Roundtable 2007 cohen

54

1 A Perspective on Newspapers in the Digital Age Bob Cohen President & CEO Scarborough Research ASTECH/INMA Roundtable on Strategic Marketing Vail, Colorado August 27, 2007

-

Upload

smartfocusworld -

Category

Business

-

view

433 -

download

0

description

Transcript of Roundtable 2007 cohen

1

A Perspective on

Newspapers in the

Digital Age

Bob Cohen President & CEO

Scarborough Research

ASTECH/INMA

Roundtable on Strategic Marketing

Vail, Colorado

August 27, 2007

2

Agenda:

Marketing

The Internet

Media

The Consumer

Newspapers

Strategic overview of media and marketing trends with implications for newspapers

3

Scarborough Research

●Comprehensive, syndicated annual survey of 81 local markets; national study (USA+)

●Annual sample of 220,000+ Adults (18+) ●Local market samples from 2,000-11,000 ●Continuous Measurement ●Measures demographics, shopping/retail

behavior, product consumption, entertainment/leisure, media usage

●Ratings service to the newspaper industry ●Accredited by the Media Ratings Council

●Valid, reliable, effective

4

MARKETING

5

The Marketing Environment

• Markets and brands are maturing, becoming more competitive

– Globalization, rapid pace of product innovation

• Increasing emphasis on ROI

• The Internet highlights improved model of feedback, accountability and efficiency

• Improved targeting of prospects

• Increasing advertiser/price pressure on media due to oversupply

– Media risks becoming ―inventory‖

• Increasing Automation

6

Marketers Are Challenged By the New Landscape

• Multi-channel/platform environment is more complex, as consumers have more choices

• More emphasis on managing the overall ―marketing mix‖

– Brands working across delivery channels

• Aggressively exploring new options

– Product placement; branded entertainment – Word-of-mouth (rediscovered) – Viral marketing, blogs; social networks – Non-traditional OOH (Out-Of-Home) venues: airports,

stadiums, in-store, malls, elevators, gas pumps – Wireless/mobile messaging – Online video – Consumer-Generated Media and CGLM

• Structure and role of advertising agencies being re-invented

7

Marketing: Accountability Leads to Focus on ROI Metrics • Seeking higher and more identifiable return on media investment

• Emphasis on ―engagement‖- with media, advertising creative and brands

• Useful orienting concept

• Re-examining consumers’ relationships with all media

– Time, involvement, participation, commitment

• Desire to improve on established metrics

• Emphasis on creating more effective ―consumer experiences‖

• Ultimate Objective: To link increased consumer engagement to sales

8

―Engagement is turning on a

prospect to a brand idea

enhanced by the

surrounding context.‖

-Advertising Research Foundation M14 Committee, March 21, 2006

9

― …Consumers’ decision making and buying behavior are driven more by unconscious thoughts and feelings…include ever-changing memories, metaphors, images, sensations, and stories that all interact with one another in complex ways to shape decisions and behavior.‖

