Risks Ahead for the Financial Industry in a Changing ... · Risks Ahead for the Financial Industry...

18

OECD Journal: Financial Market Trends Volume 2010 – Issue 1 © OECD 2010 Pre-publication version OECD JOURNAL: FINANCIAL MARKET TRENDS – VOLUME 2010 ISSUE 1 © OECD 2010 1 Risks Ahead for the Financial Industry in a Changing Interest Rate Environment Gert Wehinger * The current interest rate environment has been conducive to financial institutions assuming exposure to interest rate risks. As interest rates are expected to rise globally, albeit slowly, and current steep yield curves may soon flatten, such risks may materialise in the near future. At the same time, weaknesses in the banking sector still exist, especially for some segments of the European banking sector. While the effects of changes in interest rates and their structure on financial institutions differ, recent changes in asset and funding structures of banks make them generally more vulnerable to a changing interest rate environment. Currency risk exposure has also grown, and regional concentration may pose specific risks. An unravelling of carry trades will have a negative effect on some institutions. Proper risk management can help during an adjustment process, and regulatory reforms underway will better support risk management functions in financial institutions that are, in any case, already adjusting to the new environment. JEL Classification: G01, G12, G15, G21, G32 Keywords: financial crisis, interest rate risks, sovereign risks, bond markets, banks * Gert Wehinger is an economist in the Financial Affairs Division of the OECD Directorate for Financial and Enterprise Affairs. This article is based on a background note prepared for the OECD Financial Roundtable held on 15 April 2010 with participants from the private financial sector and members of the OECD Committee on Financial Markets. The present version takes into account the discussions and comments made at that meeting and selected developments that have taken place since. The author is grateful for additional comments from Adrian Blundell-Wignall and André Laboul, as well as editorial assistance from Laura McMahon and Jane Voros. The author is solely responsible for any remaining errors. This work is published on the responsibility of the Secretary-General of the OECD. The opinions expressed and arguments employed herein do not necessarily reflect the official views of the Organisation or the governments of its member countries.

Transcript of Risks Ahead for the Financial Industry in a Changing ... · Risks Ahead for the Financial Industry...

OECD Journal: Financial Market Trends Volume 2010 – Issue 1 © OECD 2010 Pre-publication version

OECD JOURNAL: FINANCIAL MARKET TRENDS – VOLUME 2010 ISSUE 1 © OECD 2010 1

Risks Ahead for the Financial Industry in a Changing

Interest Rate Environment

Gert Wehinger*

The current interest rate environment has been conducive to financial institutions assuming exposure to interest rate risks. As interest rates are expected to rise globally, albeit slowly, and current steep yield curves may soon flatten, such risks may materialise in the near future. At the same time, weaknesses in the banking sector still exist, especially for some segments of the European banking sector. While the effects of changes in interest rates and their structure on financial institutions differ, recent changes in asset and funding structures of banks make them generally more vulnerable to a changing interest rate environment. Currency risk exposure has also grown, and regional concentration may pose specific risks. An unravelling of carry trades will have a negative effect on some institutions. Proper risk management can help during an adjustment process, and regulatory reforms underway will better support risk management functions in financial institutions that are, in any case, already adjusting to the new environment.

JEL Classification: G01, G12, G15, G21, G32

Keywords: financial crisis, interest rate risks, sovereign risks, bond markets, banks

* Gert Wehinger is an economist in the Financial Affairs Division of the OECD Directorate for Financial and

Enterprise Affairs. This article is based on a background note prepared for the OECD Financial Roundtable held on 15 April 2010 with participants from the private financial sector and members of the OECD Committee on Financial Markets. The present version takes into account the discussions and comments made at that meeting and selected developments that have taken place since. The author is grateful for additional comments from Adrian Blundell-Wignall and André Laboul, as well as editorial assistance from Laura McMahon and Jane Voros. The author is solely responsible for any remaining errors. This work is published on the responsibility of the Secretary-General of the OECD. The opinions expressed and arguments employed herein do not necessarily reflect the official views of the Organisation or the governments of its member countries.

RISKS AHEAD FOR THE FINANCIAL INDUSTRY IN A CHANGING INTEREST RATE ENVIRONMENT

2 OECD JOURNAL: FINANCIAL MARKET TRENDS – VOLUME 2010 ISSUE 1 © OECD 2010

A. Current financial market outlook and risks

1. Selected recent developments

Financial markets are searching for direction, concerned about sovereign risk and the strength of the recovery

Financial markets are searching for direction. While the global recovery is ongoing, it is uneven across countries and regions, and investors still worry about sovereign risk and the potential fallout from fiscal austerity programmes and the gradual withdrawal of exceptional central bank support. Some emerging markets are showing signs of overvaluation, especially in Asia, which has received substantial capital inflows (Figure 1). Current weaknesses still warrant fiscal and monetary policy support in most OECD economies, but upward pressures on interest rates are increasing as public and corporate financing needs are high, while central banks have started to withdraw from the extraordinary policy measures they had taken in response to the financial and economic crisis. Significant market pressures have accelerated fiscal consolidation programmes in Europe. In emerging economies, most of which have been less afflicted by the crisis than OECD countries, markets have picked up more vigorously thanks to a relatively stronger recovery, and policy has started to tighten.

Figure 1. Returns across a broad spectrum of asset classes

Selected investment alternatives, percentage changes over period, annualised, in US dollar terms

‐64.1%‐49.0%

‐55.5%

‐53.7%

‐46.5%

‐40.5%

‐44.9%

‐50.4%

‐38.7%

‐38.6%

‐38.5%

‐43.3%

‐33.8%

‐28.7%

‐48.8%

‐28.2%

‐1.7%

‐6.7%‐10.2%

‐10.9%‐11.1%

30.0%

10.6%21.2%

‐47.5%‐42.8%

‐19.1%

12.3%

14.0%

12.7%

0.2%

49.9%

48.9%

45.5%

40.0%

33.7%

25.6%

19.5%

18.4%

16.2%

14.8%

13.5%

12.4%

11.9%

8.7%

6.7%

2.7%

29.2%

25.1%

24.8%

24.3%

21.9%

5.4%

1.2%

‐0.5%

49.7%

28.8%

19.5%

5.9%

1.3%

‐8.0%

‐13.6%

‐80% ‐60% ‐40% ‐20% 0% 20% 40% 60%

EQUITIES:INDIA‐DS Market

LATIN AMERICA‐DS MarketEMERGING MARKETS‐DS Market

ASIA EX JAPAN‐DS MarketCHINA‐DS MARKET $NASDAQ COMPOSITEWORLD‐DS Market

FTSE 100DJ US TOTAL STOCK MARKET

US‐DS MarketS&P 500 COMPOSITE

DAX 30 PERFORMANCEDOW JONES INDUSTRIALS

NIKKEI 225 STOCK AVERAGEEMU‐DS Market

TOPIX

BONDS:JPM EMBI GLOBAL MIDDLE EAST

JPM EMBI GLOBAL ASIAJPM EMBI GLOBAL AFRICA

JPM EMBI GLOBAL COMPOSITEJPM EMBI GLOBAL LATIN AMERICA

JP BENCHMARK 10 YEAR DS GOVT. INDEXEMU BENCHMARK 10 YR. DS GOVT. INDEXUS BENCHMARK 10 YEAR DS GOVT. INDEX

OTHER:Economist Commodity Inds/All ($)

S&P GSCI Commodity SpotDJ CS HEDGE HEDGE FUND $

Carry trade Index ‐ USD ‐ AUD (a)Carry trade Index ‐ USD ‐ NZ$ (a)Carry trade Index ‐ Yen ‐ AUD (a)Carry trade Index ‐ Yen ‐ USD (a)

2008 (1‐Jan‐08 to 1‐Jan‐09)

From 1‐Jan‐09 to 29‐Jul‐10 (annualised)

Notes: a) The carry trade return index is calculated based on the assumption of one-month investments in the respective currencies, borrowing in yen, applying one-month eurodollar interest rates and central exchange rates, without taking into account bid/ask spreads and transaction costs.

