Rise Aussie Mine November 2010 and Shine - pwc.com.au · PDF fileTotal borrowings 5,475 6,602...

44

What would you like to grow? pwc.com.au/industry/energy-resources Rise and Shine Aussie Mine November 2010

Transcript of Rise Aussie Mine November 2010 and Shine - pwc.com.au · PDF fileTotal borrowings 5,475 6,602...

What would you like to grow?

pwc.com.au/industry/energy-resources

Rise and Shine

Aussie MineNovember 2010

2 PwC

Michael HappellEnergy and Resources Leader

Tim GoldsmithGlobal Mining Leader

Foreword

Welcome to Aussie Mine for 2010. This year’s analysis presents an interesting foundation for what is anticipated as a return to form as Australian mid-tier miners Rise and Shine. Many mid-tier miners are currently enjoying bullet proof balance sheets, commodity price strength and a responsive and optimistic equity market, perhaps tempered by a strong Australian dollar (A$) and uncertainty around changes to the tax regime. Our analysis will provide further understanding of these key factors.

Many have bemoaned the loss of the Australian mid-tier miners through consolidation and takeover during the boom years of the past decade. We are seeing the rise of a new group of companies, now positioned to take the mantle of leaders in this sector and drive the re-emergence of a vibrant and commodity diverse Australian mid-tier.

Australia’s mining sector now has a strong and unprecedented opportunity at its doorstep. Our proximity to the growth of the emerging Asian giants and our abundance of in-demand resources to fuel that growth will continue to drive our economy, support employment and drive infrastructure development over the medium and long-term. As a nation it is up to us to support this development.

The mid-tier 50 are cashed up and poised for growth. Executives and Boards have weathered the storm, successfully raised capital and re-financed debt and are now ready to take the next step. We will see the deployment of the significant cash resources held by these companies, both through organic project development and mergers & acquisition activity. While current market conditions suggest short-term volatility will persist, investors should be poised and ready to be taken on a ride as the mid-tier Australian mining sector is ready to rise and shine.

We trust you will enjoy…

Michael Happell

Tim Goldsmith

Aussie Mine November 2010 3

Table of contents

1 Mid-tier50summaryfinancialinformation 4

2 Executive summary 5

3 Mid-tier industry in perspective 6

3.1 Market capitalisation 6

3.2 Comparison of the mid-tier 50 to other performance measures 9

3.3 M&A - from necessity to opportunity 10

3.4 Movementsinthemid-tier50 14

4 ThewayIseeit–NicoleHollows 15

5 Aggregated industry income statement 18

5.1 Focus–Accountingchanges:Rockyroadaheadforminingsector 26

6 Aggregated industry balance sheet 28

6.1 Focus - A tax on iron ore and coal, but encouraging for exploration 30

7 Aggregatedindustrycashflowstatement 32

7.1 Focus-Don’tletyourcapitalprojectbiteback 34

8 Looking ahead 36

9 Glossary 37

10 Mid-tier 50 companies analysed 38

11 Explanatorynotes 40

12 ContactingPwC 41

13 OtherMiningPublications 42

4 PwC

Mid-tier 50 summary financial information

2010 A$m

2009 A$m

Change %

Profit and Loss

Revenue 11,317 8,561 32%

Operating expenses (8,639) (6,108) 41%

Adjusted EBITDA 2,355 2,512 (6%)

Gain / (loss) on sale of investment (354) 487 (173%)

Impairment (111) (1,738) (94%)

Net profit/(loss) (26) (622) 96%

Cash Flow

Proceeds from ordinary share issues 3,794 2,410 57%

Distributions to shareholders (1,023) (966) 6%

Net operating cash inflow 1,922 2,112 (9%)

Net financing cash inflow 3,246 2,857 14%

Net borrowing inflows/(outflows) (840) 677 (224%)

Balance Sheet

Cash 7,373 3,658 102%

Property, plant and equipment and capitalised exploration 20,175 18,435 9%

Total borrowings 5,475 6,602 (17%)

Net assets 28,402 24,034 18%

Market Capitalisation

Market capitalisation 63,942 47,202 35%

Market capitalisation to net assets ratio 2.25 1.96 15%

1

Aussie Mine November 2010 5

Executive summary

Financial year 2010 saw strong growth for the mid-tier 50 as commodity prices continued to strengthen on the back of growing demand from Asia’s industrialising economies and a number of othersinthedevelopingworld.ItistimetoshineforAustralia’s mid-tier miners.

Revenue jumped by 32% largely underpinned by the strong performance of copper, gold and the unexpected star, platinum. The strong performance in these commodities has been driven by production growth as a result of the increase in the number of operating mines both locally and offshore. The increase in revenue has also been compounded by the rise in the commodity prices for copper, gold and platinum.

Whilst there has been some uncertainty surrounding the political arena in Australia and the impact of the Minerals Resource Rent Tax (MRRT) and its doomed precursor, the Resource Super Profits Tax (RSPT), the mid-tier 50 remain strong and poised for growth, with cash balances climbing to a remarkable 19% of total assets during 2010, to be in excess of $7 billion.

Equity markets have opened once again, with 10% of the market capitalisation of the mid-tier 50 at June 2010 having been raised over the past two years. While investors were willing to put their hands in their pockets, the mid-tier 50 were reluctant to spend their fortunes with capital investment falling 70% during 2010. The outcome of the Australian Federal Election and the MRRT negotiations appeared to have played a role in cautious investment decision.

On the deals front, Chinese investors continue to target Australian resource companies and projects, however the strengthening A$ no longer favours the foreign investor; as it is increasingly expensive for them to engage in M&A activity in Australia. We have noted a recent trend of Chinese entities seeking control of ASX listed vehicles with African assets, or the ability to spin African assets into these entities as Chinese companies look to leverage off in-country experience and relationships to African projects.

From a cash flow perspective, a focus on debt financing continued to be a key theme, as some companies in the mid-tier 50 rationalised investments or looked to the market for funds to reduce borrowings. By the end of 2010, the mid-tier 50 experienced ‘net zero’ gearing as cash exceeded total borrowings by $1.9 billion.

A significant challenge for the mid-tier 50 over the next 12 months is to balance the expectation of shareholders with the objectives of the companies to ensure that they look to invest in projects that give them ‘bang for their buck’.

In our 2009 publication we asked each company whether they are on the road to recovery. Now that the global financial crisis is behind us and the political arena in Australia is stabilising, the boards of the mid-tier 50 should have growth aspirations at front of mind, as it is time to Rise and Shine.

2

6 PwC

3.1 Market capitalisationBack to where we started

The market capitalisation of the mid-tier 50 has increased by over 35% to $63.9 billion in June 2010 compared to June 2009 levels, delivering strong capital gains to any investors shrewd enough to have bought at the bottom of the market.

When we look at the movements in market capitalisation over the past 24 months, the rollercoaster ride investors have been on is evident. The market came off its lofty heights in June 2008 to a nadir in late 2008/early 2009. Putting the increase in market capitalisation into context and stepping away from the headline of 35% increase – what we have seen over the past 12 months is simply a return of the value that was lost in equity markets during the global financial crisis (GFC) and fortunes and results have improved.

This market rally is framed against a weak outlook for the United States and Europe, completion of stimulus packages by government and uncertain debt and capital markets. If this subdued global outlook was to turn to a more optimistic tone and a corresponding market sentiment achieved, we may expect to see another upward push in market capitalisation for these mid-tier 50 companies.

The cut-off point for inclusion in the mid-tier 50 list has changed since our November 2009 publication. In this year’s analysis, the 50th company was Northern Iron Limited, a new entrant in 2010, with a market capitalisation of approximately $400 million. This was significantly higher than the cut-off of $227 million for 2009. This movement was consistent with the positive movement in the market for mining companies during the year.

43 of the mid-tier 50 companies increased their market capitalisation during 2010. Notably, the market capitalisation of four coal companies, Riversdale Mining Ltd, Macarthur Coal Ltd, Whitehaven Coal Ltd and Aquila Resources Ltd increased by more than $1 billion each for the period.

We continue to see strong Chinese growth metrics and do not foresee a decrease in the near term. The Chinese Communist Party (CCP) is starting to look at finalising the 12th Five-Year Plan, which will drive strategic priorities goals out to 2015. Commentary espousing a change in direction for China to a more inwardly focused growth story, must be kept in context. China requires mined commodities to bring its population from a largely rural society to an expanding middle class with all the wants and needs of consumers in developed nations. China’s influence on the Australian mining industry and demand for our commodities is not done yet. In fact, it has probably only just begun.

32% rise since June 2010

In the first three months of the 2011 financial year, the market capitalisation of the mid-tier 50 continued to exhibit accelerated growth, increasing a further 32% from June 2010, the equivalent to the entire growth achieved in FY10, these companies are once again starting to shine. Our performance appears to indicate some de-coupling from the United States and troubled European economies.

Whilst the mid-tier 50 have performed strongly across the board gold, coal and copper have been the standout performers, particularly in the period subsequent to 1 July 2010. Where there has been a distinct elevation in the growth line.

Mid-tier industry in perspective 3

China’s influence on the Australian mining industry and demand for our commodities is not done yet. In fact, it has probably only just begun.

