Revision Proceedings under Section 263 includinggy ...€¢ Wh tWhat if some other Hi hHigh CtCourt...

46

Revision Proceedings under Section 263 Revision Proceedings under Section 263 including amendment by Finance Act 2015 including amendment by Finance Act 2015 Chairman : Advocate Chairman : Advocate Vipul Vipul B. Joshi B. Joshi Group Leader : CA Group Leader : CA Ketan Ketan L Vajani Vajani Group Leader : CA Group Leader : CA Ketan Ketan L. L. Vajani Vajani [email protected] [email protected] 1 st st December, 2015 December, 2015

-

Upload

doankhuong -

Category

Documents

-

view

213 -

download

0

Transcript of Revision Proceedings under Section 263 includinggy ...€¢ Wh tWhat if some other Hi hHigh CtCourt...

Revision Proceedings under Section 263 Revision Proceedings under Section 263 including amendment by Finance Act 2015including amendment by Finance Act 2015g yg y

Chairman : Advocate Chairman : Advocate VipulVipul B. Joshi B. Joshi Group Leader : CAGroup Leader : CA KetanKetan LL VajaniVajaniGroup Leader : CA Group Leader : CA KetanKetan L. L. VajaniVajani

[email protected]@gmail.com11stst December, 2015December, 2015

03/12/2015 2

Commissioner is having power to call for andexamine the record of any proceeding underthe Actthe Act

CIT may pass the order for revision if any orderpassed by the AO is :◦ erroneous in so far as it is ;;◦ Prejudicial to the interest of revenue

Opportunity of hearing is to be granted to theassessee before making the revision order.CIT h ll k t b d h CIT shall make or cause to be made suchinquiry as may be deemed necessary.

Revision order can have the effect of :◦ Enhancing the assessment◦ Enhancing the assessment◦ Modifying the assessment◦ Cancelling the assessment◦ Directing a fresh assessment

03/12/2015 303/12/2015 Vajani & Vajani 303/12/2015 3

The term “order” includes order passedby Asst CIT or Dy. CIT on the basis ofy ydirections issued by Jt. CIT u/s. 144A

“order” includes order made by Jt. CITacting in the capacity of the AOacting in the capacity of the AO

“record” includes all records relating toany proceeding under the Act at the timef i i b h C i iof examination by the Commissioner.

If the order is subject to appeal, theCIT’s power u/s 263 shall extend toCIT s power u/s. 263 shall extend tosuch matters as had not been consideredand decided in such appeal.

03/12/2015 403/12/2015 Vajani & Vajani 403/12/2015 4

Time Limit : 2 years from the end of the financialyear in which the order sought to be revised waspassed

However in the case of an order which has beenpassed in consequence of or to give effect to anyfinding or decision in an order of ITAT/HC/SCfinding or decision in an order of ITAT/HC/SCthe above time limit does not apply and in such asituation the order can be passed at any time.

Following periods shall be excluded in computingthe time limit◦ Time taken in giving opportunity to the assessee to be

reheard under proviso to section 129reheard under proviso to section 129◦ Any period during which the proceeding under the

section is stayed by an order of injunction of anycourt.

03/12/2015 503/12/2015 Vajani & Vajani 503/12/2015 5

Order of AO shall be deemed to be erroneous so far asit is prejudicial to the interest of revenue if in theopinion of the Principal Commissioner or Commissioneropinion of the Principal Commissioner or Commissionerthe order is :

(a) Passed without making inquiries or verification(a) Passed without making inquiries or verificationwhich should have been made

(b) Passed allowing any relief without inquiring into theclaimclaim

(c) Not in accordance with any order, direction orinstruction issued by CBDT u/s. 119

(d) Not in accordance with any decision which is( ) yprejudicial to the assessee, rendered byJurisdictional High Court or Supreme Court in thecase of the assessee or any other person.

03/12/2015Vajani & Vajani 6

Any Decision of Jurisdictional High Court• What if subsequent decision of same High

Court has over-ruled the earlier decisionWh t if me the Hi h C t (L e Be h)• What if some other High Court (Larger Bench)has taken a contrary view after consideringthe view of the HCthe view of the HC

• What if the decision of High Court is receivedafter completing the assessment order ?– CIT Vs. J. M. Mittal Stainless Steel Pvt. Ltd. 263 ITR

255 (SC)

03/12/2015Vajani & Vajani 7

• At the time of completion of assessment HCd i i f f S b tl thorder is in favour of assessee. Subsequently the

SC decides against the assessee. Whetherrevision possible ?– CIT Vs. J. M. Mittal Stainless Steel Pvt. Ltd. 263 ITR 255

(SC)• Appeal against HC order filed at the stage of completion of

tassessment• Decision of SC against the same order or some other HC

C f C SC• CBDT Instruction Vs. Decision of HC / SC– Hindustan Aeronautics Ltd. Vs. CIT 243 ITR 808 (SC)– Bhartia Industries Ltd. Vs. CIT 353 ITR 486 (Cal.)

03/12/2015Vajani & Vajani 8

Whether Prospective / Retrospective / Retroactive ? Explanation whether corrective or substantive ? Additional burden on assessee

B rden of Le of Ta is à is proced ral b rden Burden of Levy of Tax vis-à-vis procedural burden Vatika Township Pvt. Ltd. 367 ITR 466 (SC) Amendment made to remove hardship to assessee Vs.p

Hardship to revenue Whether applicable where assessment order

made prior to 1-6-15 but revision order passedmade prior to 1-6-15 but revision order passedafter 1-6-15 ?

03/12/2015Vajani & Vajani 9

Ensure that order is not patently against anyorder / direction of CBDT

Ensure that order is not against any decisionof jurisdictional HC / SC on the subjectof jurisdictional HC / SC on the subject

File all the details in support of the claimeven if the same is not asked for by the AOeven if the same is not asked for by the AO

The normal inquiries shall be insisted uponand normal details shall be filed even if notasked for

03/12/2015 1103/12/2015 Vajani & Vajani 11

Not confined to Assessment Orders It can also extend to It can also extend to◦ Rectification order◦ Order passed u/s. 143(3) r.w.s. 147◦ Communication u/s. 195(2) determining tax

liability u/s. 195(1)◦ Order u/s 197(1)◦ Order u/s. 197(1)

Whether it applies to following orders ?◦ Order giving effect to Appellate OrdersOrder giving effect to Appellate Orders◦ Order u/s. 143(3) r.w.s. 263 ??

