Risk Parity: Theory and Practice - Macquarie Group · Risk Parity: Theory and Practice Edward Qian,...

32

Risk Parity: Theory and Practice Edward Qian, PhD, CFA PanAgora Asset Management Macquarie Global Quantitative Research Conference Hong Kong September 16 – 17, 2013

Transcript of Risk Parity: Theory and Practice - Macquarie Group · Risk Parity: Theory and Practice Edward Qian,...

Risk Parity: Theory and Practice Edward Qian, PhD, CFA PanAgora Asset Management Macquarie Global Quantitative Research Conference Hong Kong September 16 – 17, 2013

1

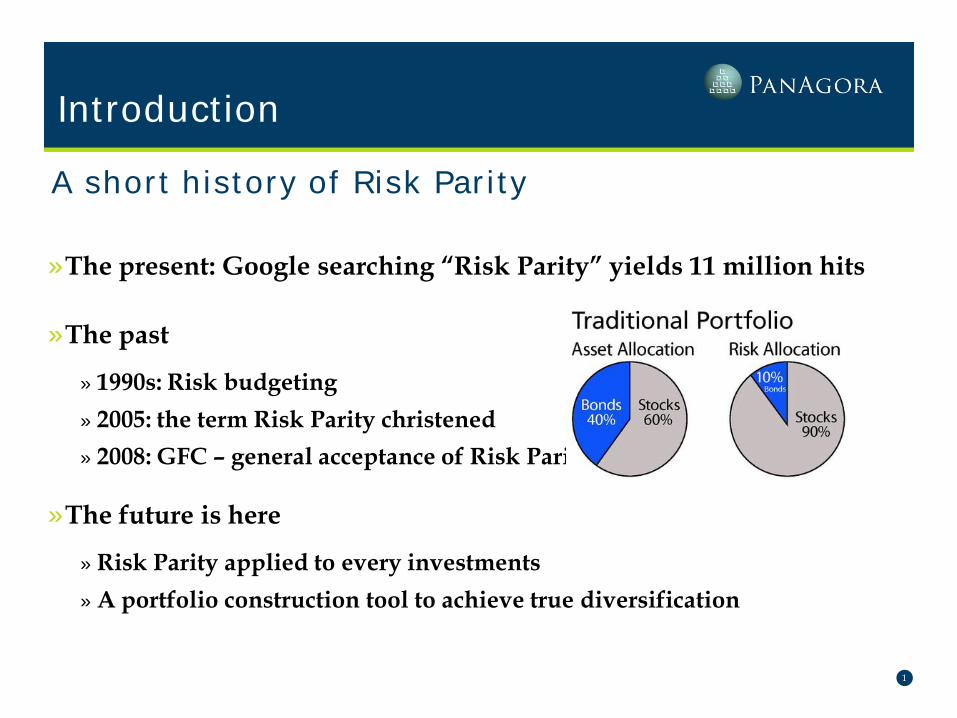

A short history of Risk Parity

»The present: Google searching “Risk Parity” yields 11 million hits

»The past

» 1990s: Risk budgeting » 2005: the term Risk Parity christened » 2008: GFC – general acceptance of Risk Parity

»The future is here

» Risk Parity applied to every investments » A portfolio construction tool to achieve true diversification

Introduction

2

Outline

»Risk Disparity: traditional portfolios and indices

»Risk Non-parity: trouble with incorrect interpretation

»Risk Parity: “smart” beta

Introduction

3

Eggs (or 95% of it) in one basket

Risk Disparity

4

Lack of diversification (asset allocation)

»Traditional “balanced” asset allocation

• Equity or equity-like assets contribute 95% of risk

Risk Disparity

60%

40% Weight

Equity Bonds 95%

5% Risk Contribution

EquityBonds

5

Risk contribution

»Assumptions: stock volatility 15%, bond volatility 5%, no correlation

»Total risk is

»Risk contributions are • Stock

• Bond

Risk Disparity

( ) ( ) %2.9%54.0%156.0 22 =×+×

( )( ) ( )

%95%54.0%156.0

%156.022

2

≈×+×

×

( )( ) ( )

%5%54.0%156.0

%54.022

2

≈×+×

×

6

Definition of risk contribution

» Marginal contribution :

» Risk contribution :

