomberg, Otkritie Capital estimates

Share price performance

60

70

80

90

100

110

120

J a n - 1 1

F e b - 1 1

M a r - 1 1

A p r - 1 1

M a y - 1 1

J u n - 1 1

J u l - 1 1

A u g - 1 1

S e p - 1 1

O c t - 1 1

N o v - 1 1

D e c - 1 1

MT S (Rebased) R TS (R ebased )

Sources: Bloomberg

We reiterate our BUY rating with a new target price of $22.8 forMTS, which still remains our top pick among Russian telecoms.MTS, which is a leader on the Russian mobile market, is well-positioned to grasp the cream of the data revenue growth. Thestock is a low leverage company, which pays high dividends andtrades at 17% discount to EM peers on 2012E EV/EBITDA multiple.

Solid 3Q11 results may signal EBITDA margin turnaround. We think that

MTS‘ 3Q11 results, posted in November 2011, could be a first sign of a marginturnaround for the company. The improvement in EBITDA margin was mainlyattributable to a reduction of Sales and marketing costs, which was a result ofreduced subscriber acquisition activity. Top line improvement came mostlyfrom increased ARPU, which continues to benefit from a rising share of VAS inMTS revenues.

Comfortable leverage. Net debt/EBITDA has declined from 1.2 to 1.1 QoQ in3Q11. This level compares to 1.4 for Rostelecom and 2.6 for VimpelCom. Themanagement confirms its intention to keep the leverage at the current level in2012.

Dividend yield projected at 7%. The company paid 78% of its net income for2010 as dividend in June 2011, which assumed $1.07/ADR. This year we expectMTS to pay the same dividend for 2011, which leads to a 6% dividend yield.

MGTS acquisition synergies could represent upside. We think the negativeeffect of MGTS‘ acquisition is already priced in, but we could see additionalupside coming from synergies. MTS estimates the deal would bring synergies ofRUB14bn, which we currently do not incorporate in our model.

Value dilutive M&A risks cannot be ruled out. Though MTS managementclaims that no cross border M&A activity is planned for 2012, we think MTScould still enter in some big M&A deal, like VimpelCom did in 2011. Sistemamanagement announced several times that MTS should become a global playerwith >200mn clients; these plans were also followed by media speculationsregarding the potential sale of SSTL (Sistema‘s Indian telecom asset) to MTS,which in fact would be negatively taken by the market, especially considering theloss-making profile of SSTL.

Catalysts. Along with the 4G auctions results, which will be released in 1H12,we think that the closest catalyst for the company will be its 4Q11 US GAAPresults, slated for 7 March 2012 – we think these should show a substantial YoYimprovement on both the top and bottom lines. Progress in the rollout of thefibre network in Moscow in 2012 will be also a very important catalyst for thecompany.

Figure 20. Key metrics ($mn) Figure 21. Valuation

2011E 2012E 2013E 2014E

Revenues 12,492 13,011 14,034 15,153

EBITDA 4,998 5,365 5,838 6,395

EBIT 2,625 3,023 3,452 3,819

Net Income 1,529 1,905 2,258 2,565

Net Debt 6,360 5,879 5,281 4,366

EPS, $ 1.52 1.89 2.24 2.54

CEPS, $ 3.87 4.21 4.60 5.10

BVPS, $ 3.54 4.37 5.29 6.26

DPS, $ 1.06 1.32 1.57 1.78

2011E 2012E 2013E 2014E

P/E 11.0 8.9 7.5 6.6

EV/EBITDA 4.7 4.2 3.8 3.3

EV/Sales 1.9 1.7 1.6 1.4

P/BV 4.7 3.8 3.2 2.7

EBITDA margin 40.0% 41.2% 41.6% 42.2%

Net margin 12.2% 14.6% 16.1% 16.9%

Revenue growth 11% 4% 8% 8%

EPS growth 11% 25% 19% 14%

Div Yield 6% 8% 9% 11%

Sources: Bloomberg, Otkritie Capital estimates Sources: Bloomberg, Otkritie Capital estimates

EQUITY | Russia

Telecom

1 February 2011

Research analysts

Alexander [email protected]+7 (495) 213 1830

8/3/2019 Rus Telecoms Report 2012 Otkritiye

http://slidepdf.com/reader/full/rus-telecoms-report-2012-otkritiye 12/26

MTS | UPDATE | Russia | 1 February 2011

Otkritie Capital 12

Valuation

Figure 22. MTS DCF Valuation, $mn

2011E 2012E 2013E 2014E 2015E 2016E 2017E 2018E 2019E

Revenue 12,492 13,011 14,034 15,153 16,245 17,293 18,309 19,407 20,506

EBITDA 4,998 5,365 5,838 6,395 7,050 7,527 7,983 8,479 8,971EBITDA Margin 40.0% 41.2% 41.6% 42.2% 43.4% 43.5% 43.6% 43.7% 43.8%

EBIT 2,625 3,023 3,452 3,819 4,288 4,587 4,871 5,180 5,485

EBIT Margin 21.0% 23.2% 24.6% 25.2% 26.4% 26.5% 26.6% 26.7% 26.8%

Unlevered PBT 2,625 3,023 3,452 3,819 4,288 4,587 4,871 5,180 5,485

* Tax Rate effective cash basis 26% 26% 26% 26% 26% 26% 26% 26% 26%

Unlevered Tax -671 -773 -882 -976 -1,096 -1,172 -1,245 -1,324 -1,402

Investment CF -3,362 -2,602 -2,666 -2,576 -2,437 -2,075 -2,197 -2,329 -2,461

(Capex)/Sales 26.9% 20.0% 19.0% 17.0% 15.0% 12.0% 12.0% 12.0% 12.0%

Other Cash Adj. (inc. Working Capital) 53 -108 -61 -84 -130 -91 -100 -113 -124

Unlevered, Adj. Free Cash Flow 1,018 1,883 2,228 2,759 3,387 4,189 4,441 4,714 4,985

Discount Factor 0.00 0.88 0.78 0.69 0.61 0.54 0.48 0.42 0.37

Present Value of FCF 0 1,664 1,740 1,904 2,066 2,257 2,115 1,984 1,854

$mn $/share

Value of Cash Flows 15,584 15.5

Value from Perpetuity 13,970 13.9

Adjustments -6,549 -6.5

Implied Equity Value 23,004 22.8

Current Market Value 16882 16.7

Upside 36.3%

Sources: Otkritie Capital estimates

Figure 23. MTS peers comparison

P/E EV/EBITDA EV/Sales

Name 2011E 2012E 2013E 2011E 2012E 2013E 2011E 2012E 2013E

MBT US Equity MTS

Current multiples 11.0 8.9 7.5 4.6 4.3 3.8 1.9 1.7 1.6

vs EM Peers -28% -29% -31% -14% -17% -21% -8% -9% -15%

vs DM Peers 6% -10% -20% -5% -9% -17% 19% 14% 4%

vs VimpelCom 43% 38% 30% 7% 15% 14% 9% 18% 18%

vs Rostelecom -6% -24% -31% -9% -6% -17% -7% -2% -7%

Sources: Otkritie Capital estimates, Bloomberg

8/3/2019 Rus Telecoms Report 2012 Otkritiye

http://slidepdf.com/reader/full/rus-telecoms-report-2012-otkritiye 13/26

MTS | UPDATE | Russia | 1 February 2011

Otkritie Capital 13

Appendix: Financial forecasts

Profitability

4,400

4,600

4,800

5,000

5,200

5,400

5,600

5,800

6,0006,200

6,400

36%

38%

40%

42%

44%

46%

48%

50%

52%54%

56%

2008 2009 2010E 2011E 2012E 2013E 2014E

EBITDA margin (LHS) EBITDA,$m

Cash flows, $m

(4,000)