-Gerald Zaltman, How Customers Think: Essential

Insights

Into the Mind of the Market

(Harvard Business School, 2003), pp.14-15

• Renewed emphasis on what consumers bring to advertising

• Relevant progress in field of neuroscience

10

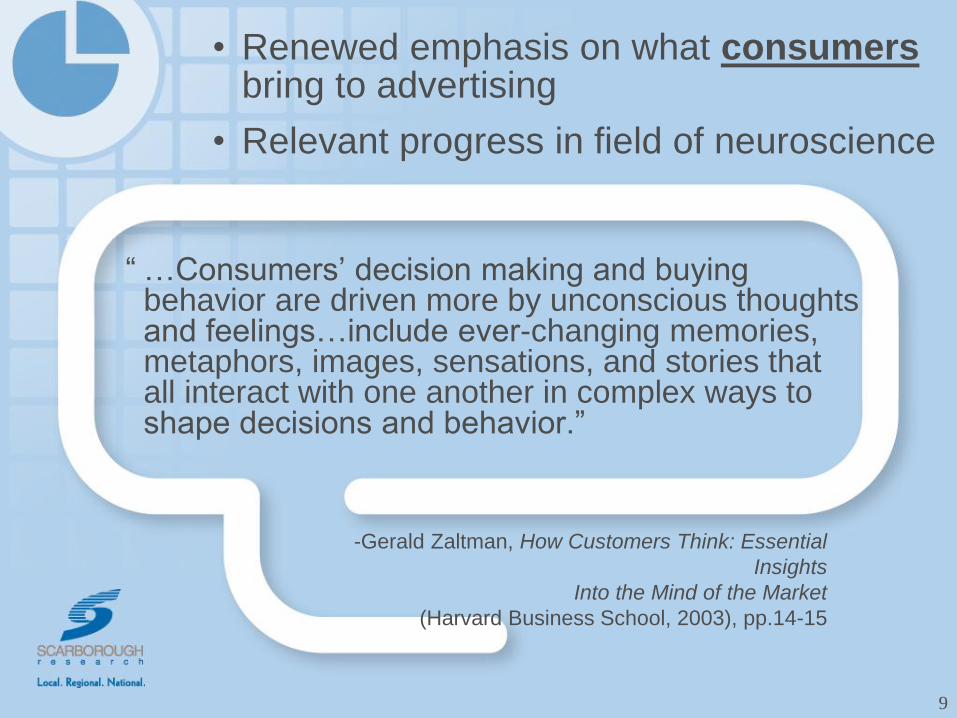

Magazines, $13.6,

(5.5%)

Newspaper,

$45.8, (18.5%)

Radio, $20.1,

(8.1%)Out Of Home,

$7.1, (2.9%)

Broadcast TV,

$47.6, (19.2%) Direct Mail,

$61.6, (24.9%)

Cable TV, $26.2,

(10.6%)

Internet, $10.6,

(4.3%)

Yellow Pages,

$14.7, (5.9%)

Source: Universal McCann, 2007

Forecast for Advertising Expenditures by Media in 2007: ($247 Billion)

11

-1.0% -1.5% -2.0%

3.0%4.2% 4.9% 6.0%

29.0%

-0.05

0

0.05

0.1

0.15

0.2

0.25

0.3

0.35

Local

TV National

TV

National

Newspap

er

Syndicat

ed TV Overall Magazin

es Cable TV Online

Where is the Growth? Zenith Forecast: US % Change for Select Media

Zenith Media, December 2006

12

THE INTERNET

13

Our mission: To connect people

to their passions, their communities

and the world’s knowledge.

14

Our mission: To organize the world’s

information and make it universally

accessible and useful.

15

The Internet is Revolutionizing Media and Marketing • Still at a very early stage of development

(Web 2.0)

• Profound influence within a relatively short period of time

• Impacting how consumers are informed, entertained, shop and socialize

• Creating a ―flat‖ world (global competitive playing field is being leveled)

