Romania Macroeconomic overview Ionut Dumitru · Ionut Dumitru Chief-economist, Raiffeisen Bank...

28

1 Romania Macroeconomic overview Ionut Dumitru Chief-economist, Raiffeisen Bank Romania chapter 1

Transcript of Romania Macroeconomic overview Ionut Dumitru · Ionut Dumitru Chief-economist, Raiffeisen Bank...

1

Romania Macroeconomic overview

Ionut Dumitru Chief-economist, Raiffeisen Bank Romania

chapter 1

2

Sustained upward trend of economic activity driven by private consumption

2

3

Economic growth pace has further accelerated in 2017 (6.9%), coming close to pre-crisis levels. GDP advance is supported by all

major demand segments: private consumption, gross fixed investments, and exports of goods and services. Still, the rapid growth

of private consumption is the main driver of the economic growth.

We expect real GDP to resume its growth starting Q2 after unexpectedly stalling in the first quarter of this year.

3

Sustained upward trend of economic activity

Source: National Institute of Statistics, Eurostat, Raiffeisen BANK

-15%

-10%

-5%

0%

5%

10%

15%

20%

13Q4 14Q4 15Q4 16Q4 17Q4

Real GDP and domestic demand

Real GDP (% yoy)

Private consumption (% yoy)

Gross fixed capital formation (% yoy)

-4

-2

0

2

4

6

8

2012 2013 2014 2015 2016 2017

Contribution to GDP growth

Net exports

Change in inventories

Gross fixed capital formation

Public consumption

Households' consumption

Real GDP (% yoy)

-9

-3

3

9

15

04Q1 07Q3 11Q1 14Q3 18Q1

Economic growth

Real GDP (% yoy)

Real GDP excluding agriculture (% yoy)

4

All major economic sectors except constructions had positive contributions to the GDP growth in 2017. Also, agriculture had a

consistent positive contribution (0.7 percentage points) to GDP advance in 2017.

4

Broadly based economic growth

Source: National Institute of Statistics, Eurostat, Raiffeisen BANK

Note: 4-quarter moving averages

-2

0

2

4

6

8

2013 2014 2015 2016 2017

Contribution of sectors to GDP growth

Services Industry

Construction Agriculture

Net taxes on products Real GDP (% yoy)

95

100

105

110

115

120

125

130

12Q4 13Q4 14Q4 15Q4 16Q4 17Q4

Gross value added by sectors (2012=100)

IndustryReal GDP

excluding

agriculture

Private

services

Construction

5

Investments showed signs of rebounding in 2017 and we expect the upward trend to remain intact in the subsequent quarters.

5

Rebound of private investments under way

Source: National Institute of Statistics, Ministry of Public Finances, Eurostat, Raiffeisen BANK

Note: 4-quarter moving averages

-15

-10

-5

0

5

10

15

20

10

Q4

11Q

4

12

Q4

13

Q4

14Q

4

15

Q4

16

Q4

17Q

4

Gross fixed capital formation

Quarterly dynamics (% qoq)

Annual dynamics (% yoy)

-60

-40

-20

0

20

40

07Q4 09Q4 11Q4 13Q4 15Q4 17Q4

Net investments, by segments

(% yoy)

New construction works

Equipments and transport means

Total investments

4

8

12

16

12

24

36

48

07Q4 09Q4 11Q4 13Q4 15Q4 17Q4

Gross fixed capital formation

Private sector (current RON bn, sa)

Public sector (current RON bn, sa, RHS)

6

Households’ disposable income keeps growing as labor market conditions are improving. Also, wages in the public sector and

pensions are again increased in 2018.

6

Growing disposable income boosts consumption

Note: Number of employees is based on a monthly survey on public sector and on private companies with at least 4 employees

Source: National Institute of Statistics, Eurostat, Raiffeisen BANK

Note: wage earnings stated in prices of December 2017

3

4

5

6

7

8

9

Ma

r-0

4

Ma

r-06

Ma

r-0

8

Ma

r-1

0

Ma

r-1

2

Ma

r-1

4

Ma

r-1

6

Ma

r-1

8

Unemployment rates

Recorded unemployment rate (%)

ILO unemployment rate (%)

850

900

950

1000

1050

3000

3250

3500

3750

4000

Ma

r-0

6

Ma

r-0

8

Ma

r-1

0

Ma

r-12

Ma

r-1

4

Ma

r-1

6

Ma

r-1

8

Employees in the economy

Employees in private sector (thous.)