» Then

» It works both ways

» It also applies to other linear risk measures such as VaR

» Financial interpretation as loss contribution

Risk Disparity

Niwi

,,1, =∂∂σ

Niw

wi

i ,,1, =∂∂σ

%100or ,11

=∂∂

=∂∂ ∑∑

==

N

i

iiN

i ii

ww

ww σ

σ

σσ

7

Lack of diversification (equity)

»Capitalization weighted index : MSCI world Index

• Country bias in risk contribution

Risk Disparity

0%

10%

20%

30%

40%

50%

60%

US JP

G

B

FR

CA

C

H

DE

AU

ES

IT

N

L H

K

SE

FI

SG

DK

B

E N

O

GR

PT

IE

AT

N

Z

Weight

Risk Contribution

US has the highest risk contribution

8

Lack of diversification (bond)

»Capitalization weighted index: WGBI (World Government Bond)

• Country bias in risk contribution

Risk Disparity

0%

5%

10%

15%

20%

25%

30%

35%

40%

US JP

GB

DE IT

FR

ES

BE

NL

CA

GR

AT

PT

DK

IE

CH

SE

PL

FI

AU

SG

NO

Weight

Risk Contribution

Japan is the second

US has the highest risk contribution

9

Lack of diversification (commodity)

»Production weighted index: GSCI (Goldman Sachs Commodity)

• Sector bias in risk contribution

Risk Disparity

0%

10%

20%

30%

40%

50%

60%

WTI

Cru

de …

Bre

nt …

Nat

ural

Gas

Hea

ting

Oil

Gas

Oil

Cop

per

Alu

min

um

Nic

kel

Zinc

Lead

Gol

d

Silv

er

Live

Cat

tle

Feed

er C

attle

Lean

Hog

s

Whe

at …

Cor

n

Soyb

eans

Suga

r

Cot

ton

Whe

at …

Cof

fee

Coc

oa

Risk Contribution

Weight

Energy sector combined has 95% of risk

10

Lack of diversification (stock indices)

»Capitalization weighted index: S&P 500

• Stock bias risk in contribution

Risk Disparity

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

1 21 41 61 81 101 121 141 161 181 201 221 241 261 281 301 321 341 361 381 401 421 441 461 481

Sorted Stocks

Top 50 stocks contribute close to 50% of risk

Bottom 250 stocks contribute only 14% of risk

11

Lack of diversification (sector)

» Another view in terms of sector risk allocation

Risk Disparity

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Dec

-94

Dec

-95

Dec

-96

Dec

-97

Dec

-98

Dec

-99

Dec

-00

Dec

-01

Dec

-02

Dec

-03

Dec

-04

Dec

-05

Dec

-06

Dec

-07

Dec

-08

Dec

-09

Chart Title Consumer Discretionary Consumer Staples Energy Financials Health Care Industrials Materials Technology Telecom Utilities

