Risk, Uncertainty, and Sensitivity Analysis How economics can help understand, analyze, and cope...

23

Risk, Uncertainty, and Sensitivity Analysis How economics can help understand, analyze, and cope with limited information

-

Upload

alexys-stroker -

Category

Documents

-

view

216 -

download

2

Transcript of Risk, Uncertainty, and Sensitivity Analysis How economics can help understand, analyze, and cope...

Risk, Uncertainty, and Sensitivity AnalysisHow economics can help understand, analyze, and cope with limited information

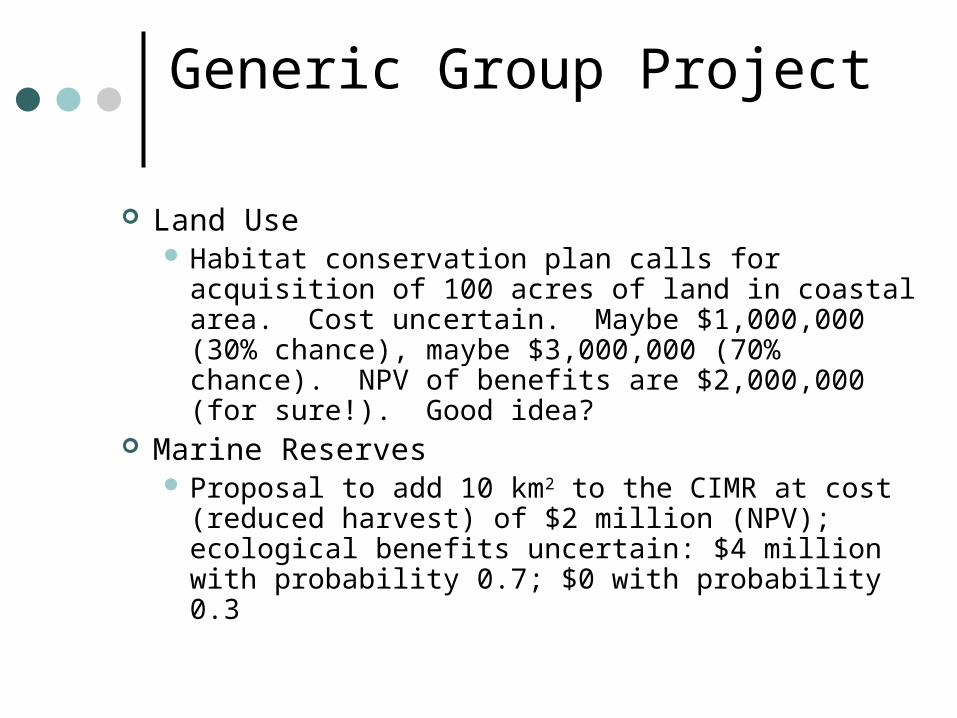

Generic Group Project

Land Use Habitat conservation plan calls for acquisition of

100 acres of land in coastal area. Cost uncertain. Maybe $1,000,000 (30% chance), maybe $3,000,000 (70% chance). NPV of benefits are $2,000,000 (for sure!). Good idea?

Marine Reserves Proposal to add 10 km2 to the CIMR at cost

(reduced harvest) of $2 million (NPV); ecological benefits uncertain: $4 million with probability 0.7; $0 with probability 0.3

