Risk assessment software

48

Implementing MYOB ProfitOptimiser in your Practice

-

Upload

richard-wood -

Category

Documents

-

view

725 -

download

0

description

Transcript of Risk assessment software

Implementing MYOB ProfitOptimiser in your Practice

Richard J. Wood

MyCorporateDoctor.com.au

Introducing your trainer…

Today’s Aim:

“To implement MYOB ProfitOptimiser in your practice, deliver value add services

to your clients and form strong partnerships”

Aims and Objectives

Aim

• MYOB ProfitOptimiser will become the foundation of effective communication between accountants, their customers and the Banks – it is imperative that you are competent and confident in its use as a partnership tool

Objectives

• Deliver a robust framework around undertaking various financial analyses using MYOB ProfitOptimiser and develop this into a basis for strategic dialogue for customer discussion - communicating outcomes in a confident and coherent manner

• Prepare you for the type of questions that you might expect to field in the use of MYOB ProfitOptimiser with customers and Banks

• Develop a customer presentation using a ‘live file’ which can be used with the customer

A. Welcome and Introduction to Value Added Services

B. Review of the Key MYOB ProfitOptimiser features, functions and benefits

C. Using MYOB ProfitOptimiser in an accounting firm - How to identify key MYOB ProfitOptimiser clients

- How to explain MYOB ProfitOptimiser outcomes to clients in terms that they can understand

D. The MYOB ProfitOptimiser consultation process

E. Using MYOB ProfitOptimiser in the Banking sector

F. Your Customer - A case study and presentation

Gaining confidence with Dialogue

Agenda

Building a better understanding of our clients

Expected Outcomes

• Employ a standard tool for financial analysis, interpretation and discussion across broad customer types

• Obtain higher levels of confidence through customer communication

• Understand and ensure the most efficient use of the Customer Dialogue process

• Produce a higher quality, differentiated Customer Value Proposition

• Enhancement of partnership between the Customer and their Bank

• Establish your Practice as “a real alternative in our chosen markets”

Introduction to Value Added Services

Profit margins are shrinking on Accounting and taxation work

Many Accountants are repositioning themselves by offering more profitable value added services like:

Strategic Planning Business Valuations Bank Submissions Working Capital Management Cash Flow Analysis