Market Cap in AUD

0

10

20

30

40

50

60

70

80

90

Aug-08 Oct-08 Dec-08 Feb-09 Apr-09 Jun-09 Aug-09 Oct-09 Dec-09 Feb-10 Apr-10 Jun-10 Aug-10

Mid-tier 50 market Capitalisation in A$m

Table 1: Mid-tier 50 market capitalisation – month end information June 2008 to October 2010Source: Capital IQ

Aussie Mine November 2010 7

Uranium no longer powering the market?

In the November 2009 publication, Extract Resources Ltd, Deep Yellow Ltd and Energy Resources of Australia Ltd were three of only nine companies that experienced increases in market capitalisation. In 2010, the market capitalisation of these companies and other companies in the uranium sector, have experienced a steady decline with the sector falling behind its peers and the market as a whole.

Two of the largest ASX listed Uranium companies, Energy Resources of Australia and Paladin Energy, experienced declines of 43% and 15% respectively between June 2009 and June 2010, this is despite revenue and profit growth year on year. This is largely due to foreign exchange movements for a commodity sold in USD and modest performance outlooks due to production challenges for these companies in the near term.

Gold, stunning growth but are we missing something?

Gold continued to outperform and shine brighter than other commodity groups, with a growth in market capitalisation of 98% in the 12 months to June 2010. In comparison, the market capitalisation of the other strong performers (coal, copper and platinum) increased by an average 45%.

The gold companies, representing 11 of the mid-tier 50, experienced a further 76% growth in market capitalisation in the quarter ended September 2010 – a phenomenal result. By September 2010, gold was significantly outperforming the ASX 300 Metals and Mining index, illustrating that gold has once again returned to favour as a commodity as noted in the performance of gold companies against other metals and mining companies on the ASX.

0.00

0.50

1.00

1.50

2.00

2.50

3.00

Jun-09 Jul-09 Aug-09 Sep-09 Oct-09 Nov-09 Dec-09 Jan-10 Feb-10 Mar-10 Apr-10 May-10 Jun-10 Jul-10 Aug-10 Sep-10

Gold Coal Copper Platinum Other Uranium Mid-tier 50 Month End Market Cap

174% Gold

(21%) Uranium

35% Platinum

98% Copper93% Coal67% Mid-tier66% Other

Mid-tier 50 market capitalisation at month ends index – by resource

27% ASX 300 M&M 27% ASX 300 M&M

58% ASX 300 Gold

27% ASX 300 M&M

Jul-09 Aug-09 Sep-09 Oct-09 Nov-09 Dec-09 Jan-10 Feb-10 Mar-10 Apr-10 May-10 Jun-10 Jul-10 Aug-10 Sep-10

0.70

0.90

1.10

1.30

1.50

1.70

ASX 300 Metals and Mining vs ASX Gold Index

A key contributing factor to the strength of gold companies is the bullish longer term gold forecasts, coupled with a strong increase in the average US dollar (US$) gold spot price to record levels. The positive outlook for gold is supported by the latest PwC gold price survey which found that 71% of companies surveyed have adjusted up their average gold price assumptions used in ongoing reserve determinations and asset carrying values as at 31 December 2009. The average price indicated by respondents was US$764 for reserves compared to US$734 in 2008 and US$825 for asset carrying values compared with 2008’s price of US$751.

Although these prices are conservative when compared to current record (nominal) gold prices of upwards of US$1300 per oz, they do show a shift in global thinking around the future of gold. We note from our work with gold companies that most consensus prices used in models have trailed the actual US$ gold price.

Table 2: Mid-tier 50 market capitalisation index by sector – Month end information June 2009 to September 2010 (30 June 2009 = 1)Source: Capital IQ

Table 3: ASX300 Metals and Mining vs ASX 300 Gold July 2009 – September 2010Source: Capital IQ

8 PwC

But A$ gold…

Although the headline US$ gold price spot has increased by around 50% as at September 2010 when compared to June 2009, its performance in appreciating currencies such as the A$ has been less impressive.

In the three months following June 2010, the strengthening of the AUD:USD exchange rate has the potential to inhibit the growth in A$ gold revenues compared with US$ counterparts. For instance, although the US$ gold prices have increased by 50% from June 2009 to September 2010, the A$ against the US$ has also appreciated by 35% over that period resulting in only an 11% increase in the A$ gold price over the same period.

Gold medal performers

During financial year 2010, three companies increased their market capitalisation by over 300%, two of these top performers were from the gold sector.

OceanaGold Corporation has three operating Gold mines in New Zealand and has the potential to add value through the re-commissioning of its Didipio mine project in the Philippines which has been on care and maintenance since 2008. On the other hand, Perseus Mining Ltd is an emerging gold producer, has had positive drill results and boasts a resource of 2.1 million ounces at its Central Ashanti gold project in West Africa which is targeting commencing production in Q3, 2011.

It is also great, of course, that the best performance is from an explorer. The success to date of Sandfire is bound to spur many others on, and is frankly exactly what the mining industry is all about.

The A$ gold price has not experienced the same record highs of the US$ gold price. However, at current prices, companies are still seeing positive share price movements, and more marginal operations are being assessed for re-commissioning. Despite the A$ price being lower than in early 2009, the market capitalisation of gold companies is up 98% for the period June 2009 to September 2010. The question arises. Are we starting to see disconnect between movement in the market capitalisation of gold companies and the A$ gold price?

Perhaps as global sentiment is still subdued and there are continued questions about the health of the United States and European economies, gold is continuing to be seen as the safe haven store of wealth. Thus investing in companies with gold exposure, in the form of current or near term production is preferable. In the period that market capitalisation of gold miners has risen by over 170%, the A$ gold price has kept in a very small band and has almost stood still. Does this mean market gold companies were undervalued in 2009, or is there really support for the recent market capitalisation?

Although the headline US$ gold price spot has increased by around 50% as at September 2010 when compared to June 2009, its performance in appreciating currencies such as the A$ has been less impressive.

Sandfire Resources (ASX:SFR) 362%

349%

341%

196%

166%

156%

154%

151%

144%

141%

OceanaGold Corporation (ASX:OGC)

Perseus Mining Ltd. (ASX:PRU)

Lynas Corp. Ltd. (ASX:LYC)

Anvil Mining Limited (TSX:AVM)

Grange Resources Limited (ASX:GRR)

Indophil Resources NL (ASX:IRN)

Brockman Resources Limited (ASX:BRM)

White Energy Company Limited (ASX:WEC)

Citadel Resource Group Limited (ASX:CGG)

The 10 mid-tier 50 companies with increase in market capitalisation

Table 5: 10 largest increases in Market Capitalisation mid-tier 50 between 30 June 2009 and 30 June 2010Source: Capital IQ

USD Gold/oz AUD Gold/oz AUD/USD exchange rate

0.00

200

400

600

800

1000

1200

1400

1600

1800

0.600

0.800

$/oz

AU

D t

o U

SD

1.00011% increase AUD

50% increase USD

35% appreciation AUD to USD

Jan-

09

Feb-0

9

Mar

-09

Apr-09

May

-09

Jun-

09

Jul-0

9

Aug-0

9

Sep-0

9

Oct-0

9

Nov-0

9

Dec-0

9

Jan-

10

Feb-1

0

Mar

-10

Apr-10

May

-10

Jun-

10

Jul-1

0

Aug-1

0

Sep-1

0

Oct-1

0

AUD and USD Gold price per oz and AUD to USD exchange rate

Table 4: AUD and USD gold per oz and AUD:USD exchange rate – January 2009 to October 2010Source: Capital IQ

Aussie Mine November 2010 9

3.2 Comparison of the mid-tier 50 to other performance measures In our November 2009 publication we investigated whether the significant fluctuations in mid-tier 50 market capitalisations were anomalies specific to the Australian economy. We noted that flailing market conditions and poor commodity prices for base metals resulting from the global economic downturn impacted resource companies across the world, with the three comparative indices (ASX 300 Metals and Mining, FTSE 350 Mining Index and TSX Global Mining Index) all virtually mirroring each other in a downward trend, finishing approximately 20% below June 2008 levels.

In 2010, this downward trend has been reversed, with all three key indexes increasing by more than 15% as commodity prices have bounced back towards pre-global economic downturn levels and optimism has crept back into the mining sector globally. The resilience of the Chinese economy and continued potential of Brazil, Russia, India and developing nations, has maintained or increased demand for our commodities to record levels, and this demand side influence has helped to pull the mining markets out of the price depression caused by the global economic downturn.

Recent data reveals that the best performing market over the 12 months to June 2010 has been the FTSE 350 Mining index (FTSE 350), which has increased 32% compared to 27% and 15% for the TSX Global Mining Index (GMI) and ASX 300 Metals and Mining (ASX 300 M&M) respectively.

In the three months post June 2010, these markets have continued to rally with the FTSE 350 and GMI both increasing a further 25%. This compares to only a 13% increase for the ASX300 M&M. Australian listed mining companies are lagging when compared to their global peers. The question is, ‘Why is this the case when we consider that headline commodity prices are strong and we are a commodity supplier’? Is it the strength of the A$? Or is it the fact that other markets have become more attractive to investors given the lack of certainty around key issues in the Australian mining industry such as the resource tax and emissions reduction?

One possible issue that may have had an impact on the performance the Australian Market in 2010 has been the controversial plan to impose a new tax regime on Australian mining operations. The media coverage the RSPT generated was astounding. Indeed the political landscape from the time it was announced has been fascinating.

