Riding the real estate cycle - Strategy& · Riding the real estate cycle ... Real estate developers...

20

Building capabilities for a sustainable future Riding the real estate cycle Strategy& is part of the PwC network

Transcript of Riding the real estate cycle - Strategy& · Riding the real estate cycle ... Real estate developers...

Building capabilities for a sustainable future

Riding the real estate cycle

Strategy& is part of the PwC network

2 Strategy&

Abu Dhabi

Ramy Sfeir Partner +971-2-699-2400 ramy.sfeir @strategyand.pwc.com

Beirut

Fadi Majdalani Partner +961-1-985-655 fadi.majdalani @strategyand.pwc.com

Dubai

Karim Abdallah Principal +971-4-390-0260 karim.abdallah @strategyand.pwc.com

Fadi Majdalani is a partner with Strategy& in Beirut and leader of the firm’s Middle East real estate practice. He specializes in corporate strategy, organization, and operations for real estate, construction, industrial, and transport companies.

Ramy Sfeir is a partner with Strategy& in Abu Dhabi and a member of the firm’s real estate practice. He specializes in strategy, operating models, and transformation for real estate developers, family conglomerates, and investment companies.

Karim Abdallah is a principal with Strategy& in Dubai and a member of the firm’s real estate practice. He specializes in corporate strategy, organization restructuring, and finance for real estate developers, conglomerates, investment companies, and public entities.

Bruno Wehbe is a senior associate with Strategy& in Beirut and a member of the firm’s real estate practice. He specializes in strategy development, megaproject concept creation and feasibility, operating model redesign, and full-fledged restructuring of real estate companies.

About the authorsContacts

This report was originally published by Booz & Company in 2013.

3Strategy&

Executive summary

The property market bust in most of the Middle East and North Africa (MENA) region exposed deep structural problems in the sector. If the leading real estate developers are to recover and deliver sustainable risk-adjusted returns to shareholders, executives will need to focus more on creating value than on simply erecting buildings. They will need to learn from their three most common mistakes — errors that became apparent during the downturn. First, developers grew in all directions with unfocused business models targeting a wide range of assets in different countries, as well as multiple segments and classes.

Second, not having to worry about commercial capabilities and profits given the buoyant market, developers concentrated on iconic assets and rushed to deliver. Third, most regional players had volatile revenue streams and managed risk poorly — depending excessively on property sales, as opposed to recurring income from leasing and other operations.

Going forward, developers should adjust their strategies in four steps. They must first decide what kind of developer they want to be and where to operate on the real estate value chain. Second, developers should master their chosen markets, and understand all components of the real estate ecosystem so that they can identify and pursue attainable growth opportunities and create sustainable value. Third, developers should manage their exposure to market risk better by seeking more balanced revenue sources, and elaborating clearer investment and development guidelines. Finally, real estate players should start developing a set of core capabilities (e.g., opportunity identification, development, asset management) to deliver sustainable value.

Real estate developers can prepare for the next property cycle by building key commercial capabilities and reconfiguring their market-facing approach. With the correct ingredients, property companies can better position themselves to capture emerging opportunities and enter underserved parts of the market as the regional recovery accelerates.

4 Strategy&

The MENA real estate development sector went, in the space of a few months, from one of the most active in the world to one in which firms sought assistance with meeting their debt obligations. Developers made similar missteps during the dramatic growth surge, missteps that became apparent as the market faltered. In order to better understand the Middle East real estate sector, one must understand the intricacies of the region and the specificities of the different sub-markets.

Real estate in the Middle East: A tale of two markets

MENA real estate consists of two very different “old” and “new” markets, with distinct and sometimes contradictory characteristics. The new markets are the rapidly growing population centers of the Gulf Cooperation Council (GCC) states,1 such as Abu Dhabi, Doha, and Dubai. These cities are being transformed by a surge in hydrocarbon revenues,

MENA property developers’ wild ride

• Real estate developers in the Middle East grew very fast into multiple real estate segments and adjacent businesses, often neglecting commercial capabilities and profits in favor of prestige projects, and failed to manage risk and revenue streams properly.

• Comparable developers in more mature markets have been growing at a more balanced pace, building a balanced business model with more

recurring revenues focusing on specific segments and classes of the market in which they can excel.

• To position themselves for the upswing, developers need to choose where they want to be on the value chain, be firmly rooted in their target market, formulate robust risk and investment guidelines, and develop their capabilities to ensure value creation and success through differentiation.

