Roularta Media Group Market review and peer benchmarking · Key monthly insights Market review and...

18

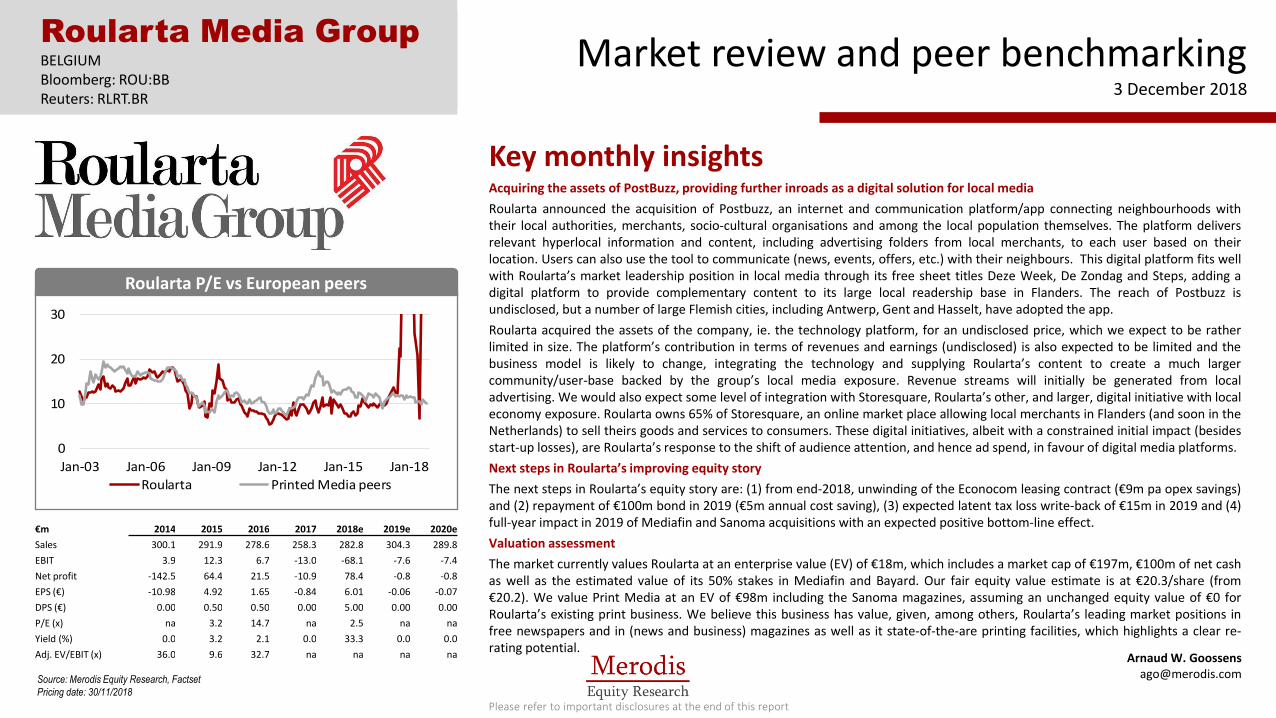

Key monthly insights Market review and peer benchmarking 3 December 2018 Acquiring the assets of PostBuzz, providing further inroads as a digital solution for local media Roularta announced the acquisition of Postbuzz, an internet and communication platform/app connecting neighbourhoods with their local authorities, merchants, socio-cultural organisations and among the local population themselves. The platform delivers relevant hyperlocal information and content, including advertising folders from local merchants, to each user based on their location. Users can also use the tool to communicate (news, events, offers, etc.) with their neighbours. This digital platform fits well with Roularta’s market leadership position in local media through its free sheet titles Deze Week, De Zondag and Steps, adding a digital platform to provide complementary content to its large local readership base in Flanders. The reach of Postbuzz is undisclosed, but a number of large Flemish cities, including Antwerp, Gent and Hasselt, have adopted the app. Roularta acquired the assets of the company, ie. the technology platform, for an undisclosed price, which we expect to be rather limited in size. The platform’s contribution in terms of revenues and earnings (undisclosed) is also expected to be limited and the business model is likely to change, integrating the technology and supplying Roularta’s content to create a much larger community/user-base backed by the group’s local media exposure. Revenue streams will initially be generated from local advertising. We would also expect some level of integration with Storesquare, Roularta’s other, and larger, digital initiative with local economy exposure. Roularta owns 65% of Storesquare, an online market place allowing local merchants in Flanders (and soon in the Netherlands) to sell theirs goods and services to consumers. These digital initiatives, albeit with a constrained initial impact (besides start-up losses), are Roularta’s response to the shift of audience attention, and hence ad spend, in favour of digital media platforms. Next steps in Roularta’s improving equity story The next steps in Roularta’s equity story are: (1) from end-2018, unwinding of the Econocom leasing contract (€9m pa opex savings) and (2) repayment of €100m bond in 2019 (€5m annual cost saving), (3) expected latent tax loss write-back of €15m in 2019 and (4) full-year impact in 2019 of Mediafin and Sanoma acquisitions with an expected positive bottom-line effect. Valuation assessment The market currently values Roularta at an enterprise value (EV) of €18m, which includes a market cap of €197m, €100m of net cash as well as the estimated value of its 50% stakes in Mediafin and Bayard. Our fair equity value estimate is at €20.3/share (from €20.2). We value Print Media at an EV of €98m including the Sanoma magazines, assuming an unchanged equity value of €0 for Roularta’s existing print business. We believe this business has value, given, among others, Roularta’s leading market positions in free newspapers and in (news and business) magazines as well as it state-of-the-are printing facilities, which highlights a clear re- rating potential. Roularta Media Group BELGIUM Bloomberg: ROU:BB Reuters: RLRT.BR Arnaud W. Goossens [email protected] Please refer to important disclosures at the end of this report €m 2014 2015 2016 2017 2018e 2019e 2020e Sales 300.1 291.9 278.6 258.3 282.8 304.3 289.8 EBIT 3.9 12.3 6.7 -13.0 -68.1 -7.6 -7.4 Net profit -142.5 64.4 21.5 -10.9 78.4 -0.8 -0.8 EPS (€) -10.98 4.92 1.65 -0.84 6.01 -0.06 -0.07 DPS (€) 0.00 0.50 0.50 0.00 5.00 0.00 0.00 P/E (x) na 3.2 14.7 na 2.5 na na Yield (%) 0.0 3.2 2.1 0.0 33.3 0.0 0.0 Adj. EV/EBIT (x) 36.0 9.6 32.7 na na na na Source: Merodis Equity Research, Factset Pricing date: 30/11/2018 Roularta P/E vs European peers 0 10 20 30 Jan-03 Jan-06 Jan-09 Jan-12 Jan-15 Jan-18 Roularta Printed Media peers

Transcript of Roularta Media Group Market review and peer benchmarking · Key monthly insights Market review and...

Key monthly insights

Market review and peer benchmarking 3 December 2018

Acquiring the assets of PostBuzz, providing further inroads as a digital solution for local media

Roularta announced the acquisition of Postbuzz, an internet and communication platform/app connecting neighbourhoods with their local authorities, merchants, socio-cultural organisations and among the local population themselves. The platform delivers relevant hyperlocal information and content, including advertising folders from local merchants, to each user based on their location. Users can also use the tool to communicate (news, events, offers, etc.) with their neighbours. This digital platform fits well with Roularta’s market leadership position in local media through its free sheet titles Deze Week, De Zondag and Steps, adding a digital platform to provide complementary content to its large local readership base in Flanders. The reach of Postbuzz is undisclosed, but a number of large Flemish cities, including Antwerp, Gent and Hasselt, have adopted the app.

Roularta acquired the assets of the company, ie. the technology platform, for an undisclosed price, which we expect to be rather limited in size. The platform’s contribution in terms of revenues and earnings (undisclosed) is also expected to be limited and the business model is likely to change, integrating the technology and supplying Roularta’s content to create a much larger community/user-base backed by the group’s local media exposure. Revenue streams will initially be generated from local advertising. We would also expect some level of integration with Storesquare, Roularta’s other, and larger, digital initiative with local economy exposure. Roularta owns 65% of Storesquare, an online market place allowing local merchants in Flanders (and soon in the Netherlands) to sell theirs goods and services to consumers. These digital initiatives, albeit with a constrained initial impact (besides start-up losses), are Roularta’s response to the shift of audience attention, and hence ad spend, in favour of digital media platforms.

Next steps in Roularta’s improving equity story

The next steps in Roularta’s equity story are: (1) from end-2018, unwinding of the Econocom leasing contract (€9m pa opex savings) and (2) repayment of €100m bond in 2019 (€5m annual cost saving), (3) expected latent tax loss write-back of €15m in 2019 and (4) full-year impact in 2019 of Mediafin and Sanoma acquisitions with an expected positive bottom-line effect.

Valuation assessment

The market currently values Roularta at an enterprise value (EV) of €18m, which includes a market cap of €197m, €100m of net cash as well as the estimated value of its 50% stakes in Mediafin and Bayard. Our fair equity value estimate is at €20.3/share (from €20.2). We value Print Media at an EV of €98m including the Sanoma magazines, assuming an unchanged equity value of €0 for Roularta’s existing print business. We believe this business has value, given, among others, Roularta’s leading market positions in free newspapers and in (news and business) magazines as well as it state-of-the-are printing facilities, which highlights a clear re-rating potential.

