Roadshow Jun 12 Eng

31

Corporate Presentation June/2012

description

Transcript of Roadshow Jun 12 Eng

Corporate PresentationJune/2012

2

The forward-looking statements contained in this presentation are based on the current assumptions and outlook of the Company’s management. Actual results, performance and events may differ significantly from those expressed or implied in these forward-looking statements as a result of several factors such as the general and economic conditions in Brazil and abroad, interest and exchange rates, future renegotiations or pre-payments of liabilities or loans denominated in foreign currency, changes in laws and regulations, and general competitive factors (regionally, nationally or internationally).

Disclaimer

3

Overview

(1) Besides the 46 hotels, we also own a minority interest in the Everest Hotels Chain (3 hotels).(2) 42,566,797 common shares.

BHG at a Glance

Brazil’s third largest hotel Company;

Focused on business tourism (three and four-star brands) in areas with high economic activity;

46¹ hotels throughout Brazil’s main regions, with a total of 8,431 rooms;

Net Revenue of R$ 51.7 mm and Hotel EBITDA of R$ 14.9 mm in the 1Q12;

16 properties in strategic locations for tourism-oriented development along the Brazilian coast;

Listed on the Novo Mercado segment of BM&FBovespa;

Shareholder Structure (04/30/12)²

Traded in the OTC Market in New York under the ticker BZHGY.

20 hotels under development throughout Brazil, which will add approx. 4,000 rooms by 2015;

LA HOTELS LLC + GPCP4 = 44.6%

MFC GLOBAL INVESTMENT = 9.0%JHL = 5.8%

ES TOURISM EUROPE = 5.4%

TREASURY = 1.1%

BOARD OF DIRECTORS & EXECUTIVES = 1.1%

OTHERS = 32.4%

4

3

Acquisition of Hotels

2

Management of Third Parties’ Hotel

Development of New Hotels

1

► Accelerate expansion► Increase the scale of

operation and brand exposure

► Entry into the Budget Segment

Franchising

4

► Highly fragmented market

► Old, poorly kept hotels

► Capacity to turnaround assets

► Track-record of attractive acquisitions

► Balanced Capital Structure

► Fee business► No overlap with

consolidation opportunities

► Increased scale benefits BHG bargain power with suppliers and customers

► Low penetration► Absence of major

companies► Expertise to

develop and operate hotels

... and its goal is to become the largest Hotel company in Brazil

BHG’s Consolidation StrategyBHG has multiple growth drivers…

5

2009 2010 2011 2012 2013 2014 2015

70%

30%

58%

42%

51%

49%

56%

44%

58%

42%

60%

40%

65%

35%

BHG’s Timeline and Announced Deals

► BHG initiated its operations in February 2009, after a merger between:

• Invest Tur : A company created in 2007, that raised R$ 945 million in an IPO for the development of 2nd home properties on Brazilian beaches;

• L.A. Hotel : A GP Investments company created in January 2008, focused on the business tourism hotel segment.

The Hotels managed figures does not include the minority participation in the 3 hotels part of the Everest Hotel Chain;The numbers presented above illustrates the position in the end of each year.

For the years 2012 through 2015, the number of rooms and hotels are based on information already disclosed to the market:

Hotels Under Management:

Fully Owned

Partially Owned

Third-Party Properties

Owned Rooms

Managed Rooms

%CAGR 09-14

15%

14%

18%

BHG is the first listed Brazilian company to operate in the tourism-oriented real estate segment.