Employees in public sector (thous., RHS)

500

1000

1500

2000

2500

3000

3500

Mar-03 Mar-06 Mar-09 Mar-12 Mar-15 Mar-18

Monthly net wages in the

economy (RON, constant prices)

Private sector Public sector

7

Some of macroeconomic indicators published at monthly frequency had a poor performance in Q1 2018, pointing to a deceleration

of economic growth in Q1. This was confirmed by flash Q1 GDP estimates released on 15 May (0.0% qoq, and 4.0% yoy).

7

Economic growth decelerated sharply in Q1 2018…

Note: confidence indicators are stated as deviations

from their long-term averages (2002-2018)

-40

-30

-20

-10

0

10

20

30

Ap

r-04

Ap

r-0

6

Ap

r-0

8

Ap

r-1

0

Ap

r-1

2

Ap

r-14

Ap

r-1

6

Ap

r-1

8

Confidence indicators

Consumer confidence indicator

Economic Sentiment Index (ESI)

Macroeconomic indicators published at monthly frequency

Source: National Institute of Statistics, Raiffeisen BANK

Q2-17 Q3-17 Q4-17 Q1-18

Industrial output 3.7 0.1 2.9 -0.6

Turnov er in industry, deflated 0.9 2.3 2.9 2.6

Exports of goods, in EUR equiv . 1.2 0.9 3.3 3.9

Retail sales turnov er, deflated 3.1 3.9 1.8 -1.6

Turnov er in market serv ices for

population 6.7 5.3 -1.7 -3.9

Turnov er in market serv ices for

enterprises 4.2 2.6 2.0 0.0

Construction output -5.7 1.8 -2.8 6.9

Economic sentiment index (lev el) 105.1 104.5 103.9 102.3

Consumer sentiment index (lev el) -14.0 -15.4 -22.7 -25.8

Number of employees (% qoq) 0.6 0.5 0.6 0.4

Quarterly change (% qoq)

8

1.6 1.6

1.2 1.2

0.9 0.90.8 0.8

0.7 0.70.6

0.50.4 0.4 0.4 0.4 0.4

0.3 0.3 0.30.2

0.10

-0.1

-0.5

0

0.5

1

1.5

2

Ire

lan

d

Gre

ec

e

Cro

atia

Cy

pru

s

Lux

em

bo

urg

Ma

lta

Latv

ia

Po

lan

d

Hu

ng

ary

Fin

lan

d

Lith

ua

nia

Slo

va

kia

Bu

lga

ria

Au

stri

a

Sp

ain

Sw

ed

en

Slo

ve

nia

Ne

the

rla

nd

s

EU

Eu

ro a

rea

Cze

ch

Re

pu

blic

De

nm

ark

Po

rtu

ga

l

Be

lgiu

m

Ge

rma

ny

Ita

ly

Fra

nc

e

Un

ite

d K

ing

do

m

Ro

ma

nia

Est

on

ia

Average qoq growth in 2017 qoq growth in Q1 2018

…Romania being one of the worst performers in Q1 2018

at the EU level

Source: Eurostat

Note: Seasonally adjusted data

9

Exports of goods and services should continue on an upward trend, helped by growing external demand. However, imports should

increase faster, fuelling a gradual enlargement of foreign trade deficit and of current account deficit.

9

Exports on an upward trend, imports are increasing faster

Source: National Bank of Romania, Raiffeisen BANK

Note: 6-months moving averages

-6

-3

0

3

6

9

12

15

Mar-13 Mar-14 Mar-15 Mar-16 Mar-17 Mar-18

Foreign trade with goods

Imports of goods (% yoy, EUR equiv.)

Exports of goods (% yoy, EUR equiv.)

-6

-5

-4

-3

-2

-1

0

1

2

Mar-13 Mar-14 Mar-15 Mar-16 Mar-17 Mar-18

External imbalances

Foreign trade balance: goods, services (% of GDP, last 6M)

Current account balance (% of GDP, last 6M)

10 10

12.6 12.5

10.2

8.0 7.9

6.4

5.04.5

3.7 3.5 3.2 3.2 3.2 2.8 2.81.9 1.9

1.4 1.1 0.8 0.7 0.5 0.3

-0.2-0.8 -0.8 -0.8

-2.1

-3.4-4.1

-6.7

-10.0

-5.0

0.0

5.0

10.0

15.0M

alta

Ire

lan

d

Ne

the

rla

nd

s

Ge

rma

ny

De

nm

ark

Slo

ve

nia

Luxe

mb

ou

rg

Bu

lga

ria

Cro

atia

Eu

ro a

rea

Est

on

ia

EU

ex

clu

din

g U

K

Sw

ed

en

Ita

ly

Hu

ng

ary

Sp

ain

Au

stri

a

EU

Cze

ch

Re

pu

blic

Lith

ua

nia

Fin

lan

d

Po

rtu

ga

l

Po

lan

d

Be

lgiu

m

Latv

ia

Fra

nc

e

Gre

ec

e

Slo

va

kia

Ro

ma

nia

Un

ite

d K

ing

do

m

Cy

pru

s

Source: AMECO database

Romania is one of the few countries in EU with current account deficit

Current account balance (% of GDP, 2017)

11

Inflows in EU funds decreased substantially in 2017 as absorption rate at the start of the new budgeting period 2014-2020 was low.