03/12/2015 1203/12/2015 Vajani & Vajani 12

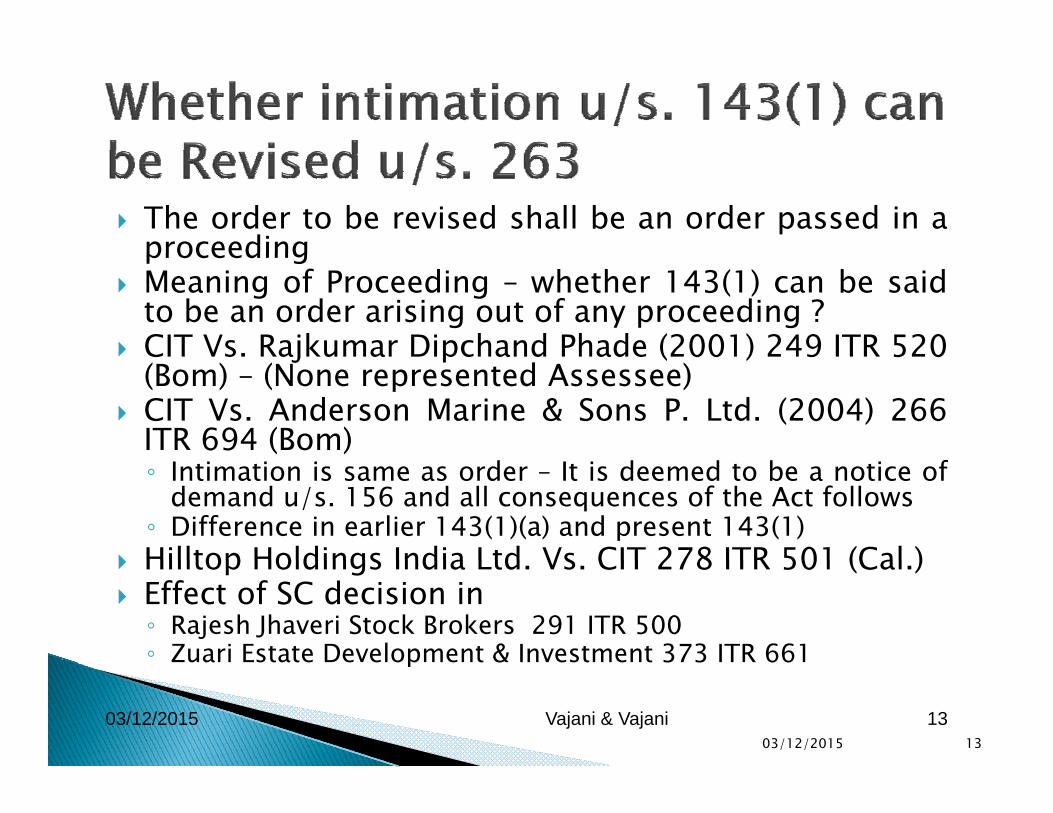

The order to be revised shall be an order passed in aproceedingproceeding

Meaning of Proceeding – whether 143(1) can be saidto be an order arising out of any proceeding ?

CIT Vs. Rajkumar Dipchand Phade (2001) 249 ITR 520 CIT Vs. Rajkumar Dipchand Phade (2001) 249 ITR 520(Bom) – (None represented Assessee)

CIT Vs. Anderson Marine & Sons P. Ltd. (2004) 266ITR 694 (Bom)◦ Intimation is same as order – It is deemed to be a notice of

demand u/s. 156 and all consequences of the Act follows◦ Difference in earlier 143(1)(a) and present 143(1)

Hilltop Holdings India Ltd Vs CIT 278 ITR 501 (Cal ) Hilltop Holdings India Ltd. Vs. CIT 278 ITR 501 (Cal.) Effect of SC decision in◦ Rajesh Jhaveri Stock Brokers 291 ITR 500◦ Zuari Estate Development & Investment 373 ITR 661

03/12/2015 13

p

03/12/2015 Vajani & Vajani 13

Explanation – Record shall mean all therecords at the time of examination by therecords at the time of examination by theCommissioner

Valuation Report submitted byD l V l i C ll hDepartmental Valuation Cell post theassessment is part of the record◦ CIT Vs. Shree Manjunathesware Packing Productsj g

& Camphor Works (1998) 231 ITR 53 (SC) CIT has power to take action under s. 263

in the case of an assessee even on the basisof the records in the cases of other persons◦ CIT Vs. Arunaben Sumankumar (2003) 259 ITR

386 (Guj)

03/12/2015 14

( j)

Malabar Industrial Co. Ltd. Vs. CIT (2000) 243 ITR 83 (SC)

• The CIT has to be satisfied of twin conditions namely (i) the• The CIT has to be satisfied of twin conditions, namely, (i) theorder of the AO sought to be revised is erroneous; and (ii) itis prejudicial to the interests of the Revenue. If one of themis absent—if the order of the ITO is erroneous but is notprejudicial to the Revenue or if it is not erroneous but is

j di i l h R b h dp jprejudicial to the Revenue—recourse cannot be had to s.263(1) of the Act.

• The phrase ‘prejudicial to the interests of the Revenue’ isnot an expression of art and is not defined in the Actnot an expression of art and is not defined in the Act.Understood in its ordinary meaning it is of wide import andis not confined to loss of tax.

• The scheme of the Act is to levy and collect tax in• The scheme of the Act is to levy and collect tax inaccordance with the provisions of the Act and this task isentrusted to the Revenue. If due to an erroneous order ofthe ITO, the Revenue is losing tax lawfully payable by aperson, it will certainly be prejudicial to the interests of theR

03/12/2015 1503/12/2015 Vajani & Vajani 1503/12/2015 15

p y p jRevenue.

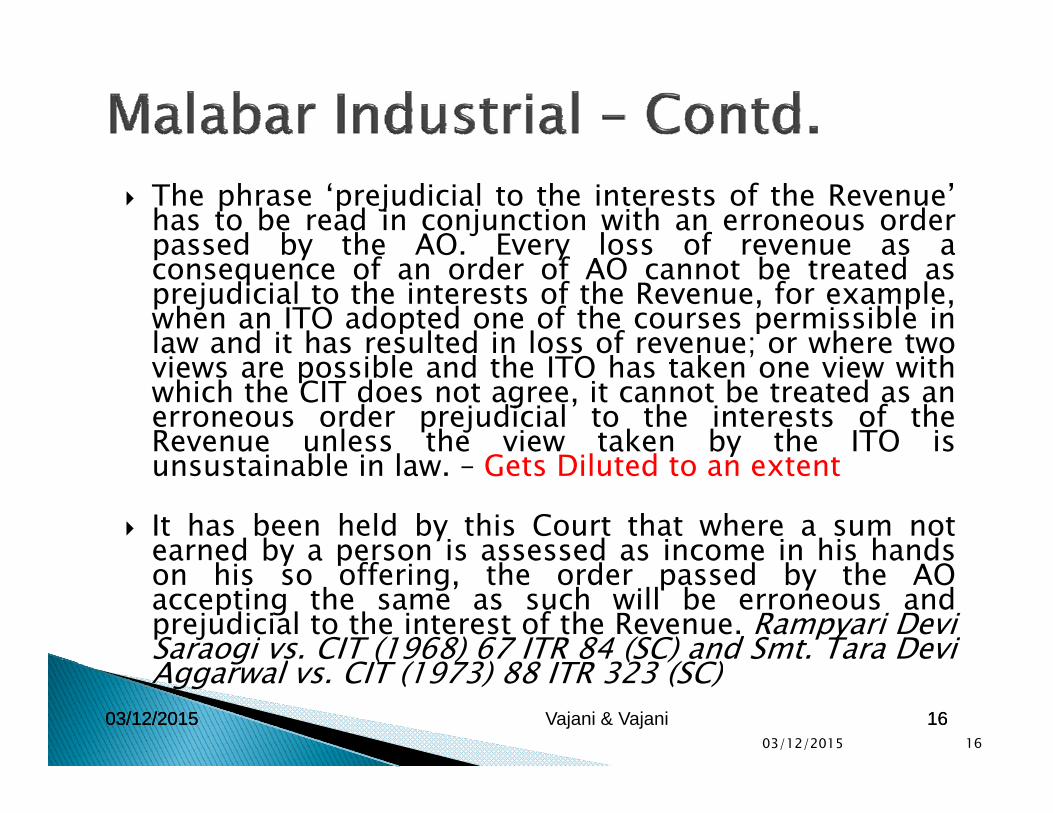

The phrase ‘prejudicial to the interests of the Revenue’has to be read in conjunction with an erroneous orderpassed by the AO. Every loss of revenue as apassed by the AO. Every loss of revenue as aconsequence of an order of AO cannot be treated asprejudicial to the interests of the Revenue, for example,when an ITO adopted one of the courses permissible inlaw and it has resulted in loss of revenue; or where two

