RRl434al14 GXBISIz Report - nrbglobalbank.comnrbglobalbank.com/files/CREDIT_RATING.pdf · NRB...

16

Credit lnformqtion snd Services Li nnited Rsting CREDIT RATING REPORT On NRB GLOBAL BANK LIMITED GXBISIz Report . . . ,... , , -.,, , .,',' t,,t .tt . , t l'' eui -" '. i " ',, '','-r" ' cnrjt ' '-',," i "'1 "i- : -iilliii'a"#es,'i''-.." "'.''.' 14tn &:i$4'..g1gsr)"'..,' 1,,:, . : " A/ lA;r,,Sigiuibag,ichai ,, ",' Dhalia;'7'A'P9""'; I"",' ', ' reil: 95'39997.4,,',''''', Fax:"W"AirAXO9,gt,, - EmtAih"l',,''"'t''' t. .,',' -"'''..'r',,'', cri s't*i *@,,c,4 da ;'can',..., ". , "' ' ,t , ,'. .',,'' '. ' ,,...,,' ' ,... ,,.., ',' , , ,.' . a'ialYstii i"-'','l' " ' l ', ',.i ', yarz,H"J* '''"' . t','' w".'' oit t<niaiia pg'. ' , ', ' ' , iriiny'.n"iii;+" "r i.':'a Lingrr r-BBBt,'"t',,', :i- sn.iffi'Tte@ T- 3' ,, -,.,'.,,-,,.' .r,,,., . ,, t.r,l;'.r,f I ,...'...,.,- i.at,. ... ll .. ,...',, oitlaokl,'5&6le' .-,' .. -,t , ,,, REPORT: RRl434al14 This is a credit rating report as per the provisions of the credit Rating companies Rutes 1996. CRISL long-term rating is.yalid. ioioii ir" yaea, "id siro,rt term rating'for six months from the date of rating. After the above periods, these ratings will not carry iny vatidity unless the bank goes f9r r?ti!15 suNgill-alce'. - CetSt forcwia Bank/FI Ratin, Methodology pubtished in CRISL website www'crislbd,om l)ate af Ratino: June 30, 2OL4 Valid up to: June 29, 2O15 Long Term Short Term Surveillance Rating BBB ST-3 Outlook Stable 1,O RATIONALE CRISL has assigned "BBB" (pronounced as triple B) rating in the Long Term and "ST-3" rating in the Short ierm to NRil Global Bank Limited (NGB), one of the nine newly floated commercial banks in the country. The above ratings have been done after an in-depth analysis of the operational and financial performance of the bank up to December 31, 2013 along with all relevant quantitative and qualitative factors up to the date of rating. While assidning the rating, CRiSL viewed the ongoing fundamentals such as good assets quality, gooi tiqriOity anO experienced top management etc. Although the above factors are iroderated, to some extent, by initial low profitability, moderate operating efficiency, low earning from core operation, absence of foreign exchange activities, limited credit portfolio, limited-clientele base etc. CRISL expects that over a period of time, the bank would be able to overcome the above limitations. The Bank started its commercial operation on October 23,2Ot3 as per central bank guideline with paid up capital of Tk. 4,250.00 million. Presently, the bank is operating with 10 branches- Total loan and bdvances of the bank stood to Tk. 2,580.02 million as on December 31, 2013 against total deposit of Tk, 3,079.84 million representing an AD ratio of 83.77o/o' Total off- bilunce sheet liability of the bank stood at Tk.466.00 million as on December 3t, 2013. During its 2 months operation NGB earned interest income of Tk.186.17 million and operating incoml of Tk.t2O.77 million. The bank is still in the process of improving the position of present low spread, establishing the Recovery unit, Monitoring and legal departme.nt, Risk ir4anagement iJnit, setting priority sector caps, overcoming the dependence on high costly term deposit, recruiting sufficient staff at various Departments for its full functioning. Banks rated in this category are adjudged to offer moderate degree of safety for timely repayment of financial obligations. Risk factors are more variable in periods of economic stiess than those rated in the higher categories. These entities are however, considered to have the capability to overcome the initial limitations over a period of time' The Short term rating "St-a" indicates good certainty of timely repayment. Liquidity factors and bank fundimentals are sound. Although ongoing funding needs may enlarge total financing requirements, access to capital markets is good. CRISL also views the bank with "stable Outlook" for its performance in line with the pace of industry. 2.O CORPORATE PROFILE 2,L Genesis NRB Global Bank Limited (NGB) is a 4th Generation private commercial bank, which was incorporated on 21 July, 2013 as a public limited company under Companies Act 1994 with the vision "to make NRB Global Bank Limited truly global providing world class services throughout the world". It is the brainchild of 25 (twenty five) well reputed visionary Non- Resident Bangladeshi (NRB) people residing in different countries of the world. NGB got license from Bangladesh Bank on August 05, 2013 and started commercial operations on October Zl, ZOtj. The bank was sponsored by local individuals with a paid up capital of Tk.4,250.00 million against an authorized capital of Tk.12,000.00 million as on December 31, ZOf j. fne bank will further enhance capital through initial public offering in near future. The bank started with the mission to build confidence among the NRBs for investment by providing fast, accurate and satisfactory customer service upholding business ethics and #.*,6nl#,[i6l# rt$:ttrn -.F ;#.i-r Co mnizlei ar EankkA",., med, FCMA, FCS Prssid*nt and fEO Credit fiatrng fnformatlon and $erviees Ltd"

Transcript of RRl434al14 GXBISIz Report - nrbglobalbank.comnrbglobalbank.com/files/CREDIT_RATING.pdf · NRB...

Credit lnformqtion snd Services Li nnitedRsting

CREDIT RATING REPORTOn

NRB GLOBAL BANK LIMITED

GXBISIz Report

. . .

,... , , -.,, , .,',' t,,t

.tt . ,

t l''

eui -" '.

i " ',, '','-r" '

cnrjt ' '-',," i "'1 "i-

:

-iilliii'a"#es,'i''-.." "'.''.'

14tn &:i$4'..g1gsr)"'..,' 1,,:, . : "

A/ lA;r,,Sigiuibag,ichai ,, ",'Dhalia;'7'A'P9""'; I"",' ', '

reil: 95'39997.4,,',''''',Fax:"W"AirAXO9,gt,, -

EmtAih"l',,''"'t''' t. .,',' -"'''..'r',,'',cri s't*i *@,,c,4 da ;'can',...,

"., "'

' ,t ,

,'. .',,'' '. '

,,...,,' '

,... ,,.., ','

, , ,.' .

a'ialYstii i"-'','l' " ' l ', ',.i ',yarz,H"J* '''"' . t',''w".''oit t<niaiia pg'. ' , ', ' '

, iriiny'.n"iii;+" "r i.':'a

Lingrr r-BBBt,'"t',,', :i-

sn.iffi'Tte@ T- 3' ,, -,.,'.,,-,,.' .r,,,.,

. ,,

t.r,l;'.r,f I ,...'...,.,- i.at,.

... ll

.. ,...',,

oitlaokl,'5&6le' .-,' .. -,t , ,,,

REPORT: RRl434al14

This is a credit rating report as per the provisions of the credit Rating companies Rutes 1996. CRISL long-term rating is.yalid.

ioioii ir" yaea, "id siro,rt term rating'for six months from the date of rating. After the above periods, these ratings will not

carry iny vatidity unless the bank goes f9r r?ti!15 suNgill-alce'. -

CetSt forcwia Bank/FI Ratin, Methodology pubtished in CRISL website www'crislbd,om

l)ate af Ratino: June 30, 2OL4 Valid up to: June 29, 2O15Long Term Short Term

Surveillance Rating BBB ST-3

Outlook Stable

1,O RATIONALE

CRISL has assigned "BBB" (pronounced as triple B) rating in the Long Term and "ST-3" ratingin the Short ierm to NRil Global Bank Limited (NGB), one of the nine newly floatedcommercial banks in the country. The above ratings have been done after an in-depthanalysis of the operational and financial performance of the bank up to December 31, 2013

along with all relevant quantitative and qualitative factors up to the date of rating. While

assidning the rating, CRiSL viewed the ongoing fundamentals such as good assets quality,gooi tiqriOity anO experienced top management etc. Although the above factors are

iroderated, to some extent, by initial low profitability, moderate operating efficiency, low

earning from core operation, absence of foreign exchange activities, limited credit portfolio,

limited-clientele base etc. CRISL expects that over a period of time, the bank would be able toovercome the above limitations.