Sources: Thomson Reuters Datastream and OECD.

RISKS AHEAD FOR THE FINANCIAL INDUSTRY IN A CHANGING INTEREST RATE ENVIRONMENT

OECD JOURNAL: FINANCIAL MARKET TRENDS – VOLUME 2010 ISSUE 1 © OECD 2010 3

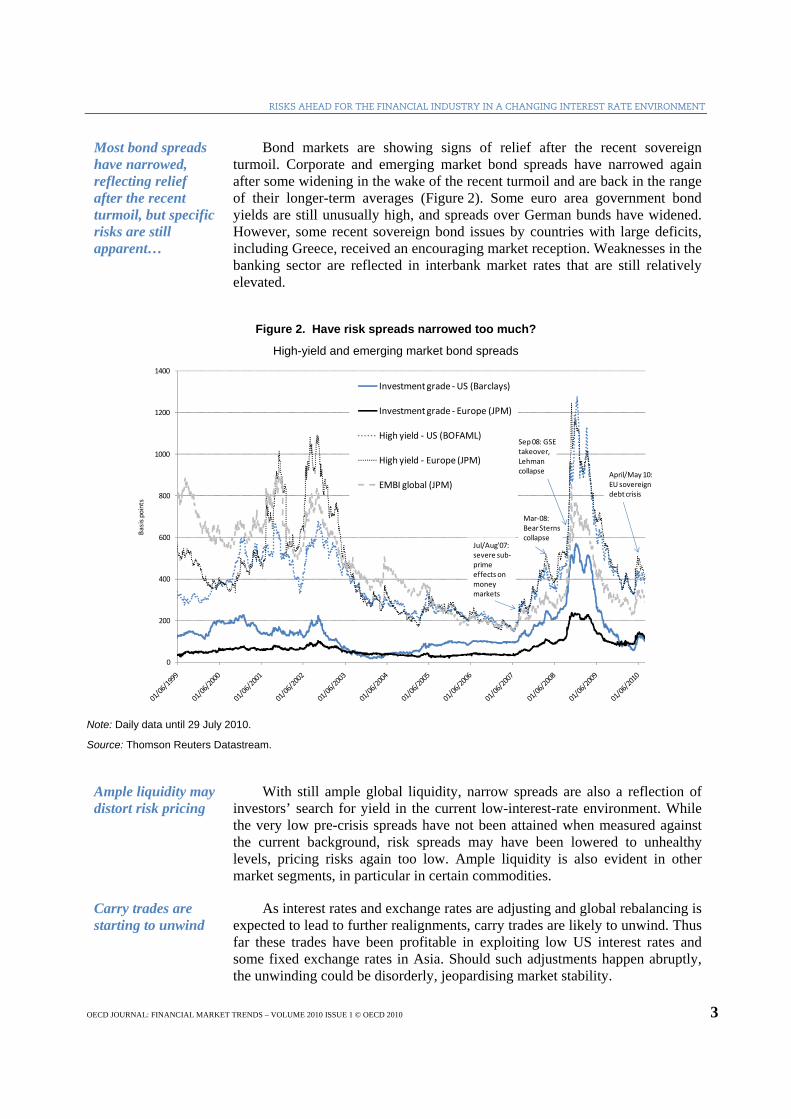

Most bond spreads have narrowed, reflecting relief after the recent turmoil, but specific risks are still apparent…

Bond markets are showing signs of relief after the recent sovereign turmoil. Corporate and emerging market bond spreads have narrowed again after some widening in the wake of the recent turmoil and are back in the range of their longer-term averages (Figure 2). Some euro area government bond yields are still unusually high, and spreads over German bunds have widened. However, some recent sovereign bond issues by countries with large deficits, including Greece, received an encouraging market reception. Weaknesses in the banking sector are reflected in interbank market rates that are still relatively elevated.

Figure 2. Have risk spreads narrowed too much?

High-yield and emerging market bond spreads

0

200

400

600

800

1000

1200

1400

Basis points

Investment grade ‐US (Barclays)

Investment grade ‐ Europe (JPM)

High yield ‐ US (BOFAML)

High yield ‐ Europe (JPM)

EMBI global (JPM)

Jul/Aug'07: severe sub‐prime effects on money markets

Mar‐08: Bear Sterns collapse

Sep 08: GSEtakeover,Lehman collapse April/May 10:

EU sovereigndebt crisis

Note: Daily data until 29 July 2010.

Source: Thomson Reuters Datastream.

Ample liquidity may distort risk pricing

With still ample global liquidity, narrow spreads are also a reflection of investors’ search for yield in the current low-interest-rate environment. While the very low pre-crisis spreads have not been attained when measured against the current background, risk spreads may have been lowered to unhealthy levels, pricing risks again too low. Ample liquidity is also evident in other market segments, in particular in certain commodities.

Carry trades are starting to unwind

As interest rates and exchange rates are adjusting and global rebalancing is expected to lead to further realignments, carry trades are likely to unwind. Thus far these trades have been profitable in exploiting low US interest rates and some fixed exchange rates in Asia. Should such adjustments happen abruptly, the unwinding could be disorderly, jeopardising market stability.

RISKS AHEAD FOR THE FINANCIAL INDUSTRY IN A CHANGING INTEREST RATE ENVIRONMENT

4 OECD JOURNAL: FINANCIAL MARKET TRENDS – VOLUME 2010 ISSUE 1 © OECD 2010

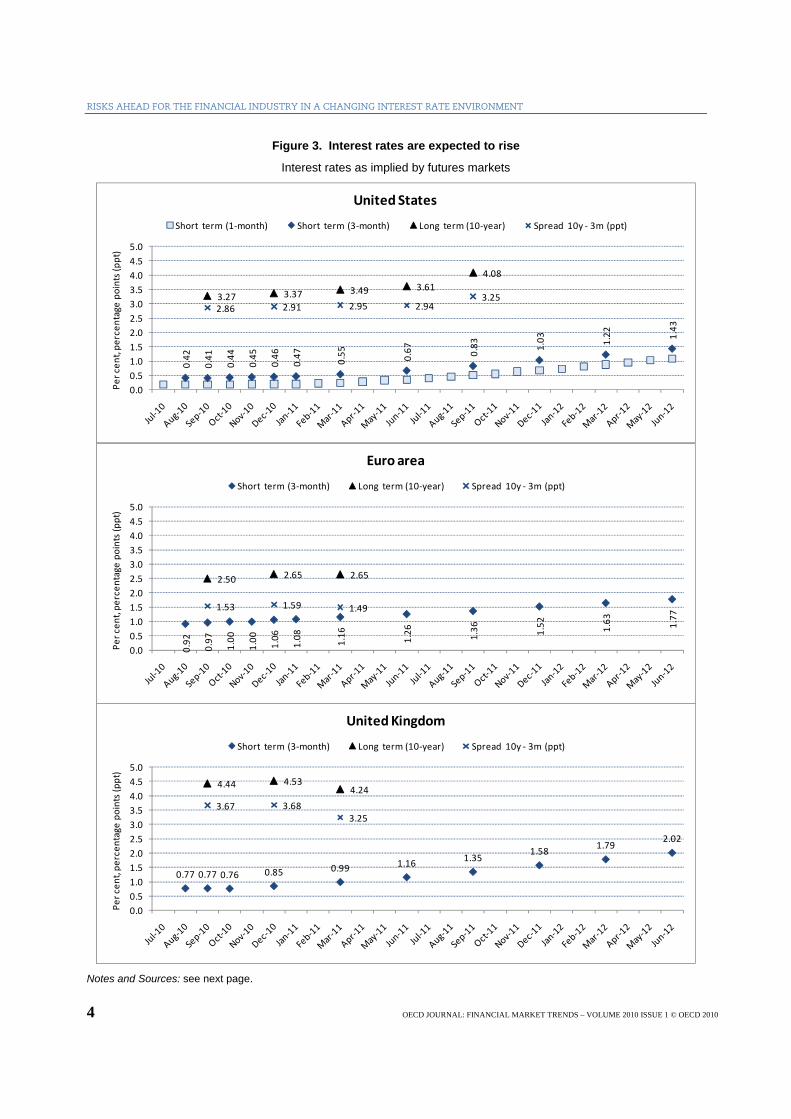

Figure 3. Interest rates are expected to rise

Interest rates as implied by futures markets 0.42

0.41

0.44

0.45

0.46

0.47 0.55 0.67 0.83 1.03 1.22 1.43

3.27 3.37 3.49 3.614.08

2.86 2.91 2.95 2.943.25

0.00.51.01.52.02.53.03.54.04.55.0

Per cen

t, pe

rcen

tage

points (ppt)