Roularta Media Group BELGIUM Bloomberg: ROU:BB Reuters: RLRT.BR

Arnaud W. Goossens [email protected]

Please refer to important disclosures at the end of this report

€m 2014 2015 2016 2017 2018e 2019e 2020e

Sales 300.1 291.9 278.6 258.3 282.8 304.3 289.8

EBIT 3.9 12.3 6.7 -13.0 -68.1 -7.6 -7.4

Net profit -142.5 64.4 21.5 -10.9 78.4 -0.8 -0.8

EPS (€) -10.98 4.92 1.65 -0.84 6.01 -0.06 -0.07

DPS (€) 0.00 0.50 0.50 0.00 5.00 0.00 0.00

P/E (x) na 3.2 14.7 na 2.5 na na

Yield (%) 0.0 3.2 2.1 0.0 33.3 0.0 0.0

Adj. EV/EBIT (x) 36.0 9.6 32.7 na na na na

Source: Merodis Equity Research, Factset

Pricing date: 30/11/2018

Roularta P/E vs European peers

0

10

20

30

Jan-03 Jan-06 Jan-09 Jan-12 Jan-15 Jan-18

Roularta Printed Media peers

2

Monthly market review dashboard

Goals of this Dashboard

Follow-up to our coverage of Roularta which was launched in October 2015 (see below)

Tool to keep investors up to date with Roularta’s equity story as well as its valuation in a sector context

Update investors on recent company and sector news flow

Corporate calendar of Roularta’s upcoming announcements and events

Friday, 1 March 2019: Announcement of FY18 results (08.15AM CET; Analyst meeting at 2PM)

Access our recent research reports on Roularta:

“Back on its feet” (initiation), 14 October 2015

“When the going gets tough” (update), 28 August 2017

“October 2018 market review” (monthly dashboard), 5 November 2018

https://documentcloud.adobe.com/link/track?uri=urn:aaid:scds:US:166d49f3-bdff-45f4-8f08-764e3c9eb7ad

3

Company profile A domestic leader in high-quality print media

Roularta is Belgium's leading media company offering

(1) local weekly free newspapers in Flanders (Deze Week, De Zondag, Steps),

(2) nationwide weekly news, business and women magazines (Knack, Le Vif L'Express, Trends, Trends Tendance, Libelle/Femme d’Aujourd’hui and Flair and Feeling/Gael),

(3) internet platforms (Storesquare, Digilocal, Proxistore, own content websites) and

(4) a 50% JV stake in Mediafin, Belgium's leading daily business newspaper (De Tijd and L’Echo).

Combined group sales are almost entirely generated in Belgium through (1) Print Media Advertising (40% of group in 2017, ie. excluding the Sanoma acquisition), (2) Readers Market (subscriptions and newsstand sales) (28%), (3) Third-Party Printing (14%), (4) Internet advertising and related (10%) and (5) other sources of revenues (inc. Line Extensions) (8%). Roularta's consolidated accounts include the full contribution of its Print Media activity (advertising and readers market ex-Bayard, internet activity, line extensions and third-party printing). The 50% stakes in Mediafin and Bayard are equity-accounted. The company acquired the women magazines in an asset deal with Sanoma (June 2018), with sales in the region of €70m for a consideration of €25m. The company recently restated its business segmentation to include two activities: Media Brands (86% of group sales in 1H18) and Printing Services (14%).

Combined sales breakdown (2017) Shareholders Company description

Combined EBIT breakdown (2016) Consolidated EBIT breakdown (2017)

Source: Merodis, Factset

Print ad39%

Readership

27%

3rd-party printing

14%

Internet10%

Line extensions

8%

TV & Radio ad

2%

Family & related

72%

Bestinver8%

Treasury shares

5%

Free float15%

Medialaan73%

Print media & others

27%

Medialaan0%

Print media & others

100%

4

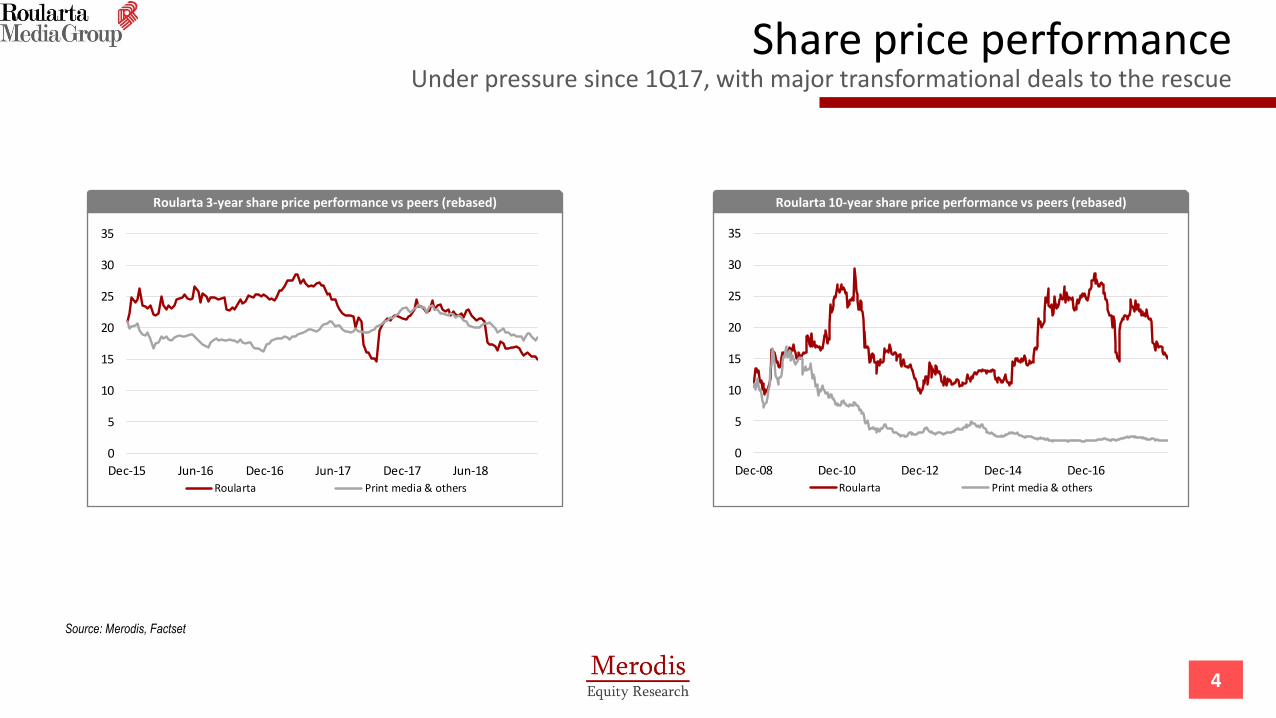

Share price performance Under pressure since 1Q17, with major transformational deals to the rescue

Source: Merodis, Factset

Roularta 3-year share price performance vs peers (rebased) Roularta 10-year share price performance vs peers (rebased)

0

5

10

15

20

25

30

35

Dec-08 Dec-10 Dec-12 Dec-14 Dec-16Roularta Print media & others

0

5

10

15

20

25

30

35

Dec-15 Jun-16 Dec-16 Jun-17 Dec-17 Jun-18Roularta Print media & others

Consensus EPS 2017-19 (€/share)

5

Analyst Recommendations, Earnings Expectations Consensus remains volatile, but stable in the past month

Source: Merodis, Factset

Consensus view

2018 consensus EPS estimates for Roularta are again flat m-o-m, still reflecting the weak results reported in August and the unexpected impairment which offset the capital gain from the disposal of the Medialaan stake. We adjusted our estimates in August, taking into account the 1H18 results.

Consensus currently expects a 2018e EPS of €-0.73 which is in line with our forecast (excluding the capital gain on Medialaan; €6.01 including the other one-time items), while 2019e consensus earnings are at €0.52 (flat m-o-m, but down 38% vs. August) vs. our forecast of €-0.06, mainly reflecting persistent top line weakness as well as start-up losses within the digital activities, which we expect to offset the full-year effect of the end of the leasing contract with Econocom (end-2018) and the repayment of the €100m bond (also end-2018).

Roularta’s share price was still under some pressure in November following the broader market sell-off of October. The stock is down 1.6% m-o-m in November following a sharper fall in October (-10%). The stock outperformed Print Media peers (-3.4% m-o-m), while underperforming the Euro Stoxx 600 (-1.1%) and Belgian SMCs (+0.2%). The share reached a new low over the last 12 months, at €14.65 (intraday on 28 November 2018), while its high during the year was €25.4 (26 February 2018).

Three brokers cover the stock, Degroof Petercam, KBC Securities and Kepler Chevreux (since September), with Factset indicating a Hold recommendation for the two latter and unchanged target prices of €17.50 and €17.90 respectively.

EPS Worms (€/share)

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

Dec-03 Dec-07 Dec-11 Dec-15

20062007200820092010201120122013201420152016201720182019

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

Mar-16 Sep-16 Mar-17 Sep-17 Mar-18 Sep-18

2018

2019

2020

Merodis Equity Research estimates (MERe) vs. consensus (%) Analyst recommendations vs. peer average