(3,000)

(2,000)

(1,000)

0

1,000

2,000

3,000

4,000

5,000

6,000

2008 2009 2010E 2011E 2012E 2013E 2014E

Operating cash flow Investing cash flow

Momentum, %

0.50

0.40

0.30

0.20

0.10

0%

10%

20%

30%

2008 2009 2010E 2011E 2012E 2013E 2014E

Revenue g rowt h E PS g rowt h

Valuation

0

2

4

68

10

12

14

2008 2009 2010E 2011E 2012E 2013E 2014E

P/E EV/EBITDA

$mn unless otherwise stated

2009 2010E 2011E 2012E 2013E 2014E

Income Statement

Revenues 9,867 11,293 12,492 13,011 14,034 15,153

Depreciation 1,844 2,000 2,374 2,342 2,386 2,576EBITDA 4,491 4,873 4,998 5,365 5,838 6,395

Operating profit (EBIT) 2,647 2,872 2,625 3,023 3,452 3,819

Net Interest expense 467 693 551 444 399 354

Non-op. expenses (589) 24 0 0 0 0

Pretax Profit 1,504 2,066 2,074 2,579 3,053 3,465

Taxes 505 517 530 659 780 885

Minority interest (20) 168 15 15 15 15

Net Profit 1,019 1,381 1,529 1,905 2,258 2,565

Cash Flow Statement

Net Change in work. cap. (397) (48) 53 (108) (61) (84)

Provisions and write-offs 589 (24) 0 0 0 0

Other - - - - - -

Operating cashflow 3,035 3,477 3,970 4,154 4,598 5,072

Capex (1,800) (2,647) (2,998) (2,602) (2,666) (2,576)

Disposals (Acquisitions) (56) 465 (364) 0 0 0

Investing cashflow (1,856) (2,182) (3,362) (2,602) (2,666) (2,576)

Equity - - - - - -Debt 131 (3,036) 280 (3,270) (1,833) (1,681)

Financing cashflow 131 (3,036) 280 (3,270) (1,833) (1,681)