The Bank started its commercial operation on October 23,2Ot3 as per central bank guideline

with paid up capital of Tk. 4,250.00 million. Presently, the bank is operating with 10 branches-

Total loan and bdvances of the bank stood to Tk. 2,580.02 million as on December 31, 2013

against total deposit of Tk, 3,079.84 million representing an AD ratio of 83.77o/o' Total off-bilunce sheet liability of the bank stood at Tk.466.00 million as on December 3t, 2013.During its 2 months operation NGB earned interest income of Tk.186.17 million and operatingincoml of Tk.t2O.77 million. The bank is still in the process of improving the position ofpresent low spread, establishing the Recovery unit, Monitoring and legal departme.nt, Risk

ir4anagement iJnit, setting priority sector caps, overcoming the dependence on high costlyterm deposit, recruiting sufficient staff at various Departments for its full functioning.

Banks rated in this category are adjudged to offer moderate degree of safety for timelyrepayment of financial obligations. Risk factors are more variable in periods of economic

stiess than those rated in the higher categories. These entities are however, considered to

have the capability to overcome the initial limitations over a period of time' The Short termrating "St-a" indicates good certainty of timely repayment. Liquidity factors and bank

fundimentals are sound. Although ongoing funding needs may enlarge total financingrequirements, access to capital markets is good.

CRISL also views the bank with "stable Outlook" for its performance in line with the pace of

industry.

2.O CORPORATE PROFILE

2,L GenesisNRB Global Bank Limited (NGB) is a 4th Generation private commercial bank, which wasincorporated on 21 July, 2013 as a public limited company under Companies Act 1994 withthe vision "to make NRB Global Bank Limited truly global providing world class services

throughout the world". It is the brainchild of 25 (twenty five) well reputed visionary Non-

Resident Bangladeshi (NRB) people residing in different countries of the world. NGB got

license from Bangladesh Bank on August 05, 2013 and started commercial operations on

October Zl, ZOtj. The bank was sponsored by local individuals with a paid up capital ofTk.4,250.00 million against an authorized capital of Tk.12,000.00 million as on December 31,

ZOf j. fne bank will further enhance capital through initial public offering in near future. The

bank started with the mission to build confidence among the NRBs for investment byproviding fast, accurate and satisfactory customer service upholding business ethics and

#.*,6nl#,[i6l#rt$:ttrn -.F

;#.i-rCo mnizlei ar EankkA",.,

med, FCMA, FCS

Prssid*nt and fEO

Credit fiatrng fnformatlon and $erviees Ltd"

Cnedit fi ruforry?mtiCIm mmd Senviees LimitedRctirtg

CREDIT RATTNG REPORTOn

NRB GLOBAL BANK LTMITED

GIBISU Report

D i v e r si f.i ed $a re h,a:l'd,i n g

transparency at all levels and creating value for communities, societies and economies inwhich it operates by ensuring growth and sustainability. The asset size of the bank stood atTk.7,490.39 million and loan & advances stood at Tk.2,580.02 million at the YE2013.Currently the Board is Chaired by Mr. Nizam Chowdhury while Mr. Md. Abdul Quddus isleading the management team as the Managing Director. At present, the bank carries out itsactivities through 10 branches operating with staff strength of 243 as on December 3L,20L3.The corporate Head Office of the bank is located at Khandker Tower, 94, Gulshan Avenue,Gulshan -1, Dhaka-1212.

2.2 Ownership PatternThe ownership pattern of NGB has been found to be concentrated within Sponsor Directors.Bank had total of 425.00 million ordinary shares of Tk.10.00 each as on 31 December, 2013owned by only Sponsors Directors, However, from ,further analysis, it has been found that99.760/o of the total shares are in the range of over 1,000,000 shares indicating concentratedownership state among shareholders.

2.3 Operational NetworkNGB is currently operating with a small network as a newly established bank and concentratedon Dhaka and Chittagong Divisions in line with the business concentration of the regions. Thebank has already launched 10 branches as on May 30,2OL4 and has also planned to open 10new branches during the year 2014. Out of these branches, the bank has to maintain 1:1ratio in operating rural/urban branches. The bank has not yet established SME/Krishi branchduring the period as per Bangladesh Bank guidelines. The bank has taken initiative tofacilitate phone banking and mobile financial services shortly. NGB is currently operating withtwo ATM booths in the Dhaka division.

2.4 Product and ServicesThe bank stafted their operation with conventional banking product. Presently, NGB focuseson term deposit as well as on low cost deposit in deposit portfolio and provides services toindividuals, small and medium sized enterprises and corporate bodies. At present, the bankhas launched different deposit products which include NGB My Wallet, NGB Business PlusAccount, NGB Current Account, NGB Savings Account, NGB Perfect Account, NGB DoubleBenefit Scheme, NGB DPS, NGB FDR, NGB Freshman Account, NGB Junior Joy Account, NGBMillionaire Account and NGB Queen Account. In addition, the bank has offered different loanproducts with various features which are NGB Adhoc Account, NGB Executive Account, NGBFestival Account, NGB Gold Account, NGB Wedding/ Marriage Account, NGB Professional LoanAccount and NGB Travel Loan Account. The bank has also planned to provide some otherproducts/services both for deposits and loan products in the upcoming years. The proposeddeposits products are- NGB Cracker/Pefect (based on daily interest earning), NGB Freshman,NGB M Piggy Bank, NGB Hers, NGB Payroll Solution-My Wallet, NGB Ensure, NGB Business,NGB NRB Deposit, NGB Millionaire, NGB Mega (Triple), NRB Fast & First/Interest Now & NGB

Quarterly Earner and the loan products are- NGB Executive, NGB Voyage, NGB Grace, NGBIDOL, NGB Jury, NGB Knots, NGB Jubilee & NGB Extra.

2.5 Market PositionThe bank has started its journey during the vulnerable economic and political condition in2013 and faces hyper competition in the banking industry. The banking industry ofBangladesh had a provisional deposit of TK.6,105.31 billlon and loan and advances ofTK.4,664.53 billion as on 31st December, 2013, shared by 56 banks consisting of 4 State-Owned Commercial Banks (SCBs), 4 specialized banks, 9 foreign banks, 31 PrivateCommercial Banks (PCBs) and 8 Islamic banks. Against the above, the deposit base and loansand advances of NGB stood at Tk.3.08 billion and Tk.2.58 billion respectively in YE2013. Onthe basis of deposit and loans & advances, market share of NGB stood at only 0.050o/o andO.O54o/o respectively in YE 2013 representing small market share. As the bank is yet to go forfull-fledged operation, the bank generated insignificant income Uo,

H:Ple(Qusiness.ir{uilffinedsc.qre,rcs

PresidentandcEo

Credit Ratrng lnformation and Services Ltd.

O p eia,ti'ng v;r1 ffi ..l:,Obranches .

Insig-pjffiant mAr.k'eS flrAf;g^',i,, ",.

: . 1-'' .:.:,' I I' r :,ri.,'1;.i:,',,,

Credit lnforffisticn mnd Seryices LimitedRstirrg

CREDIT RATING REPORTOn

NRB GLOBAL BANK LIMITED

GIBIS&Report

3.O BANKING SECTOR REVIEW

The banking sector in Bangladesh passed one of the toughest years in terms of falling creditdemand, poor asset quality, low profitability, weak governance and consequently earnedcriticism due to rising financial scams, unsecured volt management and poor creditdocumentation, particularly in state owned commercial banks.

Extending credit to new economic sectors including existing major sectors and maintainingasset quality were major challenges for 2013 due to fear of uncertainty centering politicaltransition, non-stop countrywide blockade and hartal, submissive economic activities andspillover effects of large financial scams. Excess liquidity in the market prevailed almost allover the year due to limited credit demand.

Non-performing loan in the industry alarmingly increased during the year. However, assetquality of scheduled banks has shown improvement due to flexible loan rescheduling policyallowed by central bank at the year end. NPL ratio in the banking sector was about 12olo

during first three quarters of 2013 which stood at 8.93% in Q4, 2013.

Despite all the hurdles and political turmoil Bangladesh Economy achieved growth of 6.03Yo inFY2013 (ended June 30, 2013). Commendable reserve supported by strong foreign remittanceand export growth against slow-moving import growth and low private sector credit demandwere few major driving factors of Bangladesh economy. Industry sector growth rose to 8.99o/o in 2013 against 8.90o/o in 2Ot2 where as service sector growth fell to 5,730lo in 2013 from5.9650/o in 2012.

In 2013 BB issued 9 more banking license with the main objective of expanding financialinclusion. These banks are at the initial stage of establishing and starting operation. However,these banks will have to face significant challenges to operate with 1:1 ratio in opening rural/urban branches, going for IPO within 3 years and to operate side by side with establishedbanks profitability.

A series of counteractive measures have been taken by Govt. and BB to improve riskmanagement, control practice and corporate governance of the banks. On-site and Off-sitesupervision tasks were also enhanced and made more effective to oversee Basel-IIcompliance.

