Risk and Insurance

33

Risk and Insurance Vani Borooah University of Ulster

-

Upload

missred277 -

Category

Documents

-

view

10 -

download

2

description

Basic Rish and Insurance

Transcript of Risk and Insurance

Risk and Insurance

Vani Borooah

University of Ulster

Gambles

An action with more than one possibleoutcome, such that with each outcomethere is an associated probability of thatoutcome occurring. If the outcomes aregood (G) and bad (B), denote theassociated probabilities by pG and pB

Payoffs and Utilities

With each outcome is associated a “payoff”which can be expressed in terms of money: $cGand $cB

With each payoff is associated a “utility”, u(c):u(cG) is the utility in the good situation u(cB) isthe utility in the bad situation. We assume thatutility increases with payoff

Note: a payoff is different from the utility from thepayoff

Expected Return and Utility

• Expected Return: The expected returnfrom the gamble is: ER=pGcG+pBcB

• Expected Utility: The expected utilityfrom the gamble is: EU=pGu(cG)+pBu(cB)

Note: The return expected from a gambleis different from the utility expected fromthe gamble

Facing a Gamble

You are faced with a gamble:

If you accept the gamble you will, inexchange for $W (the amount “staked”),receive CG with probability pG and CB withprobability pB

If you reject the gamble you will keep your$W

You have to decide whether or not toaccept the gamble?

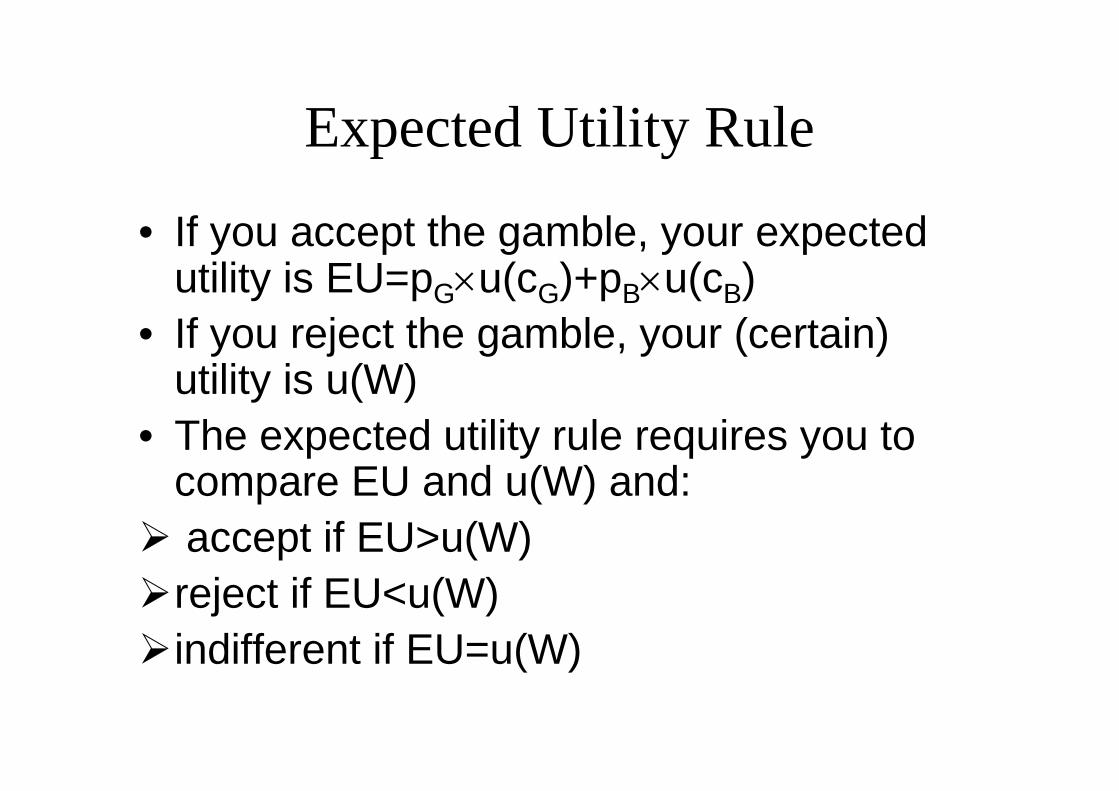

Expected Utility Rule

• If you accept the gamble, your expectedutility is EU=pGu(cG)+pBu(cB)

• If you reject the gamble, your (certain)utility is u(W)

• The expected utility rule requires you tocompare EU and u(W) and:

accept if EU>u(W)

reject if EU<u(W)

indifferent if EU=u(W)

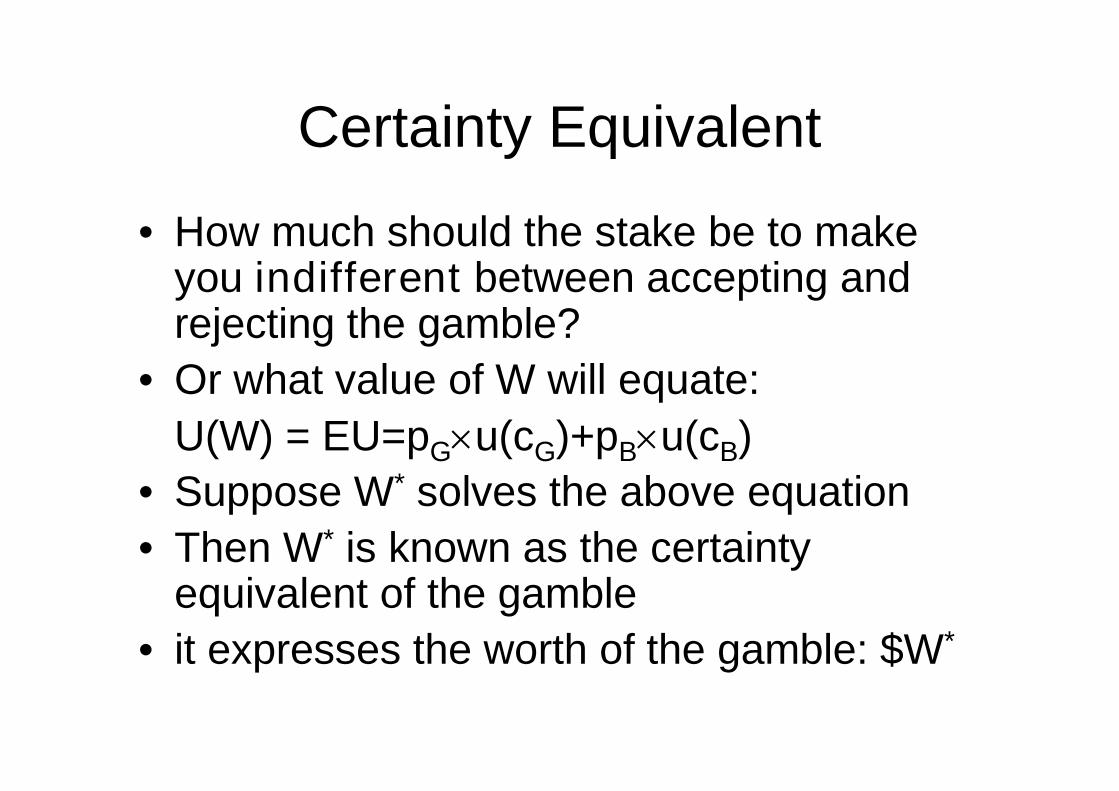

Certainty Equivalent

• How much should the stake be to makeyou indifferent between accepting andrejecting the gamble?