Jan-03 Jan-05 Jan-07 Jan-09 Jan-11 Jan-13 Jan-15 Jan-17

Roularta Sector average

Sell

Buy

MER vs Cns (%) 2018e 2019e 2020e

Sales -1.1 -2.5 -2.7

EBITDA 1.7 -75.3 -67.1

EBIT 37.8 2,812.4 na

EPS na na na

DPS 0.0 na na

Net debt 32,741.6 66.5 48.8

6

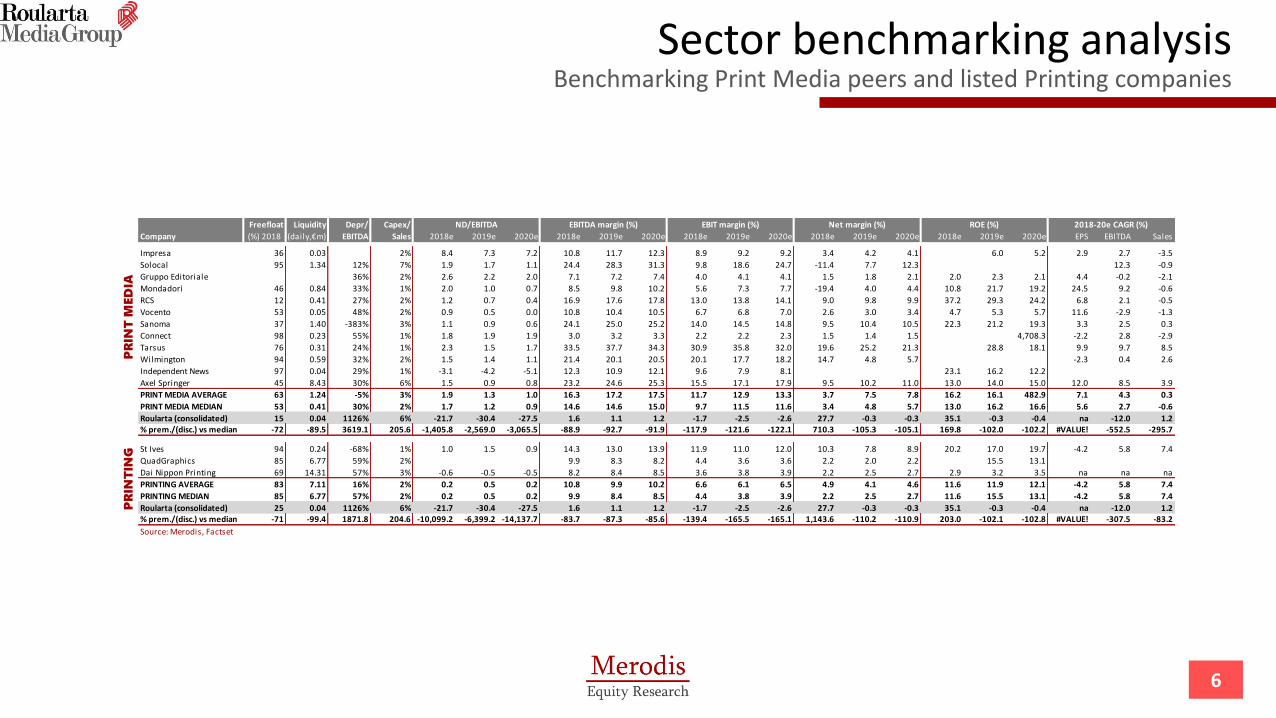

Sector benchmarking analysis Benchmarking Print Media peers and listed Printing companies

Freefloat Liquidity Depr/ Capex/

Company (%) 2018 (daily,€m) EBITDA Sales 2018e 2019e 2020e 2018e 2019e 2020e 2018e 2019e 2020e 2018e 2019e 2020e 2018e 2019e 2020e EPS EBITDA Sales

Impresa 36 0.03 2% 8.4 7.3 7.2 10.8 11.7 12.3 8.9 9.2 9.2 3.4 4.2 4.1 6.0 5.2 2.9 2.7 -3.5

Solocal 95 1.34 12% 7% 1.9 1.7 1.1 24.4 28.3 31.3 9.8 18.6 24.7 -11.4 7.7 12.3 12.3 -0.9

Gruppo Editoriale 36% 2% 2.6 2.2 2.0 7.1 7.2 7.4 4.0 4.1 4.1 1.5 1.8 2.1 2.0 2.3 2.1 4.4 -0.2 -2.1

Mondadori 46 0.84 33% 1% 2.0 1.0 0.7 8.5 9.8 10.2 5.6 7.3 7.7 -19.4 4.0 4.4 10.8 21.7 19.2 24.5 9.2 -0.6

RCS 12 0.41 27% 2% 1.2 0.7 0.4 16.9 17.6 17.8 13.0 13.8 14.1 9.0 9.8 9.9 37.2 29.3 24.2 6.8 2.1 -0.5

Vocento 53 0.05 48% 2% 0.9 0.5 0.0 10.8 10.4 10.5 6.7 6.8 7.0 2.6 3.0 3.4 4.7 5.3 5.7 11.6 -2.9 -1.3

Sanoma 37 1.40 -383% 3% 1.1 0.9 0.6 24.1 25.0 25.2 14.0 14.5 14.8 9.5 10.4 10.5 22.3 21.2 19.3 3.3 2.5 0.3

Connect 98 0.23 55% 1% 1.8 1.9 1.9 3.0 3.2 3.3 2.2 2.2 2.3 1.5 1.4 1.5 4,708.3 -2.2 2.8 -2.9

Tarsus 76 0.31 24% 1% 2.3 1.5 1.7 33.5 37.7 34.3 30.9 35.8 32.0 19.6 25.2 21.3 28.8 18.1 9.9 9.7 8.5

Wilmington 94 0.59 32% 2% 1.5 1.4 1.1 21.4 20.1 20.5 20.1 17.7 18.2 14.7 4.8 5.7 -2.3 0.4 2.6

Independent News 97 0.04 29% 1% -3.1 -4.2 -5.1 12.3 10.9 12.1 9.6 7.9 8.1 23.1 16.2 12.2

Axel Springer 45 8.43 30% 6% 1.5 0.9 0.8 23.2 24.6 25.3 15.5 17.1 17.9 9.5 10.2 11.0 13.0 14.0 15.0 12.0 8.5 3.9

PRINT MEDIA AVERAGE 63 1.24 -5% 3% 1.9 1.3 1.0 16.3 17.2 17.5 11.7 12.9 13.3 3.7 7.5 7.8 16.2 16.1 482.9 7.1 4.3 0.3

PRINT MEDIA MEDIAN 53 0.41 30% 2% 1.7 1.2 0.9 14.6 14.6 15.0 9.7 11.5 11.6 3.4 4.8 5.7 13.0 16.2 16.6 5.6 2.7 -0.6

Roularta (consolidated) 15 0.04 1126% 6% -21.7 -30.4 -27.5 1.6 1.1 1.2 -1.7 -2.5 -2.6 27.7 -0.3 -0.3 35.1 -0.3 -0.4 na -12.0 1.2% prem./(disc.) vs median -72 -89.5 3619.1 205.6 -1,405.8 -2,569.0 -3,065.5 -88.9 -92.7 -91.9 -117.9 -121.6 -122.1 710.3 -105.3 -105.1 169.8 -102.0 -102.2 #VALUE! -552.5 -295.7

St Ives 94 0.24 -68% 1% 1.0 1.5 0.9 14.3 13.0 13.9 11.9 11.0 12.0 10.3 7.8 8.9 20.2 17.0 19.7 -4.2 5.8 7.4

QuadGraphics 85 6.77 59% 2% 9.9 8.3 8.2 4.4 3.6 3.6 2.2 2.0 2.2 15.5 13.1

Dai Nippon Printing 69 14.31 57% 3% -0.6 -0.5 -0.5 8.2 8.4 8.5 3.6 3.8 3.9 2.2 2.5 2.7 2.9 3.2 3.5 na na na

PRINTING AVERAGE 83 7.11 16% 2% 0.2 0.5 0.2 10.8 9.9 10.2 6.6 6.1 6.5 4.9 4.1 4.6 11.6 11.9 12.1 -4.2 5.8 7.4

PRINTING MEDIAN 85 6.77 57% 2% 0.2 0.5 0.2 9.9 8.4 8.5 4.4 3.8 3.9 2.2 2.5 2.7 11.6 15.5 13.1 -4.2 5.8 7.4

Roularta (consolidated) 25 0.04 1126% 6% -21.7 -30.4 -27.5 1.6 1.1 1.2 -1.7 -2.5 -2.6 27.7 -0.3 -0.3 35.1 -0.3 -0.4 na -12.0 1.2% prem./(disc.) vs median -71 -99.4 1871.8 204.6 -10,099.2 -6,399.2 -14,137.7 -83.7 -87.3 -85.6 -139.4 -165.5 -165.1 1,143.6 -110.2 -110.9 203.0 -102.1 -102.8 #VALUE! -307.5 -83.2

Source: Merodis, Factset

PR

INT

ING

ROE (%) 2018-20e CAGR (%)

PR

INT

MED

IA

ND/EBITDA EBITDA margin (%) EBIT margin (%) Net margin (%)