United States

Short term (1‐month) Short term (3‐month) Long term (10‐year) Spread 10y ‐ 3m (ppt)

0.92

0.97

1.00

1.00

1.06

1.08 1.16 1.26 1.36 1.52 1.63 1.77

2.50 2.65 2.65

1.53 1.59 1.49

0.00.51.01.52.02.53.03.54.04.55.0

Per cen

t, pe

rcen

tage

points (ppt)

Euro area

Short term (3‐month) Long term (10‐year) Spread 10y ‐ 3m (ppt)

0.77 0.77 0.76 0.85 0.99 1.16 1.351.58

1.792.02

4.44 4.534.24

3.67 3.683.25

0.00.51.01.52.02.53.03.54.04.55.0

Per cen

t, pe

rcen

tage

points (ppt)

United Kingdom

Short term (3‐month) Long term (10‐year) Spread 10y ‐ 3m (ppt)

Notes and Sources: see next page.

RISKS AHEAD FOR THE FINANCIAL INDUSTRY IN A CHANGING INTEREST RATE ENVIRONMENT

OECD JOURNAL: FINANCIAL MARKET TRENDS – VOLUME 2010 ISSUE 1 © OECD 2010 5

Figure 3 (cont’d). Interest rates are expected to rise

Interest rates as implied by futures markets

1.10 1.18 1.28 1.31 1.46 1.61 1.792.01 2.21

2.45

3.27 3.39 3.49 3.58

2.09 2.08 2.03 1.97

0.00.51.01.52.02.53.03.54.04.55.0

Per cen

t, pe

rcen

tage

points (ppt)

Canada

Short term (3‐month) Long term (10‐year) Spread 10y ‐ 3m (ppt)

0.36 0.34 0.33 0.32 0.30 0.30 0.31 0.33 0.34 0.36

0.00.51.01.52.02.53.03.54.04.55.0

Per cen

t, pe

rcen

tage

points (ppt)

Japan

Short term (3‐month)

Notes: Data as of 29 July 2010. United States: Short-term future rates are calculated from CBT 30-day Fed Funds (sett. price) and CME 3-month eurodollar (sett. price); long-term futures are CBT 10-year US T-note yields. Euro area: Short-term future rates are calculated from LIFFE 3-month Euribor (sett. price); long-term futures are Eurex Euro Bund yields. United Kingdom: Short-term future rates are calculated from LIFFE 3-month STERLING (sett. price); long-term futures are LIFFE Long GILT yields. Canada: Short-term future rates are calculated from ME Bank Accept. 90-day (sett. price); long-term futures are ME 10Y Canadian govt. bond yields. Japan: Short-term future rates are calculated from TIFFE 3-month euroyen Tibor (sett. price).

Sources: Thomson Reuters Datastream, OECD.

2. Interest rate outlook and risk premia

Interest rates are expected to rise globally, although not very steeply

In this context, interest rates are expected to rise more globally, as judged by futures markets (Figure 3). For most major economies, the very low short-term rates are expected to rise only very slowly this year, with some slightly more significant increases only as of next year. In Japan, short-term rates are expected to fall well into next year. This sluggish development of short-term rates mainly reflects the expectations that central banks will accommodate the remaining weaknesses of these economies, while inflation pressures (as

RISKS AHEAD FOR THE FINANCIAL INDUSTRY IN A CHANGING INTEREST RATE ENVIRONMENT

6 OECD JOURNAL: FINANCIAL MARKET TRENDS – VOLUME 2010 ISSUE 1 © OECD 2010

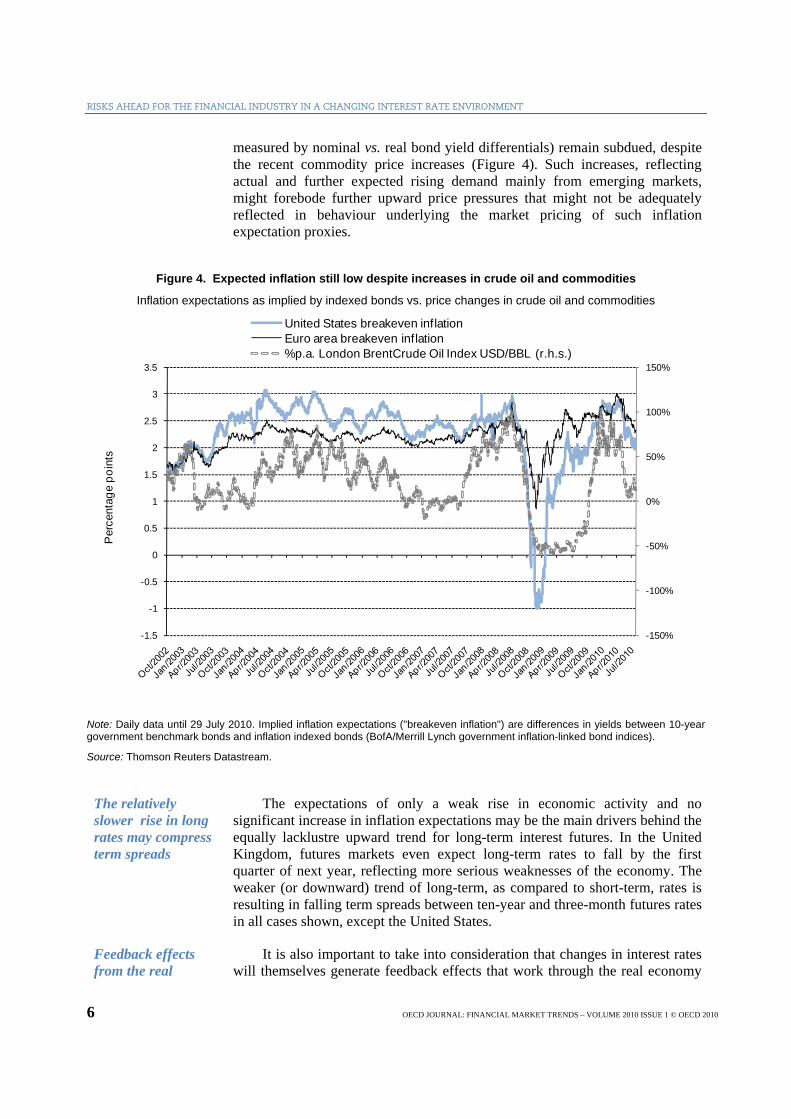

measured by nominal vs. real bond yield differentials) remain subdued, despite the recent commodity price increases (Figure 4). Such increases, reflecting actual and further expected rising demand mainly from emerging markets, might forebode further upward price pressures that might not be adequately reflected in behaviour underlying the market pricing of such inflation expectation proxies.

Figure 4. Expected inflation still low despite increases in crude oil and commodities

Inflation expectations as implied by indexed bonds vs. price changes in crude oil and commodities

-150%

-100%

-50%

0%

50%

100%

150%

-1.5

-1

-0.5

0

0.5

1

1.5

2

2.5

3

3.5

Per

cent

age

poin

ts

United States breakeven inflationEuro area breakeven inflation%p.a. London BrentCrude Oil Index USD/BBL (r.h.s.)