As already stated, the Australian mining index has lagged behind that of Canada and the UK over the past 18 months. This is not what Australian investors want to see. We also note that foreign investors view Australia as having blotted its copy book this year by announcing the RSPT. Clearly investors do not like uncertainty and question marks over taxes, carbon prices and industrial relations policy may keep a lid on some of the ambitions of the miners and their share price.

With the growth in commodity prices and strong continued demand from Asia’s industrialising economies we can expect to see demand for investment in the mid-tier 50 continue to rise. The Australian miners and the market look set to benefit if a suitable resolution with respect to the MRRT can be brokered, despite the challenge of a minority government to effect change within this parliamentary term.

All of this points to the Australian mid-tier being undervalued against the global counterparts, indicating there is a long way further to rise and shine.

S&P/ASX 300 Metals and Mining - Index Value FTSE 350 Mining Index S&P/TSX Global Mining Index - Index Value

57% FTSE

32% FTSE 35027% TSX GMI15% ASX M&M

52% TSX GMI

28% ASX M&M

0.80

1.00

1.20

1.40

1.60

1.80

Jul-09 Aug-09 Sep-09 Oct-09 Nov-09 Dec-09 Jan-10 Feb-10 Mar-10 Apr-10 May-10 Jun-10 Jul-10 Aug-10 Sep-10

Comparison of key mining indices

S&P/ASX 300 Metals & Mining - Index Value

2 weeks prior to RSPT announcement RSPT announcement

MRRT announcement

Australian election

2500

3000

3500

4000

4500

5000

5500

Jul-09 Aug-09 Sep-09 Oct-09 Nov-09 Dec-09 Jan-10 Feb-10 Mar-10 Apr-10 May-10 Jun-10 Jul-10 Aug-10 Sep-10

S&P/ASX 300 Metals and Mining – Index Value

Table 6: Comparison of key mining indices July 2009 – September 2010 (July 2009 =1)Source: Capital IQ

Table 7: S&P/ASX 300 Metals and Mining index July 2009 to September 2010Source: Capital IQ

10 PwC

3.3 M&A–fromnecessityto opportunityM&A activity in the mid-tier 50 shifted focus from being a necessity in the latter part of 2008 and the early half of 2009, to opportunity in 2010. The necessity was driven by declining commodity prices and lack of access to debt and equity markets forcing a number of companies to transact to survive. M&A activity became an alternative means of accessing cash in order to ensure survival during the GFC.

Since then, commodity prices have rebounded, credit is more forthcoming as optimism slowly returns to the market and companies have sured up their balance sheets through capital raisings totalling $29.7 billion. The mid-tier 50 holds $7.3 billion of cash on hand, indicating that there is an opportunity for many companies to capitalise on investment opportunities as they arise both in transactions and through funding organic growth. Mid-tier 50 must learn the lessons of the high impairment charges incurred last year in consideration of future opportunities.

There is still strong demand from overseas investors, notably China, however there have been two pivotal changes to the M&A environment since early 2009. Firstly, the strengthening A$ has made Australian assets more expensive. Secondly, there is now competition from within Australia. In late 2008 and early 2009, there was very limited M&A price tension from within the mid-tier 50 (as reported in our November 2009 publication). By contrast, in the current climate, with significant cash reserves and lower debt levels that now characterise many mid-tier 50 companies, M&A activity is back on the agenda.

Deals since June 2009

Since June 2009, the mid-tier 50 companies were named in 35 potential transactions, totalling $30.9 billion; of which approximately 30% have been completed. The average deal value since June 2009 is $875 million, largely consistent with our November 2009 publication where the average was $890m. The more notable difference is that the number of transactions have increased significantly from 10 in our November 2009 publication to 35 in the current year. This increase has been driven by two significant shifts in the M&A activity.

The first is that there are more Australian based companies entering into M&A transactions. The M&A activity by mid-tier companies was not evident in our November 2009 publication which is in stark contrast against the current year where the deal value of M&A activity by Australian mid-tier companies, in their capacity as bidders, and not targets, is $6.8 billion. This alone represents approximately 75% of all M&A activity (by value) across the mid-tier 50 in the previous year.

The second important factor is that M&A activity continued unabated post the announcement on 2 May 2010 of the Resource Super Profits Tax (RSPT), now rebranded as the Mineral Resource Rent Tax (MRRT). Acquiring entities compensated for the uncertainty surrounding changes to the tax regime by reflecting the additional risk in the bid price; thereby reducing it. The most significant example of this was Peabody Energy’s bid for Macarthur Coal. Peabody Energy announced a $16 per share bid for Macarthur Coal in April 2010, which was rejected by the target. Following this failed bid, a second attempt was launched at $15 per share in May 2010 on the claim that uncertainty surrounding the RSPT had impacted the bid price. This offer was rejected by Macarthur’s board and major shareholders.

The most significant completed acquisition of a mid-tier 50 company since June 2009 was Yanzhou’s $3.4 billion acquisition of Felix Resources in August 2009.

M&A activity continued unabated post the announcement on 2 May 2010 of the Resource Super Profits Tax (RSPT), now rebranded as the Mineral Resource Rent Tax (MRRT). Acquiring entities compensated for the uncertainty surrounding changes to the tax regime by reflecting the additional risk in the bid price; thereby reducing it.

The most significant completed acquisition of a mid-tier 50 company since June 2009 was Yanzhou’s $3.4 billion acquisition of Felix Resources in August 2009.

Aussie Mine November 2010 11

Completed M&A activity in the mid-tier 50, greater than A$15 million.

Target Acquirer Acquirer countryof origin

Ownership interest

Approximate deal value (A$m)

Announcement date

Status

Felix Resources Limited Yanzhou Coal Mining Co Ltd

China 100.0% 3,393 13/08/2009 Completed

Aquila Resources Limited Vale Belvedere Pty Ltd Brazil 24.5% 1,991 4/06/2010 Completed

Centennial Coal Company Limited

Banpu Minerals (Singapore) Pte Ltd

Thailand 100.0% 1,958 5/07/2010 Completed

Middlemount JV Gloucester Coal Limited Australia unknown interest 472 4/08/2010 Completed

Aquila Resources Limited Baoshan Iron & Steel Company Ltd

China 14.3% 289 28/08/2009 Completed

Riversdale Mining Limited Companhia Siderurgica Nacional (CSN)

Brazil 16.3% 190 24/11/2009 Completed

Mt Gibson Iron Limited Fushan International Energy Group Ltd

Hong Kong 14.3% 178 22/09/2009 Completed

Aurox Resources Limited Atlas Iron Limited Australia Merger 143 10/03/2010 Completed

Polaris Metals NL Mineral Resources Limited

Australia 100.0% 136 20/08/2009 Completed

Dioro Exploration NL Avoca Resources Australia 100.0% 115 29/12/2009 Completed

Sandfire Resources NL Oz Minerals Limited Australia 19.0% 100 2/07/2010 Completed

Warwick Resources Limited

Atlas Iron Limited Australia Merger 56 8/09/2009 Completed

Medusa Mining Limited

Metalloinvest Holding Russia 10.0% 54 11/11/2009 Completed

Indophil Resources NL

San Miguel Corp Philippines 10.0% 41 8/10/2010 Completed

Barrick (PD) Australia Ltd

Ivanhoe Australia Limited

Australia Osborne Copper Gold Asset

17 25/05/2010 Completed

Total 9,133

Table 8: Completed M&A activity in the mid-tier 50 between June 2009 and October 2010 greater than A$15 millionSource: mergermarkets

12 PwC

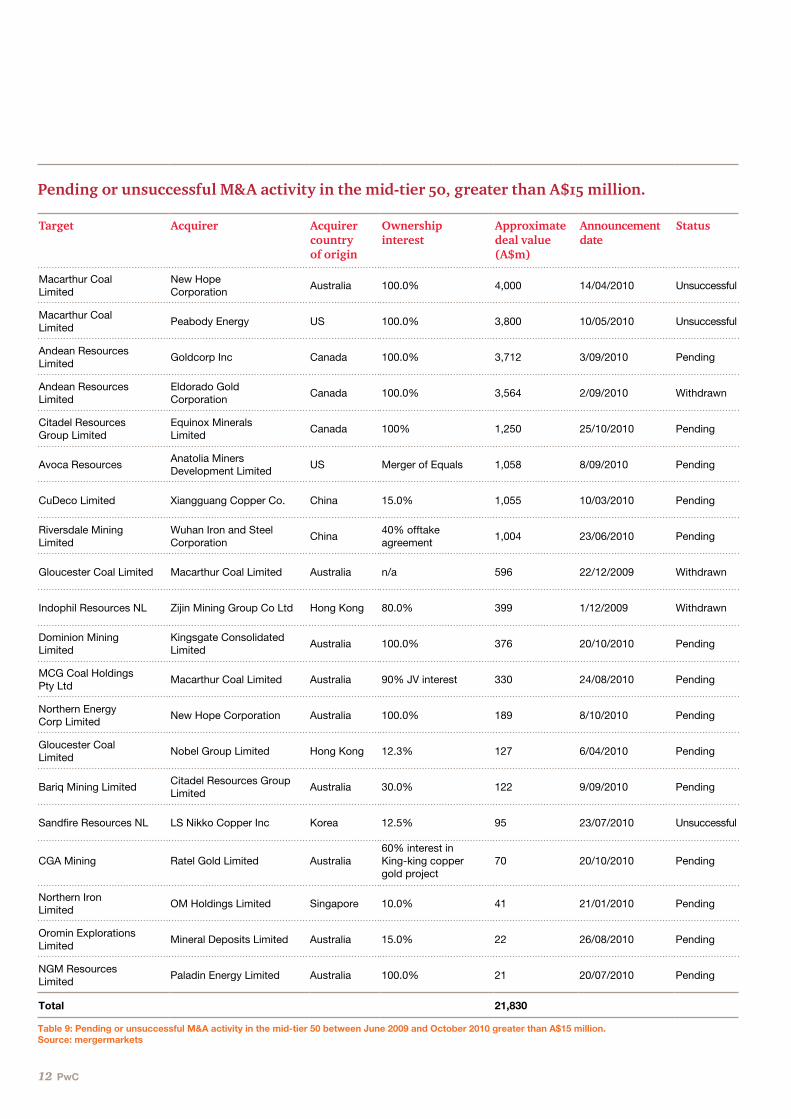

Pending or unsuccessful M&A activity in the mid-tier 50, greater than A$15 million.