16

Broadband Connectivity Continues to Grow

Source: Scarborough Research, Scarborough USA+

Release 2 2006

Based on total adults who have accessed the Internet during the

past 30 days

Broadband is defined as having a cable modem or DSL

connection in the household

29 29

38 39

30

49 51

60 62

23

44

54

0

10

20

30

40

50

60

70

18 - 34 35 - 54 55 +

2003 2004 2005 2006

17

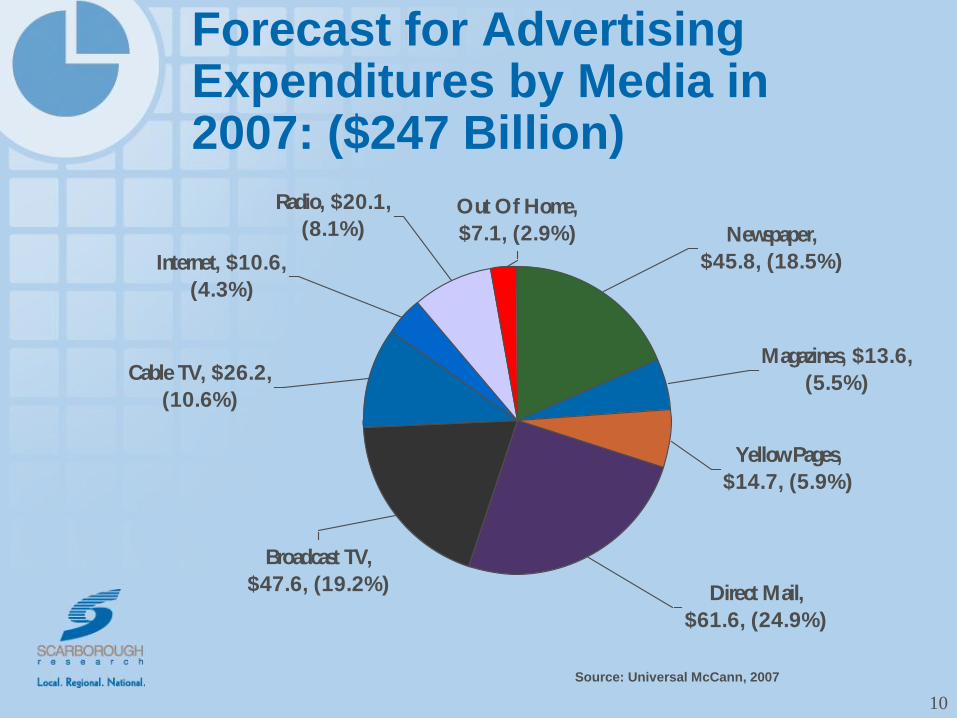

Source: Scarborough Research, Scarborough USA+ Release 2 2006;

Markets ranked by broadband penetration.

Broadband Incidence Varies Across Local Markets in the U.S.

0

10

20

30

40

50

60 Of Boston adults, 55% live in

a HHLD with a broadband

connection Austin

50%

Chicago

Phoenix 44%

Fresno

26%

Oklahoma

City 40%

NY

47%

18

Internet Users Go Online for Many Reasons

Based on consumers who accessed the Internet during the past 30 days

Source: Scarborough Research, Scarborough New York Release 1 2007 (March 2006 – February 2007)

Household/Personal

Tasks

News/Information

Entertainment

Consumer Shopping

90

49

44 39

31

26

25

24 22

21

21

20

19

17 16

16

7

7

6 5

3

Weather

News

Pay bills

Download music/listen to audio

Travel reservations

Financial info

Sports scores

Games

Download/watch video

Medical info

Auction site

Job search

Real estate listings

Blogs (read/contribute)

Automobile info

Download/watch movies

Casino-type games

Fantasy sports

Download video games

Download podcasts

19

Source: Scarborough Research, Scarborough USA+ Release 2 2002-2006 Based on total adults who accessed the Internet during the

past 30 days

Consumers are Gradually Spending More $$ Online

$465$454$446$410$384

$0

$100

$200

$300

$400

$500

$600

2002 2003 2004 2005 2006

Median Amount Spent on Internet Purchases Past 12 Months

20

Source: Scarborough Research, Scarborough USA+ Release 2 2004-2006 Based on total adults who accessed the Internet during the

past 30 days

Consumers are Gradually Spending More Time Online

5.915.545.07

0

2

4

6

8

10

2004 2005 2006

Median Time Spent Online

(Weekly)

Hours

21

Items Purchased Online

Within the Past Year

Based on total adults who accessed the Internet during the past 30 days Source: Scarborough Research,

Scarborough USA+ Release 2 2006

Consumers Are Buying Online Across Many Categories

2445

76769

1722

2525

64

255677889

21

272829

70

0

10

20

30

40

50

60

70

80

Any

Interne

t purc

hase

Airline

tick

ets

Book

s

Clothin

g or accessorie

s

Other

travel r

eservatio

ns

Toys or g

ames

Consum

er ele

ctron

ics

Hea

lth and

bea

uty ite

ms

Cultu

ral e

vent ti

ckets

Mov

ie tic

kets

Sportin

g ev

ent t

ickets

Sports

logo

app

arel

Pet s

upplies

Vehic

le

2003 2006

22

The Increasing Impact of „Search‟ • The Internet makes marketing

more efficient

• Search provides business with an efficient and less expensive way to find leads

• An increasing percentage of search is ―local‖

• We are increasingly searching to find that which we do not know

• Search will dominate on-line ad spending (Jupiter, 2006)

John Battelle, The Search: How Google and Its Rivals

Rewrote

the Rules of Business and Transformed our Culture

(Portfolio, 2005)