7

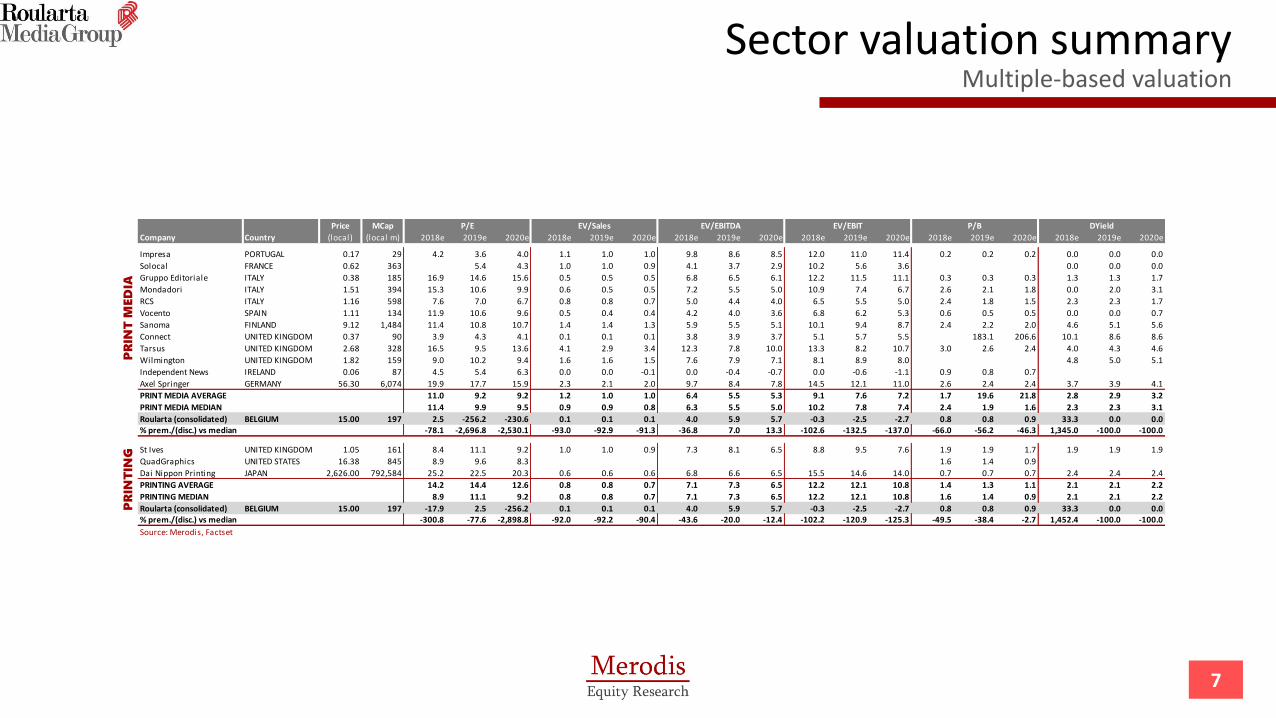

Sector valuation summary Multiple-based valuation

Price MCap

Company Country (local) (local m) 2018e 2019e 2020e 2018e 2019e 2020e 2018e 2019e 2020e 2018e 2019e 2020e 2018e 2019e 2020e 2018e 2019e 2020e

Impresa PORTUGAL 0.17 29 4.2 3.6 4.0 1.1 1.0 1.0 9.8 8.6 8.5 12.0 11.0 11.4 0.2 0.2 0.2 0.0 0.0 0.0

Solocal FRANCE 0.62 363 5.4 4.3 1.0 1.0 0.9 4.1 3.7 2.9 10.2 5.6 3.6 0.0 0.0 0.0

Gruppo Editoriale ITALY 0.38 185 16.9 14.6 15.6 0.5 0.5 0.5 6.8 6.5 6.1 12.2 11.5 11.1 0.3 0.3 0.3 1.3 1.3 1.7

Mondadori ITALY 1.51 394 15.3 10.6 9.9 0.6 0.5 0.5 7.2 5.5 5.0 10.9 7.4 6.7 2.6 2.1 1.8 0.0 2.0 3.1

RCS ITALY 1.16 598 7.6 7.0 6.7 0.8 0.8 0.7 5.0 4.4 4.0 6.5 5.5 5.0 2.4 1.8 1.5 2.3 2.3 1.7

Vocento SPAIN 1.11 134 11.9 10.6 9.6 0.5 0.4 0.4 4.2 4.0 3.6 6.8 6.2 5.3 0.6 0.5 0.5 0.0 0.0 0.7

Sanoma FINLAND 9.12 1,484 11.4 10.8 10.7 1.4 1.4 1.3 5.9 5.5 5.1 10.1 9.4 8.7 2.4 2.2 2.0 4.6 5.1 5.6

Connect UNITED KINGDOM 0.37 90 3.9 4.3 4.1 0.1 0.1 0.1 3.8 3.9 3.7 5.1 5.7 5.5 183.1 206.6 10.1 8.6 8.6

Tarsus UNITED KINGDOM 2.68 328 16.5 9.5 13.6 4.1 2.9 3.4 12.3 7.8 10.0 13.3 8.2 10.7 3.0 2.6 2.4 4.0 4.3 4.6

Wilmington UNITED KINGDOM 1.82 159 9.0 10.2 9.4 1.6 1.6 1.5 7.6 7.9 7.1 8.1 8.9 8.0 4.8 5.0 5.1

Independent News IRELAND 0.06 87 4.5 5.4 6.3 0.0 0.0 -0.1 0.0 -0.4 -0.7 0.0 -0.6 -1.1 0.9 0.8 0.7

Axel Springer GERMANY 56.30 6,074 19.9 17.7 15.9 2.3 2.1 2.0 9.7 8.4 7.8 14.5 12.1 11.0 2.6 2.4 2.4 3.7 3.9 4.1

PRINT MEDIA AVERAGE 11.0 9.2 9.2 1.2 1.0 1.0 6.4 5.5 5.3 9.1 7.6 7.2 1.7 19.6 21.8 2.8 2.9 3.2

PRINT MEDIA MEDIAN 11.4 9.9 9.5 0.9 0.9 0.8 6.3 5.5 5.0 10.2 7.8 7.4 2.4 1.9 1.6 2.3 2.3 3.1

Roularta (consolidated) BELGIUM 15.00 197 2.5 -256.2 -230.6 0.1 0.1 0.1 4.0 5.9 5.7 -0.3 -2.5 -2.7 0.8 0.8 0.9 33.3 0.0 0.0% prem./(disc.) vs median -78.1 -2,696.8 -2,530.1 -93.0 -92.9 -91.3 -36.8 7.0 13.3 -102.6 -132.5 -137.0 -66.0 -56.2 -46.3 1,345.0 -100.0 -100.0

St Ives UNITED KINGDOM 1.05 161 8.4 11.1 9.2 1.0 1.0 0.9 7.3 8.1 6.5 8.8 9.5 7.6 1.9 1.9 1.7 1.9 1.9 1.9

QuadGraphics UNITED STATES 16.38 845 8.9 9.6 8.3 1.6 1.4 0.9

Dai Nippon Printing JAPAN 2,626.00 792,584 25.2 22.5 20.3 0.6 0.6 0.6 6.8 6.6 6.5 15.5 14.6 14.0 0.7 0.7 0.7 2.4 2.4 2.4

PRINTING AVERAGE 14.2 14.4 12.6 0.8 0.8 0.7 7.1 7.3 6.5 12.2 12.1 10.8 1.4 1.3 1.1 2.1 2.1 2.2

PRINTING MEDIAN 8.9 11.1 9.2 0.8 0.8 0.7 7.1 7.3 6.5 12.2 12.1 10.8 1.6 1.4 0.9 2.1 2.1 2.2

Roularta (consolidated) BELGIUM 15.00 197 -17.9 2.5 -256.2 0.1 0.1 0.1 4.0 5.9 5.7 -0.3 -2.5 -2.7 0.8 0.8 0.9 33.3 0.0 0.0% prem./(disc.) vs median -300.8 -77.6 -2,898.8 -92.0 -92.2 -90.4 -43.6 -20.0 -12.4 -102.2 -120.9 -125.3 -49.5 -38.4 -2.7 1,452.4 -100.0 -100.0

Source: Merodis, Factset

PR

INT

ING

P/B DYieldEV/EBIT

PR

INT

MED

IA

P/E EV/EBITDAEV/Sales

EV/EBITDA ratio of Roularta vs. Print Media

8

P/E valuation relative to the sector A recent re-rating driven by an accounting impact and major digital investments which hurt profitability

Source: Merodis, Factset

Valuation

On consensus EPS estimates, Roularta shares trade at a P/E 12M forward of 37x, a 270% premium versus Print Media peers in Europe (from a 370% premium in October). Importantly, the volatility is due to the inclusion, within consensus, of the capital gain on the disposal of the Medialaan stake which has been largely offset by the value impairment of the magazine titles. In addition, profitability at Roularta is still expected to be negatively impacted by high start-up losses in the digital ventures as well as weak market conditions in the ad space for Roularta’s core activity.

As a reminder, Roularta has disposed of its stake in Medialaan, which means Roularta is now a Print Media pure play compared to the past when TV broadcasting (through Medialaan) was the main profit contributor and the key value driver of the stock (in 2016, 73% of Roularta’s EBIT and 80% of its EPS was generated by Medialaan). The rerating compared to the Print Media sector is driven entirely by the share price performance since October 2017 as well as the sharp cut in Roularta’s earnings estimates due to launching costs in digital initiatives such as Storesquare.

The Print Media sector is currently valued at 9.8x P/E 12M forward (vs. 10.4x previously, ie. a continued de-rating m-o-m) and at 5.5x EV/EBITDA 12M forward (vs. 5.0x previously), which compares to a LT average of 12.9x and 7.3x respectively. The historical valuation range for the sector is 7x-19x (P/E 12M forward) and 5x-11x (EV/EBITDA 12M forward), which suggest that the sector remains at the low-end of its historical range.

P/E ratio of Roularta vs. Print Media

EV/EBITDA Premium/(Discount) of Roularta vs. Print Media P/E Premium/(Discount) of Roularta vs. Print Media