bl d h h k h;

views are possible and the ITO has taken one view withwhich the CIT does not agree, it cannot be treated as anerroneous order prejudicial to the interests of theRevenue unless the view taken by the ITO is

t i bl i l G t Dil t d t t tunsustainable in law. – Gets Diluted to an extent

It has been held by this Court that where a sum notearned by a person is assessed as income in his handsea ed by a pe so s assessed as co e s a dson his so offering, the order passed by the AOaccepting the same as such will be erroneous andprejudicial to the interest of the Revenue. Rampyari DeviSaraogi vs. CIT (1968) 67 ITR 84 (SC) and Smt. Tara DeviA l CIT (1973) 88 ITR 323 (SC)

03/12/2015 1603/12/2015 Vajani & Vajani 1603/12/2015 16

gAggarwal vs. CIT (1973) 88 ITR 323 (SC)

One of the two possible views followed by AO Order though may be prejudicial but can not beg y p j

said to be erroneous◦ CIT Vs. Arvind Jewellers 259 ITR 502 (Guj)

CIT Vs. CIT Vs. Max India Ltd. (2007) 295 ITR( )282 (SC)◦ Where two views are possible and the ITO has taken

one view with which the CIT does not agree, it cannotb d d j di i l hbe treated as an erroneous order prejudicial to theinterest of the Revenue, unless the view taken by theITO is unsustainable in law

Effect of Explanation – 2 Clause (d) Effect of Explanation – 2 Clause (d) Whether the Explanation can override

substantive provision and settled principles ?

03/12/2015 17

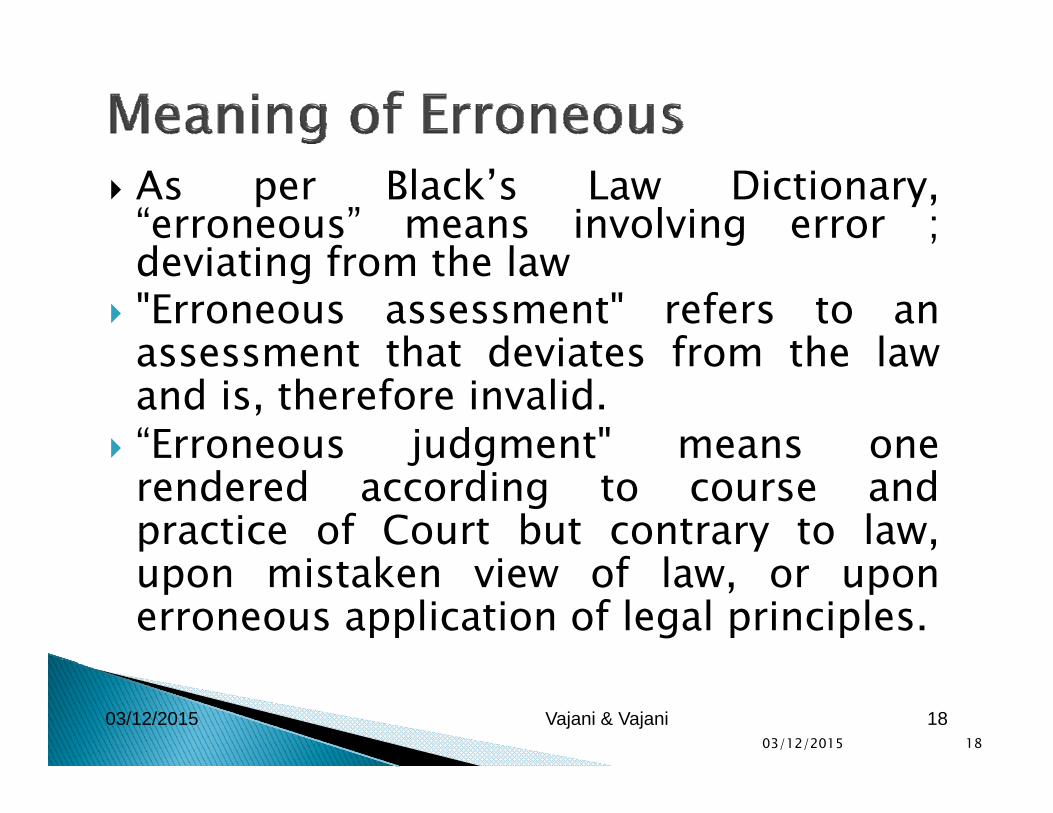

As per Black’s Law Dictionary,“erroneous” means involving error ;d i ti f th ldeviating from the law

"Erroneous assessment" refers to anassessment that deviates from the lawassessment that deviates from the lawand is, therefore invalid.

“Erroneous judgment" means oneo eous judg e t ea s o erendered according to course andpractice of Court but contrary to law,

i k i f lupon mistaken view of law, or uponerroneous application of legal principles.