23

• New delivery platforms for content

• Adding new types of content

• Evolving into other realms: visual, oral, written

• Creating new dynamic relationships

• Emphasis on multi-platform

• Personalization opportunities

• Introduces new challenges and opportunities for branding

• More multi-tasking

• Impacting audience size and composition

Established Media Being Impacted by the Internet

24

MEDIA

25

Media is in Unprecedented Flux – A Period of Unsettling and Accelerated Pace of Change • Increasing innovation and experimentation

– New content, channels and media experiences

– New business models, partnerships

• Media organizations vary in their abilities to evolve and compete

– Legacy, culture, structure, resources and marketplace assessment

• Financial models changing

• Consolidation

26

Historically, Media Development in the United States has Evidenced… • Greater openness and transparency in the public sphere

• Higher levels of commercialization

• Greater decentralization

• Increasingly rapid extension and pervasive penetration of communication networks

• Greater receptivity to new products and technologies

–Paul Starr, The Creation of the Media: Political Origins of Modern Communications, (Basic Books,2004)

27

Source: Scarborough Research 1996-2006, Top 50 Markets

Newspaper Print Audiences Steadily

Declining, Especially Among Younger

Consumers

Read Any Daily Newspaper (Yesterday)

18-34 35-44 45-54 55-64 65+

40

60

80

100

20

1996 1999 2002 2005 2006

36.0 41.5 42.3

46.4

58.7

46.4 50.5

53.2

62.3 60.2 65.4

56.0

67.4 65.4 69.7 61.4

71.5 72.9 71.2 67.9

34.5

43.8

53.7

60.0

67.6

28

Source: Scarborough Research 1996-2006, Top 50 Markets

Average Daily Readership is

Declining at a Faster Rate than

Cume Readership

68.4

77.674.9

70

74

48.950.5

54.856.2

58.9

40

50

60

70

80

1996 1999 2002 2005 2006

Daily Cume Daily Average

- 9.2

(11.9%)

- 10.0

(17.0%)

29

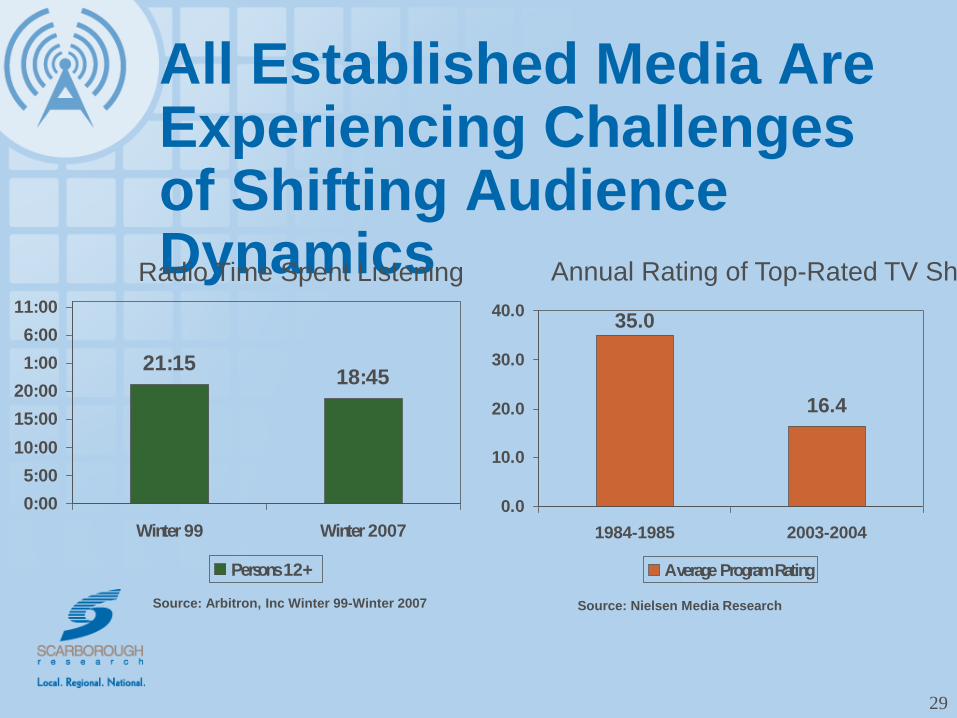

All Established Media Are Experiencing Challenges of Shifting Audience Dynamics

21:1518:45

0:00

5:00

10:00

15:00

20:00

1:00

6:00

11:00

Winter 99 Winter 2007

Persons 12+

Source: Nielsen Media Research

Radio Time Spent Listening Annual Rating of Top-Rated TV Show

Source: Arbitron, Inc Winter 99-Winter 2007

16.4

35.0

0.0

10.0

20.0

30.0

40.0

1984-1985 2003-2004

Average Program Rating

30

The Historical Barriers to Human Communication are Rapidly Diminishing Geographical

