Roadmap to mining investment in the Democratic Republic of Congo

14

1 Roadmap to mining investment in the Democratic Republic of Congo Compiled by Grace Okani March 2011

-

Upload

malvern-booysen -

Category

Documents

-

view

229 -

download

1

description

Roadmap to mining investment in the Democratic Republic of Congo

Transcript of Roadmap to mining investment in the Democratic Republic of Congo

1

Roadmap to mining investment in the Democratic

Republic of Congo

Compiled by Grace Okani

March 2011

2

I. Overview of the country

The Democratic Republic of Congo is located in central Africa and is the third largest country in Africa, occupying approximately 2.3 million square kilometres. It has enormous potential. Kinshasa is the capital.

Population is estimated at approximately 65 million. French is the official language and medium for business, there are at least 250 languages spoken, but Lingala, Swahili, Kikongo and Tshiluba are also considered as national languages and most prominent. There are as many as 250 different ethnic groups, mostly Bantu-speaking. Largest Bantu-speaking groups are Luba, Congo, Mongo, and Lunda.

The majority of the population is Christian: 46 to 48 percent is Roman Catholic, 24 to 28 percent Protestant, up to 16.5 percent members of Kimbanguist Church. About 1 percent of population is Muslim. Most other people practice traditional African religions.

The climate ranges from tropical rain forest in Congo River basin to tropical wet-and-dry in southern uplands to tropical highland in eastern areas above 2,000 meters. In general, temperatures and humidity are quite high, but with much variation; many places on both sides of equator have two wet and two dry season’s .An average annual temperature of 25°C and annual rainfall between 1,000 and 2,200 millimetres, highest in heart of Congo River basin and highlands west of Bukavu.

The political situation in the DRC has improved significantly in recent years, and in 2006 the country held its first free elections in more than 40 years. Joseph Kabila was declared the winner of the Presidential election on November 15, 2006.

The economy of the Democratic Republic of Congo has historically been dominated by its resource sector. The copper belt region of the country, in the southern Province of Katanga, is renowned as one of the richest mineral regions of the world. Adverse political events led to a significant reduction in national output however, diamonds, copper and cobalt remain the principal foreign exchange earning exports for the country. The country has affiliated itself with southern African development community.

The economic conditions of the Democratic Republic of Congo are improving as a result of recent political stability in the country. Leading this economic growth is the mining sector, especially in Katanga Province, where many multinationals companies have their operations.

Congo was beset with political and economic problems which discouraged foreign Investment. But, due to the recent stability and peace process, large number of companies have began to invest in different sectors. As elections are at hand, forecasters have relayed an influx of foreign investors after the elections. They have estimated the reserves to be twenty six trillion Dollars with only two percent of it presently been tapped. Improved political stability has boosted Congo's long-term potential to effectively exploit its vast wealth of mineral and agricultural resources. In view of Congo's recent ability to provide rudimentary institutions of law and order, potential investors should be advised of the continuing potential of doing business in Congo. Congo's business climate is rapidly beginning to improve as a result of his government's policies, but much more remains to be done.

The International Monetary Fund and the World Bank are actively engaged in the Democratic Republic of Congo and are assisting in the development of coherent legislative and economic reforms. As part of this

3

effort, in July 2002, the Government introduced a new mining code based on the Australian standard, which has significantly improved the investment climate for the mining industry and is encouraging renewed international investment.

In 2007 China agreed to invest more than US$5 billion in mining and infrastructure, predominately in rail, roads and other hard infrastructure. The country embarked in the revalidation of mining contracts which was finalized in 2010.The Democratic Republic of Congo has improved over past years; however there is still work to do in terms of corruption, remuneration of civil servants, service delivery, job creation and infrastructure development.

