Revolution in Investment Research by Alphametry - June 2015

38

JUNE 2015, GENEVA, SWITZERLAND REVOLUTION IN INVESTMENT RESEARCH A LOOK AT ECONOMIC, DIGITAL & REGULATORY CHANGES

-

Upload

fabrice-bouland -

Category

Economy & Finance

-

view

229 -

download

0

Transcript of Revolution in Investment Research by Alphametry - June 2015

JUNE 2015, GENEVA, SWITZERLAND

R E V O LU T I O N I N I N VE S T M E N T R E S E A R C HA LO O K AT E C O N O M I C , D I G I TA L & R E G U L ATO R Y C H A N G E S

T H I S P R E S E N TAT I O N I N C LU D E S I N S I G H T S I N S P I R E D

B Y N U M E R O U S I N T E R V I E W S W I T H A N A LY S T S A N D

A S S E T M A N A G E R S D U R I N G T H E PA S T 2 4 M O N T H S

I b e c a m e a n e n t r e p r e n e u r 1 5 y e a r s a g o e s s e n t i a l l y t h a n k s t o t h e I n t e r n e t .

B e f o r e c r e a t i n g B r o k e r h u b , a n E q u i t y d e r i v a t i v e s p l a t f o r m a n d OT C e x , a n i n t e r - d e a l e r b r o k e r , I s p e n t 9 y e a r s a s a p r o p r i e t a r y v o l a t i l i t y t r a d e r a t B N P P a r i b a s .

I a m f o n d o f t e c h n o l o g y a n d e n j o y t h e c h a l l e n g e o f b u i l d i n g i n n o v a t i v e b u s i n e s s e s .