5,293 5,8947,222

8,83610,220 10,900

12,480

31 34 37 48 55 59 66

11 15 16 16 16 16 16

2 3 5 9 16 18 18

18 16 16 23 23 25 32

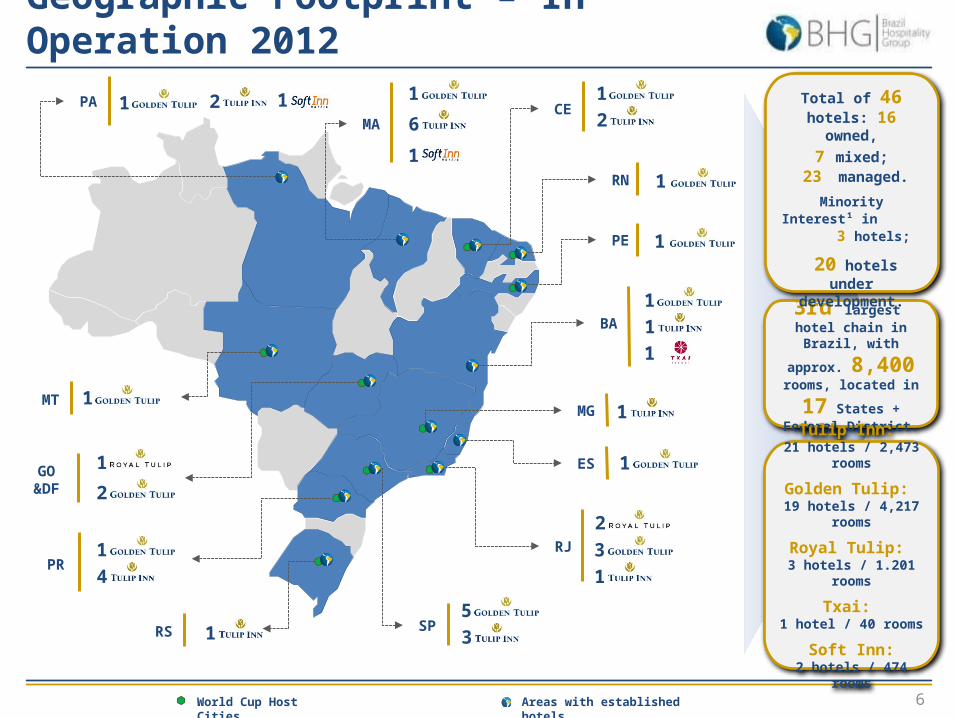

6

SP

3

2

1

1

5

3

1

1

2

1

6

1

12

1

1

4

1

2

1

1

1

1

1

ES

RJ

BA

PE

RN

CEMA

PA 1

RS

PR

GO &DF

MT

3rd largest hotel chain in Brazil, with approx.

8,400 rooms, located

in 17 States + Federal District.

Total of 46 hotels: 16 owned,

7 mixed; 23 managed.

Minority Interest¹ in 3 hotels;

20 hotels under development.