03/12/2015 1803/12/2015 Vajani & Vajani 18

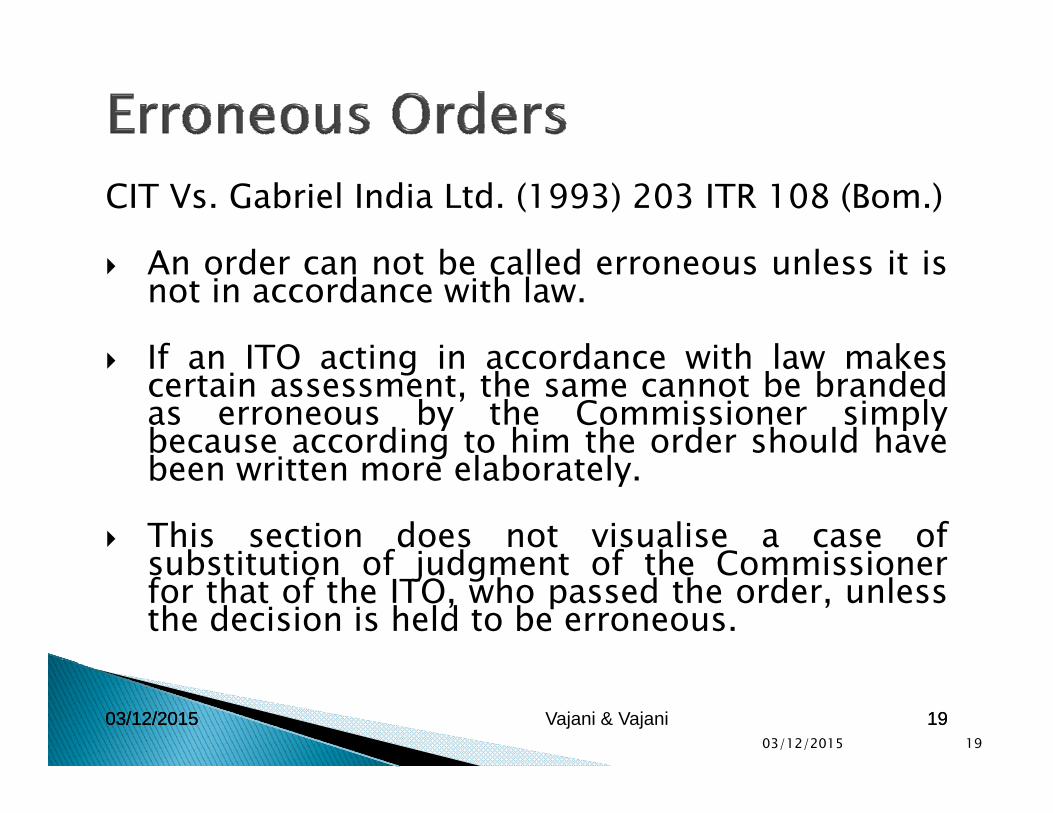

CIT Vs. Gabriel India Ltd. (1993) 203 ITR 108 (Bom.)

A d b ll d l i i An order can not be called erroneous unless it isnot in accordance with law.

If an ITO acting in accordance with law makes If an ITO acting in accordance with law makescertain assessment, the same cannot be brandedas erroneous by the Commissioner simplybecause according to him the order should haveb i l b l

gbeen written more elaborately.

This section does not visualise a case ofsubstitution of judgment of the Commissionersubstitution of judgment of the Commissionerfor that of the ITO, who passed the order, unlessthe decision is held to be erroneous.

03/12/2015 1903/12/2015 Vajani & Vajani 1903/12/2015 19

A conclusion cannot be termed to be erroneoussimply because the Commissioner does notfeel satisfied with the conclusion It may befeel satisfied with the conclusion. It may besaid in such a case that in the opinion of theCommissioner the order in question isprejudicial to the interest of the Revenue. Butth t b it lf ill t b h t t ththat by itself will not be enough to vest theCommissioner with the power of suo moturevision because the first requirement, namely,the order is erroneous, is absent.the order is erroneous, is absent.

Similarly if an order is erroneous but notprejudicial to the interest of the Revenue, thenl th f t i i t balso the power of suo motu revision cannot be

exercised. Any and every erroneous ordercannot be subject-matter of revision becausethe second requirement also must be fulfilled.

03/12/2015 2003/12/2015 Vajani & Vajani 2003/12/2015 20

the second requirement also must be fulfilled.

CIT Vs. Jawahar Bhatacharjee (2012) 341 ITR434 (G )(FB) A t d434 (Gau.)(FB) – Assessment made on◦ wrong assumption of facts or◦ on incorrect application of law orpp◦ without due application of mind or◦ without following the principles of natural justice

would be 'erroneous‘ Failure to apply the correct provision of law

as may be applicable in given facts of thecase will be resulting in an erroneous ordercase will be resulting in an erroneous order –CIT Vs. Emery Stone Manufacturing Co.(1995) 213 ITR 843 (Raj)

03/12/2015 2103/12/2015 Vajani & Vajani 21

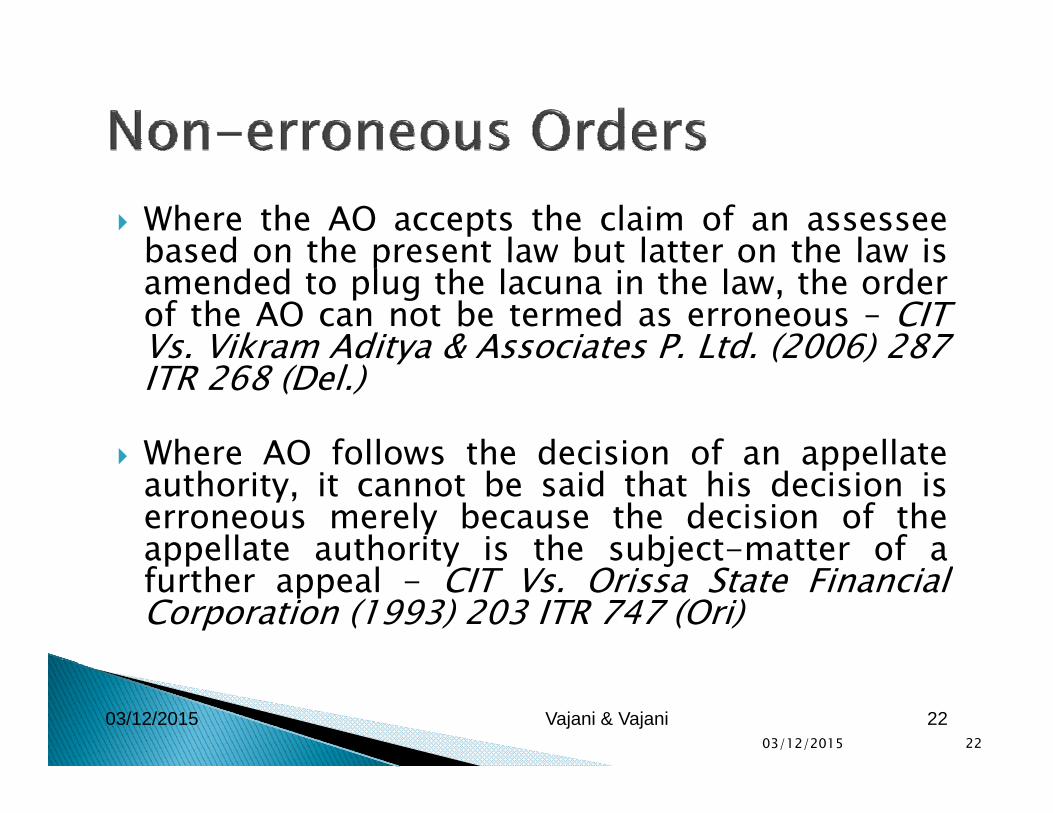

Where the AO accepts the claim of an assesseebased on the present law but latter on the law isbased on the present law but latter on the law isamended to plug the lacuna in the law, the orderof the AO can not be termed as erroneous – CITVs. Vikram Aditya & Associates P. Ltd. (2006) 287Vs. Vikram Aditya & Associates P. Ltd. (2006) 287ITR 268 (Del.)