FA B R I C E B O U L A N D , C E O , A L P H A M E T RY

A N I N D U S T R Y I N T R O U B L E ? T H E S TAT E O F E Q U I T Y R E S E A R C H

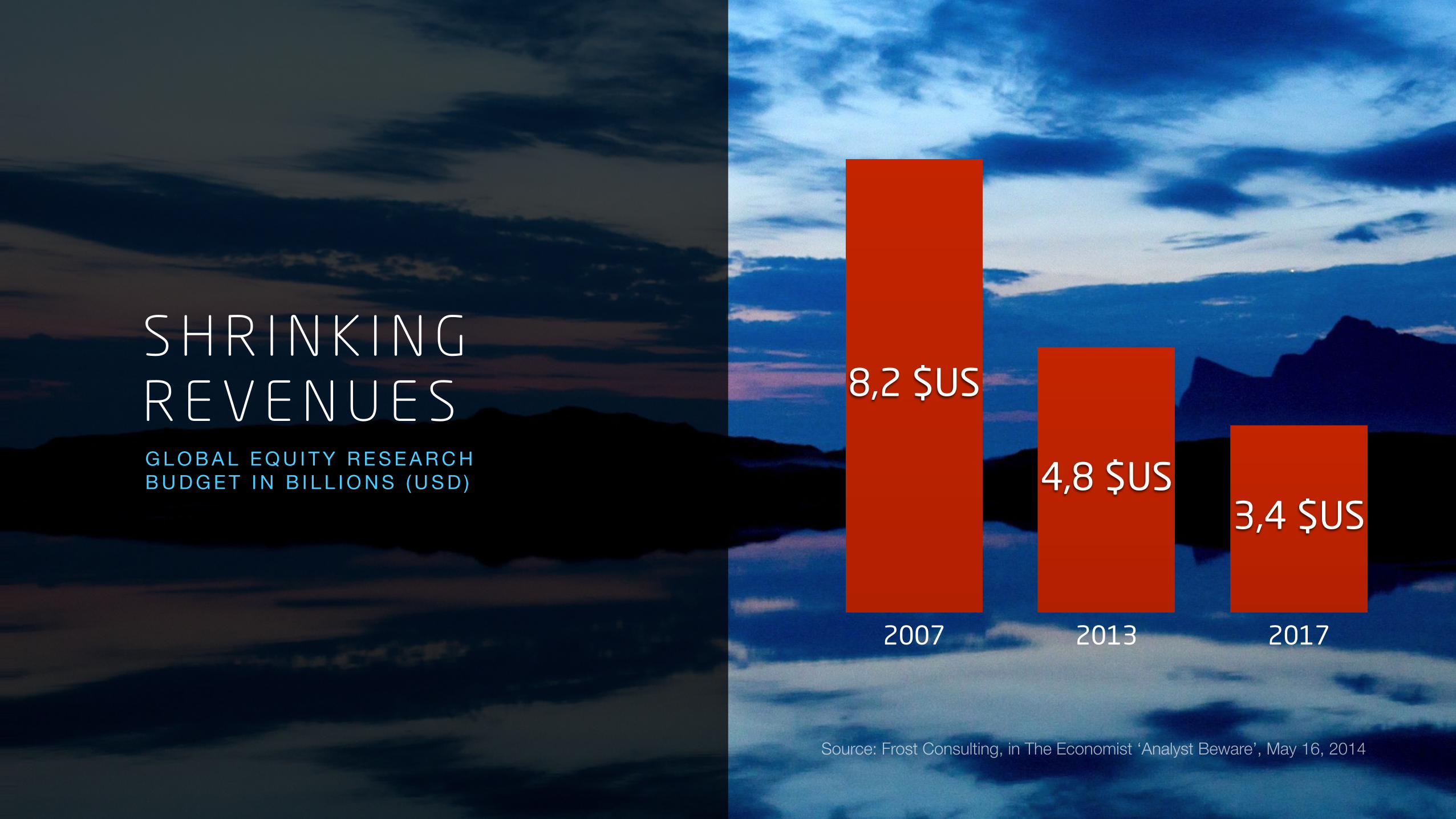

S H R I N K I N G R E V E N U E SG L O B A L E Q U I T Y R E S E A R C H B U D G E T I N B I L L I O N S ( U S D )