Key highlights

1 The GCC consists of Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, and the United Arab Emirates.

5Strategy&

an influx of expatriate workers, and the entry of speculative capital. The new markets present a plethora of opportunities. They are known for landmark property developments, as well as large and megaprojects that have enjoyed strong government backing in terms of land access, regulatory facilitation, and direct or indirect financing. These aspects of the new markets that made them so attractive, however, played a role in dooming them to suffer worse when the property market went through its inevitable down cycle. The flurry of opportunities in the new markets encouraged many developers to grow beyond their original mandates, scale, and capabilities. Unsurprisingly, the real estate bust hit most segments of these new markets very hard.

By contrast, the old markets — the cities of the Levant, such as Amman, Beirut, and Cairo — have matured over the past decades, and presented moderate growth opportunities following more than a century of cyclical economic and social development. The old markets, characterized by relatively constrained availability of land and financing, present limited opportunities. New developments are generally small to medium-sized, managed by a fragmented group of private developers. The property market still cycles moderately in the old markets, but its effect on the broader economy is more constrained than in the new ones (see Exhibit 1).

Exhibit 1The Middle East is divided into two main property markets

Source: Strategy&

“Old” markets “New” markets

Beiru

t

Amm

anC

airo

Doha

Duba

i

Abu

Dhab

i

Kuw

ait

Riya

dh

Demandgrowth and key drivers

Supplystructure andproject size

Role ofgovernment

Availabilityof land

- Moderate past decade growth rate (2–8% per annum) - Key driver: local population growth - Fragmented: many small to medium- sized developers account for most supply- Small to medium-sized property developments- Limited- Developers are mainly private companies and individuals- Slow change in regulations- Scarce. Limited free land in key metropolitan areas. New developments mainly outside cities- Most land owned by the private sector

- High past decade growth rate (>10% per annum)- Key drivers: expatriate influx, economic growth, investor confidence, abundant liquidity- Concentrated: few large developers make up bulk of supply- Large to mega master and landmark property developments- Key enabler- Strong government backing for developers in two key areas: access to land and financing, active change in regulations- Abundant. Key population densities currently being defined- Most land owned by the government, which provides cheap and easy access to selected developers

Key Middle East Cities by Market Dimensions (“Old” to “New”)

6 Strategy&

Chronicle of a property bust foretold

The deep challenges faced by the leading real estate players are nowhere better illustrated than by the experience of the United Arab Emirates (UAE). Property assets and prices in the UAE grew sharply on a wave of massive projects coupled with the availability of speculative capital in unparalleled quantities before crashing and causing difficulties that rippled out to the broader economy.

For understandable reasons, UAE real estate developers put speed and scale before all other factors in making decisions. The country was engaged in a high-priority program to encourage new economic activities, in particular in technology and services. Seeking to capitalize on its prime location and to leverage the business-friendly environment it had created, the UAE needed to provide a sufficient volume of high-quality real estate to support such emerging industries as finance, communications, and tourism. Real estate companies therefore built their businesses and operating models around the promise of creating, developing, selling, and operating large-scale developments — the sooner the better.

The initial results were impressive. Real estate prices grew at an explosive rate of more than 10 percent per annum from the beginning of the century until 2008. Thousands of real estate brokerages opened their doors. Development companies were established by local governments, large families, and influential speculative investors. This was done to support national economic ambitions, and to provide leadership in entrenching the infrastructure and the megaprojects, for which local authorities often provided the land. This active surge in supply was easily financed given buoyant commodity prices and fiscal surpluses, and was magically met by a highly speculative and liquid demand, an environment in which apartments were “flipped” many times before construction was completed.

The property boom turned to bust in 2009–10. After a decade of expansion, the global financial crisis, the disappearance of speculative investment and even real end user demand, along with the drying up of local funding combined to push the UAE property market into recession and the economy to slow down.

The impact on real estate developers’ income was all the worse, however, because of the sector’s structural deficiencies (see Exhibit 2, page 7). Their weaknesses were anchored in the way the sector had evolved over the previous years, characterized by (1) expanding everywhere, with unfocused market strategies; (2) rushing to deliver, neglecting value creation; and (3) having volatile revenue streams and insufficient risk management.