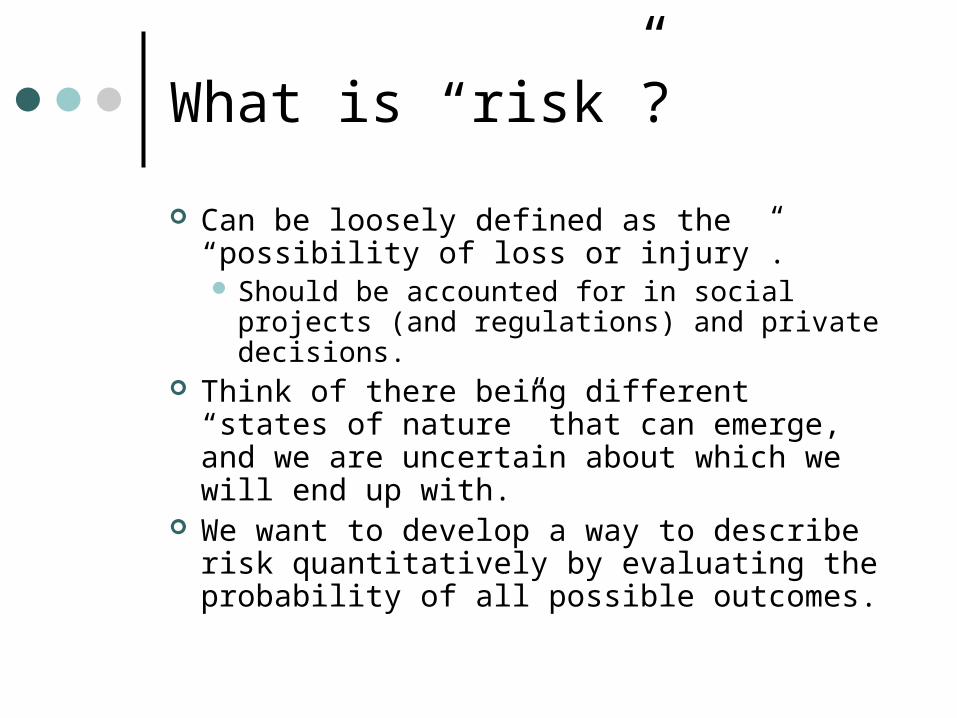

What is “risk”?

Can be loosely defined as the “possibility of loss or injury”. Should be accounted for in social projects

(and regulations) and private decisions. Think of there being different “states of

nature” that can emerge, and we are uncertain about which we will end up with.

We want to develop a way to describe risk quantitatively by evaluating the probability of all possible outcomes.

Attitude toward risk

Problem: Dean Haston likes to ride her bike to school. If it is raining when she gets up, she can take the bus. If it isn’t, she can ride, but runs the risk of it raining on the way home.

Value of riding bike (no rain) = $4 each way Value of riding bike in rain = -$4 (each way) Value of taking bus = $1 (each way)

Dean Haston’s options & the “states of nature”

The Asst. Dean can either ride her bike or take the bus.

Bus: She gains $1 each way: $2 Bike: Depends on the “state of nature”

Rain (on way home): $4 - $4 = 0.No rain: $4 + $4 = $8.

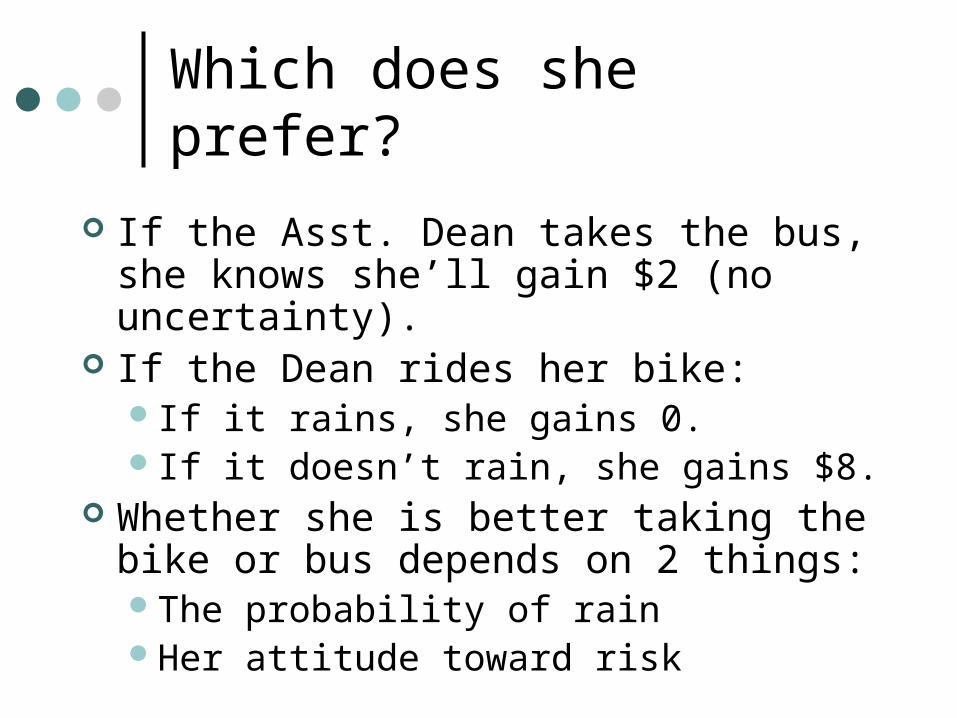

Which does she prefer?

If the Asst. Dean takes the bus, she knows she’ll gain $2 (no uncertainty).

If the Dean rides her bike:If it rains, she gains 0.If it doesn’t rain, she gains $8.

