Running a home - P4I · Introduction to running a home 5 1. ... PowerPoint or smart-board...

102

MONEY MANAGEMENT RUNNING A HOME Hannah Kovacs & Jayne Garner

Transcript of Running a home - P4I · Introduction to running a home 5 1. ... PowerPoint or smart-board...

MONEY MANAGEMENTRUNNING A HOME

Hannah Kovacs & Jayne Garner

Copyright © Axis Education 2007

The worksheets may be produced for use at one site within the purchasing institution foreducational use only without permission from the Publisher, providing that the work has beenpaid for.

Otherwise, no part of this publication may be photocopied, recorded, or otherwise reproduced,stored in a retrieval system or transmitted in any form or by any electronic or mechanical meanswithout prior permission of the copyright owner.

Work sent on approval or inspection and not yet paid for may not be copied under anycircumstances.

ISBN 978-1-84618-113-9

Axis Education

PO Box 459

Shrewsbury SY4 4WZ

Email: [email protected]

www.axiseducation.co.uk

First published 2007

Contents

3

Money m

anagem

ent

nC

redit a

nd loans

Introduction and guidelines for use 4

Section 1. Introduction to running ahome 5

1. How do you run your home? 8

2. Now and then 10

3. Household expenditure 12

4. Running a home 14

Section 2. Paying for where you live 15

1. Renting a home 19

2. A place to rent 21

3. Deposits on rented homes 23

4. Council housing 25

5. Getting on the property ladder 27

6. How much can I borrow? 28

7. Shared ownership 30

8. Shared ownership – how much will it cost? 32

Section 3. Insurance 34

1. Types of insurance 37

2. Why do you need building and contents insurance? 38

3. The cost of insurance 40

4. Home contents insurance 43

5 That’s why you need it 45

Section 4. Bills, bills, bills 46

1. Reading meters 51

2. Comparing your meter and your bill 53

3. The cost of power 54

4. Paying bills – different ways 56

5. Why use direct debit? 58

6. Choosing a supplier 59

7. Monthly outgoings 61

8. When to pay the bills 62

9. How to read a water meter 64

10. How much water? 66

11. Council tax 68

12. Where does your money go? 70

13. TV licence 72

14. Identifying luxury bills 73

Section 5. Other costs around the home 74

1. Standby 77

2. Dishwasher versus washing up 79

3. Professional versus DIY 80

4. Contingency 82

Section 6. Green household 84

1. Being a green householder 86

2. Going green 88

3. Household recycling 89

4. Recycling facts 91

Bank of puzzles 93

Bank of puzzles answers 99

Glossary 100

Money m

anagem

ent

nR

unnin

g a

hom

e n

Teacher’s n

ote

s

n

4

The other books in the series are

• Banking

• Credit and loans

• Dealing with debt

• Planning for the future

• Post-16 options

• Smart consumer

• Taxation and wages

Running a home contains a variety of exercises,covering a range of topics relating to relevantaspects of running a home efficiently. A full list ofthese is contained in the contents.

The purpose of Running a home is to give yourstudents the practical skills they need forsuccessfully taking care of their personal homefinances. The exercises in this title give your studentshelpful advice and tips on managing householdbills, rent, mortgages and insurance. Your studentswill learn to use maths skills to work out how tosave both money and energy. Maths activities suchas reading gauges, averages, handling data, money,percentages, ratio and rounding are featured.

You will find that Running a home contains activitiesappropriate for adult students working at EntryLevel 3/Level 1 as well as school students,principally at Key Stage 4. As well as learning theskills outlined in the aims of the exercises, yourstudents should also develop communication skillsand the ability to work co-operatively with others.

Each exercise has a set of Teachers' Notes providingspecific guidance for how they could best be used.The following general guidelines apply to all of theexercises.

• You should always explain the aims of the exercise to your students

• It will probably be useful to begin each exercise with a brief whole-class discussion to establish the aims and an understanding of the relevance of the work

• You can allow less able students to work in pairs or in small, suitably selected groups

• One of the most important basic skills is readingand all students should be encouraged and helped to read the worksheets. The language level in this book has been designed to extend your students as well as to equip them with the types and levels of communication they will meetwhen they work on running an efficient home. Less able students might need help with reading some sections but you should point out that over-simplified language would be inappropriate and patronising.

• The bank of puzzles at the back of Running a home provides your students with additional practice with the more technical vocabulary used in this title.

Several of the exercises in this title containmathematical calculations relating to home financeissues. You may find that less able students needhelp in completing some of them. Further guidancecan be found in the specific Teachers’ Notes. Theteaching notes also contain suggestions forextension activities, several of which involve accessto the internet.

Each section has been designed to provide sufficientmaterial for at least a one-hour lesson. Most aresuitable for completion for between two and fourlessons. The time taken on the various activitieswithin the sections will depend on the needs andabilities of the students but as a general rule, nosingle activity should last for longer than twentyminutes.

Introduction and guidelines for use

This is one of a set of eight titles aimed at developingimportant financial capability skills.

Money m

anagem

ent

nR

unnin

g a

hom

e n

Teacher’s n

ote

s

n

5

Aims

• To help students self-evaluate how well they run a home.

• To raise students’ awareness of how households spend their money and how this has changed over time.

Preparation andResources

For this section you will need to distribute a copy ofeach of the following worksheets to each member ofthe group:

• How do you run your home?

• Now and then

• Household expenditure

• Running a home

Alternatively, the worksheets could be made intooverhead transparencies or incorporated into aPowerPoint or smart-board presentation.

Teaching Suggestions

After your students have completed ‘How do yourun your home?’ you should hold a short discussioninvolving the whole group. You might need toexplain the meaning and importance of some terms.You could introduce them to the glossary on pages100–102 to focus your discussion.

The data in ‘Now and then’ may be a surprise forsome students. You could go on to discuss thepossible reasons for changes in the relativeproportion of income spent on different things. Forexample, the decrease in the amount people spendon alcohol is due to better health education andawareness campaigns.

‘Household expenditure’ requires students to extractdata from a table about the relative expenditure ofdifferent types of households.

‘Running a home’ requires students to compile a listof monthly household expenses.

Extension work

1. Using the information covered in this section, divide your students into two groups. The first group should research and discuss the pros of running a home efficiently and the second groupshould research and discuss the cons of running a home efficiently. You should then bring the twogroups together and hold a discussion with the first group arguing for efficiency and the secondgroup arguing against.

2. To help your students become more familiar withsome of the technical terms used in this section, ask them to complete the wordsearch on page 93.

3. Ask your students to choose four words from theglossary for section 1 on page 100 and write a sentence for each word putting the word in an appropriate context. This will show that they have an understanding of the terms.

4. You can extend ‘Now and then’ with a discussionabout why spending on alcohol and smoking hasdecreased – due to more health warnings about these activities. You could also ask students why there has been an increase in communication costs – due to more mobile phones/internet use.

5. A good extension activity after ‘Household expenditure’ would be to ask students to conduct a piece of research with similar households to those in the table to see if their findings differ from these national findings.

1. Introduction to running a home

This section will help raise your students’ awarenessof the need to run a home efficiently.

6

Money m

anagem

ent

nR

unnin

g a

hom

e n

Teacher’s n

ote

s

Answers and Mapping

How do you run your home?, pages 8–9

There are no definitive answers but hopefullystudents will begin to identify the best ways to runtheir homes.

NCPSHEKS3 – 1a, 1g; KS4 – 1a, 1e

Key skillsC1.2.1

Adult core curriculaRt/E3.8

Now and then, pages 10–11

1. 21%

2. 12%

3. 100%

4. 3/7

5. Communication

6. 3/7

7. Transport

8. 1/3

NCMathsKS3 – Ma2.1d, Ma2.3a, Ma2.3c, Ma2.3m, Ma2.4b,Ma4.1cKS4 – Ma2.1d, Ma2.3a, Ma2.3c, Ma2.3m, Ma2.4b,Ma4.1c

PSHEKS3 – 1g, KS4 – 1e

Key skillsN1.1.1, N1.1.2, N1.2.1, N1.2.2, N1.3.3

Adult core curriculaN1.L1.1, N1/L1.3, N2/L2.3, MSS1/E3.1, HD1/E3.1,HD1/L1.2

Household expenditure, pages 12–13

1.

