Risk Analysis

18

Lecture 4. Security Analysis RISK ANALYSIS of SECURITIES

-

Upload

cometajanet -

Category

Business

-

view

50 -

download

0

Transcript of Risk Analysis

Lecture 4. Security Analysis

RISK ANALYSIS of SECURITIES

Risk in holding securities is generally associated with possibility that realized returns will be less than the expected returns.

ORRisk can be defined as the probability that the expected return from the security will not materialize.

Every investment involves uncertainties that make future investment returns risk-prone. Risk could be categorized depending on whether it affects the market as whole, or just a particular industry.

Types of Investment Risk

Systematic Risk

Unsystematic Risk Risk is the potential for variability in returns. Total variability in returns of a security represents the total risk of that security.

RISK

Systematic risk refers to that portion of total variability in return caused by factors affecting the prices of all securities. Economic, political, and social changes are sources of systematic risk. Nearly all stocks listed on the National Stock Exchange (NSE) move in the same direction as the NSE Index. On an average, 50 percent of the variation in a stock’s price can be explained by variation in the market index. In other words, about half of the total risk on an average common stock is systematic risk.

Systematic Risk is further subdivided into:Market Risk, (variation in returns caused by the volatility of stock market)Interest Rate Risk (Variation in bond prices due to change in interest rate)Purchasing Power Risk (Inflation results in lowering of the purchasing power of money) (Demand pull inflation and cost push inflation)

Systematic Risk

Unsystematic risk is the portion of total risks that is unique to a firm or industry. Factors such as management capability, consumer preferences, raw material scarcity and labour strikes cause unsystematic variability of returns in a firm. Unsystematic factors are largely independent of factors affecting securities markets in general.

Unsystematic Risk is further subdivided into: (Operating Environment, and Financing Pattern)

Business Risk (Variability in Operation Income caused by Operating Conditions)Financial Risk (Variability in EPS due to the presence of debt in Capital Structure)

Unsystematic Risk

Remember the difference: Systematic (market) risk is

attributable to broad macro factors affecting all

securities. Non-systematic (non-market) risk is

attributable to factors unique to a security.

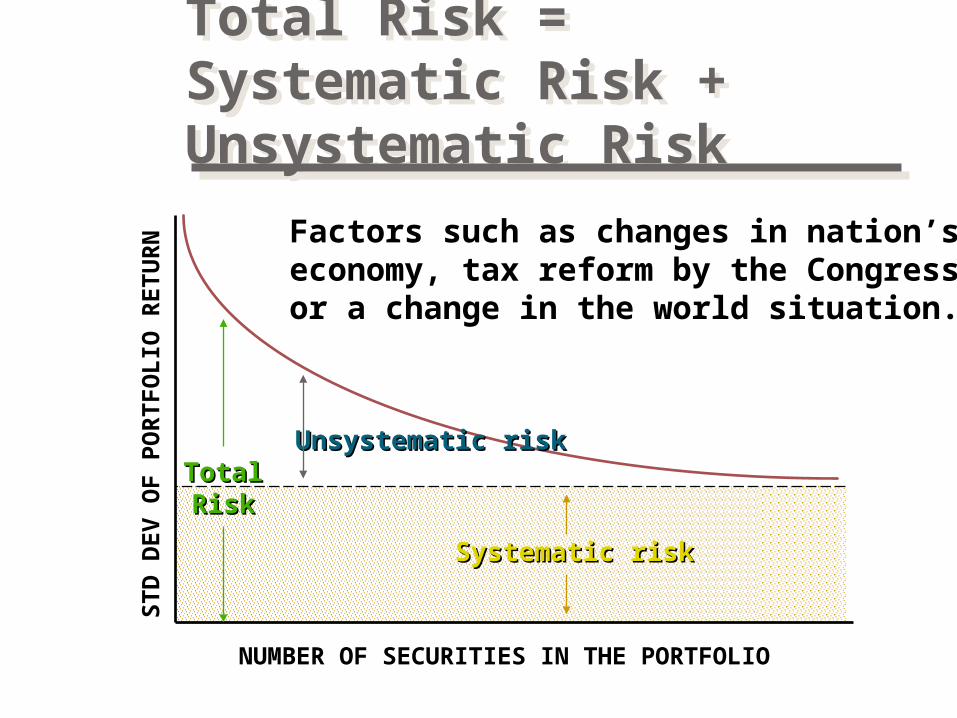

Total Risk = Systematic Risk + Unsystematic Risk

Total Risk = Systematic Risk + Unsystematic Risk

TotalTotalRiskRisk

Unsystematic riskUnsystematic risk

Systematic riskSystematic risk

ST

D D

EV

OF

PO

RT

FO

LIO

RE

TU

RN

NUMBER OF SECURITIES IN THE PORTFOLIO

Factors such as changes in nation’s economy, tax reform by the Congress,or a change in the world situation.