Still, stable foreign capital inflows (FDIs and capital transfers in EU funds) provided a good coverage of the current account deficit in 2017.

Substantial decline of EU funds inflows

Source: National Bank of Romania, Eurostat, Raiffeisen BANK

Note: Adjusted current account balance = current account balance + FDIs + Capital account balance

-2

0

2

4

6

8

10

20

03

20

04

20

05

200

6

20

07

20

08

20

09

201

0

20

11

20

12

20

13

20

14

20

15

20

16

201

7

Foreign direct investments

(% of GDP)

Equity Debt instruments Total FDIs

-15

-10

-5

0

5

10

Ma

r-06

Ma

r-08

Ma

r-10

Ma

r-12

Ma

r-14

Ma

r-16

Ma

r-18

Structure of adjusted current account

balance

Capital account balance (% of GDP, last 12 months)

FDIs (% of GDP, last 12 months)

Current account balance (% of GDP, last 12 months)

311

1,4081,443

1,0371,422

2,111

4,149 4,259

4,882

5,888

3,413

1,653

8001,188

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

16Q

1

20

17Q

1

20

18Q

1

Net inflows from the EU (EUR, mn)

12

Public finances - the most important macroeconomic risk

12

13

Public budget deficit target was kept at 3% of GDP in 2018, but we see risk for the deficit to outpace this level in the absence of

corrective measures.

Fiscal deficit reached once again 3% of GDP (ESA2010)

Source: AMECO database, Ministry of Finance

Note: in-house seasonally adjusted data; cash

methodology

-1.4

-2.4

-2.8

-0.7

-3.0

-4

-3

-2

-1

0

1

2

Jan

Feb

Ma

r

Ap

r

Ma

y

Jun

Jul

Au

g

Sep

Oc

t

No

v

De

c

Year-to-date public budget

execution (% of GDP)

2015 2016 2017

2018 2018 Target

-10.0

-9.0

-8.0

-7.0

-6.0

-5.0

-4.0

-3.0

-2.0

-1.0

0.0

200

0

200

1

200

2

200

3

200

4

200

5

200

6

200

7

200

8

200

9

201

0

201

1

201

2

201

3

201

4

201

5

201

6

201

7

201

8f

201

9f

Effective deficit Structural deficit

Maastricht criterion Medium term objective (MTO)

14 14

-10

-9

-8

-7

-6

-5

-4

-3

-2

-1

0

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18f

20

19

f

European Union

Romania

Opposite direction of the fiscal deficit in Romania vs EU average (% of GDP, ESA2010)

Source: AMECO database

15

-4

-3

-2

-1

0

1

2

3C

yp

rus

Cze

ch

Re

pu

blic

Ge

rma

ny

Ma

lta

Lux

em

bo

urg

Sw

ed

en

Cro

atia

Ne

the

rla

nd

s

Bu

lga

ria

Slo

ve

nia

Lith

ua

nia

Gre

ec

e

Est

on

ia

De

nm

ark

Ire

lan

d

Au

stri

a

Eu

ro a

rea

Eu

ro a

rea

Fin

lan

d

Eu

rop

ea

n U

nio

n

Po

rtu

ga

l

Slo

va

kia

Latv

ia

Be

lgiu

m

Po

lan

d

Ita

ly

Un

ite

d K

ing

do

m

Fra

nc

e

Hu

ng

ary

Sp

ain

Ro

ma

nia

Effective balance Structural balance Maastricht criterion

Romania would have the highest budget deficit (% of GDP, ESA2010) in the EU in 2018

