Risk Trading Unit – Natural Catastrophes in the Bond

41

1 Risk Trading Unit “Trading risk into value” Innsbruck, July 2007 Marcel Grandi Natural Catastrophes in the Bond Market - A Trader‘s View

Transcript of Risk Trading Unit – Natural Catastrophes in the Bond

1

Risk Trading Unit – Trading risk into value

Risk Trading Unit

“Trading risk into value”Innsbruck, July 2007

Marcel Grandi

Natural Catastrophes in the Bond Market- A Trader‘s View

2

Risk Trading Unit – Trading risk into value

Agenda

1. Market development and functional areas

2. Examining the needs of insurers and investors

3. Operating structures – assessing required elements

4. Case study

5. Risk trading at Munich Re

Agenda

3

Risk Trading Unit – Trading risk into value

1. Market development and functional areas

Risk Trading Unit – Trading risk into value

4

Risk Trading Unit – Trading risk into value

5,3

8,4

15,0

1,32,4

5,0

2,52,0 2,3 2,7

1,81,3

5,1

3,3

1,21,11,3 1,1 1,0

2,41,3

0123456789

1011121314151617

1997* 1998 1999 2000 2001 2002 2003 2004 2005 2006 May2007

OutstandingCat Bonds

Issued Cat Bonds in USD bn

Market development and functional areas

* and prior Source: Goldman Sachs

0

50

100

150

200

250

300

350

1999 2000 2001 2002 2003 2004 2005 2006 2007

Munich Re Group Issues

Market Development and functional areas

5

Risk Trading Unit – Trading risk into value

Hurricane U.S. Nationwide15005/07Carillon Series 2

Hurricane in East and Golf coast areaEarthquake in New Madrid area and California

18212/99Gold Eagle**

Hurricane in New York & Miami area16512/00PRIME Hurricane

Earthquake in N and S CaliforniaWindstorm in selected European Countries

13512/00PRIME CalQuake & EuroWind

Hurricane in East and Golf coast areaEarthquake in New Madrid area

12004/01Gold Eagle 2001**

Windstorm in selected European Countries11011/05Aiolos

Hurricane U.S. Nationwide8506/06Carillon Series 1

Earthquake in California19012/06Lakeside Re

Typhoon Japan8006/98Pacific Re

Covered PerilsVol.*ClosingTransaction Name

* In USD mn; **Munich Re of America, formerly American Re

Market development and functional areas

Munich Re Track Record

6

Risk Trading Unit – Trading risk into value

The cat bond market has further matured in 2005, 2006, 2007Record issuance in 2006 Large pipeline in 2007

New risks transferred to capital markets (industrial 3rd party liability, motor portfolio, trade credit, Mexico EQ, Mediterranian EQ, cat mortality) allow investors to diversify into new risk classes

Cat bond spreads widened substantially after Hurricane Katrina after tightening before Katrina

Storm resulted in first total loss, i.e. Kamp ReSpread widening in particular for critical exposure zones (e.g. US Hurricane)No detaching of capital markets from reinsurance cycleStrong differences in prices for risks with identical expected loss levelSpreads tightening again

Market development and functional areas

Market development and functional areas

7

Risk Trading Unit – Trading risk into value

Diversified investor market (cat funds, hedge funds, traditional asset managers)

Higher risk/return layers placed

Competition through „Sidecars“ (private equity)

Munich Re reentered the cat bond market

European windstorm bond (Aiolos) over EUR 110mn (USD 128mn)

Hurricane cat bond shelf program in June 2006 (Carillon)

Second series in Mai 2007 (USD 150mn, B rating)

Cat bond transaction for Zurich in December 2006 (Lakeside)

