Robotics Industry Report

14

Robotics Industry report 10/09/2014 Junaid Farooq

-

Upload

junaid-farooq -

Category

Documents

-

view

30 -

download

0

Transcript of Robotics Industry Report

Robotics Industry report

10/09/2014Junaid Farooq

History and Major Markets

• First robot introduced in US in 1961 developing into first electrical robot in 1973

• Large scale development in robot versatility during 200x• Early robots were designed for repeatability perfection

Industry Size ~ US$ 180bnFactory & process automation represent ~ 56% (US$ 100bn) & 44% (US$80bn) of total industry respectively

• Robot Markets:• China• USA• Japan• Germany• Korea

Robot Components & Deployment Costs• Motion control AC servomotors and drives represent ~US$18bn plus

market• Programmable logic controller (PLC)• Computer numerical control (CNC).Sold with motion control. Sale about

US$10bn per annum• Distributed control systems• Sensors• Mechanical actuators• Reduction gears manufactured by Nabtesco commanding 60% of global

market- Profit margin around 20% or nearly twice as high as an average robot manufacturers

• Deployment costs: • 20-25% of cost is the robot unit (manipulator)• 20-25% is the cost of auxiliary equipment• 50-60% of system cost is application software

Investment areas & Market Drivers

• Drivers:• E-commerce is one of the market drivers for robotic industry• Expanding middle class• Increasing labour costs and quality standards

Component market share in 2011

Growing market

• Global automation index increased considerably and leading as compared to MSCI world index

• Sharp increase in demand post GFC period

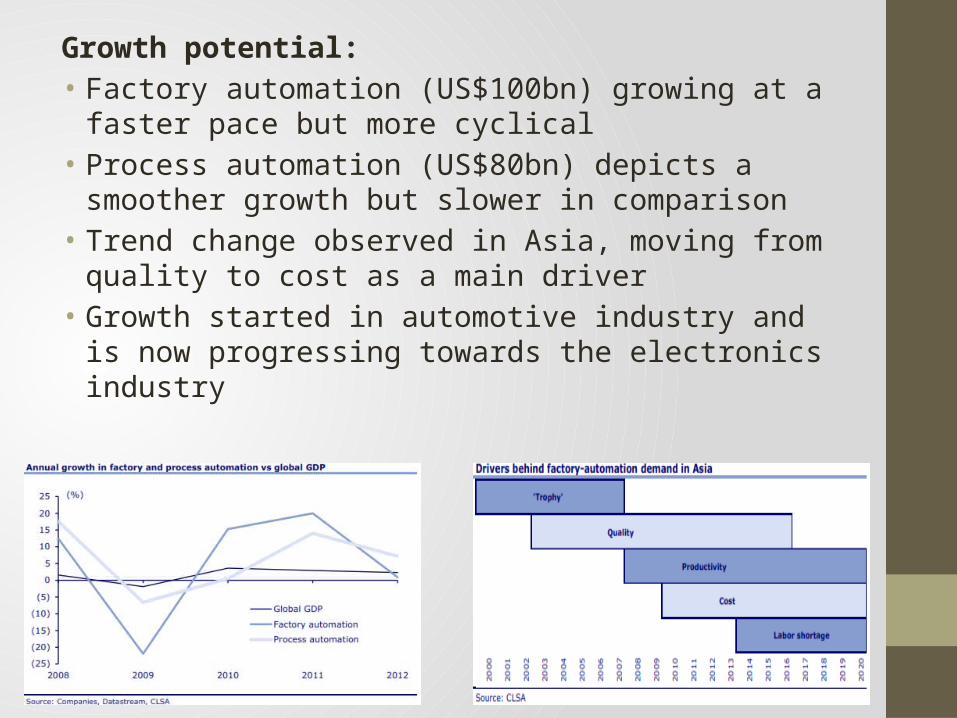

Growth potential:• Factory automation (US$100bn) growing at a faster pace but

more cyclical• Process automation (US$80bn) depicts a smoother growth but

slower in comparison• Trend change observed in Asia, moving from quality to cost as

a main driver• Growth started in automotive industry and is now progressing

towards the electronics industry

Segmentation of automation industry

Global growth forecast and big four market share

• The industry has seen an average compounded annual growth rate of 8% (2007-2013)

Projected revenue growth of the robotics market

China• China and other emerging markets investing heavily in

robotics• Biggest robot manufacturers in China is Siasun robotics

followed by GSK and Estun• Chinese lagging behind because of technology gap and

reliance on components from abroad. Foreign brands are the global standards

• Credit crunch in china. Imports from japan decreasing YoY • Increasing labour costs mean companies will prefer

automation

United States

• US market share dominated primarily by Fanuc• Market regaining strength after GFC• US manufacturing’s competitiveness improved due to weaker

dollar, labour cost containment and automation

Japan

• Weaker Yen attracting domestic CAPEX• Bold tax cuts and lease support from Japanese PM Shinzo Abe• Weak domestic consumption not encouraging manufacturers

to increase capacity

Conclusion

• Automation industry has grown dramatically but the technology has lacked behind and progressed at a much slower pace

• Growth observed in automation industry post GFC period• China to follow up technological advancements during the

next decade and thus does not present a competition globally yet

• Strong conviction that Japan’s automation recovery will be strong in the near future

• Payback period observed in the consideration of automation by manufacturers