Source: AMECO database

16

In 2017, fiscal revenues reached the 23-year low,

being the second lowest at the EU level

16

27.6

25.9

26.4

29.1

31.2

30.7

28.8

28.4

27.927.7

28.3

28.928.7

27.3

26.2

27.2

28.2

27.8

27.327.4

28.0

26.6

25.8

25.0

26.0

27.0

28.0

29.0

30.0

31.0

32.0

199

5

199

6

199

7

199

8

199

9

200

0

200

1

200

2

200

3

200

4

200

5

200

6

200

7

200

8

200

9

201

0

201

1

201

2

201

3

201

4

201

5

201

6

201

7

40.0

38.4

35.1

29.9

25.8

20.0

25.0

30.0

35.0

40.0

45.0

50.0

Fra

nc

e

De

nm

ark

Be

lgiu

m

Sw

ed

en

Fin

lan

d

Au

stria

Ita

ly

Gre

ec

e

Eu

ro a

rea

Ge

rma

ny

Eu

rop

ea

n U

nio

n

Luxe

mb

ou

rg

Ne

the

rla

nd

s

Hu

ng

ary

Cro

atia

Po

rtu

ga

l

Slo

ve

nia

Cze

ch

Re

pu

blic

Un

ite

d K

ing

do

m

Po

lan

d

Cyp

rus

Sp

ain

Est

on

ia

Ma

lta

Slo

va

kia

Latv

ia

Lith

ua

nia

Bu

lga

ria

Ro

ma

nia

Ire

lan

d

Source: AMECO database, ESA2010

Development of fiscal revenues (% of GDP) in Romania Fiscal revenues (% of GDP) in 2017 in the EU countries

17

Public sector wage bill would reach the pre-crisis high in

2018 (ESA2010)

17

6.66.4

5.4

5.8

8.17.9

8.38.5

8.1 8.1

8.7

9.29.4

10.1

10.4

9.6

7.8 7.8

8.1

7.7 7.7

8.9

9.7

10.410.3

5.0

6.0

7.0

8.0

9.0

10.0

11.0

Development of wage bill in the public sector (% of GDP, ESA2010) in Romania

Source: AMECO database

18

57.1

59.4

55.9 56.4

58.9 57.1

62.5 62.7

59.5 61.2

62.4 62.2 64.0

73.1

86.1

82.1

69.9 68.2 68.7

66.4 65.1

73.5

79.6 81.3

82.3

45

50

55

60

65

70

75

80

85

90

199

5

199

6

199

7

199

8

199

9

200

0

200

1

200

2

200

3

200

4

200

5

200

6

200

7

200

8

200

9

201

0

201

1

201

2

201

3

201

4

201

5

201

6

201

7

201

8f

201

9f

Source: AMECO database; Note: Social spending=wage spending plus social benefits

60.0

64.3

69.771.8

79.6

45.0

50.0

55.0

60.0

65.0

70.0

75.0

80.0

85.0

Ne

the

rla

nd

s

Ge

rma

ny

Sw

ed

en

Cze

ch

Re

pu

blic

Hu

ng

ary

Lux

em

bo

urg

Un

ite

d K

ing

do

m

Ma

lta

Be

lgiu

m

Ire

lan

d

Eu

rop

ea

n U

nio

n

Eu

ro a

rea

Cro

atia

Latv

ia

Fra

nc

e

De

nm

ark

Au

stri

a

Lith

ua

nia

Slo

va

kia

Est

on

ia

Ita

ly

Bu

lga

ria

Slo

ve

nia

Po

lan

d

Fin

lan

d

Po

rtu

ga

l

Gre

ec

e

Cy

pru

s

Sp

ain

Ro

ma

nia

The burden of social spending in Romania is the highest in EU

Development of social spending as % of fiscal revenues in Romania Social spending as % of fiscal revenues in EU countries, 2017

19

4.1 3.9

2.6

1.8 1.6

3.4

2.7

3.2 3.5

2.8 2.8

5.2

6.1

6.5

5.8 5.7 5.5

4.8

4.5 4.3

5.1

3.6

2.8

1.0

2.0

3.0

4.0

5.0

6.0

7.0

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

19

4.4

3.7

2.8 2.7

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

6.0

Est

on

ia

Gre

ec

e

Sw

ed

en

Hu

ng

ary

Luxe

mb

ou

rg

Latv

ia

Fin

lan

d

Po

lan

d

Ne

the

rla

nd

s

De

nm

ark

Fra

nc

e

Cze

ch

Re

pu

blic

Slo

va

kia

Lith

ua

nia

Au

stria

Slo

ve

nia

Ro

ma

nia

Cy

pru

s

Eu

rop

ea

n U

nio

n

Cro

atia

Un

ite

d K

ing

do

m

Eu

ro a

rea

Ma

lta

Be

lgiu

m

Ge

rma

ny

Bu

lga

ria

Sp

ain

Ita

ly

Ire

lan

d

Po

rtu

ga

l

Public investments reached in 2017 the 13-year low, being very close to the EU average

Development of public investments (% of GDP) in Romania Public investments (% of GDP) in 2017 in the EU countries