In a milestone move, BB has brought amendments to Guidelines on Risk Based CapitalAdequacy (RBCA) December 2010 and developed SME rating methodology for launching SMErating in Bangladesh. Under changed framework capital requirement for credit risk of allscheduled banks for claim on SME will depend on credit rating by recognized External CreditAssessmertt Institute (ECAI) as exposure to small enterprise amounting to Tk. 3 million &above and exposure to medium enterprise have been brought under variable risk weightinstead of earlier fixed risk weight. BB recognized CRISL and other ratings agencies andissued rating mapping.

For ensuring more transparency and bringing discipline through strengthening supervision,Parliament has amended The Bank Company (amended) Act 2013 which got President'sconsent on July 22, 2013. The new Act brought amendments in the areas of fixation ofnumber of Directors to 20, including Independent Directors, consent from BSEC in appointingIndependent Director, embargo on dividend declaration, holding of another company's shareby bank not exceeding LOo/o of paid-up capital, fixation of loan limit on any particularcompany, group, etc.

Moreover, to reign in investment in capital market by private sector commercial banksBangladesh Bank has issued broad guideline for investment in capital market on May 25,20L4through DOS.

Besides in February, 2011 BB published revised Process Document for SRP-SREP Dialogue onICAAP in May, 2013 for implementation of pillar II of Basel-II and has already started dialogue

Mu ar\hbed, FCMA, FCs

Presidemt and C$0

ereditSatrng lnformatian and $ervlees Ltd*

Crmd[r t rr$mrry?mfi*m mmd Smrsfitrffi$ L$smxtm#ffimting

CREDIT RATING REPORTOn

NRB GLOBAL BANK LIMITED

GilnilS& Reporr

'20 members :Eoa,rd

with private sector commercial banks on their submitted ICAAP document. Moreover veryrecently on March 3t,2OL4 after a Quantitative Impact Study (QIS) Bangladesh Bank hasissued an Action PIan/Roadmap for implementing Basel III in Bangladesh.

Overall banking industry had a deposit (including Govt. deposit) and advance including bill ofTk.6201.10 billion and Tk.476L.51 billion respectively in YE2013 against Tk.5339.87 billionand Tk.4386.15 billion respectively in YE2OI2.

The performance of the banking sector was mixed as it has also improved over the yearsaccording to various indicators such as capital to risk weighted asset, rate of non-performingloans (NPL) to total loan, expenditure income ratio, net profit after tax, return on asset, returnon equity and liquidity.

The NPL ratio of the banking sector as a whole has improved to 8.93% in YE2013 against10.03o/o in YE2012. The average NPL of the 4 state owned banks was around 19.80Yo in Q4,2013 whereas NPL of the 39 private commercial banks also slightly improved to 4.54o/o inYE2013 against 4.58o/o in Y82012. The NPL of the 9 foreign banks showed upward trend whichis around 5.500/o in YE2013 against 3.53o/o in the YE2012.

However, the operational profit and net profit after tax of the banking sector increased toTk.352.10 billion (Tk.340.20 billion in YE2012) and Tk.72.50 billion (Tk.44.7O billion inYE2012) respectively in YE2013. Net profit after tax of SCBs has significantly increased toTk.12.50 billion in YE2013 as against net loss of Tk,10.20 billion in YE?OL2. Return on Asset(ROA) and Return of Equity (ROE) stood at 0.90olo and 10,80% respectively in YE2013 asagainst O.640/o and 8.20o/o respectively in YE 2012.

Overall capital of the banking industry has increased toTk.49B.90 billion in June 30,2013 fromTk.205.80 billion as at December 31, 2008. Overall CAR has increased to 11.52o/o in YE2013from 10.460lo in YE2012. The capital adequacy ratio of SCBs, PCBs, FCBs stood at 10.81yo,t2.52o/o and 20.27o/o respectively in YE2013 as against 8.13o/o, 11.38olo and 20.560lorespectively in YE2012. However, CAR of specialized banks deteriorated to -9.650/o in YE 2013from -7.78o/o in YEZOIZ.

4.O CORPORATE GOVERNANCE

4.1 Board of DirectorsAs a new bank, the members of the Board of NGB stood at 20 and all the members aresponsor shareholders. The bank has not yet appointed any Independent Director. The Board isChaired by Mr. Nizam Chowdhury, who was nominated as the first Chairman of the Board ofDirectors. The Board approves strategic and major policy decisions and oversees managementto attain company's goal, reviews business plan and budget of the bank etc. Board conducted03 meetings during 2013.The Board approves budget and reviews the business plan, policies,procedures, risk management and has continued giving direction as per prevailing economicand market environment. For smooth operation of the bank, the Board formed threecommittees namely Executive Committee (EC), Audit Committee (AC) and Risk ManagementCommittee (RMC).

4.2 Key Board CommitteesThe Board has formed a 7 member Executive Committee (EC) Chaired by Mrs. MaimunaKhanam. The Committee conducted 02 meetings during 2013. The Executive Committeeapproves the credit and business proposals as per approved policy of the Board as well asreviews the policies and guidelines issued by Bangladesh Bank,

Executiue Commlffee,',conducted 2 meetings

The Audit Committee (AC) is comprised of five members. The committee is Chaired byMohammad Fazlay Morshed. Other four members are Mr. Mohammad Hanif Chowdhury,Md. Delwar Hossain, Mr. Mohammed Shahjahan Meah and Mr. Rashed Uddin Mahmud.members play key role in finalization of the financial statements of the bank and otherunder specific Terms of Reference (ToR) that sets out its responsibilities and composition.

Mr.Mr.AC

roleNo

meeting was held in Audit Committee during 2013.

prcsidrnt and ffi$(rEditfieftfi$ Inf*rrnation and Servi*es i_td"

Credit I nforrmstion ur"rd Senrrices LimiteCRsting

CREDTT RATING REPORTOn

NRB GLOBAL BANK LIMITED

GnnISU Report

Experignced t :

management

The Board also formed a 5 member Risk Management Committee in 2013, which is Chaired byMr. Mohammad Hanif Chowdhury. The committee monitors the risk management procedure inline with Risk Management Guidelines conferring the way out to address the lapses identifiedby the Risk Management Unit.

4.3 Management Committee (MANCOM)The Management Committee of NGB is headed by Mr. Md. Abdul Quddus, as the ManagingDirector who joined the bank on August L4, 20t3. Before joining NGB, Mr. Quddus was theDeputy Managing Director of First Security Islami Bank Ltd. and has been serving in thebanking sector for around 36 years, In Management Committee, Mr. Quddus is aided by a

Deputy Managing Directors along with one Senior Executive Vice President, two Executive VicePresidents, one Senior Vice President, one Vice President and one Assistant Vice President.The day-to-day banking functions are handled by thqse professionals having modern bankingknowledge and experience, The above management team has to provide wide succession planto carry out the objectives of the bank smoothly.

The management of the bank formed other committees to handle the banking operationefficiently. The Committees are- Management Credit Committee (MCC), Human ResourcesCommittee (HRC), Asset Liability Management Committee (ALCO), Corporate SocialResponsibility Committee (CSR), Green Banking Committee & Procurement Committee.

4.4 Delegation of PowerThe bank has policies regarding delegation of power of management in terms of investment,administrative and financial issues, Delegation varies depending on different mode ofinvestment which is Tk.15,000 to Tk.50,000 for Managing Director and beyond the above limitis executed by EC. CRISL observes that the Board has to delegate substantial administrativepower to the management for smoothing the day-to-day functioning of the bank.

4.5 Human Resources ManagementNGB has been operating with total staff strength of 243 as on December 31, 2013. The totalHR strength is categorized in different positions which are Executives (20), Officers (176) andsub-staff (47). The bank has Board approved service rules including compensation package,incentive bonus, gratuity, contributory provident fund, benevolent fund and medical benefitetc. NGB has qualified and experienced professionals in its human resource set up. In order toimprove the efficiency of the human resources of the bank, NGB has been arranging trainingprograms for its employees to participate.

4.6 Management Information SystemAs a new bank the Management Information System is at developing stage. For smoothoperation, the bank has implemented centralized core banking software of Temenos (T24).This T24 has been developed using a complete Service-Oriented Architecture (SOA) thatintegrate the required functionality alongside the needs of the business. The core bankingsolution is capable of handling both back office and front offices activities. The above softwarehelps the Bank to cover retailing banking module, corporate bank module, credit module,treasury module & foreign exchange module. NRB Global Bank has already provided thefacility of Automated Teller Machine (ATM) and at present, 2 ATM booths are running. Thebank also used CISCO technology platform with Adaptive Identification and Mitigation (AIM)architecture to secure and protect bank network from external threats and malicious attack.All branches are connected with Head office and are providing branch banking service usingLAN/ WAN. The bank has established the Data Centre to provide a reliable infrastructure for IToperation in Head Office but it will go live and become fully operational within few months.Again, to be compliant with Bangladesh Bank ICT Security Policy, the bank is searching for asuitable place for Disaster Recovery site which is minimum 15 KM Arial distance from DataCentre.