Target Acquirer Acquirer countryof origin

Ownership interest

Approximate deal value (A$m)

Announcement date

Status

Macarthur Coal Limited

New Hope Corporation

Australia 100.0% 4,000 14/04/2010 Unsuccessful

Macarthur Coal Limited

Peabody Energy US 100.0% 3,800 10/05/2010 Unsuccessful

Andean Resources Limited

Goldcorp Inc Canada 100.0% 3,712 3/09/2010 Pending

Andean Resources Limited

Eldorado Gold Corporation

Canada 100.0% 3,564 2/09/2010 Withdrawn

Citadel Resources Group Limited

Equinox Minerals Limited

Canada 100% 1,250 25/10/2010 Pending

Avoca Resources Anatolia Miners Development Limited

US Merger of Equals 1,058 8/09/2010 Pending

CuDeco Limited Xiangguang Copper Co. China 15.0% 1,055 10/03/2010 Pending

Riversdale Mining Limited

Wuhan Iron and Steel Corporation

China 40% offtake agreement

1,004 23/06/2010 Pending

Gloucester Coal Limited Macarthur Coal Limited Australia n/a 596 22/12/2009 Withdrawn

Indophil Resources NL Zijin Mining Group Co Ltd Hong Kong 80.0% 399 1/12/2009 Withdrawn

Dominion Mining Limited

Kingsgate Consolidated Limited

Australia 100.0% 376 20/10/2010 Pending

MCG Coal Holdings Pty Ltd

Macarthur Coal Limited Australia 90% JV interest 330 24/08/2010 Pending

Northern Energy Corp Limited

New Hope Corporation Australia 100.0% 189 8/10/2010 Pending

Gloucester Coal Limited

Nobel Group Limited Hong Kong 12.3% 127 6/04/2010 Pending

Bariq Mining Limited Citadel Resources Group Limited

Australia 30.0% 122 9/09/2010 Pending

Sandfire Resources NL LS Nikko Copper Inc Korea 12.5% 95 23/07/2010 Unsuccessful

CGA Mining Ratel Gold Limited Australia 60% interest in King-king copper gold project

70 20/10/2010 Pending

Northern Iron Limited

OM Holdings Limited Singapore 10.0% 41 21/01/2010 Pending

Oromin Explorations Limited

Mineral Deposits Limited Australia 15.0% 22 26/08/2010 Pending

NGM Resources Limited

Paladin Energy Limited Australia 100.0% 21 20/07/2010 Pending

Total 21,830

Table 9: Pending or unsuccessful M&A activity in the mid-tier 50 between June 2009 and October 2010 greater than A$15 million.Source: mergermarkets

Aussie Mine November 2010 13

Completed: Yanzhou Coal Mining Co Ltd acquired Felix Resources Limited for

A$3.4bn Completed: Vale Belvedere Pty Ltd acquired 24% of Aquila Resources Limited for

Completed: Banpu Minerals (Singapore) Pte Ltd acquired Centennial Coal Company Limited for

Pending: Xiangguang Copper Co. acquiring CuDeco Limited forPending:

Wuhan Iron and Steel Corporation acquiring Riversdale Mining Limited for

A$2bn A$2bn

A$1.1bn

Pending: Goldcorp Inc acquiring Andean Resources Limited for

Pending: Anatolia Miners Development Limited merging with Avoca Resources for

A$3.7bn

A$1.1bn

A$1bn

Pending: Equinox Minerals Limited acquiring Citadel Resources Group Limited for

A$1.3bn

14 PwC

3.4Movements in the mid-tier 50Mixed bag of new entrants – growth across the board

The new entrants into this year’s analysis represent a diverse range of commodity groups including gold, copper, iron ore and coal. There has been strong growth across the sector and gold plays stand-out. Companies such as Perseus Mining Ltd, OceanaGold Corporation, Sandfire Resources and Resolute Mining Ltd have all entered our list – as strong growth in market cap has been delivered following further exploration of deposits and a surge in underlying gold prices. All up there were 11 new entrants in 2010.

Exits from the mid-tier are primarily driven by volatility in market capitalisations of the smaller end of the list. However, three significant exits for other reasons are noteworthy. The takeover of Felix Resources by Yanzhou Coal and the takeover of Sino Gold by Eldorado Gold Corp continues the theme of foreign interest which was noted in last year’s publication. The third exit is by Centamin Egypt who chose to de-list from the ASX and maintain LSE and TSX listing.

Despite market capitalisation for the mid-tier 50 increasing in aggregate by over 35% from June 2009 over the course of the 2010 financial year none of the companies included in last year’s publication have grown beyond our $5 billion ceiling for inclusion in the mid-tier 50. There continues to be a pronounced separation between the big end of town and the largest company by market capitalisation in our analysis, which is Alumina Ltd at $3.7 billion. BHP Billiton, Rio Tinto, Newcrest, Coal & Allied and Fortescue Metals continue to be excluded from the list on the basis that their market capitalisation exceeded the $5 billion threshold.

The new entrants into this year’s analysis represent a diverse range of commodity groups including gold, copper, iron ore and coal.

Aussie Mine November 2010 15

The way I see itNicole Hollows – Chief Executive Officer andManaging Director of Macarthur Coal Limited

4

The industry may have done better to own these assets if the primary goal of QR is to maximise return rather than to invest in the industry’s expansion requirements.

AussieMine(AM): Macarthur’s 2010 earnings were better than expected, primarily due to additional tonnage from earlier ship loading than planned, what is Macarthur’s strategy for coping with infrastructure constraints going forward and how do you see the broader infrastructure challenges facing Australian miners being resolved?

Nicole Hollows (NH): MCC strategy is based on operational excellence and sustainable growth with 9.2mtpa by 2014. Sustainable growth is achievable at MCC as we have a strong pipeline for organic growth and expect to announce our fourth mine project by the end of the year.

Access to infrastructure is an ongoing issue in our industry which is why it is part of our strategy at MCC to look at ways to diversify three key areas: port, product and geographical location. The time it takes to secure port and rail access is often longer than it takes to develop a mine, so we have taken a long term approach to securing access to support our current and future mine sites.

In order to resolve the infrastructure challenges faced by Australian miners, it will be necessary to secure investment in expansion of the ports and rail networks to ensure they keep pace with demand for Australia’s exports – particularly coal. The impact of infrastructure constraints on the Australian coal industry is felt by the mining companies, their customers and shareholders. The industry is aware of the challenges ahead and hopes that the state and federal government can work towards a cohesive national infrastructure network.

AM: Do you see the sale of Queensland Rail impacting the current rail landscape in the medium term?

NH: There are two aspects that need to be discussed in relation to this. Firstly, the potentially diverging interests between QR and industry in the medium term. In short, we expect that the sale of the integrated coal business, train and tracks, will lead the new owners to sweat the asset harder and for longer in order to maximise their investment return, rather than investing to meet the industry’s expansion requirements. As a result we expect that in the short to medium term we will see the fallout of that approach – further constraints on the coal chain from delayed investment and potentially higher costs given the influence QR will have over above and below rail costs.

The industry may have done better to own these assets if the primary goal of QR is to maximise return rather than to invest in the industry’s expansion requirements. The undesired impact of mining companies owning infrastructure, however, is that it will prove to be a significant barrier to entry. This is particularly the case for the smaller companies as not many other investors would be willing to take these significant risks so early on.

The second aspect is that, despite regulation, the integration of trains and track is also of concern in how the daily operation is executed, given that there are now other rail operators. From November this year, MCC will have 100% of its above rail business with Pacific National, resulting in a disconnect between above rail operators and below rail operators. On a positive side, the fact that QR will be public will give rise to public scrutiny on their investments, just like us. We hope that such pressure will encourage QR to pursue growth investments at reasonable returns. The potential solution towards effective integration is to move towards a requirement to buy port and rail capacity together, rather than allow it to be done in isolation.

16 PwC

AM: Talk of carbon tax has recently returned to the political arena, Keith De Lacy (Macarthur Chairman) has recently expressed some concern over reducing the competitiveness of efficiently mined, high calorific Australian coal compared with less efficient foreign sources, what is your view of the best way forward on emissions?