2. £16.60

3. Transport

4. Alcohol and tobacco

5. Education

6. 15.8%

7. 22.5%

8. 4.8%

NCMathsKS3 – Ma2.1d, Ma2.3a, Ma2.3m, Ma2.4b, Ma4.1cKS4 – Ma2.1d, Ma2.3a, Ma2.3m, Ma2.4b, Ma4.1c

PSHEKS3 – 1g, KS4 – 1e

Key skillsN1.1.1, N1.1.2, N1.2.1, N1.2.2, N1.3.3

Adult core curriculaN1.L1.1, N1/L1.3, MSS1/E3.1, HD1/E3.1, HD1/L1.2

1. Introduction to running a home

Spending type Couple with children Couple withoutchildren

Food and non-alcoholic drink

£62.80 £46.20

Alcohol and tobacco £13.00 £13.90

Clothing andfootwear

£33.60 £24.50

Transport £85.60 £77.80

Communication £15.10 £12.70

Recreation andculture

£79.00 £68.10

Education £14.30 £3.90

Restaurants andhotels

£47.20 £45.50

Total £350.60 £292.60

7

Money m

anagem

ent

nR

unnin

g a

hom

e n

Teacher’s n

ote

s

Running a home, page 14

NCPSHEKS3 – 1a, 1g; KS4 – 1a, 1e

Key skillsC1.2.1

Adult core curriculaRt/E3.8

1. Introduction to running a home

Household expenses phone, gas and electricity, broadband, TVlicence, insurance, food, laundry, cleaningproducts

Transport running a car, taking public transport, taxis

Savings pension, investments

Debts credit cards, loans, overdrafts

Work union fees, subscriptions, transport, lunch

Educationstudent loan repayments, evening classes,books, stationery

Luxuries cigarettes, alcohol, magazine

Healthcare prescriptions, optician, dentist, medicines

Entertainmentdrinking, eating out, clubbing, cinema, CDs,DVDs

Sport and fitness gym membership, team membership, sportsequipment

One-off expenses presents, holidays, having to buy new thingsfor the house e.g. new cooker etc

Money m

anagem

ent

nR

unnin

g a

hom

e

8

If you are good at planning and organising things you should be able to run a homewell. This in turn could save you some serious money. Knowing that you are beingcharged the least amount possible for household bills, that you’re paying a keenprice for insurance and that your house is as energy efficient as possible will all saveyou money.

Find out how good you are at running a home by answering the questions inthis quiz.

1. When it comes to utility bills you:

a) have a quick check once a year to make sure you’re getting the best deal

b) haven’t even got a clue how much you pay for each bill

c) check every month to see if you could be paying less

2. When it comes to paying your bills you:

a) usually wait for the bill to arrive in the post and then pay by cheque

b) only pay up once you’ve had a reminder

c) always choose direct debit – it’s the cheapest way to pay

3. When it comes to recycling you:

a) sometimes take glass to the bottle bank

b) recycling… what’s that?

c) sort out all your rubbish – anything that can be recycled, is

4. Council tax is money used to:

a) keep the buses running

b) pay councillors’ wages

c) fund a number of services such as the police, recycling and rubbish collection

5. If money is tight you:

a) just stop paying your bills

b) borrow money from a mate

c) identify your luxury bills and get rid of them

1. How do you run your home?

Money m

anagem

ent

nR

unnin

g a

hom

e

9

6. If something goes wrong in the house you:

a) have no cash reserves so you wouldn’t know what to do

b) would borrow money from friends or family

c) have some money put aside for such emergencies

7. As far as you’re concerned, Sky TV is classed as:

a) essential, you would NEVER get rid of it, no matter how tight money was

b) something you could live without – just about

c) a luxury that you could easily do without if you were struggling to pay the bills

8. When it comes to insurance you know that:

a) it costs a bomb

b) it doesn’t come cheap, but at least you know you are covered in an emergency

c) it’s essential to have the right cover for all the things you own

Now work out your score.

If you got mostly a):

It looks like you need some major help in running your home. All of the worksheets in thisbook will help you learn how to be more efficient, not just with money, but with energyand recycling too.

If you got mostly b):

You’re not doing badly, but you could do better. There are many savings to be madearound the home and you could be missing out. Read on to find out how you could berunning your home more efficiently.

If you got mostly c):

Congratulations! It looks like your home is run pretty smoothly! However, there areprobably a few hints and tips that you could put to good use, so carry on reading!

1. How do you run your home?

Money m

anagem

ent

nR

unnin

g a

hom

e

10

Spending patterns have changed dramatically over the past 30 years or so. Mosthouseholds now have a much higher income, which means that they have a greaterproportion of money to spend on luxury items. Other changes in society, such as theintroduction of mobile phones and the internet, have also affected what householdsspend their money on.

This graph shows the percentage of household expenditure spent on different goodsand services between 1971 and 2005.

Use the graph to answer the questions on page 11.

1. Now and then

0

5

10

15

20

25

1971

21%

12%

12%

12%

12%

12%

12%

11%12

%

1%2% 2% 2% 2%

15%

15%

15%

15%

9% 9% 9%7%

6%

10%

6% 6%

10% 11

%

11%

17%

7% 7% 7%6%

5%4% 4%

6% 6% 6%

Food

& n

on-a

lcoh

olic

dri

nk

Tran

spor

t

Com

mun

icat

ion

Recr

eatio

n &

cul

ture

Hou

seho

ld g

oods

& s

ervi

ces

Alc

ohol

& t

obac

co

Clo

thin

g &

foo

twea

r

Rest

aura

nts

& h

otel

s

1981

1991

2001

2005

Graph to show percentage of household expenditure

Money m

anagem

ent

nR

unnin

g a

hom

e

11

1. In 1971, what percentage of household expenditure was spent on food and non-alcoholicdrink?

2. In 2005, what percentage of household expenditure was spent on recreation and culture?

3. By what percentage did expenditure on communication increase between 1971 and 2005?

4. By what fraction did spending on alcohol and tobacco decrease between 1971 and 2005?

5. Which category had the least amount spent on itin 1981?

6. By what fraction has expenditure on food and non-alcoholic drink decreased from 1971 to 2005?

7. In 2005, which category shows the biggest expenditure?

8. By what fraction did expenditure increase on recreation and culture between 1971 and 2005?

1. Now and then

Money m

anagem

ent

nR

unnin

g a

hom

e

12

Not only is the way we spend our household money affected by time, but also by thetype of household we live in. Obviously people with children are likely to spend moremoney than people who don’t have children, but do they spend their money on thesame types of things?

This table shows the weekly household expenditure in pounds on various differentthings, from food to transport. The table shows how much couples with childrenspent and how much couples without children spent in 2005/06.

1. Household expenditure

Spending type Couple with children Couple without children

Food and non-alcoholic drink £62.80 £46.20

Alcohol and tobacco £13.00 £13.90

Clothing and footwear £33.60 £24.50

Transport £85.60 £77.80

Communication £15.10 £12.70

Recreation and culture £79.00 £68.10

Education £14.30 £3.90

Restaurants and hotels £47.20 £45.50

Total

Money m

anagem

ent

nR

unnin

g a

hom

e

13

Use the information in the table to answer the questions.

1. Work out the total spending per week for coupleswith children and couples without and put your answers in the table on page 12.

2. How much more money did couples with childrenspend on food and non-alcoholic drink per week compared to couples without children?

3. What did couples without children spend most oftheir money on?

4. What did couples with children spend the least amount of their money on?

5. What did couples without children spend the least amount of money on?

6. Express the amount of money that couples without children spent on food and non-alcoholicdrink as a percentage of their total weeklyexpenditure.

7. Express the amount of money that couples with children spent on recreation and culture as a percentage of their total weekly expenditure.

8. Express the amount of money that couples without children spent on alcohol and tobacco asa percentage of their weekly expenditure.

1. Household expenditure

Money m

anagem

ent

nR

unnin

g a

hom

e

14

Nowadays there are a lot of expenses that we pay every month to keep a householdticking over and sometimes to make our lives a little easier. These can be anythingfrom running water, to those little luxuries like a DVD on a Friday night!

Fill in the table under each heading with as many expenses as you can think ofthat you may pay each month.

1. Running a home

Household expenses

Transport

Savings

Debts

Work

Education

Luxuries

Healthcare

Entertainment

Sport and fitness

One-off expenses

Money m

anagem

ent

nR

unnin

g a

hom

e n

Teacher’s n

ote

s

n

15

Aims

• To help students calculate rent.

• To give students the information they need to know about rent deposits.

• To give students tools and tips for getting on the property ladder and to work out costs.

Preparation andResources

For this section you will need to distribute a copy ofeach of the following worksheets to each member ofthe group:

• Renting a home

• A place to rent

• Deposits on rented homes

• Council housing

• Getting on the property ladder

• How much can I borrow?

• Shared ownership

• Shared ownership – how much will it cost?

Alternatively, the worksheets could be made intooverhead transparencies or incorporated into aPowerPoint or smart-board presentation.

Access to the internet will be useful for the extensionactivities on ‘How much can I borrow?’.

Teaching Suggestions

‘Renting a home’ helps students to understandabbreviations in adverts for homes to rent.Depending on the needs of your students you mayfind it useful to work through a couple of theabbreviations first as a class activity.

‘A place to rent’ gives students the sums they needto make accurate comparisons between rentpayable weekly and rent payable monthly. It would

be useful to work through two examples of your ownbefore asking students to answer the questions.

‘Deposits on rented homes’ is a numeracy activitydesigned to help students work out how muchdeposit landlords want from their tenants. Theinformation on this page reflects recent changes inthe law.

‘Council housing’ is a numeracy activity wherestudents compare rents of different sized councilproperties.

‘Getting on the property ladder’ is a comprehensionexercise about why getting a first home is becomingincreasingly difficult.

‘How much can I borrow?’ is a numeracy activitywhere students calculate the maximum amount amortgage lender is likely to offer different peopleaccording to their incomes.

‘Shared ownership’ requires students to calculatemortgages for shared ownership housing.

‘Shared ownership – how much will it cost?’requires students to work out monthly payments forshared ownership housing including mortgage andrent.

Extension work

1. To help your students become more familiar withsome of the more difficult terms used in this section, ask them to complete the crossword on page 94.

2. Ask your students to choose four words from theglossary for section 2 on page 100 and write a sentence for each word putting the word in an appropriate context. This will show that they have an understanding of the terms.