To be fully functional as an automated system the bank has become the member ofBangladesh Automated Clearing House (BACH), NGB has already submitted all requiredreports to Bangladesh Bank (online e.g. online CIB, CTR/SRT reporting) for activating'GoAML'software. Now, the bank is in under process of a full functional HRIS (Human ResourcesInformation System), Inventory Management System and a full functional website.

:

I " ." "''....I .:'''

"

'. '

"'

I FugeIe{iI I

Muzefiar

Fresi

F{}dA, pc3

Cr*dit ftatrnE lnformatlon and $ert'ices Ltd.

Credit lnforrnstion and Services LimitedRoting

CREDIT RATING REPORTOn

NRB GLOBAL BANK LIMITED

GnBlStL Reporr

In the year 20L4 NRB Global Bank willesta blish ca ll center with world lead ing

be launching internet banking facilities. Bank will alsotechnology solution from AVAYA.

5.O RISK MANAGEMENT

Risk management is an essential part of bank management. In order to ensure effective riskmanagement, Risk Management Unit was formed with Mr. R Q M Forkan, DMD as its head.The bank has formed Risk Management Division (RMD). The Bank has also formed RiskManagement Committee (RMC) of the Board on November 26, 2Ol3 in compliance with theBank Company Act, 1991 and BB Circular. As a part of proactive approach the Bank hasalready submitted internal Capital Adequacy Assessment Process (ICAAP) documents to BB.Currently RMD is developing risk management paper, stress testing report and so fofth. Thebank is in the initial stage to develop sectoral study report for loan disbursement policy. Inaddition to regulatory requirement, in ideal situation Bank can also adopt risk based loanpricing through rating model, strong data base management, sectoral study and capitalrationing to strengthen the risk management function.

5.1 Credit Risk ManagementNGB has detailed credit risk guideline in line with Bangladesh Bank guidelines. NGB creditapproval procedure emphasizes thorough credit risk assessment before extending loan. TheCredit Risk Assessment includes borrower analysis, industry analysis, environmental analysis,historical financial analysis, projected financial performance, risk mitigating factor analysisand security of proposed loan. The credit manager/relationship manager makes theassessment of the credit proposals and places it to the credit committee of Head Office forapproval. The credit committee reviews the credit proposals and recommends to appropriateauthority (as per delegated limit) for approval. The Executive Committee approves the creditproposals, which are beyond approving limit of management. Board of Directors reviews thecredit proposals which are approved by the Executive Committee. While reviewing CRISLobserved that the bank does not have separate division for credit monitoring & recovery butthese divisions are under process of forming. Therefore, all duties of the officers /executivesof the bank involved in credit related activities are done through credit administration. CreditRisk Management Depaftment is responsible for maintaining asset quality, assessing risk inlending to a particular customer, formulating policy/ strategy for lending operations. Riskgrading is done as per Bangladesh Bank's guidelines. The prime responsibillties of therelationship Managers/ officers are the early identification, prompt reporting and proactivemanagement of Early Alert Policy.

While reviewing CRISL observed that though the bank has designed credit manual for overallcredit risk management, the bank is yet to put sectoral cap for investing its deposit fund invarious ecgnomic sectors. Moreover, the bank does not have any sectoral study for financinga particular sector, which CRISL believes is crucial for any new bank. While reviewing CRISLalso observes that, the bank does not have any separate independent evaluation procedurefor credit marketing and credit approval of a loan file. In addition to the above, the bank haslack of documentation in some loan cases which will put the bank in an unsecured position interms of security aspects.

While reviewing the risk weight of on-balance sheet exposure under credit risk it was revealedthat there was no risk under 0olo risk category, 0.05o/o under 2Oo/o,23.53o/o under 50o/o, nilunder 75olo, t9.t6o/o under 100o/o, 57.260/o under 125olo, nil under 150o/o category and nilunder Credit risk mitigation. The above information reveals that major exposure of the bankfalls relatively under high risk category. Among the corporate exposure, it has been foundthat 100o/o exposure is on unrated categories (t25o/o risk categories). The bank requires itsclient's credit rating by ECAIs under Basel-II guideline which can contribute significantlytowards improvement of CAR in future.

5.2 Asset Liability Management (ALM)In order to have an effective management of assetLiability Committee (ALCO) and amended the AssetBangladesh Bank ALM guideline. ALCO is headed by

liability, NGB has reorganizedLiability Manual in conformityManaging Director and_he is

the Assetwith the

aided by,

Muzaffpresidsnt

and (80eredit Ratrng rnformation and seryices Ltd"

F{s

Credit lnformction and Services LimltedRating

CREDIT RATING REPORTOn

NRB GLOBAL BANK LIMITED

GffiIS&Report

DMD, Head of Credit Administration Division, Head of Consumer Banking (Principal Branch),Head of International Division, Head of Treasury Division & Member Secretary of ALCO, Headof Credit Division, Head of Internal Control & Compliance Division, Head of Finance &Accounts, Head of IT and Head of Marketing & Development Division etc. ALCO meeting isheld in every month and before meeting key agendas are prepared and circulated to all themembers of the ALCO and minutes are prepared accordingly. ALCO is responsible forreviewing the liquidity management, deposit and investment trend, deposit mix, maturityprofile, monitoring of limit; interest rate profile etc. ALCO held 08 regular meetings in 2013.

5.3 Operational Risk Management

5.3.1 Internal Control and Compliance'Internal Control and Compliance Division' of the bank has been established to minimize theoperational irregularities, lapses, malpractices, corruptions and frauds arising out of thedeviations from the set rules and procedures. NRB Global Bank Ltd. has also established a

System of Internal Control, which has been designed to manage all the risk. The bankregularly reviews the effectiveness of internal control process through its Audit Committeeand Executive Committee. But the bank has not yet segregated tasks into separate divisionnamely Audit & Inspection Division, Compliance Division and Monitoring Division but all theactivities of those are done under Internal Control and Compliance Division. However, CRISLreviews that due to lack of internal audit, no inspection/audit has been conducted regardingall core risk categories, non-payment of cheques and accepted bills and employment practicesand workplaces safety by internal audit.

5.3.2 Preventaon of Money LaunderingAnti Money Laundering risk is defined as the loss of reputation and expenses incurred aspenalty for being negligent in prevention of money laundering. The Bank has formed AntiMoney Laundering Committee under the leadership of the Chief Anti Money LaunderingCompliance Officer (CAMLCO) headed by an EVP, Mr. Mohmmad Enamul Islam Khan. Forcomplying with the Anti Money Laundering (AML) and Combating Financing of Terrorism (CFT)activities, the bank has a designated Chief Anti-Money Laundering Compliance Officer(CAMLCO) under Anti-Money Laundering Division, head office, who has sufficient authority toimplement and enforce corporate wide AML policy, procedure & measure. Moreover, everybranch of NGB has a designated Branch Anti-Money Laundering Compliance Officer (BAMLCO)under Branch Anti-Money Laundering Compliance Unit, who independently reviews thetransaction of accounts, with verification of Know Your.Customer (KYC) and SuspiciousTransaction Report (STR). Presently the bank is submitting Cash Transaction Report (CTR)generated by the cash transaction limit of Tk.10 lac. Bank has established a manual forPrevention of Anti-Money Laundering and issues circulars from time to time giving specificguidelines in accordance with Bangladesh Bank guidelines, regulations, Anti-MoneyLaundering Act, 2009 & Anti Terrorism Act 2009. Besides the above, to launch 'GoAML'software as per the guideline of Bangladesh Financial Intelligence Unit (BIFU) of BB for thesurveillance and detection of terrorist financing and money laundering where all branchesreport CTRs to Head Office, AMLD for final repofting to BB, the bank has already submitted allrequired reports to Bangladesh Bank.

5.4 Market RiskMajor market risks arise from interest rate risk, equity and commodity financing risk andforeign exchange risk. The position of NGB in these regards stand as follows:

5.4.1 Interest Rate RiskPresent competition for deposit and lifting lending cap has created substantial interest raterisk for the banks. The bank has very little scope to revise pricing of loan from time to timedue to immense competition in the market. The Asset Liability Management Committee(ALCO) has been assigned to monitor and review the interest rates of NGB. The committee inits monthly meeting takes decision in respect of interest rates of the bank. The ALCO hasestablished its own Interest Rate Policy for monitoring and minimization of interest rate risksat an acceptable level. Guidelines and actions are taken in adherence to the policies issued byBangladesh Bank from time to time,

Presid*nt and {f0Credit Hatrng Infarmatlon and Services Lrd-

Credit trnforrmation snd Services !-i rnitedRsting

CREDIT RATING REPORTOn

NRB GLOBAL BANK LIMITED

GnBilS&Report

Average financialperfarrnance

5.4.2 Equity Risk and Commodity Financing RiskNGB has no investmeni in capital ,aiket though- most of the newly. established bank have

rlirt"Jin" i"urney. The eank'has investment in commodity based industries like' agriculture'

trade service and constiuillon inoustry, which may create commodity financing risk like most

oth"r ao*r"rcial banks since commodity market is volatile'

5.5 Foreign Exchange RiskIn order to address tne foieign exchange risk NGB has adopted foreign exchange risk manual

and investment guideline in'iine with the Bangladesh bank.instruction. The bank is not fully

functional in all areas of foreign exchange tranlaction' on the other hand, the bank is in. the

process of having correspond6nt relatio-nship. by opening of NoSTR.o accounts with Mashreq

Lunf, USn; Sonati ean-kiUr) ltO., Londoni United eank of India, Kolkata, India & AB Bank

Ltd., Mumbai, India.