Total Risk = Systematic Risk + Unsystematic Risk

Total Risk = Systematic Risk + Unsystematic Risk

TotalTotalRiskRisk

Unsystematic riskUnsystematic risk

Systematic riskSystematic risk

ST

D D

EV

OF

PO

RT

FO

LIO

RE

TU

RN

NUMBER OF SECURITIES IN THE PORTFOLIO

Factors unique to a particular companyor industry. For example, the death of akey executive or loss of a governmentaldefense contract.

The risk involved in investment depends on various factors such as:

i) The length of the maturity period - longer maturity periods impart

greater risk to investments.

ii) The credit-worthiness of the issuer of securities - the ability of

the borrower to make periodical interest payments and pay back

the principal amount will impart safety to the investment and this

reduces risk.

iii) The nature of the instrument or security also determines the risk.

Generally, government securities and fixed deposits with banks

tend to be riskless or least risky; corporate debt instruments like

debentures tend to be riskier than government bonds and

ownership instruments like equity shares tend to be the riskiest.

The relative ranking of instruments by risk is once again

connected to the safety of the investment.

iv) Equity shares are considered to be the most risky

investment on account of the variability of the rates of returns

and also because the residual risk of bankruptcy has to be

borne by the equity holders.

v) The liquidity of an investment also determines the risk involved

in that investment. Liquidity of an asset refers to its quick

salability without a loss or with a minimum of loss.

vi) In addition to the aforesaid factors, there are also various others

such as the economic, industry and firm specific factors that

affect the risk an investment.

Another major factor determining the investment decision is the rate

of return expected by the investor. The rate of return expected

by the investor consists of the yield and capital

appreciation.

Unsystematic Risk

Volatility may be described as the range of movement

(or price fluctuation) from the expected level of return.

The variance and standard deviation measure the extent

of variability of possible returns from expected return.

Measurement of Risk

Determining Standard Deviation (Risk Measure)

Determining Standard Deviation (Risk Measure)

= ( ri - r )2

n-1n-1

Standard DeviationStandard Deviation, , is a statistical measure of the variability of a distribution

around its mean.It is the square root of variance.

Note, this is for a discrete distribution.

= ( ri - r )2

n-1n-1

Standard DeviationStandard Deviation, , is a statistical measure of the variability of a distribution

around its mean.It is the square root of variance.

Note, this is for a discrete distribution.

n

i=1

Coefficient of VariationCoefficient of VariationThe ratio of the standard deviation standard deviation of a

distribution to the mean mean of that distribution.It is a measure of RELATIVERELATIVE risk.

CV = / rr

The ratio of the standard deviation standard deviation of a distribution to the mean mean of that distribution.

It is a measure of RELATIVERELATIVE risk.

CV = / rr

Risk AttitudesRisk Attitudes

Certainty equivalent > Expected valueRisk PreferenceRisk Preference

Certainty equivalent = Expected valueRisk IndifferenceRisk Indifference

Certainty equivalent < Expected valueRisk AversionRisk Aversion

Most individuals are Risk AverseRisk Averse.

Certainty equivalent > Expected valueRisk PreferenceRisk Preference

Certainty equivalent = Expected valueRisk IndifferenceRisk Indifference

Certainty equivalent < Expected valueRisk AversionRisk Aversion

Most individuals are Risk AverseRisk Averse.

Risk Attitude Example

You have the choice between (1) a guaranteed dollar reward or (2) a coin-flip gamble of

$100,000 (50% chance) or $0 (50% chance). The expected value of the gamble is $50,000.

Mary requires a guaranteed $25,000, or more, to call off the gamble.

Raleigh is just as happy to take $50,000 or take the risky gamble.

Shannon requires at least $52,000 to call off the gamble.

Risk Attitude ExampleRisk Attitude ExampleWhat are the Risk Attitude tendencies of each?What are the Risk Attitude tendencies of each?

Mary shows “risk aversion”“risk aversion” because her “certainty equivalent” < the expected value of the gamble..

Raleigh exhibits “risk indifference”“risk indifference” because her “certainty equivalent” equals the expected value of the gamble..

Shannon reveals a “risk preference”“risk preference” because her “certainty equivalent” > the expected value of the gamble..