• Or what value of W will equate:

U(W) = EU=pGu(cG)+pBu(cB)

• Suppose W* solves the above equation

• Then W* is known as the certaintyequivalent of the gamble

• it expresses the worth of the gamble: $W*

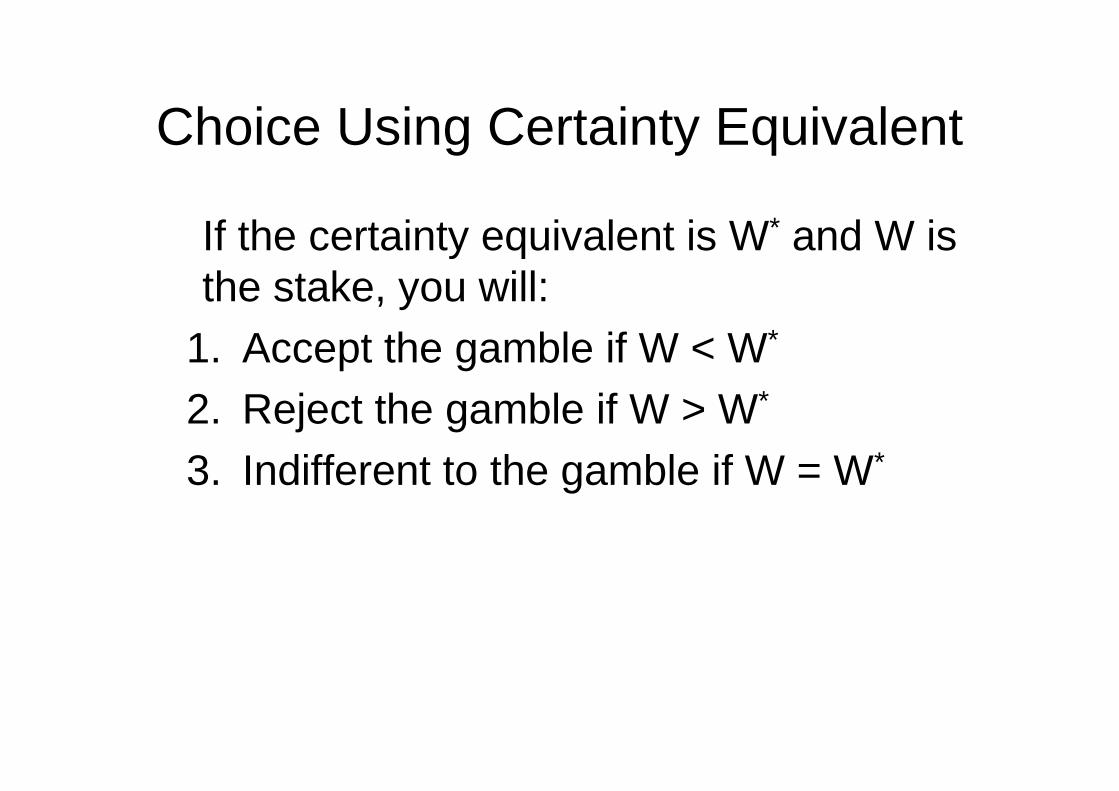

Choice Using Certainty Equivalent

If the certainty equivalent is W* and W isthe stake, you will:

1. Accept the gamble if W < W*

2. Reject the gamble if W > W*

3. Indifferent to the gamble if W = W*

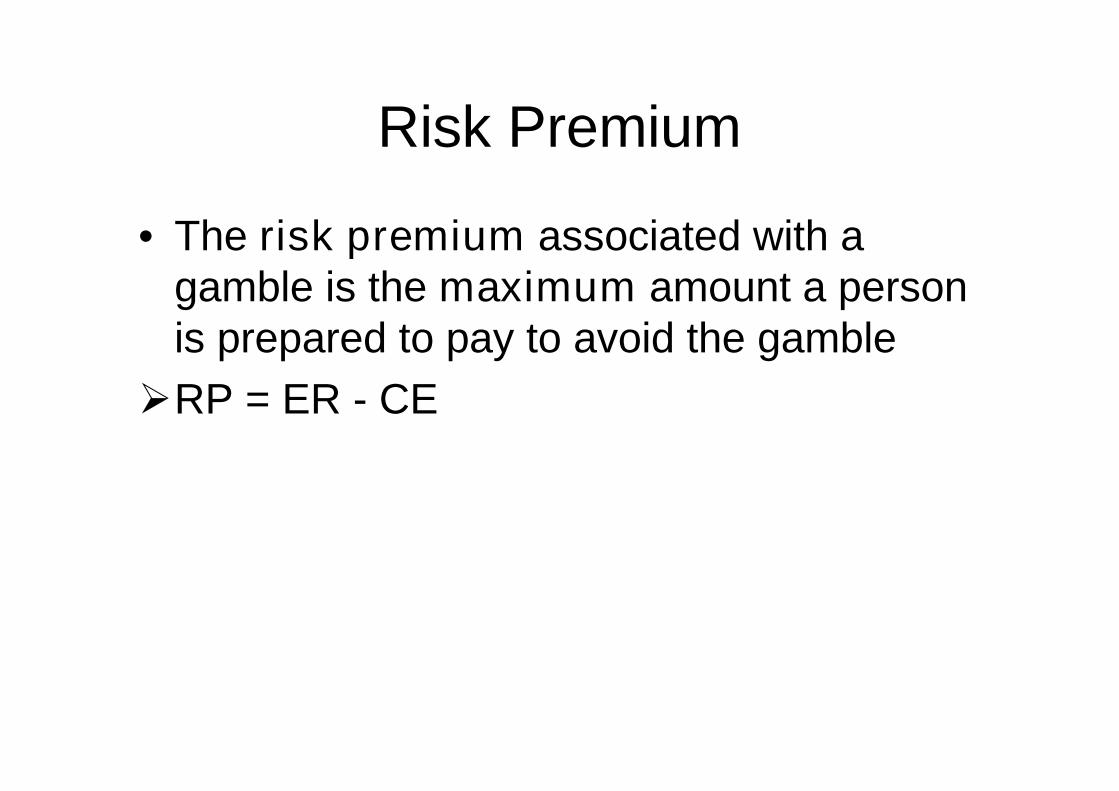

Risk Premium

• The risk premium associated with agamble is the maximum amount a personis prepared to pay to avoid the gamble

RP = ER - CE

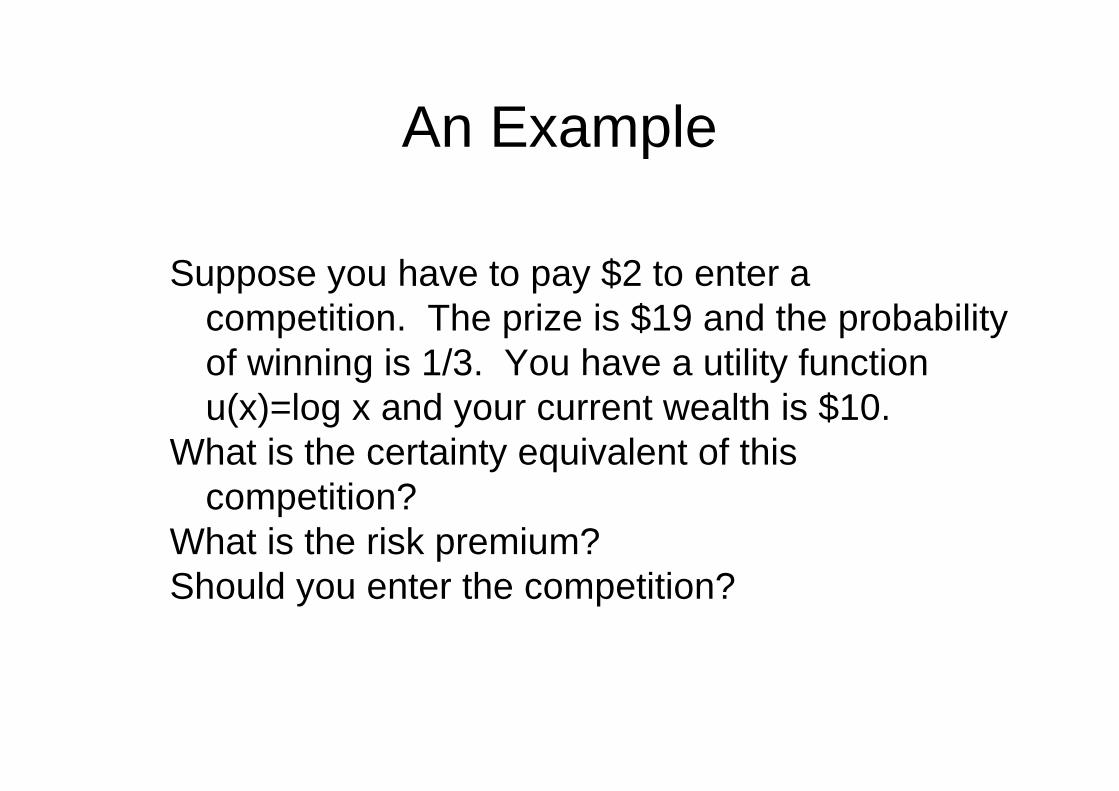

An Example

Suppose you have to pay $2 to enter acompetition. The prize is $19 and the probabilityof winning is 1/3. You have a utility functionu(x)=log x and your current wealth is $10.

What is the certainty equivalent of thiscompetition?

What is the risk premium?Should you enter the competition?