Note: Daily data until 29 July 2010. Implied inflation expectations ("breakeven inflation") are differences in yields between 10-year government benchmark bonds and inflation indexed bonds (BofA/Merrill Lynch government inflation-linked bond indices).

Source: Thomson Reuters Datastream.

The relatively slower rise in long rates may compress term spreads

The expectations of only a weak rise in economic activity and no significant increase in inflation expectations may be the main drivers behind the equally lacklustre upward trend for long-term interest futures. In the United Kingdom, futures markets even expect long-term rates to fall by the first quarter of next year, reflecting more serious weaknesses of the economy. The weaker (or downward) trend of long-term, as compared to short-term, rates is resulting in falling term spreads between ten-year and three-month futures rates in all cases shown, except the United States.

Feedback effects from the real

It is also important to take into consideration that changes in interest rates will themselves generate feedback effects that work through the real economy

RISKS AHEAD FOR THE FINANCIAL INDUSTRY IN A CHANGING INTEREST RATE ENVIRONMENT

OECD JOURNAL: FINANCIAL MARKET TRENDS – VOLUME 2010 ISSUE 1 © OECD 2010 7

economy could amplify or mitigate interest rate movements

and may mitigate or amplify interest rate movements. These changes are driven primarily by spending and investment decisions by firms and households. Important channels in this context are income and wealth effects. Regarding the income effect, for example, household spending decisions will depend on changes in the debt servicing burden. Likewise, investment decisions by firms will depend on financing costs and the burden of servicing current debt, even though firms tend to enjoy greater financing and risk hedging flexibility than households. For the same reasons, small firms would be more affected than large firms. Regarding the wealth effect, spending and investment decisions may be sensitive to changes in net wealth incurred by changes in interest rates. Both effects would then feed back into the financial sector in terms of credit demand, default rates and the like, with perhaps significant second- and third-round repercussions on interest rates and risk spreads (e.g. credit restrictions leading to further default rates and lower spending).

3. Sovereign risk and some implications

Sovereign risk premia and inflation may not be adequately reflected in futures prices

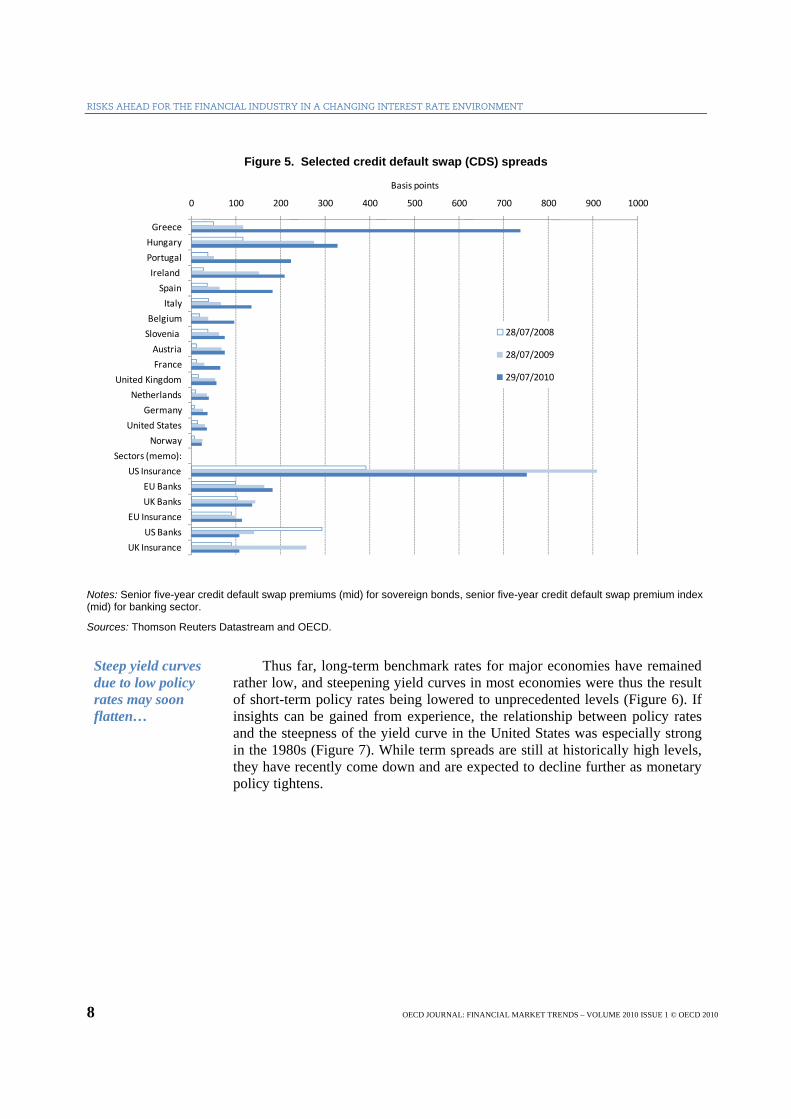

Looking at current developments and the risks ahead, the projections, as implied by futures markets and presented here, are highly uncertain. For one, these futures refer to supposedly “riskless” government paper, and it is only recently that the risk concept for government securities is being questioned (and may lead to a major overhaul of models and concepts in finance). The Greek crisis has shown that being part of a monetary union does not prevent speculative attacks on a member of the union, and widening deficits in many other OECD economies have put sovereign risks on top of risk watchers’ lists. Sovereign credit default swap (CDS) spreads have been reflecting such trends more strongly (Figure 5) – making some sovereigns look riskier than the banking sectors in major economies. However, the EU-IMF rescue package for Greece,1 ECB interventions in the euro area secondary markets for public and private debt securities, as well as the enhanced efforts for fiscal consolidation made by many European governments, have calmed the markets, and risk spreads have declined from their recent peaks.

Sovereign defaults may become a possibility

Even some large economies, whose market size and currency standing gives them easy access to market financing, are on rating agency watch for downgrades if their budget plans are considered to be unsustainable. For such economies, the problem may be that their relatively good liquidity position is hiding problems of a worsening, unsustainable solvency position. In the absence of immediate market pressure, necessary adjustment may be further delayed. While sovereign default is unlikely for large economies, a “quasi” default via high inflation may be an option, even though not an immediate one given the slack in most economies since the 2008 crisis. For smaller members of the euro area (as for any fixed exchange rate regime economy) this option is not available at a national level. As inflation cannot deviate too much from euro-wide inflation, a real devaluation, i.e. deflation, would be warranted. But this could trigger a detrimental debt-deflation spiral, in which the real value of debt increases, with negative feedback from deflation and recession.

RISKS AHEAD FOR THE FINANCIAL INDUSTRY IN A CHANGING INTEREST RATE ENVIRONMENT

8 OECD JOURNAL: FINANCIAL MARKET TRENDS – VOLUME 2010 ISSUE 1 © OECD 2010

Figure 5. Selected credit default swap (CDS) spreads

0 100 200 300 400 500 600 700 800 900 1000

Greece

Hungary

Portugal

Ireland

Spain

Italy

Belgium

Slovenia

Austria

France

United Kingdom

Netherlands

Germany

United States

Norway

Sectors (memo):

US Insurance

EU Banks

UK Banks

EU Insurance

US Banks

UK Insurance

Basis points

28/07/2008

28/07/2009

29/07/2010

Notes: Senior five-year credit default swap premiums (mid) for sovereign bonds, senior five-year credit default swap premium index (mid) for banking sector.

Sources: Thomson Reuters Datastream and OECD.

