RMB Morgan Stanley Off-Piste Conference - mpact.com · 5 │ Mpact Limited 2013 RMB Morgan Stanley...

25

1 │ Mpact Limited Annual Results│ 8 March 2012 RMB Morgan Stanley Off-Piste Conference 2-3 October 2013 Cape Town

Transcript of RMB Morgan Stanley Off-Piste Conference - mpact.com · 5 │ Mpact Limited 2013 RMB Morgan Stanley...

1 │ Mpact Limited Annual Results│ 8 March 2012

RMB Morgan Stanley Off-Piste Conference2-3 October 2013Cape Town

│ Presentation title │ 00 Month 201122 │ Mpact Limited 2013 RMB Morgan Stanley Off-Piste Conference

Agenda

• Introduction

• Mpact business overview

• Group financial performance review

• Strategy

• Outlook

3 │ Mpact Limited 2013 RMB Morgan Stanley Off-piste Conference

Introduction

• Listed on JSE Main Board 11 July 2011 – demerged from Mondi Limited

• Mpact is a leading Southern African producer of paper and plastic packaging

• Market capitalisation – R4,4bn at 25 September 2013

│ Presentation title │ 00 Month 201144 │ Mpact Limited 2013 RMB Morgan Stanley Off-Piste Conference

Agenda

• Introduction

• Mpact business overview

• Group financial performance review

• Strategy

• Outlook

5 │ Mpact Limited 2013 RMB Morgan Stanley Off-piste Conference

SA packaging sector overview

PAGE 5

SA packaging ex-converter sales1 2012 (Volume) SA packaging ex-converter sales1 2012 (Value)

1. Source: BMI Report (2013) 2. “Ex converter” sales refer to sales of packaging materials converted in the country by local producers (includes imports and exports)3. Private Consumption Expenditure (PCE) : Consumption spending by households, which is the largest component of total spending in the economy. Source: BMI (2013); ABSA and South

African Reserve Bank4. Source: IMF

Industry overview

Other, 4.3% Metal,

8.8%

Glass, 32.4%

Paper, 31.2%

Plastic, 23.4%

Other, 0.8%

Metal, 11.1%

Glass, 12.6%

Paper, 27.7%

Plastic, 47.7%

80

90

100

110

120

2007 2008 2009 2010 2011 2012

Corrugated Cartonboard Rigids Flexibles Metal Glass

Inde

x(2

007

= 10

0)

Total packaging volume % growth forecast in tons“Ex Converter” Sales

ValueCAGR

(’07 - ’12)

VolumeCAGR

(’07 - ’12)

Globalconsumption

CAGR(’10 - ’15)

Rigids 7.7% 2.9% 4.1%

Corrugated 5.0% 0.1%2.4%

Cartonboard 6.0% (0.7%)