Tulip Inn: 21 hotels / 2,473 rooms

Golden Tulip: 19 hotels / 4,217 rooms

Royal Tulip: 3 hotels / 1.201 rooms

Txai: 1 hotel / 40 rooms

Soft Inn:2 hotels / 474 rooms

Geographic Footprint – In Operation 2012

Areas with established hotelsWorld Cup Host Cities

MG 1

7

Rio de Janeiro

TI Angra dos Reis

TI Campos

TI Itaguaí

Paraná

Belo Horizonte

TI Savassi

Areas with established hotelsWorld Cup Host Cities

Owned

Managed

Under Development

Key

RT = GT = TI = SI =

SI Maringá

Campo Grande

TI Campo Grande

Fortaleza

TI Sobral

Palmas

GT Palmas

TI Palmas

Belém

RT Bolonha

TI Hangar

SI Hangar

GT Belo Horizonte

Geographic Footprint – Under Development

Maceió

Gran Solare

TI Maringá

TI Marabá

GT Marabá

Maranhão

SI Imperatriz

TI Castanhal

Gran Solare

20 hotels under development, with

a total of aprox. 4,000 rooms until

2015

8

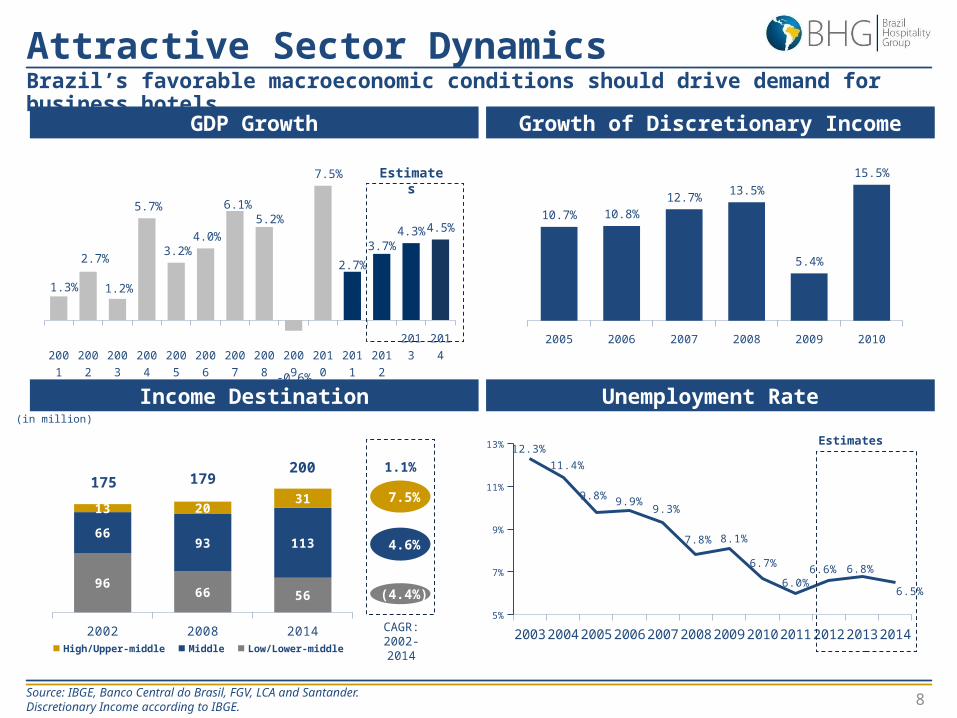

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

1.3%

2.7%

1.2%

5.7%

3.2%4.0%

6.1%5.2%

-0.6%

7.5%

2.7%

3.7%4.3% 4.5%

GDP Growth Growth of Discretionary Income

Income Destination Unemployment Rate(in million)

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 20145%

7%

9%

11%

13% 12.3%11.4%

9.8% 9.9%9.3%

7.8% 8.1%

6.7%

6.0%6.6% 6.8%

6.5%

2005 2006 2007 2008 2009 2010

10.7% 10.8%12.7% 13.5%

5.4%

15.5%Estimates

2002 2008 2014

9666 56

6693 113

13 2031

High/Upper-middle Middle Low/Lower-middle

200175

Attractive Sector DynamicsBrazil’s favorable macroeconomic conditions should drive demand for business hotels.

Source: IBGE, Banco Central do Brasil, FGV, LCA and Santander.Discretionary Income according to IBGE.

7.5%

4.6%

(4.4%)

CAGR: 2002-2014

1.1%179

Estimates

9

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

5.0 5.4 6.4 7.1 8.1 7.8

8.9 8.6 9.3 10.2

11.1

► Important events in Brazil: Rio + 20 (2012), Confederation Cup

(2013), World Youth Day (2013), World Cup (2014), Copa

América (2017) and Olympic Games (2016);

► Massive investments, over R$110bn, in infrastructure to adopt

the stadia and to prepare host cities;

► BNDES launched a credit line of R$1bn for the hotel sector to

support investments and construction of hotels.

Relevant Upcoming Events Arrivals of Foreign Tourists in Brazil

2014 World Cup and 2016 Olympic Games will consolidate Brazil as a tourist destination.

Domestic Passenger Air Traffic in Brazil

(in million)

(in million)

Attractive Sector DynamicsBrazil’s booming business activity combined with the country’s unique natural environment creates favorable dynamics for tourism.

CAGR 10E-20E = 7.3%

Source: IBGE, Ministério do Turismo, Embraer and Research Reports.

2007 2008 2009 2010 2011

44.4 47.8 56.2

68.3

79.0

+15.8%

10

Accor

Atlântica

BHG

Blue Tree

Nacional

Inn

Transam

érica

Sol M

eliá

Allia Hotel

s

Windso

r

Slave

iro

Owned Managed

Natural Consolidator

Hotel Industry in Brazil Number of Rooms (Jun/12)

Number of hotels Number of rooms

6.1%12.9%6.0%

16.4%

87.9%

70.7%

Independent International chains National chains

6,076 Hotels 410,327 rooms

44% 90%86% 100%

21,028

12,876

4,172 3,986 2,940 3,391 2,930 2,7722,819

BHG has approximately 8,300 rooms among its owned and managed properties, taking advantages of synergies of scale in its operations.

Source: Jones Lang La Salle and BHG estimates.