COMPLIANCE vs VALUE ADD

The Dilemma

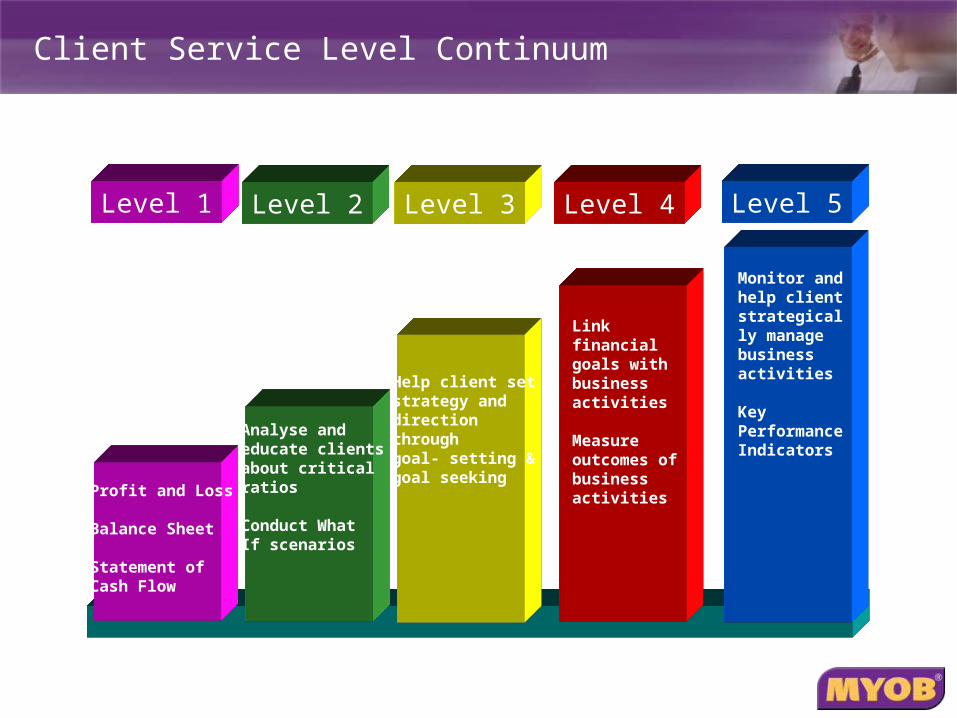

Level 5Level 4Level 3Level 2Level 1

Profit and Loss

Balance Sheet

Statement of Cash Flow

Analyse and educate clientsabout criticalratios

Conduct What If scenarios

Help client setstrategy and direction throughgoal- setting &goal seeking

Link financial goals with business activities

Measure outcomes of business activities

Monitor and help client strategically manage business activities

Key Performance Indicators

Client Service Level Continuum

Level 5Level 4Level 3Level 2Level 1

COMPLIANCE

RELIANCE

Technical Foundation

ThoroughAnalysis

FutureFocus

Link to Performance

ContinuousImprovement

Collect Data Organise & Inform Analysis & Knowledge Applied Wisdom

Move from Compliance to Reliance

Using MYOB ProfitOptimiser

in an Accounting Firm

Collecting

Recording

Summarising

Analysing

Stages of Accounting

KEY ISSUESDrivers :• Price• Volume• Days Receivable• Days Inventory• Days Payable

• Impacts on cash flow

• Low margin businesses are more likely to be under stress

• Working Capital % must be less than the Gross Margin %

• $37.20 of Working Capital is absorbed from each additional $100 of Sales

STRESS TESTING ACTIONS• Goal seek : Gross Margin %• Sensitivity Analysis : 1% Change drivers

Cash flow on incremental sales will decline as the

working capital % approaches the gross margin %

When Goal seeking solve by sensitivity. With sensitivity analysis review changes and undo before

changing the next driver

Working Capital %

KEY ISSUESDrivers :• Price• COGS

• Operating measure before overheads

• Before interest & tax

• Return on Sales before overheads, interest & tax

• $30 of gross operating profit is made per $100 of Sales

STRESS TESTING ACTIONS• Goal seek : 1% change in Gross margin %• Sensitivity Analysis : 1% Change drivers

Businesses with a low Gross Margin % are driven

by price rather than volume

When Goal seeking solve by sensitivity. With sensitivity analysis review changes and undo before

changing the next driver

Gross Margin %

KEY ISSUESDrivers :• Price• COGS• Overheads

• (Volume is a driver when some• Overheads are fixed)

• Operating measure

• Before interest & tax

• Net Operating Return on Sales

• $4.72 of operating profit is made per $100 of Sales

STRESS TESTING ACTIONS• Goal seek : 1% change in Net Profitability• Sensitivity Analysis : 1% Change drivers

Operating profit should bemeasured before interest.Interest is a financing cost,

not an operating cost.

When Goal seeking solve by sensitivity. With sensitivity analysis review changes and undo before

changing the next driver

Net Profitability

KEY ISSUESDrivers :• Price• Volume• COGS• Overheads• Other• Interest

• EBIT capability to service interest

• For every $1 of interest, there is $2.71 of EBIT to pay it

STRESS TESTING ACTIONS• Goal seek : The required lending covenant • Sensitivity Analysis : 1% Change drivers

The appropriate interest cover will depend on an

assessment of the business risks of the

customer

When Goal seeking solve by sensitivity. With sensitivity analysis review changes and undo before

changing the next driver

Interest Cover EBIT – Key Covenant Ratio

KEY ISSUESDrivers :• Days Receivable• Days Inventory• Days Payable

• For every $1 of Current Liabilities there is $2.19 of Current Assets to pay them

• The current ratio should reflect an appropriate relationship between all three of the drivers

STRESS TESTING ACTIONS• Goal seek : Rule of thumb - two times• Sensitivity Analysis : 1% Change drivers