6.O PERFORMANCE

6.1 Financial PerformanceOveratt financial per-formance of NGB has been found to be below average as the bank could

noi g;ne.ateo sunicieni revenue compared to expenses as the- bank started its business

opiritio" on october zi, zotg.cnlSL evaluated the two months financial performance of the

OInf< Ou.ing 2013 in terms of Return on Asset (ROA), Return on_ Equity (ROE) and -Net

int"i"rVp.,ifit margin (NIM). Interest Income of NGB stood to TK. 185.17 million in YE2013'

Interest income consisted of interest on loans and advances of Tk'26.41 million (14'19olo of

interest income) and interest on balance with other bank and financial institution of Tk'

lisi.ig million (85.81o/o of interest income) which implies low earning from core.operation'

ngiirit ln" runiu, the bank paid Tk,65.69 mittion as interest paid on deposit resulting to net

inierest income or 1.izo.+b million in YE2o13' During the year 2013 the total operating

iniorn" stood at Tk.L2o.77 million, The above operating income-revealed that 99'75o/o income

g";"tut"O from net interest/net profit on investments, O'2Oo/o income from commission'

6xchange & brokerage & 0,05o/o income from other operating income' The operating expenses

itooO Jt Tk.85.54 million in yE2O13. The major portion of the-above operating expe.nse

.o.p.ii"O oi "*p"nr"

for Rent, Taxes, Insurance, Eiectricity, etc (60.14olo) followed by salary

&. uiio*un.", (is.Orozo) and other expenses (10'450/o), consequen-tly, the operating profit

Oifo." piouirion stood [o TK. 35.23 miilion during the jame qerig!, Net profit before-tax^and

n"t fori after tax subsequently stood at TK. 4'49 million and TK' (10'76) million in YE2013' In

its consequences, the nlirrn on Assets (RoA) and the Return on Equity (ROE) after.tax stood

"i ""iv--'o.i4o/o dnd -o.zsoto respectivlly in yezorg' As a newly operated bank, all .the

investment portfolio oi tne nanr' is unciassified so against the same bank kept required

;."ri;i;;; of rk.go.zs million in YE2o13. Net interest/profit margin (NIM) stood at 2'25o/o in

YE2013.

NGB,s earnings from core business has to be augmented for its long-term sustainability as a

5r"kid ;;*iany anO itio to comply with licensing requirement of BB for going into initial

public offering (IPO) within three years'

It is wofth to mentionable here that the bank deposited significant amounting of Tk.2,450'00

,ittion in Reliance Finance Ltd. as a FDR which is consider as related party transaction

indicating concentrated investment. During 1Q of 2014 the bank's total loan & advances stood

atiu.z,izo.16 million. Due to the low investment growth in the industry NGB has increased

its investment exposure to low yielding government security'

Since the bank has operated for only two months during the year 2013, CRISL also reviewed

ihu Munag"rent Accounts up to June 30,2014. The above account reveals that the Interest

in.or" stboO atTK. 529.05 million as on June 30,20t4. Againstthe same, the bank paid Tk.

2gO.34 million as interest on deposit resulting to net interest income of Tk'238'7L million'

O-riirS tnit perioO the total operating income stood at TK' 247 '78 million against the

opui"iing "*funr"s

of TK.2!6.04 million resulting to profit b.efore provision of Tk'31'75

million. As on June 30, 2O!4 it showed that the total loans and advances of NGB increased

signifi.antf, to 'ft. S,dee.79 million from Tk' 2,580.O2 million in YE2013 which ultimately

M urail; r(l-Ii.* eri, Frri &, Fe 3

Prcsiddnt and ffOCredit Aafing lnformation and Serviees Ltd,

Credit lnforrnotion ond Seruices LimitedRoting

CREDIT RATING REPORTOn

NRB GLOBAL BANK LIMITED

GnB[Snz Report

increased the interest income to Tk. 529.05 million from !86.t7 million in YE2013' Again on

the same date, the bank also invested in govt. securities. Therefore, the investment income

as well as interest income both ultimately turned the net profit after tax to Tk. 3.37 million as

at June 30,2Ot4 from net loss of Tk. (10.76) million in YE2013 after adjustment of operatingexpenses.

6.2 Operating EfficiencYOverall operating efficiency of NRBGL has been found to be moderate. The operatingefficiency is reviewed in terms of operating income, operating expenses, cost-to-income ratioand yield against per Tk.100 staff cost. The operating income and expenses of the bank stoodat tk.tZO.jl million and Tk.85.54 million respectively during the year 2013. Accordingly,efficiency ratio stood at 70.830/o in YE2013. Yield per 100 Taka Staff cost stood at Tk.274.38in yE 2013. As the bank is at its inltial stage of operation, operational performance could notstand at an expected level due to comparatively high fixed operating cost driven by opening ofnew branches. CRISL assumes that operating performance of the bank is expected to improvewith the courses of time through increasing operating income by expanding its businessavenues to various economic sectors, non-funded income base and increased investmentincome from treasurY operation.

7.O ASSET MANAGEMENT

As a newly established and low investment exposure with limited cliental based bank, theoverall asset quality of the Bank has been found to be good indicating no classified as well as

rescheduled investment in YE2013. The bank conducted only two large loan exposure (fundedTk. 150.76 million & non-funded of Tk. 475.80 million) which stood at Tk.626.56 million inyE2O13. The assets of NGB stood at TK.7,490.39 million in YE2013. The above assets base

has been financed by insider liabilities (Shareholders'equity) of 56.600/o and outsider liabilitiesof 43.4Oo/o (Outsider liabilities comprised of 4L.L2o/o deposit, 2.28o/o other liabilities) as on

December 31, 2013.

7.1 Loans and advancesOverall asset quality of NGB has been found to be good in YE2013. Total loans and advances

of the bank stood at TK. 2,580.02 million in YE2013 (TK. 5,048.79 million as at June 30,

2OL4). Total loans and advances have been found to be unclassified up-to the date of ratingdeclaiation. Moreover, CRISL foresees that the bank has to put utmost importance on keeping

the existing asset quality unharmed. Against total provisional requirement of Tk. 25.98 million

for loans and advances in YE2013 and the bank also kept a provision of Tk. 25.98 million as

on December 31, 20L3. Moreover, regarding off-balance sheet exposure the bank kept a

provision of Tk.4.76 million as on December 3t,20t3 against required provision of fk.4.76million.

7.2 Sectoral and Credit ConcentrationThe bank has staded its operation with concentration on private sector like internal tradefinance (SME) A consumer finance because of its limited scope to invest. But the bank has allout efforts to invest in diversified business sectors. During the period under review, overallsectoral portfolio reveals that 93olo investment has been in working capital finance andremaining 7olo investment in term loan facilities. On the other hand, as at March 31, 2014, thesectoral portfolio reveals that77.3}o/o investment was in trade service followed by 2t.24o/o inothers,0.8oo/o in agriculture and 0.630lo in housing. However, there is little investment in

agricultural sector during the rating period. According to geographical location-wise analysis,it has been found that 100o/o of portfolio was invested in Dhaka region due to minimumbranch network which implies that there is no investment in rural areas. Due to being a newlyestablished bank, NGB will face the challenge to diversified quality based investment exposureand high concentration of investment portfolio in all areas indicating additional capital chargewill be applicable as per Pillar-Il of Basel-II through SRP process documents. However, thebank has planned to invest more in SMEs sector, retail sector & women enterprise sector in

the up-coming year, However the bank invested 100o/o of its portfolio with holding securityother than the debtor's personal security. CRISL reviewed the Group exposure and revealedthat only NASSA Group has taken the Overdraft facilities of Tk.600.00 million for 3 concerns'

iji,

l1t+

President and CtO

(*gditSatrng lnfnrmation and Serviee$ L-t#"

Credit fi m$orrylmti*m m rrd Senvfr ctrs Li m itmdRcting

CREDIT RATTNG REPORTOn

NRB GLOBAL BANK LIMITED

Gilntffi& Report

However, the bank has also planned to focus the financing activities of syndicate loan andexpand the group financing.