17%

8,431

11

Economies of Scale

Proven capacity to integrate and turnaround targets hotels

Main Synergies

► Better allocation of clients among hotels, minimizing sales losses;

► Marketing synergies strengthening brands;

► National / international sales force - call centers in Brazil and abroad;

► Negotiating power with travel agencies and tour operators;

► Scale to serve corporate clients in various regions.

Commercial

► Professional administration instead of family managed;

► Centralized administrative operations;

► Joint negotiation of supply contracts;

► IT systems that allow major cost reductions;

► Benchmark of best operational practices among the various hotels;

► Capacity for attraction and retention of talent.

Operational / Administrative

72% of all hotel rooms in Brazil are independently managed, creating the opportunity for post-acquisition operational turnaround

(1) 2008 - February 2011: 231 rooms in operation; In March/2011: 327 rooms in operation.

RevPar (R$)

EBITDA (R$ million)Hotel’s Acquisition (fev/2008)

2007 2009 2011

2.6

6.3

10.4

Golden Tulip Regente Case¹

Daily Rate of R$ 180;

OCC of 66%

Daily Rate of R$ 278; OCC of 76%

2007 2009 2011

120.0

170.0

212.0

12

EBITDA Multiples

2012 7.0x

2011 8.5x

2009 9.8x

2007 19.7x

EBITDA (R$ million)

2012 13.6

2011 10.4

2009 6.3

2007¹ 2.6

Golden Tulip Regente Case

Total Invested Value

BHG significantly improved the hotel's EBITDA reducing it's multiple and the time required for the investment's capital return since it’s acquisition in fev/08.

2007¹ = EBITDA generated by the former owner.

Estimate

Estimate

2007 2009 2011 2012

51.2

61.8

88.694.9

13

Acquisition Track Record and Pipeline• BHG has a solid track record of acquiring operating properties and a robust pipeline.

Projects

RoomsShare

(%)Price ¹

(R$ million)Mult.² 2013

Hotel A(Rio de Janeiro)

143 100% $105.0 9.1x

Hotel B(Rio de Janeiro)

189 100% $199.1 9.3x

Hotel C(Porto Alegre)

171 100% $60.0 7.1x

Hotel D(Maceió)

149 100% $18.5 5.3x

Hotel E(Fortaleza)

202 20% $9.3 5.8x

Hotel F(São Luis)

243 20% $11.4 6.3x

Hotel G(Joinville)

140 100% $17.0 6.8x

Hotel H(Uberlândia)

128 25% $3.8 5.4x

TOTAL 1,365 - $424.1 6.9x

Acquisition Track Record Acquisition Pipeline

316 million invested in 2011

EverestRooms: 181

(8,5%)

2010

Batista Campos and Nazaré

Rooms: 190

2010

IntercontinentalRooms: 418

2010

SofitelRooms: 388

2011

Soft Inn “Plus” Batista CamposRooms: 258

2011

Golden Tulip Recife PalaceRooms: 299

2010

Tulip Inn Hangar and Soft Inn

Hangar

Rooms: 1322011

Golden Tulip Connext

Rooms: 1272011

Historical Multiple of

Acquisitions of 7.6x

(08-12).

1) Includes retrofit expenses;2) Multiple EBITDA = BHG’s EBITDA Share + administration fees after taxes (when applied).

14

Tulip Inn Model Strategy

Tulip Inn Double Room (Project) Tulip Inn Double Room (Preview)

► Project model with 140 apartments;

► Construction timeframe of 30 months;► Including 6 months for licensing and project

approval;

► BHG’s share of the project will usually be: 25%;

► Land Acquisition estimated at 25% of the construction’s cost;

► SPE 60% with Long Term debt (BNDES);► Debt Cost: TJPL + 3,8%► Term:12 years with 4 years of interest grace period

► We conducted a Geographical Study which defined 31 target cities as potential markets to be explored;

► Our strategy is to develop and construct around 5,600 new rooms between 2011 and 2016;

► Total Equity necessary from BHG will be R$ 100 million, considering that we will leverage 60% though BNDES and have partners from the remaining portion.

We will also build new economic hotels (greenfield projects)Greenfield Hotels

15

Done Deals & Pipeline | Greenfield Hotels

*Investment¹ = BHG’s participation share in the deal; Multiple 2015² = Considering BHG´s share on the hotel´s EBITDA + management fees.