Time

Money

Social Class/Culture

31

TiVo/DVR/

“SLING BOXES”

DIGITAL OUT-OF-HOME

ADVERTISING

SATELLITE RADIO HD RADIO HIGH DEFINITION TV

PDA‟s iPODS

And more “new” media delivery options continue to enter

the marketplace…

CELL/MOBILE

PHONES

APPLE iPHONE VIDEO GAMES

32

Source: Scarborough Research, Scarborough USA+ Release 2 2006 Based on total

adults

Younger Adults are Early Adopters of New Services

12 10 10 82

7 8 6 7 72 3 3 4 5

13

222425

72

1

1520

17

74

61

58

98

0

20

40

60

80

100

Wire

less S

ubscr

iber

Camera

/pict

ure tak

ing

Dow

nload

ring

tone

s

Insta

nt m

essagin

g

Pictu

re m

essagin

g

Interne

t

Dow

nload

video

gam

es

E-ma

il

Push To Ta

lk - 2

way

Stream

vide

o clips

18-34 35-54 55+

Wireless Features Currently Use

33

THE CONSUMER

34

―Keeping the consumer at the center of the decision-making process is key to identifying solutions to the challenges all of us face in a world that is increasingly more fragmented due to the multiple ways media are consumed.‖

-Jim Stengel, Global Marketing Officer, ―P&G‖

ANA Marketing Musings,

September 13, 2005

The Consumer

• World of greater instability, uncertainty and stress

• Globalization, a shrinking and inter-dependent planet (―the new normal‖)

• Economic anxiety, greater $ inequality

• Political polarization

• Increasing ethnic diversity

• Generational dynamics

• Technology as ―fact of life‖

• Environmental focus

35

• Need for community, connections and security

• Hunger for leadership and ―moral compass‖

• Ongoing emphasis on personal choice & control

• Need for ―filters‖ and downtime

• Counterpoints of fantasy, experimentation and status

Resulting In…… Consumer Trends……

36

Marketers and Media Need to Respond to Demand for

Relevancy

and Cut Through Clutter w/o Alienating Consumers

But Concerns About Intrusiveness of Marketing Remain High

According to The 2005 Marketing Receptivity Survey

by Yankelovich Partners

• 54% of consumers try to resist being exposed or even paying attention to marketing and advertising

• 69% are interested in products that block/skip/opt out of marketing and advertising

• 56% avoid buying products that overwhelm them with marketing and advertising

“INTEGRITY IN MARKETING IS NOT

OPTIONAL”

Advertising Age, July 30, 2007

37

US Dept. of Commerce Reported eCommerce (by Quarter)

$0

$5

$10

$15

$20

$25

$30

$35

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q

Source: US Department of Commerce

$ billions

2002 2003 2004 2005 2006

38

NEWSPAPERS

39

68%

68%

73%

75%

76%

77%

74%

76%

76%

79%

60% 65% 70% 75% 80%

Read Past 5

Week Days

Read Past 4

Sundays

Adults 18+ Luxury Vehicle* European Trip* * HHI $75K+ College Grad+

Newspapers Continue to

Appeal to Upscale

Consumers

Source: Scarborough Research 2006, Scarborough USA + R2

2006

*Model type of any domestic/foreign vehicle owned or leased

(HHLD)

**Places visited outside continental U.S. past 3 years

40

Integrated Newspaper Audience • Newspapers are Successfully

Extending their Audience Online –Online exclusive audience is meaningful

and often growing, young and affluent

–Potential for net increase in newspaper reach overall

–Significant increase in online revenue

• Key success factors – Integration into the overall business

strategy

–Unique and specialized content

–Relentless cross promotion

–Leveraging strong established local media brands

41

Website Involvement Extends Newspaper Reach

Source: Scarborough Research, Local Market Studies, R12007

66.0 66.9 67.879.1 82.1

21.7 22.0 25.214.9 14.112.3 11.1 7.0 6.0 3.8

0%

100%

NY Times Atlanta

Journal-

Constitution

Washington

Post

Chicago

Tribune

Denver

Post/Rocky

Mountain

News

% o

f Tot

al A

udie

nce

Print Exclusive Print & Web Dual Website Exclusive

% DMA* REACH: (27.1%) (53.2%) (65.7%) (48.8%) (57.7%)