Market development and functional areas

Market development and functional areas

8

Risk Trading Unit – Trading risk into value

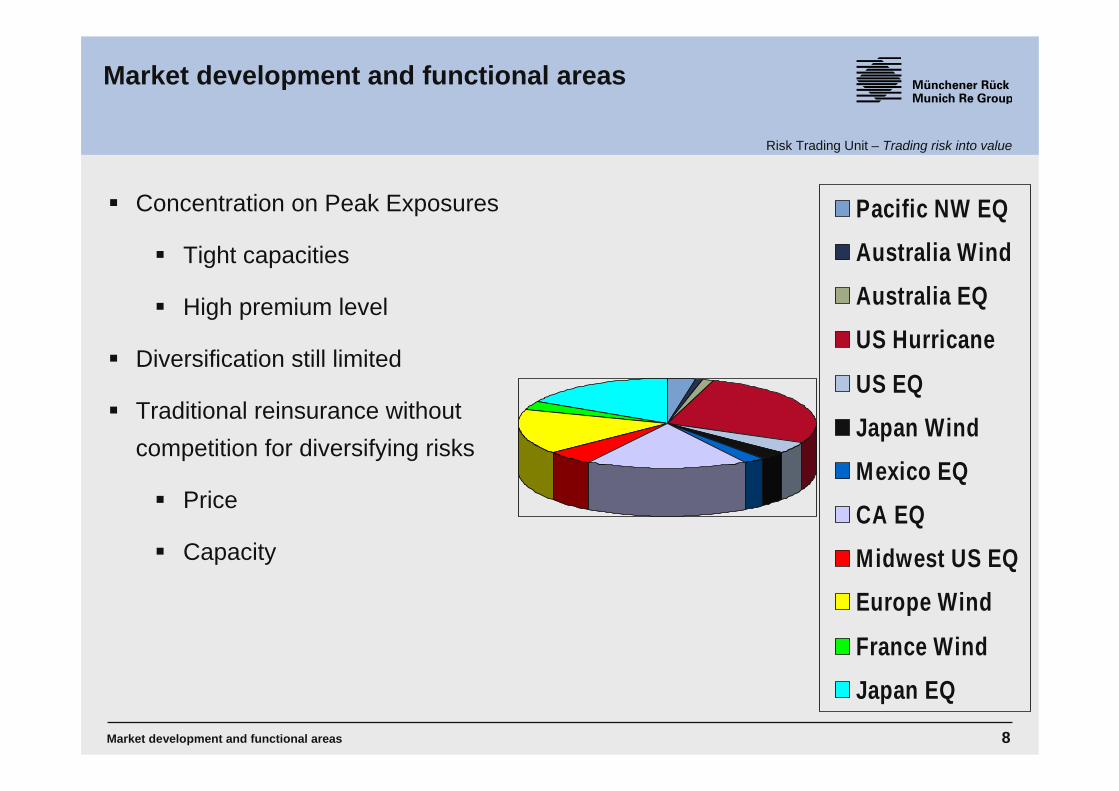

Concentration on Peak Exposures

Tight capacities

High premium level

Diversification still limited

Traditional reinsurance without competition for diversifying risks

Price

Capacity

Pacific NW EQAustralia WindAustralia EQUS HurricaneUS EQJapan WindMexico EQCA EQMidwest US EQEurope WindFrance WindJapan EQ

Market development and functional areas

Market development and functional areas

9

Risk Trading Unit – Trading risk into value

Investors’ comfort with regard to owning insurance risk will increase due to

Proven track record of past transactions

Better model availability leading to reduced asymmetric information

Sponsors’ net benefit will rise due to

Lower transaction costs per annum because of increased volumes, multi-year transactions and prevailing best practice methods; use of unissued shelf registrations which allow several takedowns

Less risk discounts demanded by investors

Decrease in basis risk as modeling capability is improved

Even without much interference from outside, the market for capital markets risk transfer solutions is likely to grow further with at least slowly increasing growth rates

Market development and functional areas

Market development and functional areas

10

Risk Trading Unit – Trading risk into value

2. Examining the needs of insurers and investors

Risk Trading Unit – Trading risk into value

11

Risk Trading Unit – Trading risk into value

Needs of insurers and investors – insurer’s view

Advantages

Capacity in tighter markets

Additional and alternative capacity

Diversification

Collateralization

Immediate liquidity

Transparency

Multi year cover

Disadvantages

Basis risk

Decreases with improvements of modelling capabilities

Transaction costs

Risk transfer costs

Tightening of prices between reinsurance and capital markets for Peak Exposures

Complexity

Dependence on investor preferences

Needs of insurers and investors – insurer’s view

12

Risk Trading Unit – Trading risk into value

Needs of insurers and investors – investor’s view

Advantages

High yield

Compared to credit markets

Track Record

One default

Uncorrelated asset class

Investment in pure insurance risks

Not possible in insurance stocks

Traded Cat Bond Spreads

0 1000 2000 3000

B

B+

BB-

BB

BB+

BBB+

Rat

ing

Spread

max min

0,23

1,6

2,7

2,8

8,5

Expected Loss

3,6

Needs of insurers and investors – insurer’s view

13

Risk Trading Unit – Trading risk into value

Needs of insurers and investors – investor’s view

Comparison of BB rated CMBS with a BB rated cat bond (Lakeside)

31.12.2003 31.12.2004 30.12.2005 29.12.20060

50100150200250300350400450500550600650

Vergleich Spread CMBS vs. ILS Produkt

Credit Spread CMBS BB Risk

Current ILS Bond Spread

Spr

ead

in B

P

Needs of insurers and investors – insurer’s view

14

Risk Trading Unit – Trading risk into value

Needs of insurers and investors – issues for investors

Liquidity

High bid/offer spreads

Secondary market write downs (after issuance)