Projects

RoomsInvest.¹(R$ mm)

Share (%) LaunchMult. 2015²

Itaguaí(Rio de Janeiro)

200 $6.5 53% 2013 3.5x

Campos(Rio de Janeiro)

160 $20.0 100% 2013 7.8x

Maringá(Paraná)

228 $9.5 51% 2013 3.4x

Palmas(Tocantins)

140 $5.0 50% 2013 2.7x

Belo Horizonte(Minas Gerais)

240 $16.7 25% 2014 7.3x

Sobral(Ceará)

120 $3.0 33% 2013 2.8x

Angra dos Reis(Rio de Janeiro)

120 $3.6 33% 2014 2.6x

Campo Grande(MS)

140 7.0 33% 2014 4.9x

TOTAL 1,348 $71.3 - - 4.4x

Done Deals

Projects

RoomsInvest.¹(R$ mm)

Share (%) LaunchMult. 2015²

Uberlândia (MG)

302 $3.0 10% 2013 5.5x

Porto Velho(RO)

200 $12.0 51% 2015 5.8x

Marabá(PA)

200 $12.0 51% 2015 6.6x

São José do Rio Preto (SP)

140 $10.0 51% 2014 6.2x

Sorocaba (SP)

140 $10.0 51% 2014 6.2x

Campinas(SP)

140 $10.0 51% 2014 6.2x

Macaé (RJ)

150 5.0 25% 2014 5.0x

Resende (RJ)

140 5.0 25% 2014 5.0x

TOTAL 1,412 $67.0 - - 5.8x

Pipeline

• The Done Deals listed above only illustrates the Tulip Inn Greenfield Projects where BHG holds equity participation.

16

► Golden Tulip Hospitality is part of an international hotel company with more than 1,000 hotels in 40 countries

► In July of 2009, Golden Tulip was acquired by Starwood Capital, becoming the world’s 8th largest hotel chain

► Brands:

– 5 star:

– 4 star:

– 3 star:

► BHG – Golden Tulip Agreement:– Exclusive use of the Golden Tulip brand in

South America– Benefits in royalty and international

marketing fees– Access to an international distribution

network and call centers around the world– Use of Value Drivers, Golden Tulip’s

commercial tools – Access to Golden Tulip miles program

(Flavours)

Description Benefits for BHG

► 6-star resort in Itacaré, BA► Established tourist destination with one of

the best resorts in the country and the world

► BHG-owned brand

► Use of the Txai brand in real estate development projects

► Leverage of the Txai brand in condo-hotel and villa/home launches

► Synergies with Txai projects

BHG has an exclusivity agreement with Golden Tulip allowing access to an international distribution network and guaranteeing operating standards in its hotels.

Strong Brands

► The Soft Inn brand allows BHG to operate in every segment of the Hotel Industry, acessing all kinds of guest profiles.

► Budget:

► Group recently acquired by BHG

17

Tier 1 Management Team

BHG has a team of top executives with broad experience in various industries.

- Bachelors degree in Hotel Management (Cornell University)- Bachelors degree in Management (Hotel Man. Sch. Les Roches)- M&A manager of Odebrecht- M&A director of Westmont Hospitality Group

Fabrício MuzzioDirector of Investments

- Master degree in International Business (Florida Int. Univ.)- Bachelors degree in Hotel Management (FIU e HHS Hague)- CEO of Brazil Fast Food Corporation- Occupied different positions in marketing and sales of Shell

Pieter van Voorst VaderCEO

Ricardo LevyCFO & IRO- MBA in Management (Coppead)- Bachelors degree in Management (PUC-RJ)- Former financial superintendent of Light (energy provider)

Reginaldo L. OliviOperations Officer- Bachelors degree in Economics (PUC-SP)- Director of Grupo Chambertin Hotels Administration- Director of Olivi Advising and Consultancy

André Luiz D. LameiroCommercial Officer- Bachelors degree in Economics (FMV)- Bachelors degree in Marketing (Amnnhembi)- Director of Grupo Chambertin Hotels Administration

► Latin America’s leader in private equity

► Raised more than US$4 billion from private equity investors

► Concluded 48 investments in 15 different sectors

► In May of 2006, became the first private equity firm to list on a Latin American stock exchange

► Counts on a group of experienced professionals recognized by the market for their expertise

Focused Management Team and Sponsorship

18

Geographic Footprint

BHG’s strategy for the land bank is to monetize the properties through environmental licenses and partnerships.