Net Change in Cash 1,310 (1,741) 888 (1,718) 98 815

Balance sheet

Cash & equivalents 2,736 1,261 2,149 431 529 1,344

Current Assets 1,666 1,463 1,571 1,568 1,646 1,737

PP&E 11,057 11,361 12,350 12,610 12,891 12,891

Goodwill and other 306 392 481 569 660 752

Total Assets 15,764 14,478 16,552 15,179 15,725 16,724

Current Liabilities 2,257 2,398 2,648 2,625 2,732 2,832

S-T Debt 0 0 0 0 0 0

L-T Debt 6,327 7,150 8,510 6,310 5,810 5,710

Other L-T Liabilities 1,103 1,119 1,134 1,149 1,164 1,179

Shareholders Funds 3,345 3,125 3,574 4,408 5,333 6,317

Total L iabilities & Equity 13,031 13,792 15,865 14,492 15,039 16,038

Net Debt 3,591 5,888 6,360 5,879 5,281 4,366

Margins and profitability

EBIT Margin 26.8% 25.4% 21.0% 23.2% 24.6% 25.2%

EBITDA Margin 45.5% 43.1% 40.0% 41.2% 41.6% 42.2%

Net Margin 10.3% 12.2% 12.2% 14.6% 16.1% 16.9%

ROE 30.5% 44.2% 42.8% 43.2% 42.3% 40.6%

ROA 6.5% 9.5% 9.2% 12.6% 14.4% 15.3%

ROIC 19.7% 21.2% 17.9% 20.0% 22.2% 24.3%

Momentum

Revenue growth -4% 14% 11% 4% 8% 8%

EBITDA growth -13% 9% 3% 7% 9% 10%

EPS growth -47% -48% 11% 25% 19% 14%

Liquidity and solvency

Cash Ratio 1.2 0.5 0.8 0.2 0.2 0.5

Current Ratio 0.7 0.6 0.6 0.6 0.6 0.6

Interest Coverage 5.7 4.1 4.8 6.8 8.7 10.8

Debt/Equity 1.9 2.3 2.4 1.4 1.1 0.9

Debt/Total assets 0.4 0.5 0.5 0.4 0.4 0.3

Net debt / EBITDA 0.8 1.2 1.3 1.1 0.9 0.7

ValuationP/E 6.3 12.2 11.0 8.9 7.5 6.6

P/CE 2.2 5.0 4.3 4.0 3.6 3.3

P/BV 1.9 5.4 4.7 3.8 3.2 2.7

EV/Sales 2.1 2.0 1.9 1.7 1.6 1.4

EV/EBITDA 4.6 4.7 4.7 4.2 3.8 3.3

Dividend yield, (ords) 15.5% 6.4% 6.3% 7.9% 9.4% 10.6%

Dividend yield, (prefs) - - - - - -

Per Share Data

EPS - stock 1 2.65 1.37 1.52 1.89 2.24 2.54

DPS, ords 2.60 1.07 1.06 1.32 1.57 1.78

DPS, prefs - - - - - -

BVPS - stock 1 8.70 3.10 3.54 4.37 5.29 6.26

Source: Company data, Otkritie Capital estimates

8/3/2019 Rus Telecoms Report 2012 Otkritiye

http://slidepdf.com/reader/full/rus-telecoms-report-2012-otkritiye 14/26

Otkritie Capital 14

UPDATE

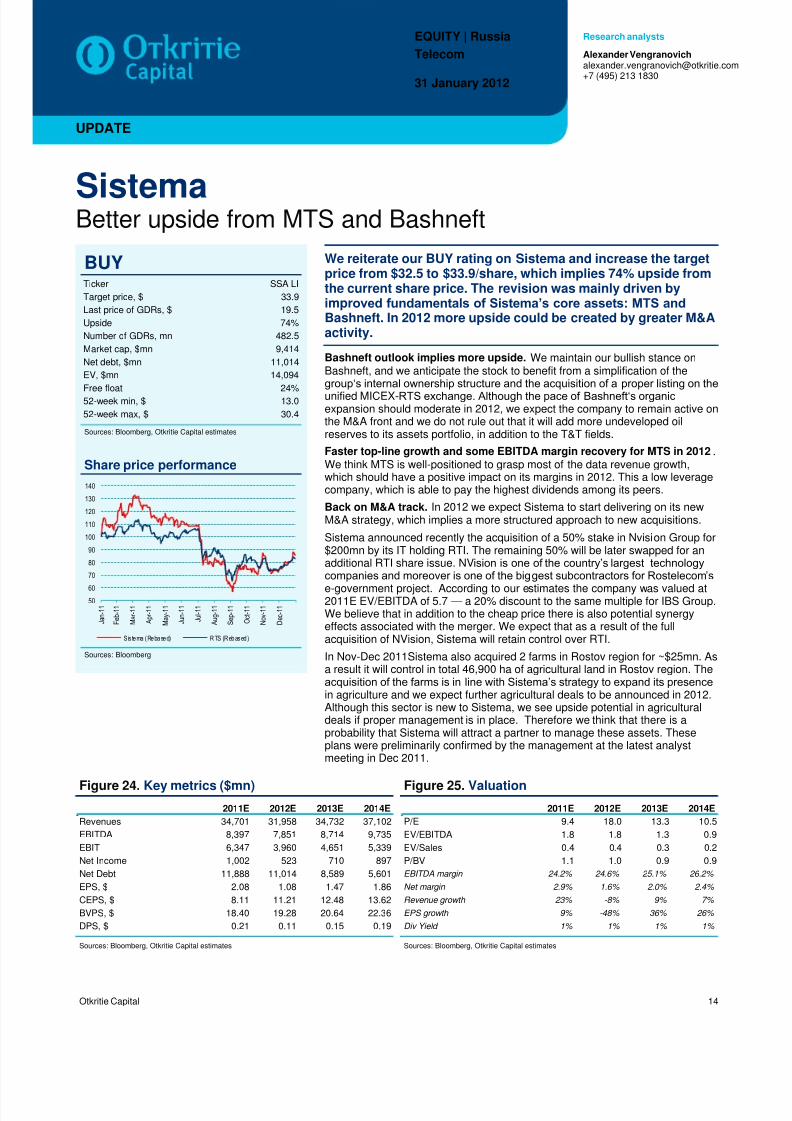

SistemaBetter upside from MTS and Bashneft

BUYTicker SSA LI

Target price, $ 33.9

Last price of GDRs, $ 19.5

Upside 74%

Number of GDRs, mn 482.5

Market cap, $mn 9,414

Net debt, $mn 11,014EV, $mn 14,094

Free float 24%

52-week min, $ 13.0

52-week max, $ 30.4

Sources: Bloomberg, Otkritie Capital estimates

Share price performance

50

60

70

80

90

100

110

120

130

140

J a n - 1 1

F e b - 1 1

M a r - 1 1

A p r - 1 1

M a y - 1 1

J u n - 1 1

J u l - 1 1

A u g - 1 1

S e p - 1 1

O c t - 1 1

N o v - 1 1

D e c - 1 1

Sistema (Rebased) RTS (Rebased)

Sources: Bloomberg

We reiterate our BUY rating on Sistema and increase the targetprice from $32.5 to $33.9/share, which implies 74% upside fromthe current share price. The revision was mainly driven byimproved fundamentals of Sistema’s core assets: MTS andBashneft. In 2012 more upside could be created by greater M&Aactivity.

Bashneft outlook implies more upside. We maintain our bullish stance onBashneft, and we anticipate the stock to benefit from a simplification of thegroup‗s internal ownership structure and the acquisition of a proper listing on theunified MICEX-RTS exchange. Although the pace of Bashneft‗s organicexpansion should moderate in 2012, we expect the company to remain active onthe M&A front and we do not rule out that it will add more undeveloped oilreserves to its assets portfolio, in addition to the T&T fields.

Faster top-line growth and some EBITDA margin recovery for MTS in 2012.We think MTS is well-positioned to grasp most of the data revenue growth,which should have a positive impact on its margins in 2012. This a low leveragecompany, which is able to pay the highest dividends among its peers.

Back on M&A track. In 2012 we expect Sistema to start delivering on its newM&A strategy, which implies a more structured approach to new acquisitions.

Sistema announced recently the acquisition of a 50% stake in Nvision Group for$200mn by its IT holding RTI. The remaining 50% will be later swapped for anadditional RTI share issue. NVision is one of the country‘s largest technologycompanies and moreover is one of the biggest subcontractors for Rostelecom‘se-government project. According to our estimates the company was valued at2011E EV/EBITDA of 5.7 — a 20% discount to the same multiple for IBS Group.We believe that in addition to the cheap price there is also potential synergyeffects associated with the merger. We expect that as a result of the fullacquisition of NVision, Sistema will retain control over RTI. In Nov-Dec 2011Sistema also acquired 2 farms in Rostov region for ~$25mn. Asa result it will control in total 46,900 ha of agricultural land in Rostov region. Theacquisition of the farms is in line with Sistema‘s strategy to expand its presencein agriculture and we expect further agricultural deals to be announced in 2012.Although this sector is new to Sistema, we see upside potential in agriculturaldeals if proper management is in place. Therefore we think that there is aprobability that Sistema will attract a partner to manage these assets. Theseplans were preliminarily confirmed by the management at the latest analystmeeting in Dec 2011.

Figure 24. Key metrics ($mn) Figure 25. Valuation

2011E 2012E 2013E 2014E

Revenues 34,701 31,958 34,732 37,102

EBITDA 8,397 7,851 8,714 9,735

EBIT 6,347 3,960 4,651 5,339

Net Income 1,002 523 710 897

Net Debt 11,888 11,014 8,589 5,601

EPS, $ 2.08 1.08 1.47 1.86

CEPS, $ 8.11 11.21 12.48 13.62

BVPS, $ 18.40 19.28 20.64 22.36

DPS, $ 0.21 0.11 0.15 0.19

2011E 2012E 2013E 2014E

P/E 9.4 18.0 13.3 10.5

EV/EBITDA 1.8 1.8 1.3 0.9

EV/Sales 0.4 0.4 0.3 0.2

P/BV 1.1 1.0 0.9 0.9

EBITDA margin 24.2% 24.6% 25.1% 26.2%

Net margin 2.9% 1.6% 2.0% 2.4%

Revenue growth 23% -8% 9% 7%

EPS growth 9% -48% 36% 26%

Div Yield 1% 1% 1% 1%

Sources: Bloomberg, Otkritie Capital estimates Sources: Bloomberg, Otkritie Capital estimates

EQUITY | Russia

Telecom

31 January 2012

Research analysts

Alexander [email protected]+7 (495) 213 1830

8/3/2019 Rus Telecoms Report 2012 Otkritiye

http://slidepdf.com/reader/full/rus-telecoms-report-2012-otkritiye 15/26

Sistema | UPDATE | Russia | 1 February 2011

Otkritie Capital 15

Valuation

Figure 26. Sistema SOTP valuation

Company OwnershipTarget Enterprise

value, $mnAdjustments

(Net debt+associates), $mnTarget Value

Of Sistema's Stake, $mnPer Share

of Sistema, $

Telecoms

MTS 53% 29,553 6,549 12,192 25.3

SSTL 57% 653 653 0 0.0

Oil & Energy

Bashneft 63% 12,019 2,420 7,352 15.2

Bashkiria Oil & Energy assets 17-50% 809 42 767 1.6

Russneft 49% 6,090 5,366 724 1.5

Technology

Sitronics 62% 756 641 71 0.1

RTI 82% 589 370 179 0.4

NVision 50% 400 0 200 0.4

Binnopharm 100% 63 63 0 0.0

Consumer

Detskiy Mir 75% 303 0 227 0.5

MBRD 99% 544 539 1.1

Medsi 100% 203 76 127 0.3

Intourist 66% 179 120 59 0.1

SMM 75% 333 89 183 0.4

Agriculture 100% 25 0 25 0.1

Sum Of The Parts Valuation

Gross SOTP value 22,645 46.9

Intercompany transactions, PV as 2% of Gross SOTP value (453) (0.9)