2007 2013 2017

3,4 $US4,8 $US

8,2 $US

Source: Frost Consulting, in The Economist ‘Analyst Beware’, May 16, 2014

C O N T E N T D I S P E R S I O N

Dominant incumbents

Emerging expertise

New producers

S U P P LY I S S U E S

Coverage concentration

Market opacity

Out-of-date delivery

T H E C H A N G I N G N E E D S O F A S S E T M A N A G E M E N T

A D J U S T I N G T O T H E I N V E S T M E N T P R O C E S S

T H E E X PA N D I N G R E S E A R C H U N I V E R S E

REGIONAL OPPORTUNITIES

NEW STRATEGIES

DATA-DRIVEN

I N D U S T R I A L I Z E D P R O C U R E M E N T

Acquisition process

Content exploitation

Business analytics

D E E P E R I N T E G R AT I O N

Numerous origins, types and formats

Actionable content

Automated trade execution

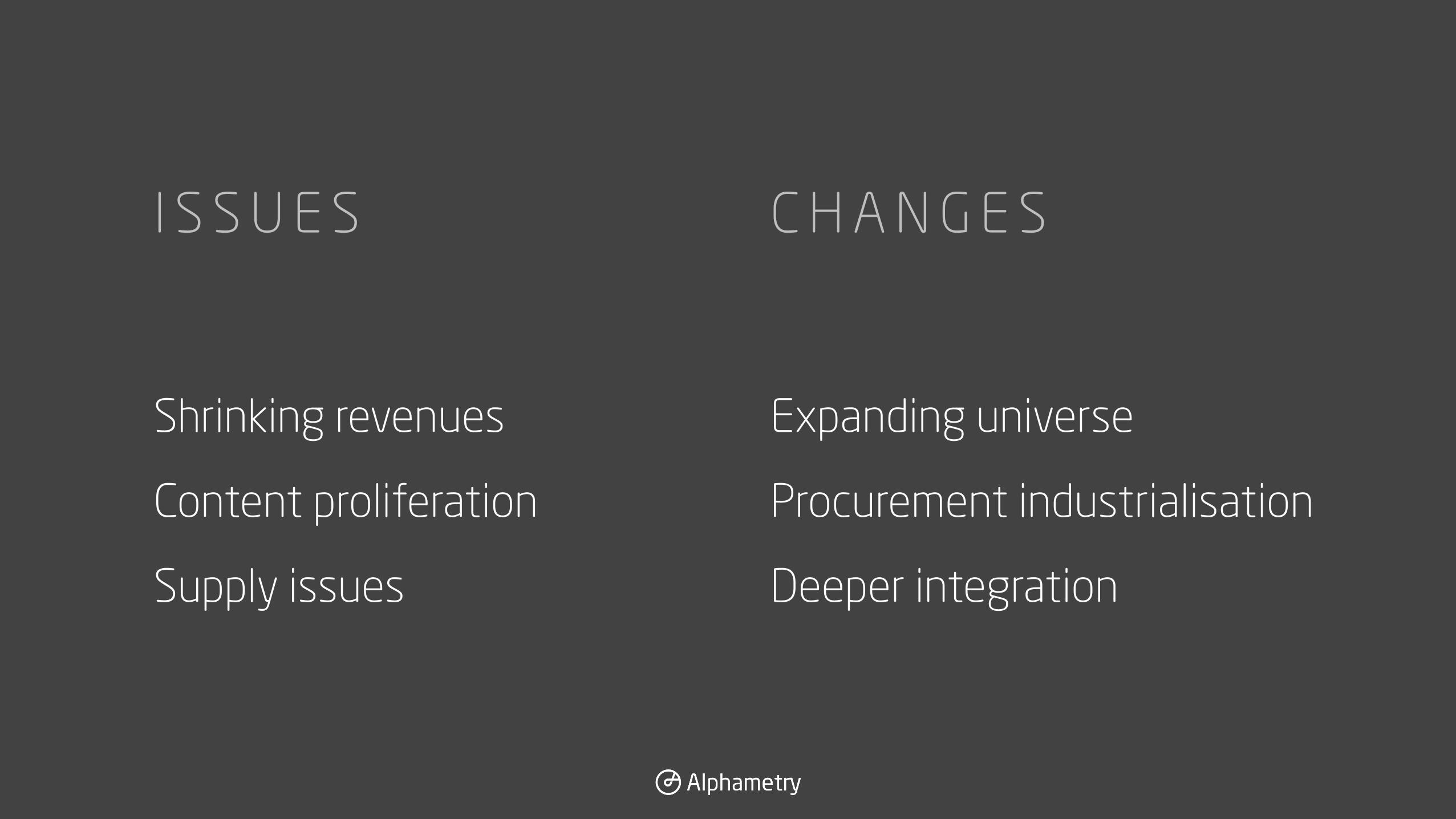

Expanding universe

Procurement industrialisation

Deeper integration

Shrinking revenues

Content proliferation

Supply issues

C H A N G E SI S S U E S

S AV I N G E Q U I T Y R E S E A R C H

T H E C O M M I S S I O N S H A R I N G A G R E E M E N T

R E S E A R C H U N B U N D L I N G PA R T 1

H O W T H E C S A W O R K S

RESEARCH BUYER

BROKER

RESEARCH PROVIDER

Source: University of Edinburgh Business School/Bloomberg, December 2014

T H E S U C C E S S O F C S A s

About the same 17 %

More in 2015 59 %

Less in 2015 24 %

Compared to 2010, do you expect CSAs paid to independent research providers to be…

— M A R T I N W H E AT L E Y, C H I E F E X E C U T I V E O F T H E F C A

There is a strong evidence to suggest the current model of using dealing commission

to pay for research reduces transparency and creates a link between research spend and trading volume, without a clear assessment

of the value this offers to investors.