*Designated Market Area (DMA): Nielsen Media Research

defined geographical area based on television signal strength

42

Source: Scarborough Research, Local Market Studies, R2 2005, R12007

Dual

Web Excl

Print Excl

38.9 35.6

48.1 44.6

19.5 17.8

5.3 5.9

3.1 4.6

1.9 3

2.3 3.3

10.1 11.7

17.2 16.5

5.6 7.3

6.2 6 39.8 38.6

0

10

20

30

40

50

60

70

80

AJC 2005 2007

Wash Post Chic Trib NY Times 2005 2007 2005 2007 2005 2007

Total Audience

Growing Website Audience is Helping to Offset the Decline in Print Readership

54.3 53.2

-1.1%

68.4 65.7

-2.7%

47.4 48.8

+1.4%

28.1 27.1

-1.0%

-1.7%

-1.2% -3.5%

-3.3%

43

…Continued

52.347.4 45.6

39.1

56.249.7 48.3

42.4

6.48.2 10.0

12.6

6.410.4 11.7

12.2

1.42.2 3.7

5.4

1.4 2.6 3.65.2

-20

80

2005 2007 2005 2007 2005 2007 2005 2007

% o

f Tota

l A

udie

nce

Print Exclusive Print & Web Dual Website Exclusive

*Designated Market Area (DMA): Nielsen Media Research defined geographical area based on television

signal strength

Denver Post/

Rocky Mountain News

Arizona

Republic Kansas City

Star San Diego

Union-Tribune

Source: Scarborough Research, Local Market Studies, R2 2005, R12007

60.1% 57.7% 64.0% 62.7%

63.5% 59.9% 59.3% 57.1% -2.4% -2.2%

-1.3% -3.6%

-4.9% -6.5%

-6.5% -5.9%

44

Newspapers are Expanding the Footprint of the Media Brand

• Similar to all established media

• Development of a portfolio of print, online & video products to better reach the marketplace

• Aggregate audience for a total portfolio may actually be growing

45

Newspaper

Website

Spanish Language

Publication

Specialty

Publication

Print Classified

Sections

Online Classified Advertising

Local

Community

Newspaper DAILY

NEWSPAPER

“Part of our opportunity is having multiple platforms to reach the audience in our market…One at a time, they can be niche target opportunities; together they can form the new definition of mass.” - Hyde Post, Vice President, Internet, The Atlanta Journal-Constitution

46

Free vs. Paid Newspapers: Context

• Non-traditional publishers (e.g. Metro International)

•Strategy — Compete with traditional newspapers to capture current readers and non-readers

• Traditional paid newspapers publishing free dailies:

•Strategy — Capture non-readers, extend their audience and attempt to upsell to the paid product