The Current Ratio covenant has been set for your business by taking the following factors into

account…

When Goal seeking solve by sensitivity. With sensitivity analysis review changes and undo before

changing the next driver

Current Ratio

KEY ISSUESDrivers :• Price• Volume• Days Receivable• Days Inventory• Days Payable• Plant, Prop & Equip• Investments

• Impacts on liquidity

• Mix of Operating Working Capital and Non-Current Assets is important

• Capital Turnover

• $1.37 of Sales per $100 of Capital invested

STRESS TESTING ACTIONS• Goal seek : Activity of 1.0 to commence analysis• Sensitivity Analysis : Change drivers

Normally, manufacturers have a low activity ratio compared to

retailers. What type of business does the customer

have ?

When Goal seeking solve by sensitivity. With sensitivity analysis review changes and undo before

changing the next driver

Activity

KEY ISSUESDrivers :• Creditor days• Other current• Liabilities• Long Term Liabilities• Equity

STRESS TESTING ACTIONS• Goal seek : to 1.5• Sensitivity Analysis : Change drivers

How much total liabilities a business has for every dollar

of equity

When Goal seeking solve by sensitivity. With sensitivity analysis review changes and undo before

changing the next driver

Total Liability/Equity

KEY ISSUESDrivers :• Days Receivable• Days inventory• Equity• Non current assets

STRESS TESTING ACTIONS• Goal seek : For example - 70%• Sensitivity Analysis : Change drivers

How much total equity has the owner got if his assets as

opposed to outside funding or creditors. Usually a low figure

indicates that an owner is not in control of his own assets..

Also called Capital AdequacyWhen Goal seeking solve by sensitivity. With sensitivity analysis review changes and undo before

changing the next driver

Equity to Total Assets

KEY ISSUESDrivers :• Change in Net Assets• Change in Equity

A simple method for calculating the net cash flow movement for the period under review

STRESS TESTING ACTIONS• Goal seek : A positive Cash Flow or Zero• Sensitivity Analysis : Not applicable

Cash flow is calculated as the movement on the net change

in debt for the period

When Goal seeking solve by sensitivity. With sensitivity analysis review changes and undo before

changing the next driver

Cash Flow

KEY ISSUESDrivers :• Interest expense• Short/long term debt• Short/long term equity

STRESS TESTING ACTIONS• Goal seek : For example 2• Sensitivity Analysis : 1% Change drivers

Measure relationship between the borrowed funds and the

investment in the business by the owner

When Goal seeking solve by sensitivity. With sensitivity analysis review changes and undo before