II. Steps involved to mining investment in the Democratic Republic of Congo

i. First step

A. Business trip Meeting with key government authorities (Premier or mayor) Meeting with key government departments (Mines, Cadastre, Finance and Environment) Meeting with key people (Lawyers, geologists, accountant) Meeting with the consulate or embassy of the relevant country in Drc Meeting with directors at Gecamines (State owned Mining companies) JV and mining concessions

ii. Second step

A. Company formation The principal business structures used by private parties to execute mining activities are the two following types of locally incorporated companies:

1. The private limited liability company (SPRL), with a minimum of two shareholders (but does not benefit from tax deductions for interest on shareholders’ advances).Shares cannot be ceded to persons outside the company and the liability of shareholders is limited to the nominal value of the shares of each holder, SPRLs are usually small- and medium-sized businesses(such as Boss Mining Sprl, and Mutanda mining Sprl )

2. The company limited by shares (SARL), with a minimum of seven shareholders (but its incorporation requires approval by presidential decree) (both requirements will disappear when the DRC’s adhesion to OHADA will take effect).It is a joint stock company, that is a corporation. Shareholders are liable only for the amount of their equity subscription. Public shares may be issued. The board of directors is responsible to shareholders for management. SARLs are normally large private businesses( such as Tenke-Fungurume mining Sarl and Anvil Mining Sarl

There are some restrictions and limitations imposed on mining companies with regards to the use of domestic and foreign employees, with the mining operators being able to employ a maximum of 5% of foreign employees for management staff and a maximum of 10% for other positions. Certain jobs are reserved for DRC nationals, but derogations may be granted. Foreign employees are required to obtain a work permit, generally valid for two years and renewable. The Mining Code and the Mining Regulation provide for mainly

4

self-contained environmental measures (however, see also Law No. 011-2002 of 29 August 2002 on the Forestry Code), and health and safety rules. The principal regulatory bodies that administer those laws are the department in charge of the protection of the mining environment (for environmental matters) and the directorate of mines (for health and safety matters).

B. Requirements for company formation in the Democratic Republic of Congo

Requirements Departments/office Costs Notes

Trade Licence Ministry of Commerce USD 1 Valid for foreigners only

Authentification of Statutes Notaries office From USD 50 to USD 500

Registration in the new Court of commerce

USD 800 in the case whereby foreigners contributed to the majority of the capital

Trade register/Gazette Court of commerce USD 200 for the case Congolese

nationals

National identification Number

Ministry of Commerce USD 200 for companies

Tax Number Government tax authorities Free of Charge

Import-export number Ministry of Commerce USD 250 for companies

Prices are subject to changes

Some other required documents:

Copy of identity cards , Criminal record (Criminal Investigation Body) Non-civil servant certificate (commune)

a. Mineral resources in the Democratic Republic of Congo.

Mines

DRC’s mining sector has an extremely varied range of minerals and offers large possibilities for their exploitation. The minerals hereafter can be exploited:

Basic metal: - Iron ore: Both Kasaï, Bas-Congo, Katanga, Eastern Province, South-Kivu.

Non-ferrous metals: - Aluminum: Bas-Congo. - Copper: Katanga, Bas-Congo, Bandundu, both Kasaï. - Lead: Bas-Congo, Eastern Kasaï, Kivu. - Zinc: Eastern Kasaï, Katanga. - Tin: Katanga and Kivu.

5

Alloy metal: - Nickel chromium: both Kasaï; - Wolframite: North-Kivu (Bushasha and Butembo); - Manganese: Katanga (Kisenge and Kasekelesa); - Vanadium: Bas Congo; - Cobalt: Katanga Province.

Strategic metal: - Beryllium: South-Kivu (Kamituga-Kasoko) and Katanga (Mituaba); - Monazite: Maniema, South-Kivu, Katanga and both Kasaï. - Lithium: Manono, Katanga; - Colombo Tantalite : Manono (Katanga), Sud-Kivu, Maniema.

Precious and semi-precious mineral substances: - Silver: Bas Congo, Eastern Kasaï, South-Kivu, Eastern Province, Maniema; - Gold : Eastern Province, Kivu, Maniema, Katanga, Bas Congo, both Kasaï; - Platinum : Western Kasaï, Katanga, Maniema; - Diamond : both Kasaï, Bandundu, Équateur, Eastern Province, Maniema, North-Kivu

b. Investment opportunities

Investors can start the activities hereafter which constitute important investment opportunities:

Mining Sector Exploitation of:

Copper and cobalt : Katanga ; Diamond : Eastern Kasaï, Western kasaï, Bandundu, Eastern Province, Equateur ; Coltan : North-Kivu, South-Kivu, Maniema ; Coal : Katanga ; Iron : Bas-Congo, Eastern-Kasaï, Western Kasaï, Eastern Province Mining and geologic research all over the national area ; Investment opportunities in mining sector ;

iii. Third step

A. Exploration and Exploitation Permits for the Democratic Republic of the Congo Exploration operations are subject to the prior approval of a mitigation and rehabilitation plan (MRP) subsequent to the delivery of the exploration permit. However, prospecting and small-scale exploitation permits are only subject to codes of conduct. An exploration permit may be obtained in a maximum of 47 calendar days from the date of filing the request, whist the approval of the MRP may be obtained in a maximum of 24 calendar days from its filing.

