Robo-Advisors for Portfolio Managementonlinepresent.org/proceedings/vol141_2016/21.pdf ·...

5

Robo-Advisors for Portfolio Management Jae Yeon Park 1 , Jae Pil Ryu 1 , Hyun Joon Shin 2,1* 1 KIS Pricing Inc., Seoul, Korea; {jaeyeon.park, jaepilryu}@kispricing.com 2 Department of Management Engineering, Sangmyung University, Cheonan, Korea; [email protected] Abstract. Recently, the demand that manage portfolio by using robo-advisor have been increasing. The scale of asset management with robo-advisor is two hundred trillion won, which is still relatively small amount but it is expected more than two thousand trillion won in 2020. Almost all the U.S. asset management companies which have a lot of investment and interest in robo- Advisor have invested huge sums of money to development and adaptation of robo-Advisor. And at the same time, they can cut cost as investment manpower decrease at the same time. Robo-advisor have advantages not only management cost saving result from low commission but also good decision making through systematic and quantitative analysis. In other words, robo-advisor is the system to make investment decision exclude human psychology or emotion. In this research, we investigate the effectiveness of Robo-advisor, basic principle of performance, and the current state of United States’ robo-advisor management corporations. Also, we compare and analyze Schwab Intelligent, Wealthfront and Betterment which are the representative robo-advisor manage corporation. They have similar basic investment strategy and philosophy of robo-advisor but, there are big differences in methodology such as investment asset type, or understanding customer’s tendency. Keywords: Robo-Advisors, Portfolio Management, Mean-Variance model, Certified Investment Manager 1 Research Background In modern society, most people have either a direct or an indirect interest in investing in financial instruments. However, many individual investors make investment decisions based on their limited knowledge on financial instruments rather than relying on professional knowledge. In contrast, institutional investors, armed with better information, invest huge amounts of their management funds; this constantly exposes them to risks caused by diverse unpredictable variables in the financial market. These conditions in the financial market have increased investors’ demand for robo-advisors. Robo-advisor is an artificial intelligence system that makes decisions based on algorithms by collecting vast quantities of big data. This decision-making * Corresponding author Advanced Science and Technology Letters Vol.141 (GST 2016), pp.104-108 http://dx.doi.org/10.14257/astl.2016.141.21 ISSN: 2287-1233 ASTL Copyright © 2016 SERSC

Transcript of Robo-Advisors for Portfolio Managementonlinepresent.org/proceedings/vol141_2016/21.pdf ·...

Robo-Advisors for Portfolio Management

Jae Yeon Park1 , Jae Pil Ryu1, Hyun Joon Shin2,1*

1KIS Pricing Inc., Seoul, Korea;

{jaeyeon.park, jaepilryu}@kispricing.com 2Department of Management Engineering, Sangmyung University, Cheonan, Korea;

Abstract. Recently, the demand that manage portfolio by using robo-advisor

have been increasing. The scale of asset management with robo-advisor is two

hundred trillion won, which is still relatively small amount but it is expected

more than two thousand trillion won in 2020. Almost all the U.S. asset

management companies which have a lot of investment and interest in robo-

Advisor have invested huge sums of money to development and adaptation of

robo-Advisor. And at the same time, they can cut cost as investment manpower

decrease at the same time. Robo-advisor have advantages not only management

cost saving result from low commission but also good decision making through

systematic and quantitative analysis. In other words, robo-advisor is the system

to make investment decision exclude human psychology or emotion. In this

research, we investigate the effectiveness of Robo-advisor, basic principle of

performance, and the current state of United States’ robo-advisor management

corporations. Also, we compare and analyze Schwab Intelligent, Wealthfront

and Betterment which are the representative robo-advisor manage corporation.

They have similar basic investment strategy and philosophy of robo-advisor

but, there are big differences in methodology such as investment asset type, or

understanding customer’s tendency.

Keywords: Robo-Advisors, Portfolio Management, Mean-Variance model,

Certified Investment Manager

1 Research Background

In modern society, most people have either a direct or an indirect interest in investing

in financial instruments. However, many individual investors make investment

decisions based on their limited knowledge on financial instruments rather than

relying on professional knowledge. In contrast, institutional investors, armed with

better information, invest huge amounts of their management funds; this constantly

exposes them to risks caused by diverse unpredictable variables in the financial

market. These conditions in the financial market have increased investors’ demand for

robo-advisors. Robo-advisor is an artificial intelligence system that makes decisions

based on algorithms by collecting vast quantities of big data. This decision-making

* Corresponding author

Advanced Science and Technology Letters Vol.141 (GST 2016), pp.104-108

http://dx.doi.org/10.14257/astl.2016.141.21

ISSN: 2287-1233 ASTL Copyright © 2016 SERSC

technique was demonstrated by AlphaGo, which is a computer program developed by

Google (Park, 2016).