Risk assessment

Rating and pricing based on risk modelling

Different modelling approaches of the Modelling Agencies

Modelling arbitrage

Change in modelling approach

E.g. US Hurricane

Doubling of industry losses

Downgrade of outstanding Hurricane Bonds

Needs of insurers and investors – insurer’s view

15

Risk Trading Unit – Trading risk into value

Needs of insurers and investors – conflict of interest

Investor market

Excess demand for hurricane protection first half 2006

Secondary market pricing

Write down of new issues

Change in investor appetite

Preference for one year deals

Regional covers instead of whole market

Exclusions (flood)

MR requirements

High volume

Fair price

Multi year cover

Whole market protection

No exclusions

Example US Hurricane – MR cat bond 2006 (Carillon I)

Needs of insurers and investors – insurer’s view

16

Risk Trading Unit – Trading risk into value

3. Operating structures – assessing required elements

Risk Trading Unit – Trading risk into value

17

Risk Trading Unit – Trading risk into value

Operating structures – assessing required elements

Efficient protection

Success of placement

CostsCompliance with

regulations

Operating structures – assessing required elements

18

Risk Trading Unit – Trading risk into value

Operating structures – assessing required elements

Structural considerations

Determine risk to be securitized (peak exposure)

Determine expected loss (EL) probability of securitisation

Select the EL range offering the best economics (protection vs. price)

The lower the EL, the higher the multiple to be paid as spread

The higher the EL the lower the multiple

Increasing investor appetite for higher EL ranges

Fit in overall reinsurance program

Operating structures – assessing required elements

19

Risk Trading Unit – Trading risk into value

Operating structures – assessing required elements

Selection of trigger type

Parametric (based on event generation)

Industry loss (based on damage caused)

Modelled loss (reference portfolio)

Indemnity (based on financial loss of sponsor)

Basis RiskSponsor

Modelling RiskInvestor

Parametric Modelled Loss Indemnity

Operating structures – assessing required elements

20

Risk Trading Unit – Trading risk into value

Operating structures – assessing required elements

Selection of trigger type

Indemnity trigger

Best for sponsor (no basis risk)

Availability of exposure data

Publication of exposure data

Challenging to sell to investors (moral hazard)

Synthetic trigger (parametric, modelled loss, market loss)

Wide market acceptance (clarity & transparency)

Assessment of basis risk essential

Availability of internal know how

Operating structures – assessing required elements

21

Risk Trading Unit – Trading risk into value

Operating structures – assessing required elements

Clarity on accounting and taxation

Balance sheet consolidation to be avoided

Close coordination with auditors

No financial leverage

Use reinsurer as fronter and legal sponsor

Taxation regime

No unfavourable taxation of collateral trust assets and premium cash flows (excise tax)

SPV location decisive

Double tax treaties in place

Operating structures – assessing required elements

22

Risk Trading Unit – Trading risk into value

Operating structures – assessing required elements

Selection of service providers

Modelling Agency (inc. loss verification)

Credibility of model crucial for rating and success of transaction

SPV administrator

Indenture trustee

Legal

Limited number of law firms active

Placement (one placement bank sufficient)

Beauty contest

Rating agency (one agency sufficient)

Operating structures – assessing required elements

23

Risk Trading Unit – Trading risk into value

Form of issuance

144A private placement standard „Principal at Risk“

Tranching

Currency

SPV

Off Shore (Cayman or Bermuda, Ireland)

Minimal capitalization provided by Charitable Trust

Consolidation with sponsor unlikely

Operating structures – assessing required elements

Operating structures – assessing required elements

24

Risk Trading Unit – Trading risk into value

Operating structures – assessing required elements

Project management (responsible for execution and success)

Conceptual design

Internal coordination

Internal submission

Engagement of service providers (organization of beauty contests)