Net SOTP value 22,192 46.0

Discount due to Sistema's holding structure 20.0%

Discounted Net SOTP value 17,754 36.8

Corporate debt (1,416) (2.9)

Sistema's SOTP value, adjusted to net corporate debt 16,338

Target Price/GDR 33.9

Sources: Otkritie Capital estimates, Bloomberg

Figure 27. Sistema upside breakdown by drivers, $/share

19.4

6.3

5.9

2.5

2.2 2.9

0.9

33.9

0

5

1015

20

25

30

35

40

C u r r e n t p r i c e

M T S u p s i d e

D i s c o u n t c o n t r a c t i o n

B a s h n e f t u p s i d e

D e v e l o p i n g a s s e t s u p s i d e

C o r p o r a t e d e b t

I n t e r c o m p a n y t r a n s a c t i o n s

T a r g e t p r i c e

Sources: Otkritie Capital Estimates

8/3/2019 Rus Telecoms Report 2012 Otkritiye

http://slidepdf.com/reader/full/rus-telecoms-report-2012-otkritiye 16/26

Sistema | UPDATE | Russia | 1 February 2011

Otkritie Capital 16

Figure 28. Sistema discount to market NAV, %

-10%

0%

10%

20%

30%

40%

50%

A

p r - 0 9

M

a y - 0 9

J

u n - 0 9

J u l - 0 9

A

u g - 0 9

S

e p - 0 9

O

c t - 0 9

N

o v - 0 9

D

e c - 0 9

J

a n - 1 0

F

e b - 1 0

M

a r - 1 0

A

p r - 1 0

M

a y - 1 0

J

u n - 1 0

J u l - 1 0

A

u g - 1 0

S

e p - 1 0

O

c t - 1 0

N

o v - 1 0

D

e c - 1 0

J

a n - 1 1

F

e b - 1 1

M

a r - 1 1

A

p r - 1 1

M

a y - 1 1

J

u n - 1 1

J u l - 1 1

A

u g - 1 1

S

e p - 1 1

O

c t - 1 1

N

o v - 1 1

D

e c - 1 1

J

a n - 1 2

Average discount

Sources: Otkritie Capital estimates, Bloomberg

8/3/2019 Rus Telecoms Report 2012 Otkritiye

http://slidepdf.com/reader/full/rus-telecoms-report-2012-otkritiye 17/26

Sistema | UPDATE | Russia | 1 February 2011

Otkritie Capital 17

Appendix: Financial forecasts

Profitability

5,000

5,500

6,000

6,500

7,000

7,500

8,000

8,500

9,0009,500

10,000

20%

22%

24%

26%

28%

30%

32%

34%

36%38%

40%

2008 2009 2010 2011E 2012E 2013E 2014E

EBITDA margin (LHS) EBITDA,$m

Cash flows, $m

(8,000)

(6,000)

(4,000)

(2,000)

0

2,0004,000

6,000

8,000

2008 2009 2010 2011E 2012E 2013E 2014E

Operating cash flow Investing cash flow

Momentum, %

5

0%

500%

1,000%

1,500%

2,000%

2,500%

3,000%

2008 2009 2010 2011E 2012E 2013E 2014E

Revenue g rowt h E PS g rowt h

Valuation

0

20

40

60

80

100

120

140

160

2008 2009 2010 2011E 2012E 2013E 2014E

P/E EV/EBITDA

$mn unless otherwise stated

2009 2010 2011E 2012E 2013E 2014E

Income Statement

Revenues 18,750 28,098 34,701 31,958 34,732 37,102

Depreciation 2,491 2,946 2,912 4,887 5,311 5,674EBITDA 6,727 7,309 8,397 7,851 8,714 9,735

Operating profit (EBIT) 4,237 4,362 6,347 3,960 4,651 5,339

Net Interest expense 1,054 1,466 1,516 1,437 1,227 1,016

Non-op. expenses (128) 24 0 0 0 0

Pretax Profit 3,055 2,921 4,831 2,522 3,424 4,323

Taxes 747 1,089 1,932 1,009 1,369 1,729

Minority interest 643 1,199 1,896 990 1,344 1,697

Net Profit 1,643 919 1,002 523 710 897

Cash Flow Statement

Net Change in work. cap. (1,947) (474) 894 (468) 473 404

Provisions and write-offs - - - - - -

Other 261 147 181 167 181 194

Operating cashflow 3,090 4,736 4,989 5,110 6,676 7,168

Capex (3,434) (4,180) (4,531) (4,135) (4,199) (4,109)

Disposals (Acquisitions) (2,636) (410) 0 0 0 0

Investing cashflow (6,071) (4,590) (4,531) (4,135) (4,199) (4,109)

Equity 1,215 280 0 0 0 0Debt 7,248 157 500 (2,000) (2,000) (2,000)

Financing cashflow 4,380 (1,015) 500 (2,000) (2,000) (2,000)