3. You could extend ‘Renting a home’, ‘A place to rent’ and ‘Deposits on rented homes’ with similar activities using adverts from your local newspaper.

4. Follow up ‘Council housing’ by asking students to find out the costs of different sized council

2. Paying for where you live

This section will teach your students the skills theyneed to calculate rent. They will also learn about waysof getting on the property ladder.

16

Money m

anagem

ent

nR

unnin

g a

hom

e n

Teacher’s n

ote

s

properties in their local area. They can present their findings in a bar chart.

5. Follow up ‘How much can I borrow?’ by asking students to calculate the highest price home a set of people can afford, bearing in mind the amount of deposit they can afford. For example:

a) Debbie and Mark have £10,000 for a deposit.

b) Charlie has £3,000 for a deposit.

c) Will and April have £8,000 for a deposit.

d) Misha has £2,000 for a deposit.

e) Jade and Katie have £4,000 for a deposit.

f) Barclay has no deposit.

g) Aidan and Becca have £2,500 for a deposit.

You should remind students that there will beadditional fees when buying a home – they could dosome research to find out what these are and howmuch they are likely to be.

6. You could follow up the shared ownership worksheets with similar activities using different proportions of shared ownership: 60:40, 70:30, 75:25 and so on.

Answers and mapping

Renting a home, pages 19–20

1. avail ‚ available

gch ‚ gas central heating

d/g ‚ double glazing

immed ‚ immediately

ff ‚ fully furnished

pcm ‚ per calendar month

gge ‚ garage

pw ‚ per week

n/s ‚ non smoker

inc ‚ including bills

unfurn. ‚ unfurnished

p/f ‚ part furnished

ref ‚ reference needed

ch ‚ central heating

2a) Baker Road. One bed ground floor flat. D/g, ff, with gge. With kitchen/dining room and showerin bathroom. Avail for 6 month let. N/s and strictly no pets. £540 pcm.

Double glazing, fully furnished, garage, available, no smoking, per calendar month

2b) Russell Crescent. Two bed house with gge. Includes entrance hall, fitted kitchen and garden. Avail immed. Has d/g and gch. Refneeded. £307 pw.

Garage, available, immediately, double glazing,gas central heating, reference, per week

Framework for teaching EnglishYear 7 – W14, R1, R2, R6; Year 8 – W7c, R4; Year 9 – R1

Adult core curriculaRt/E3.1, Rt/E3.7, Rt/E3.8, Rw/E3.2, Rw/E3.2

A place to rent, pages 21–22

1. £115.38 per week

2. £650 per month

3. £380.77 per week

4. £182.31 per week

5. £541.67 per month

6. £121.15 per week

7. £144.23 per week

8. £476.67 per month

9. Orpwood Road

10. Hatchford Road

11. Hall Street

12. St David’s Street

NCMathsKS3 – Ma2.1d, Ma2.3a, Ma2.4b

2. Paying for where you live

17

Money m

anagem

ent

nR

unnin

g a

hom

e n

Teacher’s n

ote

s

KS4 – Ma2.1d, Ma2.3a, Ma2.4b

Adult core curriculaN2/L1.5; MSS1/L1.1

Deposits on rented homes, pages 23–24

1. £1,093.85

2. £750

3. £2,284.62

4. £576.92

5. £500

6. £692.31

7. Paradise Street works out the cheapest at £1041.67

8. St David’s Street works out the most expensive at£3,934.62

NCMathsKS3 – Ma2.1d, Ma2.2e, Ma2.3a, Ma2.4bKS4 – Ma2.1d, Ma2.2e, Ma2.3a, Ma2.4b

Adult core curriculaN1/E3.2, N1/E3.4, N2/L1.9; MSS1/L1.1

Council housing, pages 25–26

1. £2,392.52

2. £248.65

3. £2,020.72

4. £1,716.52

5. £227.11

6. £2,983.76

7. £168.39

8. £2,725.32

NCMathsKS3 – Ma2.1d, Ma2.2e, Ma2.3a, Ma2.4bKS4 – Ma2.1d, Ma2.2e, Ma2.3a, Ma2.4b

Adult core curriculaN1/E3.2, N1/E3.4, N2/L1.9; MSS1/L1.1

Getting on the property ladder, page 27

1. People are finding it difficult to get on the property ladder because there is a widening gapbetween the cost of houses and income.

2. Having a financial history with a mortgage lender can help you borrow money in the future because, as long as you always make your repayments, it shows other lenders that you are reliable.

3. Other advantages to owning your own home could include:

• It is a nest egg for the future.

• Owning gives you security because you can live in the house for as long as you want.

• Owning your own house gives you the freedom to decorate or restorate to your heart’s content.

EnglishEn2.1a, En2.4a

Framework for teaching EnglishYear 7 – W14, R1, R2; Year 8 – W7c, R1; Year 9 – R1

PSHEKS3 – 1g; KS4 – 1e

Key skills C1.2.1

Adult core curriculaRt/E3.1, Rt/E3.4, Rt/E3.5, Rt/E3.8, Wt/E2.1,Ww/E3.3

How much can I borrow?, pages 28–29

1. £120,000

2. £105,000

3. £57,000

2. Paying for where you live

18

Money m

anagem

ent

nR

unnin

g a

hom

e n

Teacher’s n

ote

s

4. £110,000

5. £72,000

6. £75,000

7. £111,000

8. £90,000

9. £120,000

10. £72,500

NCMathsKS3 – Ma2.1d, Ma2.2e, Ma2.3a, Ma2.3m, Ma2.4bKS4 – Ma2.1d, Ma2.2e, Ma2.3a, Ma2.3m, Ma2.4b

Adult core curriculaN2/L1.9; MSS1/L1.1

Shared ownership, pages 30–31

1. Mortgage needed: £60,750

2. Mortgage needed: £68,750

3. Mortgage needed: £83,750

4. Mortgage needed: £73,750

5. Mortgage needed: £35,000

6. Mortgage needed: £90,000

7. Mortgage needed: £115,000

8. Mortgage needed: £58,000

NCMathsKS3 – Ma2.1d, Ma2.2e, Ma2.3a, Ma2.3m, Ma2.4bKS4 – Ma2.1d, Ma2.2e, Ma2.3a, Ma2.3m, Ma2.4b

Adult core curriculaN2/L1.9; MSS1/L1.1

Shared ownership – how much will it

cost?, pages 32–33

1. £530.52

2. £98.32

3. Bedford Road

4. £520.38

5. £600.44

6. Long Lane

7. £923.26

8. Long Lane

9. £140.24

10. £650.47

NCMathsKS3 – Ma2.1d, Ma2.2e, Ma2.3a, Ma2.3m, Ma2.4bKS4 – Ma2.1d, Ma2.2e, Ma2.3a, Ma2.3m, Ma2.4b

Adult core curriculaN2/L1.9; MSS1/L1.1

2. Paying for where you live

Propertytype

50%purchase

price

Mortgageper month

Rental permonth

Total costper month

Puddle Road

2-bed flat £71,500 £413.41 £178.75 £592.16

ChurchLane

2-bed flat £72,500 £419.19 £181.25 £600.44

Snow HillRoad

2-bed house

£90,000 £520.38 £225.00 £745.38

ArcherStreet

3-bed house

£102,000 £589.76 £256.25 £846.01

BedfordRoad

2-bed flat £75,000 £433.65 £133.53 £567.18

Long Lane3-bed house

£68,750 £397.51 £98.32 £495.83

Milton Row 1-bed flat £67,500 £390.28 £140.24 £530.52

LondonRoad

1-bed flat £92,500 £534.83 £211.83 £746.66

MiddleStreet

3-bed house

£112,500 £650.47 £127.87 £778.34

HoptonRoad

4-bed house

£122,500 £708.29 £214.97 £923.26

Money m

anagem

ent

nR

unnin

g a

hom

e

19

Running your own home can be an expensive business. Owning your own home canbe even more expensive. For some people just getting enough money to pay a depositon a mortgage is a real struggle. So many people choose to rent instead. This meanspaying someone a monthly or weekly fee to live in their property.

Quite often houses or flats to rent are advertised in newspapers or on the internet. Tofit in as much information in the advert as possible, shortened forms of words areoften used. These are called abbreviations.