Flexibles 5.0% 1.3% 3.8%

Metal 1.5% (3.4%) 1.7%

Glass 5.5% 0% 2.7%

GDP� 1.9%

PCE� 2.6%

World GDP� 2.8%

Glass

6 │ Mpact Limited 2013 RMB Morgan Stanley Off-piste Conference

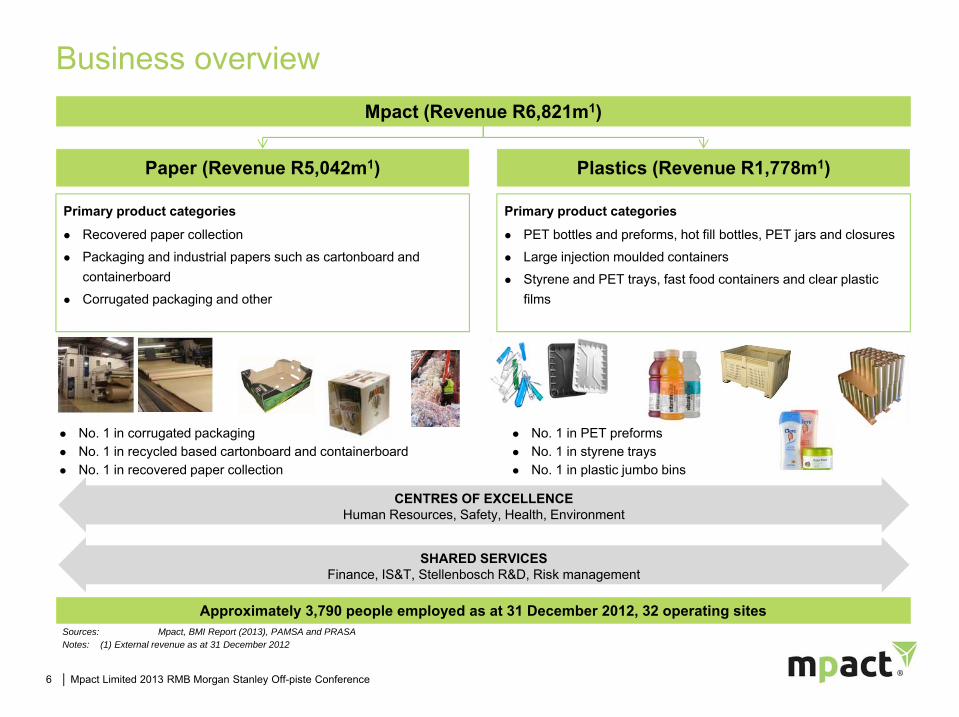

Business overview

Plastics (Revenue R1,778m1)

Mpact (Revenue R6,821m1)

Primary product categories

Recovered paper collection

Packaging and industrial papers such as cartonboard and containerboard

Corrugated packaging and other

Primary product categories

PET bottles and preforms, hot fill bottles, PET jars and closures

Large injection moulded containers

Styrene and PET trays, fast food containers and clear plastic films

Paper (Revenue R5,042m1)

No. 1 in corrugated packaging No. 1 in recycled based cartonboard and containerboard No. 1 in recovered paper collection

No. 1 in PET preforms No. 1 in styrene trays No. 1 in plastic jumbo bins

CENTRES OF EXCELLENCEHuman Resources, Safety, Health, Environment

Approximately 3,790 people employed as at 31 December 2012, 32 operating sites

SHARED SERVICESFinance, IS&T, Stellenbosch R&D, Risk management

Sources: Mpact, BMI Report (2013), PAMSA and PRASANotes: (1) External revenue as at 31 December 2012

7 │ Mpact Limited 2013 RMB Morgan Stanley Off-piste Conference

Richards Bay

Durban

Port Elizabeth

Nelspruit Maputo1

East London

Bloemfontein�

Cape Town

Piet Retief

Pretoria

Felixton

Corrugated

Recycling

Plastics

Harare

Packaging and Industrial Paper

Walvis Bay1

Windhoek1 Brits

Johannesburg

Atlantis

Operating structure which enables superior flexibility and responsiveness to customer requirements

Broad manufacturing and service footprint enabling Superior customer focus Responsiveness and flexibility in meeting

customer requirements Customised solutions

Source: MpactNotes: (1) Mpact has 2 sheet plants in Mozambique and Namibia in which it holds a controlling interest

(2) Corrugated sales office

Paarl

Springs

Midrand

Geographical footprint

8 │ Mpact Limited 2013 RMB Morgan Stanley Off-piste Conference

Paper business overview

PAGE 8

Key products : Cartonboard: Containerboard: Retail ready packaging: Regular slotted cartons: POS packaging and displays: Die-cut solutions

Key customers : Packaging converters (containerboard and cartonboard): Agricultural producers: FMCG companies: Quick service restaurants: Other consumer and industrial packaging companies

Operations : Recycling (7): Paper Manufacturing (3): Corrugated (9) + (2)1 + (1)

Employees : 2,444

Leader in recovered paper collection, production of cartonboard, containerboard and corrugated packagingSources: Mpact and financial figures extracted from audited Mpact financial informationNotes: (1) Mpact has 2 sheet plants in Mozambique and Namibia in which it holds a controlling interest

Paper

Divisions : Recycling: Paper Manufacturing: Corrugated and converting

CartonboardStandard and customised cases

Frui

t and

veg

etab

le tr

ays

Retail ready packaging

Containerboard

External Revenue (2012)

R5,042m

EBITDA (2012)

R746m

74% 76%

Other

9 │ Mpact Limited 2013 RMB Morgan Stanley Off-piste Conference

Recycling

PAGE 9Paper

Geographic footprint

Customer base

Sources of recovered paperCollected volumes (kt)