7Strategy&

Expanding everywhere, with unfocused market strategies

Most developers rapidly expanded their operations along three axes: the value chain, geography, and property segments. Broad expansion’s short-term appeal was considerable during the boom years; however, such an approach lacked long-term rationale, resulting in a clear financial cost. Real estate players were unable to pay sufficient attention to their core business, namely development, which affected their ability to deliver sustainable profit streams.

Value chain. Real estate developers grew their interests across the real estate value chain and into adjacent sectors. They operated as land traders, master developers, property developers, investment managers, and property managers. Some even set up facility management subsidiaries. Others invested in real estate funds in far-flung geographies. Some developers ventured outside real estate, to little profit, setting up hotels and operating schools. Some built and began operating leisure assets such as marinas, golf courses, and theme parks. Selective expansion into adjacent businesses was inevitable given the strategic complementarity of some of these recreation assets to large-scale, luxury developments that were being built in a supply market that did not provide the appropriate products and services.

Exhibit 2UAE developers suffered dramatic income swings

1 Aldar, Deyaar, Emaar, RAK Properties, Sorouh, Union Properties

Source: Company annual reports

12.4

2007

-14.4

2010

10.6

2008

1.3

2009

1.4

20112006

10.1

2012

4.2

Net Income Evolution of Top-Listed UAE Developers1 (in Billions of UAE Dirhams)

8 Strategy&

These excursions, however, were not done with the correct level of capabilities and focus, and proved to be going too far and too fast for many real estate firms, leaving them out of focus and out of pocket.

Geography. Some UAE developers spread themselves thin by expanding too quickly overseas. Although geographic diversification tends to hedge risk better than diversification across property segments, a mere presence in foreign markets is not enough. Developers had barely established themselves in their home markets before they were pursuing foreign opportunities. They neglected their core territory and then failed to deliver in foreign markets. The difficulty was that developers were spoilt for choice. During the boom years, they had ample financing and encountered the irresistible temptation of playing in the old markets of the Middle East as well as farther abroad. They aggressively entered countries that appeared to be similar to their home turf, but discovered shortly thereafter that they did not know these markets well. They encountered more complex management requirements, difficulties in tendering, troubles with supply chain and project execution, and complex relations with local partners, resulting in considerable challenges.

By contrast, best-in-class international developers have taken a slow-and-steady approach to building their businesses. They have expanded in a measured way that generates sustainable returns for the long term (see Exhibit 3). Some international companies took decades to dip their toes

Exhibit 3International players expanded abroad at a slow and careful pace

1 Estimated. 2 Regional presence is defined as outside the home state for the U.S., the home province for China, and the home country for others.

Source: Company information; Strategy& analysis

LocalRegional2 XGlobal

Number of years

Lend Lease1

Company

Hines

Liberty PropertyTrust

Stockland

Hang LungProperties

1940s 1950s 1960s 1970s 1980s 1990s 2000s

15

7 8

43

19

55

19

Geographic Expansion Time Line of International Developers

9Strategy&

in foreign waters because they recognized that they lacked the capabilities in deal sourcing required abroad, as well as the necessary market capabilities, in particular access to land, local financing, and government connections critical in some geographies.