Source: AMECO database, ESA2010

20

Apr 2018/Apr

2017

Jan-Apr 2018/

Jan-Apr 2017

Buget

2018/Execution 2017

Total revenues 12.7% 11.8% 14.2%

Fiscal revenues including SSC 15.3% 10.5% 11.8%

Fiscal revenues excluding SSC 3.4% -0.3% 3.5%

Corporate income tax 4.2% -0.2% 2.0%

Personal income tax -29.6% -18.2% -31.0%

Property taxes 28.6% 6.7% 8.6%

Taxes on goods and services 11.0% 4.1% 14.5%

VAT -2.0% 1.1% 14.5%

Excises 50.0% 14.7% 13.6%

Social security contributions (SSC) 40.9% 33.6% 28.0%

Non-fiscal revenues 3.5% 13.9% -7.0%

EU funds (2014-2020) -28.4% 26.0% 66.4%

Total expenditures 19.5% 21.5% 13.9%

Current expenditures 20.9% 18.2% 14.0%

Wages 26.9% 20.4% 16.6%

Goods and services 11.1% 12.2% -1.7%

Interest expenses 147.6% 56.2% 19.5%

Subsidies 33.3% 26.8% 16.3%

Social assistance 8.0% 10.8% 6.5%

EU funds (2014-2020) -19.8% 28.7% 75.1%

Capital expenditures -20.7% 156.8% 5.6%

Total investment spending -16.7% 103.4% 44.3%

Surplus(+) / Deficit(-) 854.3%

-0.65% of GDP

in 2018 vs

+0.16% of GDP

in 2017

11.1%20

Budget spending is growing too fast and the “room for

maneuver” (=cutting investments) is much lower

Source: Ministry of Finance, cash

methodology;

If the annual growth of revenues is

higher/lower than the budgeted one for the

full year, then the cell is filled with green/red.

If the annual growth of expenditures is

higher/lower than the budgeted one for the

full year, then the cell is filled with red/green.

21

Monetary policy tightening as inflation rate increases rapidly

21

22

Elevated inflation rate (5.2% yoy as of April) was fuelled by strengthening of underlying inflationary pressures, by increase of administered

prices, and by increase of fuel prices (increase of excises and of oil price).

Annual inflation rate would likely stabilize around 5.0% in Q2 – Q3 2018, before decreasing towards 3.5% at the end of the year.

22

Strengthening of underlying inflationary pressures

Source: National Bank of Romania, National Institute of Statistics, Raiffeisen BANK

Note: CORE 3 = CPI excluding administered prices, volatile prices

of foods and fuels, and tobacco and alcohol

5.2

4.0

7.2

2.6

-8

-4

0

4

8

12

Apr-13 Apr-14 Apr-15 Apr-16 Apr-17 Apr-18

Inflation dynamics by components

CPI (% yoy) Foods (% yoy)

Non-foods (% yoy) Services (% yoy)

-4

-2

0

2

4

6

8

Dec-13 Dec-14 Dec-15 Dec-16 Dec-17 Dec-18

Inflation outlook

CORE 3 inflation measure (% yoy)

CPI (%, yoy)

NBR mid-point target (%, yoy)

Outlook

23

-4

-3

-2

-1

0

1

2

3

4

5

6

Apr-13 Apr-14 Apr-15 Apr-16 Apr-17 Apr-18

Annual inflation rate (national definition)

Poland Hungary Romania

Inflation rate in Romania increased the fastest and it is the

highest in EU – we cannot blame “exogenous” factors

23

-0.3-0.1

0.30.5

0.60.7 0.7

0.80.9

1.11.2

1.31.4 1.4 1.4 1.4

1.61.7

1.8 1.8 1.81.9 1.9

2.12.2

2.4

2.93.0

4.3

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

Cy

pru

s

Ire

lan

d

Po

rtu

ga

l

Gre

ec

e

Ita

ly

De

nm

ark

Ne

the

rla

nd

s

Fin

lan

d

Po

lan

d

Sp

ain

Eu

ro a

rea

Luxe

mb

ou

rg

Eu

rop

ea

n U

nio

n

Ge

rma

ny

Cro

atia

Ma

lta

Be

lgiu

m

Bu

lga

ria

Cze

ch

Re

pu

blic

Fra

nc

e

Sw

ed

en

Au

stria

Slo

ve

nia

Latv

ia

Lith

ua

nia

Hu

ng

ary

Est

on

ia

Slo

va

kia

Ro

ma

nia

Dec-16 Apr-18

Annual inflation rate (HICP) in the EU countries (%)