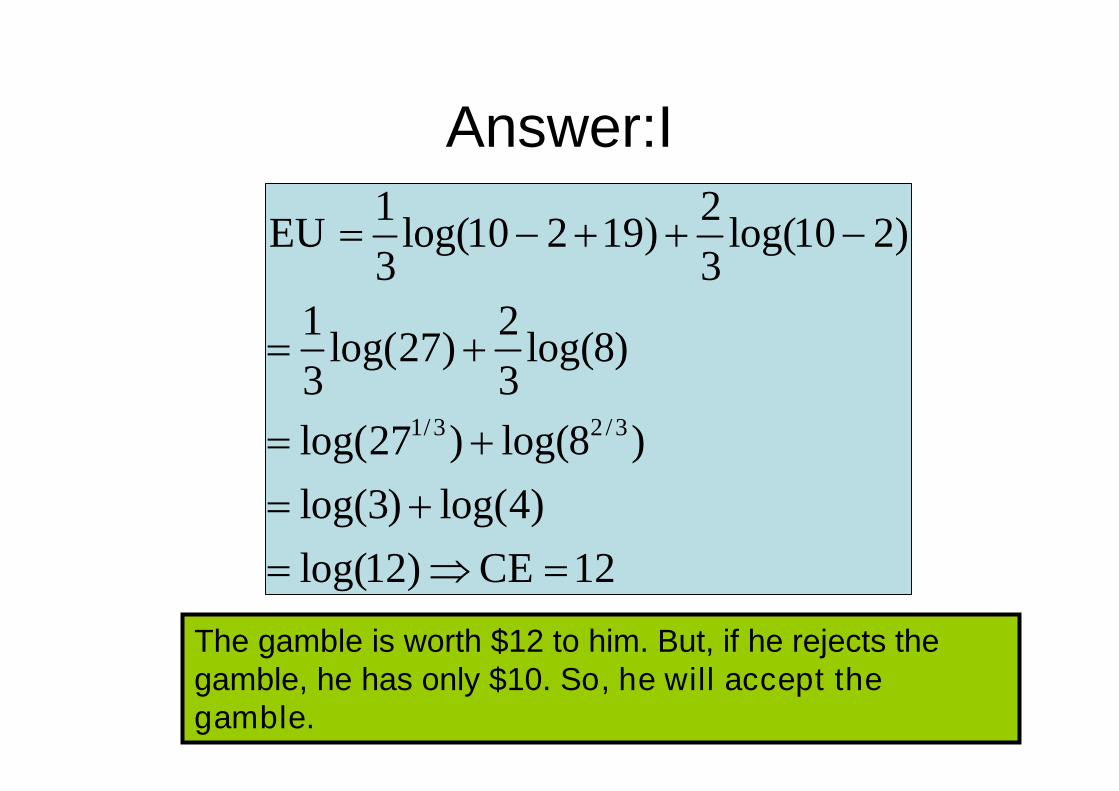

Answer:I

1/3 2 /3

1 2log(10 2 19) log(10 2)

3 3

1 2log(27) log(8)

3 3

log(27 ) log(8 )

log(3) log(4)

log(12) 12

EU

CE

The gamble is worth $12 to him. But, if he rejects thegamble, he has only $10. So, he will accept thegamble.

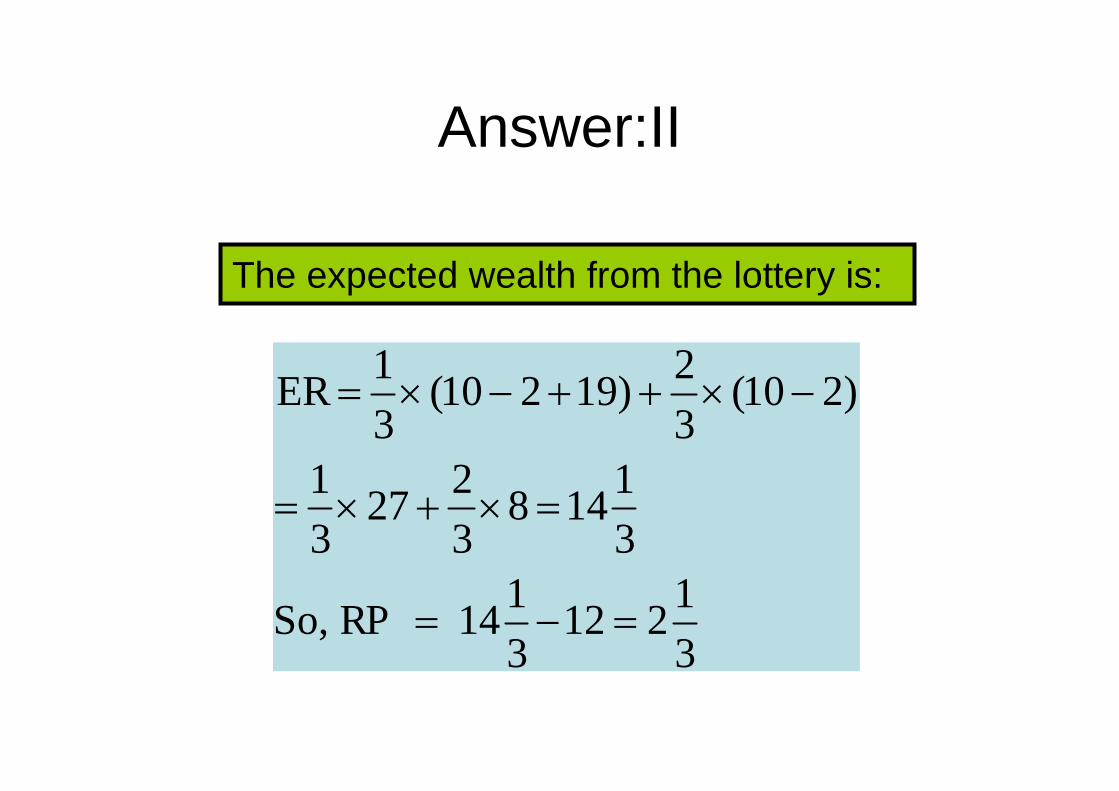

Answer:II

The expected wealth from the lottery is:

1 2(10 2 19) (10 2)

3 3

1 2 127 8 14

3 3 3

1 1So, 14 12 2

3 3

ER

RP

Attitudes to Risk

• Intuitively, whether someone accepts agamble or not depends on his attitude torisk

• Again intuitively, we would accept“adventurous” persons to accept gamblesthat more “cautious” persons would reject

• To make these concepts more precise wedefine three broad attitudes to risk

Three Attitudes to Risk

• The Risk Averse Person

• The Risk Neutral Person

• The Risk Loving Person

• To define these attitudes, we use theconcept of a fair gamble

• In essence, a fair gamble allows youreceive the same amount of moneythrough two distinct ways:

• Gambling or not gambling

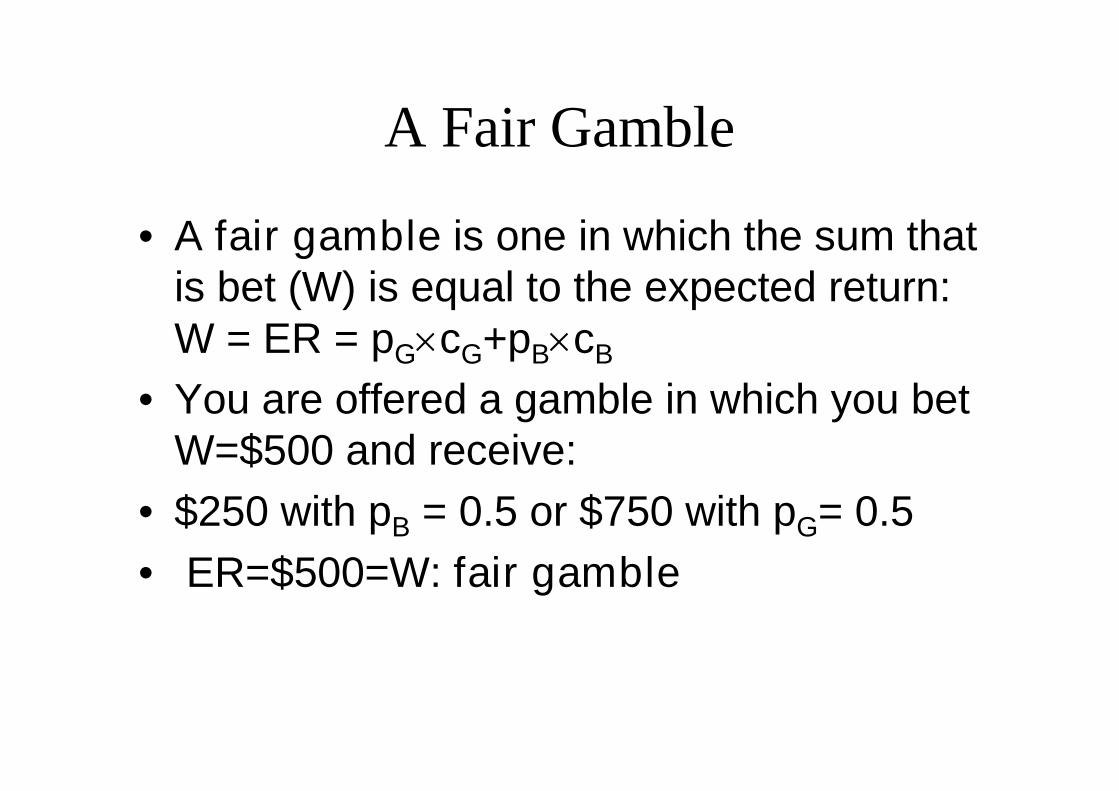

A Fair Gamble

• A fair gamble is one in which the sum thatis bet (W) is equal to the expected return:W = ER = pGcG+pBcB