Tech Bubble

Credit Bubble

Ris

k C

ontr

ibut

ion

12

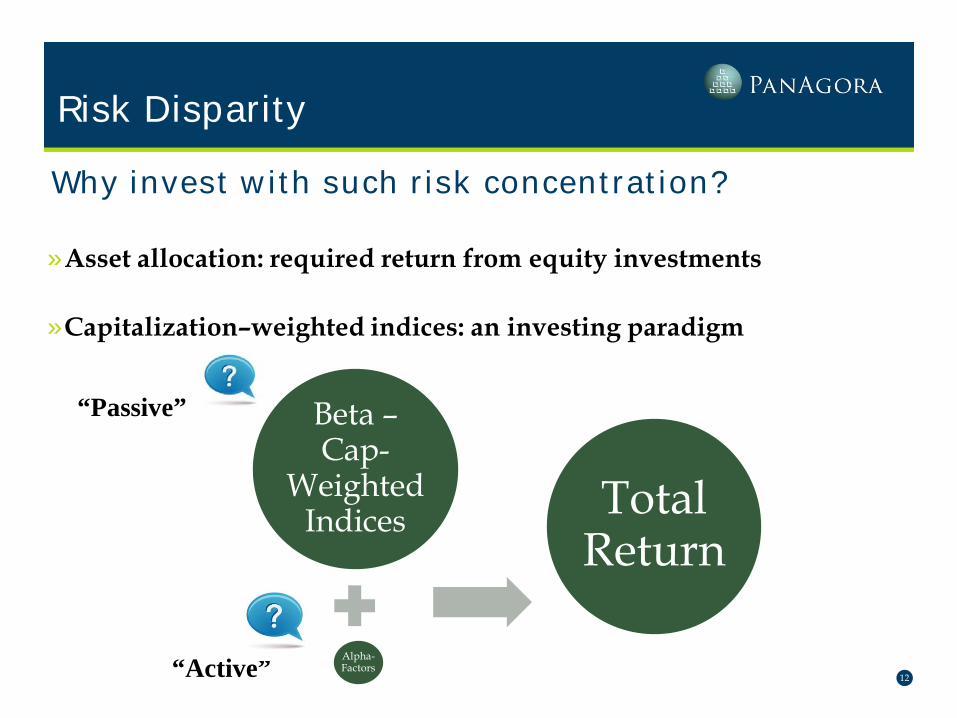

Why invest with such risk concentration?

»Asset allocation: required return from equity investments

»Capitalization–weighted indices: an investing paradigm

Risk Disparity

Beta – Cap-

Weighted Indices

Alpha- Factors

Total Return

“Passive”

“Active”

13

The painful consequences

»Unintended risk concentrations in asset/country/sector/stock

»Volatile returns, sensitivity to macro environment, low Sharpe

ratios

»The reason why hedge funds look attractive!

Risk Disparity

14

Not all Risk Parity are created equal.

Risk Non-parity

Injury risk, parity could prevent Chip Kelly's schemes from succeeding in NFL

15

Equal risk contribution

»Assumptions: stock volatility 15%, bond volatility 5%

»Then equal risk contribution portfolio is 25%/75% in stock/bond

»Risk contributions are • Stock

• Bond

Risk Non-parity

( )( ) ( )

%50%575.0%1525.0

%1525.022

2

=×+×

×

( )( ) ( )

%50%575.0%1525.0

%575.022

2

=×+×

×

60/40

25/75 Risk Parity

Risk Parity Line

Levered Risk Parity

1%

2%

3%

4%

5%

6%

7%

8%

0% 5% 10% 15% 20%

Retu

rn

Risk

Risk Parity Line and Traditional Frontier

16

Equal risk allocation is not necessarily Risk Parity

»Asset class 1/n leads to Risk Non-parity

»Asset category 1/n leads to Risk Non-parity

» 4 equity asset classes plus High Yield, EM Debt, Corporate Bonds, Government Bonds

»The fallacy of 1/n

Risk Non-parity

17

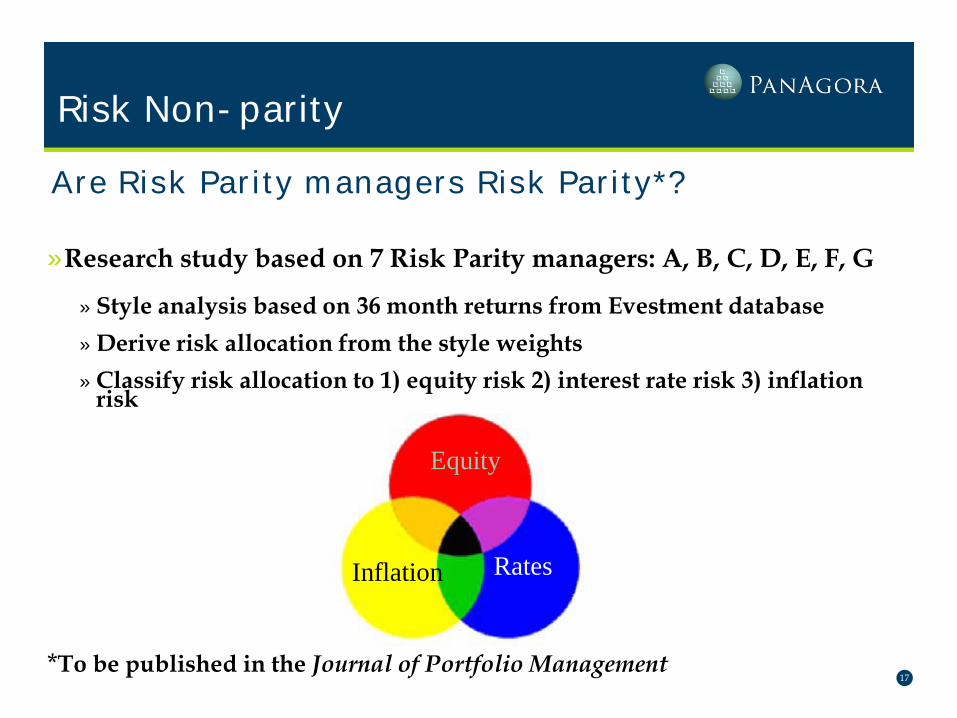

Are Risk Parity managers Risk Parity*?