Exploitation permits are subject to the prior approval of an environmental impact study (EIS) and an environmental management plan (EMP). Exploitation permits may be obtained in a maximum of 252 calendar days.

As part of its environmental management plan, the holder of an exploration or exploitation right must provide for the measures of remediation and environmental rehabilitation after closure, the costs of which need to be entirely backed by a financial guarantee. However, the funding of the guarantee depends on the type of operation and its duration, and can take place over time. The amount is revised mid-term.

The rights of aboriginal, indigenous, lawful occupants and currently or previously disadvantaged peoples are protected by the mining rights.

6

Any private party can engage in non-artisanal exploration or exploitation of mineral substances in the DRC provided he or she is the holder of a valid mining right (exploration or exploitation), which is obtained upon completion of the corresponding administrative procedure. The granting of mining titles is based on a ‘first-come, first-served’ principle: the applications for mining rights for a given ‘perimeter’ (demarcated surface area with indefinite depth) composed of quadrangles or ‘squares’ are registered in the chronological order of their filing.

In exceptional cases, the minister of mines may submit to tender, open or by invitation, mining rights relating to a specific deposit. To maintain the validity of his or her mining rights, the holder must commence exploration within six months (exploration permit) or commence development and construction works within three years (exploitation permit) as of the date the title evidencing his or her right is issued, and pay the surface duty per square relating to his or her title at the counter of the Mining Registry. If he or she fails to fulfil any of these obligations, the holder may be deprived of his or her right. A title-holder must also comply with specific rules relating to, among others, protection of the environment, cultural heritage, health and safety or construction and planning of infrastructure.

There are no distinctions between mining rights that may be acquired by domestic parties and those that may be acquired by foreign parties, except for artisanal diggers and traders (small-scale mining), who can only be individual DRC nationals, and except for foreign companies that are requested to incorporate a local company before they apply for an exploitation permit. Foreign parties must elect domicile with an authorized domestic mining and quarry agent and act through his or her intermediary. A foreign party need not have a domestic partner, but a company wishing to obtain an exploitation permit must transfer 5 % (non-dilatable) of its share capital to the state.

The surface rights are acquired by private parties according to the Land Law No. 73-021 of the 20th of July 1973, the state has the exclusive, inalienable and imprescriptible property of the land. The state can grant surface rights to private or public parties that have to be distinguished from mining rights since surface rights do not entail the right to exploit the mineral substances of the soil or subsoil and, inversely, a mining right does not entail any surface occupation right over the surface. However, subject to any rights of third parties over the surface concerned, the holder of an exploitation mining right has, with the authorization of the governor of the province concerned, and on the advice of the administration of mines, the right to occupy within his or her mining perimeter the land necessary for his or her activities and associated industrial activities, including the construction of industrial plants and dwellings, to use the water, dig canals and channels, and establish means of communication and transport of any type. Nevertheless, any occupation of land preventing the rightful surface right holders from using the surface, or any modification rendering the land unfit for cultivation, will entail the obligation for the holder of the mining rights to pay fair compensation. The mining rights holder is also liable for the damage caused to the occupants of the land in connection with his or her mining activities, even if they are authorized. The Mining Code provides for judicial and arbitral recourses in the event of disputes.

1. Mining prospecting

As a company under Congolese law, the requirement hereafter should be fulfilled:

Obtain a prospecting permit from Mining land-registry (CAMI)

- Cost : 2.55 to 124.03 USD per square - Requirements:

To be eligible for mining laws ; To prove his/her financial capacity equal at least ten times the total amount of annual

superficiary duties per square to be paid for the last year of the 1st validity period of that duty ;

7

To get ready and have his lightening plan and that of rehabilitation approved within the six months of delivery of the prospecting permit.