NH: First of all it should be noted that the industry, as a whole, is supportive of reducing emissions. The key issue has become how this should be done. We believe that an approach towards an effective emissions reduction scheme should be transitional, practical and internationally competitive. Companies should be incentivised, by way of an offset, to invest in technologies that reduce emissions because currently the only method for reducing emissions is to reduce output. Reducing output is not only unpractical and devastating to the Australian economy, but there is no evidence to indicate this method would lessen emissions on a global scale. This is because Australia, in general, exports high quality coal which allows lower quantities to be used in a blast furnace to manufacture steel. If an emissions reduction scheme were imposed and output in Australia were to be cut back, the developing countries would simply source additional coal to fill the supply gap from other countries with a lower quality coal, thereby increasing the quantity required to make the same amount of steel. This would ultimately increase the intensity of emissions on a global scale.

AM: What do you see as the main challenges and unresolved areas of MRRT in its current form?

NH: I think we can all agree that the MRRT is an improvement from the previously disastrous RSPT. Having said that, it is critical not to underestimate the complexity of a resources rent tax. The petroleum industry tax still has issues that require attention and they have had twenty years to hammer out the detail. The issues that we face with the MRRT can be split into two components:

1. The lack of clarity. Importantly there is no clarity over the definition of a project, including the ability to transfer profits and costs, the taxation point or valuation methodologies. Furthermore there is no real clarity as to whether this is a resource rent tax or a profits tax. We currently pay around 42-43% effective tax and it is important for the government to realise that we need to remain internationally competitive if the industry is to continue to provide a revenue

stream for government and fund future growth and jobs. The discussions around the detail of the tax are showing some inconsistencies around the point at which the value of the product is determined compared to the point at which costs are eligible as deductions

2. The additional administration burden. This will particularly be felt by the smaller companies who do not initially fall under the MRRT but need to keep records in the event that their profits reach a level where they are required to pay.

AM: There has been a large amount of M&A activity impacting Macarthur and your competitors this past year. Do you expect this to continue and do you see any change to the types of buyers involved in these transactions?

AM: International demand for coal has been particularly strong, are there any particular trends emerging or shifts in demand that you see?

NH: We continue to see growth in demand from the developing countries particularly China, Brazil and India. Steel production is now at pre-GFC levels, with over half the increase in demand stemming from China to fuel their urbanisation and infrastructure programs. Incidentally China has now become a net importer rather than exporter of metcoal, importing 40 mtpa (whilst the whole seaborne metcoal trade is approximately 250 mtpa).

Globally, steel industry customers are increasingly able to take PCI coal as a cost effective means of reducing the amount of coking coal required for the blast furnaces and this will result in ongoing growth in the PCI coal market. We expect ageing coke ovens and blast furnace expansions to create stronger differential growth for LV PCI coal.

NH: Our focus is on organic growth, but we will consider acquisitions where they align with the business strategy and our focus on sustainable growth. MCC would now consider offshore investment if aligned to strategy. This decision has primarily been driven by the increased regulation and approval process in Australia. There is nothing wrong with the regulation, the issue becomes how it is rolled out from a cost and time perspective. Currently in Australia, the process to obtain a mining licence can take between four to five years which is quite significant. There has also been a shift of costs in Australia, previously Australia was considered a low cost area, currently with the increasing infrastructure and labour costs, this is no longer the case.

In terms of the buyers involved in the M&A transactions, we expect to see more users and sovereign type investors. Examples of these at MCC are POSCO and the CITIC group respectively. The reasons behind the increased interest are to secure supply and to gain better access to the Australian market. Mining companies will also need size and scale to marry up with the large infrastructure commitments required to get product from the mine to the market.

AM: There has recently been a push by the Australian Institute of Company Directors to boost female board representation. Do you think more should be done in this area and how do you think more balance may be achieved?

NH: I am an advocate of creating a pipeline for talent rather than relying on quotas at the end point. At MCC we have 33% female executives and over 40% female managers and that makes it easier to achieve diversity at the senior levels of the organisation.

Lifestyle choices have previously played a significant part in the low levels of female representations at the board level. In the age of high cost and inflexible childcare costs it was generally accepted for a parent, usually the female, to stay at home and care for their children. This mindset, however, is slowly changing and the choice to stay at home is now an economic decision; with the parent with the best earning capacity continuing to work.

NH: If an emissions reduction scheme were imposed and output in Australia were to be cut back, the developing countries would simply source additional coal to fill the supply gap from other countries with a lower quality coal, thereby increasing the quantity required to make the same amount of steel.

Aussie Mine November 2010 17

We currently pay around 42-43% effective tax and it is important for the government to realise that we need to remain internationally competitive if the industry is to continue to provide a revenue stream for government and fund future growth and jobs.

Lastly, in order to address this lack of female board representation, it is important for women to learn to be less cautious in taking on new opportunities. There is some evidence that suggest women wait until they feel 100% capable of stepping up rather than accepting that some of the skills needed will be learnt on the job.

AM: In your role as the President of the QRC what are the big issues on your radar - aside from infrastructure and MRRT?

NH: There are several national priorities currently on our radar. Firstly, the national health and safety harmonisation agenda is a key issue. Locally, the challenge is that the Queensland Government is determined to retain local mine safety laws. There are clearly also local concerns relating to the inadequacies of the current industry input to governance of the health and safety system. Secondly, energy and climate change policy has previously been an issue on our radar. While possibly on the backburner at present, it is an issue that is expected to loom large on the national agenda after the next federal election. Lastly, skills, education and training is a core issue. The national context is the impending report of the National Resource Sector Employment Taskforce.

AM: What do you see as the main opportunities and challenges facing the wider Australian mid-tier mining industry?

NH: The main challenge facing this industry is the cost and access to skilled labour. If all projects are given the green light (the CSG projects in Gladstone, LNG projects in North Western Shelf and the Rio Tinto project in Pilbara) there would be a further and significant tightening in skilled labour availability. The key here is to ensure appropriate education and training for young Australians. This can be done through various channels such as increased trade based education in schools in conjunction with practical industry training. Not only would this assist to alleviate the skills shortage, but it also means that the young Australians are better equipped for the workforce as a result of their education gained at school and their practical experience gained from the industry.

Other challenges in the industry relate to access to capital, securing infrastructure and being able to make the financial commitments to secure long term access. Managing the continuous increase in costs (as a result of carbon taxes, MRRT, regulatory changes, labour costs, the list continues!).

At MCC we have 33%

female executives and over 40% female managers and that makes it easier to achieve diversity at the senior levels of the organisation.

The key opportunity that faces this industry is the strong long term demand for Australian products. Furthermore, the investment in the infrastructure at Wiggins Island Port and the rail development will ensure continued growth in this industry.

The key opportunity that faces this industry is the strong long term demand for Australian products. Furthermore, the investment in the infrastructure at Wiggins Island Port and the rail development will ensure continued growth in this industry.

18 PwC

2010 A$m

2009 A$m

Change %

Revenue from ordinary activities

- Operating revenue 11,317 8,561 32%

- Non-operating revenue 197 391 (50%)

Total Revenue 11,513 8,952 29%

Less expenses from ordinary activities (8,639) (6,108) 41%

Exploration expenses (378) (456) (17%)

Operating Expenses (9,018) (6,564) 37%

Gross Profit 2,496 2,388 5%

Other income/ (expenses) (141) 124 (214%)

Adjusted EBITDA 2,355 2,512 (6%)

Gain / (loss) on sale of investments (354) 487 (173%)

Impairment (111) (1,738) (94%)

EBITDA 1,890 1,262 50%

Depreciation and amortisation (1,134) (796) 43%

EBIT 756 466 62%

Net interest expense (359) (382) (6%)

Profit from ordinary activities before tax 397 84 373%

Income tax expense (423) (706) (40%)

Net Profit / (Loss) (26) (622) 96%

RevenueTop five mid-tier companies by revenue:

CompanyName 2010 A$m

2009 A$m

Change %

1 Centennial Coal 808 895 (10%)

2 Energy Resources Australia 773 685 13%

3 New Hope 745 701 6%

4 Macarthur Coal 681 762 (11%)

5 OZ Minerals / Oxiana 609 01 100%

1) Nil revenue recognised in 2009 as a result of the sale of certain assets to Minmetals. The assets have been classified as discontinued operations and therefore not included in the revenue from continuing operations result. 2010 revenue is from Prominent Hill.