1. Use arrows to match the abbreviation to its full version.

2. Renting a home

avail

gch

d/g

immed

ff

pcm

gge

pw

n/s

inc

unfurn

p/f

ref

ch

double glazing

available

per week

part furnished

unfurnished

central heating

per calendarmonth

gas centralheating

reference needed

garage

non smoker

including bills

fully furnished

immediately

Money m

anagem

ent

nR

unnin

g a

hom

e

20

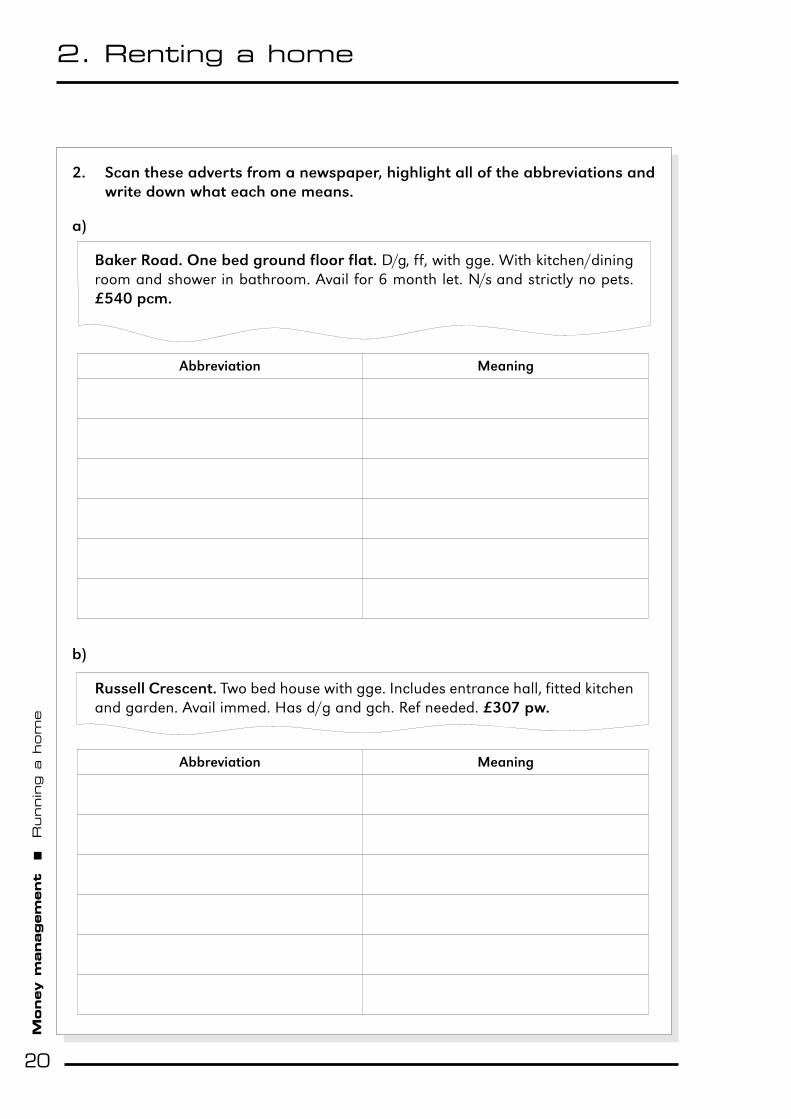

2. Scan these adverts from a newspaper, highlight all of the abbreviations andwrite down what each one means.

a)

Baker Road. One bed ground floor flat. D/g, ff, with gge. With kitchen/diningroom and shower in bathroom. Avail for 6 month let. N/s and strictly no pets.£540 pcm.

b)

Russell Crescent. Two bed house with gge. Includes entrance hall, fitted kitchenand garden. Avail immed. Has d/g and gch. Ref needed. £307 pw.

2. Renting a home

Abbreviation Meaning

Abbreviation Meaning

Money m

anagem

ent

nR

unnin

g a

hom

e

21

When you see adverts for houses or flats to rent, the money is payable per calendarmonth (pcm) or per week (pw). Make sure you know the payment terms otherwiseyou may think you’re getting a bargain when you could be paying a small fortune.

If you are looking at lots of properties you will need to compare like with like. Thesesums tell you what to do.

To work out how much a property costs per week when you only know the pcm price you need to do this sum:

pcm x 12, then divide this answer by 52.

To work out how much property costs per month when you only know the pw price you need to do this sum:

pw x 52, then divide this answer by 12.

Look at each of these adverts for properties to rent in Birmingham and answerthe questions on page 22.

2. A place to rent

Birmingham Post 13 March

Hall Street. Spacious two-bedroom apartment.Unfurnished. £790 pcm

Avon Court. Two bed house.Unfurnished. £150 pw

Orpwood Road. Two-bedroom house. Unfurnished.£500 pcm

Hatchford Road. One-bedroom apartment. Furnished.£110 pw

Quinton Court. One-bedroom apartment. Furnishedwith parking. £525 pcm

St David’s Street. Three-bedapartment. Furnished. £1650pcm

Snow Hill Road. Two-bedroom flat. £625 pcm

Paradise Street. Two-bedroom apartment. Furnished.£125 pw

Money m

anagem

ent

nR

unnin

g a

hom

e

22

1. How much does it cost to rent the two-bedroom flat on Orpwood Road per week?

2. How much does the two-bedroom house on AvonCourt cost per month?

3. How much does it cost to rent the three-bedroomapartment on St David’s Street per week?

4. How much does it cost to rent the two-bedroom apartment on Hall Street per week?

5. How much does it cost to rent the two-bedroom apartment on Paradise Street per month?

6. How much does it cost to rent the one-bedroom apartment on Quinton Court per week?

7. How much does it cost to rent the two-bedroom flat on Snow Hill Road per week?

8. How much does it cost to rent the one-bedroom apartment on Hatchford Road per month?

9. Which two-bedroom house or apartment is the cheapest to rent?

10. Which one-bedroom apartment or house is the cheapest to rent?

11. Which two-bedroom house or apartment is the most expensive to rent?

12. Which property is the most expensive to rent overall?

2. A place to rent

Money m

anagem

ent

nR

unnin

g a

hom

e

23

When you rent a house or apartment from a private landlord, you often have to paythem a deposit. This deposit, by law, will never be for more than two months’ rent. Itis usually for between four and six weeks’ rent.

The deposit covers the property owner for any damage that may happen to thehouse or flat while you are living in it. This can include damage to fixtures andfittings, furniture, cleaning, removing rubbish, unpaid rent and replacing locks if youhave lost the keys or not returned them.

Having to pay not only your first months’ rent, but a hefty deposit as well, can makeyour first few months in you new home a bit more difficult. By checking out howmuch deposit and how much rent you need to pay it will give you a better idea abouthow you’re going to finance your move.

In April 2007 a new rule was introduced to stop landlords from unfairly keeping atenant’s deposit when he or she moves out. It is called the Tenancy Deposit Protectionscheme. There are two different types of scheme.

The first works by putting the deposit into a holding account, which is looked after bythe scheme. When the tenant moves out, as long as there has been no damage tothe property, the tenant will get his or her deposit back in full. If there are anyarguments about the deposit, the scheme looks after the money until it has beensorted out.

The second scheme works by providing insurance cover. If the landlord does not giveback the deposit when the tenant moves out, despite there being no reason for thelandlord to keep it, the insurance company will cover the cost.

Work out how much the deposit will be for each of these properties.

1. The two-bedroom apartment on Hall Street costs £790pcm and the deposit is six weeks’ rent. How much does the deposit cost?

2. The two-bedroom flat on Avon Court costs £150pw and the deposit is five weeks’ rent. How much does the deposit cost?

3. The three-bedroom apartment on St David’s Street costs £1650pcm and the deposit is six weeks’ rent. How much does the deposit cost?

2. Deposits on rented homes

Money m

anagem

ent

nR

unnin

g a

hom

e

24

4. The two-bedroom flat on Snow Hill Road costs £625pcm and the deposit is four weeks’ rent. How much does the deposit cost?

5. The two-bedroom apartment on Paradise Street costs £125pw and the deposit is four weeks’ rent. How much does the deposit cost?

6. The two-bedroom house on Orpwood Road costs £500pcm and the deposit is six weeks rent. How much does the deposit cost?

7. Which house or apartment works out the cheapest for the first months’ rent and deposit?

8. Which house or apartment works out the most expensive for the first months’ rent and deposit?

2. Deposits on rented homes

Money m

anagem

ent

nR

unnin

g a

hom

e

25

If you struggle to afford to rent or buy a house there are other options available toyou. Each council in the United Kingdom has houses and flats that are available topeople living in the area. These properties are normally much cheaper than privatelyrented accommodation. The council will decide whether you are eligible for councilhousing by using a point system to assess your situation. Your current home (or lackof one) and who you are responsible for (children, disabled people), will affect thekind of home you may get and how quickly you get one.

This table shows how much council housing rent in Falkirk cost per week in2007/2008. Use this table to answer the questions on page 26.

2. Council housing

No. of rooms Weekly rent

1 £33.01

2 £38.86

3 £46.01

4 £52.41

5 £57.38

Money m

anagem

ent

nR

unnin

g a

hom

e

26

1. How much does it cost per year to rent a three-bedroom property?

2. How much does it cost per month to rent a five-bedroom property?

3. How much does it cost per year to rent a two-bedroom property?

4. How much does it cost per year to rent a one-bedroom property?

5. How much does it cost per month to rent a four-bedroom property?

6. How much does it cost per year to rent a five-bedroom property?

7. How much does it cost per month to rent a two-bedroom property?

8. How much does it cost per year to rent a four-bedroom property?

Housing associations are the other type of organisation that provides low-cost,affordable housing. Housing associations can help you find a place to rent or a placeto buy.

Use the internet to find housing associations in your area. Type ‘housingassociation’ and then the name of the city, town or county you live in into asearch engine. Make a list of their names and the sorts of accommodation eachassociation provides.

2. Council housing

Money m

anagem

ent

nR

unnin

g a

hom

e

27

Read this information about getting on the property ladder and answer thequestions.

Getting on the property ladder is becoming more and more difficult. Houseprices have soared over the past few years making it more difficult for first-timebuyers to buy a home. Over the past decade the average age of first-time buyershas increased from mid-twenties to mid-thirties. Part of the problem is thewidening gap between house prices and income.

Rising house prices have led to lots of people buying properties with someoneelse, whether it be a partner, friend or family member. It makes the wholeprocess a lot easier and cheaper!

