Role of Nuclear Cogeneration in a Low Carbon Energy … of Nuclear Cogeneration in a Low Carbon...

14

© 2015 Organisation for Economic Co-operation and Development © 2015 Organisation for Economic Co-operation and Development Role of Nuclear Cogeneration in a Low Carbon Energy Future? NC2I Conference, Brussels, 14-15 September 2015 Dr. Henri PAILLERE Senior Nuclear Analyst, Nuclear Development Division [email protected]

Transcript of Role of Nuclear Cogeneration in a Low Carbon Energy … of Nuclear Cogeneration in a Low Carbon...

© 2015 Organisation for Economic Co-operation and Development © 2015 Organisation for Economic Co-operation and Development

Role of Nuclear Cogeneration in a

Low Carbon Energy Future?

NC2I Conference, Brussels, 14-15 September 2015

Dr. Henri PAILLERE Senior Nuclear Analyst,

Nuclear Development Division

© 2015 Organisation for Economic Co-operation and Development © 2015 Organisation for Economic Co-operation and Development 2

Nuclear Reactors: Generations I to IV

Bulk of today’s nuclear fleet

New build (essentially after

Fukushima Daiichi accident)

But only a fraction of today’s 438 reactors operate in cogeneration mode (essentially district heating)

(estimated 1% of total nuclear heat used to produce non-electric applications)

© 2015 Organisation for Economic Co-operation and Development © 2015 Organisation for Economic Co-operation and Development 3

Electricity Generation by Source (%), World and OECD

Nuclear energy is:

• The largest source of low C electricity in OECD countries (18% > 13.4% hydro)

• The 2nd largest at world level behind hydro (10.8% < 16.5% hydro)

2/3 world electricity still produced from fossil fuel!

© 2015 Organisation for Economic Co-operation and Development

But what about other sectors?

industry (process heat & industrial processes (H2 production, synthetic fuel

production, desalination…), buildings (district heating), transport sectors

Can nuclear energy also make a difference?

Nuclear energy = low carbon source of electricity AND heat

4

© 2015 Organisation for Economic Co-operation and Development © 2015 Organisation for Economic Co-operation and Development 5

Enhance security of energy supply

Improve energy (fuel) efficiencies

Reduce CO2 emissions

Minimize heat losses (2/3 heat wasted in current

nuclear steam cycles)

(non-nuclear) CHP since long applied in

many industrial sectors

Why nuclear cogeneration?

Potential in 4 areas: (i) desalination (ii) district

heating in residential/commercial areas (iii) industrial

process heat (iv) fuel synthesis (e.g. Hydrogen)

© 2015 Organisation for Economic Co-operation and Development © 2015 Organisation for Economic Co-operation and Development

Application Level of maturity Possible new projects &

recent activity

Challenges

District

Heating

Demonstrated at industrial

scale & currently operating

(Russia, Switzerland, …)

Option for future new build in

Finland or Poland, feasibility

studies in France for coupling

existing NPPs to DH systems

Differences between

electricity & heat markets.

Economic assessment.

Desalination Tested at industrial scale in

the past (BN-350)

Small small scale

applications in NPPs to

supply fresh water to plant

Huge needs in the future

(projects in the MENA region:

Egypt, Saudi Arabia?)

Complexity and scale of

investments in water

infrastructures.

Public acceptance?

Long term?

High

temperature

process heat

Demonstrated at industrial

scale for low temp. steam

applications.

R&D HTR and cogeneration

NHDD project in Korea “clean

steel”

NGNP Alliance & EU’s NC2I

collaboration

Synthetic fuel production

Business model (nuclear

operator industrial

application operator)

Licensing, safety, public

acceptance, Long term

Hydrogen

production

Demonstrated at lab scale for

thermochemical cycles

(HTTR) and HTE

NHDD in Korea, on-going R&D

(Gen IV)

Hydrogen economy?

Competition with electric

mobility?

Nuclear hybrid

energy system

R&D on low carbon energy

systems involving nuclear &

variable renewables

Assessment of services

provided by nuclear (electricity,

storage, heat)

Economic assessment

Long term prospects

6

© 2015 Organisation for Economic Co-operation and Development © 2015 Organisation for Economic Co-operation and Development 7

https://www.oecd-nea.org/pub/techroadmap/

© 2015 Organisation for Economic Co-operation and Development © 2015 Organisation for Economic Co-operation and Development

Key technologies to reduce emissions in the power

sector, from 6DS to 2DS: (from IEA ETP 2015)

Basket of low C technologies (incl. CCS) + ability to perform electricity savings

Cumulatively, nuclear (≈wind) is the technology allowing most CO2 savings up to 2050

Example of policy measures: CO2 price to increase to 100 USD/t CO2 in 2030, 170

USD/t CO2 in 2050

8

© 2015 Organisation for Economic Co-operation and Development © 2015 Organisation for Economic Co-operation and Development 9

CO2 is not the only problem! Air pollution (from particles

from fossil fuel combustion) is a greater health problem

WHO:

7 million

deaths/year due

to air pollution

(from cooking

stoves, transport,

and fossil-fuelled

power and

industrial plants

© 2015 Organisation for Economic Co-operation and Development © 2015 Organisation for Economic Co-operation and Development

Nuclear since 2010, update of early roadmap

• Fukushima Daiichi accident (March 2011)

– Impact on energy policies & public acceptance

– Safety evaluations and upgrades

• Aftermath of financial crisis (2007-2008) and

economic crisis

• Uranium market depreciation

• Shale gas revolution in the US (and US coal prices)

– Also affecting competitiveness of “nuclear cogeneration” vs. gas

• Cost overruns and delays in some FOAK Gen III projects

• Lower than anticipated costs for onshore wind and solar

PV

Eco

no

mic

s / C

om

pe

titio

n / M

ark

ets

10

© 2015 Organisation for Economic Co-operation and Development © 2015 Organisation for Economic Co-operation and Development

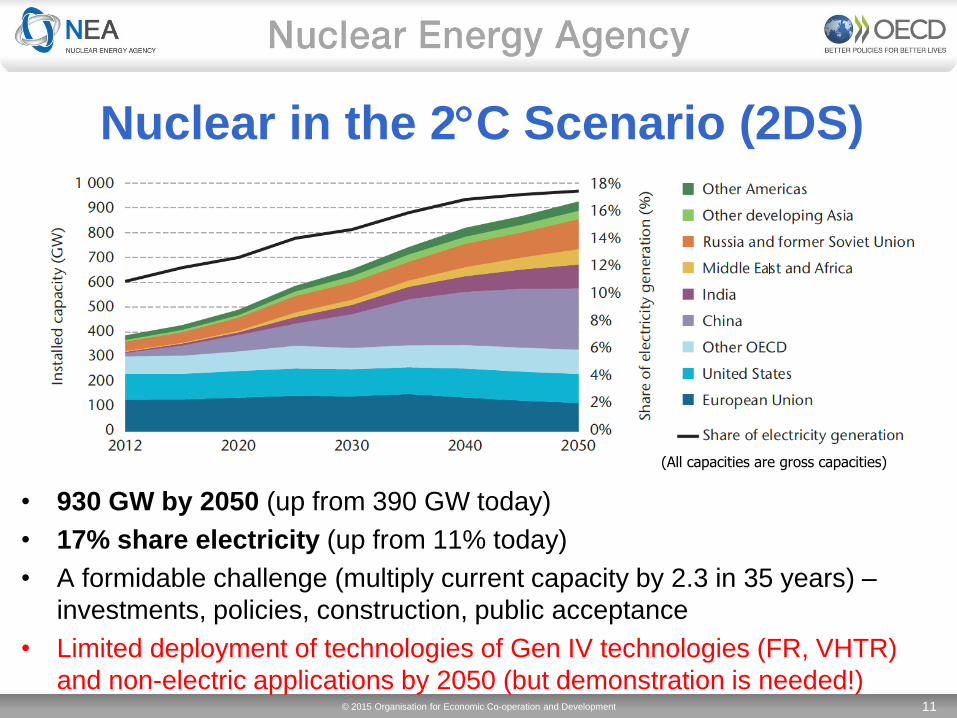

Nuclear in the 2C Scenario (2DS)

• 930 GW by 2050 (up from 390 GW today)

• 17% share electricity (up from 11% today)

• A formidable challenge (multiply current capacity by 2.3 in 35 years) –

investments, policies, construction, public acceptance

• Limited deployment of technologies of Gen IV technologies (FR, VHTR)

and non-electric applications by 2050 (but demonstration is needed!)

(All capacities are gross capacities)

11

© 2015 Organisation for Economic Co-operation and Development © 2015 Organisation for Economic Co-operation and Development 12

IEA/NEA Nuclear Technology Roadmap on

nuclear cogeneration

© 2015 Organisation for Economic Co-operation and Development © 2015 Organisation for Economic Co-operation and Development

Conclusions (1) Over 750 reactor-years of non-electric applications of nuclear

energy– though not always in a commercial / liberalised

market environment.

Cogeneration: Can improve the overall efficiency of NPPs;

Opens different streams of revenues to operators;

Can contribute significantly to reduction CO2 emissions from non-

power sector

Has a potential to play in future low C energy systems, where nuclear

would provide electricity & storage through production of fuels

Selling commercially both electricity and non-electric

products remains a challenge. Some economic assessment

tools exist but standardised methodologies for non-electric

applications missing.

Launch of an OECD/NEA Study in July 2015 (EC contribution

would be welcome!) 13

© 2015 Organisation for Economic Co-operation and Development © 2015 Organisation for Economic Co-operation and Development

Conclusions (2)

Significant development of non-electric applications of nuclear

energy are not expected in the short to mid-term, especially

if/where fossil-based alternatives (gas) remain cheap. Carbon

constraints / pricing is required

But RD&D is needed to prepare long term deployment

NEA launched the Nuclear Innovation 2050 initiative

Work needed to provide information to general public and

policy makers about nuclear cogeneration

OECD/NEA is following with great interest the development of

the NC2I in Europe, as well as other developments (N.

America, Japan, Korea)

14