“

T H E R E G U L ATO R Y S H I F TR E S E A R C H U N B U N D L I N G PA R T I I

Financial Conduct Authority 9

Feedback statement on DP14/3 – Discussion on the use of dealing commission regime FS15/1

February 2015

1.25 By clearly separating the payment for research from execution arrangements, it removes the inducement risk and conflicts of interest for portfolio managers that their execution behaviour and choice of brokers may be unduly influenced. This will drive proper scrutiny by portfolio managers over the amounts paid for research and the benefits it provides and also improve their ability to monitor and comply with best execution obligations on behalf of their customers.

1.26 Importantly, it recognises that external research can be a core cost of business to a portfolio manager in developing investment ideas. It will, under ESMA’s proposals, be a cost and charge that is akin to a portfolio manager’s own spending on analysts and internal research, which they already reflect in their upfront annual management charges (AMCs). Research would no longer be paid for in transaction fees that have no correlation to the quantity and value of research received and consumed.

1.27 ESMA’s approach will also promote transparency and competition in the market for research, allowing independent providers to compete more easily with larger brokers based on price and quality – encouraging a focus on value-added coverage.

1.28 The ‘research payment account’ option created by ESMA also takes into account some of the concerns expressed by stakeholders in the consultation (and in responses to our DP) on the impact on smaller asset managers and the availability of small and medium-sized enterprise (SME) research in the market.