Buying a home instead of renting has a lot of advantages. Buying a house is anest-egg for the future. Most houses increase in value over the years, whichmeans that you will be making money while you are living in your house. Payingrent will only line the pockets of your landlord!

Owning your own home also gives you security. As long as you can make therepayments on your mortgage, you can live in the house for as long as you want,without the threat of someone turfing you out six months down the line!

Freedom is another advantage when you own your own place. You can decorateit how you want; you can keep pets and make any changes to the propertywithout having to get someone else’s permission.

The final advantage to buying a house is that it can help you to create a financialhistory with the company that lends you the money. This can make it mucheasier to borrow money in the future, because if you always pay on time otherlenders will see that you have a good credit history, and will be more likely tolend you money.

1. Why are people finding it so difficult to get on the property ladder?

2. Why can having a financial history with a mortgage lender help you borrowmoney in the future?

3. Give two other advantages to owning your own home.

2. Getting on the property ladder

Money m

anagem

ent

nR

unnin

g a

hom

e

28

To get a mortgage you need to be working and earning a steady income. If you arebuying a house on your own, the maximum amount of money you can borrow isusually based on your salary x 3 (in some cases it can stretch to 3.5). If you are buyinga house with someone else the amount you can borrow is both your salaries x 2.5.

For example, Nathan earns £25,000 per year, so the maximum he can borrow is:

£25,000 x 3 = £75,000

If Nathan decided to buy a house with his partner, who earns £18,000 per year, themaximum they could borrow would be:

£25,000 + £18,000 = £43,000

£43,000 x 2.5 = £107,500

Since the Credit Crunch, some lenders have chosen to use an “ability to pay” score tocalculate how much money they will lend you. This is worked out using an incomeand expenditure assessment. If you have any debts such as loans or credit card bills,this can affect how much you are allowed to borrow.

Work out how much money each of these people can borrow to buy a house.

1. Debbie earns £18,000 a year and Mark earns £25,000 a year. How much money could they borrow if they decide to buy a house together?

2. Yung earns £35,000 per year. How much money could he borrow?

3. Charlie earns £19,000 per year. How much money could he borrow?

4. Will earns £14,000 per year and April earns £30,000 per year. How much money could they borrow if they decide to buy a house together?

5. Misha earns £24,000 per year. How much moneycould she borrow?

6. Jade and Katie both earn £15,000 per year. How much money could they borrow if they decide to buy a house together?

2. How much can I borrow?

Money m

anagem

ent

nR

unnin

g a

hom

e

29

7. Barclay earns £37,000 per year. How much money could he borrow?

8. Aidan earns £12,000 per year and Becca earns £24,000. How much money could they borrow if they decide to buy a house together?

9. Justine earns £40,000 per year. How much could she borrow?

10. Louise earns £13,000 a year and Dan earns £16,000 per year. How much money could they borrow if they decide to buy a house together?

Another factor affecting your mortgage deal is the size of the deposit you can affordto pay upfront. Until recently mortgages of 100% of the value of the property werevery common. This is no longer the case. Most lenders are requesting a deposit ofbetween 3 and 25% of the value of the property. In many cases, the bigger yourdeposit, the lower the rate of interest charged on the mortgage.

If you are thinking of buying a house, the more you save up before you find yourdream property, the easier it will be to get a good mortgage rate.

2. How much can I borrow?

Money m

anagem

ent

nR

unnin

g a

hom

e

30

If house prices are going up, and wages are not, how are you supposed to afford toget on the property ladder? One solution to the problem is shared ownership.

Shared ownership lets you buy a share of a property (for example 50%) from ahousing association. You pay the mortgage to your lender and you also pay rent tothe housing association for the share that they own. This method helps a lot ofpeople get their foot on the rung; it means you don’t have to get a huge,unaffordable mortgage but are at least taking steps towards investing in your ownproperty. In time, when you can afford to, you may be able to buy the whole propertyfrom the housing association.

Work out how much the mortgage would be for each of these shared ownershipproperties.

Mortgage needed

1. Description: Two-bedroom flat

Property value: £135,000

Share percentage: 45%

2. Description: Two-bedroom flat

Property value: £137,500

Share percentage: 50%

3. Description: Three-bedroom house

Property value: £167,500

Share percentage: 50%

4. Description: Four-bedroom house

Property value: £295,000

Share percentage: 25%

2. Shared ownership

Money m

anagem

ent

nR

unnin

g a

hom

e

31

Mortgage needed

5. Description: Two-bedroom flat

Property value: £140,000

Share percentage: 25%

6. Description: Two-bedroom house

Property value: £180,000

Share percentage: 50%

7. Description: Three-bedroom house

Property value: £230,000

Share percentage: 50%

8. Description: Three-bedroom flat

Property value: £145,000

Share percentage: 40%

2. Shared ownership

Money m

anagem

ent

nR

unnin

g a

hom

e

32

Because shared ownership means you buy a percentage of the home and rent therest, it is vital to work out exactly how much it will cost you per month for theproperty.

Fill in the missing amounts in this table and then answer the questions on page33.

2. Shared ownership – how much will it cost?

Property type

50% purchase

price

Mortgage per month

Rental permonth

Total cost per month

Puddle Road

2-bed flat £71,500 £413.41 £178.75

Church Lane 2-bed flat £72,500 £181.25 £600.44

Snow Hill Road

2-bed house £90,000 £520.38 £745.38

Archer Street 3-bed house £102,000 £589.76 £256.25

Bedford Road 2-bed flat £75,000 £433.65 £567.18

Long Lane 3-bed house £68,750 £98.32 £495.83

Milton Row 1-bed flat £67,500 £390.28 £530.52

London Road 1-bed flat £92,500 £534.83 £211.83

Middle Street 3-bed house £112,500 £650.47 £778.34

Hopton Road 4-bed house £122,500 £708.29 £214.97

Money m

anagem

ent

nR

unnin

g a

hom

e

33

1. How much in total will you pay for the cheapest 1-bedroom flat each month?

2. How much rent would you have to pay for the house on Long Lane each month?

3. Which is the cheapest two-bedroom property?

4. How much would the mortgage be per month for the house on Snow Hill Road?

5. In total, how much would it cost each month to live in the flat on Church Lane?

6. Which is the cheapest three-bedroom property?

7. How much will it cost each month to live in the house on Hopton Road?

8. Which property is the cheapest overall?

9. How much rent would you have to pay for the flat on Milton Row each month?

10. How much would the mortgage be per month for the house on Middle Street?

2. Shared ownership – how much will it cost?

Money m

anagem

ent

nR

unnin

g a

hom

e n

Teacher’s n

ote

s

n

34

Aims

• To help students understand the need for insurance.

• To compare the cost of insurance according to location.

• To work out how much insurance they need.

• To find out about the Boscastle flood and its impact on insurance.

Preparation andResources

For this section you will need to distribute a copy ofeach of the following worksheets to each member ofthe group:

• Types of insurance.

• Why do you need building and contents insurance?

• The cost of insurance.

• Home contents insurance.

• That’s why you need it!

Alternatively, the worksheets could be made intooverhead transparencies or incorporated into aPowerPoint or smart-board presentation.

You will need access to the internet for ‘Why do youneed building and contents insurance?’.

Teaching Suggestions

‘Types of insurance’ requires students to matchdefinitions to names of insurance cover.

‘Why do you need building and contents insurance?’gives students information about the need forinsurance and asks them to complete a researchactivity using the internet.

‘The cost of insurance’ provides students with achart comparing the cost of insurance in differentareas of the UK. Students have to answer thequestions and compare some of the data using abar chart.

‘Home contents insurance’ provides students with alist of items likely to be in their homes and requiresthem to work out their total replacement value.

‘That’s why you need it’ is a comprehension activityabout the 2004 flood in Boscastle. All the answersare numbers.

Extension work

1. To help your students become more familiar withsome of the more difficult terms used in this section, ask them to complete the wordladder onpage 95.

2. Ask your students to choose two words from the glossary for Section 3 on page 100 and write a sentence for each word putting the word in an appropriate context. This will show that they have an understanding of the terms.

3. As a follow up to ‘Types of insurance’ you could ask students to choose two of the types of insurance listed and to compare three online quotes for it.

4. As a follow up to ‘Why do you need building andcontents insurance?’ you could ask students to compare the relative costs of insurance and claims with examples of policies with different amounts of excess.

5. You can extend ‘Home contents insurance’ by asking students to find out about the consequences of making a home insurance claim while being under-insured.

3. Insurance

This section will teach your students about homeinsurance – why it is needed and its relative costs.

35

Money m

anagem

ent

nR

unnin

g a

hom

e n

Teacher’s n

ote

s

Answers and mapping

Types of insurance, page 37

Travel Ë Covers you if you have to cancel yourholiday or it is cut short by reasons out of yourcontrol such as unexpected illness. It also covers youif you miss your transport or it is delayed. Medicalor emergency expenses, personal injury or death,accidental damage or injury caused by you, andlost, damaged or stolen personal property are allcovered.

Contents Ë Covers you for theft, loss or damage topossessions in your home.

Building Ë Covers the structure of your homeagainst damage that might be caused by fire, floodor storm. You have to have this insurance if you ownyour home.

Car Ë Covers you if you injure someone or damagesomeone else’s property while driving a car. It cancover damage to your own car too.

Medical/health Ë Pays your bills if you need privatemedical care.