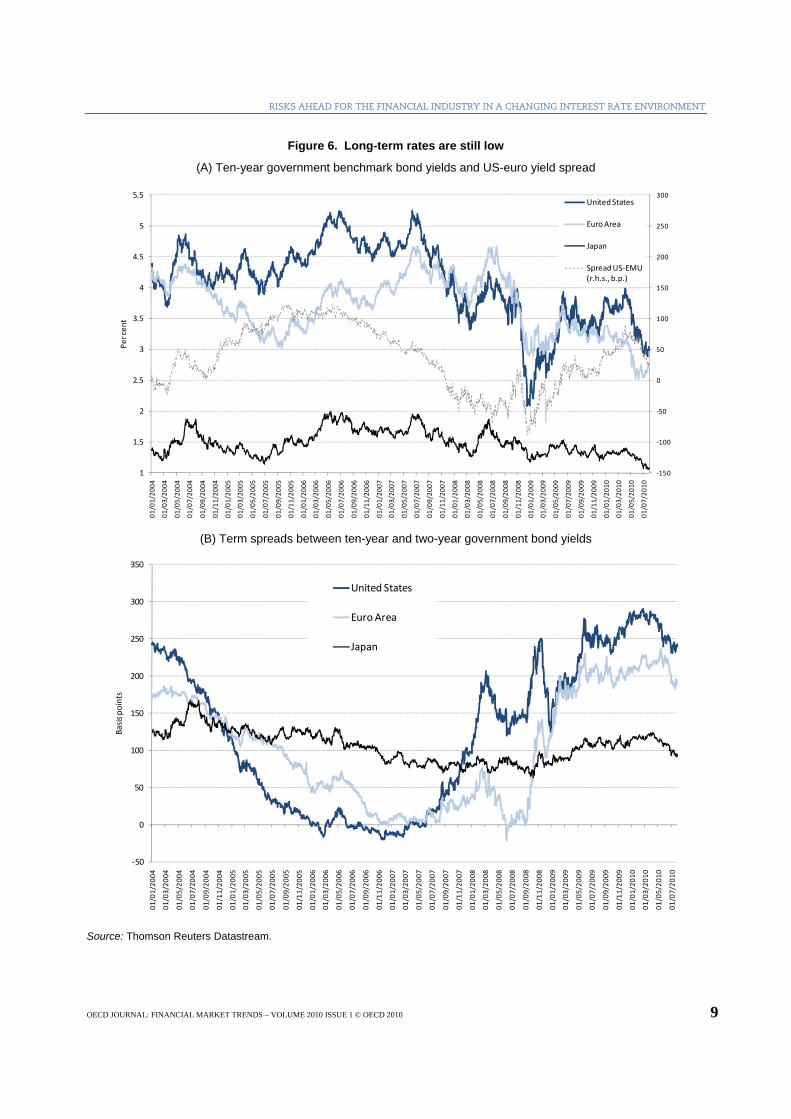

Steep yield curves due to low policy rates may soon flatten…

Thus far, long-term benchmark rates for major economies have remained rather low, and steepening yield curves in most economies were thus the result of short-term policy rates being lowered to unprecedented levels (Figure 6). If insights can be gained from experience, the relationship between policy rates and the steepness of the yield curve in the United States was especially strong in the 1980s (Figure 7). While term spreads are still at historically high levels, they have recently come down and are expected to decline further as monetary policy tightens.

RISKS AHEAD FOR THE FINANCIAL INDUSTRY IN A CHANGING INTEREST RATE ENVIRONMENT

OECD JOURNAL: FINANCIAL MARKET TRENDS – VOLUME 2010 ISSUE 1 © OECD 2010 9

Figure 6. Long-term rates are still low

(A) Ten-year government benchmark bond yields and US-euro yield spread

‐150

‐100

‐50

0

50

100

150

200

250

300

1

1.5

2

2.5

3

3.5

4

4.5

5

5.5

01/01/20

04

01/03/20

04

01/05/20

04

01/07/20

04

01/09/20

04

01/11/20

04

01/01/20

05

01/03/20

05

01/05/20

05

01/07/20

05

01/09/20

05

01/11/20

05

01/01/20

06

01/03/20

06

01/05/20

06

01/07/20

06

01/09/20

06

01/11/20

06

01/01/20

07

01/03/20

07

01/05/20

07

01/07/20

07

01/09/20

07

01/11/20

07

01/01/20

08

01/03/20

08

01/05/20

08

01/07/20

08

01/09/20

08

01/11/20

08

01/01/20

09

01/03/20

09

01/05/20

09

01/07/20

09

01/09/20

09

01/11/20

09

01/01/20

10

01/03/20

10

01/05/20

10

01/07/20

10

Per cen

t

United States

Euro Area

Japan

Spread US‐EMU (r.h.s., b.p.)

(B) Term spreads between ten-year and two-year government bond yields

‐50

0

50

100

150

200

250

300

350

01/01/20

04

01/03/20

04

01/05/20

04

01/07/20

04

01/09/20

04

01/11/20

04

01/01/20

05

01/03/20

05

01/05/20

05

01/07/20

05

01/09/20

05

01/11/20

05

01/01/20

06

01/03/20

06

01/05/20

06

01/07/20

06

01/09/20

06

01/11/20

06

01/01/20

07

01/03/20

07

01/05/20

07

01/07/20

07

01/09/20

07

01/11/20

07

01/01/20

08

01/03/20

08

01/05/20

08

01/07/20

08

01/09/20

08

01/11/20

08

01/01/20

09

01/03/20

09

01/05/20

09

01/07/20

09

01/09/20

09

01/11/20

09

01/01/20

10

01/03/20

10

01/05/20

10

01/07/20

10

Basis p

oints

United States

Euro Area

Japan

Source: Thomson Reuters Datastream.

RISKS AHEAD FOR THE FINANCIAL INDUSTRY IN A CHANGING INTEREST RATE ENVIRONMENT

10 OECD JOURNAL: FINANCIAL MARKET TRENDS – VOLUME 2010 ISSUE 1 © OECD 2010

Figure 7. US monetary policy impact on yield curves

Term spread of ten-year minus two-year benchmark yield vs. Fed funds target rate

0

2

4

6

8

10

12

14

16

18

20‐200

‐150

‐100

‐50

0

50

100

150

200

250

300

Jan‐1980

Oct‐1980

Jul‐1981

Apr‐1982

Jan‐1983

Oct‐1983

Jul‐1984

Apr‐1985

Jan‐1986

Oct‐1986

Jul‐1987

Apr‐1988

Jan‐1989

Oct‐1989

Jul‐1990

Apr‐1991

Jan‐1992

Oct‐1992

Jul‐1993

Apr‐1994

Jan‐1995

Oct‐1995

Jul‐1996

Apr‐1997

Jan‐1998

Oct‐1998

Jul‐1999

Apr‐2000

Jan‐2001

Oct‐2001

Jul‐2002

Apr‐2003

Jan‐2004

Oct‐2004

Jul‐2005

Apr‐2006

Jan‐2007

Oct‐2007

Jul‐2008

Apr‐2009

Jan‐2010

Basis p

oints

memo: US recessions (NBER) United StatesEuro Area JapanUS Fed funds target rate (r.h.s., inverted)

Source: Thomson Reuters Datastream.

…but fiscal pressures and corporate financing needs may lift rates at the long end

But further fiscal pressures will keep government financing needs at high levels and add to inflation risks further down the line. Paired with competition for financing from the corporate sector, in particular from financial institutions that have to roll over massive amounts of debt in the near future, this should raise rates at the long end, likely more than futures markets currently expect. Should monetary policy react to such pressures, raising rates more than markets currently predict, this could counterbalance the rise at the long end and flatten yield curves even more. All this will also depend on the impact of inflation and inflation expectations on the short and the long end of the curve, and how much monetary policy will “lean against the wind”.

B. Financial sector soundness, risk exposures and risk management

1. Current weaknesses

Weaknesses in the banking sector are still pertinent...