Source: Mpact Note: (1) Mondi Shanduka Newsprint

Sappi

Nampak

Kimberly Clark

Lothlorien

Gayatri

Independents

Key competitorsRichards Bay

Durban

Port Elizabeth

East London

Cape Town

JohannesburgSprings

Pretoria

Midrand

Governments and local authorities

Schools

Paper banks

Converters

Agents, dealers, waste management companies

Business and offices

Kerbside

Imports

Mobile cages and bakkies

59% Current recovery rate of recoverable paper in SA

Target rate63%

Mpact Recycling shareholding 75% Mpact Limited

25% Mondi Limited

Internal consumption, 70%

MSN1 and others, 30%457k tons

402

441448 450

457

2008 2009 2010 2011 2012

• The largest paper recycler in SA

• Recovery and recycling of paper in SA ensures local beneficiation of raw materials and creation of jobs

• Over 100,000 people involved in the recycling industry in SA

• Seven operations in major centres and 42 buy-back centres

• Over 40 entrepreneurial companies empowered to facilitate collection strategies

10 │ Mpact Limited 2013 RMB Morgan Stanley Off-piste Conference

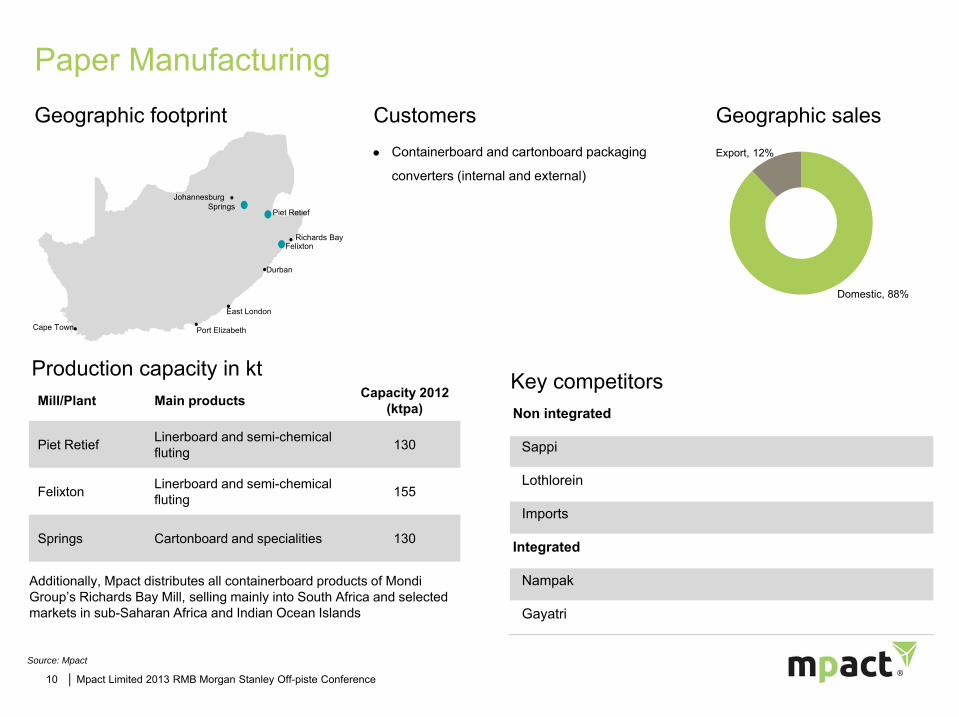

Paper Manufacturing

PAGE 10Paper

Geographic footprint Customers

Key competitors Production capacity in kt

Additionally, Mpact distributes all containerboard products of Mondi Group’s Richards Bay Mill, selling mainly into South Africa and selected markets in sub-Saharan Africa and Indian Ocean Islands

Mill/Plant Main products Capacity 2012 (ktpa)

Piet Retief Linerboard and semi-chemical fluting 130

Felixton Linerboard and semi-chemical fluting 155

Springs Cartonboard and specialities 130

Containerboard and cartonboard packaging

converters (internal and external)