Whether she is better taking the bike or bus depends on 2 things:The probability of rainHer attitude toward risk

The probability of rain

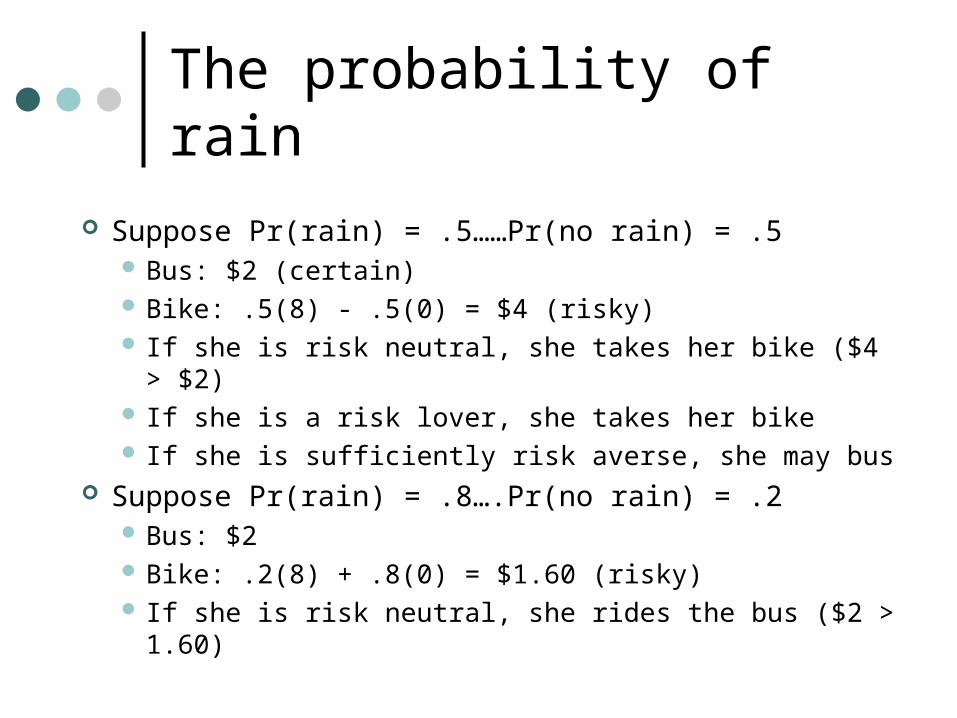

Suppose Pr(rain) = .5……Pr(no rain) = .5 Bus: $2 (certain) Bike: .5(8) - .5(0) = $4 (risky) If she is risk neutral, she takes her bike ($4 > $2) If she is a risk lover, she takes her bike If she is sufficiently risk averse, she may bus

Suppose Pr(rain) = .8….Pr(no rain) = .2 Bus: $2 Bike: .2(8) + .8(0) = $1.60 (risky) If she is risk neutral, she rides the bus ($2 > 1.60)

Risk more generallyCoin toss pays $10 or $20

Utility

Some good (or $)10 2015

Q: Would this person ratherget 15 for sure or play coin toss?

U(15)

.5*U(10)+ .5*U(20)

This person isRISK AVERSE

Risk attitudes in general

Generally speaking, most people risk averse. Diversification can reduce risk. Since gov’t can pool risk across all taxpayers, there is

an argument that society is essentially risk neutral. Most economic analyses assume risk neutrality. Note: may get unequal distribution of costs and

benefits.