1.29 The flexibility over how research costs are absorbed by portfolio managers should also reduce concerns over the short-term transition to this new model. It will allow portfolio managers to budget and pay for research that adds value to their clients, while adding scrutiny such that it is unlikely managers will continue to pay for low value, duplicative research, reducing overproduction and inefficiency in resource allocation by providers.

1.30 Overall, we believe it will address long-standing concerns from our supervisory work that current market practice – even with our specific dealing commission rules and disclosure requirements – is not delivering a good outcome for investors. The combination of improved cost control and scrutiny over research purchasing and execution decisions by investment managers, with more effective competition in the market for research, should lead to improved outcomes for investors.

Our views on technical aspects of ESMA’s advice

Interaction with Commission Sharing Arrangements and existing market practicesWhile borrowing some features from CSAs, ESMA clearly expresses the view that CSAs ‘do not entirely address the conflicts of interest at stake’ and indicates that they have ‘formulated additional requirements which are aimed at further limiting these conflicts of interest.’ In the technical advice, ESMA proposes that the research payment account and charge should be agreed upfront between the portfolio manager and their client, and be based on a budget set by the firm relating to their external research needs and not linked to trading volume or values. It also requires the portfolio manager to be responsible for operating the research payment account and managing the allocations made from within their budget.

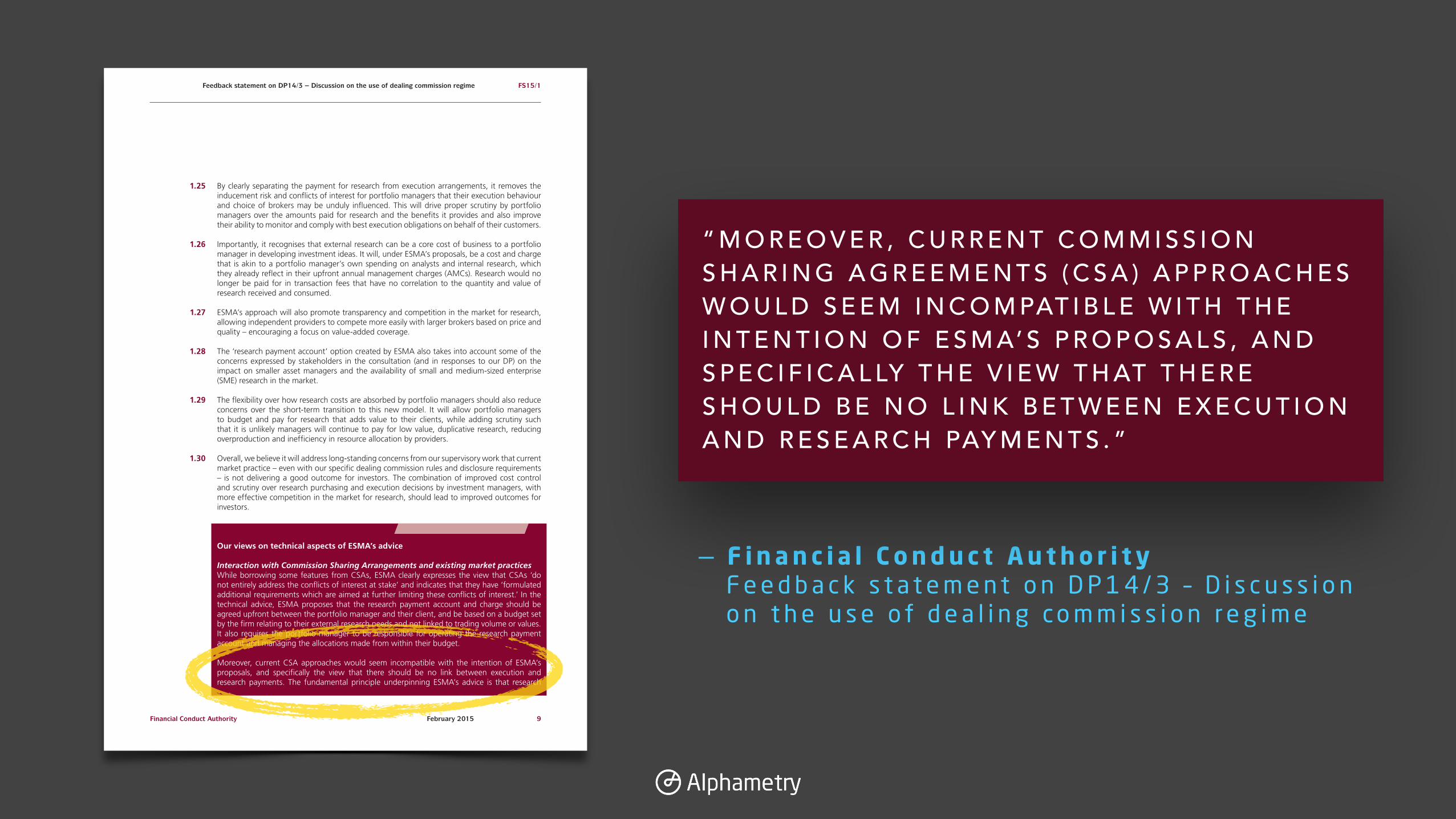

Moreover, current CSA approaches would seem incompatible with the intention of ESMA’s proposals, and specifically the view that there should be no link between execution and research payments. The fundamental principle underpinning ESMA’s advice is that research

— F i n a n c i a l C o n d u c t A u t h o r i t y F e e d b a c k s t a t e m e n t o n D P 1 4 / 3 – D i s c u s s i o n o n t h e u s e o f d e a l i n g c o m m i s s i o n r e g i m e

“ M O R E O V E R , C U R R E N T C O M M I S S I O N S H A R I N G A G R E E M E N T S ( C S A ) A P P R O A C H E S W O U L D S E E M I N C O M PAT I B L E W I T H T H E I N T E N T I O N O F E S M A’ S P R O P O S A L S , A N D S P E C I F I C A L LY T H E V I E W T H AT T H E R E S H O U L D B E N O L I N K B E T W E E N E X E C U T I O N A N D R E S E A R C H PAY M E N T S . ”