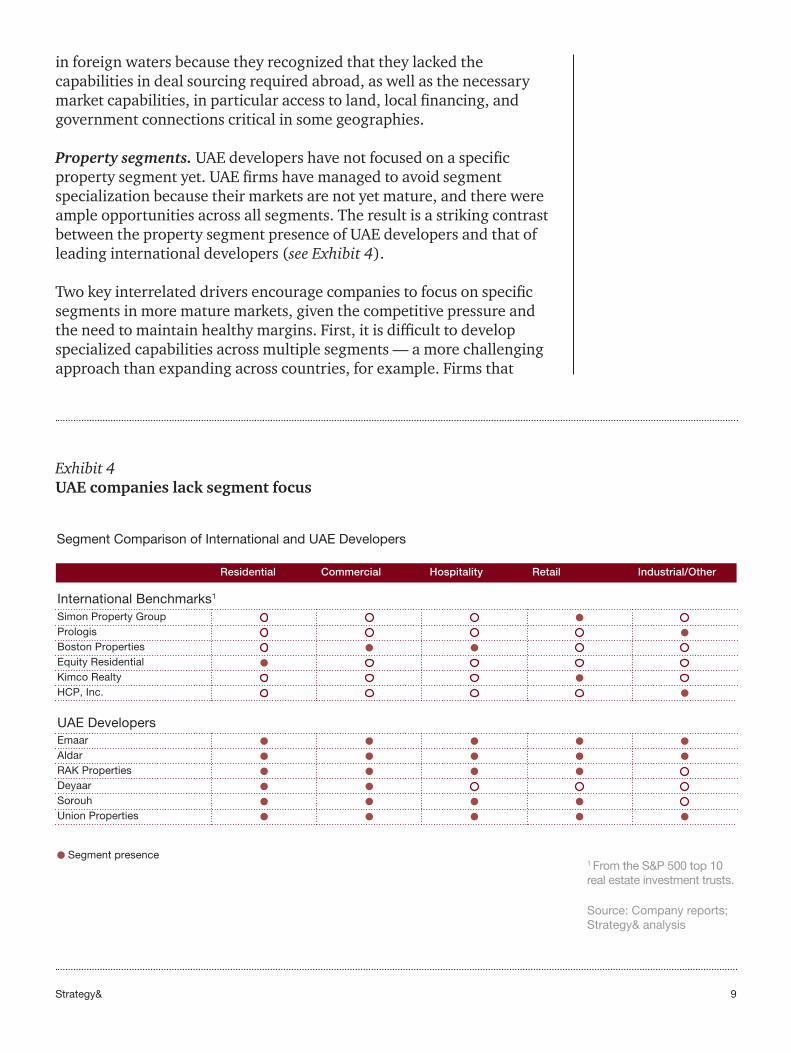

Property segments. UAE developers have not focused on a specific property segment yet. UAE firms have managed to avoid segment specialization because their markets are not yet mature, and there were ample opportunities across all segments. The result is a striking contrast between the property segment presence of UAE developers and that of leading international developers (see Exhibit 4).

Two key interrelated drivers encourage companies to focus on specific segments in more mature markets, given the competitive pressure and the need to maintain healthy margins. First, it is difficult to develop specialized capabilities across multiple segments — a more challenging approach than expanding across countries, for example. Firms that

Exhibit 4UAE companies lack segment focus

1 From the S&P 500 top 10 real estate investment trusts.

Source: Company reports; Strategy& analysis

Simon Property Group

Residential Commercial Hospitality Retail Industrial/Other

PrologisBoston PropertiesEquity ResidentialKimco RealtyHCP, Inc.

UAE Developers

International Benchmarks1

EmaarAldarRAK PropertiesDeyaarSorouhUnion Properties

Segment presence

Segment Comparison of International and UAE Developers

10 Strategy&

attempt to cover all segments now understand they will be unable to convincingly master one. Second, increasingly sophisticated investors tend to be more cautious about companies with vague, unfocused strategies going after multiple property segments.

In the long run, regional developers will want to consider narrowing their sights. They should consider specializing in one or two segments in order to create a lasting competitive advantage that differentiates their company irrespective of the real estate cycle.

Rushing to deliver, neglecting value creation

The intensity of the UAE real estate boom provided developers with only limited opportunities to build commercially driven capabilities, the essential source of competitive advantage. Most companies were not structured to allow them to maintain focus on commercial aspects of their activities throughout the development cycle, and many firms did not possess development and asset management capabilities sufficient for maximizing value creation.

A number of real estate companies have gone through two cultural evolution phases since their inception.

Design-driven organizations. The property development sector was initially defined by iconic properties that would shape the new urban skyline, and make names for companies, cities, and nations. In this initial stage, developers focused mainly on their architectural and design capabilities, placed less priority on costs and budgets, and ventured mainly into developing landmarks — the dream of every architect.

Delivery-driven organizations. In their next organizational phase, and as markets started to cool down, real estate developers shifted their focus to delivery capabilities such as project management, procurement, and cost control. Governments, which had provided generous support, now wanted results and imposed challenging completion deadlines. Some developers also faced tighter-than-expected budgets. Within organizations, influence shifted away from the designers and architects (who valued aesthetics and functionality), to project managers, engineers, and accountants (whose mission was to deliver on time and on budget).

Project directors, now in charge of delivery, started making significant trade-offs, sometimes putting delivery and cost before design, occasionally harming the ultimate product and its commercial potential. Some new delivery-driven organizations pushed “value engineering” too far, eliminating important aspects of the design on the basis of cost and delivery difficulties. This had a deleterious impact on some completed assets in the market and their potential for income generation. For

In the long run, regional developers will want to consider narrowing their sights.