»Research study based on 7 Risk Parity managers: A, B, C, D, E, F, G

» Style analysis based on 36 month returns from Evestment database » Derive risk allocation from the style weights » Classify risk allocation to 1) equity risk 2) interest rate risk 3) inflation

risk

*To be published in the Journal of Portfolio Management

Risk Non-parity

Equity

Rates Inflation

18

Why three risk premia?

»The short answer: only these three are “independent”

»The long answer

» Asset allocation portfolios are exposed to growth risk and inflation risk » To hedge growth risk, balance risk allocation to equity and interest rate

» To hedge inflation risk, balance risk allocation to nominal assets (equity & interest rate) and real assets (inflation linked bonds & commodities)

»Hybrid asset classes (HY, EMD, Credit, TIPS) are mostly

combinations of the three primary risk premia

Risk Non-parity

19

The three risk premia

Risk Non-parity

Equity

Rates Inflation

Credit/EMD/HY

ILB

MAT/ENE

20

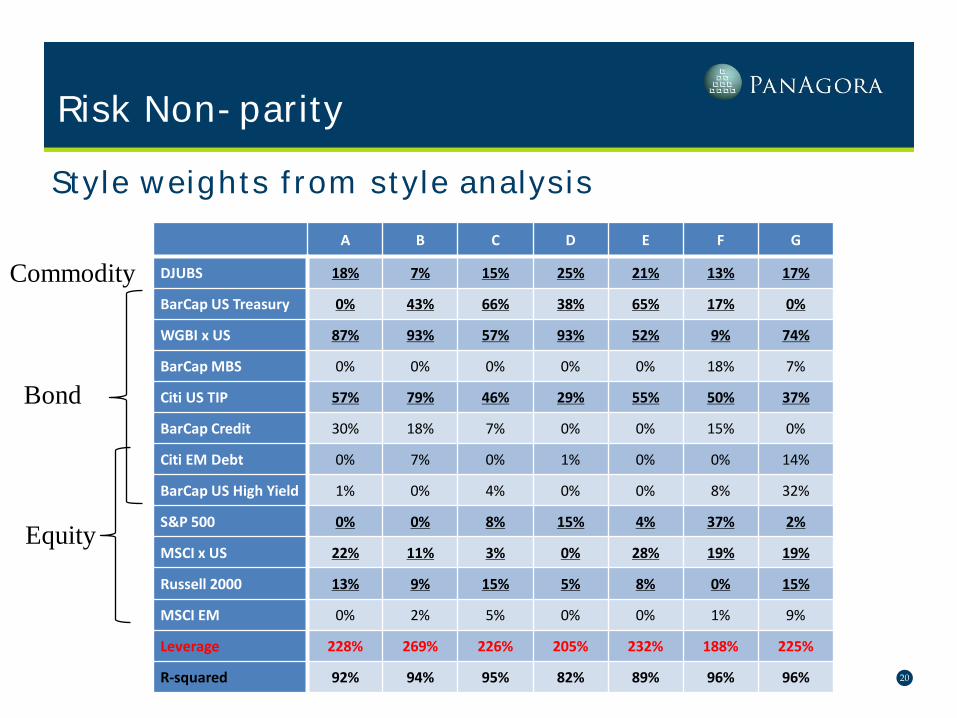

Style weights from style analysis

Risk Non-parity

A B C D E F G

DJUBS 18% 7% 15% 25% 21% 13% 17%

BarCap US Treasury 0% 43% 66% 38% 65% 17% 0%

WGBI x US 87% 93% 57% 93% 52% 9% 74%

BarCap MBS 0% 0% 0% 0% 0% 18% 7%

Citi US TIP 57% 79% 46% 29% 55% 50% 37%

BarCap Credit 30% 18% 7% 0% 0% 15% 0%

Citi EM Debt 0% 7% 0% 1% 0% 0% 14%

BarCap US High Yield 1% 0% 4% 0% 0% 8% 32%

S&P 500 0% 0% 8% 15% 4% 37% 2%

MSCI x US 22% 11% 3% 0% 28% 19% 19%

Russell 2000 13% 9% 15% 5% 8% 0% 15%

MSCI EM 0% 2% 5% 0% 0% 1% 9%

Leverage 228% 269% 226% 205% 232% 188% 225%

R-squared 92% 94% 95% 82% 89% 96% 96%

Bond

Equity

Commodity

21

All look Risk Parity?