2. Mining exploitation

As a company under Congolese law, the requirement hereafter should be fulfilled:

Get a prospecting permit form Mining land-registry (CAMI)

- Cost : 195.4 to 679.64 USD per square - Requirements :

Evidence of the existence of an economically exploitable deposit (feasibility study) ; Proof of the existence of the necessary financial resources, To obtain a prior approval of environmental impact study and of plan of project

environmental management.

B. Mining Duties, Royalties and Taxes for the Democratic Republic of the Congo

There are generally several duties, royalties and taxes that are payable by private parties on the concessions; firstly, the tax and customs regime that applies to mining activities is exhaustive: the Mining Code provides for all the taxes, charges, royalties and other fees owed to the Treasury by a mining title holder in respect of his or her mining activities, to the exclusion of any other form of taxation. This principle does not, however, prevent the tax agencies from often claiming additional taxes. When applicable, the tax provisions of the Mining Code refer to the general tax legislation. Second, the Mining Code provides a certain guarantee of stability: the existing tax, customs, exchange and other benefits applicable to mining activities remain in effect for 10 years in favour of each concerned mining title holder in the event that the Mining Code is amended.

A mining royalty is owed as from the date of commencement of effective exploitation. The mining royalty is calculated on the value of sales made, less transport costs and fewer assays, insurance and marketing costs. The rate of the mining royalty is 0.5% for iron or ferrous metals, 2% for non-ferrous metals and 2.5% for precious metals.

A professional tax on benefits at the preferential Mining Code rate of 30% (instead of the 40% corporate tax rate) is levied on the net profits from exploitation determined in accordance with the accounting and tax legislation in force.

An exploration permit holder is liable for the tax on the surface area of mining concessions at the rates of US$0.02 per hectare for the first year, US$0.03 for the second year, US$0.035 for the third year and US$0.04 for each subsequent year. An exploitation permit holder is liable for this tax at US$0.04 per hectare for the first year, US$0.06 for the second year, US$0.07 for the third year and US$0.08 for subsequent years.

A special surface duty, payable annually to the Mining Registry, is levied on the number of squares held by a title-holder. The duty is meant to cover service and management costs of the Mining Registry and the Ministry of Mines. For an exploration permit, the annual duty per square amounts to US$2.55 for each of the first two years, US$26.34 for each subsequent year, US$43.33 for each year of the first renewal period and US$124.03 for each year of the second renewal period. For an exploitation permit, the annual duty per square is US$424.78 for an ordinary exploitation permit, US$679.64 for a tailings exploitation permit and US$195.40 for a small-scale exploitation permit.

It is important to note that there are some tax advantages and incentives available to private parties that perform mining activities, which entail some reductions or exemptions from taxes and customs duties, these include a 10% reduction on professional tax benefits; reductions on export customs duties; withholding tax on

8

interest and dividends: zero instead of 20% on interest paid on loans contracted abroad in foreign currency; 10 instead of 20% on dividends and other distributions; and special facilities are granted for deductions for exploration and development, provisions for depletion allowances, depreciations, etc. it is also noteworthy to say that there are no distinctions based on nationality of the exploring or exploiting parties

III. Acquisition

Buying existing business (less risky than starting business from scratch).

A. Checklist of items while evaluating the value of the business

Inventory Furniture, Fixtures, Equipment and Building Copies of all contacts and legal documents Incorporation Financial statement for the past five years Sales records Complete list of liabilities All account receivables All account payables Merchandise return Customer patterns Marketing strategies Advertising costs Price checks Industry and market history Location and market area Reputation of the business Seller customer ties Inflated salaries List of current employees and organizational chart OSHA requirements Insurance Product liability B. Determining a fair price

Different methods Multipliers Book value Return of investment Capitalized earning Intangible value

9

C. Art of deal

Pay 30 to 50 percent of the price in cash and finance the remaining amount

Alternatives to cash

Use the Sellers’s assets Buy co-op Lease an option to buy Use an employee stock ownership plan Assume liabilities or decline receivables D. Common mistakes to avoid

Buying on price Cash shortage Buying all receivables Failure to verify all data Heavy payment schedules Treating the seller unfairly E. Transition Time

Quite difficult for small businesses, however it can be difficult for large businesses (Case of Tenke-Fungurume mining Sarl in Dr Congo)