Expected payoff more generally

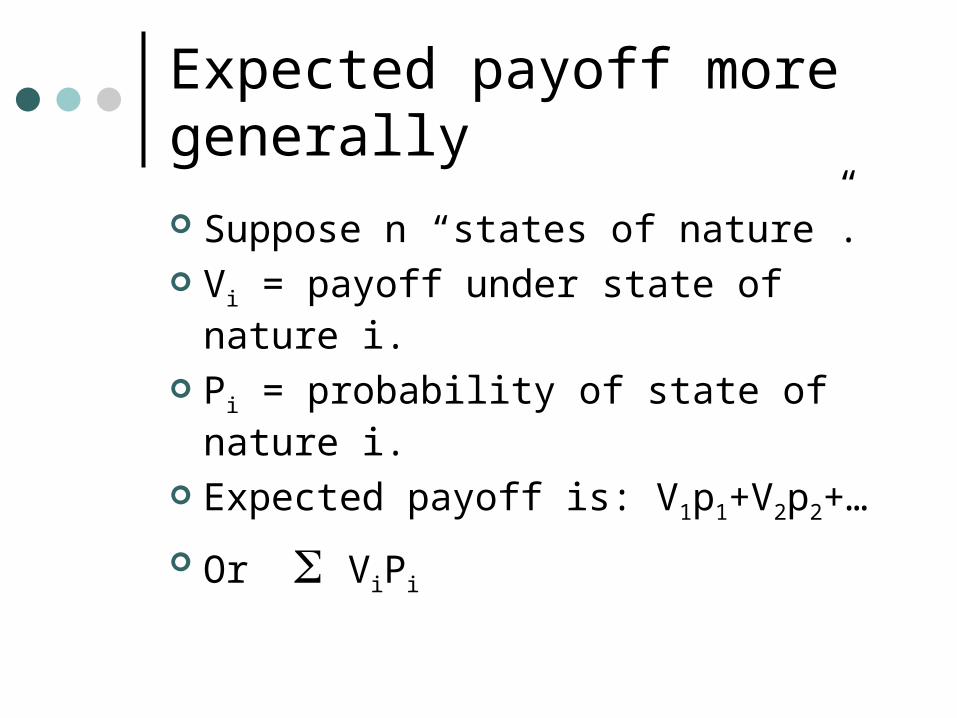

Suppose n “states of nature”. Vi = payoff under state of nature i.

Pi = probability of state of nature i.

Expected payoff is: V1p1+V2p2+…

Or ViPi

Example: Air quality regulations New air quality regulations in Santa

Barbara County will reduce ground level ozone.Reduce probability of lung cancer by .001%;

affected population: 100,000. How many fewer cases of lung cancer can

we expect?…about 1.00001*100,000 = 1.We don’t know who will get sick but this is

our expectation of the number of cases

Example: Climate change policy

2 states of natureHigh damage (probability = 1%)

• Cost = $1013/year forever, starting in 100 yrs.

Low damage (probability = 99%)• Cost = $0

Cost of control = $1011

Should we engage in control now?

Control vs. no control (r=2%)

Control now: high cost, no future lossCost = $1011

Don’t control now: no cost, maybe high future loss:If high damage = 1013[1/(1.02100) +

1/(1.02101) + 1/(1.02102) + … ] = (1013/(.02))/(1.02100) = $7 x 1013

If no damage = $0.

Overall evaluation

Expected cost if control = $1011

Expected cost if no control = (.01)(7 x 1013) + (.99)(0) = $7 x 1011

By this analysis, should control even though high loss is low probability event.

Value of Information

The real question is not: Should we engage in control or not?

The question is: Should we act now or postpone the decision until later?

So there is a value to knowing whether the high damage state of nature will occur.

We can calculate that value…this is “Value of information”

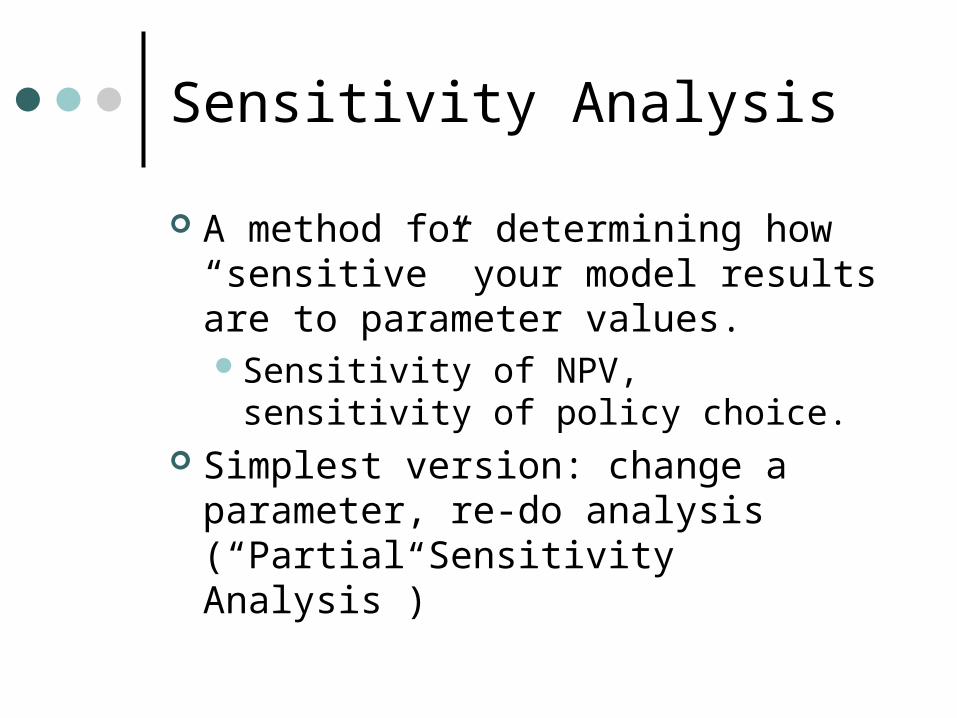

Sensitivity Analysis

A method for determining how “sensitive” your model results are to parameter values.Sensitivity of NPV, sensitivity of policy

choice. Simplest version: change a

parameter, re-do analysis (“Partial Sensitivity Analysis”)