Manage internal and external interfaces and service providers

Manage costs

Control time schedule

Controlling

Operating structures – assessing required elements

25

Risk Trading Unit – Trading risk into value

4. Case Study

Risk Trading Unit – Trading risk into value

26

Risk Trading Unit – Trading risk into value

Covered Territory: California Risk: EarthquakeModeling Agent: RMS

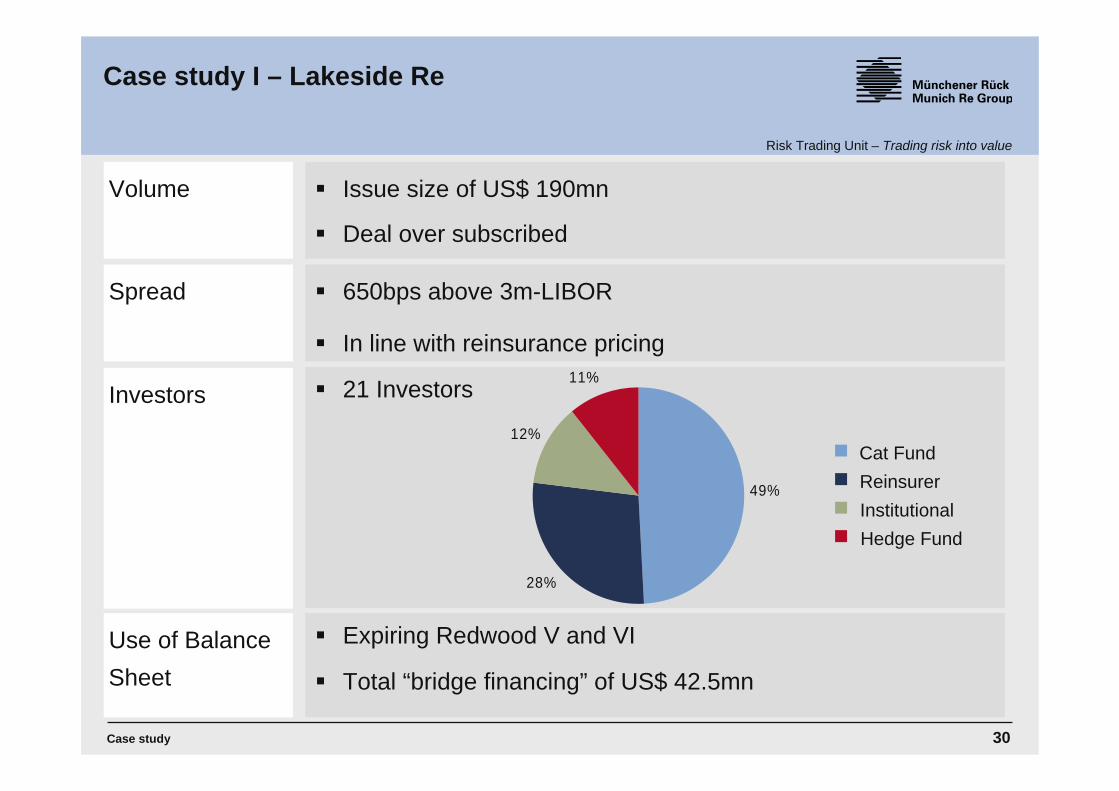

USD 190mn principal at risk bonds3-year EQ cover for Zurich AmericanDual Trigger based on PCS industry loss and Zurich ultimate net loss (UNL)Rating S&P: BB+Spread: 650bps above LIBOR

Executive summary

Case study I – Lakeside Re

Case study

27

Risk Trading Unit – Trading risk into value

Issuer Lakeside Re Ltd., a Cayman Islands exempted company licensed as a Class B insurer

Reinsurer Münchener Rückversicherungs-Gesellschaft Aktiengesellschaft (“Munich Re”)

Ceding Insurer Zurich American Insurance Company (“Zurich”), for itself and its Pool Members (“ZAIC Pool”)

Ceding Insurer Affiliates Certain branches and affiliates of the Zurich Insurance Company other than the ZAIC Pool

Securities Offered US$ 190,000,000 Principal At-Risk Variable Rate Notes

Closing Date December 20, 2006

Risk Period December 21, 2006 to December 23, 2009

Scheduled Redemption Date December 31, 2009

Triggers (i) Industry Loss threshold based on PCS Reports

(ii) Ultimate Net Loss based on actual claims

Covered Territory The United States state of California

Named Peril Earthquake

S&P Rating On the Closing Date, the Notes are expected to be rated “[BB+]”

Distribution 144A Private Placement to Qualified Institutional Buyers in Permitted Jurisdictions who, for U.S. Persons, are also Qualified Purchasers and residents of and purchasing in a Permitted U.S. Jurisdiction or a Permitted Non-U.S. Jurisdiction

Case study I – Lakeside Re

Case study

28

Risk Trading Unit – Trading risk into value

Collateral Account$ 190mn

$ 190mn Reinsurance Agreement

Outstanding Principal Amount at Redemption

$ 190mnPrincipal At-Risk Variable

Rate Noteholders

DepositBank

$ 190mn Retrocession Agreement

Premiums

$ 190,mn Bank Deposit

LIBOR - Eligible Bank Fee

$ 190mn Note Proceeds

LIBOR + 650bps

Lakeside Re Ltd.