Geographic sales

Non integrated

Sappi

Lothlorein

Imports

Integrated

Nampak

Gayatri

Durban

Port Elizabeth

East London

Cape Town

JohannesburgSprings

Piet Retief

Felixton

Domestic, 88%

Richards Bay

Source: Mpact

Export, 12%

11 │ Mpact Limited 2013 RMB Morgan Stanley Off-piste Conference

Durban

Port Elizabeth

Nelspruit Maputo1

East London

Bloemfontein2

Walvis Bay1

Windhoek1

Cape Town

JohannesburgSprings

Epping

Brakpan

Corrugated Packaging

PAGE 11Paper

Geographic footprint Customers

Key competitors Production in m2 (million)

Overview

Sources: Mpact and BMI Report (2013)Notes: (1) Mpact has sheet plants in Mozambique and Namibia (holding a controlling interest)

(2) Corrugated sales office in Bloemfontein(3) Management estimates

Nampak

New Era

APL

Corruseal

Houers

Three high-graphic printing

machines situated in Springs,

Pinetown and Epping offering

high-quality graphic printing on

corrugated board. These are

complimented by in-house graphic

design facilities

ISO 14,000 and ISO 9,000

environmental and quality

management systems,

respectively

Corrugated packaging products

include: Corrugated regular cases Die-cut cases Folded glued cases Trays Point of sale displays

Localised customer base

Customers include producers of agricultural,

food durable and non durable goods3:

Sheet board, 20% Agricultural,

38%

FMCG, 30%

Other, 12%

305 328367 381 369 387 391 413

2005 2006 2007 2008 2009 2010 2011 2012

12 │ Mpact Limited 2013 RMB Morgan Stanley Off-piste Conference

Plastics business overview

PAGE 12

Leader in the manufacture of PET preforms, styrene trays and plastic jumbo bins

Key products : PET preforms, bottles and jars: Plastic jumbo bins, wheelie bins, plastic crates: Plastic containers such as bottles, jars, closures, with in-mould labelling capability

: Styrene and PET trays, fast food containers and clear plastic films

Key customers : FMCG companies (carbonated soft drinks, personal care, pharmaceuticals, food producers)

: Fast food producers: Agricultural producers: Retail chains

Operations : Styrene trays and clear plastic films (3): Large injection moulds (2): PET injection (1) , FMCG plastic packaging (3) and closures (1)

Employees : 1,234

Plastic Jumbo Bins, Wheelie Bins, Plastic Crates and Pallets

Styrene and PET Trays, Fast Food Containers and Clear Plastic Film

PET Preforms, Bottles and Jars

FMCG Bottles, Jars, Closures and In-Mould Labelling

External Revenue (2012)

R1,778m

EBITDA (2012)

R226m

Plastics

Sources: Mpact and financial figures extracted from audited Mpact financial information

26% 24%

13 │ Mpact Limited 2013 RMB Morgan Stanley Off-piste Conference

Plastics segment overview

PAGE 13Plastics

Geographic footprint Customer base

Key competitors Mills/plants and main productsMill/Plant Main products

WadevillePET preforms, jars, bottles and hot fill bottles, closuresInjection moulding, blow moulding

Atlantis (Large Injection) Plastic jumbo bins, wheelie bins, plastic cratesInjection moulding

Brits Plastic jumbo bins, wheelie bins, plastic cratesInjection moulding

PinetownFMCG packaging bottles, jars, closures, in-mould labelsInjection moulding, blow moulding, IML

RobertvilleFMCG plastic bottles, jars, closuresInjection moulding, blow moulding, compression moulding

Atlantis (FMCG)FMCG plastic bottles, jars, closuresInjection moulding, blow moulding, PET bottles and printing

Versapak Paarl Styrene trays, fast food containers, PET trays and blisterpack and clear plastic films

Versapak Harare Styrene trays, fast food containers and clear plastic films

Nampak

Astrapak

Bowler Metcalf

Polyoak

MCG

CIBA

Boxmore

Beverage, 27%1

Food, 23%Distributors, 19%

Retail, 9%

Personal care, 8%

Agricultural, 7%

Home care, 6% Other, 1%

Durban

Port Elizabeth

Brits

East LondonAtlantis

Johannesburg

Paarl

Pretoria

Harare

Pinetown

Robertville Wadeville

Note: (1) A significant proportion of beverage sales is made up by an Amalgamated Beverages (ABI) contract for PET preforms