Aggregated industry income statement

5

Aussie Mine November 2010 19

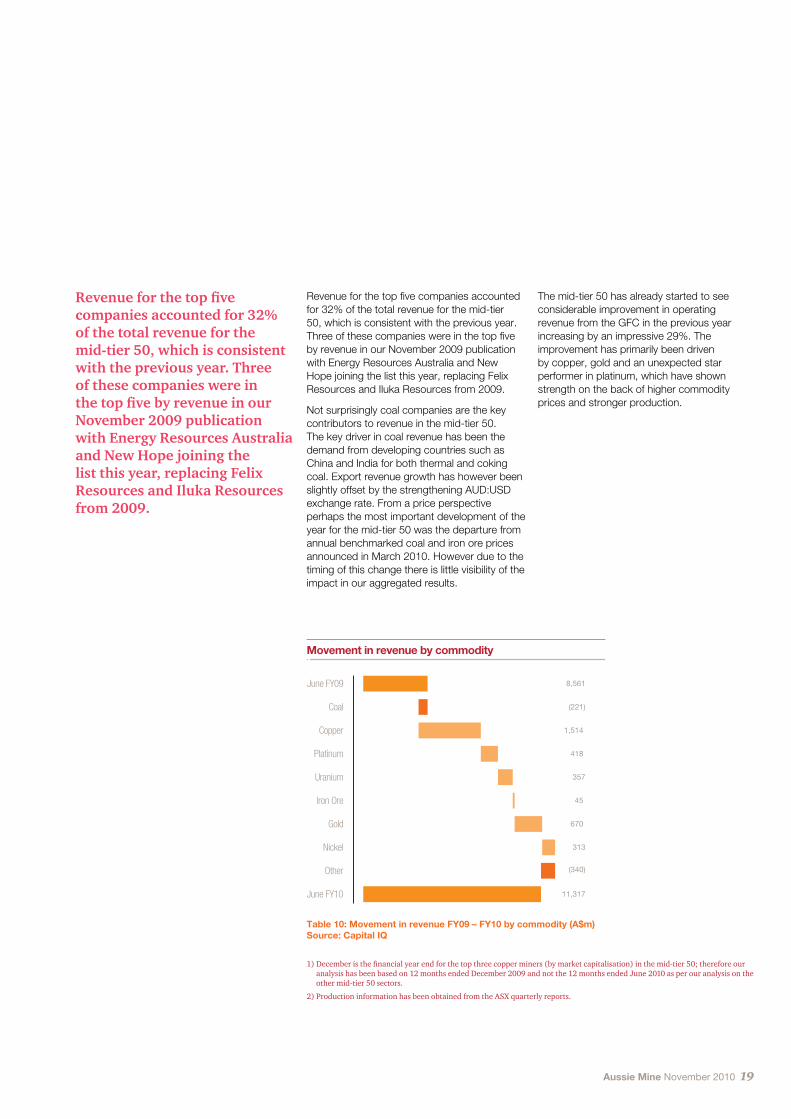

Revenueforthetopfivecompanies accounted for 32% of the total revenue for the mid-tier 50, which is consistent with the previous year. Three of these companies were in thetopfivebyrevenueinourNovember2009publication withEnergyResourcesAustraliaandNewHopejoiningthelist this year, replacing Felix ResourcesandIlukaResources from 2009.

Revenue for the top five companies accounted for 32% of the total revenue for the mid-tier 50, which is consistent with the previous year. Three of these companies were in the top five by revenue in our November 2009 publication with Energy Resources Australia and New Hope joining the list this year, replacing Felix Resources and Iluka Resources from 2009.

Not surprisingly coal companies are the key contributors to revenue in the mid-tier 50. The key driver in coal revenue has been the demand from developing countries such as China and India for both thermal and coking coal. Export revenue growth has however been slightly offset by the strengthening AUD:USD exchange rate. From a price perspective perhaps the most important development of the year for the mid-tier 50 was the departure from annual benchmarked coal and iron ore prices announced in March 2010. However due to the timing of this change there is little visibility of the impact in our aggregated results.

8,561

(221)

1,514

418

45

357

670

313

(340)

11,317

June FY09

Coal

Copper

Platinum

Uranium

Iron Ore

Gold

Nickel

Other

June FY10

Movement in revenue by commodity

The mid-tier 50 has already started to see considerable improvement in operating revenue from the GFC in the previous year increasing by an impressive 29%. The improvement has primarily been driven by copper, gold and an unexpected star performer in platinum, which have shown strength on the back of higher commodity prices and stronger production.

Table 10: Movement in revenue FY09 – FY10 by commodity (A$m) Source: Capital IQ

1) December is the financial year end for the top three copper miners (by market capitalisation) in the mid-tier 50; therefore our analysis has been based on 12 months ended December 2009 and not the 12 months ended June 2010 as per our analysis on the other mid-tier 50 sectors.

2) Production information has been obtained from the ASX quarterly reports.

20 PwC

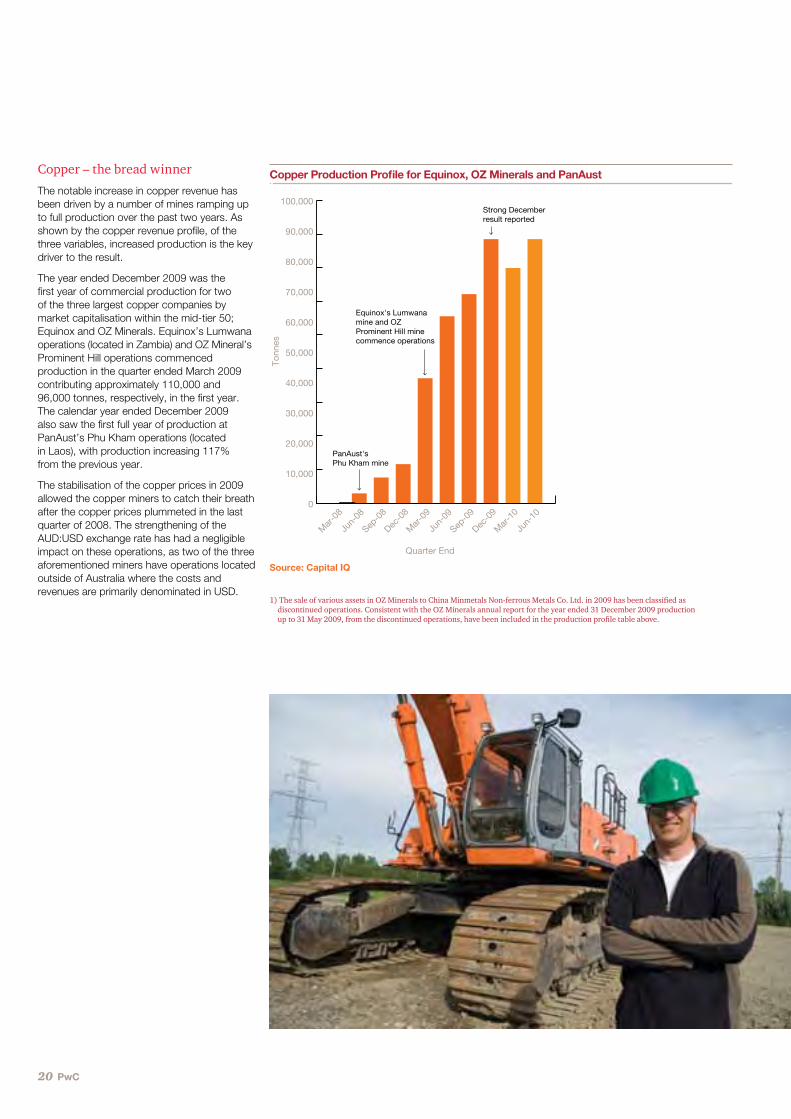

Copper – the bread winner

The notable increase in copper revenue has been driven by a number of mines ramping up to full production over the past two years. As shown by the copper revenue profile, of the three variables, increased production is the key driver to the result.

The year ended December 2009 was the first year of commercial production for two of the three largest copper companies by market capitalisation within the mid-tier 50; Equinox and OZ Minerals. Equinox’s Lumwana operations (located in Zambia) and OZ Mineral’s Prominent Hill operations commenced production in the quarter ended March 2009 contributing approximately 110,000 and 96,000 tonnes, respectively, in the first year. The calendar year ended December 2009 also saw the first full year of production at PanAust’s Phu Kham operations (located in Laos), with production increasing 117% from the previous year.

The stabilisation of the copper prices in 2009 allowed the copper miners to catch their breath after the copper prices plummeted in the last quarter of 2008. The strengthening of the AUD:USD exchange rate has had a negligible impact on these operations, as two of the three aforementioned miners have operations located outside of Australia where the costs and revenues are primarily denominated in USD.

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

100,000

Mar

-08

Jun-

08

Sep-0

8

Dec-0

8

Mar

-09

Jun-

09

Sep-0

9

Dec-0

9

Mar

-10

Jun-

10

Quarter End

Tonn

es

PanAust'sPhu Kham mine

Equinox's Lumwanamine and OZProminent Hill minecommence operations

Strong Decemberresult reported

Copper Production Profile for Equinox, OZ Minerals and PanAust

1) The sale of various assets in OZ Minerals to China Minmetals Non-ferrous Metals Co. Ltd. in 2009 has been classified as discontinued operations. Consistent with the OZ Minerals annual report for the year ended 31 December 2009 production up to 31 May 2009, from the discontinued operations, have been included in the production profile table above.

Source: Capital IQ

Aussie Mine November 2010 21

Gold

During the year, gold producers continued to be one of the stand out performers in the mid-tier 50; weathering the effects of the GFC and the continually strengthening AUD:USD exchange rate. The increase in production, particularly for offshore gold producers, has been the driver in gold revenues. The improvement in the US$ gold price throughout the year indicates that it is once again returning to favour as a relatively secure store of wealth.