changing the next driver

Debt to Equity

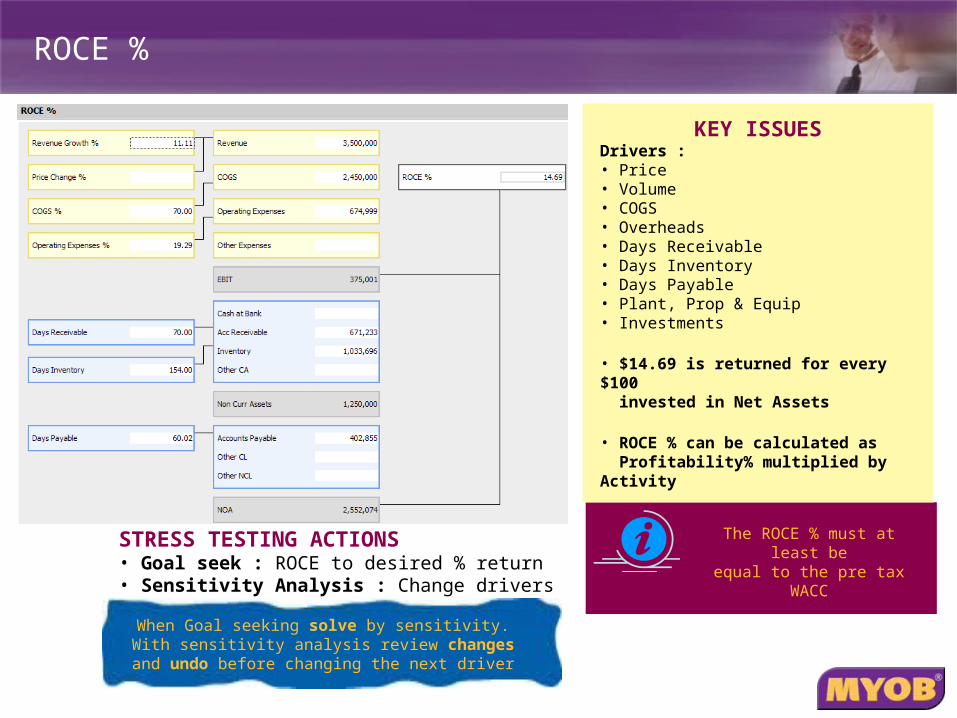

KEY ISSUESDrivers :• Price• Volume• COGS• Overheads• Days Receivable• Days Inventory• Days Payable• Plant, Prop & Equip• Investments

• $14.69 is returned for every $100 invested in Net Assets

• ROCE % can be calculated as Profitability% multiplied by Activity

STRESS TESTING ACTIONS• Goal seek : ROCE to desired % return• Sensitivity Analysis : Change drivers

The ROCE % must at least beequal to the pre tax WACC

When Goal seeking solve by sensitivity. With sensitivity analysis review changes and undo before

changing the next driver

ROCE %

KEY ISSUESDrivers :• Price• Volume• COGS• Overheads• Days Receivable• Days Inventory• Days Payable

• Cash Flow at an EBIT level

• Cash flow before any tax or interest expense or hard core debt repayment dividends and Capital expenditure

STRESS TESTING ACTIONS• Goal seek : Cash After Operations to at least meet tax, interest and dividend obligations• Sensitivity Analysis : Change drivers

Should at least be positive to be able to meet interest, tax

and dividend liabilities

When Goal seeking solve by sensitivity. With sensitivity analysis review changes and undo before

changing the next driver

Cash After Operations

The MYOB ProfitOptimiser Consultation Process

How Accountants can use MYOB ProfitOptimiser

• As a Bureau Service for clients to improve their financial performance and assist with finance applications.

• By annualising and projecting financial data to the end of a specific reporting period (3,6 or 12 months).

• The 3 key financial drivers are then interpreted and analysed:

• Profitability

• Cash Flow

• Financial Growth

How Accountants can use MYOB ProfitOptimiser

• By working with clients to devise ‘What If’ scenarios to improve financial performance.

• Goal Seeking is then performed to visualise future improvements.

• Projections are then completed for future periods.

• Anticipated profit and tax position is then assessed and profit and tax management initiatives are suggested.

• The agreed performance measures are then documented for the client.

• A follow up consultation is then arranged.

The Ideal Consultation – Part A

• Explain Loading screen

• Explain Strategy screen (6 items max)

• Display screen based pre analysis reports

• Variance report

• Working Capital Report

• Cash Wastage report

The Ideal Consultation – Part B

• Perform What-If Analysis (2-3)

• Undertake Goal Seeking (1 only)

• Project budget for next period (roll forward)

• Display screen based post analysis reports

• Variance report

• Working Capital Report

• Cash Wastage report

The Ideal Consultation – Part C

• Provide Financial Diagnostic Report pre improvements

• Organise next consultation with the intention of quarterly meetings

• Post Financial Diagnostic Report (post improvements) within one week

The customer’s ability to service the loan

• Today’s debt is repaid from tomorrows cash flow – assumptions? (Capacity to service)• Cash Flow Quality• The need for debt and how it arises• Fast growth symptoms and consequences

• Working capital per $100 of sales

• Cash flow/changing debt

• Net cash income short term after debt obligation

• Interest cover EBIT

• Cash after operations

Dialogue Opportunity

Identify Strengths and Manage Issues

Identify issues, communicating the issues with the customer and working with the customer to

minimise/mitigate those issues.