As mentioned above, artificial intelligence technology has been embodied in the

form of robo-advisors that offer a novel asset management and customer service

system in the financial sector. People’s interest in robo-advisors has grown over time.

In particular, robo-advisors have certain advantages, such as high accessibility by

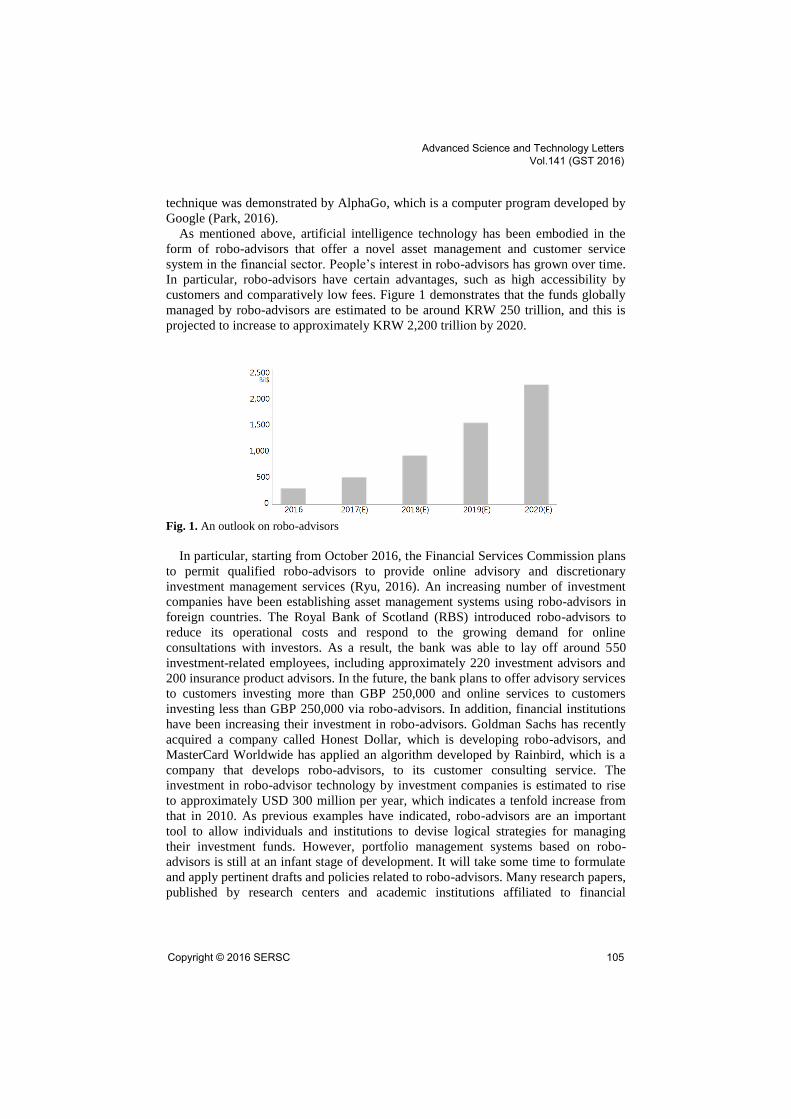

customers and comparatively low fees. Figure 1 demonstrates that the funds globally

managed by robo-advisors are estimated to be around KRW 250 trillion, and this is

projected to increase to approximately KRW 2,200 trillion by 2020.

Fig. 1. An outlook on robo-advisors

In particular, starting from October 2016, the Financial Services Commission plans

to permit qualified robo-advisors to provide online advisory and discretionary

investment management services (Ryu, 2016). An increasing number of investment

companies have been establishing asset management systems using robo-advisors in

foreign countries. The Royal Bank of Scotland (RBS) introduced robo-advisors to

reduce its operational costs and respond to the growing demand for online

consultations with investors. As a result, the bank was able to lay off around 550

investment-related employees, including approximately 220 investment advisors and

200 insurance product advisors. In the future, the bank plans to offer advisory services

to customers investing more than GBP 250,000 and online services to customers

investing less than GBP 250,000 via robo-advisors. In addition, financial institutions

have been increasing their investment in robo-advisors. Goldman Sachs has recently

acquired a company called Honest Dollar, which is developing robo-advisors, and

MasterCard Worldwide has applied an algorithm developed by Rainbird, which is a

company that develops robo-advisors, to its customer consulting service. The

investment in robo-advisor technology by investment companies is estimated to rise

to approximately USD 300 million per year, which indicates a tenfold increase from

that in 2010. As previous examples have indicated, robo-advisors are an important

tool to allow individuals and institutions to devise logical strategies for managing

their investment funds. However, portfolio management systems based on robo-

advisors is still at an infant stage of development. It will take some time to formulate

and apply pertinent drafts and policies related to robo-advisors. Many research papers,

published by research centers and academic institutions affiliated to financial

Advanced Science and Technology Letters Vol.141 (GST 2016)

Copyright © 2016 SERSC 105

investment companies, explain the advantages of robo-advisors and the visions for its

future growth.