IV. Joint Venture

A. Forming a joint venture: Checklist

Screening of prospective partners Joint development of a detailed business plan and short listing a set of prospective partners based on

their contribution to developing a business plan. Due diligence; checking credentials of other parties. B. Benefits of joint ventures

Provide companies with opportunity to obtain new capacity and expertise Allow companies to enter into related business and geographic markets and obtain new technological

knowledge Have relatively short life spam (5 to 7 years) and therefore do not represent a long-term commitment In the era of divesture and consolidation, offer creative way for companies exist From non-core businesses: companies can gradually separate a business from the rest of the

organization and ultimately sell it to the other parent company (roughly 80% all joint venture end in sale by one partner or the other.

C. Preparation for a successful JV: Human resource action steps

Business strategy Human resources strategy Leadership Communication Talent

10

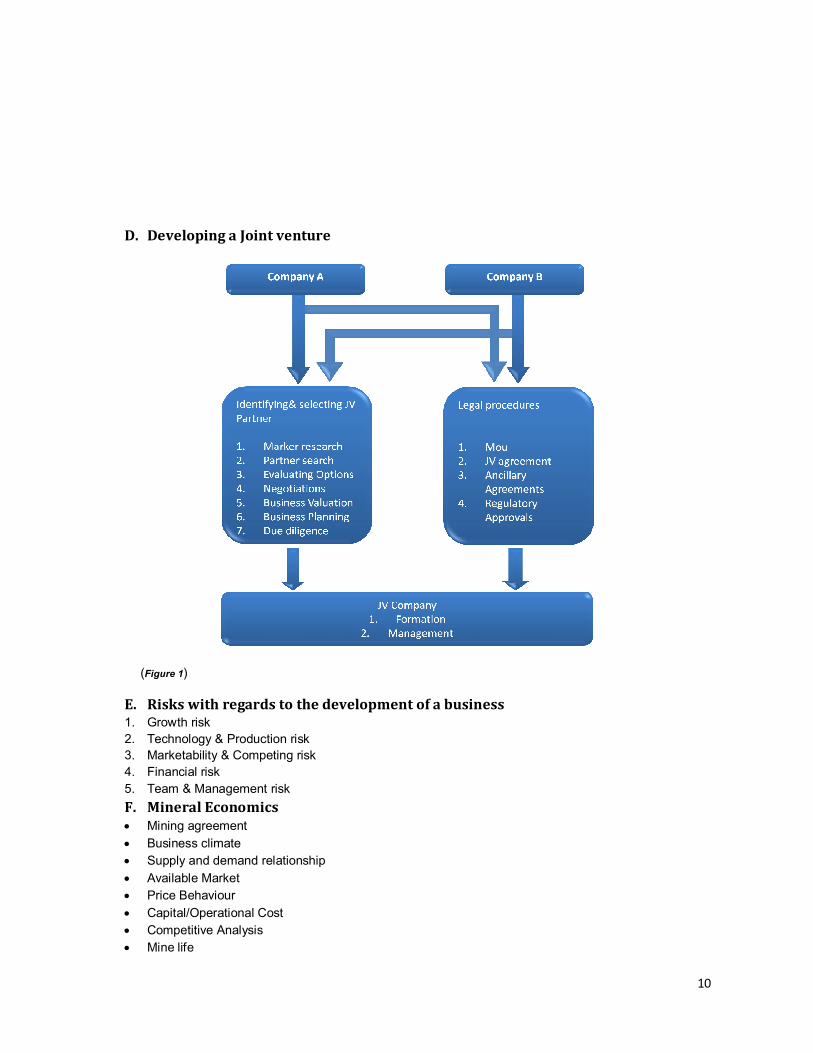

D. Developing a Joint venture

(Figure 1)

E. Risks with regards to the development of a business 1. Growth risk 2. Technology & Production risk 3. Marketability & Competing risk 4. Financial risk 5. Team & Management risk F. Mineral Economics Mining agreement Business climate Supply and demand relationship Available Market Price Behaviour Capital/Operational Cost Competitive Analysis Mine life

11

Economic Evaluation Financial Engineering Taxation Planning Financial Evaluation Risk Analysis /Treatment Strategic alliance/Joint venture