ZurichAmerica

Munich Re

Premiums

Case study I – Lakeside Re

Case study

29

Risk Trading Unit – Trading risk into value

Estimated InsuredIndustry Losses

($ in millions)

AnnualProbability

of Exceedance

Estimated Zurich Portfolio Losses

($ in millions)91.679 0,10%84.111 0,13%73.672 0,20%64.840 0,29%61.154 0,33%58.525 0,37% Exhaustion Amount56.908 0,40%51.889 0,50%51.708 0,50% Trigger Amount45.722 0,67%40.000 0,88%37.628 1,00%32.305 1,33%25.329 2,00%14.594 4,00%

3.972 10,00%

Industry Trigger Amount

For the indemnity layer, the expected loss is 0,43%

Case study I – Lakeside Re

Case study

30

Risk Trading Unit – Trading risk into value

21 InvestorsInvestors

49%

28%

12%

11%

Volume Issue size of US$ 190mn

Deal over subscribed

Use of Balance Sheet

Expiring Redwood V and VI

Total “bridge financing” of US$ 42.5mn

Case study I – Lakeside Re

Spread 650bps above 3m-LIBOR

In line with reinsurance pricing

Cat FundReinsurerInstitutionalHedge Fund

Case study

31

Risk Trading Unit – Trading risk into value

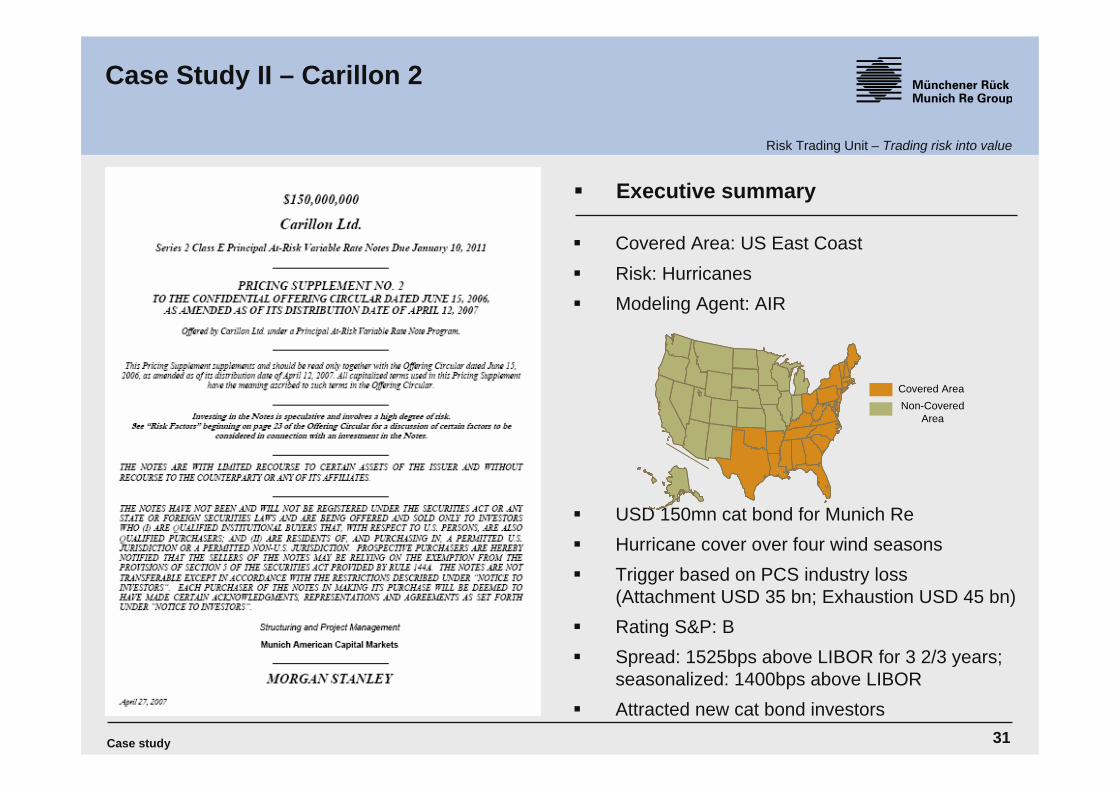

Covered Area

Covered Area: US East CoastRisk: HurricanesModeling Agent: AIR

USD 150mn cat bond for Munich ReHurricane cover over four wind seasonsTrigger based on PCS industry loss (Attachment USD 35 bn; Exhaustion USD 45 bn)Rating S&P: BSpread: 1525bps above LIBOR for 3 2/3 years; seasonalized: 1400bps above LIBORAttracted new cat bond investors