Payment protection Ë Covers you if youunexpectedly can’t make loan or mortgagerepayments due to accident, illness, unemploymentor death.

Dental Ë Cover if you need to have any treatmentdone on your teeth.

Pet Ë Cover if your pet gets ill or is injured.

Income protection Ë Replaces part of your incomeif you can’t work due to long-term illness ordisability.

Critical illness cover Ë Pays out a lump sum if youare diagnosed with certain life-threateningconditions such as some types of cancer or heartattack.

Life insurance/assurance Ë In the event of yourdeath by paying out a fixed cash lump sum.

NCPSHEKS3 – 1g; KS4 – 1e

Framework for teaching EnglishYear 7 – W14, W20; Year 8 – W7c, W10

Adult core curriculaRs/E2.1, Rs/E2.3, Rs/E2.4

Why do you need building and contents

insurance?, pages 38–39

To complete this task successfully, the learner shouldbe able to extract the correct information fromhis/her research on the internet.

NCEnglishEn2.1a, En3.3, En5a, En5b, En3.9b

ICT KS3 – 1a, 1b, 2a; KS4 – 1a, 2b

PSHEKS3 – 1g; KS4 – 1e

Framework for teaching EnglishYear 7 – W14, R1, R2, R6, Wr11; Year 8 – W7c, R1,R2, Wr10; Year 9 – R2, Wr9

Key skills C1.2.1, C1.2.2, C1.2.3, C1.3.1, C1.3.2, C1.3.3,ICT1.1.1

Adult core curriculaRt/E3.1, Rt/E3.3, Rt/E3.4, Rt/E3.7, Rt/E3.8, Rs/E3.1,Rw/E3.1, Rw/E3.5, Ws/E3.1, Ws/E3.2, Ws/E3.3,Ww/E3.1, Ww/E3.3

3. Insurance

36

Money m

anagem

ent

nR

unnin

g a

hom

e n

Teacher’s n

ote

s

The cost of insurance, pages 40–42

1. Bishops Castle, Shropshire

2. Camden/City of Westminster

3. £719.29

4. £261.70

5. £244.74

6. £209.62

7. £525.76

NCMathsKS3 – Ma2.1d, Ma2.3a, Ma2.4b; KS4 – Ma2.1a,Ma2.3a, Ma2.4b

PSHEKS3 – 1g; KS4 – 1e

Key skills N1.1.1, N1.1.2, N1.2.1, N1.2.2, N1.3.3

Adult core curriculaMSS1/E3.1, N1/L1.3, N2/L1.4, HD1/L1.1, HD1/L1.2

Home contents insurance, pages 43–44

Answers will vary. You should check the realism ofthe list of contents and the accuracy of thecalculations.

NCMathsKS3 – Ma2.1d, Ma2.3a, Ma2.4bKS4 – Ma2.1d, Ma2.3a, Ma2.4b

Adult core curriculaRw/E3.3, N2/L1.5; MSS1/L1.1

That’s why you need it!, page 45

1. 37.5mm

2. 7.5cm

3. £15million

4. August 16 2004

5. Around 50

6. Two billion litres

NCEnglishEn2.1a, En5a, En5b, En3.9b

PSHEKS3 – 1g; KS4 – 1e

Framework for teaching EnglishYear 7 – W14, R1, R2, R6; Year 8 – W7c, R1, R2;Year 9 – R2

Key skills C1.2.1, C1.2.2, C1.2.3

Adult core curriculaRt/E3.1, Rt/E3.3, Rt/E3.4, Rt/E3.7, Rt/E3.8, Rs/E3.1,Rw/E3.1, Rw/E3.5, Ww/E3.1, Ww/E3.3

3. Insurance

Chart to show the average insurancepremiums in the top 10 mostexpensive areas in the UK

Cam

den

Hul

l

Gri

msb

y

Gou

dhur

st/C

ranb

rook

Whi

tsta

ble

Live

rpoo

l

Loug

hton

Que

enbo

roug

h

Gla

sgow

Man

ches

ter

Money m

anagem

ent

nR

unnin

g a

hom

e

37

Insurance is an agreement where you pay a company money and they pay your costsif you have an accident or injury or something you own is damaged or lost. In somecases you have to take out insurance, for example when you buy a house. In othercases you don’t have to, but taking out insurance is a wise move.

Match these different types of insurance with the correct definition.

3. Types of insurance

Cover if you need to have any treatment done on yourteeth.

Covers you for theft, loss or damage to possessions inyour home.

Covers the structure of your home against damage thatmight be caused by fire, flood or storm. You have to havethis insurance if you own your home.

Covers you if you unexpectedly can’t make loan ormortgage repayments due to accident, illness,unemployment or death.

Pays out a lump sum if you find you have certain life-threatening conditions such as some types of cancer orheart attack.

In the event of your death this pays out a fixed cash lumpsum.

Replaces part of your income if you can’t work due tolong-term illness or disability.

Covers you if you injure someone or damage someoneelse’s property while driving a car. It can cover damageto your own car too.

Cover if your pet gets ill or is injured.

Pays your bills if you need private medical care.

Covers you if you have to cancel your holiday or if aholiday is cut short by reasons out of your control suchas unexpected illness. It also covers you if you miss yourtransport or it is delayed. Medical or emergencyexpenses, personal injury or death, accidental damageor injury caused by you, and lost, damaged or stolenpersonal property are all covered.

Travel

Contents

Building

Car

Medical/health

Dental

Pet

Paymentprotection

Life insurance/assurance

Critical illnesscover

Incomeprotection

Money m

anagem

ent

nR

unnin

g a

hom

e

38

When you buy a house you have to take out building insurance. This kind ofinsurance will pay out money to you if the structure of your house is damaged. Thisincludes any damage to the roof, floor, ceilings, doors and windows and should coverthe full cost of rebuilding your home altogether, if necessary.

Contents insurance is another type of insurance that is recommended if you rent orown your home, but you don’t have to have it. This type of insurance covers yourpersonal belongings and the things in your home and garden from loss or damage.Items include furniture, electrical appliances, clothing, food and drink and domesticappliances.

Building and contents insurance usually covers any damage caused by:

• earthquakes

• theft

• bad weather, such as floods and storms

• falling trees

• fire

• lightning

• explosions

• aircraft or things falling from them

• impact from a vehicle

You should think hard when you choose where to buy your building or contentsinsurance. It is always best to get several different quotes. Don’t just go with the firstcompany you find. Check what each policy covers. Some might not cover you againstflood damage for example. You should also check how much excess you might haveto pay. Excess is the first amount that you have to pay yourself. It could be £50, itcould be £200, but it is worth knowing what you are signing up to first.

3. Why do you need building and contents insurance?

Money m

anagem

ent

nR

unnin

g a

hom

e

39

Use the internet to find out how much it would cost to get building insurancefrom each of these companies. You should expect to have to put in some of yourpersonal details such as who you live with, your postcode, the birth date of theoldest person living in the house and even whether or not you live in aneighbourhood watch area!

You could use a comparison website to research insurance costs. There are lots youcould choose from including: www.moneysupermarket.com,www.comparethemarket.com and www.confused.com.

3. Why do you need building and contents insurance?

Name of insurer

Web address Premium Excess amount

Halifax www.halifax.co.uk

Churchill www.churchill.com

Norwich Union www.norwichunion.com

Tesco www.tescofinance.com

The AA www.theaa.com

More Than www.morethan.com

Money m

anagem

ent

nR

unnin

g a

hom

e

40

The cost of buildings and contents insurance can vary depending on where you live inthe country. The difference in price can be for a number of reasons including thecrime rate in your area, the average value of property or the risk of flooding in yourarea.

Based on a three-bedroom house these tables show the 10 most expensive andthe 10 cheapest areas for home insurance. Use the tables to answer thequestions on pages 41–42.

3. The cost of insurance

Postcode Post area Average premium

NW1 Camden/City of Westminster £903.81

HU3 Hull £552.00

DN32 Grimsby £489.23

TN17 Goudhurst/Cranbrook, Kent £479.88

CT5 Whitstable, Kent £477.98

L8 Liverpool £476.69

IG10 Loughton, Essex £473.10

ME11 Queensborough, Isle of Sheppey £470.45

G42 Glasgow £469.70

M14 Manchester £464.77

The 10 most expensive areas in the UK for home insurance

Money m

anagem

ent

nR

unnin

g a

hom

e

41

1. Which area has the cheapest average premium?

2. Which area has the most expensive average premium?

3. How much cheaper is the average premium in Bishops Castle than in Camden?

3. The cost of insurance

Postcode Post area Average premium

SY9 Bishops Castle, Shropshire £184.52

EX19 Winkleigh, Devon £189.73

SA64 Goodwick, Pembrokeshire £206.78

PL28 Padstow, Cornwall £208.00

IV6 Muir of Ord, Scotland £208.12

KW16 Orkney, Scotland £215.33

LL77 Llangefni, Anglesey £219.69

KW12 Halkirk, Scotland £220.03

KA28Millport, Island of GreatCumbrae

£221.51

IP16 Leiston, Suffolk £222.45

The 10 cheapest areas in the UK for home insurance

Money m

anagem

ent

nR

unnin

g a

hom

e

42

4. How much cheaper is the average premium in Padstow, Cornwall than in Glasgow?

5. How much cheaper is the average premium in Halkirk, Scotland than in Manchester?

6. Workout the (mean) average premium of the cheapest areas in the UK.

7. Workout the (mean) average premium of the most expensive areas in the UK.

8. On a separate piece of paper draw a bar chart to show the average premiums in each of the postal areas for the 10 most expensive areas.