Net Change in Cash 1,400 (868) 869 (1,125) 425 988

Balance sheet

Cash & equivalents 4,013 3,145 4,014 2,889 3,313 4,302

Current Assets 13,678 14,576 17,073 15,367 16,378 17,868

PP&E 19,267 19,040 20,659 19,906 18,794 17,228

Goodwill and other 9,066 10,494 10,313 10,146 9,965 9,771

Total Assets 42,011 44,109 48,044 45,420 45,137 44,868

Current Liabilities 13,178 13,928 16,500 15,353 16,312 17,117

S-T Debt 3,737 3,196 3,246 3,146 3,046 2,946

L-T Debt 11,204 12,207 12,657 10,757 8,857 6,957

Other L-T Liabilities - - - - - -

Shareholders Funds 6,793 7,967 8,880 9,303 9,961 10,786

Total L iabilities & Equity 42,011 44,109 48,044 45,420 45,137 44,868

Net Debt 10,928 12,258 11,888 11,014 8,589 5,601

Margins and profitability

EBIT Margin 22.6% 15.5% 18.3% 12.4% 13.4% 14.4%

EBITDA Margin 35.9% 26.0% 24.2% 24.6% 25.1% 26.2%

Net Margin 8.8% 3.3% 2.9% 1.6% 2.0% 2.4%

ROE 24.2% 11.5% 11.3% 5.6% 7.1% 8.3%

ROA 3.9% 2.1% 2.1% 1.2% 1.6% 2.0%

ROIC 13.7% 12.9% 18.4% 11.7% 14.6% 18.2%

Momentum

Revenue growth 17% 50% 23% -8% 9% 7%

EBITDA growth 23% 9% 15% -6% 11% 12%

EPS growth 2,553% -44% 9% -48% 36% 26%

Liquidity and solvency

Cash Ratio 0.3 0.2 0.2 0.2 0.2 0.3

Current Ratio 1.0 1.0 1.0 1.0 1.0 1.0

Interest Coverage 4.0 3.0 4.2 2.8 3.8 5.3

Debt/Equity 2.2 1.9 1.8 1.5 1.2 0.9

Debt/Total assets 0.4 0.3 0.3 0.3 0.3 0.2

Net debt / EBITDA 1.6 1.7 1.4 1.4 1.0 0.6

ValuationP/E 5.7 10.2 9.4 18.0 13.3 10.5

P/CE 2.3 2.4 2.4 1.7 1.6 1.4

P/BV 1.4 1.2 1.1 1.0 0.9 0.9

EV/Sales 0.8 0.5 0.4 0.4 0.3 0.2

EV/EBITDA 2.2 2.1 1.8 1.8 1.3 0.9

Dividend yield, (ords) - - 1.1% 0.6% 0.8% 1.0%

Dividend yield, (prefs) - - - - - -

Per Share Data

EPS - stock 1 3.41 1.90 2.08 1.08 1.47 1.86

DPS, ords - - 0.21 0.11 0.15 0.19

DPS, prefs - - - - - -

BVPS - stock 1 14.08 16.51 18.40 19.28 20.64 22.36

Source: Company data, Otkritie Capital estimates

8/3/2019 Rus Telecoms Report 2012 Otkritiye

http://slidepdf.com/reader/full/rus-telecoms-report-2012-otkritiye 18/26

Otkritie Capital 18

UPDATE

RostelecomTimes are changing, but our view remains the same

SELLTicker RTKM RX

Target price, RUB 117

Last price of common shares, RUB 146

Upside -20%

Number of common shares, mn 2,943.3

Market cap, $mn 14,833

Net debt, $mn 3,991EV, $mn 18,823

Free float 31%

52-week min, RUB 127

52-week max, RUB 221

Sources: Bloomberg, Otkritie Capital estimates

Share price performance

70

80

90

100

110

120

130

140

J a n - 1 1

F e b - 1 1

M a r - 1 1

A p r - 1 1

M a y - 1 1

J u n - 1 1

J u l - 1 1

A u g - 1 1

S e p - 1 1

O c t - 1 1

N o v - 1 1

D e c - 1 1

Roste lecom (Rebased) RTS (Rebased)

Sources: Bloomberg

We increase our target price for Rostelecom from RUB110 toRUB117/ordinary share, but still reiterate SELL rating for the stock.Rostelecom is the least preferred stock in our universe. We expectnegative dynamics in the company’s fixed line business, which islosing customers, who are shifting to mobile communications.We’ve seen little progress in Rostelecom mobile operations in 2011and do not expect a breakthrough in 2012. The company remains alow-dividend payer with 1.7% dividend yield on ordinary shares.

Skylink acquisition provides 3G licenses. Rostelecom has acquired a 100% stakein Skylink in December 2011 for RUB 9.4bn. We expect the company to use Skylink3G licenses in the regions to enter new regions and attract new customers, thoughthe major risks of that strategy lie on the execution side. As the mobile market issaturated

Joint 4G rollout with Skartel – not a game changer. Skartel (Yota brand) has only150 base stations and network rollout implies substantial investments, which are stillnot included in Rostelecom financial model, therefore we do not expect substantialupside from earlier 4G rollout.

B2G services revenue could surprise on the both sides. Rostelecom‘s project for online broadcasting from election sites will only be partially financed by the state,which is ready to pay only RUB13bn, while the cost of the project is estimated ashigh as RUB20-30bn. We doubt that the company could find additional uses for

infrastructure created, otherwise it would need to recognize a loss of as much asRUB17bn (impairment on the equipment). That could amount to as much as 40% ofthe company‘s FY12 net income under US GAAP

Svyazinvest-Rostelecom restructuring details to be announced in 2012. In 2012the decision regarding the second stage of Svyazinvest-Rostelecom restructuringshould be announced. While we do not think the deal terms would be beneficial forthe minorities, there is still potential upside from that. Overall we do not expect therestructuring to be finished before 2013.

Dividend yield is expected to be the lowest among Russian peers. Rostelecom‘snew dividend policy assumes payment of minimum 20% of net income under USGAAP as dividend for ordinary shares, that means RUB 8.5bn to be paid in 2012,which assumes RUB2.9/share or only 1.7% dividend yield. We estimate preferredshares to earn a 4% dividend yield in 2012.

LSE listing could create additional share overhang. The company is expected to

obtain LSE listing in February 2012 and we expect that some minority shareholders(e.g. Nafta Moskva) could decide to sell their shares, which could create additionalshare overhang risk.

Figure 29. Key metrics (RUBmn) Figure 30. Valuation

2011E 2012E 2013E 2014E

Revenues 292,108 320,568 325,219 342,938

EBITDA 114,738 126,283 119,534 124,913

EBIT 60,021 58,565 64,816 70,195

Net Income 38,841 37,177 41,911 45,985

Net Debt 135,639 121,263 98,625 74,663

EPS, RUB 12.67 12.13 13.67 15.00

CEPS, RUB 30.52 34.21 31.52 32.85

BVPS, RUB 82.18 91.46 102.34 114.18DPS, RUB 2.64 2.53 2.85 3.12

2011E 2012E 2013E 2014E

P/E 11.5 12.0 10.7 9.7

EV/EBITDA 5.1 4.5 4.6 4.2

EV/Sales 2.0 1.8 1.7 1.5

P/BV 1.8 1.6 1.4 1.3

EBITDA margin 39.3% 39.4% 36.8% 36.4%

Net margin 13.3% 11.6% 12.9% 13.4%

Revenue growth 6% 10% 1% 5%

EPS growth 24% -4% 13% 10% Div Yield 2% 2% 2% 2%

сизифов трудSources: Bloomberg, Otkritie Capital estimates Sources: Bloomberg, Otkritie Capital estimates

EQUITY | Russia

Telecom

1 February 2011

Research analysts

Alexander [email protected]+7 (495) 213 1830

8/3/2019 Rus Telecoms Report 2012 Otkritiye

http://slidepdf.com/reader/full/rus-telecoms-report-2012-otkritiye 19/26

VimpelCom | UPDATE | Russia | 1 February 2011

Otkritie Capital 19

Valuation

Figure 31. Rostelecom DCF Valuation

DCF 2011E 2012E 2013E 2014E 2015E 2016E 2017E 2018E 2019E

Revenue 292,108 320,568 325,219 342,938 358,172 373,136 388,284 405,088 423,802

EBITDA 114,738 126,283 119,534 124,913 128,903 132,990 137,791 144,136 151,847EBITDA Margin 39.3% 39.4% 36.8% 36.4% 36.0% 35.6% 35.5% 35.6% 35.8%

EBIT 60,021 58,565 64,816 70,195 74,185 78,272 83,073 89,418 97,129

EBIT Margin 20.5% 18.3% 19.9% 20.5% 20.7% 21.0% 21.4% 22.1% 22.9%

tax on EBIT (14,565) (14,211) (15,728) (17,033) (18,002) (18,993) (20,158) (21,698) (23,569)

depreciation 54,718 67,718 54,718 54,718 54,718 54,718 54,718 54,718 54,718

CAPEX+ Acquisitions (92,029) (83,348) (68,296) (68,588) (68,053) (67,164) (66,008) (68,865) (72,046)