Climate change: sensitivity to r

0

1E+11

2E+11

3E+11

4E+11

5E+11

6E+11

7E+11

8E+11

0 0.01 0.02 0.03 0.04 0.05 0.06

Discount rate (r)

Lo

ss f

rom

no

co

ntr

ol

Sensitivity to Uncertainty on the probability of high damage

0.00E+00

2.00E+11

4.00E+11

6.00E+11

8.00E+11

1.00E+12

1.20E+12

0 0.005 0.01 0.015 0.02

p

Ben

efi

ts a

nd

Co

sts

Cost

E[Damage]

More sophisticated sensitivity The more nonlinear your model, the

more interesting your sensitivity analysis.

Should examine different combinations. Monte Carlo Sensitivity Analysis:

Choose distributions for parameters. Let computer “draw” values from distn’sPlot results

Managing Risk

Risk is a problem of its own Several tools available to reduce risk

InsuranceLiability

Insurance—fire insurance example

Probability of loss: 0.001; Loss=$100,000 Expected annual loss: $100 No insurance

Most years: no loss; some years $100,000 loss 1000 houses pool $100 each/yr ($100,000/yr)

Most years—one loss Sometimes no losses, sometimes 2-3 losses Much less variability in annual losses

Fire is amenable to risk pooling Risks uncorrelated Earthquake insurance in Cal NOT amenable to risk pooling

• Most years no loss; some years enormous loss

Conditions for insurability of risks

Loss must be amenable to risk pooling There must be a clear loss Loss must be in well-defined period of time Frequency of loss must allow a premium calculation Moral hazard must not be severe (eg, hazardous

waste insurance causes folks to be sloppy) Adverse selection must not be severe (eg, only high

risk folks take out insurance)

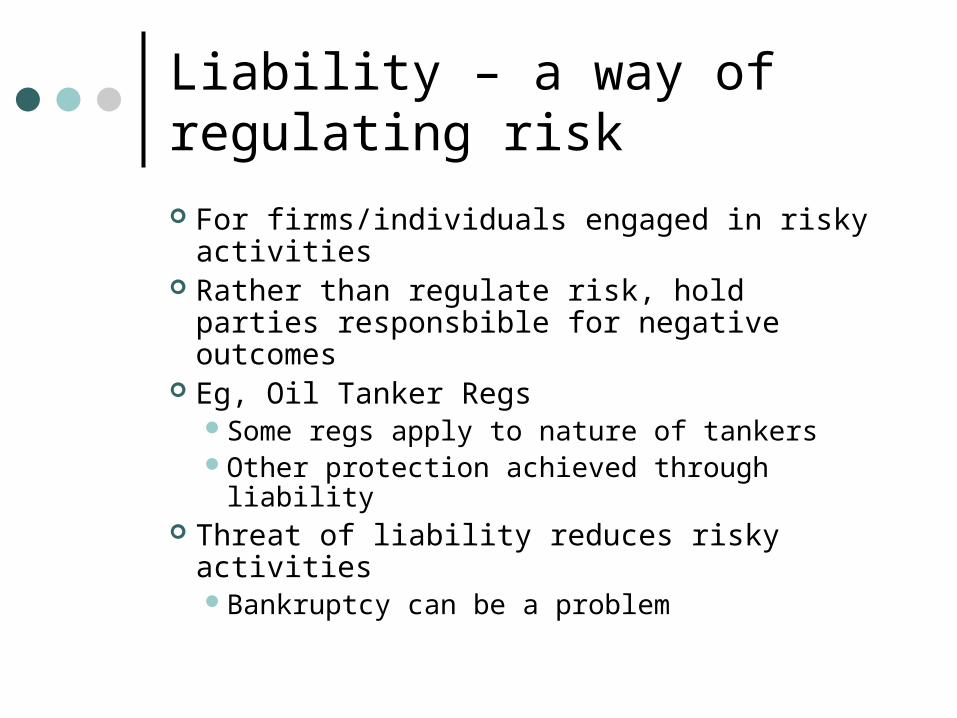

Liability – a way of regulating risk

For firms/individuals engaged in risky activities

Rather than regulate risk, hold parties responsbible for negative outcomes

Eg, Oil Tanker RegsSome regs apply to nature of tankersOther protection achieved through liability

Threat of liability reduces risky activitiesBankruptcy can be a problem