2 Research Plan

This study is based on a survey, and thus, aims to collect and summarize detailed and

objective research data rather than qualitative or abstract data. It is composed of four

sub-topics, the details of which are as follows:

1 Introduce a mean-variance model, which is a basic model for portfolio

management based on robo-advisors, and explain its strengths and

weaknesses.

2 Discuss the common attributes of robo-advisors and passive indexing, and

explain the operating methods of robo-advisors.

3 Briefly introduce the techniques of robo-advisors deployed by diverse

financial management companies; compare and contrast the management

methods used by Schwab Intelligent, Wealthfront, and Betterment, all of

which are considered the most advanced in this field.

4 Explore the possibility of robo-advisors being an effective alternative to

traditional (funds or portfolio) management strategies.

This paper will focus on the current status of robo-advisors rather than a positive

vision of their future. In addition, by introducing U.S. representative firms that

manage the highest amount of funds through robo-advisors, we would like to describe

the realistic and effective features of robo-advisors rather than approaching the

subject from an academic and theoretical perspective.

3 Analysis of Asset Management Strategy of Robo-Advisors

3.1 Type of Investment Assets

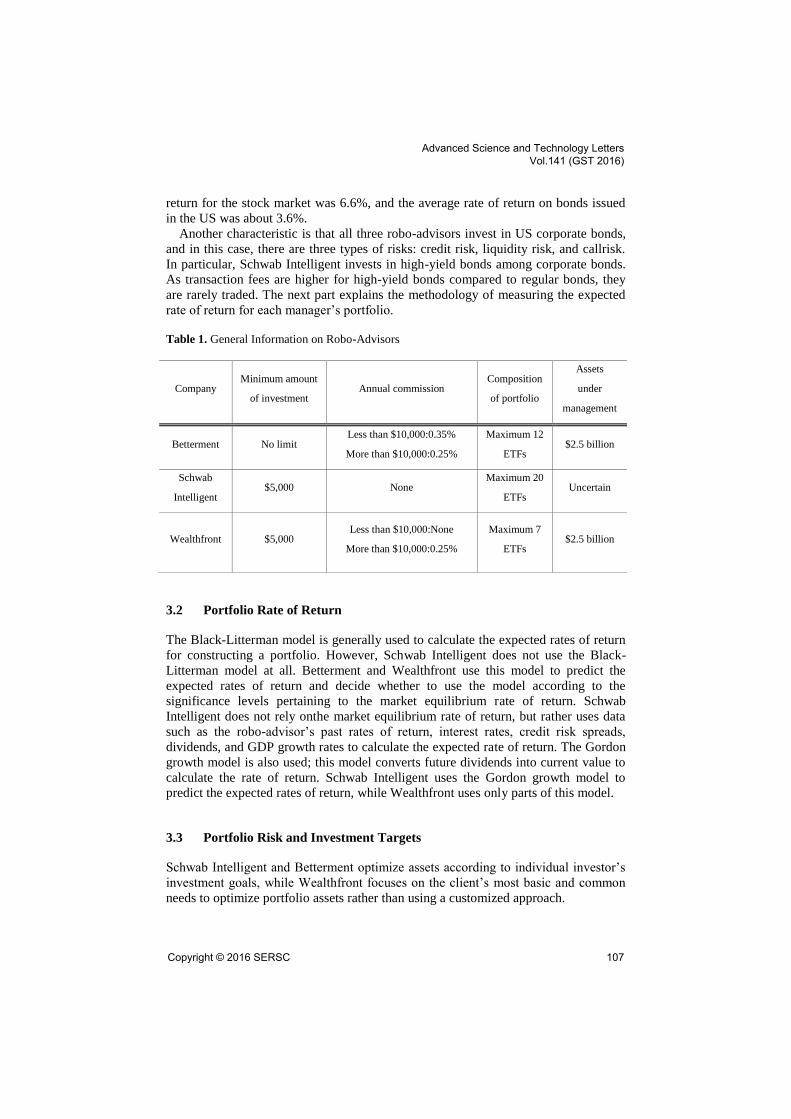

This part introduces major asset management companies that use robo-advisors, and

compares and analyzes their robo-advisor methodologies.US robo-advisors usually

demand that clients at least meet the minimum investment thresholds. Furthermore,

their portfolios have 10–20 assets and most of them are ETFs. The general

information on robo-advisors, as investigated in the study, is presented in Table 1

below.