3. The cost of insurance

Money m

anagem

ent

nR

unnin

g a

hom

e

43

Do you know how much your things are worth? Many people make the mistake ofguessing the value of the contents of their home. This is a bad idea. If somethingwere to happen in your house, imagine how much it would cost to replace all of yourpersonal possessions and furniture. This is why it is a good idea to go round everyroom in your home and price up everything you own. Many home insurers haveforms to fill in to help make sure you don’t miss anything.

Use this form to fill in the value of the contents in your home. If you have morethan one bedroom, use the guidelines for the main bedroom for the others.

Living room Kitchen

3. Home contents insurance

Sofa/furniture

CD player

Television

Video/DVDplayer

Gamesconsole/games

Flooring

Lighting/lamps

Curtains

Other

Moveablefurniture

Fridge/freezer

Washingmachine

Tumble dryer

Cooker

Microwave

Dishwasher

China/crockery

Kitchen utensils

Flooring

Lighting

Curtains

Other

Money m

anagem

ent

nR

unnin

g a

hom

e

44

Dining room Main bedroom

Bathroom Entertainment

Total for all rooms =

3. Home contents insurance

Furniture

China/crockery

Cutlery

Table linen

Wines/spirits

Flooring

Lighting

Curtains

Other

Furniture

Clothes/accessories

Shoes

Make-up/toiletries

Television

DVD player

Flooring

Lighting

Curtains

Other

Towels

Furniture

Flooring

Lighting

Curtains

Other

CDs/records

Videos/DVDs

Books

Computer/laptop

CD player

Camera/video

Toys/games

Money m

anagem

ent

nR

unnin

g a

hom

e

45

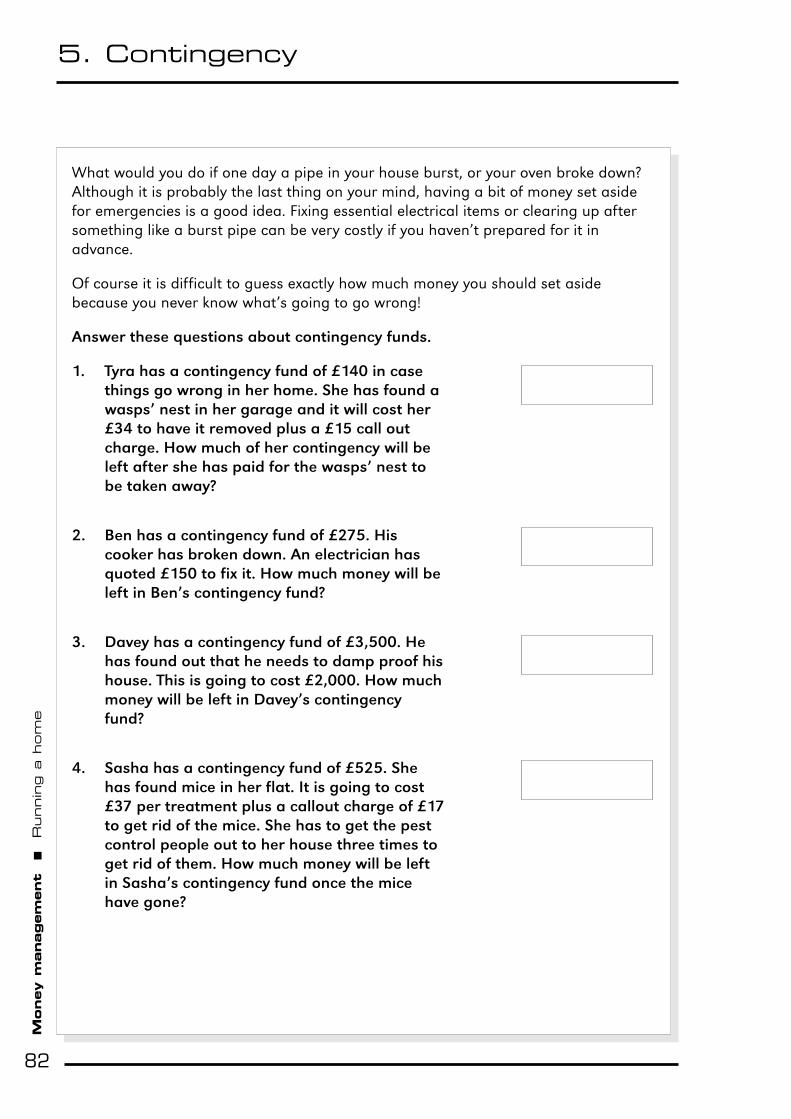

Read the information about the flooding of Boscastle and answer the questions.

On August 16 2004 the small Cornish village of Boscastle was severely flooded.Despite it being the height of summer about 75mm of rain fell in just two hours.This sudden downpour caused two rivers that ran into the village to burst theirbanks and flow through the main streets. It has been estimated that about twobillion litres of water washed through the village that day. This water destroyedwalls and washed away cars (around fifty vehicles were written off) and even theriverbanks themselves. The water also damaged at least 50 local shops andbusinesses, as well as people’s homes, causing millions of pounds of damage.Luckily nobody was killed.

Estimates are that car and contents insurance companies paid out £15million tothe tiny village to repair the damage caused by the floods.

Without insurance, most of the people of Boscastle would have been unable torebuild their lives or replace their belongings damaged by the floods. This isone example where having insurance certainly did pay off.

1. How many mm of water fell in Boscastle in one hour?

2. How many cm of water fell in Boscastle in two hours?

3. How much money was paid out to the villagers ofBoscastle in insurance?

4. On what date did the Boscastle disaster occur?

5. How many vehicles were destroyed by the floods?

6. How many litres of water were estimated to havewashed through the village?

3. That’s why you need it

Money m

anagem

ent

nR

unnin

g a

hom

e n

Teacher’s n

ote

s

n

46

Aims

• To teach students how to read meters.

• To teach students how to check and calculate utility charges.

• To give students the skills they need to compare charges.

Preparation andResources

For this section you will need to distribute a copy ofeach of the following worksheets to each member ofthe group:

• Reading meters

• Comparing your meter and your bill

• The cost of power

• Paying bills – different ways

• Why use direct debit?

• Choosing a supplier

• Monthly outgoings

• When to pay the bills

• How to read a water meter

• How much water?

• Council tax

• Where does your money go?

• TV licence

• Identifying luxury bills

Alternatively, the worksheets could be made intooverhead transparencies or incorporated into aPowerPoint or smart-board presentation.

If you want to carry out the extension activities forworksheets on gas/electricity bills and council tax,you will need access to the internet.

Teaching Suggestions

The first three pages of this section aim to teachstudents how to read utility meters. ‘Readingmeters’, ‘Comparing your meter and your bill’ and‘The cost of power’ fit well together as a combinedactivity.

‘Paying bills’ is a comprehension style activity wherestudents have to decide which payment method ismost appropriate for the people’s circumstances.

‘Why use direct debit?’ is a comprehension activitywhere students have to list the advantages ofpaying by direct debit.

‘Choosing a supplier’ is a numeracy activity wherestudents have to compare the relative costs ofdifferent suppliers and different payment methods.You may need to remind some students that thereare 12 months in the year and run through aworked example for the whole class.

‘Monthly outgoings’ helps students use a calendarto plan when to pay bills.

‘When to pay the bills’ is another numeracy activitywhere students calculate monthly payments forutility bills.

‘How to read a water meter’ and ‘How muchwater?’ aim to teach students how to read watermeters and make calculations based on thereadings. These worksheets fit well together as ajoint activity.

‘Council tax’ provides students with a chartcomparing the cost of council tax in different cities.Students have to answer the questions and comparedata using a bar chart.

4. Bills, bills, bills

This section will give your students all the skills theyneed to deal with household bills.

47

Money m

anagem

ent

nR

unnin

g a

hom

e n

Teacher’s n

ote

s

‘Where does your money go?’ provides studentswith a pie chart showing how one council spends itstax. Students have to carry out calculations basedon the information in the chart.

‘TV licence’ is a numeracy activity where studentscalculate the relative costs of paying for a TVlicence using different payment methods.

‘Identifying luxury bills’ is a classification activitywhere students have to identify bills that could beclassed as non-essential luxuries.

Extension work

1. To help your students become more familiar withsome of the more difficult terms used in this section, ask them to complete the crossword on page 96.

2. Ask your students to choose four words from the glossary for section 4 on page 101 and write a sentence for each word putting the word in an appropriate context. This will show that they have an understanding of the terms.

3. All of the meter reading activities could be followed up with additional practice. You could split your class into four groups and ask each group to produce meter readings for the other groups to read. They could all then calculate the cost of the energy/water used.

4. There is some crossover with the skills taught in Money Management – Smart Consumer. You may find some of the worksheets from Smart Consumer would be helpful to use at this point.

5. There are many websites that compare costs of gas and electricity suppliers. You could set your students the task of finding the best deal for different types of households. www.moneysupermarket.com is a good place to start.

6. You could extend the work on council tax by asking students to find out the costs of council tax in your local area. They could also try to find out how their council spends its money (as in ‘Where does your money go?’).