0

10

20

30

Jan-03 Jan-06 Jan-09 Jan-12 Jan-15 Jan-18

Roularta Printed Media peers

-100%

-50%

0%

50%

100%

Jan-03 Jan-06 Jan-09 Jan-12 Jan-15 Jan-18

0

10

20

30

Jan-03 Jan-06 Jan-09 Jan-12 Jan-15 Jan-18

Roularta Printed Media peers

-100%

-50%

0%

50%

100%

150%

200%

Jan-03 Jan-06 Jan-09 Jan-12 Jan-15 Jan-18

9

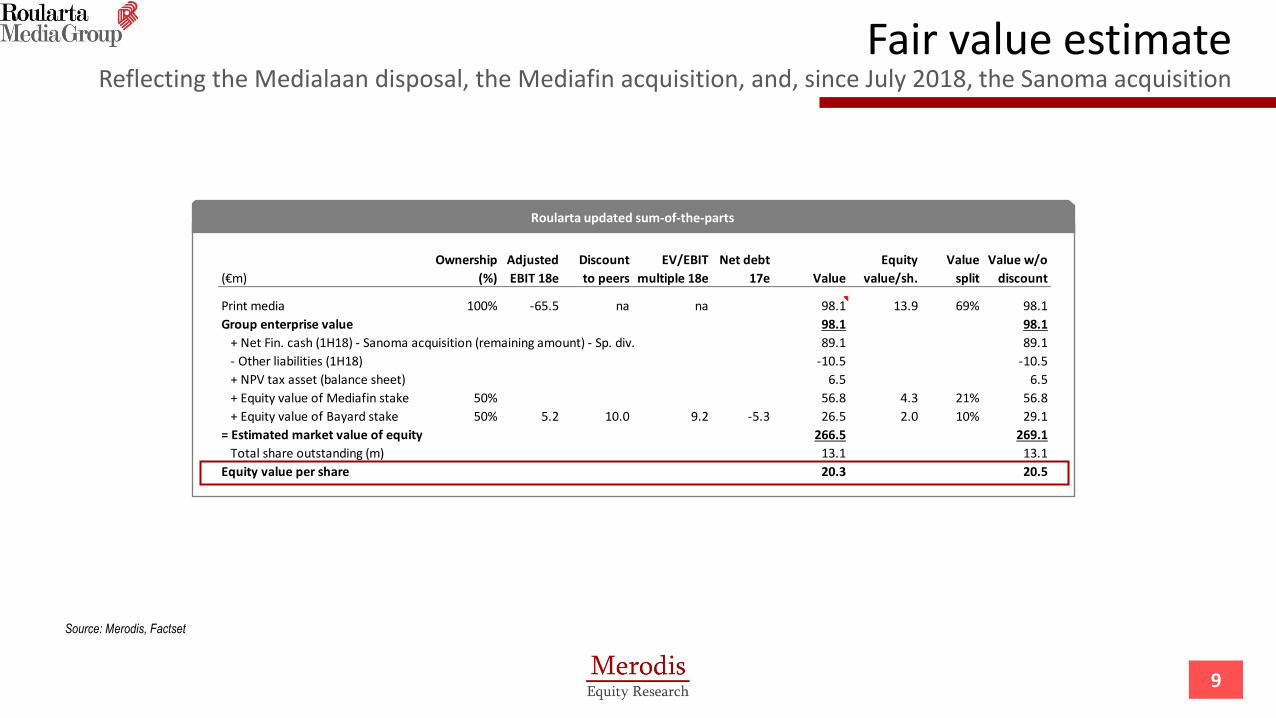

Fair value estimate Reflecting the Medialaan disposal, the Mediafin acquisition, and, since July 2018, the Sanoma acquisition

Source: Merodis, Factset

Roularta updated sum-of-the-parts

(€m)

Ownership

(%)

Adjusted

EBIT 18e

Discount

to peers

EV/EBIT

multiple 18e

Net debt

17e Value

Equity

value/sh.

Value

split

Value w/o

discount

Print media 100% -65.5 na na 98.1 13.9 69% 98.1

Group enterprise value 98.1 98.1

+ Net Fin. cash (1H18) - Sanoma acquisition (remaining amount) - Sp. div. 89.1 89.1

- Other liabilities (1H18) -10.5 -10.5

+ NPV tax asset (balance sheet) 6.5 6.5

+ Equity value of Mediafin stake 50% 56.8 4.3 21% 56.8

+ Equity value of Bayard stake 50% 5.2 10.0 9.2 -5.3 26.5 2.0 10% 29.1

= Estimated market value of equity 266.5 269.1

Total share outstanding (m) 13.1 13.1

Equity value per share 20.3 20.5

10

Valuation indicators

Source: Merodis, Factset

Print Media valuation correlation with expected EPS growth

Gruppo Editoriale

Mondadori

RCS

VocentoSanomaTarsus

Wilmington

0

2

4

6

8

10

12

14

16

18

20

0 5 10 15 20 25 30

P/E

19

e

EPS CAGR 2018-20e

PEG

5.0x

PEG

2.0x PEG

1.0x

Print Media sector valuation correlation with EBIT margins

y = 0.0821x - 0.0377R² = 0.8385

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

-10 0 10 20 30 40

EV

/Sa

les

19

e

EBIT margin (%) 19e

Roularta

Mediafin

2019 expected sales growth (%)

11

Sales growth expectations Impacted by cyclical and structural effects

Source: Merodis, Factset

Expected Sales Growth

At the end of November, consensus cut Print Media sector sales growth expectations for 2018 from -4.1% to -12.6% driven mainly by sharp downgrades at Independent News and Media (2018 sales expected at -22% y-o-y from -7.4% expected previously) as well as at Mondadori (2018 sales expected at -28% y-o-y from -2% expected previously). The latter is driven mainly by the expected disposal of Mondadori’s French activity (classified as a discontinued asset).

Consensus sales expectations for Roularta in 2018 are flat m-o-m, following a sharp increase in July and August with the inclusion of the Sanoma assets acquired in June 2018. Consensus now expects 9% sales growth.

As a reminder the announced disposal of Medialaan and acquisition of Mediafin have no impact on Roularta’s consolidated sales as the stakes are equity-accounted JVs.

The sector is suffering from the structural impact of online media gaining market share over traditional Printed Media and TV in terms of advertising revenues. This is driven by changes in viewership, which is moving from the traditional media to online.

2018 expected sales growth (%)

2019 expected sales growth, Roularta vs. peers 2018 expected sales growth, Roularta vs. peers

-40%

-30%

-20%

-10%

0%

10%

20%

Mar-15 Dec-15 Sep-16 Jun-17 Mar-18

ROU-BRU

IPR-LIS

IPDC-DUB

GEDI-IT

MN-MIL

VOC-MCE -10%

-5%

0%

5%

10%

15%

20%

Mar-15 Dec-15 Sep-16 Jun-17 Mar-18

ROU-BRU

IPR-LIS

IPDC-DUB

GEDI-IT

MN-MIL

VOC-MCE

-15%

-10%

-5%

0%

5%

10%

15%

Mar-15 Mar-16 Mar-17 Mar-18ROU-BRU Peer avg.

-10%

-5%

0%

5%

10%

Mar-15 Oct-15 May-16 Dec-16 Jul-17 Feb-18 Sep-18

ROU-BRU Peer avg.

2019 expected EBITDA growth (%)

12

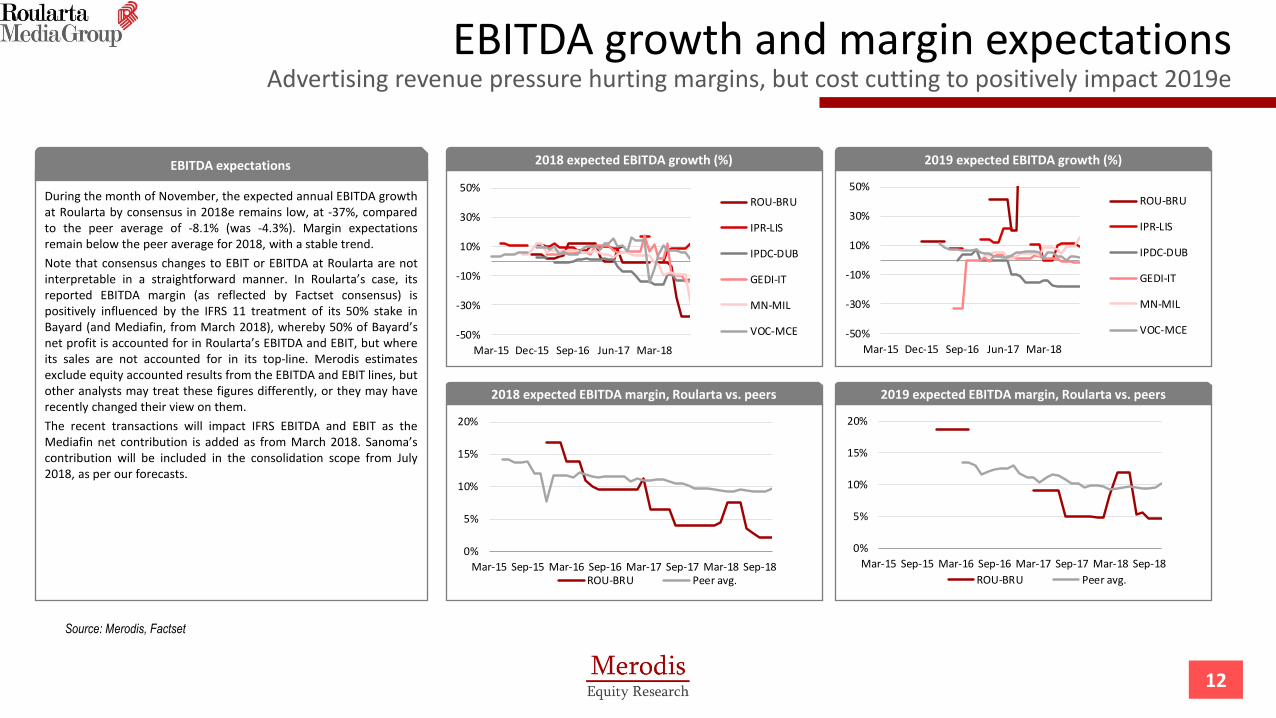

EBITDA growth and margin expectations Advertising revenue pressure hurting margins, but cost cutting to positively impact 2019e

Source: Merodis, Factset

EBITDA expectations

During the month of November, the expected annual EBITDA growth at Roularta by consensus in 2018e remains low, at -37%, compared to the peer average of -8.1% (was -4.3%). Margin expectations remain below the peer average for 2018, with a stable trend.

Note that consensus changes to EBIT or EBITDA at Roularta are not interpretable in a straightforward manner. In Roularta’s case, its reported EBITDA margin (as reflected by Factset consensus) is positively influenced by the IFRS 11 treatment of its 50% stake in Bayard (and Mediafin, from March 2018), whereby 50% of Bayard’s net profit is accounted for in Roularta’s EBITDA and EBIT, but where its sales are not accounted for in its top-line. Merodis estimates exclude equity accounted results from the EBITDA and EBIT lines, but other analysts may treat these figures differently, or they may have recently changed their view on them.