• Early warning indicators of credit deterioration – list…• Positive recognition of customers strong or improved

performance• Profitability• Cash Flow & Funding• Working Capital management• Non Current Assets

• Covenants and feedback procedures• Stress testing assumptions

• Liabilities/Equities• Equities/Assets

• Goal seeking

• ROCE%

• Interest Cover EBIT

• Net Profitability %

Dialogue Opportunity

Identify Strengths and Manage Issues

Using covenants as a risk control mechanism

• Covenants should be used as early warning indicators for a review of risk

• “Trigger to dig deeper”• If breeched use MYOB ProfitOptimiser to sensitize

and understand “why”• What are the options to redress the breach?

• Covenants should be set at a level that will facilitate early detection of risk

• Use MYOB ProfitOptimiser to sensitize and stress test the business to assist in setting covenants at appropriate levels• Share with customers the reasons why covenants are

set at a particular level• Use MYOB ProfitOptimiser to model the risks that the

business may face if the covenants are breeched

Dialogue Opportunity

Identify Strengths and Manage Issues

Short Term Liquidity

• Working Capital Management• The impact of fast growth• The drivers of operating working capital investment• Focus on Lead indicators

• Cash Wastage

• Working Capital

• Separate Finance from operations

• Goal seeking

• Current Ratio

Dialogue Opportunity

Identify Strengths and Manage Issues

Long Term Solvency

• The Balance Sheet structure• Valuing the Net Assets• Cause and effect - a strategic approach• Focus on Lead Lag indicators

• ROCE%

• Valuation

• Total Liabilities/Equity

• Goal seeking

• Equity/Total Assets

Dialogue Opportunity

Identify Strengths and Manage Issues

A Quick Business Diagnosis

• Is the Gross Margin % equal to or greater than that of similar businesses?• Is the Net Profitability % equal to or greater than that of similar

businesses? • Is the Gross Margin % greater than the Working Capital %• Equity of total assets • Is the Interest Cover ratio within normal covenant levels or

industry benchmarks

• Drivers of ROCE%

• Equity/Total Assets• Sensitivity analysis

• Interest Cover

Dialogue Opportunity

Identify Strengths and Manage Issues

Successful customer = Successful practice

• Transparency - communicating credit requirements and decisions to customers/accountants• Financial performance - Annual reviews at very least• Who else do you need to build a partnership with?

i.e. Accountant• Enable customers to see the benefits, cost savings &

management efficiency • BBM coaching customers in the use of the tool

• Present Data

• Stress testing

• Data Exchange

Dialogue Opportunity

Lets do this together !

ProfitabilityProfitability

Cash Flow &Funding

Cash Flow &Funding

Working Capital Management

Working Capital Management

Non-Current AssetsNon-Current Assets

Price Volume COGS Overheads Interest Cover Next $100 of sales

Working Capital % Cash Wastage Gross Cash Profit Cash after Ops Net Cash after Ops. Net Cash Income Change via debt Current Ratio Total liabilities/to equity Equity to Total Assets

A/R Days Inventory Days A/P Days Activity Ratio

Activity Ratio ROCE% Intangibles

1Strong

Weak Market Growth Market Share Delivery/Reliability Quality/Specifications New Product Develop New Market Develop Customer Retention Customer Growth Longer Contracts Product Costing Marketing Strategy Admin Costs Employee Satisfaction Teamwork Productivity Creativity Foreign Exchange issues

Supplier Terms of payment Customer Terms of Payment Credit Policy Credit Management Systems Taxation Strategy Funding Policy – NCA Dividend Policy Repayment of Equity Loans Statutory obligations unpaid

Forecasting accuracy Discounts - Suppliers Obsolete stock Inv. Management Sys. A/R Management Sys. A/P management Sys.