Blackheath

│ Presentation title │ 00 Month 20111414 │ Mpact Limited 2013 RMB Morgan Stanley Off-Piste Conference

Agenda

• Introduction

• Mpact business overview

• Group financial performance review

• Strategy

• Outlook

15 │ Mpact Limited 2013 RMB Morgan Stanley Off-piste Conference

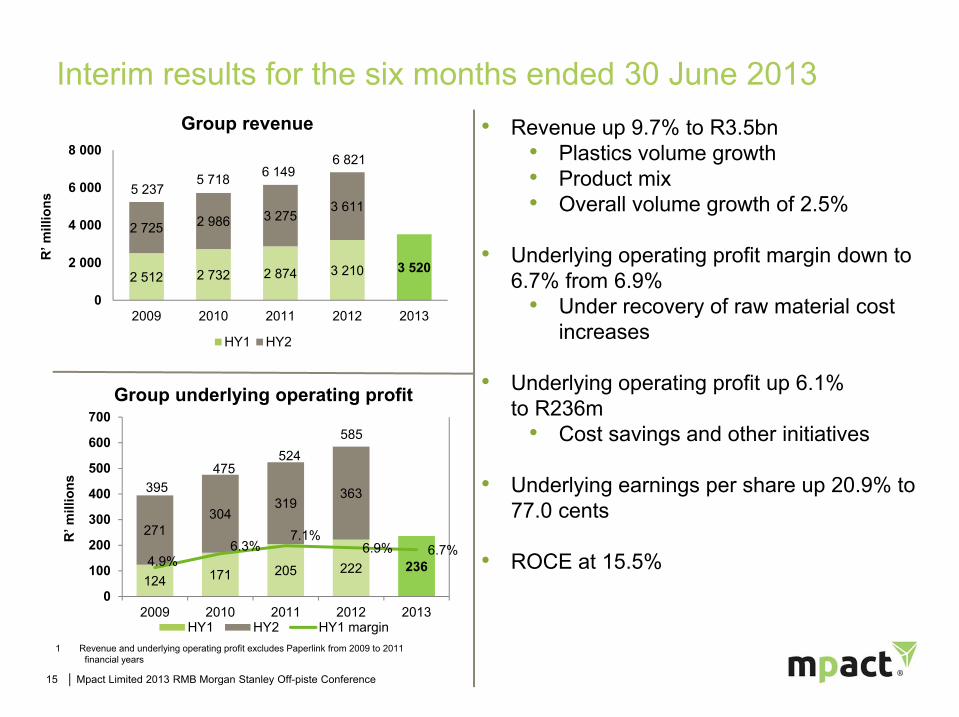

Interim results for the six months ended 30 June 2013�

2 512 2 732 2 874 3 210 3 520

2 725 2 986 3 2753 611

0

2 000

4 000

6 000

8 000

2009 2010 2011 2012 2013

R’ m

illio

ns

Group revenue

HY1 HY2

5 2375 718 6 149

6 821

124 171 205 222 236

271304

319363

4.9%6.3%

7.1%6.9% 6.7%

0

100

200

300

400

500

600

700

2009 2010 2011 2012 2013

R’ m

illio

ns

Group underlying operating profit

HY1 HY2 HY1 margin

395475

524585

• Revenue up 9.7% to R3.5bn• Plastics volume growth • Product mix• Overall volume growth of 2.5%

• Underlying operating profit margin down to 6.7% from 6.9%

• Under recovery of raw material cost increases

• Underlying operating profit up 6.1%to R236m

• Cost savings and other initiatives

• Underlying earnings per share up 20.9% to 77.0 cents

• ROCE at 15.5%

1 Revenue and underlying operating profit excludes Paperlink from 2009 to 2011 financial years

16 │ Mpact Limited 2013 RMB Morgan Stanley Off-piste Conference

Financial review

1 Underlying operating profit includes operating profit of subsidiaries before special items.

R’millions H1 2012 H1 2013 Change

Underlying operating profit1 222 236 6.1%

Net finance costs (64) (60) 6.4%

Associates and JV net earnings 2 4 81.8%

Underlying profit before tax 160 180 12.1%

Tax before special items (50) (51) (2.4%)