Source: Eurostat, National Statistical Institutes

24

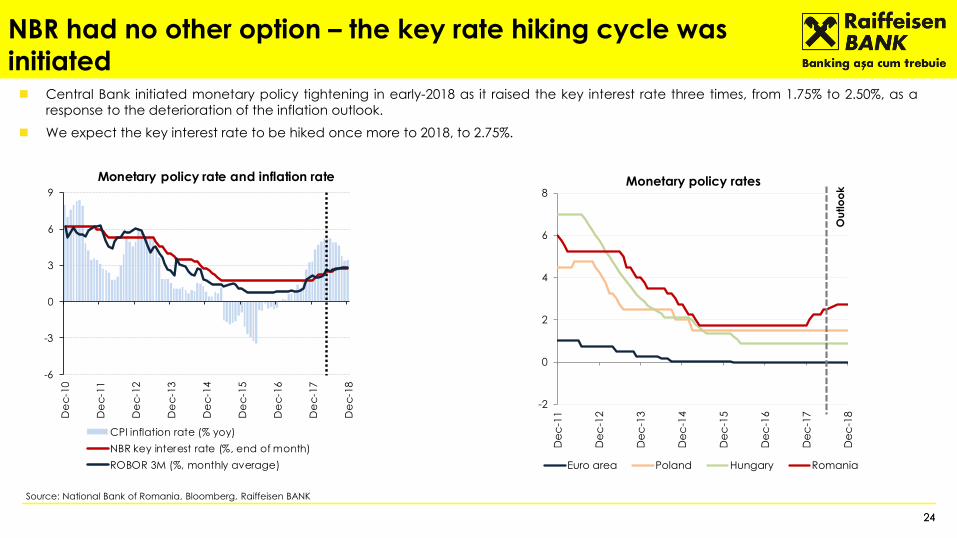

Central Bank initiated monetary policy tightening in early-2018 as it raised the key interest rate three times, from 1.75% to 2.50%, as a

response to the deterioration of the inflation outlook.

We expect the key interest rate to be hiked once more to 2018, to 2.75%.

24

NBR had no other option – the key rate hiking cycle was

initiated

Source: National Bank of Romania, Bloomberg, Raiffeisen BANK

-6

-3

0

3

6

9

De

c-1

0

De

c-1

1

De

c-1

2

De

c-1

3

De

c-1

4

De

c-1

5

De

c-1

6

De

c-1

7

De

c-1

8

Monetary policy rate and inflation rate

CPI inflation rate (% yoy)

NBR key interest rate (%, end of month)

ROBOR 3M (%, monthly average)

-2

0

2

4

6

8

De

c-1

1

De

c-1

2

De

c-1

3

De

c-1

4

De

c-1

5

De

c-1

6

De

c-1

7

De

c-1

8

Monetary policy rates

Euro area Poland Hungary Romania

Ou

tlo

ok

25 25

Disclaimer Financial Analysis

Risk notifications and explanations

Warnings

Figures on performance refer to the past. Past performance is not a reliable indicator for future results and the development of a financial instrument, a financial index or a securities service. This is

particularly true in cases when the financial instrument, financial index or securities service has been offered for less than 12 months. In particular, this very short comparison period is not a reliable indicator

for future results.

Performance of a financial instrument, a financial index or a securities service is reduced by commissions, fees and other charges, which depend on the individual circumstances of the investor.

The return on an investment in a financial instrument, a financial or securities service can rise or fall due to exchange rate fluctuations.

Forecasts of future performance are based purely on estimates and assumptions. Actual future performance may deviate from the forecast. Consequently, forecasts are not a reliable indicator for future

results and the development of a financial instrument, a financial index or a securities service.

A description of the concepts and methods used in the preparation of financial analyses is available here.

Detailed information on sensitivity analyses (procedure for checking the stability of potential assumptions made in the context of financial analyses) is available here.

Disclosure of circumstances and interests which may jeopardise the objectivity of Raiffeisen Bank Romania (RBRO) is available here.

The distribution of all recommendations relating to the calendar quarter prior to the publications date, as well as the distribution of recommendations in the context of which services of investment firms set

out in Sections A investment services and activities) and B (ancillary services) of Annex I of Directive 2014/65/EU of the European Parliament and of the Council have been provided in the past 12 months is

available here.

Detailed up-to-date information regarding methodology, conflicts of interest and disclaimer are available on the website of Raiffeisen Bank Romania SA, at the following web address:

https://www.raiffeisen.ro/despre-noi/guvernanta-corporativa/cercetare-economica/

26 26

Disclaimer Financial Analysis

Important: Please read the references at the end of this report to possible conflicts of interest and disclaimers/disclosures.