* Values in R$ million. ¹ Book Value considering only BHG’s share. TBD = To Be Defined. PSV* = Estimated PSV.

1 Project under development. 50% sold on the 1st sales lot.

2 properties for development

2 long-term land banks

1 long-term land bank

8 properties for development

2 properties for development

Other properties

Canavieiras I BA 569 26,6 8,2 -

Txai Paraty RJ 480 12,3 4,8 -

Canavieiras II BA 577 16,0 8,4 -

Carro Quebrado AL 1.265 22,6 7,6 -

Deep Beach RJ 2.260 30,1 12,3 -

Txai Salvador BA 5 6,9 2,7 -

Canavieiras III BA 102 4,8 1,3 -

Wind Beach CE 11.254 9,0 5,4 -

Nossa Shra. Vit. BA 729 10,8 4,6 -

Wind Farm

Long Beach CE 54.014 13,1 8,5 1.75%

Port Beach PI/MA 8.332 13,8 5,9 TBD

Total Book Value - 288,0 159,0 -

Rent

Properties States Sqmt Invest. Value

Book Value¹ PSV*

Under development

Txai Terravista BA 72 15,9 9,4 63,0

Txai Ganchos SC 530 8,1 3,1 117,5

Conduru BA 430 12,7 10,3 26,1

Properties States Sqmt Invest. Value

Book Value¹

Negotiated Value

Done Deals

Kino SP 7.200 45,4 26,8 52,4

Txai Itacaré BA - - 18,5 18,5

P. Camaragibe AL 1.630 56,6 32,4 TBD

Singlehome BA 3.695 28,7 25,1 TBD

Land Bank | Additional Source of Value

Greenfield areas

States where BHG operates

19

2012201120102009

189.4157.7

153.8125.0

2012201120102009

67.3%66.9%

64.2%

65.1%

Occupancy Rate (%) Daily Rate (R$)

Hotel’s Indicators: 2009 - 2012The performance of Company's hotel's indicators since 2009, including projections for 2012 and 2014 – when Brazil will host FIFA's World Cup.

Estimate

Estimate

Estimate

RevPar (R$)

8.1%

2012201120102009

262.0235.5

229.9194.52.4%

2.5%

20

Net Operating Revenue (in R$ mm) Hotel’s EBITDA (in R$ mm) and Margin (%)

Company’s EBITDA (in R$ mm) and Margin (%) Net Profit (in R$ mm)

Driven by the maturity of the acquired hotels, BHG expects a solid growth in EBITDA and Net Operating Revenue for 2012.

Historical Financial Highlights

201120102009

9.6

(6.2)

2.6

2009 2010 2011(10.9)

10.7

41.9

(14.2)

8.7

23.7

201120102009

176.6

121.8

76.9

2009 2010 2011

19.3

33.0

58.225.1

27.1

33.0

21

At the end of 2011, the Company reappraised hotels acquired more than 3 years ago in Rio de Janeiro and São Paulo, which are recorded under property, plant and equipment in the amount of R$133.5 million. Upon reappraisal by the consulting firm APSIS, a specialist in the reappraisal of assets, the properties were valued at R$465.9 million. Even so, the difference of R$332.4 million was not recorded in the Company’s balance sheet,

Financial Highlights | 2011

When considering only the calculation of Net Asset Value (NAV) using the new market value of the Company’s assets, it is clear that BHG is undervalued, with a difference between NAV in 2011 without and with adjustments of 48.5%.

Annual Data

Indicators 2011 Unadjusted 2011 Adjusted

Portfólio R$ million 885.5 1,217.8

Hotels R$ million 727.3 1,059.7

Landbank R$ million 158.2 158.2

Net Debt R$ million (199.6) (199.6)

NAV R$ million 685.9 1,018.2

No. of Shares Million 41.1 41.1

NAV/shares R$ 16.70 24.79

Share Price R$ 15.50 15.50

% of NAV % 92.8% 62.5%

2011 = Price on 12/31/11;

22

Leadership Position and Scalability

Natural Consolidator

Strong Brands

Focused Management Team and Sponsorship

Land bank: Additional Source of Capital

Attractive Sector Dynamics

1

2

3

4

5

6

Investment Case Key PointsBHG has competitive advantages that position it to become the largest and most profitable player in the Brazilian hotel industry.