Answers and mapping

Reading meters, pages 51–52

1. 3856

2. 86394

3. 3805

4. 9274

5. 7205

6. 07345

Key skillsN1.1.1

Adult core curriculaHD1/L1.1

Comparing your meter and your bill, page

53

1. Overestimated by 427 units.

2. Underestimated by 91 units.

3. Overestimated by 545 units.

4. This is the correct reading.

Key skillsN1.1.1

Adult core curriculaN1/L1.1, N1/L1.3, HD1/L1.1

The cost of power, pages 54–55

1. 544

2. 9.02 pence

3. 005645

4. Bills, bills, bills

48

Money m

anagem

ent

nR

unnin

g a

hom

e n

Teacher’s n

ote

s

4.

5.

6.

7.

8.

NCMathsKS3 – Ma2.1d, Ma2.3a, Ma2.4bKS4 – Ma2.1a, Ma2.3a, Ma2.4b

PSHEKS3 – 1g; KS4 – 1e

Key skillsN1.1.1, N1.1.2

Adult core curriculaN1/L1.1, N1/L1.3, N1/E3.4, HD1/E2.1

Paying bills – different ways, pages 56–57

1. A meter

2. Quarterly bill

3. Standing order

NCEnglishEn2.1a

PSHEKS3 – 1g; KS4 – 1e

Adult core curriculaRt/E3.1, Rt/E3.8, Ws/E2.1

Why use direct debit?, page 58

The student should use the information on theworksheet to come up with as many points aspossible as to why Dave should choose direct debitas the method to pay his bills.

EnglishEn2.1a, En2.1b, En2.1c, En2.1d

PSHEKS3 – 1g; KS4 – 1e

Framework for teaching EnglishYear 7 – W14, R1, R2, R4, R6, R7, R8, R11; Year 8 – W7c, R1, R2, R3, R4; Year 9 – R2

Key skills C1.2.1, C1.2.2, C1.2.3, C1.3.1

Adult core curriculaRt/L1.1, Rt/L1.2, Rt/L1.4, Rt/L1.5, Rs/L1.1, Rw/L1.2,Rw/L1.3, Ww/L1.1, Ww/L1.2

Choosing a supplier, pages 59–60

1. Atlantic Electric and Gas

2. Southern Electric

3. Atlantic Electric and Gas

4. EDF Energy pre-payment meter

5. Atlantic Electric and Gas monthly direct debit

6. £51 per year

7. £35 per year

8. £66 per year

9. Your answer to this question will depend on yourpersonal, financial situation.

MathsKS3 – Ma2.1d, Ma2.3a, Ma2.4bKS4 – Ma2.1a, Ma2.3a, Ma2.4b

PSHEKS3 – 1g; KS4 – 1e

Key skills N1.1.1

Adult core curriculaN2/E3.3, MSS1/E3.1, HD1/E3.1

4. Bills, bills, bills

49

Money m

anagem

ent

nR

unnin

g a

hom

e n

Teacher’s n

ote

s

Monthly outgoings, page 61

1. Natalie = £95.05

2. James = £90.82

3. Raj = £146.61

4. Grace = £114.99

5. Jessie = £105.48

NCMathsKS3 – Ma2.1d, Ma2.3a, Ma2.4b; KS4 – Ma2.1a,Ma2.3a, Ma2.4b

PSHEKS3 – 1g; KS4 – 1e

Key skills N1.1.1, N1.1.2, N1.2.1, N1.2.2

Adult core curriculaMSS1/E3.1, N1/L1.3, N2/L1.4

When to pay the bills, pages 62–63

Adult core curriculaWt/E1.1, Ws/E11, Ww/E1.1, MSS1/E3.3

How to read a water meter, pages 64–65

1. 8 Waterford Road = 303

1. Grove Corner = 638

3. Ivy House = 716

4. Clover Cottage = 282

5. 4 Shrewsbury Road = 738

6. 3 Church Lane = 728

Key skillsN1.1.1

Adult core curriculaHD1/L1.1

How much water?, pages 66–67

1. 26,400 gallons

2. 62,700 gallons

3. 77,220 gallons

4. 18,700 gallons

5. 54,340 gallons

6. 98,780 gallons

7. 980 litres per week

8. 215.6 gallons

9. £1.88 per week

NCMathsKS3 – Ma2.1d, Ma2.3a, Ma2.4bKS4 – Ma2.1a, Ma2.3a, Ma2.4b

PSHEKS3 – 1g, KS4 – 1e

Key skillsN1.1.1, N1.1.2, N1.2.1, N1.2.2

Adult core curriculaN1/L2.2, MSS1/L1.1, MSS1/L1.4, MSS1/L2.6

4. Bills, bills, bills

M T W T F S S

1 2Jodie –Mobilephone

3 4

5Jodie –

6

Tom –Gas

7

Tom –Counciltax

8

Tom –Electricity

9

Jodie –Carinsurance

10 11

12 13 14 15 16 17 18

19 20 21

Jodie –Water

22

Jodie –Counciltax

23

Jodie –Electricity

24 25

26

Jodie –Gas

27

Tom –Mobilephone

28

Tom –Water

29 30

50

Money m

anagem

ent

nR

unnin

g a

hom

e n

Teacher’s n

ote

s

Council tax, pages 68–69

1. Band C

2. £1,422.21

3. Band H

4. £904.27

5. £1,536.51

6. £1,638.99

7. £1,452.96

8. £1,449.09

9. £1,406.05

10. Birmingham

11.

NCMathsKS3 – Ma2.1d, Ma2.3a, Ma2.4bKS4 – Ma2.1a, Ma2.3a, Ma2.4b

PSHEKS3 – 1g, KS4 – 1e

Key skillsN1.1.1, N1.1.2, N1.2.1, N1.2.2, N1.3.3

Adult core curriculaN1/L1.3, MSS1/E3.1, HD1/E3.1, HD1/L1.2

Where does your money go?, pages 70–71

1. £101.06

2. £1,087.15

3. £107.18

4. £55.12

5. £1,304.58

6. £35.73

7. £122.50

8. £652.29

9. £119.43

10. £91.87

NCMathsKS3 – Ma2.1d, Ma2.3a, Ma2.4bKS4 – Ma2.1a, Ma2.3a, Ma2.4b

PSHEKS3 – 1g, KS4 – 1e

Key skillsN1.1.1, N1.1.2, N1.2.1, N1.2.2, N1.3.3

Adult core curriculaN1/L1.1, N1/L1.3, MSS1/E3.1, HD1/E3.1, HD1/L1.2

TV licence, page 72

1. 36p

2. £2.53

3. 12p

4. 85p

5. £1,000

NCMathsKS3 – Ma2.1d, Ma2.3a, Ma2.4bKS4 – Ma2.1a, Ma2.3a, Ma2.4b

PSHEKS3 – 1g, KS4 – 1e

Key skillsN1.1.1, N1.1.2, N1.2.1, N1.2.2, N1.3.3

Adult core curriculaN1/L1.1, N1/L1.3, MSS1/E3.1, HD1/E3.1, HD1/L1.2

Identifying luxury bills, page 73

Your students should identify which outgoings theyfeel are a luxury and they could live without.

Adult core curriculaRw/E1.1, HD1/E1.2

4. Bills, bills, bills

0

500

1000

1500

2000

A graph to show the mean average council tax bill in each area

Stoke

on Tr

ent

South

ampto

n

Man

ches

ter

Birmin

ghamNew

cast

le u

pon Tyne

£145

2.96

£135

6.51

1449

.09

£140

6.05

£638

.99

Money m

anagem

ent

nR

unnin

g a

hom

e

51

Money m

anagem

ent

nR

unnin

g a

hom

e

To make sure you are not paying more for your utility bills than you need to youshould always make sure you pay bills based on a reading not an estimate. You cantake a meter reading and send it to the company that supplies you with your gas orelectricity. This gives them the information they need to work out exactly how muchthey should charge you, instead of asking you to pay for an estimate.

There are three different types of meter that you might see. This is how you wouldread each meter:

4. Reading meters

51

9 4 5 5 3 2

09455 000

If the meter reading display lookslike this then you should use thefirst four figures only.

If the meter display looks like this youshould use the first five digits.

If the meter display has dials youshould use the numbers on thebottom four dials from left to right. Ifa hand is between two numbers, usethe lower one.

Money m

anagem

ent

nR

unnin

g a

hom

e

52

Now practise your meter reading skills. Read these meters and write themeasurements in the boxes below.

4. Reading meters

3 8 0 5 8 2

7 2 0 5 6 3

863947 00

07345 75

3. 4.

5. 6.

1. 2.

Money m

anagem

ent

nR

unnin

g a

hom

e

53

To double check that you are being charged the right amount of money for your gasor electricity you should compare your meter reading with the reading on your bill. Ifthe gas or electricity company have used an estimate of your energy consumption,the chances are you could be paying a lot more than you need to.

Compare the meter reading on the bill with the reading on the meter. If thereading is not correct, how far out is it?

4. Comparing your meter and your bill

8 4 7 5 0 0

Last time This time Units used

007284 008902 1618

9 2 6 4 0 0

Last time This time Units used

008347 009173 826

6 2 9 4 0 0

Last time This time Units used

005273 006839 1566

1.

2.

3.

5 5 8 3 0 0

Last time This time Units used

004283 5583 1300

4.

Correct? Yes/No

Over/under byunits

Correct? Yes/No