Risk Non-parity

A B C D E F G

Commodities 18% 7% 15% 25% 21% 13% 17%

Bonds 174% 239% 180% 161% 172% 118% 163%

Equities 35% 22% 31% 20% 39% 58% 45%

Leverage 228% 269% 226% 205% 232% 188% 225%

R-squared 92% 94% 95% 82% 89% 96% 96%

22

Risk allocation from style analysis – surprise!

Risk Non-parity

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

A B C D E F G

Equity

Interest Rate

Inflation

23

Risk allocation to risk on risk off

Risk Non-parity

A B C D E F G

Risk on (E & C) 67% 33% 60% 64% 66% 86% 93%

Risk off (Rate) 33% 67% 40% 36% 34% 14% 7%

24

Why some managers are not risk parity?

»High notional allocation to bonds and portfolio leverage do not

equate to Risk Parity

»Equal risk allocation is not Risk Parity

»Oversized strategic bets to either equity or interest rate are not

Risk Parity

Risk Non-parity

25

It is very hard to know who is “smart” in investing.

Risk Parity as “Smart” Beta

26

“Smart” or not?

»“Smart” beta

» Minimum variance » Maximum diversification » Equal weight » Risk Parity

»Not so “smart” beta

» Capitalization weighted indices

Risk Parity as “Smart” Beta

27

Why are cap-weighted indices not “smart”?

»Indices are from research of very smart people

»Implied returns of S&P 500 index seem to be “smart”

Risk Parity as “Smart” Beta

Weight

Exp. Return

Volatility

Sharpe Ratio CSD 10.7% 7.7% 26.5% 0.29

CSS 11.3% 4.7% 17.1% 0.27

ENG 12.4% 7.5% 28.0% 0.27

FIN 14.2% 9.5% 33.0% 0.29

HEA 11.8% 4.9% 18.2% 0.27

IND 10.5% 8.2% 27.6% 0.30

MAT 3.6% 8.9% 31.0% 0.29 TEC 18.6% 7.0% 24.4% 0.29

TEL 3.1% 5.1% 20.9% 0.24 UTL 3.7% 4.2% 18.3% 0.23

wΣλµ =

µλ Σ

−= 11w

28

All “smart” betas seem somewhat “naïve”

Risk Parity as “Smart” Beta

0%

2%

4%

6%

8%

10%

12%

1 2 3 4 5 6 7 8 9 10

Wei

ght

Security

Equally Weighted

0%

2%

4%

6%

8%

10%

12%

1 2 3 4 5 6 7 8 9 10

Expe

cted

Ret

urn

Security

Minimum Variance

0%

2%

4%

6%

8%

10%

12%

1 2 3 4 5 6 7 8 9 10

Shar

pe R

atio

Security

"Maximum Diversification"

0%

2%

4%

6%

8%

10%

12%

1 2 3 4 5 6 7 8 9 10

Risk

Allo

catio

n

Security

Risk Parity

29

The value of not knowing

Risk Parity as “Smart” Beta

0.5

1

2

4

8

Dec-9

4

Dec-9

5

Dec-9

6

Dec-9

7

Dec-9

8

Dec-9

9

Dec-0

0

Dec-0

1

Dec-0

2

Dec-0

3

Dec-0

4

Dec-0

5

Dec-0

6

Dec-0

7

Dec-0

8

Dec-0

9

Dec-1

0

Dec-1

1

Dec-1

2

RP CW

EW MV

MD

RP CW EW MV MDExcess Return 7.4% 3.7% 4.6% 3.6% 4.7%Risk 14.5% 15.8% 17.3% 10.6% 11.7%Sharpe Ratio 0.51 0.23 0.27 0.34 0.40

30

Risk Parity everywhere

» Multi Asset portfolio allocation

» Equity investments » Global/US/International/EM/Sector

» Fixed income investments » Government/Credit/Inflation-linked/High Yield

» Commodities

» Factor premia

Risk Parity as “Smart” Beta

31

Conclusion

Risk Parity

» Risk Parity provides a tool to build diversified portfolios with

fundamental intuition

» Diversification works but conventional investment approach

lacks diversification (Risk Disparity)

» Risk Parity is subject to wrong interpretation (Risk Non-parity)

» Risk Parity beta as “smart” beta from top-down to bottom-up