7.3 Off-Balance Sheet ExPosureTotal off-Balance sheet exposure of the bank stood at TK. 466.00 million in YE2013. Off-balance sheet exposure only consisted of Letters of guarantee. Credit risk for Off-Balancesheet exposure stood at Tk. 356.90 million which is 5.95o/o of total RWA. The bank madeprovision amounting TK. 4.76 million as on December3l, 2Ot3 for OBS exposure. Whilereviewing the risk weight-wise classification of the credit equivalent of off-balance sheetexposure, it has been revealed that 100% of the exposures falls under 125olo risk as all theexposures were unrated.

As a newly established bank, NGB is operating with the minimum required capital base asprescribed by the Bangladesh Bank. The bank started its journey with Tk.4,250.00 millionpaid up capital as minimum regulatory capital requirement of Tk. 4,000.00 million. Under riskbased capital adequacy framework of Basel-II, the total RWA of the bank stood atTK.5,995.30 million as on December 31, 2013 of which 99.L2o/o emanated from credit risk andrest 0.88o/o from operational risk. Against the above, total eligible capital stood atTk.4,269.98million comprising Tier-I (core capital) ot Tk.4,239.24 million and Tier-II (supplementarycapital) of Tk.30.73 million representing a capital surplus of Tk.269.98 million. The RWCAR ofthe bank stood at 71.22o/o in YE2013 and 58.31olo at 1't quarter of 20L4. The CAR on corecapital (Tier-1) stood at 7O.7Lo/o and on supplementary capital (Tier-II) stood at 0.51o/o inYE2013, Like most of the banks in the industry, NGB focus on capital management tomaintain adequate capital buffer for Basel-II capital adequacy framework. The bank is

currently operating with limited investment portfolio with unclassified exposure and most ofthe funds are invested in bank and NBFIs as deposited fund indicating high CAR. CRISL viewsthat CAR of the bank might decrease in the up-coming year due to increase of risk weightedassets. In accordance the above the Bank needs to concentrate on its client ratings tomaintain capital adequacy in near future because the bank exposed to mostly unratedcorporate exposure. Moreover, as central bank is going to issue guideline on Basel-III, bankmay require more capital to comply with requirement.

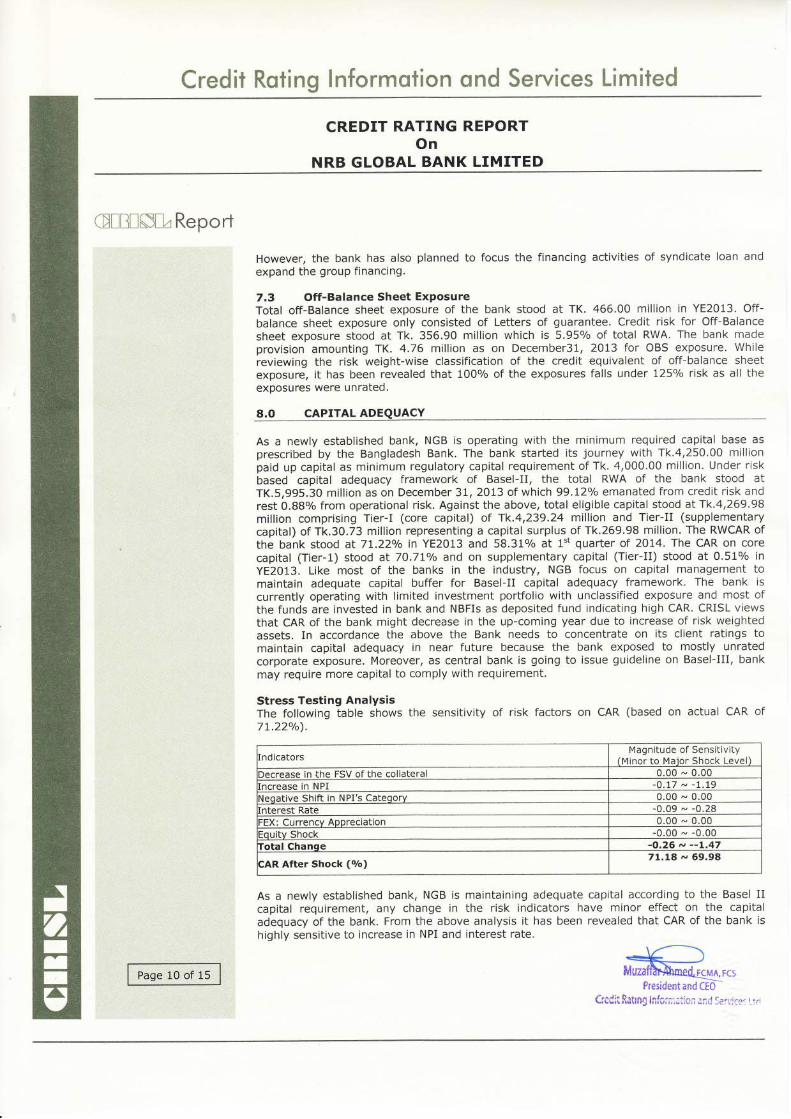

Stress Testing AnalysisThe following table shows the sensitivity of risk factors on CAR (based on actual CAR of7!.22o/o).

nd icatorsMagnitude of Sensitivity

(Minor to Maior Shock Level)

Decrease in the FSV of the collateral 0.00 - 0.00ncrease ln NPI -0.t7 - -1.19

Neqative Shift in NPI's Category 0.00 - 0.00nterest Rate -0.09 - -0.28

FEX: Currencv Appreciation 0.00 - 0.00ouitv Shock -0.00 - -0.00

Iotal Chanse 'O.26 r\, --L.47

CAR After Shock (o/o)71.18 '., 69.98

As a newly established bank, NGB is maintaining adequate capital according to the Basel IIcapital requirement, any change in the risk indicators have minor effect on the capitaladequary of the bank. From the above analysis it has been revealed that CAR of the bank is

highly sensitive to increase in NPI and interest rate.

CAPITAL ADE

Fresident and tEO

Credit ! mforry?mtior"r snd Services LlrnitmdRutinE

CREDIT RATING REPORTOn

NRB GLOBAL BANK LIMITED

GilnilS& Reporr

Goad,,liquidity

9,O LIQUIDITY AND FUNDING

9.1 Liquidity PositionThe overall liquidity of the bank has been found to be good during YE2013. Both CRR andSLR of NGB are adequately maintained as per requirement of the Bangladesh Bank up-to thedate of rating. The CRR and SLR requirement was TK. t7.67 million and TK. 55.96 millionrespectlvely as on 31st December, 2013; against which NGB kept TK. 1,176.85 million andTK. 1,195.28 million respectively. Total surplus of the bank against required CRR and SLRstood at TK. 2,280.82 million at YE2013. The bank's liquidity ratio stood to L22.24o/o inYE2013. The loan and advances to deposit ratio stood lo 79.37o/o in YE2013. Again, loan andadvance to deposits and equity ratio stood at 34.44o/o in YE2013. CRISL opines thatmaintaining excess liquidity may not be prudent for asset liability management as the bank is

committed to pay depositors a certain interest.

CRISL reviewed bucket wise payment obligation in comparison to its available assets atdifferent maturity buckets. The analysis shows that the bank had net positive gap of TK.L7t.29 million up to 1 month maturity bucket. In 1 to 3 months maturity bucket the positiveliquidity gap was TK 1,035.98 million and in 3 to 12 months maturity bucket it had positiveliquidity gap of fK. 2,4L6.66 million. Hence it is expected that the bank will be able to meetits obligations with sufficient cumulative surplus.

9.2 Fund ManagementNGB has been operating with average funding base, The funding mix consists of 4t.L2o/odeposits and others; 56.600/o shareholders equity and 2.28o/o other liabilities. Total depositsconsists of Term Deposit of TK,3,023.94 million (98,18olo of total deposit), Current Deposits ofTK.13.26 million (0.43olo of total deposits) and Saving Bank Deposits of TK. 42.65 million(1.39o/o of total deposits). CRISL reviews the funding structure and revealed that high costdeposit stood at fk3,023.94 million (around 98olo of total deposit mix) in YE2013 whichultimately increased the cost burden as the investment growth is tight. Top 10 depositors areholding 93.19o/o of total deposit at YE2013. The bank's weighted average cost of fund stood at11.88o/o at YE2013 indicating a higher side.