Most robo-advisors automatically select and invest in stocks and bonds. For stocks,

there are cases where one sector is thoroughly divided up and invested in. Schwab

Intelligent invests in about 30 assets, and the other two companies invest in around 10

or less assets. In particular, all three companies are investing in global bonds when

using robo-advisors. There is a small difference in the asset types that the three

companies invest in, with Schwab Intelligent and Wealthfront investing in resources

such as gold and related ETFs. Betterment can be seen as lacking from a diversity

perspective. During the years 1802–2012, before gold prices were hit by volatility, the

average rate of return for gold and related ETF products was 0.7%, the average rate of

Advanced Science and Technology Letters Vol.141 (GST 2016)

106 Copyright © 2016 SERSC

return for the stock market was 6.6%, and the average rate of return on bonds issued

in the US was about 3.6%.

Another characteristic is that all three robo-advisors invest in US corporate bonds,

and in this case, there are three types of risks: credit risk, liquidity risk, and callrisk.

In particular, Schwab Intelligent invests in high-yield bonds among corporate bonds.

As transaction fees are higher for high-yield bonds compared to regular bonds, they

are rarely traded. The next part explains the methodology of measuring the expected

rate of return for each manager’s portfolio.

Table 1. General Information on Robo-Advisors

Company Minimum amount

of investment Annual commission

Composition

of portfolio

Assets

under

management

Betterment No limit Less than $10,000:0.35%

More than $10,000:0.25%

Maximum 12

ETFs $2.5 billion

Schwab

Intelligent $5,000 None

Maximum 20

ETFs Uncertain

Wealthfront $5,000 Less than $10,000:None

More than $10,000:0.25%

Maximum 7

ETFs $2.5 billion

3.2 Portfolio Rate of Return

The Black-Litterman model is generally used to calculate the expected rates of return

for constructing a portfolio. However, Schwab Intelligent does not use the Black-

Litterman model at all. Betterment and Wealthfront use this model to predict the

expected rates of return and decide whether to use the model according to the

significance levels pertaining to the market equilibrium rate of return. Schwab

Intelligent does not rely onthe market equilibrium rate of return, but rather uses data

such as the robo-advisor’s past rates of return, interest rates, credit risk spreads,

dividends, and GDP growth rates to calculate the expected rate of return. The Gordon

growth model is also used; this model converts future dividends into current value to

calculate the rate of return. Schwab Intelligent uses the Gordon growth model to

predict the expected rates of return, while Wealthfront uses only parts of this model.

3.3 Portfolio Risk and Investment Targets

Schwab Intelligent and Betterment optimize assets according to individual investor’s

investment goals, while Wealthfront focuses on the client’s most basic and common

needs to optimize portfolio assets rather than using a customized approach.

Advanced Science and Technology Letters Vol.141 (GST 2016)

Copyright © 2016 SERSC 107

Schwab Intelligent and Betterment have different methods for measuring investors’

risk preference and investment goals. Schwab Intelligent uses a questionnaire to

measure investors’ risk preference, whereas Wealthfront measures the extent to which

each client handles risk through a behavioral approach. Betterment does not use a

behavioral approach, but rather uses the glide path, an asset allocation method, in all

cases except for retirement planning. Thus, the investment asset types of the three

companies vary according to clients’ investment goals and risk profiles.

4 Conclusion

This study examined US asset management firms that use robo-advisors to manage

assets, and investigated the robo-advisor strategies of the top companies, namely

Schwab Intelligent, Wealthfront, and Betterment. As described above, their

investment philosophies for robo-advisors are similar, but each robo-advisor uses

different approaches in its process of selecting asset types and assets to invest in.

References

1. Park, J.H., Ryu, J.P., Shin, H.J.: Predicting KOSPI Stock Index using Machine Learning

Algorithms with Technical Indicators. Journal of Information Technology and

Architecture, vol. 13, pp. 331-340 (2016)

2. Ryu, J.P., Han, C.H., Shin, H.J.: Sector Investment Strategies Using Big Data Trends.

Journal of Information Technology and Architecture, vol. 13. pp. 111-121 (2016)

3. Gladden, M.E.: Cryptocurrency with a Conscience: Using Artificial Intelligence to

Develop Money that Advances Human Ethical Values. Ethics in Economic Life, vol. 18.

pp. 85-98 (2015)

4. Sendhil, M., Noeth, M., Schoar, A.: The Market for Financial Advice: An Audit Study.

National bureau of economic research, DOI: 10.2139/ssrn.1572334 (2012)

5. Taleb, N.N., Blyth, M.: The Black Swan of Cairo: How Suppressing Volatility Makes the

World Less Predictable and More Dangerous. Foreign Affairs, vol. 90. pp. 33-39 (2011)

Advanced Science and Technology Letters Vol.141 (GST 2016)

108 Copyright © 2016 SERSC