The recent transactions will impact IFRS EBITDA and EBIT as the Mediafin net contribution is added as from March 2018. Sanoma’s contribution will be included in the consolidation scope from July 2018, as per our forecasts.

2018 expected EBITDA growth (%)

2019 expected EBITDA margin, Roularta vs. peers 2018 expected EBITDA margin, Roularta vs. peers

0%

5%

10%

15%

20%

Mar-15 Sep-15 Mar-16 Sep-16 Mar-17 Sep-17 Mar-18 Sep-18ROU-BRU Peer avg.

0%

5%

10%

15%

20%

Mar-15 Sep-15 Mar-16 Sep-16 Mar-17 Sep-17 Mar-18 Sep-18

ROU-BRU Peer avg.

-50%

-30%

-10%

10%

30%

50%

Mar-15 Dec-15 Sep-16 Jun-17 Mar-18

ROU-BRU

IPR-LIS

IPDC-DUB

GEDI-IT

MN-MIL

VOC-MCE -50%

-30%

-10%

10%

30%

50%

Mar-15 Dec-15 Sep-16 Jun-17 Mar-18

ROU-BRU

IPR-LIS

IPDC-DUB

GEDI-IT

MN-MIL

VOC-MCE

2019 expected Payout, Sector

13

Consensus payout expectations Margin pressure and the Medialaan/Mediafin swap may impact the dividend strategy

Source: Merodis, Factset

Dividend payout

Roularta announced on 16 January 2018 that no ordinary dividend will be paid out on 2017 earnings, which compared to our previous forecast of €0.20/share. The company announced, however, a €5/share interim dividend (€63m pay out) which was paid out on 19 July 2018. The intention was to remunerate shareholders for the €145m capital gain on the Medialaan disposal which was closed in February 2018.

Roularta’s targeted pay-out ratio is 30%, which is in line with its average payout ratio prior to the acquisition in France of c32% (2002-2006) and broadly in line with the Sector average.

Consensus still expects Roularta to pay out a dividend in 2019e (contrary to MERe), with an expected payout of 14% (flat m-o-m).

The Mediafin acquisition and the Medialaan disposal is likely to have a negative impact on Roularta’s dividend outlay given the lower cash-generation potential of Mediafin vs. Medialaan. Given our forecast of losses in 2018e and 2019e, we do not expect any dividends soon despite the company’s solid balance sheet which holds an expected net cash position of €99m for 2018e.

2018 expected Payout, Sector

2019 expected payout, Roularta vs. Peers 2018 expected payout, Roularta vs. Peers

0

20

40

60

80

100

120

Mar-15 Mar-16 Mar-17 Mar-18ROU-BRU Peer avg.

0

10

20

30

40

50

Mar-15 Sep-15 Mar-16 Sep-16 Mar-17 Sep-17 Mar-18 Sep-18ROU-BRU Peer avg.

0

20

40

60

80

100

120

Mar-15 Dec-15 Sep-16 Jun-17 Mar-18

ROU-BRU

IPR-LIS

IPDC-DUB

GEDI-IT

MN-MIL

VOC-MCE 0

10

20

30

40

50

Mar-15 Dec-15 Sep-16 Jun-17 Mar-18

ROU-BRU

IPR-LIS

IPDC-DUB

GEDI-IT

MN-MIL

VOC-MCE

2019 NFD/EBITDA, sector

14

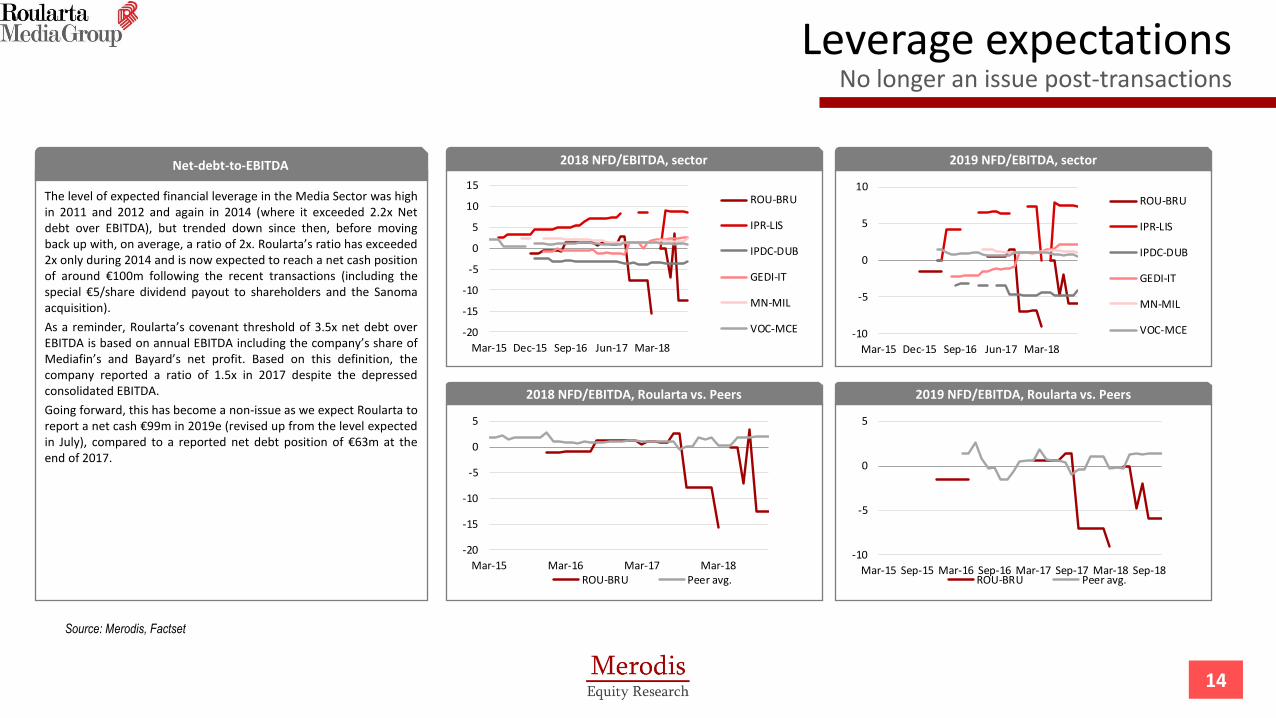

Leverage expectations No longer an issue post-transactions

Source: Merodis, Factset

Net-debt-to-EBITDA

The level of expected financial leverage in the Media Sector was high in 2011 and 2012 and again in 2014 (where it exceeded 2.2x Net debt over EBITDA), but trended down since then, before moving back up with, on average, a ratio of 2x. Roularta’s ratio has exceeded 2x only during 2014 and is now expected to reach a net cash position of around €100m following the recent transactions (including the special €5/share dividend payout to shareholders and the Sanoma acquisition).

As a reminder, Roularta’s covenant threshold of 3.5x net debt over EBITDA is based on annual EBITDA including the company’s share of Mediafin’s and Bayard’s net profit. Based on this definition, the company reported a ratio of 1.5x in 2017 despite the depressed consolidated EBITDA.

Going forward, this has become a non-issue as we expect Roularta to report a net cash €99m in 2019e (revised up from the level expected in July), compared to a reported net debt position of €63m at the end of 2017.

2018 NFD/EBITDA, sector

2019 NFD/EBITDA, Roularta vs. Peers 2018 NFD/EBITDA, Roularta vs. Peers

-20

-15

-10

-5

0

5

10

15

Mar-15 Dec-15 Sep-16 Jun-17 Mar-18

ROU-BRU

IPR-LIS

IPDC-DUB

GEDI-IT

MN-MIL

VOC-MCE -10

-5

0

5

10

Mar-15 Dec-15 Sep-16 Jun-17 Mar-18

ROU-BRU

IPR-LIS

IPDC-DUB

GEDI-IT

MN-MIL

VOC-MCE

-20

-15

-10

-5

0

5

Mar-15 Mar-16 Mar-17 Mar-18ROU-BRU Peer avg.

-10

-5

0

5

Mar-15 Sep-15 Mar-16 Sep-16 Mar-17 Sep-17 Mar-18 Sep-18ROU-BRU Peer avg.