Changes in WC (530) 3,684 4,030 3,011 2,841 2,724 2,494 2,362 2,375

FCF 7,615 32,408 39,539 42,303 45,690 49,556 54,118 55,935 58,606

discount factor 0.89 0.79 0.70 0.62 0.56 0.49 0.44 0.39

Discounted cash flow 28,809 31,245 29,716 28,531 27,508 26,704 24,536 22,852

RUBmn RUB/share

PV of CF unitl 2020 219,900 74.7PV of terminal value 222,131 75.5

Enterprise value 442,032 150.2

Less net debt (116,764) -39.7

Less minorities (11,870) -4.0

Add associates 30,848 10.5

Equity fair value 344,246 117.0

Current market cap 434,984 148

downside -20.9%

Sources: Otkritie Capital Estimates

Figure 32. Rostelecom peers comparison

P/E EV/EBITDA EV/SalesName 2011E 2012E 2013E 2011E 2012E 2013E 2011E 2012E 2013E

RTKM rx equity Rostelecom

Current multiples 11.8 11.7 10.9 5.1 4.5 4.6 2.0 1.8 1.7

vs EM Peers -23% -6% 1% -6% -12% -5% -1% -7% -8%

vs DM Peers 13% 18% 17% 5% -4% 0% 28% 16% 12%

vs MTS 6% 32% 46% 10% 6% 20% 7% 2% 8%

vs VimpelCom 53% 82% 89% 18% 21% 37% 17% 21% 28%

Sources: Otkritie Capital Estimates, Bloomberg

8/3/2019 Rus Telecoms Report 2012 Otkritiye

http://slidepdf.com/reader/full/rus-telecoms-report-2012-otkritiye 20/26

VimpelCom | UPDATE | Russia | 1 February 2011

Otkritie Capital 20

Appendix: Financial forecasts

Profitability

85,000

95,000

105,000

115,000

125,000

135,000

145,000

155,000

30%

32%

34%

36%

38%

40%

42%

44%

2008 2009 2010 2011E 2012E 2013E 2014E

EBITDA margin (LHS) EBITDA,RUBm

Cash flows, RUBm

(100,000)

(50,000)

0

50,000

100,000

150,000

2008 2009 2010 2011E 2012E 2013E 2014E

Operating cash flow Investing cash flow

Momentum, %

0.05

0%

5%

10%

15%

20%

25%

2008 2009 2010 2011E 2012E 2013E 2014E

Revenue g rowt h E PS g rowt h

Valuation

0

2

4

6

810

12

14

16

18

2008 2009 2010 2011E 2012E 2013E 2014E

P/E EV/EBITDA

RUBmn unless otherwise stated

2009 2010 2011E 2012E 2013E 2014E

Income Statement

Revenues 264,645 275,731 292,108 320,568 325,219 342,938

Depreciation 51,517 51,138 54,718 67,718 54,718 54,718EBITDA 101,570 101,419 114,738 126,283 119,534 124,913

Operating profit (EBIT) 50,053 50,281 60,021 58,565 64,816 70,195

Net Interest expense 13,389 9,033 12,572 12,572 12,572 12,572

Non-op. expenses - - - - - -

Pretax Profit 36,664 41,248 47,448 45,993 52,244 57,622

Taxes 8,074 10,041 12,445 11,912 13,429 14,734

Minority interest - - - - - -

Net Profit 26,263 31,338 38,841 37,177 41,911 45,985

Cash Flow Statement

Net Change in work. cap. (1,435) 2,393 (530) 3,684 4,030 3,011

Provisions and write-offs - - - - - -

Other - - - - - -

Operating cashflow 86,255 85,042 93,128 108,679 100,759 103,814

Capex (45,352) (51,845) (58,422) (83,348) (68,296) (68,588)

Disposals (Acquisitions) (1,816) (30,470) (33,607) 0 0 0

Investing cashflow (47,168) (82,315) (92,029) (83,348) (68,296) (68,588)

Equity - - - - - -Debt - - - - - -

Financing cashflow (35,985) (18,763) (428) (9,383) (8,765) (10,118)

Net Change in Cash 3,102 (16,036) 672 15,948 23,698 25,109

Balance sheet

Cash & equivalents 34,243 18,207 18,879 34,827 58,525 83,633

Current Assets 65,958 53,082 55,825 75,373 99,659 127,009

PP&E 293,497 301,068 338,379 354,009 367,587 381,457

Goodwill and other 5,831 4,531 4,531 4,531 4,531 4,531

Total Assets 404,752 435,253 434,773 429,976 427,231 424,839

Current Liabilities 90,165 95,509 96,192 99,970 102,517 105,273

S-T Debt 49,104 50,096 50,096 50,096 50,096 50,096

L-T Debt 67,092 87,941 87,941 87,941 87,941 87,941

Other L-T Liabilities - - - - - -

Shareholders Funds 217,411 213,107 251,948 280,411 313,750 350,072

Total Liabilities & Equity 403,180 426,811 466,865 502,043 539,908 581,127

Net Debt 97,531 136,027 135,639 121,263 98,625 74,663

Margins and profitability

EBIT Margin 18.9% 18.2% 20.5% 18.3% 19.9% 20.5%

EBITDA Margin 38.4% 36.8% 39.3% 39.4% 36.8% 36.4%

Net Margin 9.9% 11.4% 13.3% 11.6% 12.9% 13.4%

ROE 12.1% 14.7% 15.4% 13.3% 13.4% 13.1%

ROA 6.5% 7.2% 8.9% 8.6% 9.8% 10.8%

ROIC 14.3% 12.5% 15.0% 15.9% 19.5% 23.8%

Momentum

Revenue growth 2% 4% 6% 10% 1% 5%

EBITDA growth 14% -0% 13% 10% -5% 4%

EPS growth -3% 19% 24% -4% 13% 10%

Liquidity and solvency

Cash Ratio 0.4 0.2 0.2 0.3 0.6 0.8

Current Ratio 0.7 0.6 0.6 0.8 1.0 1.2

Interest Coverage 3.7 5.6 4.8 4.7 5.2 5.6

Debt/Equity 0.5 0.6 0.5 0.5 0.4 0.4

Debt/Total assets 0.3 0.3 0.3 0.3 0.3 0.3

Net debt / EBITDA 1.0 1.3 1.2 1.0 0.8 0.6

ValuationP/E 17.0 14.3 11.5 12.0 10.7 9.7

P/CE 5.7 5.4 4.8 4.3 4.6 4.4

P/BV 2.1 2.1 1.8 1.6 1.4 1.3

EV/Sales 2.1 2.1 2.0 1.8 1.7 1.5

EV/EBITDA 5.4 5.8 5.1 4.5 4.6 4.2

Dividend yield, (ords) - - 1.8% 1.7% 2.0% 2.1%

Dividend yield, (prefs) - 0.5% - - - -

Per Share Data

EPS - stock 1 8.57 10.22 12.67 12.13 13.67 15.00

DPS, ords - - 2.64 2.53 2.85 3.12

DPS, prefs - 0.43 - - - -

BVPS - stock 1 70.91 69.51 82.18 91.46 102.34 114.18

Source: Company data, Otkritie Capital estimates

8/3/2019 Rus Telecoms Report 2012 Otkritiye

http://slidepdf.com/reader/full/rus-telecoms-report-2012-otkritiye 21/26

Otkritie Capital 21

UPDATE

VimpelComGood prospects, but too many moving parts

BUYTicker VIP US

Target price, $ 14

Last price of common shares, $ 10.5

Upside 33%

Number of common shares, mn 1,628.2

Market cap, $mn 17,129

Net debt, $mn 22,103

EV, $mn 39,232

Free float 17%52-week min, $ 9.16

52-week max, $ 14.7

Sources: Bloomberg, Otkritie Capital estimates

Share price performance

65

70

7580

85

90

95

100

105

110

115

J a n - 1 1

F e b - 1 1

M a r - 1 1

A p r - 1 1

M a y - 1 1

J u n - 1 1

J u l - 1 1

A u g - 1 1

S e p - 1 1

O c t - 1 1

N o v - 1 1

D e c - 1 1

VimpelCom (Rebased) RTS (Rebased)