• You are offered a gamble in which you betW=$500 and receive:

• $250 with pB = 0.5 or $750 with pG= 0.5

• ER=$500=W: fair gamble

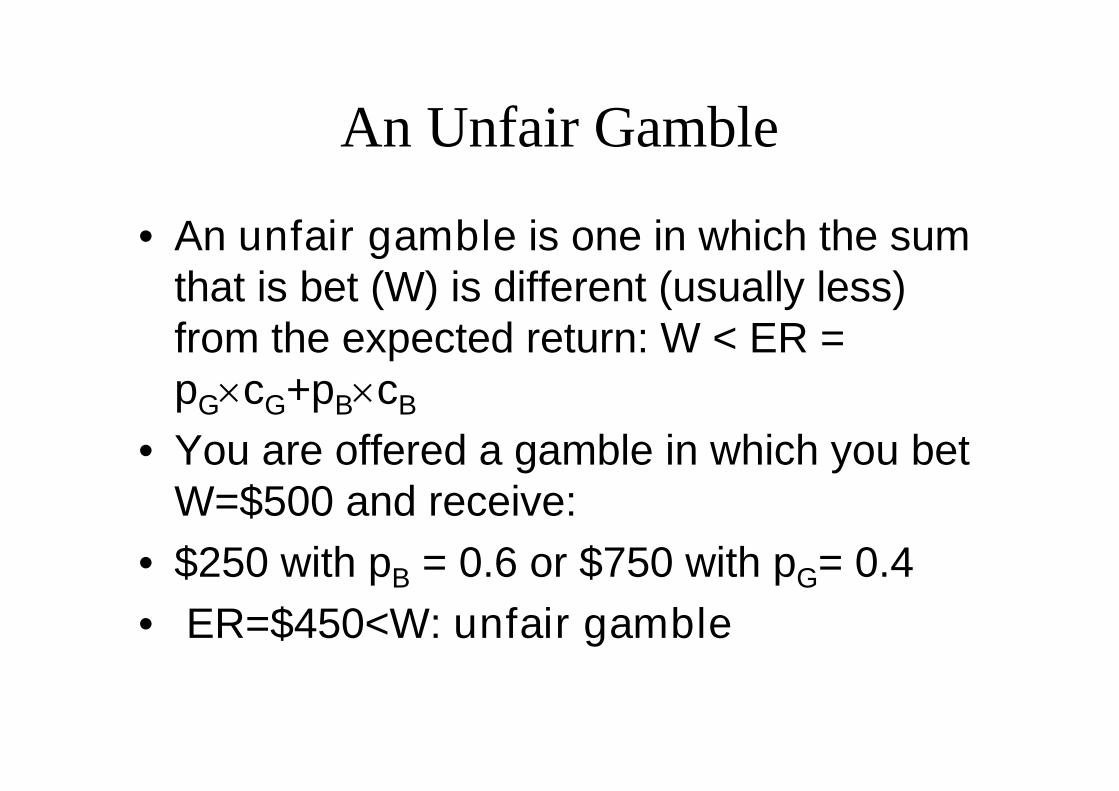

An Unfair Gamble

• An unfair gamble is one in which the sumthat is bet (W) is different (usually less)from the expected return: W < ER =pGcG+pBcB

• You are offered a gamble in which you betW=$500 and receive:

• $250 with pB = 0.6 or $750 with pG= 0.4

• ER=$450<W: unfair gamble

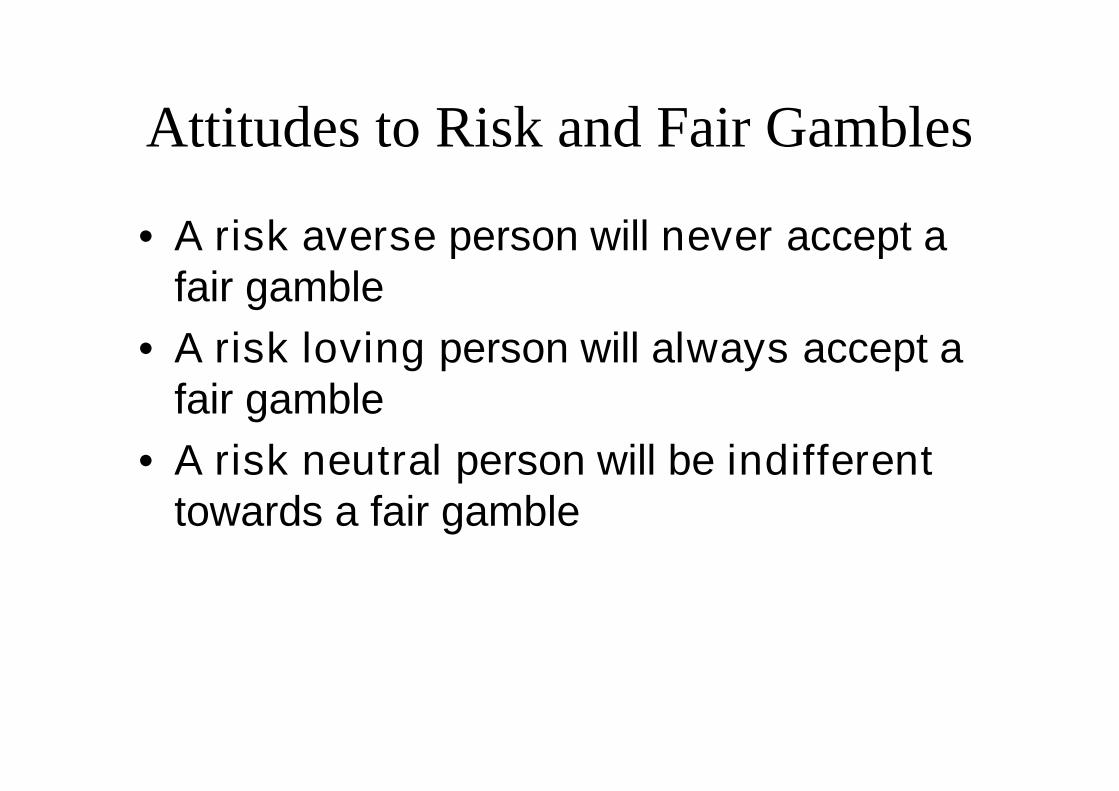

Attitudes to Risk and Fair Gambles

• A risk averse person will never accept afair gamble

• A risk loving person will always accept afair gamble

• A risk neutral person will be indifferenttowards a fair gamble

What Does This Mean?

• Given the choice between earning thesame amount of money through a gambleor through certainty

The risk averse person will opt forcertainty

The risk loving person will opt for thegamble

The risk neutral person will be indifferent

Diminishing Marginal Utility

• Why does the risk averse person reject thefair gamble?