Where AO follows the decision of an appellate Where AO follows the decision of an appellateauthority, it cannot be said that his decision iserroneous merely because the decision of theappellate authority is the subject-matter of aappe ate aut o ty s t e subject atte o afurther appeal - CIT Vs. Orissa State FinancialCorporation (1993) 203 ITR 747 (Ori)

03/12/2015 2203/12/2015 Vajani & Vajani 22

Order of AO can be treated as erroneouswhere the AO does not make any inquiryabout a particular issue

Difference between Lack of inquiry and Difference between Lack of inquiry andinadequate inquiry Effect of Explanation 2 (a)◦ CIT Vs. Sunbeam Auto Ltd. (2011) 332 ITR 167CIT Vs. Sunbeam Auto Ltd. (2011) 332 ITR 167

(Del.)◦ CIT Vs. Vikas Polymers (2012) 341 ITR 537 (Del)

03/12/2015 23

AO is required to apply his mind to thef f h ’facts of the assessee’s case

If from the records, it can be seen that noinquiry is made by the AO on a particularinquiry is made by the AO on a particularissue then the order is prone to Revision

Where AO made applied his mind to aparticular issue but did not apply his mindto any other issue – the Revision ispermissible for the area where there is notpermissible for the area where there is notapplication of mind - CIT Vs. HindustanLever Ltd. (2012) 343 ITR 161 (Bom.)

03/12/2015 24

Lack of Inquiry is different than possiblef hfurther inquiries

Possibility of further inquiries will not be areason for revision Effect of Explanation 2reason for revision - Effect of Explanation -2(a)◦ Baljees Vs. ACIT (2004) 85 TTJ (Chd) 543◦ Salora International Ltd. Vs. Addl. CIT (2005) 2 SOT

705 (Del.)◦ Amrik Singh Vs. ACIT (2010) 36 DTR (Chd)(Trib) 111Amrik Singh Vs. ACIT (2010) 36 DTR (Chd)(Trib) 111

CIT can also not make fishing or roving inquiryin revision proceedings - Explanation 2(a)

03/12/2015 25

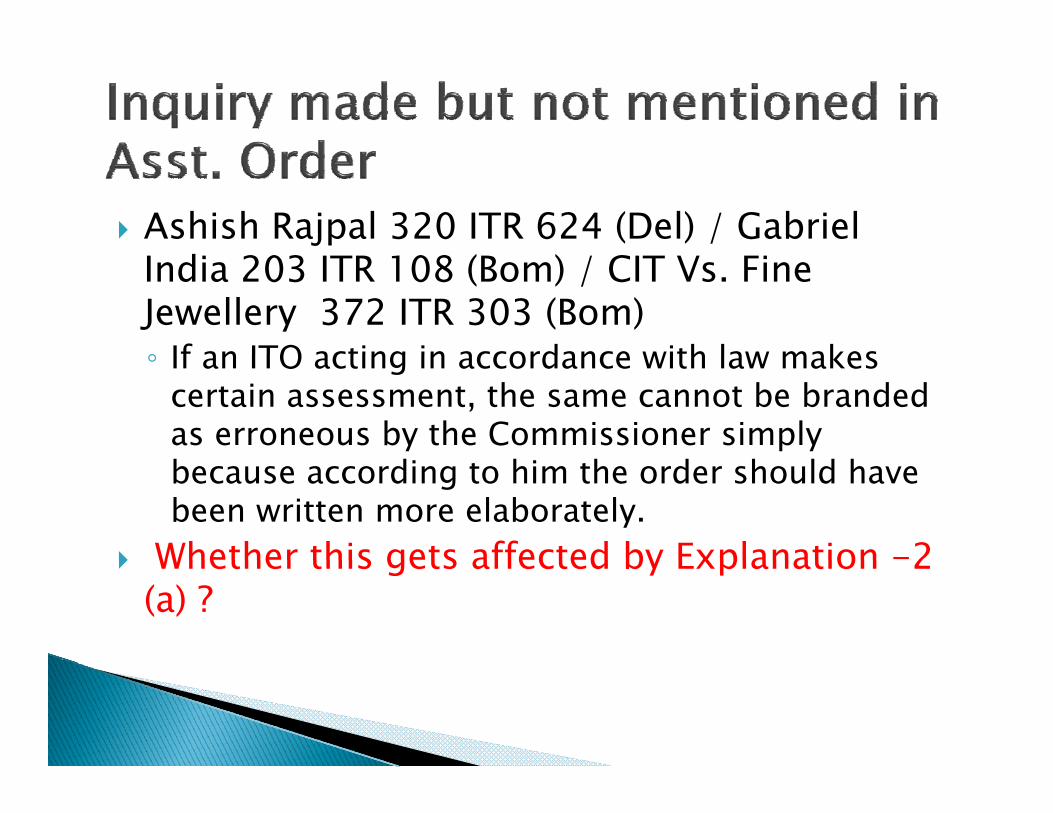

Ashish Rajpal 320 ITR 624 (Del) / Gabriel India 203 ITR 108 (Bom) / CIT Vs. Fine Jewellery 372 ITR 303 (Bom) ◦ If an ITO acting in accordance with law makes◦ If an ITO acting in accordance with law makes

certain assessment, the same cannot be branded as erroneous by the Commissioner simply because according to him the order should have been written more elaborately.

Whether this gets affected by Explanation -2 Whether this gets affected by Explanation 2 (a) ?

Favourable view : Penalty proceedings are separateproceedings and they do not form part of theproceedings and they do not form part of theassessment proceedings.◦ Addl CIT Vs. J. K. D’costa (1982) 133 ITR 7 (Del.) - SLP

dismissed at [(1984) 147 ITR (St ) 1]dismissed at [(1984) 147 ITR (St.) 1]◦ CIT Vs. Keshrimal Parasmal (1985) 157 ITR 484 (Raj)◦ Surendra Prasad Singh & Others Vs. CIT (1988) 173 ITR 510

(Gau.)(Gau.)◦ CIT Vs. Subhash Kumar Jain (2011) 335 ITR 364 (P & H)

CIT can not set aside the assessment order for sole CIT can not set aside the assessment order for solepurpose of initiation of penalty proceedings – CITVs. Parmanand M. Patel (2005) 278 ITR 3 (Guj)

03/12/2015 27

Contrary view : The AO has to initiate the penalty proceedingsduring the assessment proceedings. Failure to initiate penaltyg p g p ymeans that AO has not decided an issue which ought to havebeen decided by him during the assessment proceedings◦ Addl CIT Vs. Indian Pharmaceuticals (1980) 123 ITR 874 (MP)◦ CIT Vs. Surendra Prasad Agrawal (2005) 275 ITR 113 (All)CIT Vs. Surendra Prasad Agrawal (2005) 275 ITR 113 (All)◦ CIT Vs. Ashok Construction Co. (2006) 280 ITR 368 (All.)

C.A. Abraham vs. ITO (1961) 41 ITR 425 (SC) and CIT vs.Bhikaji Dadabhai & Co (1961) 42 ITR 123 (SC) has held thatBhikaji Dadabhai & Co. (1961) 42 ITR 123 (SC) has held thatthe assessment does not mean only computation of incomebut consideration of all facts including the liability for penaltythat may attract the provisions contained in s. 271(1)(a) of theActAct.