The banking sector is still fragile. While banks are preparing for tighter capital and liquidity requirements that are likely to be required when Basel III concludes at the end of 2010 (although phase-in periods will apply), many weaknesses remain. Exposure to commercial real estate risks (small banks in the US and some regional banks in Europe) and sovereign risks (in Europe) are of major concern, and so is funding. While major US banks have been enjoying solid profits and deleveraging for some time, the process of deleveraging is

RISKS AHEAD FOR THE FINANCIAL INDUSTRY IN A CHANGING INTEREST RATE ENVIRONMENT

OECD JOURNAL: FINANCIAL MARKET TRENDS – VOLUME 2010 ISSUE 1 © OECD 2010 11

lagging in Europe. However, profit reports of major European banks for the first half of 2010 have been rather positive, mostly due to falling loan losses. The results of Europe’s stress-testing of 91 banks announced on 23 July, found that (only) seven banks need more capital. This has boosted confidence and calmed the markets.

...especially for some segments of the European banking sector

Despite the relatively comforting results of the European banking sector stress tests, the aggregate results illustrate, according to the Committee of European Banking Supervisors (CEBS), “the continued reliance on government support for currently 38 institutions participating in the exercise. Consequently, it seems too early to speak about a generic ‘forced’ withdrawal. Any considerations of possible exit strategies should rather take into account detailed case-by-case analysis in order to ensure banks’ long-term viability after an exit from government support has taken place.”2 Moreover, observers have commented on the weaknesses in the German Sparkassen sector, which was not part of these stress tests.

Table 1. Banks’ market value losses and gains

Change in market value of largest G20 banks, in USD billiona)

2010b) 2009 2008 2007 2006 2005memo:MV (latest)e)

memo: recoveryf)

United States 72.8 220.1 - 338.0 - 295.2 175.0 - 19.9 811.5 86.7 United Kingdom 41.4 179.3 - 256.7 - 72.8 109.0 - 19.1 421.8 86.0 Italy - 28.5 40.0 - 177.8 73.2 61.4 47.1 142.3 6.5 France - 27.5 107.4 - 157.6 - 31.6 108.6 13.4 184.3 50.7 China - 6.5 136.4 - 124.3 60.1 82.3 - 347.3 104.5 Australia - 6.7 139.7 - 110.9 43.7 38.9 18.2 258.1 119.9 Japan 27.0 - 40.5 - 107.6 - 111.8 - 48.6 204.0 283.6 - 12.5 Russian Federation 8.6 61.4 - 107.5 24.7 45.3 17.1 99.0 65.1 Canada 16.8 112.2 - 97.4 12.2 31.1 37.2 261.6 132.4 Brazil 1.7 150.8 - 88.1 60.6 37.8 29.9 299.7 173.1 Germany - 0.2 28.0 - 80.0 - 3.7 34.1 14.8 68.1 34.8 Turkey 18.7 49.9 - 67.6 39.6 - 4.0 25.7 112.6 101.5 South Korea - 0.6 38.2 - 63.8 - 0.0 11.9 39.1 71.2 59.0 India 15.9 45.5 - 59.3 56.5 16.7 11.6 113.9 103.7 South Africa 8.6 22.4 - 22.3 - 0.2 6.8 7.9 70.9 138.8 Indonesia 17.9 24.2 - 16.2 7.6 14.1 - 1.4 66.0 259.9 Mexico 4.0 7.2 - 8.9 5.6 6.6 0.8 28.4 125.9 Argentina 1.2 2.8 - 3.2 - 1.2 2.3 0.2 6.5 121.8

G20 countries' total 164.7 1 324.9 -1 887.3 - 132.6 729.2 426.5 3 646.8 78.9

memo item: Euro area totalc) - 120.6 304.0 - 788.0 81.6 379.2 105.4 711.6 23.3

memo item: G7 totalc) 101.8 646.5 -1 215.1 - 429.6 470.5 277.5 2 184.5 61.6 memo item: Globald) 130.5 1 710.6 -2 787.4 - 49.8 1 138.8 504.2 4 888.1 66.1

Sorted by 2008 losses. a) Based on banks contained in respective countries' Datastream bank indices. Note that such data are not available for Saudi Arabia. b) From 1-Jan-10 to 29-Jul-10. c) Based on banks contained in respective countries' Datastream bank indices. d) Based on banks in Datastream worldwide bank index. e) Memo item: Market valuation as of 05-Apr-10. f) Ratio of sum of change in 2009 and 2010(b) over the negative change in 2008, in per cent.

Sources: Thomson Reuters and OECD.

RISKS AHEAD FOR THE FINANCIAL INDUSTRY IN A CHANGING INTEREST RATE ENVIRONMENT

12 OECD JOURNAL: FINANCIAL MARKET TRENDS – VOLUME 2010 ISSUE 1 © OECD 2010

Favourable profit conditions for banks are waning and bank share prices have been declining in many cases

While financial institutions have been profiting from improving and favourable conditions over the last year, earnings reports as recently released by some major banks for the second quarter of 2010 show that these conditions are waning. Over the past year and well into 2010, share prices of the sector have improved to an extent that by now most banking sectors have recuperated most or even overcompensated previous (2008) losses in market value (based on sectoral indices for G20 economies; Table 1). However, more recent developments led to year-to-date (end-of-July) declines in market value in several cases, and these declines were particularly strong for banks in France and Italy. If measured against broad stock market developments (and looking at a slightly different sample highlighting some more European banking sectors), the situation for the banking sectors in several countries looks even gloomier (Figure 8).

Figure 8. Weaknesses in the banking sector still pertinent

Year-on-year growth of selected banking sector equity indices relative to total stock market

8.7

‐2.6

‐3.3

‐7.2

‐8.7

‐9.7

‐10.8

‐12.5

‐13.2

‐13.6

‐16.6

‐21.3

‐29.5

‐32.0

‐34.0

‐100 ‐80 ‐60 ‐40 ‐20 0 20 40 60

Canada

United Kingdom

Australia

Spain

Germany

United States

Sweden

France

Japan

Italy

Switzerland

Euro Area

Netherlands

Belgium

Greece

Per cent

Year‐to‐date (as of 29‐Jul‐2010, annualised) 2009 2008

Note: Sorted by year-to-date declines. Sources: Thomson Reuters Datastream and OECD.

Many smaller US banks are affected, and important risks remain to the US financial system overall

In the United States, defaults among smaller banks reached record levels in 2009, affecting 140 banks; this is almost triple the total of 53 failed banks in the period 2000-2008 as a whole (26 failed banks in 2008 already having been the record of that period). Government support (liability guarantees and capital) will still be needed, as vulnerabilities remain high and low capital levels may be squeezed by further losses, stemming from commercial property and

RISKS AHEAD FOR THE FINANCIAL INDUSTRY IN A CHANGING INTEREST RATE ENVIRONMENT

OECD JOURNAL: FINANCIAL MARKET TRENDS – VOLUME 2010 ISSUE 1 © OECD 2010 13

consumer loans, for example, as well as by feedback effects from lower economic activity. The fragility of the current situation has also been noticed by the IMF in its recent Financial System Stability Assessment of the United States, which found that bank balance sheets “remain fragile and capital buffers may still be inadequate in the face of further increases in nonperforming loans.”3

2. Interest rate risk, exchange rate risk and sovereign exposures

Interest rate risks are related to repricing risk, yield curve risk, basis risk and optionality

In addition to the current weakness and vulnerability of the financial sector rooted in the crisis, a changing interest rate environment and exchange rate adjustment are posing specific, additional risks further down the line. The key elements of interest rate risk for banks include repricing risk, yield curve risk, basis risk and optionality.4 Repricing risks arise from timing differences in the maturity for fixed-rate and repricing for floating-rate bank assets, liabilities and off-balance-sheet positions. Yield curve risks cover adverse effects on a bank's income or underlying economic value stemming from unanticipated shifts of the yield curve. Basis risks are rooted in an imperfect correlation in the adjustment of the rates earned and paid on different instruments with otherwise similar repricing characteristics. Optionality has become an increasingly important source of interest rate risk, arising from the options embedded in many bank assets, liabilities and off-balance-sheet portfolios.