V. Mining Companies and Contracts in the Democratic Republic of Congo

A. Contracts

1 For Gécamines: 28 contracts

- Anvil Mining Kulu Concentrate Kinsevere, AMCK Sprl - Boss Mining Sprl - Chabara Mining Sprl - Compagnie Minière de Tondo, CMT Sprl - Compagnie Minière du Sud Katanga, CMSK Sprl - Congolaise des Mines et de Développement, Comide Sprl - Compagnie Minière de Luisha, Comilu Sprl - Compagnie Minière de Musonoi, Commus Sprl - Congo Zinc Sprl - DRC Copper and Cobalt Project, DCP Sarl - Kasonta Lupota Mines, Kalumines Sprl - Kamoto Copper Company, KCC Sarl - Kipushi Corporation, Kico Sarl - Kingamyambo Musonoi Tailings, KMT Sarl - Minière de Kasombo, Mikas Sprl - Minière de Kalumbwe Myunga, MKM Sprl - Mukondo Mining Sprl - Mutandaya Mukonkota Mining, MUMI Sprl - PTM Sprl (Cayman) - Prospection de la Zone Centre Est, PZCE Sprl - Ruashi Mining Sprl - Savannah Mining Sprl (KMC Sprl) - Shituru Mining Corporate, SMCO Sprl - Société Minière de Kolwezi, SMK Sprl - Société d'Exploitation de Kipoi, SEK Sprl - Société Minière de Kabolela et de Kipese, SMKK Sprl - Société de Traitement de Terril de Lubumbashi, STL/GTL Sprl - Swanmines Sprl

2. For Kisenge Manganese: 2 contracts

- Orama Properties Sprl - Sentinelles Sprl

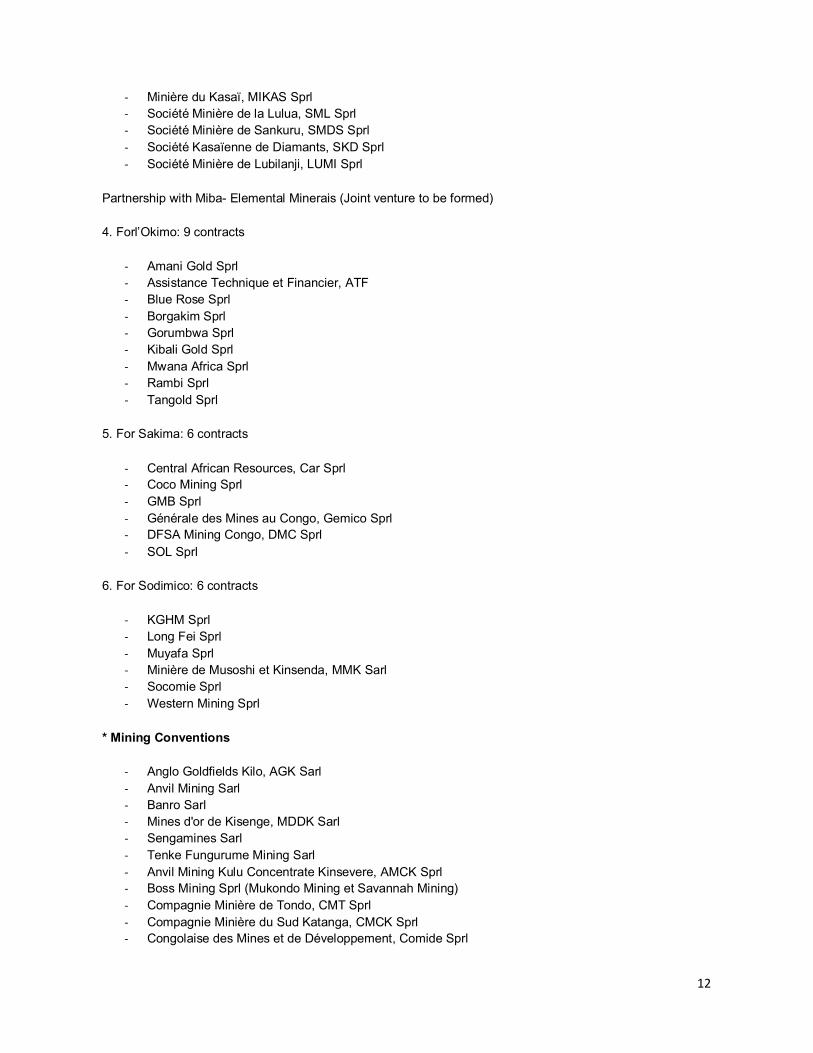

3. For Miba : 6 contracts

12

- Minière du Kasaï, MIKAS Sprl - Société Minière de la Lulua, SML Sprl - Société Minière de Sankuru, SMDS Sprl - Société Kasaïenne de Diamants, SKD Sprl - Société Minière de Lubilanji, LUMI Sprl