Financial Highlights1Q12

24

Hotel’s Indicators – SSS¹ Hotel’s EBITDA (R$ mm) and margin (%) – SSS¹

Financial Highlights | 1Q12

(1) The 1Q12 results consider the same base of owned hotels in 1Q11, totaling 2,533 owned rooms (“Same Store Sales”).

Hotel’s Indicators Hotel’s EBITDA (R$ mm) and margin (%)

1Q11 4Q11 1Q12

12.915.8

13.9

34.1%36.6%

31.8%

1Q11 4Q11 1Q12

142.1155.8 164.5

216.1230.3

258.3

65.8% 67.7% 63.7%

RevPar (R$) Average Daily Rate (R$) Occupancy (%)

1Q11 4Q11 1Q12

147.4160.2 161.1

225.6239.2

261.8

65.3% 67.0% 61.5%

RevPar (R$) Average Daily Rate (R$) Occupancy (%)

13.2

18.8

14.9

32.4%35.0%

28.8%

1Q11 4Q11 1Q12

25

Gross Operating Revenue (R$ mm)

Net Profit (R$ million)

Financial Highlights | 1Q12

BHG’s EBITDA (R$ mm) and EBITDA margin(%)

Net Operating Revenue - NOR (R$ million)

40.8

53.8 51.7

1Q11 4Q11 1Q12

4.5% 3.8% 4.2%21.3%

24.6% 20.9%

74.2%

71.6%74.9%

1Q11 4Q11 1Q12

Management Fees F&B Room Revenue

45.0

57.460.2

7.2

16.7

11.4

17.7

31.1

22.0

1Q11 4Q11 1Q12

26

2Q09 3Q09 4Q09 1Q10 2Q10 3Q10 4Q10 1Q11 2Q11 3Q11 4Q11 1Q12

4.2 4.8 4.5 6.6 6.1

10.5 11.3 13.2 12.2

14.1

18.8

14.9

2Q09 3Q09 4Q09 1Q10 2Q10 3Q10 4Q10 1Q11 2Q11 3Q11 4Q11 1Q12

16.8 18.3 21.3 22.129.0

35.3 37.2 40.8 39.8 42.3

53.8 51.7

(R$ thousand)

(R$ thousand)

727.3

Asset

27.3

Hotels portfolio

262.0

234.7

Total Debt

Total Cash & Cash Equivalents

Net Debt

23# of properties*

158.4Landbank areas

16# of properties

Balance Sheet

725.8Net Equity

Net Operating Revenue

Hotel´s EBITDA

BHG – 1Q12 (in R$ mm)

Financial Highlights | 1Q12BHG has a balanced capital structure, key for its strategy of consolidating the hotel industry.

CAGR = 12.2%

CAGR = 10.8%

* Includes owned and partially owned hotels.

27

The hotels operation presented a Net Revenue of R$51.7 mm and EBITDA of R$14.9 mm in 1Q12. Company’s EBITDA reached R$ 14.9mm and a Net Loss of R$ 2.4 mm.

Financial Highlights | 1Q12

BHG (R$ million)1Q12 4Q11 1Q11 ∆% (1Q12

X 4Q11)∆% (1Q12 X 1Q11)

Net Revenues 51.7 53.8 40.8 -3.8% 26.8%

(-) Cost of Services (15.9) (16.1) (12.4) -1.1% 28.2%

(-) Hotel Adm. Exp. (14.8) (13.4) (10.0) 10.7% 47.9%

(-) Maintenance (2.3) (1.8) (1.9) 25.8% 22.8%

(-) Marketing and Commercial Exp. (3.9) (3.7) (3.3) 4.6% 16.9%

HOTEL - EBITDA 14.9 18.8 13.2 -20.9% 12.5%

(+) Rev. from Non - Ope. Prop. 3.2 5.0 - n.m. n.m.

(-) Administrative Expenses (5.3) (5.5) (4.2) -3.1% 27.3%

(+/-) Real Estate Op. Expenses (1.3) (1.6) (1.8) -15.4% -26.4%

BHG - EBITDA 11.4 16.7 7.2 -32.2% 57.3%

(+/-) Depre./Amort. (6.1) (4.0) (3.5) 50.2% 74.0%

(+/-) Financial Result (7.9) (6.4) (0.6) 23.1% 1137.4%

(+/-) Others 2.0 1.2 6.7 n.m. n.m.