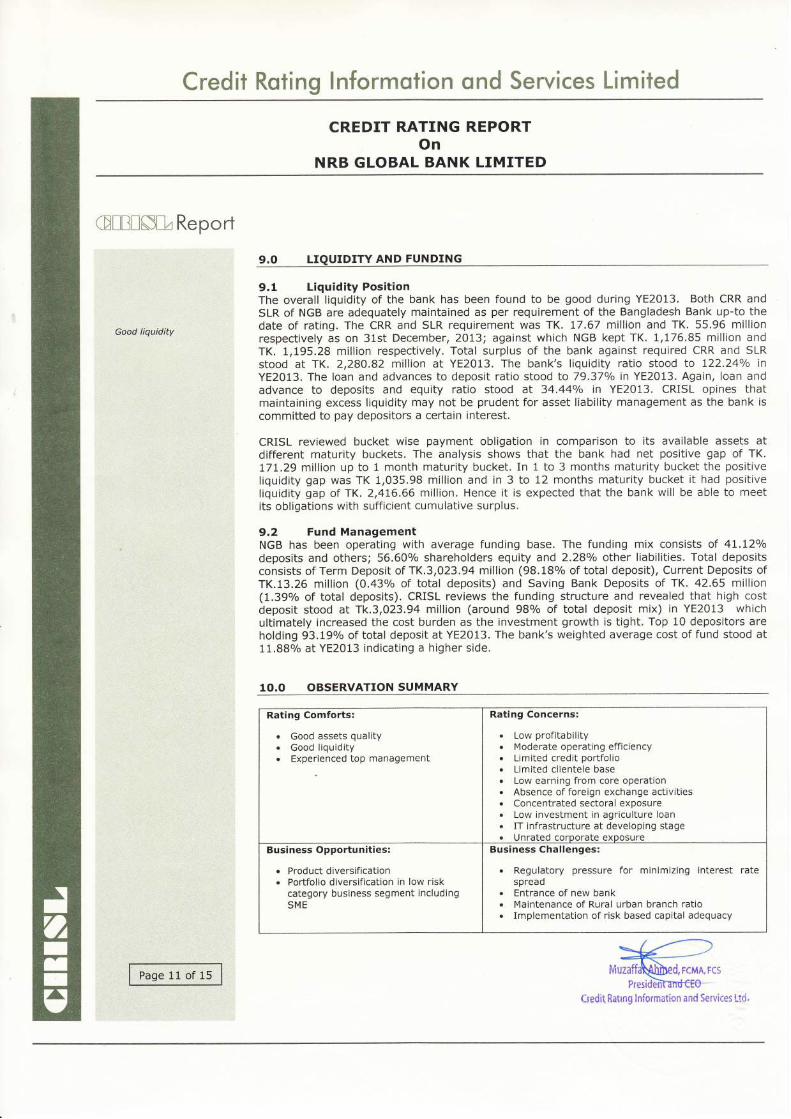

1O.O OBSERVATION SUMMARY

Rating Comforts:

r Good assets quality. Good liquidity. Experienced top management

Rating Concerns:

. Low profitability

' Moderate operating efficiency. Limited credit portfolio. Limited clientele base. Low earning from core operation. Absence of foreign exchange activities. Concentrated sectoral exposure. Low investment in agriculture loan

' IT infrastructure at developing stage

' Unrated corporate exposureBusiness Opportu nities:

. Product diversification

. Portfolio diversification in low riskcategory business segment includingSME

Business Challenges:

. Regulatory pressure for minimizing interest ratespread

o Entrance of new bankr Maintenance of Rural urban branch ratio. Implementation of risk based capital adequacy

f*uzaff, FCS{4, FCS

Presid

(redit Hatrng lnformation a$d Services Ltd.

Cnedit I mforry]utiom mmd Serv$cffis tirmitedffi,mtir:g

CREDIT RATTNG REPORTOn

NRB GLOBAL BANK LIMITED

GilnilS& Report

11.O PROSPECTS

Having many challenges, the banking sector is expected to remain stable during the year2014. Although the main driving force of the economy i.e RMG sector will continue to face thechallenges of wages hike, GSP withdrawal of USA, political uncertainty, severe competitionamong many banks, the RGM is expected to perform well and will move to stable pace, It is

also anticipated that foreign currency reserve will increase further in FY2014-15 ($19 billion inFebruary,2014). Bangladesh Bank has taken number of steps to accelerate the economic andbanking growth like broadening the Export Development Fund (EDF), number of reformmeasures at the administrative level and so forth.

Unavailability of gas and power may continue to adversely affect investments growth andemployment. Capital market, another area of discomfort, is yet to stabilize as real investors'confidence has not been restored. Ongoing downward trend in real estate business, ship-breaking and commodity trading is also expected to continue to remain stable in 20L4. foovercome the above challenges banks should focus on improving the quality of assets throughstrong monitoring, actively follow risk management guideline, strong review of portfolio,improve information technology as well as focus on human resource development. In addition,Overall banking industry may improve in the upcoming year if stability in the politicalcondition may continue with increase the credit growth as well as priority for infrastructuredevelopment.

END OF THE REPORT

(Information used herein is obtained from sources believed to be accurate and reliable, However, CRISL does notguarantee the accuracy, adequacy or completeness of any information and is not responsible for any errors oromissions or for the results obtained from the use of such information, Rating is an opinion on credit quality onlyand is not a recommendation to buy or sell any securities. Ail rights of this report are reserved by CRISL. Contentsmay be used by news media and researchers with due acknowledgement)

[We have examined, prepared, finalized and issued this report without compromising with the matters of anyconflict of interest, We have also complied with all the requirements, policy procedures of the BSEC rules asprescribed by the Bangladesh Securities and Exchange Commission,l

ed, rc*tn, FesPrkipl*nt and efo

Credit franng trnf*rmffin and Serviees l"td"

iFil1" I rs+t t I Urirj

Cnedxt R*timg $m$mrmmtEmm mmd $mruic#$ E-$ rmEted

CREDIT RATTNG REPORTOn

NRB GLOBAL BANK LIMITED

Gil3n$&Report

L2.O CORPORATE INFORMATION

DATE OF INCORPORATION:FUNCTIONING DATE:

BOARD OF DIRECTORS:Mr. Nizam ChowdhurYMr. Mohammad Hanif ChowdhurY

Mr. Ghulam MohammedMr. Mohd. Ataur Rahman BhuiYan

Mr. Mohammed Shahjahan Meah

Dr. Mohammed FaruqueMrs. Sarina Tamanna Huq

Mr. Mohammed Manzoor Alam Seth

Mr. Mohammed YousufMr. Osman GaniMr. Rashed Uddin Mahmud

Mrs. Maimuna KhanamMr. Morshedul AlamMr. Md. Delwar HossainMr. Kamal Pasha

Mr. Md. lahangir HossainMr. A.H Md' Mahmud Ribon

Mrs. Mohammed FazlaY Morshed

Mrs. Reshma Parvin Morshed

Mr, Subrata Kumar BhowmickMr. Md. Abdul Quddus

Auditors: Hoda Vasi ChowdhurY & Co'

Core Management BodY:

Mr. Md. Abdul QuddusMr.RQMForkanMr. Kazi Mashiur Rahman JaYhad

Mr. Mohmmad Enamul Isalm Khan

Mr.JQMHabibullah,FCSMr. Zulfiker Ahmed KhanMr. Md" Zillur Rahman, FCA, ACS

Mr. M. Morshedul Quader Kalili

Mrs" Mahbuba Mohsin JoYa

Mr. Mohammad Kamrul Hossain

Mr. Md' Habibur RahmanMr" Md. Mehedi Hasan

Managing DirectorDMDSEVP (Credit)EVP (General Services)SVp (ff rman Resources & Company Secretary

SVP (International Division)VP (Finance & Accounts)VP (Retail Banking)SAVP (Research & Development In- charge)

SAVP (tnformation TechnologY)

AVP (TreasurY In-Charge)FAVP (ADC & Cards)

2tth JulY 2OL323th October 2OL3

ChairmanVice- ChairmanDirectorDirectorDirectorD i recto rDirectorD i recto rD i recto rD i recto rDirectorD irecto rD irectorDirectorD irecto rD irecto rDirectorDirectorDirectorDirectorManaging Director

d, rcMn, Fes

{redit ftatrng lnfclmaiion e;"d Servicss Ltd'