• Answer: because her marginal utility ofmoney diminishes

Example

• Your wealth is $10. I toss a coin and offer you $1if it is heads and take $1 from you if it is tails

• This is a fair gamble: 0.511+0.59=10, but youreject it

• Because, your gain in utility from another $1 isless than your loss in utility from losing $1

• Your MU diminishes, you are risk averse

• Conversely, if you are risk averse, your MUdiminishes

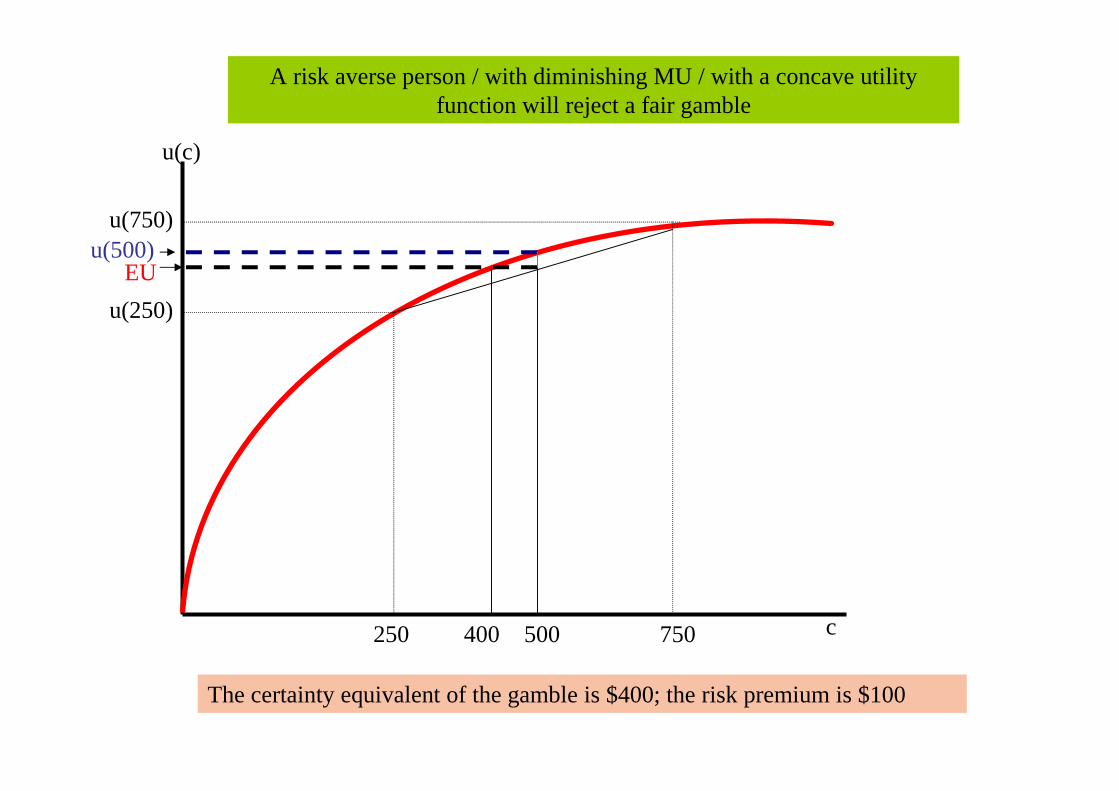

c

u(c)

u(250)

u(750)

250 750500

EUu(500)

A risk averse person / with diminishing MU / with a concave utilityfunction will reject a fair gamble

400

The certainty equivalent of the gamble is $400; the risk premium is $100

c

u(c)

u(250)

u(750)

250 750500

u(500)

=EU

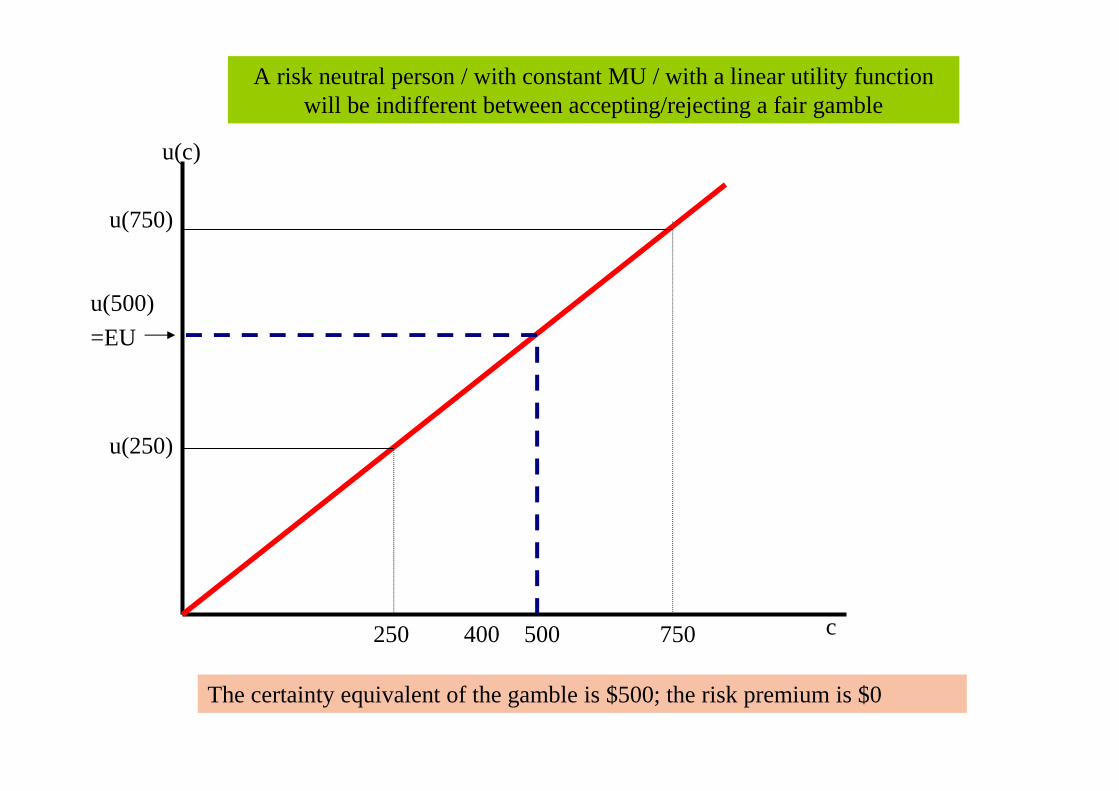

A risk neutral person / with constant MU / with a linear utility functionwill be indifferent between accepting/rejecting a fair gamble

400

The certainty equivalent of the gamble is $500; the risk premium is $0

c

u(c)

u(250)

u(750)

250 750500

EU

u(500)

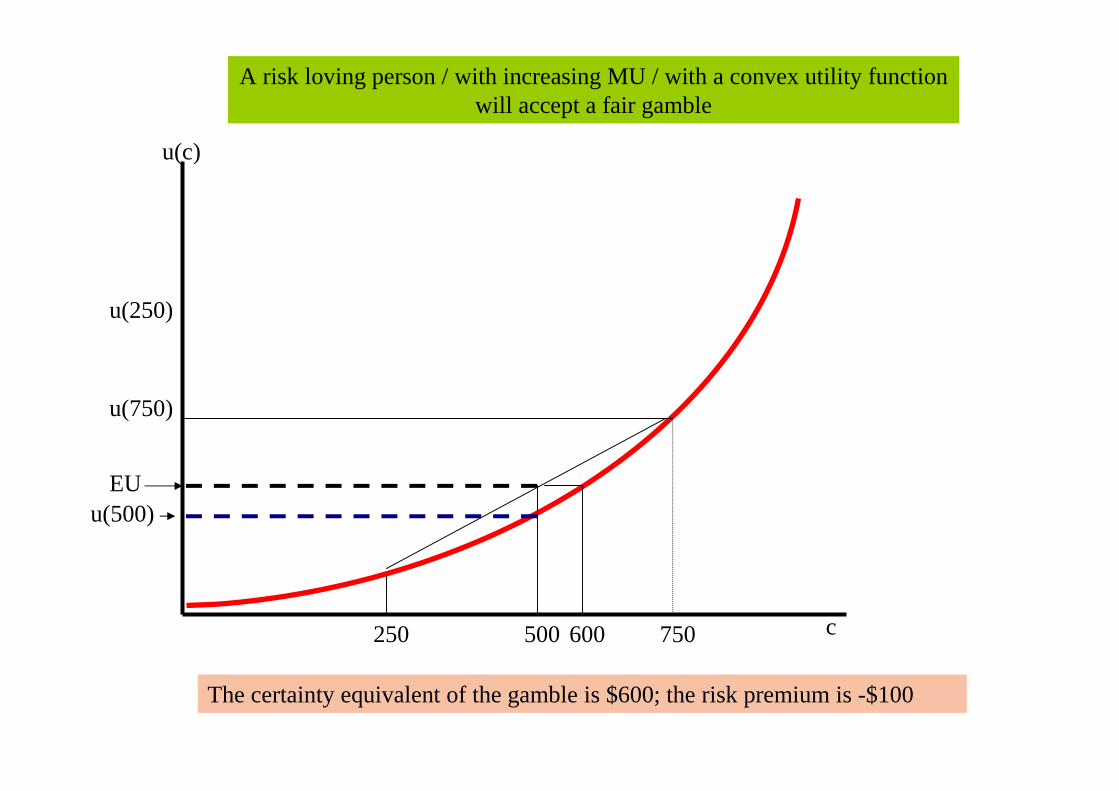

A risk loving person / with increasing MU / with a convex utility functionwill accept a fair gamble

600

The certainty equivalent of the gamble is $600; the risk premium is -$100

Contingent Commodities

• With contingent commodities, the nature ofthe commodity depends upon thecontingency:

A house before a storm is a different goodafter a storm

A car before an accident is a differentgood after an accident

A holiday in sunshine is a different goodfrom a holiday during which it rains

Trade in Contingent Markets

• The risk of a gamble is the difference between the payoff inthe good state (CG) and that in the bad state (CB): Risk = CG-CB

• When we buy insurance we try to reduce risk by tradingbetween two contingent states: “good” and “bad”

• We do this by buying wealth in the bad state and paying for itfrom wealth in the good state

• The rate at which we can make this exchange depends on thepremium $ (per $ of insurance bought) charged by theinsurance company

• $(1-) of additional CB can be bought by giving up $ of CG

• So $1 of additional CB can be bought by giving up (/1-) ofCG

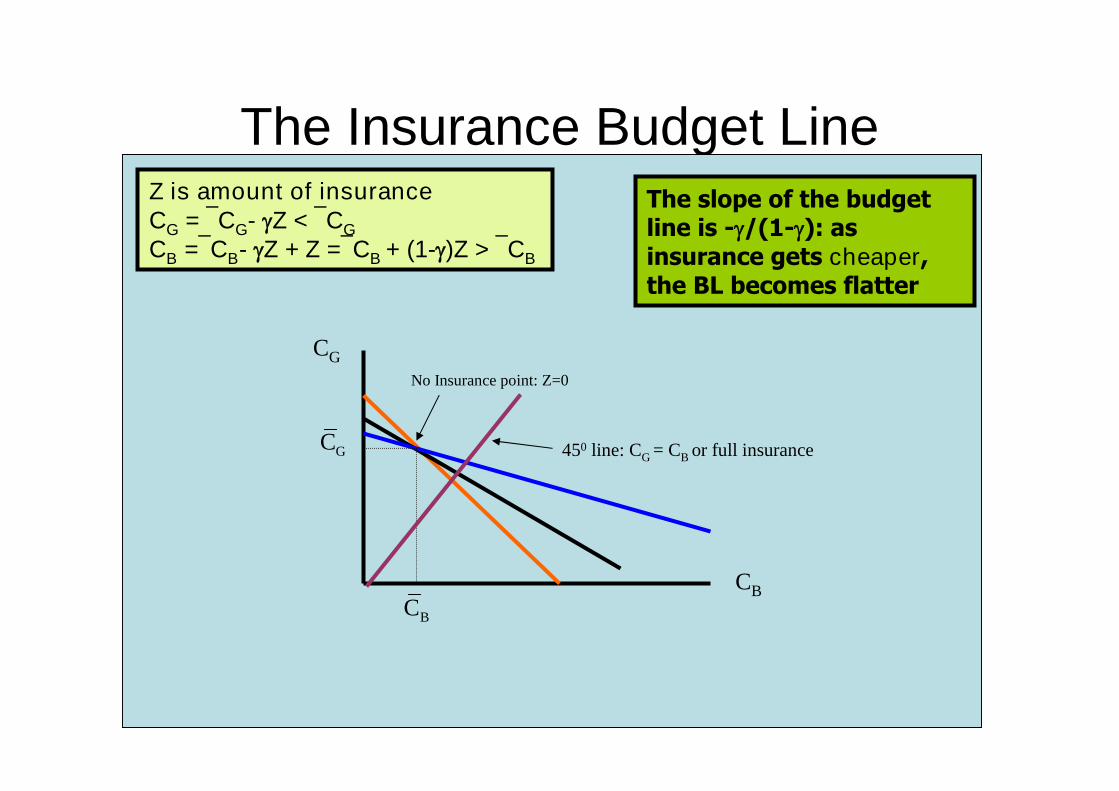

The Insurance Budget Line

CG

CB

No Insurance point: Z=0

450 line: CG = CB or full insurance

The slope of the budgetline is -/(1-): asinsurance gets cheaper,the BL becomes flatter

GC

BC

Z is amount of insuranceCG = CG- Z < CG

CB =CB- Z + Z =CB + (1-)Z > CB

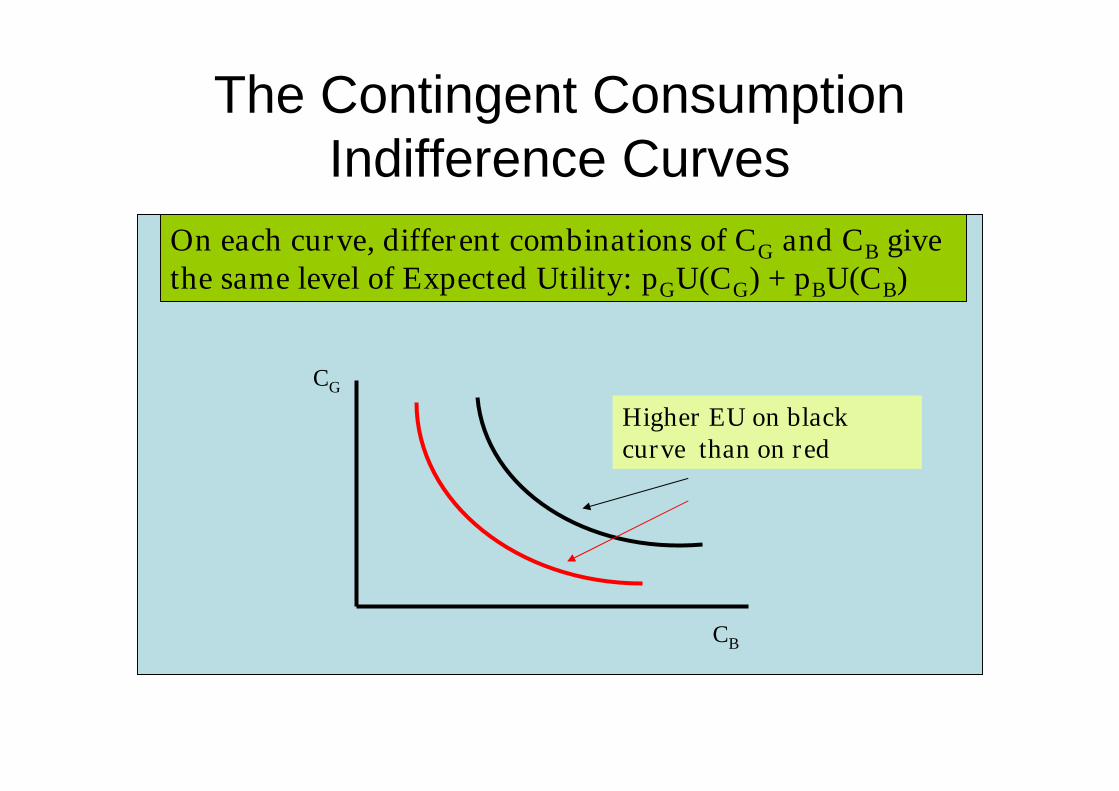

The Contingent ConsumptionIndifference Curves

CG

CB

On each curve, different combinations of CG and CB givethe same level of Expected Utility: pGU(CG) + pBU(CB)