Historical EBIT Margin, Roularta vs. Peers

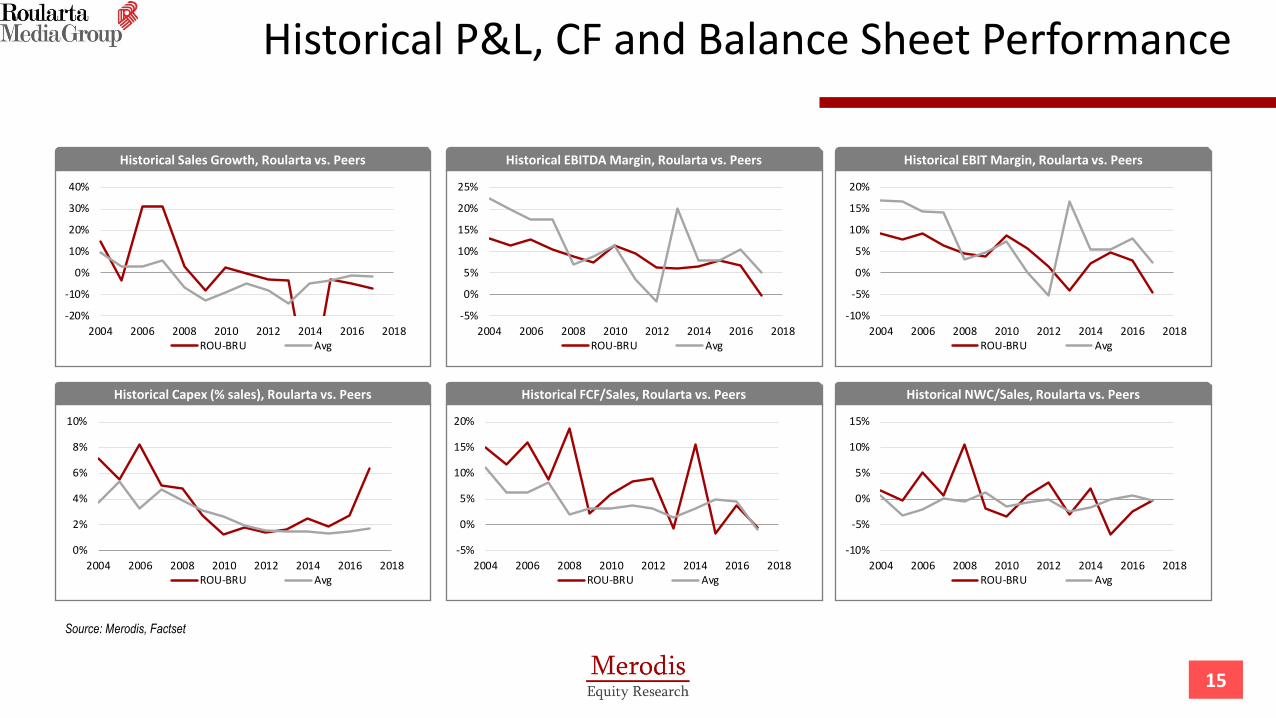

15

Historical P&L, CF and Balance Sheet Performance

Source: Merodis, Factset

Historical EBITDA Margin, Roularta vs. Peers

Historical NWC/Sales, Roularta vs. Peers Historical FCF/Sales, Roularta vs. Peers

Historical Sales Growth, Roularta vs. Peers

Historical Capex (% sales), Roularta vs. Peers

-20%

-10%

0%

10%

20%

30%

40%

2004 2006 2008 2010 2012 2014 2016 2018ROU-BRU Avg

-5%

0%

5%

10%

15%

20%

25%

2004 2006 2008 2010 2012 2014 2016 2018ROU-BRU Avg

-10%

-5%

0%

5%

10%

15%

20%

2004 2006 2008 2010 2012 2014 2016 2018ROU-BRU Avg

0%

2%

4%

6%

8%

10%

2004 2006 2008 2010 2012 2014 2016 2018ROU-BRU Avg

-5%

0%

5%

10%

15%

20%

2004 2006 2008 2010 2012 2014 2016 2018ROU-BRU Avg

-10%

-5%

0%

5%

10%

15%

2004 2006 2008 2010 2012 2014 2016 2018ROU-BRU Avg

16

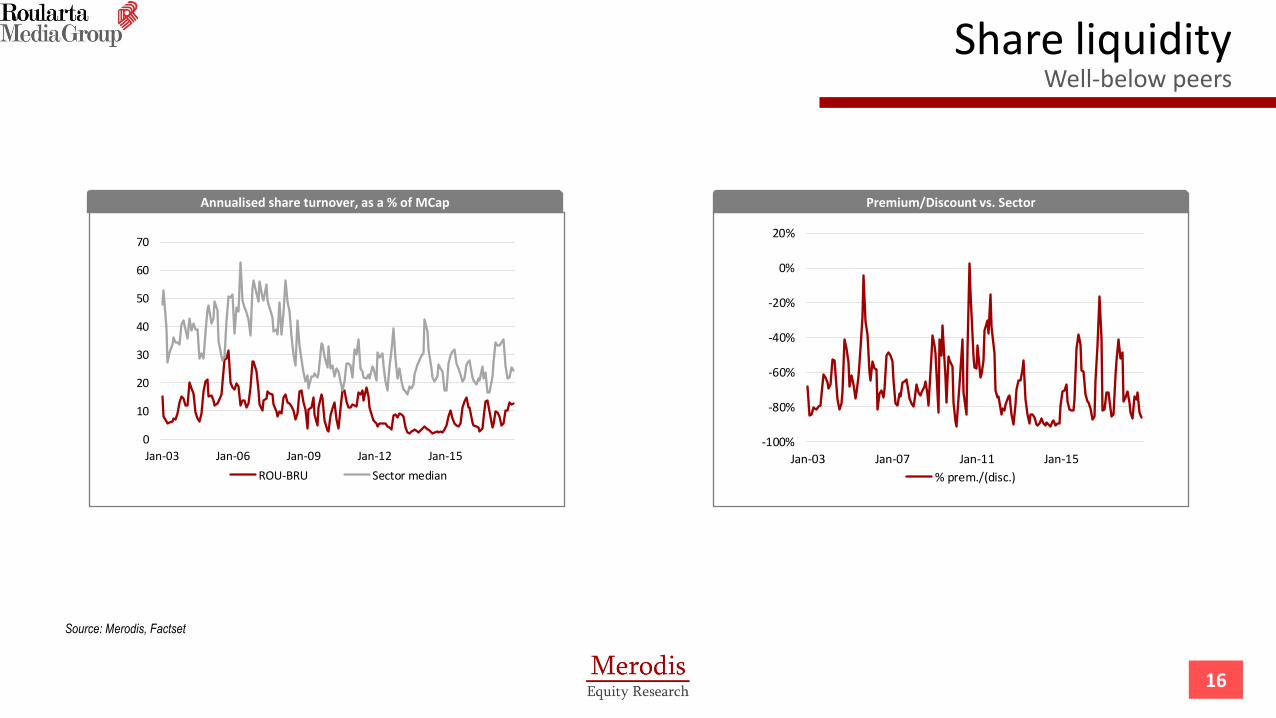

Share liquidity Well-below peers

Source: Merodis, Factset

Annualised share turnover, as a % of MCap Premium/Discount vs. Sector

0

10

20

30

40

50

60

70

Jan-03 Jan-06 Jan-09 Jan-12 Jan-15

ROU-BRU Sector median

-100%

-80%

-60%

-40%

-20%

0%

20%

Jan-03 Jan-07 Jan-11 Jan-15

% prem./(disc.)

17

Financial tear sheet

Ente

rpri

se V

alu

e (

€m

): 1

8M

arke

t C

ap. (

€m

): 1

97

Fre

e-f

loat

MC

ap (

€m

): 3

0

Co

nso

lid

ate

d P

&L (

€m

)2

00

62

00

72

00

82

00

92

01

02

01

12

01

22

01

32

01

42

01

52

01

62

01

72

01

8e

20

19

e2

02

0e

CA

GR

06

-17

CA

GR

18

-20

e

Sale

s6

09

76

77

82

70

77

12

73

17

12

67

73

00

29

22

79

25

82

83

30

42

90

-7.5

1.2

EBIT

DA

78

81

70

53

82

70

45

42

20

18

16

15

34

-32

.7-1

2.0

EBIT

51

50

33

10

57

36

5-4

94

12

7-1

3-6

8-8

-7n

a-6

6.9

Pre

tax

pro

fit

49

36

18

-35

12

8-4

-57

-37

2-1

8-7

3-7

-7n

a-6

9.6

Net

pro

fit

25

16

14

-43

11

5-3

-58

-14

26

42

1-1

17

8-1

-1n

an

aC

om

bin

ed

P&

L (

€m

)2

00

62

00

72

00

82

00

92

01

02

01

12

01

22

01

32

01

42

01

52

01

62

01

72

01

8e

20

19

e2

02

0e

06

-17

18

-20

eSa

les

49

14

77

47

14

76

28

73

29

36

13

49

12

.1EB

ITD

A4

64

85

55

31

15

31

31

62

03

.9EB

IT2

33

34

23

6-1

18

01

4n

aP

reta

x p

rofi

t1

62

63

73

1-1

67

52

4n

aN

et p

rofi

t-5

8-1

42

64

21

-11

75

24

na

Cash

Flo

w (

€m

)2

00

62

00

72

00

82

00

92

01

02

01

12

01

22

01

32

01

42

01

52

01

62

01

72

01

8e

20

19

e2

02

0e

06

-17

18

-20

eA

dj.

EB

ITD

A7

28

06

73

67

76

33

92

11

71

51

61

53

4-3

2.2

-12

.0W

CR

22

46

2-1

0-1

94

17

-16

4-1

7-8

04

14

-1n

an

aG

ros

Op

CF

95

84

12

92

65

86

65

65

21

-38

18

18

2-3

5.3

-50

.2C

ap

ex-5

0-3

8-3

5-2

0-8

0-4

-6-7

-5-8

-16

-4-1

4-7

-9.6

32

.3FC

F2

01

37

4-8

24

46

44

-10

27

05

-26

58

-1n

an

aN

et d

isp

./(a

cq.)

-21

4-1

44

57

-91

01

91

21

61

72

20

-90

na

na

Div

iden

ds

pa

id-8

-8-9

00

-6-4

00

0-6

-6-6

30

0-2

.3n

aEq

uit

y is

sue

51

-13

28

20

-30

00

00

00

00

na

na

Oth

ers

-29

-2-1

7-1

20

-16

-19

2-4

1-6

31

00

00

na

na

Net

Deb

t (i

ncr

.)/d

ecr.