Drivers linked to MYOB ProfitOptimiser Points for Discussion

Funding Policy Valuation policy Depreciation Policy Unused Capacity Intangibles Investments Excess cash

2

3

4

1

Financial Performance Assessment …Four Customer Perspectives

MYOB ProfitOptimiser and the Banks

Using MYOB ProfitOptimiser

in the Banking Sector

MYOB ProfitOptimiser & Australian Banks

Bank

The Partnership Model

Two perspectives of Financial Performance in the Dialogue Channel

Non-Current Asset Management

Financialperformance andrisk monitoring

The Customer Perspective

The Lender Perspective

$

TransparencyTransparency

Working CapitalManagement

Cash Flow

ProfitabilityDebt Service

Capability

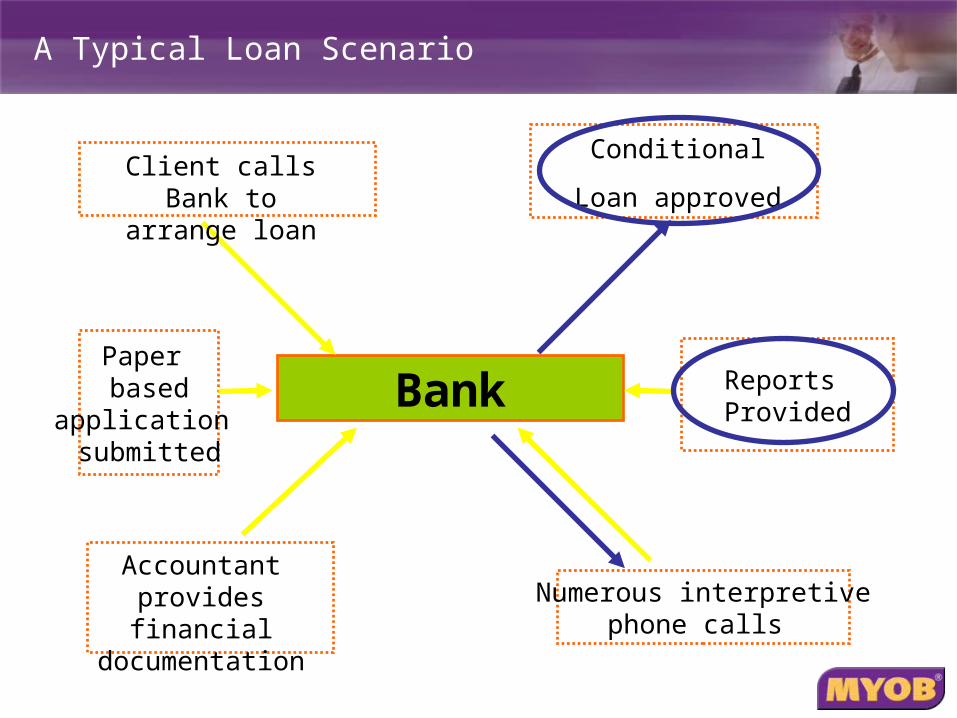

Bank Reports Provided

Numerous interpretivephone calls

Paper based

application submitted

Client calls Bank to arrange loan

Conditional

Loan approved

Accountant provides financial

documentation

A Typical Loan Scenario

Case Studies

Your Customer A Case Study and Presentation

MYOB ProfitOptimiser case study preparation

Required preparation activities for participants…

• Participation in MYOB ProfitOptimiser introductory training - you should have by now a sound understanding of the product navigation and use

• Select one of your customers to use as a ‘case study’ within the training session – your post course activity requires that you present what you complete in the training session to this customer. Save to USB device or CD.

• In preparation for this case study think about any financial ‘issues’ facing this customer (e.g. working capital management), and what might then be relevant to your customer for analysis in MYOB ProfitOptimiser.

• For this selected customer, bring their most recent two consecutive financial periods as an MYOB ProfitOptimiser model to the course – saved on a USB device or CD.

• Bring any other customer detail (or market details) which may assist with this analysis to be performed on your customer.

Your customer - A case study and presentation

Required ...

• Load your customer case study into MYOB ProfitOptimiser from your USB device or CD and using the structured approach to commencing a dialogue, prepare for your customer presentation. When preparing for your presentation remember to make sure that you:

– Explain the benefits

– Cover the key issues

– Highlight the advantages of a proactive approach

• One or two participants will be selected to present their findings to the group who will be asked to provide constructive feedback from the client’s perspective.

• In your analysis focus upon the following

– Profitability

– Cash Flow & Funding

– Working Capital Management

– Non-Current Asset Efficiency

Questions and Answers

Thank You