Mary shows “risk aversion”“risk aversion” because her “certainty equivalent” < the expected value of the gamble..

Raleigh exhibits “risk indifference”“risk indifference” because her “certainty equivalent” equals the expected value of the gamble..

Shannon reveals a “risk preference”“risk preference” because her “certainty equivalent” > the expected value of the gamble..

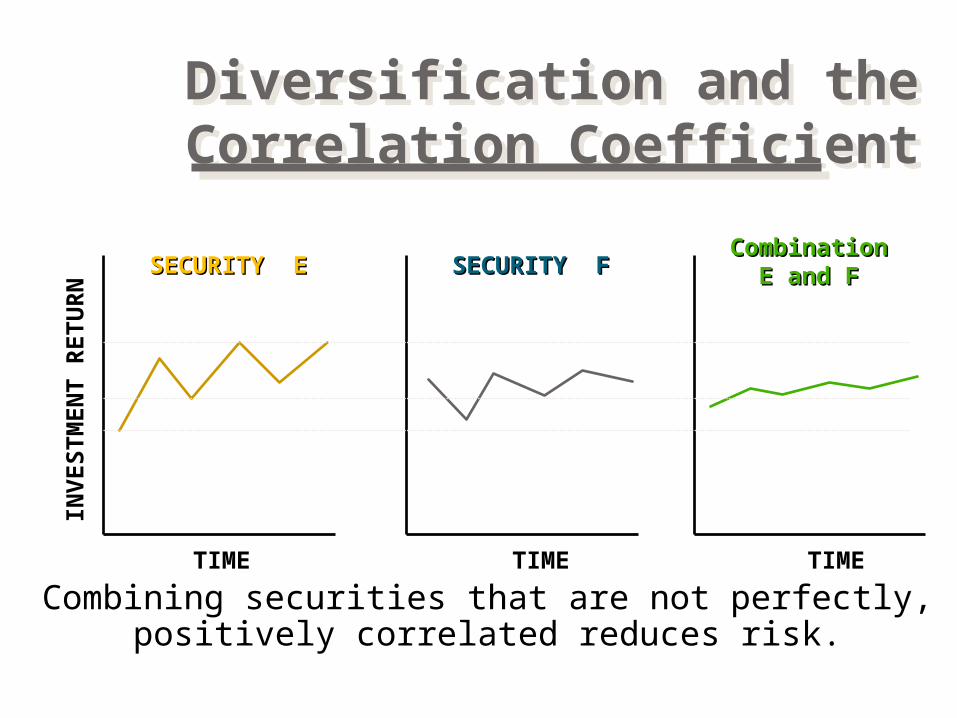

Diversification and the Correlation CoefficientDiversification and the Correlation Coefficient

Combining securities that are not perfectly, positively correlated reduces risk.

Combining securities that are not perfectly, positively correlated reduces risk.

INV

ES

TM

EN

T R

ET

UR

N

TIME TIMETIME

SECURITY ESECURITY E SECURITY FSECURITY FCombinationCombination

E and FE and F

Risk premium – a return premium that reflects the issue and issuer characteristics associated with a given investment vehicle

Realized return – current income actually received by an investor during a given period

Paper return – a return that has been achieved but not yet realized by an investor during a given period

Holding Period Return (hpr) – the total return from holding an investment for a specified holding period, usually 1 year or less

Yield (internal rate of return) – the compound annual rate of return earned by a long-term investment; the discount rate that produces a present value of the investment’s benefits that just equals its cost

Risk premium – a return premium that reflects the issue and issuer characteristics associated with a given investment vehicle

Realized return – current income actually received by an investor during a given period

Paper return – a return that has been achieved but not yet realized by an investor during a given period

Holding Period Return (hpr) – the total return from holding an investment for a specified holding period, usually 1 year or less

Yield (internal rate of return) – the compound annual rate of return earned by a long-term investment; the discount rate that produces a present value of the investment’s benefits that just equals its cost

Return Determinants

Holding Period ReturnHolding Period Return

HPR= C + CG VV00

C = current income during periodC = current income during periodCG = capital gain(loss) during periodCG = capital gain(loss) during period[Ending investment value – Beginning [Ending investment value – Beginning

investment value]investment value]VV00 = beginning investment value = beginning investment value

HPR= C + CG VV00

C = current income during periodC = current income during periodCG = capital gain(loss) during periodCG = capital gain(loss) during period[Ending investment value – Beginning [Ending investment value – Beginning

investment value]investment value]VV00 = beginning investment value = beginning investment value