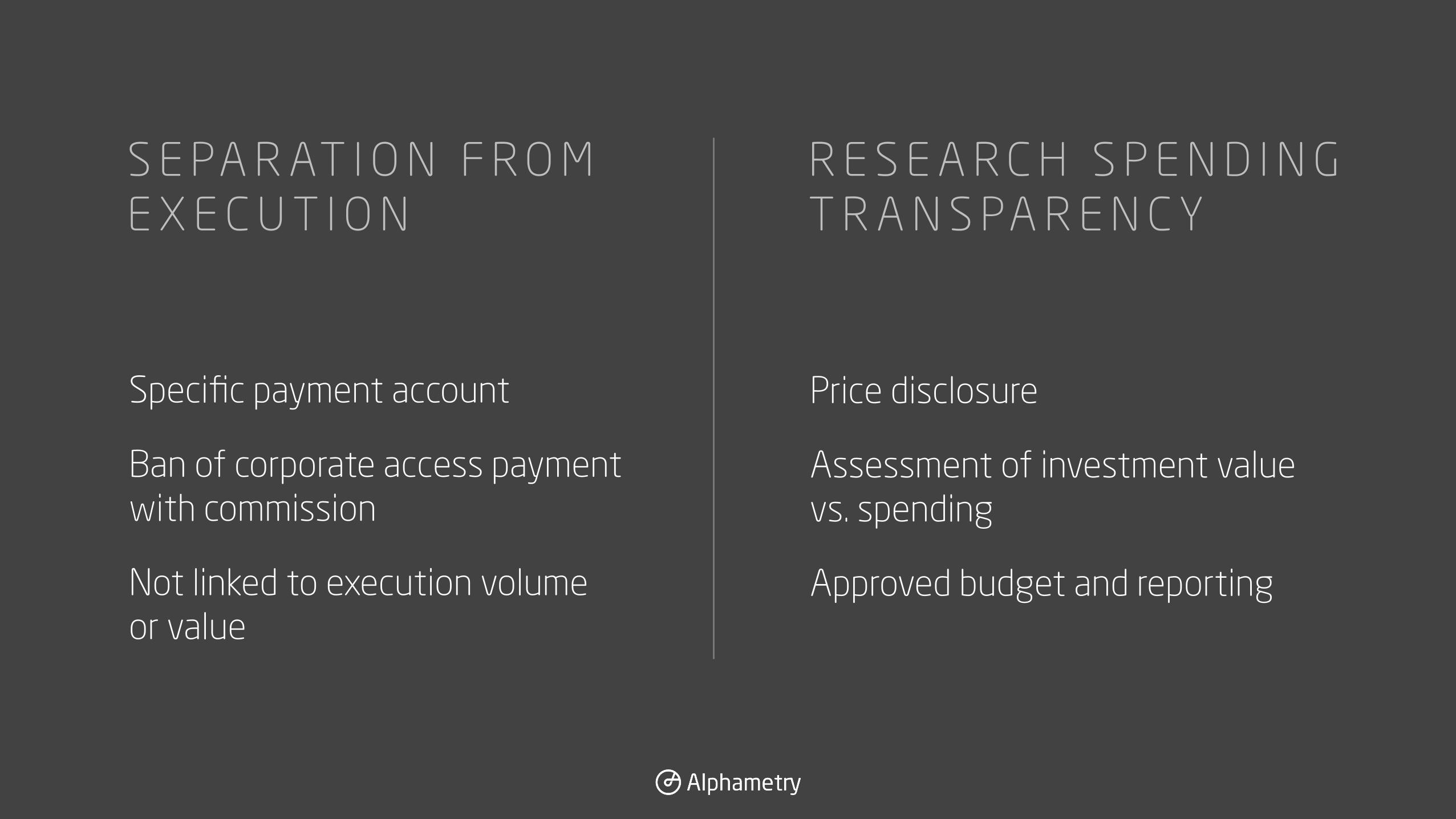

R E S E A R C H PAY M E N T A CC O U N T

( R PA )

S E PA R AT I O N F R O M E X E C U T I O N

Specific payment account

Ban of corporate access payment with commission

Not linked to execution volume or value

R E S E A R C H S P E N D I N G T R A N S PA R E N C Y

Price disclosure

Assessment of investment value vs. spending

Approved budget and reporting

A REGULATORY JOURNEY

July 2014The UK Financial Conduct Authority (FCA) aggressively calls for a ban of fund managers' license to pay for research with client commissions

December 2014 The European Securities and Markets Authority (ESMA) backs away from research commission ban but introduces a Research Payment Account (RPA) with a specific charge to the client

February 2015 The FCA views Commission Sharing Agreements (CSAs) as linking research payments to commissions and interprets they are ‘no longer compatible’ with upcoming MiFid II regulations April 2015

The European Commission (EC) issues a draft showing concessions which would allow fund managers to notify clients instead of receiving their approvals for research budgetsJune 2015

Deadline for The European Parliament and Council to approve ESMA’s final technical advice. If legislated as a “directive” instead of "regulation,” it would allow National Competent Authorities (NCAs) to interpret the guidance