Total non-controlling interests (6) (3) 55.0%

Underlying earnings 104 126 20.7%

Special items (after tax and minorities) (4) - 100%

Reported profit after tax and non-controlling interests

Underlying earnings per share (cents)

100 126 25.4%

63.7 77.0 20.9%

17 │ Mpact Limited 2013 RMB Morgan Stanley Off-piste Conference

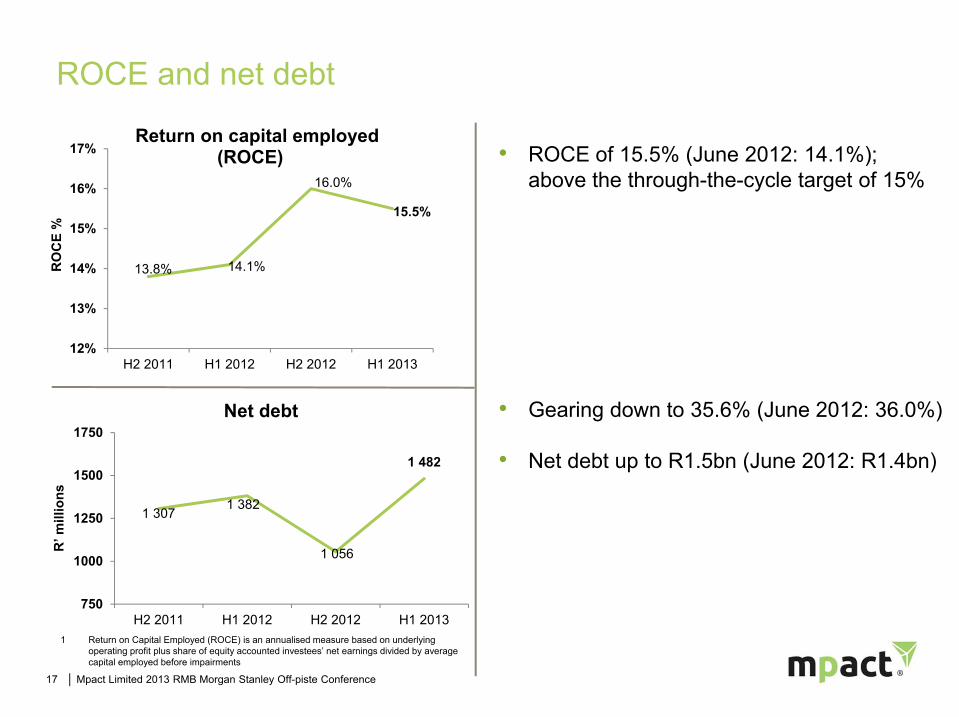

ROCE and net debt

13.8% 14.1%

16.0%

15.5%

12%

13%

14%

15%

16%

17%

H2 2011 H1 2012 H2 2012 H1 2013

RO

CE

%

Return on capital employed (ROCE)�

1 3071 382

1 056

1 482

750

1000

1250

1500

1750

H2 2011 H1 2012 H2 2012 H1 2013

R’ m

illio

ns

Net debt

• ROCE of 15.5% (June 2012: 14.1%);above the through-the-cycle target of 15%

• Gearing down to 35.6% (June 2012: 36.0%)

• Net debt up to R1.5bn (June 2012: R1.4bn)

1 Return on Capital Employed (ROCE) is an annualised measure based on underlying operating profit plus share of equity accounted investees’ net earnings divided by average capital employed before impairments

18 │ Mpact Limited 2013 RMB Morgan Stanley Off-piste Conference

Paper business

• Revenue up 6.9% to R2.6bn• Volumes up 1.3% • Price increases below inflation• Favourable product mix variance

• Underlying operating profit up 8.9% to R251m

• Stringent cost control• Offset by exchange rate driven

raw material cost increases • Integration benefits

150 192 220 231 251

265285

291331

7.8%9.1%

10.2% 9.7% 9.9%

0

100

200

300

400

500

600

2009 2010 2011 2012 2013

R’ m

illio

ns

Underlying operating profit�

HY1 HY2 HY1 margin

Paper 72%

Revenue

1 For comparative purposes, full year 2009, 2010 and 2011 underlying operating profit has been restated to reflect corporate costs of R50 million directly attributable, but previously not charged to the Paper business