Non-Covered Area

Executive summary

Case Study II – Carillon 2

Case study

32

Risk Trading Unit – Trading risk into value

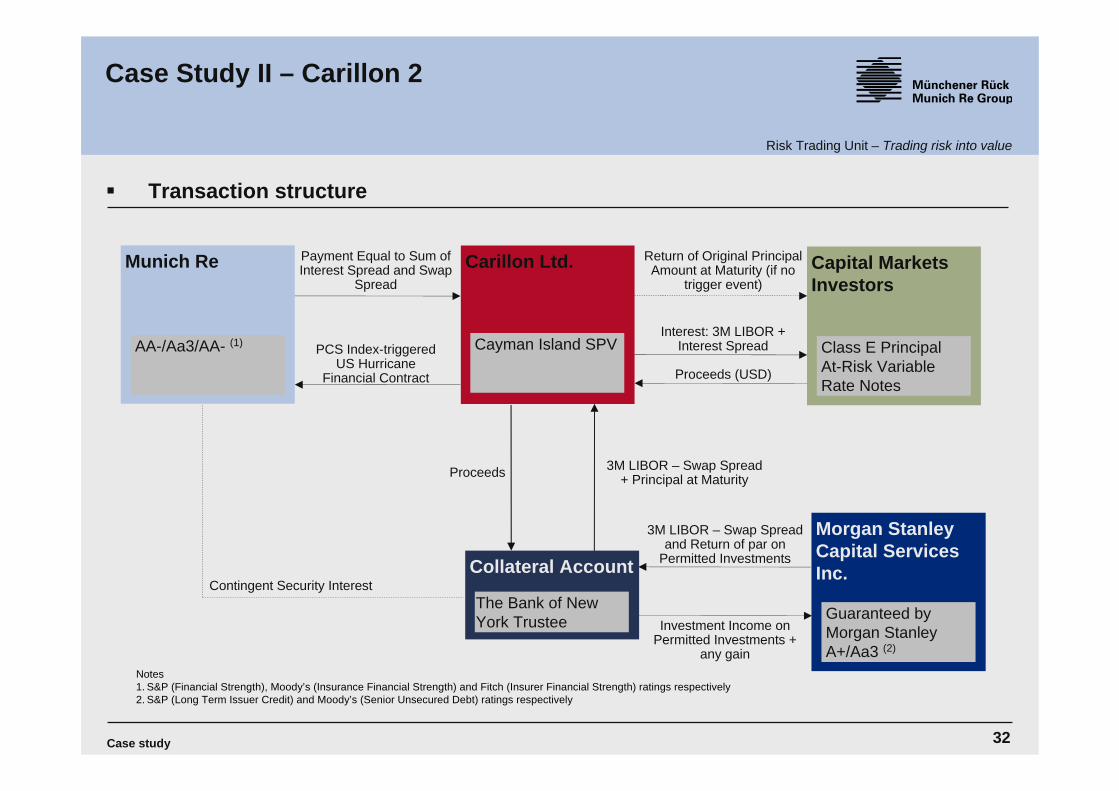

Transaction structure

Carillon Ltd. Capital Markets Investors

Morgan Stanley Capital Services Inc.

Guaranteed by Morgan StanleyA+/Aa3 (2)

Cayman Island SPV Class E Principal At-Risk Variable Rate Notes

Investment Income on Permitted Investments +

any gain

3M LIBOR – Swap Spread and Return of par on

Permitted Investments

Return of Original Principal Amount at Maturity (if no

trigger event)

Interest: 3M LIBOR +Interest Spread

Proceeds (USD)

PCS Index-triggeredUS Hurricane

Financial Contract

Payment Equal to Sum of Interest Spread and Swap

Spread

Collateral Account Contingent Security Interest

Munich Re

AA-/Aa3/AA- (1)

Proceeds 3M LIBOR – Swap Spread + Principal at Maturity

The Bank of New York Trustee

Notes1. S&P (Financial Strength), Moody’s (Insurance Financial Strength) and Fitch (Insurer Financial Strength) ratings respectively2. S&P (Long Term Issuer Credit) and Moody’s (Senior Unsecured Debt) ratings respectively