January 2017MiFID II takes effect

R E S E A R C H U N B U N D L I N G PA R T I I I : T H E 2 0 B I L L I O N $ Q U E S T I O N

TO B A N O R N OT TO B A N r e s e a r c h p a y m e n t w i t h d e a l i n g

c o m m i s s i o n

VA L U AT I O NR PA : T H E C O N S E Q U E N C E S

?– A F U N D M A N A G E R

How do you price something which has

been free for 40 years…

“

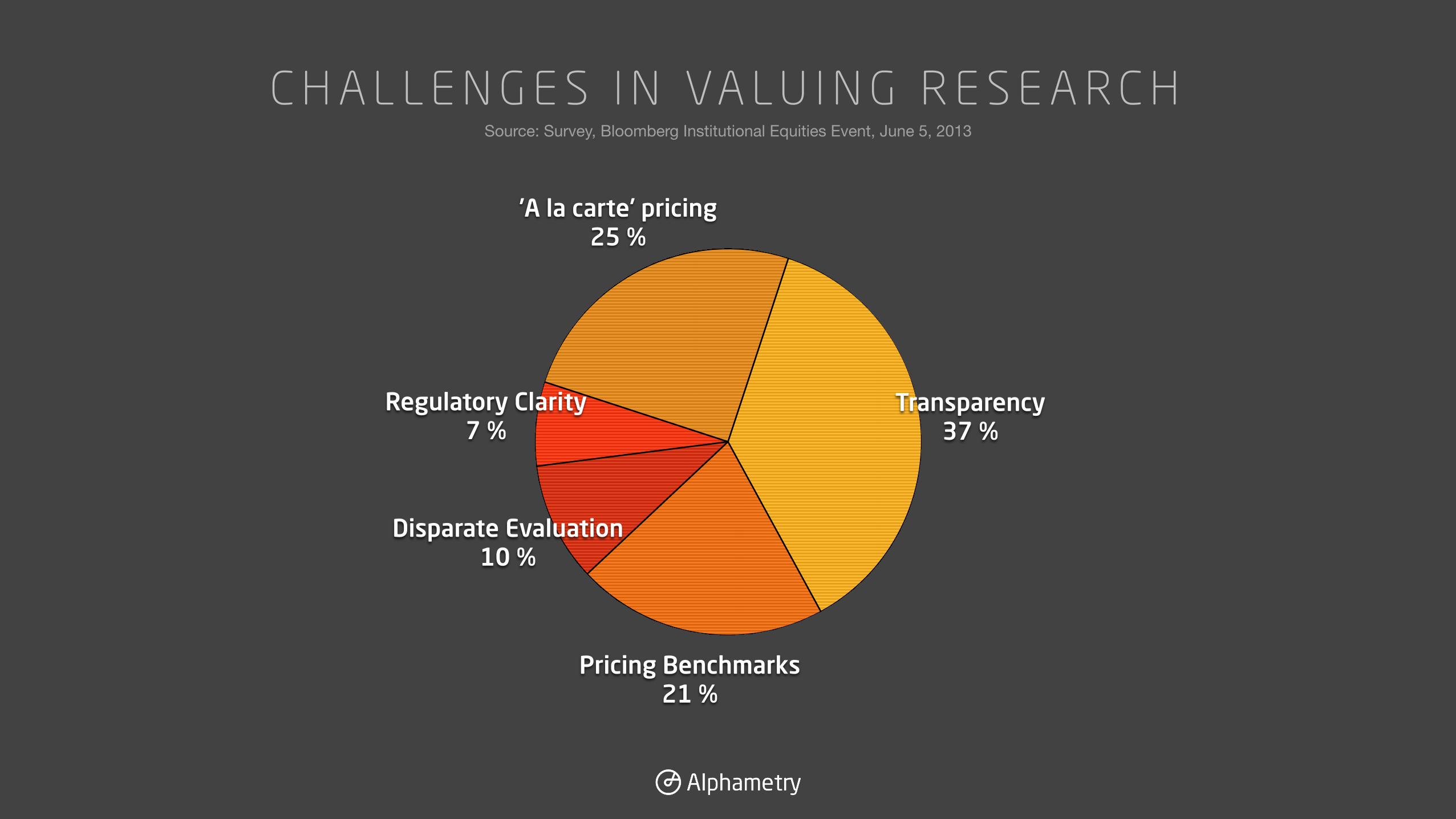

Source: Survey, Bloomberg Institutional Equities Event, June 5, 2013

C H A L L E N G E S I N VA L U I N G R E S E A R C H

Regulatory Clarity 7 %

Disparate Evaluation 10 %

Pricing Benchmarks 21 %

Transparency 37 %

'A la carte' pricing 25 %

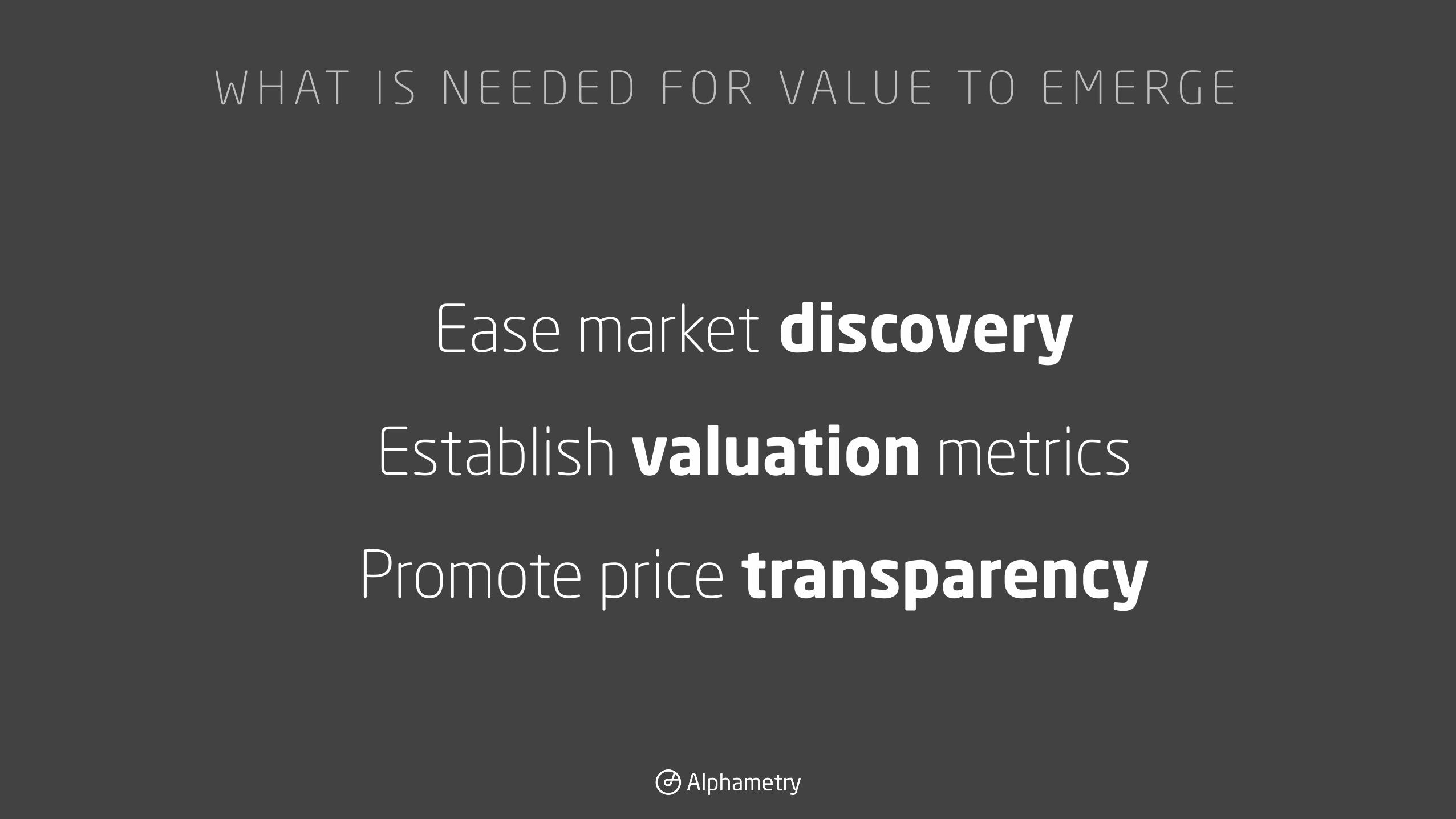

Ease market discovery

Establish valuation metrics

Promote price transparency

W H AT I S N E E D E D F O R VA L U E TO E M E R G E

I N V E S T M E N T R E S E A R C H 3 . 0A N I N D U S T RY R E B O R N

T H E R E G U L ATO R T R E N D # 1

Investor-centric

Information transparency

Regional policies convergence

D I G I TA L R E S E A R C H T R E N D # 2

Exponential data production

Analytical tools democratisation

Research componentization

A D A P T I N G O R G A N I S AT I O N A L S T R U C T U R E S

T R E N D # 3

Digital asset capabilities

Value chain fragmentation

Increase collaboration