The increase in output resulted from the steady ramp-up of production in Australia and the commencement of a number of operations offshore. Mid-tier 50 gold mining companies with operations in Australia have, in aggregate, increased output by 21% with notable increases from Avoca Resources (73%). Avoca Resources increased production through a combination of organic growth (primarily through the Trident resource at Higginsville during the quarter ended June 2009) and through their acquisition of Dioro Exploration NL in December 2009. The increase in output from Australian based operations, are however, marginally offset by the strengthening AUD:USD exchange rate.

Offshore gold operations continued to show strong growth throughout the year ended 2010; primarily driven by start up operations at two mine sites. Mine sites for CGA and Mineral Deposits commenced offshore operations in the Philippines and West Africa respectively in the quarter ended June 2009. During their first full year of production CGA produced approximately 150,000oz of gold whilst Mineral Deposits produced approximately 172,000oz of gold. Offshore operations have increased, in aggregate, by 62% from FY09 with OceanaGold Corporation contributing nearly 35% of offshore production in FY10.

The continuous upward trend in gold prices during the year has also contributed to the success of companies within this sector of the mid-tier 50. This increase in the USD price for gold, as previously noted, has been offset by the strengthening AUD:USD exchange rate over the same period for companies that operate within Australia.

1,381

531

256

(149)

2,020

Jun-09

Production

Price

FX

Jun-10

Gold Revenue Profile (A$m)

1) Production information has been obtained from the ASX quarterly reports. The movement in the annual reports taken from the ASX is marginally different to the movement as per the quarterly reports.

Source: Capital IQ

Quarter End

oz

50,000

0

100,000

150,000

200,000

250,000

Sep-0

8

Dec-0

8

Mar

-09

Jun-

09

Sep-0

9

Dec-0

9

Mar

-10

Jun-

10

Gold Produced offshore Gold Produced locally

Gold Production – Local vs Offshore

1) Production information has been obtained from the ASX quarterly reports. The movement in the annual reports taken from the ASX is marginally different to the movement as per the quarterly reports.

Source: Capital IQ

22 PwC

The unexpected star performer

Platinum has been spurred on by the consistently improving price, compounded by the increase in production by the two largest platinum producers in the mid-tier 50. Aquarius Platinum (operations located in South Africa and Zimbabwe) and Zimplats (operations located in Zimbabwe) both showed strong revenue growth, increasing 29% and 185% respectively. The surge in revenue at Zimplats saw it catapult to third position in the top five mid-tier 50 performers based on net profit. Platinum production increased at Zimplats by 84% whilst the price of platinum increased 86% from FY09, contributing to its success during the year. The revenues recognised from the increased output and the improving US$ price was not affected by the strengthening A$ as both companies have operations outside Australia.

Commodity AUD average spot price

movement (July2009–

June 2010)

AUD average spot price

movement (July2010–

Sept 2010)

USD average spot price

movement (July2009–

June 2010)

USD average spot price

movement (July2010–

Sept 2010)

Copper 17% 6% 35% 8%

Gold 4% 10% 25% 12%

Nickel 24% 7% 45% 9%

Table 12: Commodity price movementsSource: Capital IQ

0.50

0.60

0.70

0.80

0.90

1.00

1.10

Jul-0

8

Aug-0

8

Sep-0

8

Oct-0

8

Nov-0

8

Dec-0

8

Jan-

09

Feb-0

9

Mar

-09

Apr-09

May

-09

Jun-

09

Jul-0

9

Aug-0

9

Sep-0

9

Oct-0

9

Nov-0

9

Dec-0

9

Jan-

10

Feb-1

0

Mar

-10

Apr-10

May

-10

Jun-

10

Jul-1

0

Aug-1

0

Sep-1

0

Average rate FY09 is 0.7473Average rate for quarter ended

September 2010 is 0.9046

Average rate for FY10 is 0.8824

AU

D

AUD vs USD price fluctuations

Table 11: AUD vs USD exchange rate – July 2008 to October 2010Source: Bloomberg

Foreign exchange – saviour to villain

The weak A$ reduced the impact of declining metals prices during the global economic downturn in the previous year. Post-GFC, however, the continually strengthening AUD:USD exchange rate is starting to erode the potential heights in the top line results of Australian based mining companies across the board.

The relatively strong performance of companies in the copper, gold and platinum sectors may be attributed to the fact that nine of the twenty one companies have operations located outside Australia (the largest proportion across the sectors); therefore the revenues have not been adversely affected by the strengthening A$.

In US$ terms we have witnessed increases in commodity prices during the quarter ended September 2010 which has been sparked by a revival in prospects for the global economy and continued weakness in the US. This partly reflects low interest rates, which have fuelled the appetite for risk, and speculation regarding near-term supply. China has been the main driver of recent demand growth with a seemingly insatiable appetite for commodities. The key question remains – if China’s demand growth slows, will growth in the rest of the world be sufficient to prevent the market from moving back into surplus? India may prove to be the answer to this question, but perhaps more likely this question will never actually get asked as China maintains its long-term goals and continues to grow.

One can only wonder at the returns that may have been generated by Australian based operators had they entered into hedge agreements when the A$ was at 67 cents to the US$ as it was during the quarter ended December 2008…

Aussie Mine November 2010 23

Margin Squeeze

Consistent with the revenue analysis, the increase in costs from ordinary activities have primarily been driven by the copper and gold sectors within the mid-tier 50. The rising input and labour costs have placed additional pressure on the margins.

It would, however, be unfair to draw a broad stroke across the entire mid-tier 50 and conclude that margins are decreasing in each sector. There are several sectors within the mid-tier 50 that, despite rising production, have managed to maintain and, in some instances, improve the margin from the previous year. Platinum and gold were the best performers with 46% and 17% improvements in margin respectively from FY09, whilst copper producers have seen a considerable squeeze on their margins.

Of the $1.5 billion increase in costs from FY09, $700 million relates to the commencement or ramp-up of production, whilst the remaining $843 million relates to financial instrument losses (approximately $730m) and foreign exchange losses (approximately $110 million). This sector has been significantly adversely affected by the revaluations in financial instruments, more so than any other mid-tier 50 sector (the coal sector had the second largest financial instrument impact with a gain of $26 million). The financial instrument and foreign exchange impacts have been analysed in conjunction with copper operating costs below. If the impact of the derivative instruments are “normalised”, the margins in the copper sector would improve considerably from 13% to 43%.

The gross margin across the coal sector reduced to 22% in FY10, down from 33% in FY09, attributable to both revenue and cost squeezes. Revenue was impacted as a result of the lower export sales prices. Operating costs increased as a result of increased rail and haulage costs for transport of product coal to the ports. The best coal performers, based on gross margins, were New Hope, Macarthur Coal and Whitehaven Coal with margins of 33%, 24% and 24% respectively. The ability of these companies to maintain margins is as a result of a higher portion of domestic sales.

Extract from the income statement

FY10 FY09

Operating Revenue 11,317 8,561

Operating Costs (8,639) (6,108)

Gross Profit 2,677 2,453

Margin 24% 29%

Table 13: Commodity price movementsSource: Capital IQ

6,108

232

154

1,545

10

141

124

258

123

(55)

8,639

June FY09

Bauxite

Coal

Copper

Platinum

Uranium

Iron ore

Gold

Nickel

Other

June FY10

Movement in operating costs

Table 14: Movement in operating costs FY09 – FY10 (A$m)Source: Capital IQ

Operating costs

The increase in operating costs from the previous year have been separated out into the respective sectors below in order to highlight key movements.

24 PwC

Copper – to hedge or not to hedge?

Of the total increase in operating costs from the previous year, $700 million relates primarily to the commencement of production at two mines and a further one ramping up production. This increase is expected given the higher costs of mining during the ramp-up phase. Equinox’s Lumwana operation commenced production in the quarter ended March 2009 and ramped up to 20 mtpa in the second half of the 2010 financial year. OZ Minerals’ operation at Prominent Hill also commenced production in the quarter ended March 2009 and achieved full production levels at the end of the 2009 calendar year. Lastly, PanAust’s Phu Kham operations ramped up operations during FY10, with operating costs increasing from the prior year as the mine continued to increase throughput.

The remaining $843 million increase in costs from the previous year relate to financial instrument and net foreign exchange losses. The financial instrument losses (approximately $730 million) were realised as a result of movements in the mark-to-market valuations of copper put options and forwards primarily in Equinox Minerals. Equinox Minerals realised hedge losses of approximately $415 million in 2009 compared to the previous year where it recognised hedge gains of approximately $320 million. The loss in 2009 was due to revaluing the hedge book to the current market prices and the strengthening copper price from US$1.38/lb at December 2008 to US$3.33/lb at December 2009. The net foreign exchange losses (approximate $110 million) related to OZ Minerals. The majority of the losses were recorded on US$ denominated assets (cash and debtors) net of the US$ denominated liability for convertible bonds.

The shining example of cost management

The gold sector has the second highest increase in operating costs; despite this, it has been one of the best performing sectors based on gross margin. This has primarily been due to the gold miners’ ability to control cash costs over the last two year period with average cash costs around US$530/oz in FY10, down from US$550/oz in FY09. Therefore the incremental costs of higher production levels were minimised, affording greater margins.