Agreed additions or conditional offer and the effect of MakData P. Ltd. Vs. CIT (2013) 358 ITR 593 (SC)

03/12/2015 28

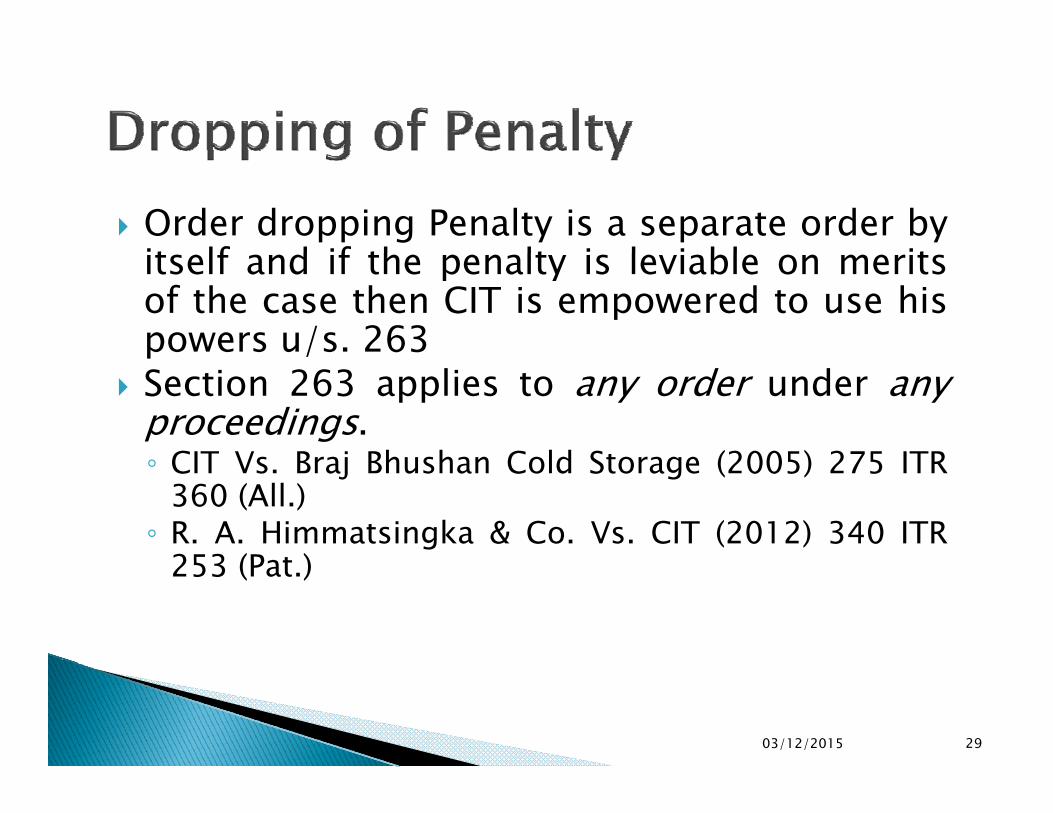

Order dropping Penalty is a separate order byit lf d if th lt i l i bl ititself and if the penalty is leviable on meritsof the case then CIT is empowered to use hispowers u/s. 263p /

Section 263 applies to any order under anyproceedings.

CIT Vs Braj Bhushan Cold Storage (2005) 275 ITR◦ CIT Vs. Braj Bhushan Cold Storage (2005) 275 ITR360 (All.)◦ R. A. Himmatsingka & Co. Vs. CIT (2012) 340 ITR

253 (Pat )253 (Pat.)

03/12/2015 29

Retrospective Amendment made after the AOpasses the order – whether revision permissiblepasses the order whether revision permissible

Position on date of order Vs. Position on date ofexamination by CIT

Revision held permissible – CIT Vs. VincastEngineering (2006) 280 ITR 385 (All) NoneEngineering (2006) 280 ITR 385 (All) – Noneappeared for Assessee

Law shall be seen as on the date when the AOpassed the order -p

Revision held not permissible – CIT Vs. Saluja EximLtd. (2010) 329 ITR 603 (P & H) following CIT Vs.Max India Ltd. (2007) 295 ITR 282 (SC)◦ In Max India the fact was that two views were possible at◦ In Max India, the fact was that two views were possible at

the time of passing of the revision order by CIT and theretrospective amendment was made after the order u/s.263 by CIT.

03/12/2015 30

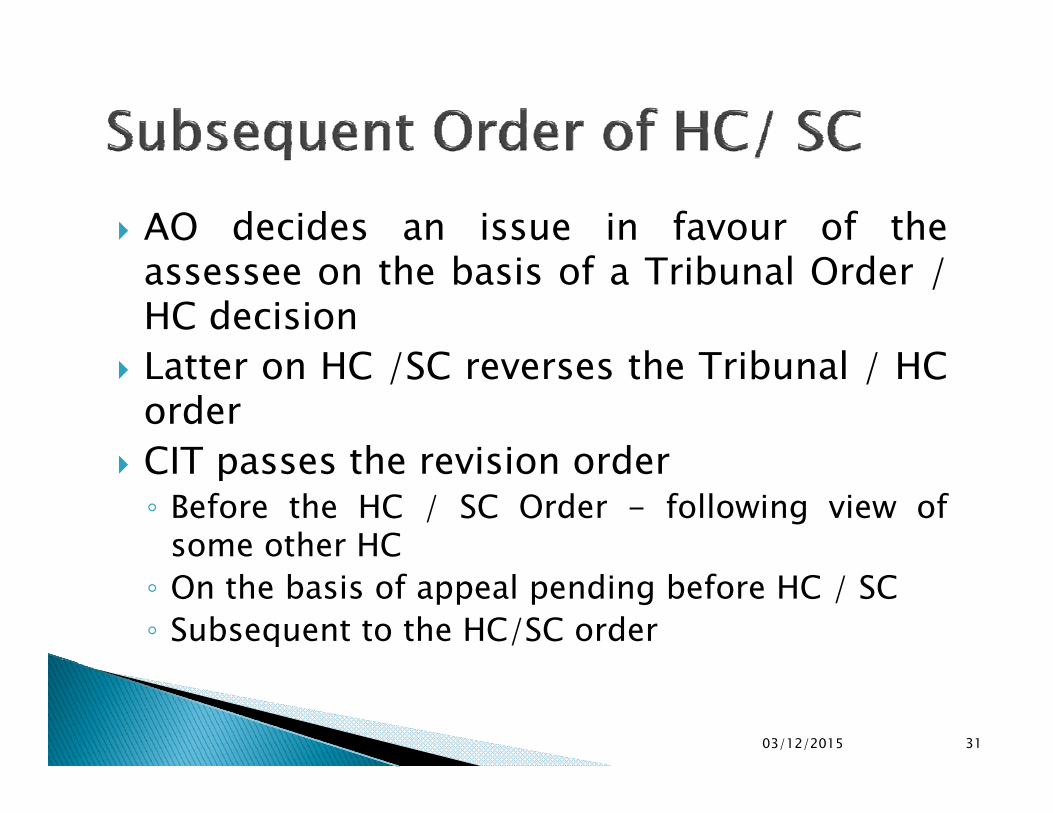

AO decides an issue in favour of theassessee on the basis of a Tribunal Order /HC decisionL tt HC /SC th T ib l / HC Latter on HC /SC reverses the Tribunal / HCorder

CIT passes the revision order CIT passes the revision order◦ Before the HC / SC Order - following view of

some other HC◦ On the basis of appeal pending before HC / SC◦ Subsequent to the HC/SC order

03/12/2015 31

Before the order of Higher forum◦ CIT Vs. G. M. Mittal Stainless Steel P. Ltd. (2003)

263 ITR 255 (SC) Pending appeal before Higher forum Pending appeal before Higher forum◦ K. N. Agarwal Vs. CIT (1991) 189 ITR 769 (All)◦ CIT Vs. Paul Brothers (1995) 216 ITR 548 (Bom( ) (

HC – Nag. Bench) Subsequent to the order from HC /SC◦ CIT Vs. Seshasayee Paper Boards Ltd. (1996) 217

ITR 358 (Mad.)