C H A N G I N G D E M O G R A P H I C S

T R E N D # 4

A free-lance society

The millennial portfolio manager

T H E R I S E O F D I S T R I B U T I O N P L AT F O R M S

T R E N D # 5

Interactivity value enablers

Brand new markets

Information industry re-intermediation

FA B R I C E B O U L A N D , C E O i n f o @ a l p h a m e t r y. c o m

A l p h a m e t r y i s a n o n l i n e m a r k e t p l a c e f o r a s s e t

m a n a g e r s t o s e a m l e s s l y d i s c o v e r a n d b u y u n i q u e

i n v e s t m e n t s t r a t e g i e s f r o m a w i d e s c o p e o f e q u i t y

e x p e r t s .

W e s c r e e n c o n t r i b u t o r s w o r l d w i d e a n d c a l c u l a t e

r e a l - t i m e p e r f o r m a n c e a n d a c t i v i t y m e t r i c s t o h e l p

t h e m e n g a g e m o r e e a s i l y w i t h t h e b u y - s i d e

c o m m u n i t y .

T h e A l p h a m e t r y t e a m i s c o m p o s e d o f c r o s s - i n d u s t r y

e x p e r t s w i t h d e e p b a c k g r o u n d s i n f i n a n c i a l m a r k e t s

a n d h i g h - a v a i l a b i l i t y c o m p u t i n g a n d i n f r a s t r u c t u r e .

I n p r i v a t e b e t a s i n c e d e c e m b e r 2 0 1 4

O p e n p u b l i c b e t a s u m m e r 2 0 1 5 !

P r e - r e g i s t e r a t w w w. a l p h a m e t r y. co m