(+/-) Minority Interest 0.3 0.3 0.2 0.9% 32.1%

(-) Taxes and Social Cont. (2.3) (4.1) (3.8) -44.7% -40.7%

Net Profit/Loss (2.5) 3.7 6.3 -169.5% -140.7%

28

EBITDA Margin and Business MixEBITDA Margin(1)

Lodging Corps Lodging REITs

Full-Service Select-Service

Business Mix (EBITDA) (1)

1. Reflects full year 2010 results, except where noted;Source: Barclays.

CHH IHGMAR

HOT

Whitb

read

BHG

Mandari

n

Sol M

elia H

MHGC

Posadas

Accor

RLH

NH Hoteles

Rezidor

0%

10%

20%

30%

40%

50%

60%

70% 64%

34%29% 27% 27% 24% 21% 19% 18% 18% 15% 15% 14% 11%

4%

LHO DRH HST RLJ CLDT HT INN

27%23%

19%

29% 29% 27% 25%

CHH IHGMAR

HOT

Mandari

n

Sol M

elia H

MHGC

Posadas

Accor

RHL

Rezidor

LHO

DRHHST RLJ

CLDT HT

INN0%

20%

40%

60%

80%

100%

100%87%

57%45%

17%35% 28%

44%32%

66%

13%

19% 38%83%

75%

56% 72% 32%68%

9%

26%

100% 100% 100% 100% 100% 100% 100%

24% 17% 25%9%

24%

91%

8%

Managed/Franchised Owned Others

2011Results

29

Rezidor MAR CHH HOT MHGC RLH H ING BHG CLDT INN Posadas RLJ Whitbread HT-2%

0%

2%

4%

6%

8%

10%

12%

14%

11.4%

5.0%3.9%

2.9% 2.8% 2.8% 2.3% 2.1% 1.9%0.9% 0.8% 0.8% 0.7% 0.7% 0.5%

CHH MAR HOT BHG MHGC IHG H CLDT Rezidor RLH INN HT RJL Posadas Whitbread0%

10%

20%

30%

40%34%

18.0%

11.6% 11.3% 10.0%7.3% 7.1% 6.0% 5.1% 3.9% 3.4% 3.2% 2.7% 1.7% 1.4%

Corporate Overhead2011 Overhead as % of Enterprise Value

2011 Overhead as % of Revenue

(1)

2011Results

Source: Barclays.

2011Results

30

Jan-09Apr-09Jul-09Oct-09Jan-10Apr-10Jul-10Oct-10Jan-11Apr-11Jul-11Oct-11Jan-12Apr-12

IMOBIBOVBHG

Apr-11M

ay-11Jun-11Jul-11Aug-11Sep-11Oct-11Nov-11Dec-11Jan-12Feb-12M

ar-12

IMOBIBOVBHG

Comparative between the IMOB (real estate) and IBOV indexes, both related to BM&FBovespa, and the Company's equity (BHGR3) considering the period of 2009 – up to today¹.

Capital Market Performance | 2012

Jan/09 Abr/12 ∆% (2009-2012)

BHGR3 (R$) 10.80 23.08 114%

IBOV (ths) 40.20 61.82 54%

IMOB (ths) 0.32 0.83 152%

Apr/11 Abr/12 ∆% (12M)

BHGR3 (R$) 22.70 23.08 2.0%

IBOV (ths) 69.26 61.82 -5.2%

IMOB (ths) 0.94 0.83 -7.1%

2.0%

-5.2%-7.1%

2009 - 2012 Moving Average (12M)

¹Today = Stock price on 04/30/12;Source: Bloomberg.

152%

114%

54%

31

Contacts

Peter van Voorst Vader (CEO) +55 (21) [email protected]

Ricardo Levy (CFO & IRO) +55 (21) [email protected]

![KOF Roadshow 2011 Octubre ENG 2.ppt [Modo de compatibilidad] · Microsoft PowerPoint - KOF Roadshow 2011 Octubre ENG 2.ppt [Modo de compatibilidad] Author: MX01001659 Created Date:](https://static.fdocuments.in/doc/165x107/61436e126b2ee0265c020a4a/kof-roadshow-2011-octubre-eng-2ppt-modo-de-compatibilidad-microsoft-powerpoint.jpg)