Publisher: Raiffeisen Bank Romania S.A.

Raiffeisen Bank Romania S.A. (herein after referred to as “RBRO”), a credit institution with registered office at Sky Tower, 246C Calea Floreasca, 1st District, code 014476, Bucharest, Romania, e-mail: [email protected],

website: www.raiffeisen.ro, Unique identifier 361820, Fiscal Code RO014460, BIC Code RZBRROBU, registered at Trade Register under no. J40/44/1991, listed in the Banking Register under no. RB-PJR-40-009/1999, in its

capacity as an Intermediary, registered with the Romanian Financial Supervisory Authority under no. PJR01INCR/400009 is authorized and supervised by Romanian National Bank (as credit institution), 25 Lipscani Street,

District 3, Postal code 030031, Bucharest, Romania, website: www.bnro.ro and by Financial Supervision Authority (as intermediary on capital markets by Decision no. A75/ 30.01.2014, completed by Decision no.

A239/27.03.2014), 15 Splaiul Independenţei, District 5, Postal Code 050092, Bucharest, Romania, website: www.asfromania.ro.

The shares of RBRO are not listed on any stock exchange. RBRO is a issuer of bonds’ that are traded on Bucharest Stock Exchange, therefore RBRO is acting and treated as an issuer on Romanian capital markets. For

further details on our issuer quality, please refer to the following address: https://www.raiffeisen.ro/despre-noi/guvernanta-corporativa/detinatori-de-obligatiuni.

RBRO is part of Raiffeisen Group, a financial group providing financial services in Austria and 15 Central Eastern European countries. Additionally, the Group comprises numerous other financial service providers, for

instance in the fields of leasing, asset management as well as mergers and acquisitions. RBRO offers a wide spectrum of financial services and products.. The Economic and Sectorial Research Directorate within RBRO

produces and disseminates reports and analyses covering the main macroeconomic developments in Romania.

RBRO´s ultimate parent company is Raiffeisen Bank International AG ("RBI") (Vienna Stock Exchange; ticker RBI AV). RBI is a credit institution domiciled in Austria. For many years RBI has been operating in Central and

Eastern Europe (CEE), where it maintains a network of subsidiary banks, leasing companies and numerous financial service providers in several markets. Although in the past 12 months RBI or its affiliated entities may have

concluded transactions with products or services (including but not limited to investment banking services) or with the subject company or companies mentioned in this report, no employee of RBI or of its affiliates has the

ability to influence the substance of the macroeconomic research reports prepared by the analysts of RBRO.

This research report is for information purposes only and may not be reproduced or distributed to other persons without RBRO´s permission. This document is governed by Romanian legislation in force and constitutes

neither a solicitation of an offer nor is it a prospectus in the sense of the Romania Capital Market Law no. 297/2004 or any other comparable foreign law. Unless otherwise explicitly set out herein, references to legal acts

refer to acts which are in force in Romania.

Any investment decision in respect of securities, financial products or investments may only be made on the basis of (i) an approved and published prospectus or (ii) the complete documentation that will be or has been

published in connection with the securities, financial products or investments in question and must not be made on the basis of this document. This document does not constitute a personal recommendation to buy or sell

financial instruments, or consultancy in the sense of the Capital Market Law no. 297/2004 or counseling/advisory of any kind.

Neither this document nor any of its components shall form the basis for any kind of contract or commitment whatsoever. This document is not a substitute for the necessary advice on the purchase or sale of securities,

investments or other financial products. In respect of the sale or purchase of securities/financial instruments, investments or financial products, an authorized advisor may provide individualized advice which might be

suitable for investments and financial products.

This document is fundamentally based on generally available information and not on any confidential information which the author that has prepared this document has obtained exclusively on the basis of his/her client

relationship with a third person. RBRO deems all of the information included herein to be reliable, but does not make any warranties regarding its accuracy and completeness. Nonetheless, where there is any doubt as to

whether a source is reliable, RBRO will clearly indicate this fact in the report.

27 27

Disclaimer Financial Analysis

Past performance is no guarantee for the future performance of the financial instruments. No assurance can be given regarding the favorable return of the financial instruments portfolio or of an issuer described in this

report. It is possible that, due to various factors, the projections are not met. Nor RBRO, nor any of its directors, officers or employees is responsible for any loss or damage that may result from the use of this document, of

its content or in some other way.

Any transaction with financial instruments involves risks among which are included but not limited to: the fluctuation of the prices in the relevant market; the unpredictability of dividends, profitability and profits; the

fluctuation of the exchange rates, of the interest rates and of the yields.