Case Study II – Carillon 2

Case study

33

Risk Trading Unit – Trading risk into value

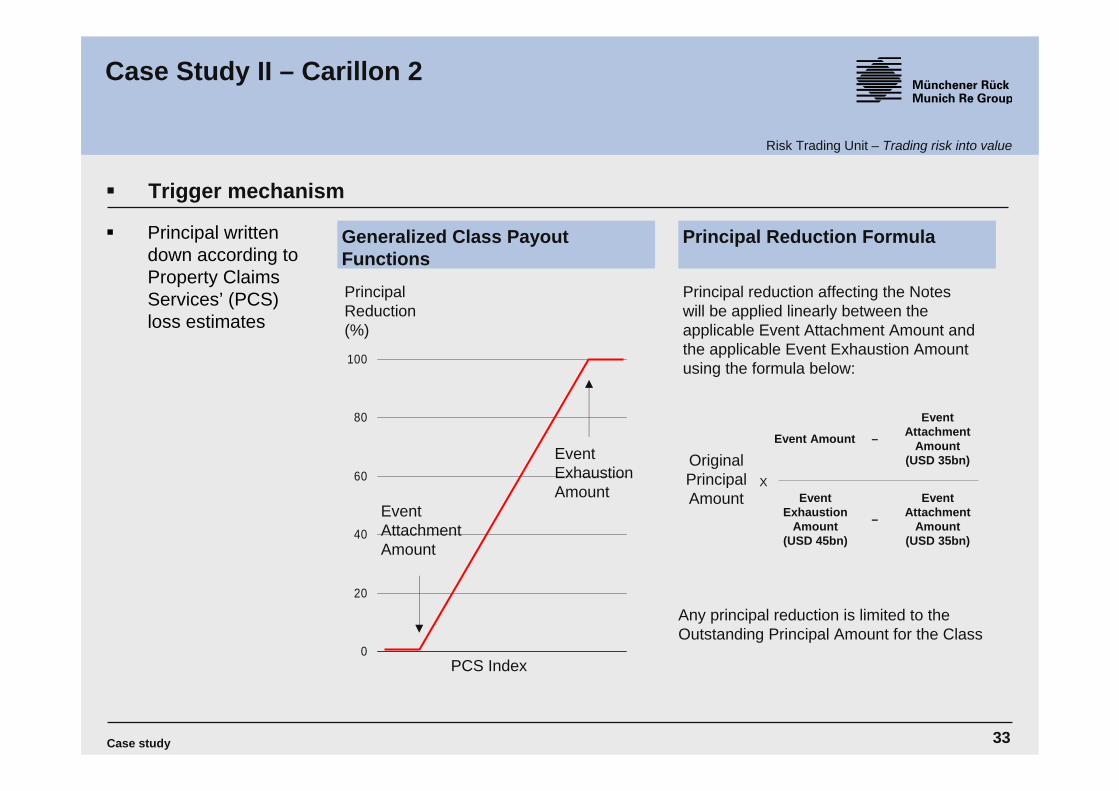

Trigger mechanism

Principal Reduction Formula

Principal reduction affecting the Notes will be applied linearly between the applicable Event Attachment Amount and the applicable Event Exhaustion Amount using the formula below:

Any principal reduction is limited to the Outstanding Principal Amount for the Class

OriginalPrincipalAmount

X

Event Attachment

Amount (USD 35bn)

Event Amount –

Event Attachment

Amount (USD 35bn)

Event Exhaustion

Amount(USD 45bn)

–

Generalized Class Payout Functions

0

20

40

60

80

100

Principal Reduction(%)

EventAttachmentAmount

EventExhaustionAmount

PCS Index

Principal written down according to Property Claims Services’ (PCS) loss estimates