11Strategy&

example, a developer would cut corners on the recreational facilities for a five-star hotel, putting in a mediocre pool and a spa that was smaller than planned. Yet it was precisely the installation of such luxury features that would have allowed the hotel to charge top prices.

Once the crisis hit, developers were unable to generate the returns that they had expected. Potential clients and buyers, some of whom had purchased properties in advance, were disappointed to receive a product different from that promised by glossy marketing brochures. Investors and financiers were similarly crestfallen, having extended backing on the understanding that the completed asset would be able to charge premium rates.

Having volatile revenue streams and insufficient risk management

Weak risk management capabilities also had a significant impact on the sector in general. UAE developers targeted quick, high-margin returns from developing and selling mostly residential assets. The result was that UAE developers became highly dependent on asset disposals, which are one-off transactions involving considerable risk. More than 90 percent of UAE developers’ revenues at the peak of the cycle in 2008 came from sales, while developers in more stable, more mature markets took in around 60 percent from selling assets (see Exhibit 5). When the

Exhibit 5UAE developers relied too much on sales at the height of the boom

Source: Company annual reports; Strategy& analysis

CapitaLand

53%

46%

7%1%

Hang Lung

63%

37%

HLD

68%

25%

Stockland

65%

33%

2%

Land and property salesRecurring revenue (leasing, operations, fees excluding construction) Other (including construction)

Deyaar

88%

12%

Sorouh

95%

5%

Aldar

96%

2%2%

Emaar

93%

7%

UAE Developers International Developers

Revenue Mix Analysis, 2008 (The Peak of the Recent Property Cycle)

12 Strategy&

market fell, sales revenues dried up and some developers faced difficulties covering financing costs and other overhead expenses.

Some UAE developers did start to show interest in income-producing assets just before the market began to slow. Property developers had not previously put much effort into continuous income streams from retail, commercial, or hospitality assets because of relatively lower returns. However, their interest in recurring income proved to be “too little, too late” in most cases.

Furthermore, cheap financing, a seemingly ever rising market, and weak risk management capabilities left most UAE developers with high debt-to-equity ratios. Industry averages are around 0.5, but most major UAE developers had significantly higher ratios (see Exhibit 6). Immersed in a booming market, developers had no reason to consider more sophisticated financing schemes, which are typically used to balance financial risks and returns. The result, in some cases, was that developers were forced to seek debt restructuring.

Exhibit 6UAE developers borrowed too much

1 Total liabilities/Total equity.

Source: Company annual reports; Strategy& analysis

Company Debt-to-equity ratio1 (2010)

Best practice average: 0.5

0.5

0.8

1.0

1.2

2.8

0.3

0.4

0.6

0.8

10.1

CapitaLand

Stockland

HLD

Hang Lung

Aldar

Union Properties

Sorouh

Emaar

Deyaar

RAK Properties

International Benchmarks Compared to UAE

13Strategy&

Back to basics

MENA developers should learn from the recent property cycle, and rethink the fundamentals of their sector. They need to build strong foundations that can deliver sustainable value going forward. This is because the real estate development market in the region is maturing. Such a reconsideration of strategy makes sense in the aftermath of a major market shock, as exists today.

As they position themselves for the coming recovery, real estate developers should not adopt all the approaches of similar organizations in more mature markets. Rather, they should learn from these international comparisons and rework their strategies in the following four customized ways:

Refocus value chain coverage to reflect new developer identity

Developers should clearly define their primary value creation strategy along the real estate value chain. This process begins by identifying which type of real estate developer they want to be. There are three broad profiles to choose from:

• Master developer: typically acquires large parcels of land, develops the required infrastructure and services, and then sells most of the plots to sub-developers.

• Property developer: buys serviced land from master developers (or individual land owners), develops new properties or repositions existing ones, then sells or lets the properties with direct or indirect involvement as the property manager.

• �Full-fledged�real�estate�developer:�does everything — develops land infrastructure and properties, then sells or leases these assets either directly or indirectly as the property manager.

The nature of the market to an extent drives the choice of profile and the capabilities needed to succeed. In “old” markets, the main approach is to be a property developer; there is little room for more large-scale master

14 Strategy&

developments. In “new” markets, firms tend to act as full-fledged real estate developers. It is important for developers to determine their identity, because each of these profiles requires a distinct set of capabilities. For example, property developers have broad control of the development value chain from land acquisition to concept definition, delivery, and sales and marketing. Master developers create value through access to strategic and large land plots, and have to focus their capabilities on infrastructure development and master planning.