This document may include references to financial instruments in relation to which RBRO or any person closely associated with RBRO or part of the same financial group may act as market maker or liquidity provider,

lead manager or co-lead manager over the previous 12 months or is party to an agreement with the issuer relating to the provision of investment services offered by RBRO or relating to the production of present report.

As well, RBRO or any person closely associated with RBRO or part of the same financial group might have a long or short position at any time, including possibly a position that was accumulated on the basis of the

information contained herein prior to its dissemination. RBRO may engage in transactions, for its own account or with customers, in a manner inconsistent with the views taken in this document. Others within RBRO,

including strategists, sales staff and other analysts, may take views that are inconsistent with those taken in this document.

This document might have been disclosed to the issuer to which the recommendation, directly or indirectly, relates and might have been subsequently amended. Unless otherwise expressly stated herein, the analyst

that has drafted (or contributed to) this report is not compensated by RBRO for specific investment banking transactions. Compensation of the analyst or analysts of this report is based (among other things) on the

overall profitability of RBRO, which includes, inter alia, earnings from investment banking and other transactions of RBRO. In general, RBRO prohibits its analysts and persons contributing to the report to acquire securities

or other financial instruments of any company which is covered by the analysts (and contributing persons), unless such acquisition is authorized by RBRO´s compliance department in advance.

RBRO has established the following organizational and administrative agreements, including Chinese walls, to impede or prevent conflicts of interest in relation to recommendations: RBRO has designated fundamentally

binding confidentiality zones. Confidentiality zones are units within credit institutions, which are isolated from other units by organizational measures governing the exchange of information, because compliance-relevant

information is continuously or temporarily processed in these zones.

Compliance-relevant information must not leave a confidentiality zone and is to be treated as strictly confidential in internal business operations, including interaction with other units. This is not applicable to the transfer

of information necessary for usual business operations. Such transfer of information is limited, however, to what is absolutely necessary (need-to-know principle). The exchange of compliance-relevant information

between two confidentiality zones must only be conducted with the involvement of the compliance officer.

RBRO may have effected a proprietary transaction in any investments mentioned herein or in related investments and or may have a position or holding in such investments as a result. RBRO may have acted, or might

be acting, as a manager or co-manager in a public offering of any securities mentioned in this report or in any related security.

RBRO and/or its employees have no obligation to update, modify or amend or otherwise notify a recipient of this report if the information or recommendation stated herein changes or subsequently becomes

inaccurate. The frequency of subsequent reports, if any, remains in the discretion of the author and RBRO.

28 28

Disclaimer Financial Analysis

Disclosure Aspects as per legislation in force

1. RBRO or one of its affiliated legal entities owns a net long or short position exceeding the threshold of 0,5 % of the total issued share capital of the issuer, calculated in accordance with Article 3 of Regulation (EU) No

236/2012 and with Chapter III and IV of Commission Delegated Regulation (EU) No 918/2012;

2. RBRO or one of its affiliated legal entities holds more than 5% of the entire issued share capital of the issuer;

3. The issuer holds more than 5% of the entire issued share capital of RBRO or one of its affiliated legal entities;

4. RBRO or its affiliated companies have significant financial interests with respect to the issuer;

5. RBRO or one of its affiliated legal entities is a market maker (or specialist) or designated sponsor or stabilization manager or liquidity provider in the financial instruments of the issuer;

6. During the last 12 months, RBRO or one of its affiliated legal entities played a major role or was co-leader (e.g. as manager or co-manager) in a public offering of the financial instruments of the issuer;

7. During the last 12 months, RBRO or one of its affiliated legal entities has entered into an agreement on the provision of other investment banking services with the issuer (including assuming a role as a payment office)

or received compensation for such services during the same period (in this case, disclosure only occurs if it does not breach confidentiality in relation to business information);

8. RBRO or one of its affiliated legal entities has entered into an agreement with the issuer on the provision of investment recommendations;

9. The responsible analyst owns financial instruments of the issuer which s/he analyses;

10. The responsible analyst is a member of the executive board, the board of directors or supervisory board of the issuer which s/he analyses;

11. The responsible analyst or other natural persons, who are involved in preparing the financial analysis, received or acquired stocks in the issuer s/he analyses prior to the public offering of such. Prices at which stocks

have been acquired and the dates of acquisitions will be disclosed;

12. Compensation of the responsible analyst or other natural persons, who are involved in preparing the financial analysis, is linked to a RBRO’s transactions with the issuer in question, on own account or on the

account of one of its affiliated legal entities.

Applicable disclosures: No disclosures

This report was completed on: 15 May 2018, 11:50 AM

First dissemination on: 16 May 2018, 10:30 AM