03/12/2015 32

AO refers the matter to TPO and passes assessment order inpursuance of the same – whether the order of AO can berevised

If AO fails to refer the case to in a case where it is necessaryas per CBDT instruction then the order is subject to revision– Ranbaxy Laboratories Ltd Vs CIT (2012) 345 ITR 193Ranbaxy Laboratories Ltd. Vs. CIT (2012) 345 ITR 193(Delhi)

There can not be any error in the order of AO since he hasf ll d h i i d d li d ALPfollowed the requisite procedure and applied to ALPcomputed by TPO – Essar Steel Ltd. Vs. Addl CIT (2013) 55SOT 1 (Mumbai)(URO)

Order passed by TPO can not be subject to section 263 – CITdoes not have a power to revise TPO’s order – TataCommunications Ltd. Vs. Dy. CIT ITA (TP) No. 3121 &3122/Mum/2013 – order dated 20-12-2013 – itatonline.org

03/12/2015 33

3122/Mum/2013 order dated 20 12 2013 itatonline.org

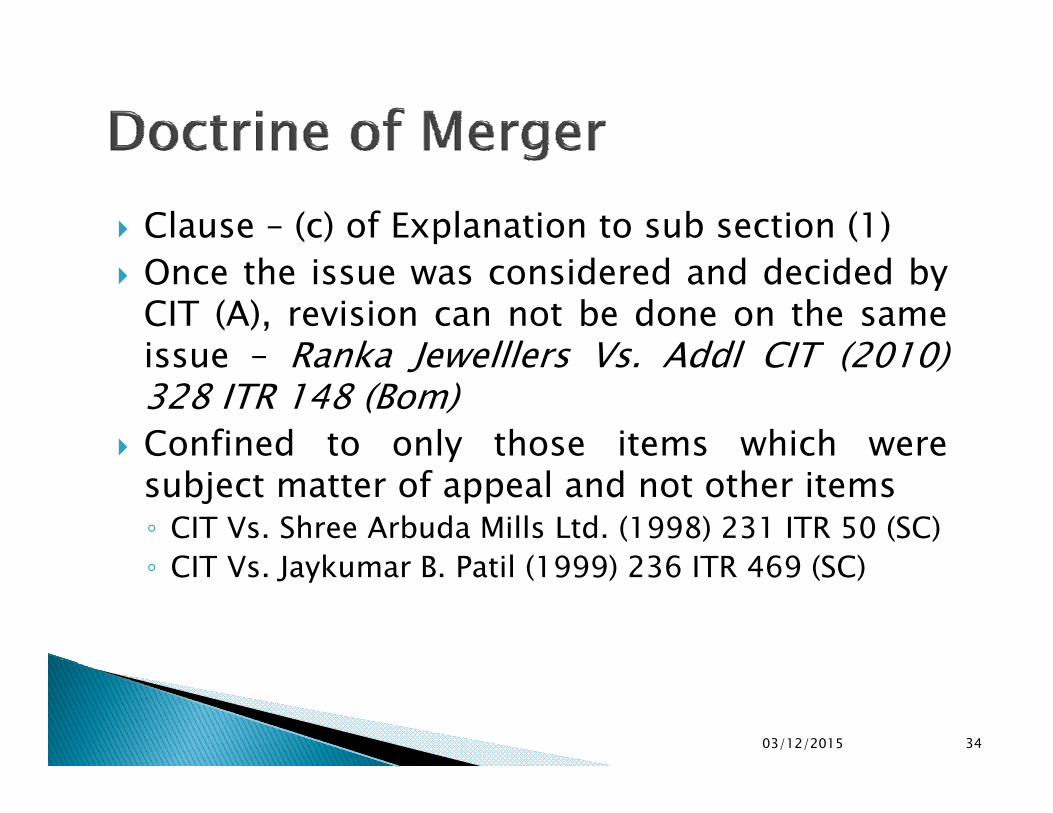

Clause – (c) of Explanation to sub section (1) Once the issue was considered and decided by

CIT (A), revision can not be done on the sameissue Ranka Jewelllers Vs Addl CIT (2010)issue – Ranka Jewelllers Vs. Addl CIT (2010)328 ITR 148 (Bom)

Confined to only those items which wereysubject matter of appeal and not other items◦ CIT Vs. Shree Arbuda Mills Ltd. (1998) 231 ITR 50 (SC)

CIT V J k B P til (1999) 236 ITR 469 (SC)◦ CIT Vs. Jaykumar B. Patil (1999) 236 ITR 469 (SC)

03/12/2015 34

CIT Vs. Ratilal Bacharilal & Sons (2006) 282ITR 457 (Bom)ITR 457 (Bom)◦ Deduction claimed u/s. 35B Rs. 8,90,676/-◦ AO allowed Rs. 5,63,350/-

A l f b l di i d b CIT (A)◦ Appeal for balance dismissed by CIT (A)◦ Latter CIT invoked revision in respect of Rs.

5,63,350/- for the reason that same was allowedwithout verifying the detailswithout verifying the details.

◦ Held Revision possible Assessee could not have been aggrieved for the amount

allowed and hence appeal was only in respect of amountallowed and hence appeal was only in respect of amountnot allowed

Merger not in respect of the amount allowed by AO

03/12/2015 35

CIT Vs. Shashi Theatre Pvt. Ltd. (2001) 248 ITR126 (Guj)

◦ AO allowed investment allowance on some of theitems of Fixed Assetsitems of Fixed Assets

◦ CIT (A) allowed on the remaining items◦ CIT proposed revision for the deduction allowed

b AOby AO◦ Held revision not possible since the order of AO

has merged with the order of CIT (A)g ( )

03/12/2015 36

Same Subject Matterj◦ CWT Vs. Sampathmal Chordia,

Executor to the Estate of Late NeniExecutor to the Estate of Late NeniKavur Bai (2002) 256 ITR 440 (Mad)

Different Subject MatterDifferent Subject Matter◦ Aerens Infrastructure & Technology

Ltd Vs CIT (2004) 271 ITR 15 (Del )Ltd. Vs. CIT (2004) 271 ITR 15 (Del.)