For some full-fledged developers in the GCC, understanding their profile presents a first step in trying to fully align their core capabilities and strengths with their identity. If they choose to remain full-fledged developers, then they will have to acquire a wide and deep set of capabilities; it might be the appropriate time to attract top talent and prepare for the future. Even if they choose to become different kinds of developers, they must know that this still involves developing a set of differentiated capabilities that will lead to a clear competitive advantage.

Choosing a developer profile also has implications for ventures into adjacent businesses. These forays should occur only for specific strategic requirements and preferably through strategic partners with the correct capabilities and within the right partnership framework to align incentives and avoid diverting the firm’s core capabilities away from its main business. For example, UAE developers who entered joint ventures (JVs) with specialized delivery companies (project management companies, construction material suppliers, etc.) saw their JV partners focus on reviving their own companies’ operations after the bust, while JV operations were left to deteriorate.

Know the market: Identify attainable areas of growth

Developers have to acquire an intimate knowledge of their core market and a realistic sense of what opportunities are within reach. This knowledge will help them comprehend where they are in terms of the real estate cycle, the long-term waxing and waning of property prices, which in turn should allow them to calibrate their strategy and resource allocation accordingly (see Exhibit 7, page 15). They should then follow three strategic imperatives in determining their geographic, property segment, and property class strategy:

• Do not expand prematurely beyond the local market.

• Start narrowing segment coverage and specialize in one or two segment types over the long term.

• Consider entering underserved property classes.

It is important for developers to determine their identity, because each of these profiles requires a distinct set of capabilities.

15Strategy&

Exhibit 7Developers have the choice of two potential investment and market strategies

Source: Strategy& analysis

Low-end

Mid-range

High-end

Developer builds and sellsfive-bedroom apartmentslarger than 500 m2, in coremetropolitan areas, tonationals.

Residential

Property class

Propertysegment

Geography

Commercial

Retail

Region Country City

Not CoveredCovered

“Generalist” — Broad, Comprehensive

“Focused” — Targeted and Niche

These three imperatives dictate that developers keep a close eye on their local market. Knowing the home market involves conducting periodic in-depth analyses that go well beyond monitoring market prices and volumes, but that also examine the underlying drivers of the real estate cycle, spanning demographic, economic, regulatory, and political dimensions.

• Demographic factors. shape demand because of population growth, internal migration, household size, age distribution, and changes in family structure.

• Economic factors affect demand and supply because of household purchasing power, the macroeconomy (growth and inflation), fiscal and monetary policies (government spending on housing, liquidity, and the cost of borrowing), foreign investment, and the attractiveness of real estate compared to other asset classes.

• Regulatory factors also have an impact on demand and supply because legislation and regulations can either provide more transparency and confidence to investors or increase the number of players and buyers by allowing the entrance of foreigners. One such

16 Strategy&

measure for buyers is Saudi Arabia’s mortgage law. Examples from the UAE include easier residency visas and ownership rights for expatriates, strata laws, escrow regulations, and leasehold laws, as well as regulations on sales and leasing pricing.

• Political factors such as domestic or regional instability can make developers shun troubled markets and induce buyers to put their money into more liquid investments.

Such analyses help to identify which phase of the cycle a market is going through. Predicting its duration is very difficult because a complex interplay of factors influences the underlying supply and demand, and so the length, of each phase of the cycle (see Exhibit 8).

Exhibit 8The real estate cycle typically spans four to 10 years

Note: Assumes no atypical conditions such as wars or severe economic recession.

Source: Strategy&

Small increaseLarge increaseSmall decreaseLarge decreaseLimited change

Supply growth

Boom RecoverySlowdown Recession

4–10 years

Demand growth

Demand grows faster than supply until the boom peak

Demand–supply gap(Total demand minus total supply)

Demand slows down and the lagging supply catches up, closing the gap

Supply exceeds the stabilized demand and widens the negative gap

Demand picks up and narrows the negative gap

Prices Already high prices continue their upward trend and stabilize on the boom peak

Prices start to quickly decrease as suppliers rush to sell inventory

Prices continue to fall and eventually bottom out

Prices start rising quickly to take advantage of the new demand

Key Phases of the Real Estate Cycle

17Strategy&

An intimate understanding of the overall property ecosystem allows firms to adjust their value creation strategy, and define how best to allocate their resources across property segments, classes, and markets. Developers will be able to proactively manage their project pipeline by allocating resources to growing geographic areas, segments, or classes, while limiting their activities in down-cycle geographies.