Sources: Bloomberg

We reiterate our BUY rating but decrease our target price forVimpelCom from $22 to $14/share. We see a long-term fundamentalupside in VimpelCom stock, though it lacks positive short-termcatalysts. Although we like the new strategy, which is focused onbalanced growth and improved efficiency, ongoing uncertaintyregarding the fate of the shareholder agreement and Djezzynationalization price could limit growth opportunities for now.VimpelCom is expected to remain a high dividend payer (with adividend yield of 7.5%) as the company is not planning fast

deleveraging in 2012. The stock is cheap trading on 27% discountto EM peers.

We expect the top-line to grow by 4.5% in 2012, while the EBITDA marginshould go up to 42%. We expect some margins improvement in Russia operations,mainly on the back of decreasing selling expenses. Most of the top-line growth isexpected to come from Asia, Africa and CIS.

Dispute between Altimo and Telenor likely to continue in 2012 after the recentacquisition of a 6% voting stake in VimpelCom from Oleg Kiselev by EastOne, whichis an investment fund of Viktor Pinchuk. Because EastOne is an independentinvestment company, the announcement increases Altimo‘s chances of prevailing inits court case against Telenor. Altimo currently holds less than 25% of VimpelCom'svoting rights, which effectively means that the VimpelCom shareholder agreementshould be terminated if Telenor cannot prove direct links between Altimo andEastOne. After termination of the agreement Altimo will likely initiate elections for anew VimpelCom Board of Directors, which could be done in 6 months after thetermination of the shareholders agreement. A new Board of Directors would mostlikely comprise 3 members each from Altimo, Telenor, and Weather Investments, aswell as 3 independent directors (one of who would probably represent EastOne). Thenew BoD combination implies that Altimo and Weather could jointly have 7 places outof 12 in the BoD, which could make their life easier to push any further M&A dealthrough.

Djezzy valuation would be the key stock driver in 1H12. VimpelCom has enteredinto a non-binding memorandum regarding the possible sale to the Algerian State ofa majority stake in its subsidiary Orascom Telecom Algerie (OTA), which operatesunder the Djezzy brand. Following signing of the memorandum, the Algerian Ministryof Finance and VimpelCom will undertake a process to agree on the valuation ofDjezzy. We expect OTA (Djezzy) valuation range to be announced in Spring 2012,which would be followed by the final price negotiation period, therefore we expect thedeal to be closed in late 2012. As a result of the transaction VimpelCom will continueto consolidate OTA in its financial results, but we think the sale could l imit OTA‘sability to upstream dividends to VimpelCom, which could have a negative effect onthe dividend yield after 2012.

Dividend yield for 2012 likely to exceed 7.5%. The management guides for anannual dividend of $0.8/ADR for 2011-2014, which translates into a 7.5% dividendyield. The interim dividend for 2011 is expected to be announced in 2Q12.

Figure 33. Key metrics ($mn) Figure 34. Valuation

2011E 2012E 2013E 2014E

Revenues 22,996 24,022 25,351 26,860

EBITDA 9,437 10,098 10,657 11,426

EBIT 4,773 5,346 5,768 6,380

Net Income 2,042 2,534 2,950 3,553

Net Debt 23,700 22,103 19,868 16,593

EPS, $ 1.25 1.56 1.81 2.18

CEPS, $ 4.12 4.48 4.81 5.28

BVPS, $ 7.11 7.86 8.73 10.19

DPS, $ 0.82 0.93 0.72 0.76

2011E 2012E 2013E 2014E

P/E 8.4 6.8 5.8 4.8

EV/EBITDA 4.3 3.9 3.5 3.0

EV/Sales 1.8 1.6 1.5 1.3

P/BV 1.5 1.3 1.2 1.0

EBITDA margin 41.0% 42.0% 42.0% 42.5%

Net margin 8.9% 10.5% 11.6% 13.2%

Revenue growth 119% 4% 6% 6%

EPS growth -7% 24% 16% 20%

Div Yield 8% 9% 7% 7%

Sources: Bloomberg, Otkritie Capital estimates Sources: Bloomberg, Otkritie Capital estimates

EQUITY | Russia

Telecom

1 February 2011

Research analysts

Alexander [email protected]+7 (495) 213 1830

8/3/2019 Rus Telecoms Report 2012 Otkritiye

http://slidepdf.com/reader/full/rus-telecoms-report-2012-otkritiye 22/26

VimpelCom | UPDATE | Russia | 1 February 2011

Otkritie Capital 22

Valuation

Figure 35. VimpelCom DCF Valuation

2011E 2012E 2013E 2014E 2015E 2016E 2017E 2018E 2019E

Revenue 22,996 24,022 25,351 26,860 28,370 29,706 30,980 32,289 33,429

EBITDA 9,437 10,098 10,657 11,426 12,068 12,785 13,333 13,897 14,387EBITDA Margin 41.0% 42.0% 42.0% 42.5% 42.5% 43.0% 43.0% 43.0% 43.0%