The current interest rate environment has been conducive to assuming interest rate risk exposure

The currently low short-term (policy) rates and steep yield curves (see above), paired with relatively stable or fixed exchange rates (especially in Asia), have been providing incentives to profit from positive carry in fixed income and foreign exchange markets. This will typically add to investors’ holdings of long-term assets and tilt funding profiles towards shorter maturities, thus potentially adding to maturity mismatches.

Effects of changes in the interest rate structure on financial institutions differ

The effects of changes in the interest structure differ across financial institutions. In general, banks and other institutions that engage in positive maturity transformation (borrowing short and lending long), and thus profit from the steepness of the yield curve, will suffer from any flattening of the curve, irrespective of whether this has been brought about by higher short-term rates or by lower long-term rates. More broadly, “asset sensitive” institutions, i.e. those whose assets are expected to re-price faster than their liabilities, would be positively affected by a rise in interest rates because their net interest margins increase. Conversely, “liability sensitive” institutions will profit from a fall in interest rates.5

Banks’ recent changes in asset and funding structures make them more vulnerable to a changing interest rate environment

Generally, the impact of interest rate changes will depend on the maturity and re-pricing structure of institutions’ balance and off-balance-sheet items, and are complex to analyse. Also, complexity of this structure has increased as financial institutions have been assuming more complex exposures to interest rate risk through structured products, with an embedded interest rate risk that has not always been fully understood. More recently, during the crisis, many banks have significantly increased their holdings of excess reserves and other short-term liquid assets, suggesting their ability to benefit from increases in

RISKS AHEAD FOR THE FINANCIAL INDUSTRY IN A CHANGING INTEREST RATE ENVIRONMENT

14 OECD JOURNAL: FINANCIAL MARKET TRENDS – VOLUME 2010 ISSUE 1 © OECD 2010

short-term rates. At the same time, increased reliance on wholesale funding (instead of deposits with low and relatively stable interest rates) has rendered banks more sensitive to interest rate changes.

Proper risk management can help during an adjustment process

Adjustments to changes in the interest rate structure will depend not only on the risk exposure of financial institutions (which is hard to monitor based on public disclosures), but also on the way in which risk embedded in these exposures is managed. Adjustment processes can be abrupt, as feedback effects may be at work that amplify the speed and extent of rebalancing. Work by the Basle Committee6 has looked at these issues well before this financial crisis and has proposed principles to be used in evaluating a bank’s interest rate risk management and interest rate risk exposure, and in developing a (supervisory) response to that risk. At the core of these principles is the involvement of the board and senior management in the oversight of interest rate risk, and the responsibility of senior management in ensuring that the structure of the bank's business and the level of interest rate risk it assumes are effectively managed, evaluated and controlled. In order to perform these tasks, banks must have adequate information systems in place, and reports, independent reviews and evaluations should result in revisions where necessary, and be made available to the relevant supervisory authorities. Banks must also hold capital commensurate with the level of interest rate risk they undertake, and should release information on the level of interest rate risk and policies for its management.

Currency risk exposure has grown, and regional concentration may pose specific risks

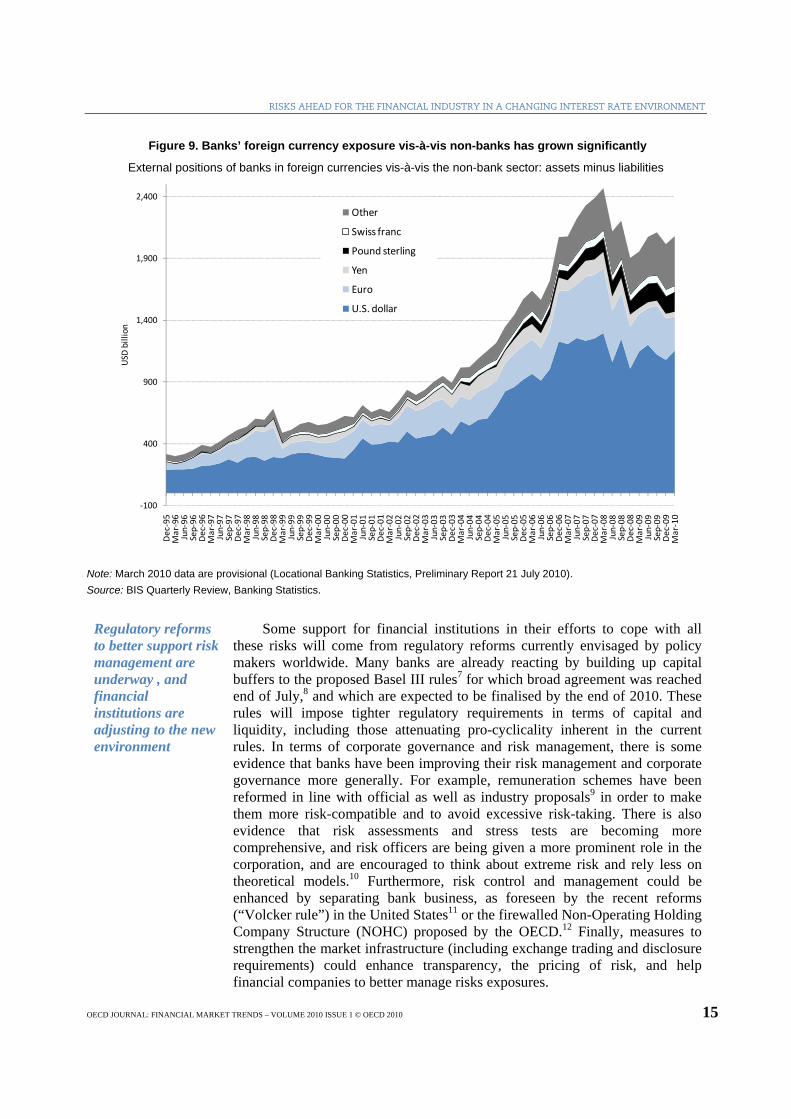

The profitably of carry trades as well as the increased globalisation of the financial industry has substantially increased banks’ foreign currency exposure (Figure 9). Profit opportunities arising from, among other factors, relatively stronger growth in certain regions as well as specific country contexts and relations (e.g. between Spain and Latin America) have favoured foreign exchange exposure of major OECD banks to emerging European and other developing regions (Figure 10). If such exposure becomes too concentrated, i.e. if not diversified over a wider range of countries and regions, this could pose risks. For example, observers have warned of the exposure of some European banks to Eastern Europe, where some economies are weakened and many financial institutions have been hit hard by the crisis. And, more recently, sovereign exposures to some countries on the euro area periphery have come into the focus.

How the unravelling of carry trades affects a given institution depends on the type of institution and the types of trades it does

The effects of exchange rates and unwinding of carry trades on financial institutions is more difficult to predict. First, the foreign exchange market is rather opaque, as participants know their positions relative to a given counterparty, but not the aggregate position of a given counterparty. Second, how the unravelling of carry trades affects a given institution depends to a large extent on the type of trades that an institution engages in. For example, for institutions that are using foreign exchange primarily to trade their proprietary books, a rapid rise in the rate of their short currencies could have significant negative effects. On the other hand, for clearing banks, an increase in volume and volatility on FX markets is likely to prove highly profitable. Overall, how currency movements affect a bank’s exposure depends primarily on the nature of the institution and the currency of its home market.