-18

2-2

48

13

91

52

22

0-7

-66

18

-51

62

-1-1

-27

.7n

aB

ala

nce

Sh

eet

(€m

)2

00

62

00

72

00

82

00

92

01

02

01

12

01

22

01

32

01

42

01

52

01

62

01

72

01

8e

20

19

e2

02

0e

06

-17

18

-20

eW

C1

71

3-4

9-3

9-2

0-2

4-4

1-2

5-5

1-2

1-1

3-1

3-1

7-3

1-2

9n

a3

3.3

Ca

pit

al

Emp

loye

d6

60

68

96

40

58

46

02

58

15

49

51

12

21

29

82

95

15

41

68

15

61

54

-12

.4-4

.3D

isco

nti

nu

ed A

sset

s0

00

00

00

01

52

00

12

90

00

na

na

Ca

sh &

Eq

uiv

ale

nt

42

32

11

07

24

43

57

95

13

43

95

14

31

05

10

41

03

0.3

-1.0

Gro

ss D

ebt

26

32

78

27

51

98

15

51

24

14

81

27

11

61

14

10

81

06

66

6-8

.00

.0Eq

uit

y2

85

28

43

18

31

23

45

35

13

45

28

71

43

20

82

22

20

32

44

23

22

28

-3.0

-3.2

Gro

wth

(%

)2

00

62

00

72

00

82

00

92

01

02

01

12

01

22

01

32

01

42

01

52

01

62

01

72

01

8e

20

19

e2

02

0e

Sale

s3

13

13

-83

0-3

-3-5

81

-4-6

10

7-5

EBIT

DA

40

4-1

4-2

45

4-1

5-3

5-6

-54

-8-1

0-9

43

55

-29

9EB

IT4

8-1

1-3

1-2

31

31

-32

-73

na

na

13

9-5

8n

an

an

an

aN

et p

rofi

t1

0-3

6-1

4n

an

a-5

0n

an

an

an

a-6

7n

an

an

an

aFC

F-5

1-3

64

91

na

na

92

-6n

an

a-1

00

18

85

9n

an

a4

2n

aN

WC

-57

-24

na

-20

-49

19

72

-38

99

-58

-39

-23

08

6-5

Ca

pit

al

Emp

loye

d1

23

4-7

-93

-4-5

-7-5

73

5-1

-48

9-7

-2Sh

are

ho

lder

Eq

uit

y3

20

12

-21

12

-2-1

7-5

04

57

-92

0-5

-2Fin

an

cial

Rati

os

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

e2

01

9e

20

20

eG

ross

ma

rgin

(%

)7

17

47

57

67

87

67

57

67

27

57

67

67

77

77

6EB

ITD

A m

arg

in (

%)

13

11

98

12

10

66

76

60

21

1EB

IT m

arg

in (

%)

97

44

96

2-4

25

2-5

-2-2

-3N

et m

arg

in (

%)

42

2-1

42

0-9

-47

22

8-4

28

00

Op

ex/S

ale

s (%

)8

78

99

29

28

89

19

49

49

49

29

49

99

89

89

8D

epre

cia

tio

n/S

ale

s (%

)3

33

32

22

33

34

44

44

Dep

reci

ati

on

/EB

ITD

A (

%)

25

29

37

42

22

22

34

41

45

52

63

11

26

22

73

33

31

0Ta

x ra

te (

%)

48

55

31

-84

37

43

28

-3-8

9-6

71

-4-8

20

00

Ca

pex

/Sa

les

(%)

85

53

10

11

22

36

15

2FC

F/Sa

les

(%)

32

9-1

36

6-1

90

2-1

02

30

WC

R/S

ale

s (%

)4

18

-1-3

12

-21

-6-3

01

5-1

WC

/Sa

les

(%)

32

-6-6

-3-3

-6-4

-17

-7-5

-5-6

-10

-10

Ca

pit

al

Emp

loye

d/S

ale

s (%

)1

08

90

82

83

85

79

77

75

74

10

21

06

59

59

51

53

Gea

rin

g (%

)7

48

35

03

93

12

51

92

65

63

62

63

1-4

0-4

2-4

2N

et D

ebt/

EBIT

DA

(x)

2.8

3.0

2.4

2.4

1.4

1.3

1.5

1.8

4.2

4.2

3.5

62

.2-2

1.7

-30

.4-2

7.5

RO

CE

po

st-t

ax

(%)

63

33

63

16

83

28

-95

01

2R

OE

(%)

10

65

-19

4-1

-18

-66

37

10

-53

50

0D

ivid

end

Pa

you

t (%

)3

35

20

02

23

00

00

10

30

08

30

0V

alu

ati

on

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

e2

01

9e

20

20

e0

6-1

71

8-2

0e

Ma

rket

Ca

pit

ali

sati

on

(€

m)

57

96

69

39

31

84

24

82

75

18

51

55

16

22

08

31

93

05

19

71

97

19

7-5

.70

.0+

Net

Fin

an

cia

l D

ebt

(€)

22

22

46

16

51

27

11

18

97

07

68

27

65

76

3-1

00

-99

-98

-10

.9-1

.0+

Res

tate

d M

in. +

oth

ers

(€m

)3

83

82

21

51

71

61

43

52

01

01

01

01

01

01

0-1

1.6

0.0

- A

sso

cia

tes

& I

nv.

(€

m)

16

11

12

10

11

12

14

14

12

31

76

16

72

09

09

09

01

.90

.0=

Ente

rpri

se V

alu

e (

€m

)8

24

94

25

68

31

63

65

36

92

54

25

31

41

11

82

19

35

81

81

92

0-7

.35

.4A

sso

c. N

FD (

gr. s

ha

re)

(€m

)0

00

00

00

00

-6-6

-6-6

-6-6

EV/S

ale

s (x

)1

.41

.20

.70

.40

.50

.50

.40

.40

.30

.40

.81

.40

.10

.10

.1EV

/EB

ITD

A (

x)1

0.5

11

.68

.25

.94

.55

.35

.66

.07

.26

.61

3.5

35

5.6

4.0

5.9

5.7

EV/E

BIT

(x)

16

.11

9.0

17

.43

0.9

6.4

10

.45

3.7

-5.1

36

.09

.63

2.7

-27

.6-0

.3-2

.5-2

.7EV

/FC

F (x

)4

2.2

75

.07

.7-3

7.3

15

.17

.95

.8-2

5.0

5.3

na

42

.8-1

3.7

3.4

2.5

-17

.2EV

/Ca

pit

al

Emp

loye

d (

x)1

.21

.40

.90

.50

.60

.60

.50

.50

.60

.40

.72

.30

.10

.10

.1P

/E (

x)2

3.3

42

.02

8.9

-45

.08

.21

7.9

-74

.0-2

.7-1

.13

.21

4.7

-27

.72

.5-2

56

-23

0.6

P/B

VP

S (x

)2

.02

.41

.20

.60

.70

.80

.50

.51

.11

.01

.41

.50

.80

.80

.9FC

F yi

eld

(%

)3

.41

.91

8.9

-4.6

9.8

16

.92

3.7

-6.5

16

.40

.01

.6-8

.62

.73

.9-0

.6P

er

share

data

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

e2

01

9e

20

20

e0

6-1

71

8-2

0e

# o

f sh

are

s1

1.0

11

1.0

41

3.1

31

3.1

31

3.1

31

3.1

41

3.1

41

3.1

41

3.1

41

3.1

41

3.1

41

3.1

41

3.1

41

3.1

41

3.1

41

.60

.0#

of

avg

sh

. (FD

, ex-

trea

s.)

10

.96

11

.03

13

.26

13

.43

13

.42

13

.21

13

.18

13

.05

12

.97

13

.07

13

.03

13

.03

13

.03

13

.03

13

.03

1.6

0.0

Sha

re p

rice

52

.65

60

.61

29

.96

14

.02

18

.85

20

.95

14

.06

11

.81

12

.36

15

.85

24

.24

23

.20

15

.00

15

.00

15

.00

-7.2

0.0

EPS

2.2

61

.44

1.0

4-0

.31

2.3

11

.17

-0.1

9-4

.44

-11

.04

.92

1.6

5-0

.84

6.0

1-0

.06

-0.0

7n

an

aEP

S FD

2.2

61

.44

1.0

4-0

.31

2.3

11

.17

-0.1

9-4

.44

-11

.04

.92

1.6

5-0

.84

6.0

1-0

.06

-0.0

7n

an

aB

VP

S2

5.8

82

5.7

02

4.2

22

3.7

52

6.2

82

6.7

32

6.2

32

1.8

41

0.9

01

5.8

01

6.9

21

5.4

51

8.5

51

7.6

61

7.3

8-4

.6-3

.2D

PS

0.7

50

.75

0.0

00

.00

0.5

00

.35

0.0

00

.00

0.0

00

.50

0.5

00

.00

5.0

00

.00

0.0

0n

an

aS

ou

rce

: C

om

pa

ny d

ata

, M

ero

dis

Eq

uity R

ese

arc

h

Fin

an

cia

l su

mm

ary

18

Disclaimer

This Report is solely for the information of the recipients. All information contained in this research report has been compiled from sources believed to be reliable. However, no representation or warranty, express or implied, is made with respect to the completeness or accuracy of its contents, and it is not to be relied upon as such. Opinions contained in this research report represent the authors’ current opinions on the date of the report only. Merodis is not soliciting an action based upon it, and under no circumstances is it to be used or considered as an offer to sell, or a solicitation of any offer to buy.

This report is provided solely for the information of professional investors who are expected to make their own investment decisions without undue reliance on this report and Merodis accepts no liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

ANALYST CERTIFICATION:

Merodis has been mandated by the subject company to produce a neutral, fair, and elaborate equity research report about the subject company with the aim to increase investors’ awareness about the stock. The authors hereby declare that this report represents their personal opinion and that the company has neither limited nor in any other way influenced the content of this report. No part of the research analyst's compensation was, is, or will be, directly or indirectly, related to the specific opinions or views expressed by the research analyst in this research report.

The authors also declare that they are not shareholders of the subject company and that they have no other economic interest in the subject company than through their current mandate.

This Report is and at all times shall remain the exclusive property of Merodis.

This Report contains statements, estimates and projections provided by the Client concerning anticipated future performance. Such statements, estimates and projections reflect assumptions by our Client concerning anticipated results, which may or may not prove to be correct. No representations, expressed or implied are made as to the accuracy of such statements, estimates and projections.

All communication regarding this Report and requests for additional information should be directed to Merodis:

Arnaud W. Goossens

Partner

For more information about

Merodis

please visit:

www.merodis.com