EBIT 4,773 5,346 5,768 6,380 6,881 7,502 7,979 8,477 8,944

EBIT Margin 20.8% 22.3% 22.8% 23.8% 24.3% 25.3% 25.8% 26.3% 26.8%

Unlevered PBT 4,773 5,346 5,768 6,380 6,881 7,502 7,979 8,477 8,944

Tax Rate effective cash basis 28% 28% 28% 28% 28% 28%

Unlevered Tax -1,336 -1,497 -1,615 -1,787 -1,927 -2,101 -2,234 -2,374 -2,504

Investment CF -5,769 -4,374 -4,056 -4,029 -4,255 -4,456 -4,647 -4,843 -5,014

(Capex)/Sales 25.1% 18.2% 16.0% 15.0% 15.0% 15.0% 15.0% 15.0% 15.0%

Other Cash Adj. (inc. Working Capital) -265 40 -74 -23 -34 -66

Unlevered, Adj. Free Cash Flow 5,346 5,926 6,154 6,429 6,646 6,802

Discount Factor 0.00 0.89 0.79 0.70 0.62 0.55 0.43 0.30 0.19

Present Value of FCF 0 3,582 3,782 3,728 3,665 3,376 2,773 2,000 1,266

$mn $/share

Value of Cash Flows 24,172 14.85

Value from Perpetuity 23,053 14.16

Adjustments -24,472 -15.03

Implied Equity Value 22,754 14.0

Adjsted MCAp 17,129 10.5

Upside 32.8%

ources: Otkritie Capital estimates, Bloomberg

Figure 36. VimpelCom peers comparison

P/E EV/EBITDA EV/Sales

Name 2011E 2012E 2013E 2011E 2012E 2013E 2011E 2012E 2013E

VIP US Equity VimpelCom

Current multiples 7.7 6.4 5.8 4.3 3.7 3.4 1.7 1.5 1.3

vs EM Peers -50% -48% -47% -20% -27% -31% -16% -23% -28%

vs DM Peers -26% -35% -38% -11% -21% -27% 9% -4% -12%

vs MTS -30% -28% -23% -6% -13% -12% -8% -16% -16%

vs Rostelecom -35% -45% -47% -15% -18% -27% -14% -17% -22%

Sources: Otkritie Capital estimates, Bloomberg

8/3/2019 Rus Telecoms Report 2012 Otkritiye

http://slidepdf.com/reader/full/rus-telecoms-report-2012-otkritiye 23/26

VimpelCom | UPDATE | Russia | 1 February 2011

Otkritie Capital 23

Appendix: Financial forecasts

Profitability

4,000

5,000

6,000

7,000

8,000

9,000

10,000

11,00012,000

13,000

36%

38%

40%

42%

44%

46%

48%

50%52%

54%

2008 2009 2010 2011E 2012E 2013E 2014E

EBITDA margin (LHS) EBITDA,$m

Cash flows, $m

(10,000)

(8,000)

(6,000)

(4,000)

(2,000)

0

2,000

4,000

6,000

8,000

10,000

2008 2009 2010 2011E 2012E 2013E 2014E

Operating cash flow Investing cash flow

Momentum, %

0.8

0.6

0.4

0.2

0%

20%

40%

60%

80%

100%

120%

2008 2009 2010 2011E 2012E 2013E 2014E

Revenue g rowt h E PS g rowt h

Valuation

0

5

10

15

20

25

2008 2009 2010 2011E 2012E 2013E 2014E

P/E EV/EBITDA

$mn unless otherwise stated

2009 2010 2011E 2012E 2013E 2014E

Income Statement

Revenues 8,711 10,513 22,996 24,022 25,351 26,860

Depreciation 1,694 2,080 4,664 4,752 4,888 5,045EBITDA 4,273 4,932 9,437 10,098 10,657 11,426

Operating profit (EBIT) 2,578 2,852 4,773 5,346 5,768 6,380

Net Interest expense 547 484 1,659 1,549 1,394 1,168

Non-op. expenses 479 (42) 0 0 0 0

Pretax Profit 1,552 2,410 3,114 3,797 4,374 5,213

Taxes 435 606 872 1,063 1,225 1,460

Minority interest (4) 48 200 200 200 200

Net Profit 1,122 1,757 2,042 2,534 2,950 3,553

Cash Flow Statement

Net Change in work. cap. (332) 1,700 2,462 (189) (176) (265)

Provisions and write-offs (345) (31) 0 0 0 0

Other - - - - - -

Operating cashflow 2,135 5,553 9,368 7,298 7,862 8,534

Capex (892) (1,757) (4,369) (4,324) (4,056) (4,029)

Disposals (Acquisitions) (542) 410 (1,400) (50) (50) (50)

Investing cashflow (1,433) (1,347) (5,769) (4,374) (4,106) (4,079)

Equity (1,272) 368 6,162 912 1,207 1,429Debt (1,857) (1,692) 18,339 (1,597) (2,235) (3,275)

Financing cashflow (3,129) (1,323) 24,501 (684) (1,028) (1,846)

Net Change in Cash (2,427) 2,882 28,100 2,240 2,727 2,609

Balance sheet

Cash & equivalents 1,447 885 300 300 300 300

Current Assets 1,520 1,440 3,449 3,603 4,056 4,566

PP&E 4,121 10,599 12,928 12,550 11,767 10,801

Goodwill and other 4,361 7,004 7,004 7,004 7,004 7,004

Total Assets 14,733 19,928 23,681 23,457 23,127 22,671

Current Liabilities 1,601 3,222 7,693 7,658 7,935 8,180

S-T Debt 0 0 0 0 0 0

L-T Debt 7,353 5,661 24,000 22,403 20,168 16,893

Other L-T Liabilities 509 522 722 922 1,122 1,322

Shareholders Funds 4,509 10,671 11,583 12,790 14,219 16,592

Total L iabilities & Equity 14,733 20,076 43,998 43,773 43,444 42,988

Net Debt 5,906 4,776 23,700 22,103 19,868 16,593

Margins and profitability

EBIT Margin 29.6% 27.1% 20.8% 22.3% 22.8% 23.8%

EBITDA Margin 49.0% 46.9% 41.0% 42.0% 42.0% 42.5%

Net Margin 12.9% 16.7% 8.9% 10.5% 11.6% 13.2%

ROE 24.9% 16.5% 17.6% 19.8% 20.7% 21.4%

ROA 7.6% 8.8% 8.6% 10.8% 12.8% 15.7%

ROIC 17.7% 14.4% 24.3% 27.6% 31.0% 36.0%

Momentum

Revenue growth -14% 21% 119% 4% 6% 6%

EBITDA growth -3% 15% 91% 7% 6% 7%

EPS growth 114% 23% -7% 24% 16% 20%

Liquidity and solvency

Cash Ratio 0.9 0.3 0.0 0.0 0.0 0.0

Current Ratio 0.9 0.4 0.4 0.5 0.5 0.6

Interest Coverage 4.7 5.9 2.9 3.5 4.1 5.5

Debt/Equity 1.6 0.5 2.1 1.8 1.4 1.0

Debt/Total assets 0.5 0.3 1.0 1.0 0.9 0.7

Net debt / EBITDA 1.4 1.0 2.5 2.2 1.9 1.5

ValuationP/E 9.6 7.8 8.4 6.8 5.8 4.8

P/CE 3.8 3.6 2.6 2.4 2.2 2.0

P/BV 2.4 1.3 1.5 1.3 1.2 1.0

EV/Sales 2.6 2.1 1.8 1.6 1.5 1.3

EV/EBITDA 5.4 4.4 4.3 3.9 3.5 3.0

Dividend yield, (ords) 5.2% 8.2% 7.7% 8.9% 6.9% 7.3%

Dividend yield, (prefs) - - - - - -

Per Share Data

EPS - stock 1 1.09 1.35 1.25 1.56 1.81 2.18

DPS, ords 0.55 0.87 0.82 0.93 0.72 0.76

DPS, prefs - - - - - -

BVPS - stock 1 4.40 8.19 7.11 7.86 8.73 10.19

Source: Company data, Otkritie Capital estimates

8/3/2019 Rus Telecoms Report 2012 Otkritiye

http://slidepdf.com/reader/full/rus-telecoms-report-2012-otkritiye 24/26

Russian telecoms 2012 | UPDATE | Russia | 1 February 2011

Otkritie Capital 24

Disclosures appendix