Partnership with Miba- Elemental Minerais (Joint venture to be formed)

4. Forl’Okimo: 9 contracts

- Amani Gold Sprl - Assistance Technique et Financier, ATF - Blue Rose Sprl - Borgakim Sprl - Gorumbwa Sprl - Kibali Gold Sprl - Mwana Africa Sprl - Rambi Sprl - Tangold Sprl

5. For Sakima: 6 contracts

- Central African Resources, Car Sprl - Coco Mining Sprl - GMB Sprl - Générale des Mines au Congo, Gemico Sprl - DFSA Mining Congo, DMC Sprl - SOL Sprl

6. For Sodimico: 6 contracts

- KGHM Sprl - Long Fei Sprl - Muyafa Sprl - Minière de Musoshi et Kinsenda, MMK Sarl - Socomie Sprl - Western Mining Sprl

* Mining Conventions

- Anglo Goldfields Kilo, AGK Sarl - Anvil Mining Sarl - Banro Sarl - Mines d'or de Kisenge, MDDK Sarl - Sengamines Sarl - Tenke Fungurume Mining Sarl - Anvil Mining Kulu Concentrate Kinsevere, AMCK Sprl - Boss Mining Sprl (Mukondo Mining et Savannah Mining) - Compagnie Minière de Tondo, CMT Sprl - Compagnie Minière du Sud Katanga, CMCK Sprl - Congolaise des Mines et de Développement, Comide Sprl

13

- Compagnie Minière de Luisha, Comilu Sprl - DRC Copper and Cobalt Project, DCP Sarl - Kamoto Copper Company, KCC Sarl - Kasonta Lupota Mines, Kalumines Sprl - KIMIN Sprl, (ex amodiation Gécamines – Somika Sprl) - Kipushi Corporation, Kico Sarl - Minière de Kasombo, Mlkas Sprl - Mukondo Mining Sprl - Mutandaya Mukonkota Mining, Mumi Sprl - PTM Sprl (Cayman) - Ruashi Mining Sprl - Shituru Mining Corporate, SMCO Sprl - Société Minière de Kolwezi, SMK Sprl - Société d'Exploitation de Kipoi, SEK Sprl - Société Minière de Kabolela and de Kipese, SMKK Sprl - Société de Traitement de Terril de Lubumbashi, STL/GTL Sprl - Swanmines Sprl

- Minière de Musoshi and Kinsenda, MMK Sarl

It should be noted that some the contracts have been terminated and finalized while others are still under review.

VI. Table of content

i. First step ................................................................................................................................................ 3

A. Business trip ....................................................................................................................................... 3

ii. Second step ........................................................................................................................................... 3

A. Company formation ........................................................................................................................... 3

B. Requirements for company formation in the Democratic Republic of Congo ..................................... 4

Mines .................................................................................................................................................... 4

iii. Third step............................................................................................................................................... 5

A. Exploration and Exploitation Permits for the Democratic Republic of the Congo ................................ 5

B. Mining Duties, Royalties and Taxes for the Democratic Republic of the Congo ................................... 7

A. Checklist of items while evaluating the value of the business ............................................................. 8

14

B. Determining a fair price...................................................................................................................... 8

C. Art of deal .......................................................................................................................................... 9

D. Common mistakes to avoid ................................................................................................................ 9

E. Transition Time .................................................................................................................................. 9

A. Forming a joint venture: Checklist ...................................................................................................... 9

B. Benefits of joint ventures ................................................................................................................... 9

C. Preparation for a successful JV: Human resource action steps ............................................................ 9

D. Developing a Joint venture ............................................................................................................... 10

E. Risks with regards to the development of a business ........................................................................ 10

F. Mineral Economics ........................................................................................................................... 10

A. Contracts ......................................................................................................................................... 11