Higher EU on blackcurve than on red

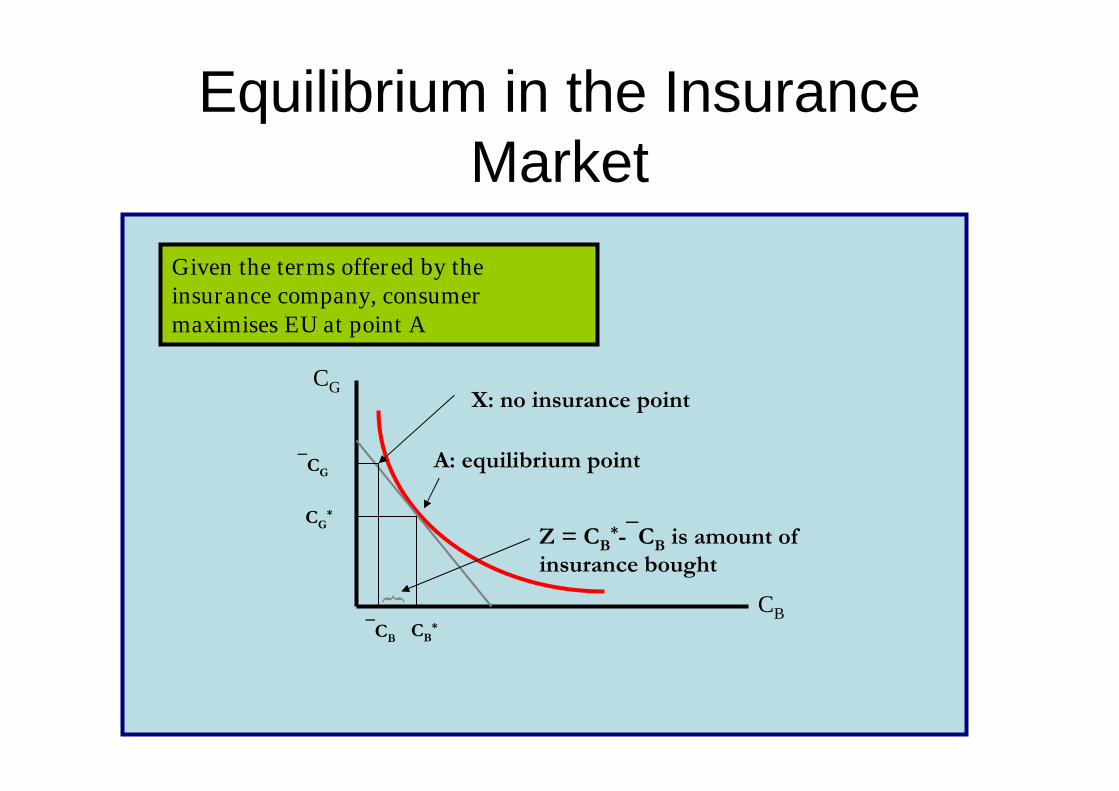

Equilibrium in the InsuranceMarket

CG

CB

Given the terms offered by theinsurance company, consumermaximises EU at point A

A: equilibrium point

X: no insurance point

CG

CB

CG*

CB*

Z = CB*-CB is amount of

insurance bought

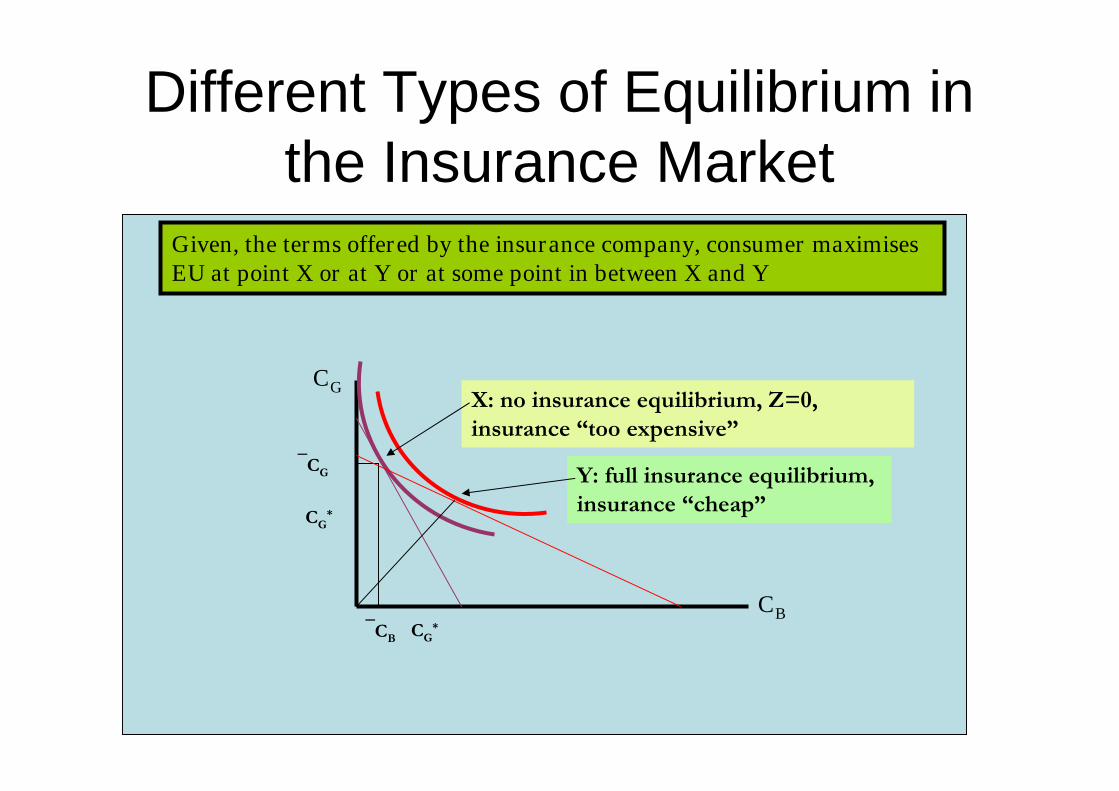

Different Types of Equilibrium inthe Insurance Market

CG

CB

Given, the terms offered by the insurance company, consumer maximisesEU at point X or at Y or at some point in between X and Y

X: no insurance equilibrium, Z=0,insurance “too expensive”

CG

CB

CG*

CG*

Y: full insurance equilibrium,insurance “cheap”

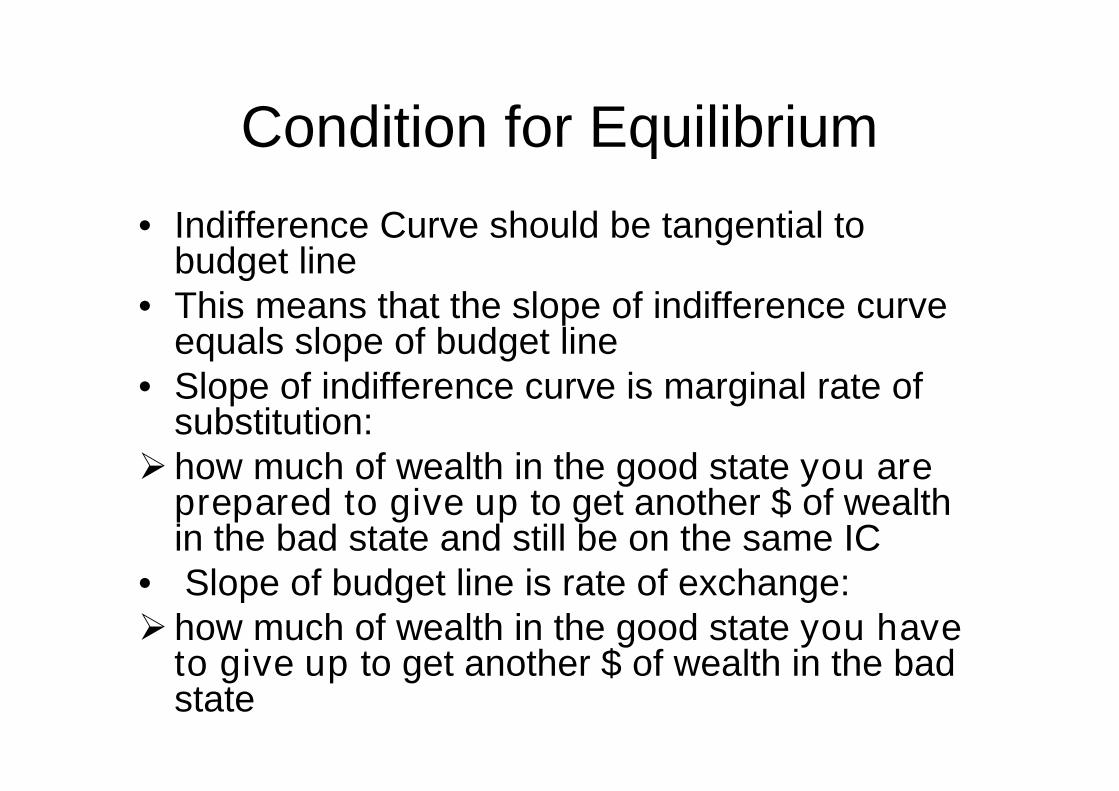

Condition for Equilibrium

• Indifference Curve should be tangential tobudget line

• This means that the slope of indifference curveequals slope of budget line

• Slope of indifference curve is marginal rate ofsubstitution:

how much of wealth in the good state you areprepared to give up to get another $ of wealthin the bad state and still be on the same IC