•Encourage young people to develop a reading habit

47

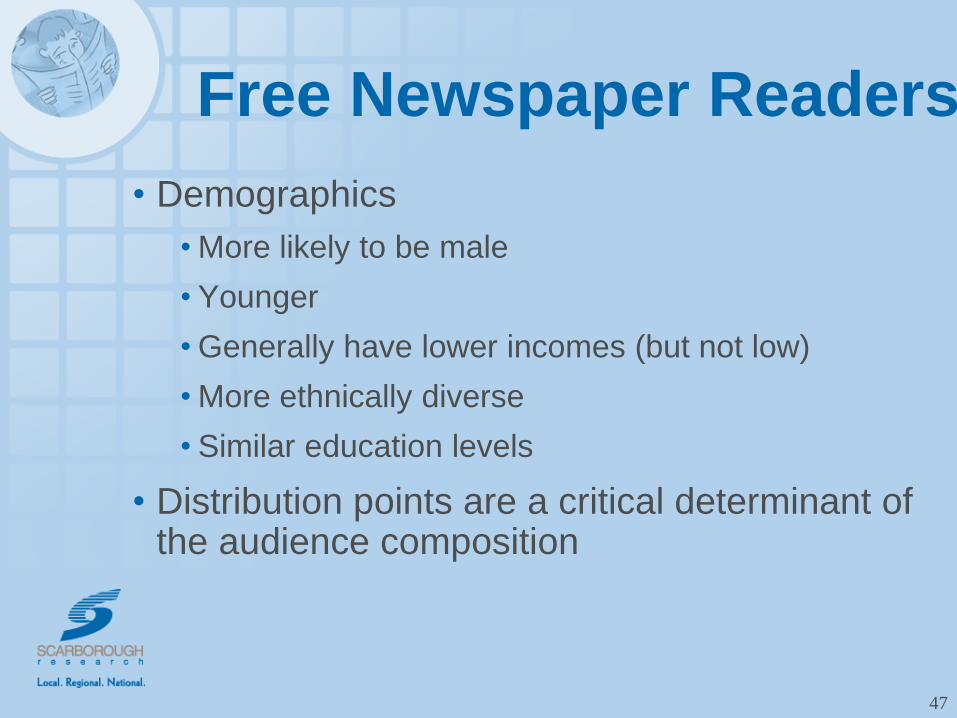

Free Newspaper Readers

• Demographics

• More likely to be male

• Younger

• Generally have lower incomes (but not low)