Case Study II – Carillon 2

Case study

34

Risk Trading Unit – Trading risk into value

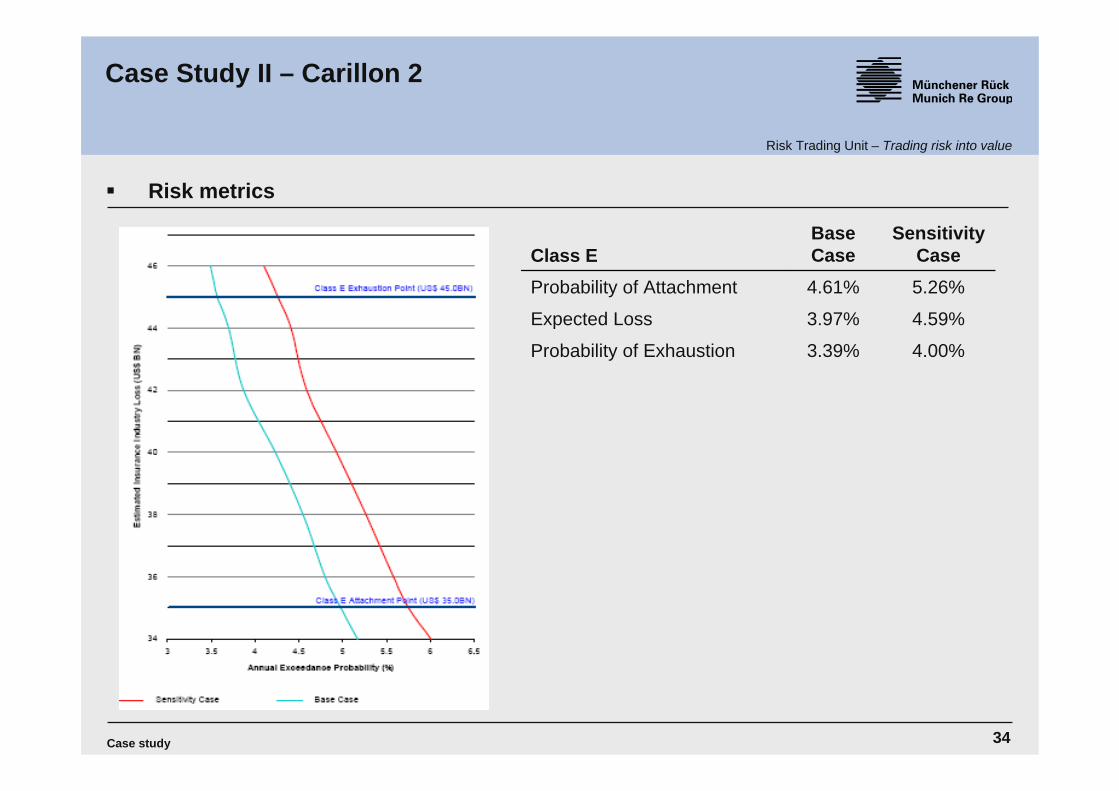

Notes1. Source: AIR Worldwide

4.00%3.39%Probability of Exhaustion

4.59%3.97%Expected Loss

5.26%4.61%Probability of Attachment

Sensitivity Case

Base CaseClass E

Case Study II – Carillon 2

Risk metrics

Case study

35

Risk Trading Unit – Trading risk into value

17 InvestorsInvestors

Volume Issue size of USD 150mn

Largest single B rated cat bond ever placed

Use of Balance Sheet Munich Re bought USD 1.5mn to round up to USD 150mn

Spread 1525 bps above 3m-LIBOR (annualized)

1400 bps seasonalized

Transaction outcome

34%

20%

12%

7%3%

24%

Hedge FundCat FundI BankReinsurer

25%

13%

11%

11%

10%

7%2%

21%

SwitzerlandCaymanBermudaGermanyU.S.U.K.CanadaOthers

Pension FundInsurer

Case Study II – Carillon 2

Case study

36

Risk Trading Unit – Trading risk into value

5. Risk trading at Munich Re

Risk Trading Unit – Trading risk into value

37

Risk Trading Unit – Trading risk into value

0

5

10

15

1997* 1998 1999 2000 2001 2002 2003 2004 2005 2006**

Outstanding Cat Bond Issued Cat Bond

Optimal moment to increase our activity in this market segmentbenefiting from a well developed infrastructure and maturing markets

Opportunities for portfolio optimization, increase of capital efficiency and additional earnings with a minimum of launching costs for MR

Attractive market conditionsAttractive market conditions

Source: Lane Financial L.L.C. 2006

* and prior; ** to date

Source: Goldman Sachs

0

1

2

3

0

1

2

3

4

5

6

7

8in bn

2001 2002 2003 2004 2005 2006

Average expected loss*(left axis in %)

Pricing “multiples“* (right axis)

*For outstanding cat bonds only

Risk Trading – Key considerations for Munich Re

Risk Trading – Key considerations for Munich Re

38

Risk Trading Unit – Trading risk into value

Retain risks

Be active player in primary and secondary market

Extension of “buy and hold” strategy

Combine and restructure risks

Sell at favourable terms and conditions

Consulting, structuring, project management and placement support

Risk fronting / transformation and (interim) capacity provider

Optimise portfolio

Use of additional capacity

Risk-based, investment and arbitrage income

Munich Re’s Risk Trading approach

Risk Trading – Active use of capital markets

Managing our own risks

Fee and arbitrage income

Improve our risk/return profile and save costs Fee and risk-based income

Managing our clients’ risks

Risk warehousing Restructuring and reselling

Risk Trading – Active use of capital markets

39

Risk Trading Unit – Trading risk into value

Dynamic market development

Doubling of market volume until 2008

Securitization market 10% of reinsurance market

Retrocession predominantly via capital markets

New investors (high net worth individuals)

New risk classes

Risk Linked Securities integral part of risk management spectrum

Outlook

Outlook

40

Risk Trading Unit – Trading risk into value

Contacts

Marcel Grandi

Senior Manager - Structuring

Phone: +49 (0)89 3891-4114

E-mail: [email protected]

Münchener Rückversicherungs-Gesellschaft

Königinstrasse 107

D-80802 München

Conatcts

41

Risk Trading Unit – Trading risk into value

Thank you for your attention!

Marcel Grandi