• Slope of budget line is rate of exchange: how much of wealth in the good state you have

to give up to get another $ of wealth in the badstate

Interpreting Equilibrium

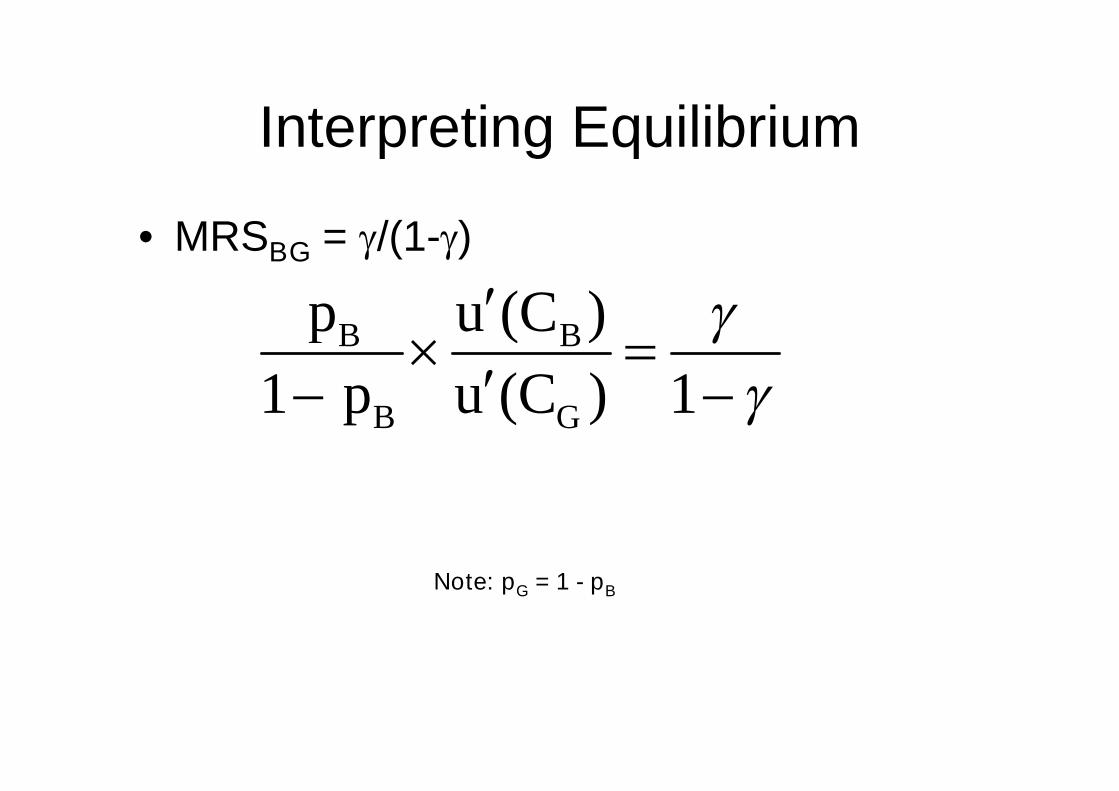

• MRSBG = /(1-)

( )

1 ( ) 1B B

B G

p u C

p u C

Note: pG = 1 - pB

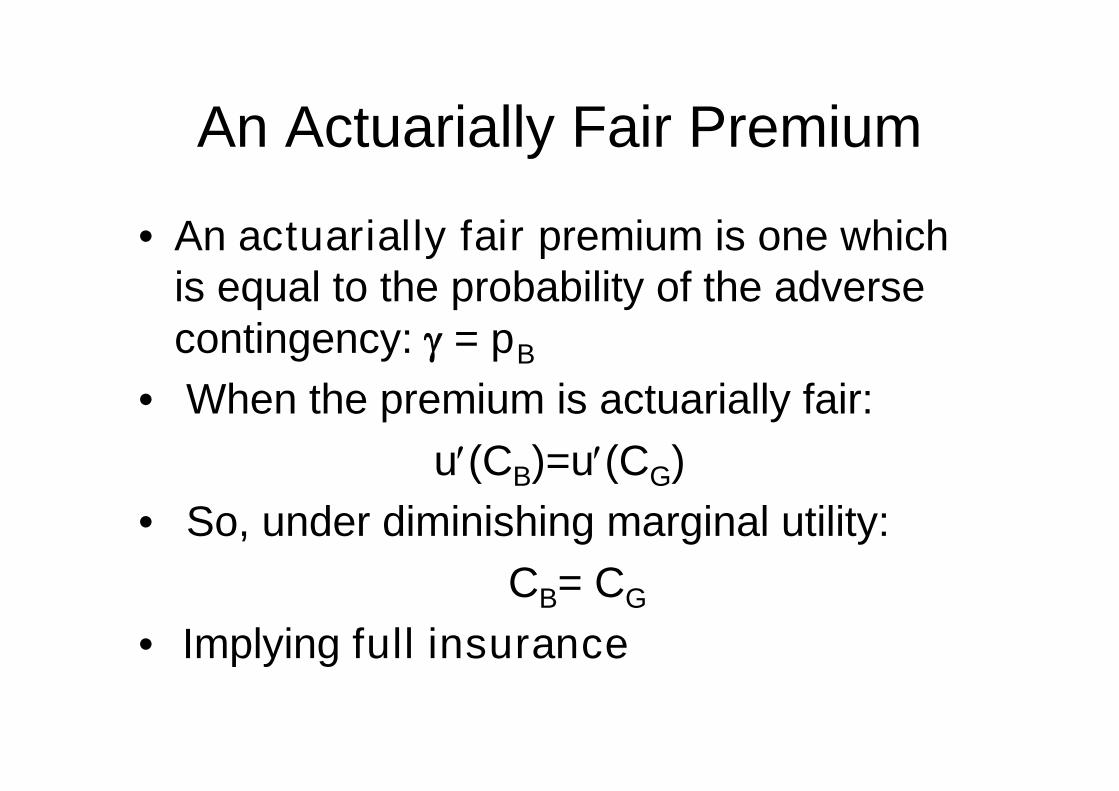

An Actuarially Fair Premium

• An actuarially fair premium is one whichis equal to the probability of the adversecontingency: = pB

• When the premium is actuarially fair:

u(CB)=u(CG)

• So, under diminishing marginal utility:

CB= CG

• Implying full insurance

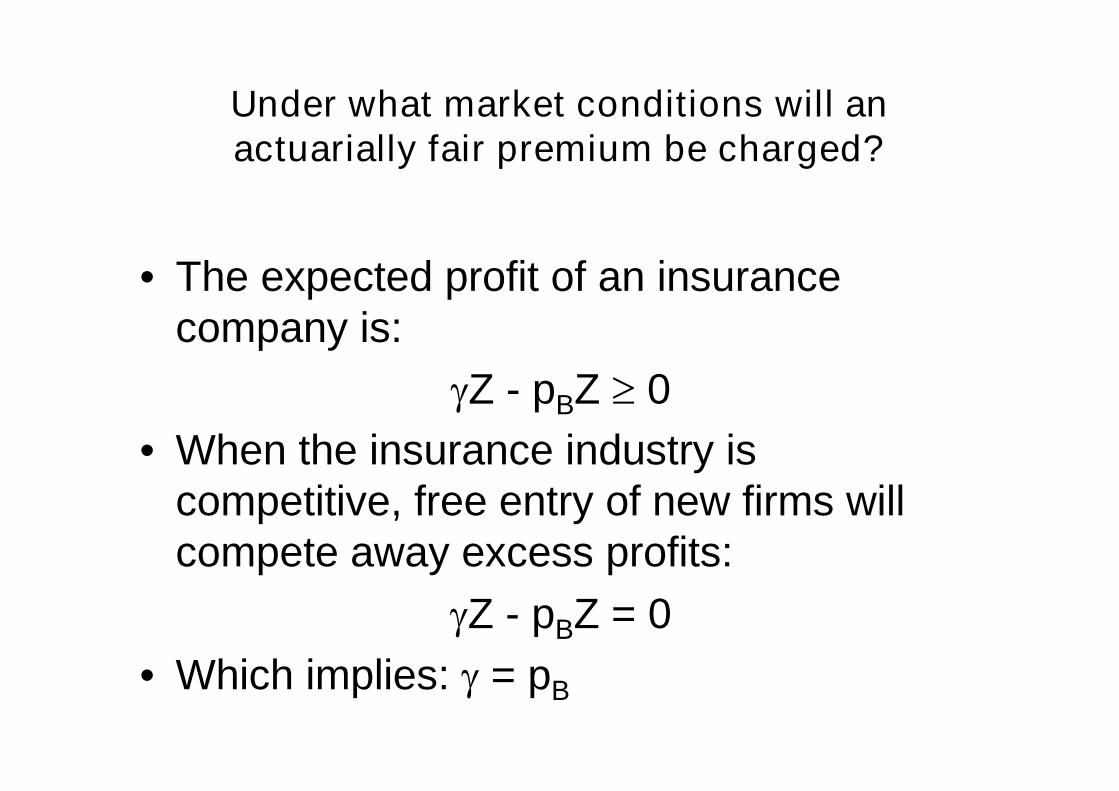

Under what market conditions will anactuarially fair premium be charged?

• The expected profit of an insurancecompany is:

Z - pBZ 0

• When the insurance industry iscompetitive, free entry of new firms willcompete away excess profits:

Z - pBZ = 0

• Which implies: = pB