f,reCEt il m$mrryxmtimm mmd Smryic#s LirmfrfwdRmtirtg

CREDIT RATING REPORTOn

NRB GLOBAL BANK LIMITED

ffiilnnffiiir Report

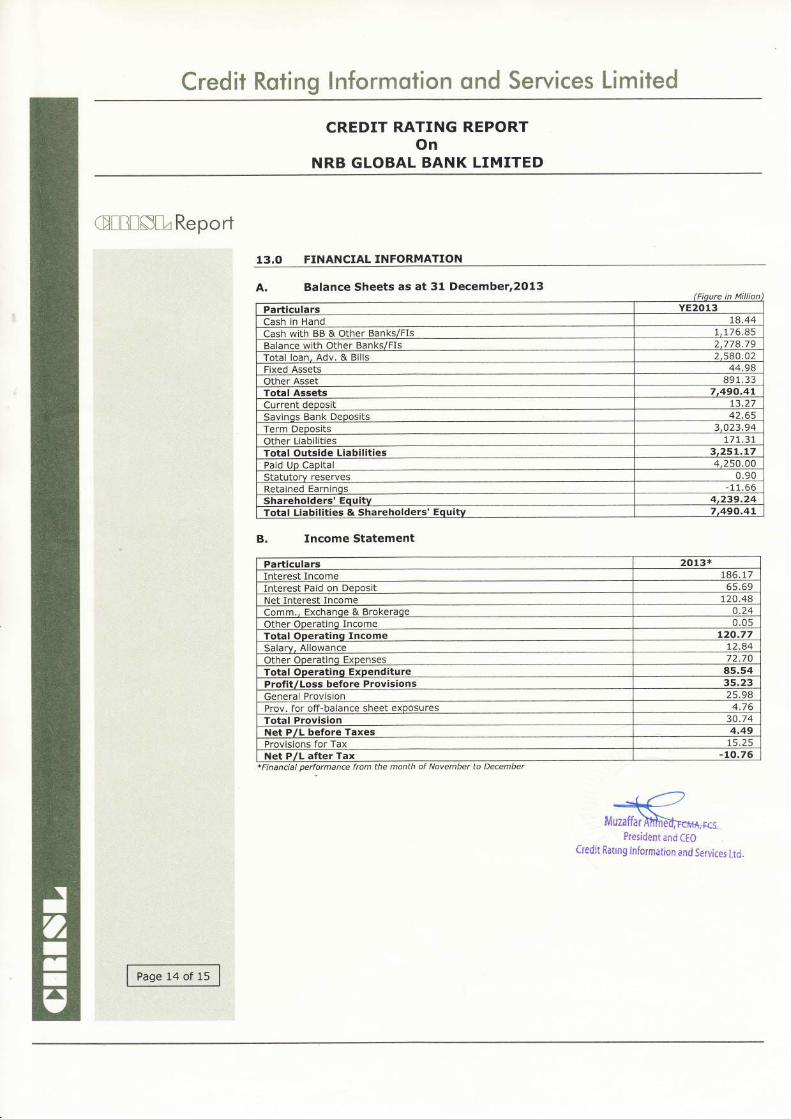

13.O FINANCIAL INFORMATION

A. Balance Sheets as at 31 Decemberr20l3

B. Income Statement

*Financial performance from the month of November to December

{redit fiatl;rE Inforrnation anC Serviees l-td.

Fiqure in Million

Particulars YE2013Cash in Hand L8.44Cash with BB & Other Banks/Fls 1,176.85Balance with Other Banks/Fls 2,778.79Total loan. Adv. & Bills 2,580. 0 2

Fixed Assets 44.98Other Asset 891.33Tota! Assets 7,490.4tCurrent deposit !3.27Savinos Bank Deposits 42.65Term Deposits 3,023.94Other Liabilities L71.37Total Outside Liabilities 3,25L.L7Paid Up Capital 4,2 50.00Statutory reserves 0 .90

Retained Earninqs - 11 .66

Shareholders' Equity 4,239.24Total Liabilities & Shareholders' Equity 7,490.4L

Pa rticu la rs 2013 x

Interest Income T86,L7Interest Paid on Deposit 65.69Net Interest Income L20.48Comm., Exchanqe & Brokeraqe 0.24Other Operatinq Income 0.0sTotal Ooeratinq Income L20,77Salarv, Allowance T2.84Other Operatinq Expenses 72.70Total Operatinq Expenditure 85.54Profit/Loss before Provisions 35.23General Provision 25.98Prov. for off-balance sheet exposures 4.7 6

Total Provision 30.74Net P lL before Taxes 4.49Provisions for Tax L5.25

Net P lL after Tax -LO.76

&luxaffarMPresiil*nt ar:d {[0

Credit lnforrnation ond Services LimitedRotinE

CREDTT RATING REPORTOn

NRB GLOBAL BANK LIMITED

GIBIS&ReportCRISL RATING SCALES AND DEFINITIONS

For long-term ratings, CRISL assigns + (Positive) sign ta indicate that the issue is rankedgeneric rating category and - (Minus) sign to indicate that the issue is ranked at the bottomcategory, Long-term ratings without any sign denote mid-levels of each group.

at the upper-end of itsend of its generic rating

LONG-TERM . BANKSRATING DEFINITION

AAATriple A(HighestSafetv)

Bank rated in this category is adjudged to be of best quality, offerhighest credit quality. Risk factors are negligible and risk free, nearestbonds and securities. Changing economic circumstances are unlikely toon this cateqory of banks.

highest safety and haveto risk free Governmenthave any serious impact

AA+, AA, AA-(Double A)

(High Safety)

Bank rated in this category is adjudged to be of high quality, offer higher safety and have highcredit quality. This level of rating indicates a corporate entity with a sound credit profile andwithout significant problems. Risks are modest and may vary slightly from time to time becauseof economic conditions.

A+, A, A-Single A

(AdequateSafety)

Bank rated in this category is adjudged to offer adequate safety for timely repayment offinancial obligations. This level of rating indicates a corporate entity with an adequate creditprofile. Risk factors are more variable and greater in periods of economic stress than thoserated in the higher categories.

BBB+, BBB,BBB-

Triple B(Moderate

Safetv)

Bank rated in this category is adjudged to offer moderate degree of safety for timely repaymentof financial obligations. This level of rating indicates that a bank is under-performing in someareas. These entities are however, considered to have the capability to overcome the above-mentioned limitations with special care and cautious operation" Risk factors are more variable inoeriods of economic stress than those rated in the hiqher cateqories.

BB+, BB, BB-Double B

(InadequateSafetv)

Bank rated in this category is adjudged to lack of keyinadequate safety. This level of rating indicates a banklikely to meet obligations when due. Overall quality maycateoorv.

protection factors, which results in anas below investment grade but deemedmove up or down frequently within this

B+, B, B-Single B(Risky)

Bank rated in this category is adjudged to be with high risk. Timely repayment of financialobligations is impaired by serious problems which the entity is faced with. Whilst an entity ratedin this category might be currently meeting obligations in time, continuance of this woulddepend upon favorable economic conditions or on some deqree of external support,

ccc+,ccc,ccc-

Triple C(Vulnerable)

Bank rated in this category is adjudged to be with vulnerable protection factors. I his ratingindicates that the degree of certainty regarding timely payment of financial obligations isdoubtful unless circumstances are favourable,

cc+rcc, cc-Double C(Hishly

Vulnerable)

adjudged to be with high vulnerable position. This rating indicatesregarding timely payment of financial obligations is quite lowerare favourable or there is possibility of high degree external

Bank rated in this category isthat the degree of certaintyunless overall circumstancessuooort.

c+, c, c-(Near toDefault)

Bank rated in this category is adjudged to be with near tofinancial obligations, This type rating may be used to coverpetition has been filed or similar action has been taken, butbeinq continued with hiqh degree of external support.

default in timely repayment ofa situation where a insolvencypayments on the obligation are

D(Default)

Bank rated in this category is adjudged todefault. This level of rating indicates thatobligations and calls for immediate external

be either currently in default or expected to be inthe entity is unlikely to meet maturing financial

support of a high order,

SHORT-TERM . BANKS

sT-1

Highest GradeHighest certainty of timely payment. Short-term liquidity including internal fundgeneration is very strong and access to alternative sources of funds is outstanding,Safety is almost like risk free Government short-term obliqations.

sT-2High GradeHigh certainty of timely payment. Liquidity factors are strong and supported by goodfundamental protection factors. Risk factors are verv small.

sT-3

Good GradeGood certainty of timely payment. Liquidity factors and company fundamentals aresound" Although ongoing funding needs may enlarge total financing requirements,access to capital markets is qood. Risk factors are small.

sT-4Moderate GradeModerate liquidity and other protection factors qualifyfactors are larqer and subiect to more variation,

issues as to invest grade. Risk

sT-5

Non-Investment GradeSpeculative investment characteristics. Liquiditydisruption in debt service. Operating factors andhigh degree of variation"

is not sufficient to insure againstmarket access may be subject to a

sr-6 DefaultIssuer failed to meet scheduled principal and/or interest payments.

,.1 .*::', : i,t*.i, *: * r.1. :CsPresidont and (€CI

(redi-t fiatrng Informatlon and Services Ltd,

'"'. i ' irr-- '''--c n*a

"iilii[ciit'r,- ";"-l-'-ijr '

-'' i#i...#;nii#il= -,ii;Hil .,I#,ffi....Iiffi".#I'#, '

"=idri,b#:bs'a#i.a+Caui 6ffiMiiui:i:*.iiia:d o,e#'=, , -'=. ; r i-:-"= -"]'.f.*,[1[ffiiJli*. E;i:6d,,ffi=

-= ---'rY!rrj -Y'Yi-:'+;r

-, o',*'''- -;'' .-'ffb't-w bhi$rbd,c '" -" -r i;-'ir;r' +"1 :L i"r**