• More ethnically diverse

• Similar education levels

• Distribution points are a critical determinant of the audience composition

48

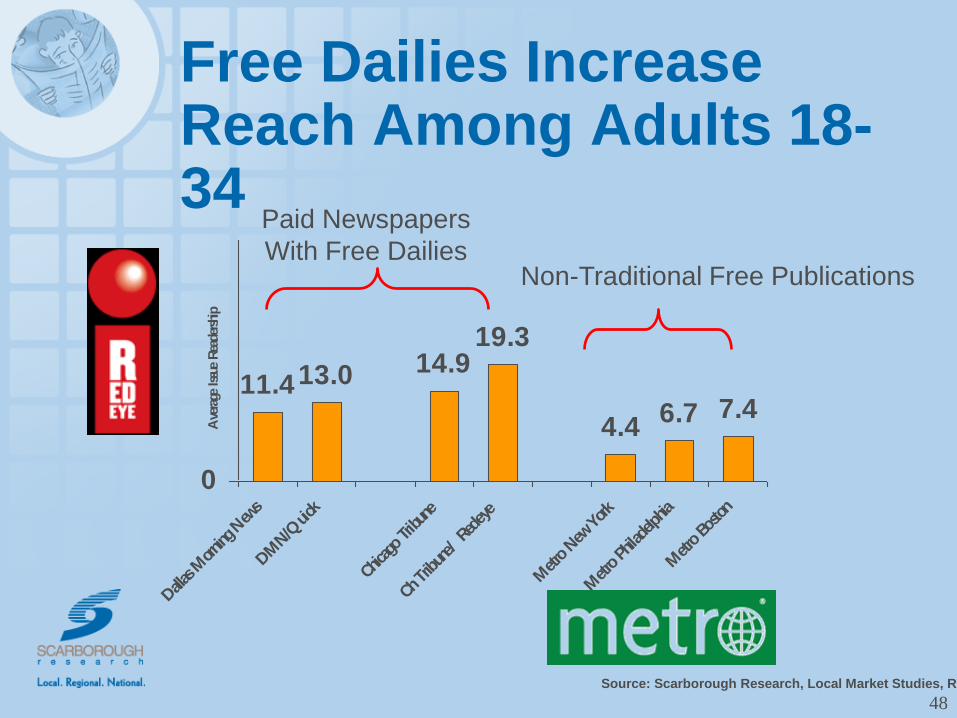

Free Dailies Increase Reach Among Adults 18-34

11.413.0 14.919.3

4.46.7 7.4

0

Dallas M

ornin

g New

s

DM

N/Q

uick

Chica

go Trib

une

Ch Trib

une/ R

edey

e

Metro N

ew Y

ork

Metro P

hilad

elphia

Metro B

oston

Ave

rage

Iss

ue R

eade

rshi

p

Source: Scarborough Research, Local Market Studies, R12007

Paid Newspapers

With Free Dailies Non-Traditional Free Publications

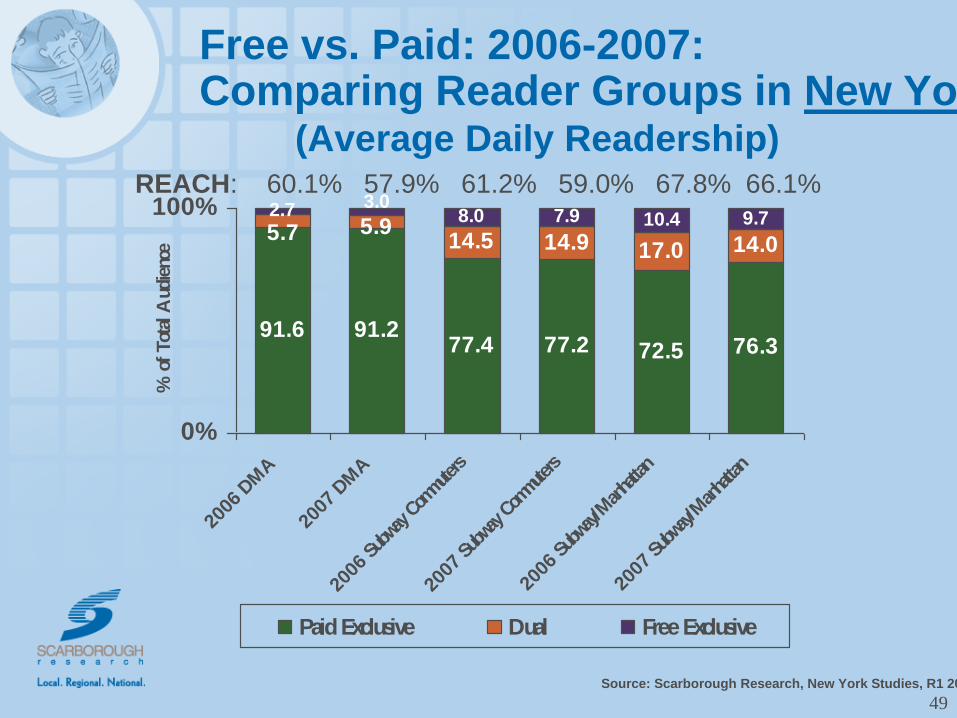

49 Source: Scarborough Research, New York Studies, R1 2006-2007

91.6 91.277.2 72.5 76.3

14.5 14.9 17.0 14.0

8.0 7.9 10.4 9.7

77.4

5.95.7

3.02.7

0%

100%

2006

DM

A

2007

DM

A

2006

Sub

way Co

mmuters

2007

Sub

way Co

mmuters

2006

Sub

way/M

anha

ttan

2007

Sub

way/M

anha

ttan

% o

f Tot

al A

udie

nce

Paid Exclusive Dual Free Exclusive

REACH: 60.1% 57.9% 61.2% 59.0% 67.8% 66.1%

Free vs. Paid: 2006-2007: Comparing Reader Groups in New York (Average Daily Readership)

50

The Relationship Between Free vs. Paid

• High levels of duplicated reading

• Free readers more likely to buy more than one paper

• Free newspapers’ exclusive readers are a relatively small group. No evidence (so far) that readers will ―trade up‖ to the paid paper.

• Free papers do not appear to cannibalize paid papers, suggesting a complementary relationship.

• Each local market will have its distinct issues and characteristics

51

Conclusion: Overall Implications For Newspapers • Understand print’s role in an evolving multi-media context

• Promote Total ―Integrated‖ Readership; sell across platforms

• Experiment, innovate, partner in different business models, assume greater risks

• Seek new ways of engaging readers, document these relationships to advertisers

• Position newspaper as part of a multi-media buy

52

…Overall Implications

• Leverage brand equity, community orientation, editorial authority

• Emphasize information with practical role, providing order and stability in people’s lives

• Value of good journalism may be less self-evident to some consumers – requires explanation and emphasis

• Environmental concerns likely to escalate

53

…Overall Implications

• Leverage Consumer Generated Local Media

–Likely to become a more important local/community factor, introducing new standards of journalism

–Even to ―hyper-local‖ level

–More two-way interactive relationships

• Tap into local networks to drive visitation to print/online papers

• Evolve appropriate business models