RISKS AHEAD FOR THE FINANCIAL INDUSTRY IN A CHANGING INTEREST RATE ENVIRONMENT

OECD JOURNAL: FINANCIAL MARKET TRENDS – VOLUME 2010 ISSUE 1 © OECD 2010 15

Figure 9. Banks’ foreign currency exposure vis-à-vis non-banks has grown significantly

External positions of banks in foreign currencies vis-à-vis the non-bank sector: assets minus liabilities

‐100

400

900

1,400

1,900

2,400

Dec‐95

Mar‐96

Jun‐96

Sep‐96

Dec‐96

Mar‐97

Jun‐97

Sep‐97

Dec‐97

Mar‐98

Jun‐98

Sep‐98

Dec‐98

Mar‐99

Jun‐99

Sep‐99

Dec‐99

Mar‐00

Jun‐00

Sep‐00

Dec‐00

Mar‐01

Jun‐01

Sep‐01

Dec‐01

Mar‐02

Jun‐02

Sep‐02

Dec‐02

Mar‐03

Jun‐03

Sep‐03

Dec‐03

Mar‐ 04

Jun‐04

Sep‐04

Dec‐04

Mar‐05

Jun‐05

Sep‐05

Dec‐05

Mar‐06

Jun‐06

Sep‐06

Dec‐06

Mar‐07

Jun‐07

Sep‐07

Dec‐07

Mar‐08

Jun‐08

Sep‐08

Dec‐08

Mar‐09

Jun‐09

Sep‐09

Dec‐09

Mar‐10

USD

billion

Other

Swiss franc

Pound sterling

Yen

Euro

U.S. dollar

Note: March 2010 data are provisional (Locational Banking Statistics, Preliminary Report 21 July 2010). Source: BIS Quarterly Review, Banking Statistics.

Regulatory reforms to better support risk management are underway , and financial institutions are adjusting to the new environment

Some support for financial institutions in their efforts to cope with all these risks will come from regulatory reforms currently envisaged by policy makers worldwide. Many banks are already reacting by building up capital buffers to the proposed Basel III rules7 for which broad agreement was reached end of July,8 and which are expected to be finalised by the end of 2010. These rules will impose tighter regulatory requirements in terms of capital and liquidity, including those attenuating pro-cyclicality inherent in the current rules. In terms of corporate governance and risk management, there is some evidence that banks have been improving their risk management and corporate governance more generally. For example, remuneration schemes have been reformed in line with official as well as industry proposals9 in order to make them more risk-compatible and to avoid excessive risk-taking. There is also evidence that risk assessments and stress tests are becoming more comprehensive, and risk officers are being given a more prominent role in the corporation, and are encouraged to think about extreme risk and rely less on theoretical models.10 Furthermore, risk control and management could be enhanced by separating bank business, as foreseen by the recent reforms (“Volcker rule”) in the United States11 or the firewalled Non-Operating Holding Company Structure (NOHC) proposed by the OECD.12 Finally, measures to strengthen the market infrastructure (including exchange trading and disclosure requirements) could enhance transparency, the pricing of risk, and help financial companies to better manage risks exposures.

RISKS AHEAD FOR THE FINANCIAL INDUSTRY IN A CHANGING INTEREST RATE ENVIRONMENT

16 OECD JOURNAL: FINANCIAL MARKET TRENDS – VOLUME 2010 ISSUE 1 © OECD 2010

Figure 10. Banks’ foreign currency exposure is substantial in some countries

Consolidated foreign claims of reporting banks vis-à-vis selected countries and regions, ultimate risk basis. Amounts outstanding as of end-March 2009, in USD billion

0 500 1,000 1,500 2,000 2,500 3,000 3,500

Other (a)

Other European banks

France

Germany

Italy

Spain

Switzerland

United Kingdom

Japan

United States

USD billion

Other developing countries

Latin America/Caribbean

Emerging Europe

Asia & Pacific

Other developed countries

United States

Western Europe

a) The rest of a total of 24 reporting countries (reporting countries are: Austria, Australia, Belgium, Canada, Chile, Chinese Taipei, Finland, France, Germany, Greece, India, Ireland, Italy, Japan, the Netherlands, Norway, Portugal, Singapore, Spain, Sweden, Switzerland, Turkey, the United Kingdom and the United States).

Note: Data are provisional (Consolidated Banking Statistics, Preliminary Report 21 July 2010).

Source: BIS Quarterly Review, Banking Statistics.

RISKS AHEAD FOR THE FINANCIAL INDUSTRY IN A CHANGING INTEREST RATE ENVIRONMENT

OECD JOURNAL: FINANCIAL MARKET TRENDS – VOLUME 2010 ISSUE 1 © OECD 2010 17

NOTES

1 Following the tensions on European sovereign issuers, the Ecofin Council and the EU Member States agreed on

10 May on a comprehensive package of stability measures, including a European Financial Stabilisation Mechanism. This arrangement will provide up to EUR 500 billion of funds committed by euro area members to members in difficulty, subject to strong conditionality. The IMF is participating in the financing arrangements with EUR 250 billion. EUR 60 billion of the EU commitment draws on an existing facility, and EUR 440 billion will be sourced through a special purpose vehicle (SPV).

2 CEBS et al. (2010).

3 IMF (2010).

4 For more details see BCBS (2004).

5 For this and the following paragraph, see also Kohn (2010).

6 BCBS (2004).

7 BCBS (2009a, b).

8 On 26 July 2010 the Group of Governors and Heads of Supervision, the oversight body of the Basel Committee on Banking Supervision, reached broad agreement on the Basel Committee's capital and liquidity reform package; see the BIS press release at http://www.bis.org/press/p100726.htm and its annex http://www.bis.org/press/p100726/annex.pdf.

9 For industry recommendations to reform remuneration policies, see IIF (2008).

10 It is also interesting to note that JPMorgan Chase has put aside USD 3 billion of “model-uncertainty reserves” to cover losses related to mishaps of quantitative models (see The Economist, “Number-crunchers crunched”, February 13, 2010).

11 The so called Dodd-Frank Wall Street Reform and Consumer Protection Act was signed into law by President Obama on 21 July 2010 and should “promote the financial stability of the United States by improving accountability and transparency in the financial system, to end ‘too big to fail’, to protect the American taxpayer by ending bailouts, to protect consumers from abusive financial services practices, and for other purposes.”

12See OECD (2009), and Blundell-Wignall et al. (2009).

RISKS AHEAD FOR THE FINANCIAL INDUSTRY IN A CHANGING INTEREST RATE ENVIRONMENT

18 OECD JOURNAL: FINANCIAL MARKET TRENDS – VOLUME 2010 ISSUE 1 © OECD 2010

REFERENCES

Basel Committee on Banking Supervision (BCBS) (2004), Principles for the Management and Supervision of Interest Rate Risk, July.

Basel Committee on Banking Supervision (BCBS) (2009a), Strengthening the Resilience of the Banking Sector, consultative document, December, available at www.bis.org/publ/bcbs164.htm.

Basel Committee on Banking Supervision (BCBS) (2009b), International framework for liquidity risk measurement, standards and monitoring, consultative document, December, available at www.bis.org/publ/bcbs165.htm.

Blundell-Wignall, Adrian, Gert Wehinger and Patrick Slovik (2009), “The Elephant in the Room: The Need to Deal with What Banks Do”, OECD Journal: Financial Market Trends, vol. 2009/2.

Committee of European Banking Supervisors (CEBS), European Central Bank (ECB) and European Commission (2010), Questions & Answers: 2010 EU-wide stress testing exercise, available at http://www.ecb.int/pub/pdf/other/euwidestresstestingexercise-qaen.pdf.

Donald L. Kohn (2010), Focusing on Bank Interest Rate Risk Exposure, Remarks at the Federal Deposit Insurance Corporation’s Symposium on Interest Rate Risk Management, Arlington, Virginia, January 29.

Institute of International Finance (IIF), Final Report of the IIF Committee on Market Best Practices: Principles of Conduct and Best Practice Recommendations – Financial Services Industry Response to the Market Turmoil of 2007-2008, July 2008, available at www.iif.com/regulatory.

International Monetary Fund (IMF) (2010), “United States: Publication of Financial Sector Assessment Program Documentation – Financial System Stability Assessment”, IMF Country Report No. 10/247; available at http://www.imf.org/external/pubs/ft/scr/2010/cr10247.pdf.

OECD (2009), The Financial Crisis: Reform and Exit Strategies, September 2009, OECD, Paris, available at www.oecd.org/dataoecd/55/47/43091457.pdf.