4 0364 407 4 573

5 042

415477

511562

1 935 2 114 2 160 2 387 2 551

2 101 2 293 2 4132 655

0

1 000

2 000

3 000

4 000

5 000

2009 2010 2011 2012 2013

R’ m

illio

ns

External revenue

HY1 HY2

Operating profit

Paper88%

19 │ Mpact Limited 2013 RMB Morgan Stanley Off-piste Conference

Plastics business

1 For comparative purposes, full year 2009, 2010 and 2011 underlying operating profit has been restated to reflect corporate costs of R14 million directly attributable, but previously not charged to the Plastics business

• Revenue up 17.7% to R969m • Volumes up 14.1% (beverages, trays

and films, and acquisitions)• Price increases below inflation

• Underlying operating profit down 7.6% to R34m

• Under recovery of polymer prices• Improvements in FMCG and

preforms & closures

577 619 715 823 969

625 691862

955

0

500

1 000

1 500

2 000

2009 2010 2011 2012 2013

R’ m

illio

ns

Revenue

HY1 HY2

1 202 1 3101 577

1 778

20 23 2337 34

4154

77

80

3.5% 3.7% 3.2%4.5%

3.5%

0

20

40

60

80

100

120

2009 2010 2011 2012 2013

R’ m

illio

ns

Underlying operating profit�

HY1 HY2 HY1 margin

61

77

100

117

Plastics28%

RevenuePlastics12%

Operating profit

│ Presentation title │ 00 Month 20112020 │ Mpact Limited 2013 RMB Morgan Stanley Off-Piste Conference

Agenda

• Introduction

• Mpact business overview

• Group financial performance review

• Strategy

• Outlook

21 │ Mpact Limited 2013 RMB Morgan Stanley Off-piste Conference

Strategy

• Leading market positions• New business, market share, key products and geographical areas• Through strategic acquisitions and organic growth

• Customer focused operating structure• Investing to meet changing customer needs and to remain cost

competitive• Continue to develop geographic footprint

• Focus on performance• Delivering acceptable returns to our shareholders • Cost containment and improved efficiencies

│ Presentation title │ 00 Month 20112222 │ Mpact Limited 2013 RMB Morgan Stanley Off-Piste Conference

Agenda

• Introduction

• Mpact business overview

• Group financial performance review

• Strategy

• Outlook

23 │ Mpact Limited 2013 RMB Morgan Stanley Off-piste Conference

Outlook

• GDP and consumer spending growth expected to remain subdued

• Cost increases in labour, electricity and other administered services expected to be above inflation

• Trading conditions to remain highly competitive with associated margin pressures

• Weak rand should improve competitive position relative to imports, offset by related cost increases

• Focus on profitability, cash generation and ROCE

• Group is well positioned in the sectors in which it operates

24 │ Mpact Limited 2013 RMB Morgan Stanley Off-piste Conference

Thank you for your participation

For further information:

www.mpact.co.za

Bruce Strong, CEO(011) 994-5508

or

Marlize KeyterKeyter Rech Investor Solutions

(011) 447-5204

25 │ Mpact Limited 2013 RMB Morgan Stanley Off-piste Conference

DisclaimerThis document including, without limitation, those statements concerning the demand outlook, expansion projects and its capital resources and expenditure,may be considered to be forward looking statements. By their nature, forward-looking statements involve risk and uncertainty and although Mpact believes thatthe expectations reflected in such forward-looking statements are reasonable, no assurance can be given that such expectations will prove to have beencorrect. Accordingly, results could differ materially from those set out in the forward-looking statements as a result of, among other factors, changes in economicand market conditions, success of business and operating initiatives, changes in the regulatory environment and other government action and business andoperational risk management. While Mpact has taken reasonable care to ensure the accuracy of the information presented, Mpact accepts no responsibility forany consequential, indirect, special or incidental damages, whether foreseeable or unforeseeable, based on claims arising out of misrepresentation ornegligence arising in connection with a forward-looking statement. This document is not intended to contain any profit forecasts or profit estimates.