Table (to the right) above highlights that despite a 44% increase in production in the June 2009 quarter, cash costs decreased from $558/oz to $512/oz over the same period. The increase in production during the quarter was due to two gold mines commencing operations and five of the remaining six producing mines experiencing double-digit growth from the previous quarter. Avoca Resources and Kingsgate Consolidated lead the way with double-digit growth of approximately 80% and 30% respectively. The impressive result from Avoca was due to commencing treatment of high grade stoping ore at Higginsville (in the Trident resource). The Kingsgate results were spurred as the gold grade of the mill ore feed at their Chatree mine site (located in Thailand) improved. Operating costs remained relatively stable over the period as the miners were able to take advantage of the improved grade ore and the economies of scale as they ramped up to full capacity. An impressive performance by any measure.

The skilled labour challenge

Skilled labour remains in high demand in the mining industry. The cost of labour represents one of the largest expenses in the income statement, and yet is one of the most difficult to control. During 2008/9, in a period of tightening margins for many miners, it is interesting to note that labour costs have not declined – the basic cost of a worker remains.

With optimism returning to the market and significant foreseeable demand for skilled workers costs associated with attracting and retaining skilled staff will continue to be a challenge for the mid-tier 50 across the board. The skill shortage will be compounded by mega-projects, such as several coal seam gas projects in Queensland, the planned LNG investment in Western Australia, Rio Tinto’s $3.2 billion combined with BHP Billion’s $5 billion committed to expansion of their Iron Ore interest in the Pilbara as well as another $5b earmarked in the near term for Olympic Dam expansion plans. The critical mass of these projects is likely to add to inflationary pressure on project resources and has potential to result in cost blow outs if these costs are not controlled adequately.

Gold Produced (RHS) Cash costs (LHS) Cash Costs (normalised)

Prod

uction (oz)

US

D/o

z

Q1FY09 Q2FY09 Q3FY09 Q4FY09 Q1FY10 Q2FY10 Q3FY10 Q4FY10

800

700

1,000

900

600

500

400

300

200

100

350,00

300,000

450,000

400,000

250,00

200,000

150,000

100,000

50,000

Gold Production and Cash Costs

1) It is important to note that cash costs have been “normalised” in the first quarter to exclude cash costs relating to two mines. Both were excluded due to abnormally high cash costs during that period as a result of one-off events associated with start-up of operations.

Aussie Mine November 2010 25

Gain / (loss) on sale of investments

During FY10 approximately 30% of companies in the mid-tier 50 had some form of capital restructure by way of asset sale which resulted in a number of small losses. The prior year gain on sale of investments is primarily driven by two significant transactions representing 95% of the total value of the asset sales during the year - New Hope Coal’s $2.4 billion pre-GFC sale of New Saraji to BHP Mitsubishi Alliance (BMA) and OZ Minerals’ $1.7 billion sale of selected assets to Minmetals.

Impairments

With the improvement in commodity prices, there has been a marked reduction in impairment write-downs from the previous year. Many of the mid-tier 50 companies, unsurprisingly, booked impairments during 2009 as a result of declining commodity prices which characterised the global economic downturn. Notably the impairment charges in FY10 have reduced by approximately 94% from the prior year, with OZ Minerals and Paladin Energy accounting for the majority of the prior year write-down, which was not repeated.

Depreciation and Amortisation

The effects of the increase in operations can also be noted in the depreciation and amortisation charges which have also increased as mines continue to depreciate their assets on a units-of-production basis.

Interest

Interest expense has eased slightly from the previous year as a result of the debt repayments and improved gearing ratios, although the full impact of these debt repayments and stronger balance sheets is likely to be seen in the coming year.

Income tax expense

Income tax expense and cash tax outflows have been skewed in 2009 by New Hope’s $2.4 billion, pre-GFC sale of New Saraj to BHP Mitsubishi Alliance (BMA). The capital gain was recorded in the 2009 accounts, but the tax payment did not fall due until the 2010 year, as reflected in the 2010 cash flow statement.

Similar to the top five by revenue, three of the companies in the November 2009 publication have retained their place in 2010. Zimplats and Mt Gibson Iron have joined the list this year with Felix Resources and Whitehaven Coal being replaced. Divestments and take-overs have played a part in the movement as Felix was taken over during the year by Yanzhou Coal Mining Company and Whitehaven Coal had a higher profit figure in the prior year following divestment of its 15% interest in Narrabri.

Adjusted EBITDA and NPAT2010 A$m

2009 A$m

Adjusted EBITDA 2,355 2,512

Gain/(loss) on sale of investments (354) 487

Impairment (111) (1,738)

EBITDA 1,890 1,262 Depreciation and amortisation (1,134) (796)

EBIT 756 466 Net interest expense (359) (382)

Profit from ordinary activities before tax 397 84

Income tax expense (423) (706)

Net Profit / (Loss) (26) (623)

Top five mid-tier companies by profit

CompanyName 2010 A$m

2009 A$m

Change %

1 Energy Resources Australia 273 223 23%

2 New Hope 184 1,950 (91%)

3 Zimplats 138 (33) 521%

4 Mt Gibson Iron 132 42 212%

5 Macarthur Coal 125 169 (26%)

26 PwC

5.1 Focus–Accountingchanges:Rockyroadaheadfor mining sector The mining sector, despite its status as a globally important industry, has received little attention over the years from the accounting standard setters. Recent proposals from the International Accounting Standards Board (IASB) and its interpretations committee (IFRIC) are making up for lost time and entities operating in the sector can look forward (or not) to being in the accounting limelight.

In this Focus we consider some of the financial reporting developments that entities operating in this sector should have on their radar.

Shake up in accounting for stripping costs

What’s the issue?

The IFRIC has issued a draft interpretation (DI) that sets out guidance on the accounting for waste removal (stripping) costs during the production phase of a mine. There is currently diversity in accounting practice over the way entities identify and allocate the benefits and the costs of stripping activity across different reporting periods.

What are the key proposals?

• Creating an asset. The stripping activity creates a benefit of improved access to the ore to be mined by the entity. Under the DI, the costs incurred on stripping will qualify as an asset when:

a) the entity controls the benefit created by the stripping activity (eg, by owning the land it is mining or owning the rights to mine the land);

b) a benefit arises as a result of stripping activity

c) a future economic benefit will flow to the entity through improved access to the ore that is expected to be economically recoverable in the future. Stripping costs that are part of a stripping activity should be accounted for as an addition to, or enhancement of, an existing asset (stripping component). For example, with the section of ore that becomes more directly accessible as a result of the stripping activity.

• Recognising the asset. The DI proposes that the stripping cost should be recognised as an asset as the stripping activity takes place.

• Initial measurement of the asset. The stripping activity should be measured initially at the direct cost to perform the stripping activity (eg, haulage, waste transportation, materials consumed, labour, fuel etc).

• Subsequent measurement of the asset. The cost of the stripping activity should be carried at cost less depreciation or amortisation and impairment charges. It should be depreciated or amortised in a rational and systematic manner over the useful life of the ore body that becomes accessible as a result of the stripping activity. The units-of-production method should be applied unless another method is more appropriate.

Application date

The proposals are currently open for comment until 30 November 2010. We expect the issue date of the interpretation to be in early 2011 with application expected in 2012.

Leases proposals set to rock the mining industry

What’s the issue?

In September 2010 the IASB and US FASB released an exposure draft (ED) on accounting for leases as part of their commitment to converging IFRS and US GAAP. The proposals would overhaul the current requirements in AASB 117 Leases and dramatically change the way entities account for leases.

If adopted, the ED will affect a number of entities in the energy and resources sector, including those that have significant operating leases (such as mining or extraction equipment) and those that have finance lease arrangements that are within the scope of the existing leasing standard (such as fleets of trucks).

What are the key proposals?

Entities would be required to recognise an asset and liability at the start of a lease. The distinction between operating and finance leases would be eliminated.

If adopted, the proposals would have wide-ranging impacts on business.

For example:

• Balance sheet: entities would be required to recognise an asset and liability at the start of all leases.

• Profit and loss metrics: all lease expenses would have an amortisation component and a financial cost component rather than an operating lease. This would directly impact the EBITDA (earnings before interest, taxes, depreciation and amortisation) calculation and other P&L metrics.

• Debt covenant measurements: measurements based on interest cover and gearing levels will incur the biggest impact as leasing expense moves from being an operating cost to being classified as an additional amortisation and finance costs.

• Contracts: related to finance liabilities and other long-term arrangements that are based on measurements relating to EBITDA would need to be considered.

• Credit levels: these could be impacted by changing debt levels.

• Remuneration: short-term bonuses and other remuneration arrangements that are impacted by the EBITDA, P&L or other balance sheet KPIs will need to be revisited.

Application date

We anticipate the final standard to have an effective date no earlier than 2012.

New accounting for extractive activities

What’s the issue?

Last year the IASB released a discussion paper (DP) on accounting for extractive activities, which addresses some of the key challenges affecting entities with upstream activities in the mining and oil and gas industries.

What are the key proposals?

1. A single financial reporting framework should be available for all mining and oil and gas activities. Currently there is divergence in practice in the accounting for exploration, development and production of minerals/oil & gas because the introduction to AASB 6 allowed entities adopting IFRS to continue to apply existing policies within their territory.

2. All reporters would use recognised definitions for ‘resources’ and ‘reserves’. This would replace the various national codes and definitions currently in place.

3. Mineral and oil & gas assets should be recognised when a legal right to explore is acquired (due to the activities enhancing the asset). This would improve consistency of reporting across jurisdictions.