Developers should review their strategy every two to three years, taking into account the foundations of market knowledge. Firms should continuously assess market opportunities to determine how their project pipelines should be adjusted. This allows developers to understand which openings in the market they should enter based on how such moves fit with their priorities and capabilities, in contrast to the previous all-at-once approach.

As an example, the changing demography of the GCC, coupled with increased government spending on national development programs, could present an opportunity for some developers to focus primarily on developing cost-efficient and “value” products for the middle- and working-class segments, thus moving away from luxury products.

Be ready for the next downturn: Balance revenue streams and risk taking

The third way real estate developers should rework their strategies is by ensuring that their business models strike the correct balance between easy short-term returns and long-term hedges. Developers should rethink their portfolios and pipeline of projects — and balance between building assets to sell and monetize versus building assets to maintain for the long term — to secure a safety net against the next down cycle. Boards should intervene by setting and monitoring, if required, financial metrics to ensure the organization can survive a market downturn. This should be done by maintaining a comfortable portfolio of recurrent income assets.

Furthermore, and to better manage risk exposure, board members and senior executives should work together to determine the boundaries of a risk–return profile that is acceptable to shareholders and investors. Effective tools that allow for the correct level of governance and control include setting debt-to-equity limits, excluding high-risk geographies, forcing a mix of asset classes, and specifying levels of recurrent revenues or coverage ratios. These metrics should be reviewed and refined as market conditions change, offering more funding opportunities or sources of risk.

18 Strategy&

Keep an eye on value creation

Finally, for developers, the correct set of core capabilities should be the few that help them deliver sustainable value for shareholders. Developers must focus their organizations on profitability, and move from being a design- or delivery-focused organization to being value-focused organizations. After years of trying to build iconic developments, followed by a rush to deliver “on time and on budget,” developers now have to reshape their organization to implant a commercial mind-set.

This means rethinking their organization, management processes, and governance frameworks to ensure the correct balance among accountability, delegation, empowerment, and control. In the past, what mattered was building the biggest and the best, and then selling it. In the future, it will become more important to construct the most profitable assets, and then actively manage them to ensure continuous value creation. Being commercially strong will be more important than being architecturally appealing. Moreover, by focusing on attractive and attainable opportunities, and delivering risk-adjusted projects well, firms can develop the differentiating capabilities that lead to success over the longer term.

19Strategy&

The rise, and apparent fall, of the MENA real estate development sector is not the end, but the beginning of the story. For all the problems following the latest downturn, real estate remains one of the sectors with the highest expected growth within the MENA region, because property remains the preferred asset class for investors. Developers still have substantial opportunities to attract capital, create value, and win a bigger share of the pie. Moreover, there are still gaps in the market, with underserved segments and classes in every geography.

The cyclical nature of the property business means that the next surge, and the next bust, are both inevitable. For developers, now is the time to reconsider business models and value creation strategies. As the MENA region proceeds through the real estate cycle, wise developers will identify the core and differentiating capabilities they need to develop to be able to play and win in their respective markets. These capabilities will allow developers to grow successfully through the cycle’s coming phases.

Conclusion

www.strategyand.pwc.com© 2013 PwC. All rights reserved. PwC refers to the PwC network and/or one or more of its member firms, each of which is a separate legal entity. Please see www.pwc.com/structure for further details. Disclaimer: This content is for general information purposes only, and should not be used as a substitute for consultation with professional advisors.

Strategy& is a global team of practical strategists committed to helping you seize essential advantage.

We do that by working alongside you to solve your toughest problems and helping you capture your greatest opportunities.

These are complex and high-stakes undertakings — often game-changing transformations. We bring 100 years of strategy consulting experience and the unrivaled industry and functional capabilities of the PwC network to the task. Whether you’re

charting your corporate strategy, transforming a function or business unit, or building critical capabilities, we’ll help you create the value you’re looking for with speed, confidence, and impact.

We are a member of the PwC network of firms in 157 countries with more than 195,000 people committed to delivering quality in assurance, tax, and advisory services. Tell us what matters to you and find out more by visiting us at strategyand.pwc.com/me.

This report was originally published by Booz & Company in 2013.