03/12/2015 37

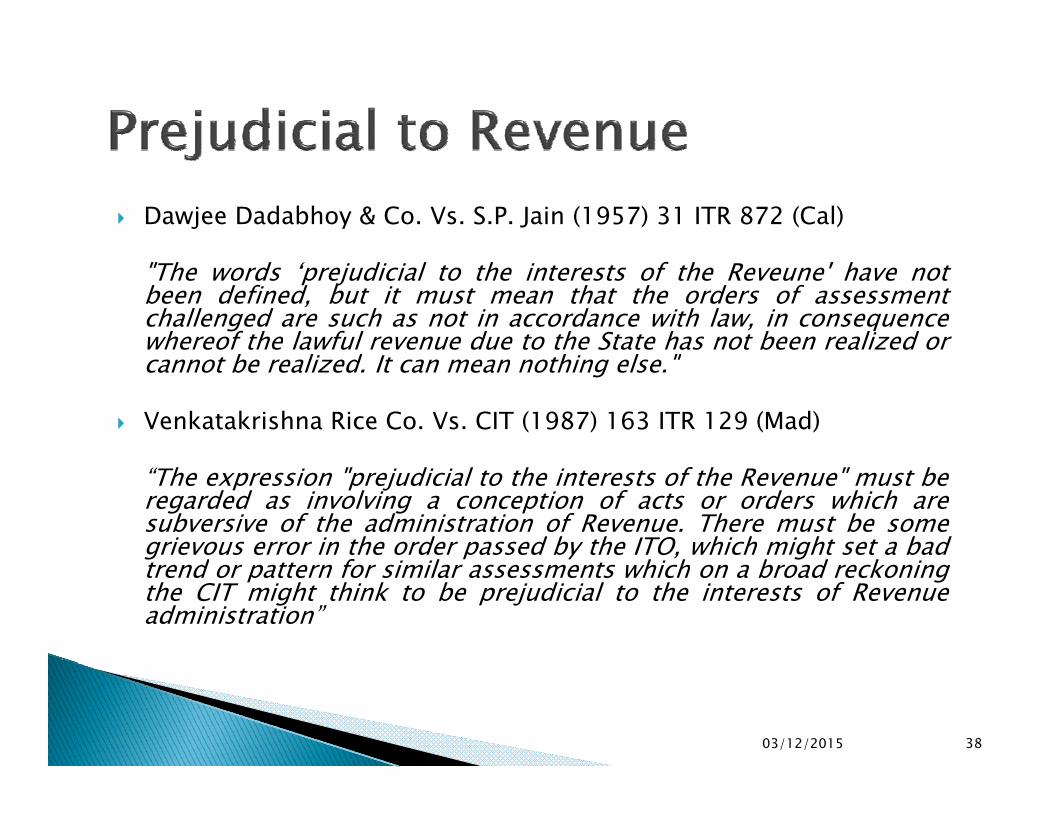

Dawjee Dadabhoy & Co. Vs. S.P. Jain (1957) 31 ITR 872 (Cal)

"The words ‘prejudicial to the interests of the Reveune' have notbeen defined, but it must mean that the orders of assessmentchallenged are such as not in accordance with law, in consequencewhereof the lawful revenue due to the State has not been realized or

b li d I hi l "cannot be realized. It can mean nothing else."

Venkatakrishna Rice Co. Vs. CIT (1987) 163 ITR 129 (Mad)

“The expression "prejudicial to the interests of the Revenue" must beregarded as involving a conception of acts or orders which aresubversive of the administration of Revenue. There must be somegrievous error in the order passed by the ITO, which might set a bad

d f i il hi h b d k itrend or pattern for similar assessments which on a broad reckoningthe CIT might think to be prejudicial to the interests of Revenueadministration”

03/12/2015 38

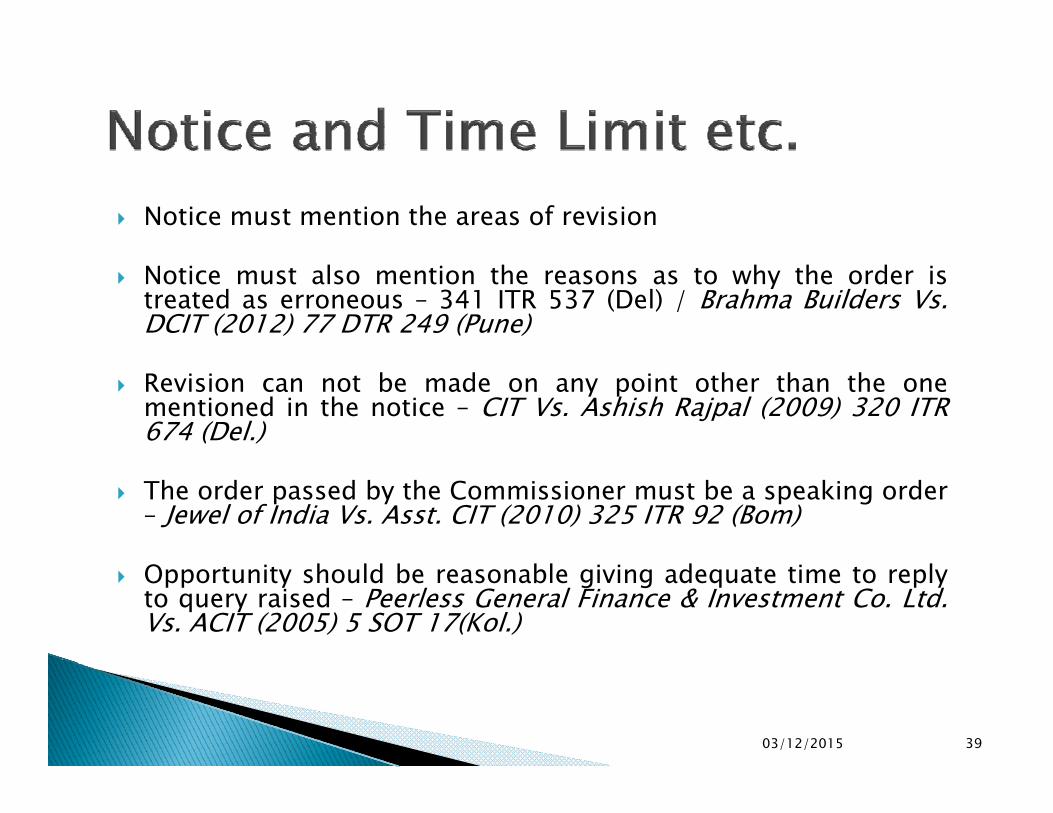

Notice must mention the areas of revision

Notice must also mention the reasons as to why the order istreated as erroneous – 341 ITR 537 (Del) / Brahma Builders Vs.DCIT (2012) 77 DTR 249 (Pune)

Revision can not be made on any point other than the onementioned in the notice – CIT Vs. Ashish Rajpal (2009) 320 ITR674 (Del.)

The order passed by the Commissioner must be a speaking order– Jewel of India Vs. Asst. CIT (2010) 325 ITR 92 (Bom)

Opportunity should be reasonable giving adequate time to replyto query raised – Peerless General Finance & Investment Co. Ltd.Vs. ACIT (2005) 5 SOT 17(Kol.)

03/12/2015 39

Time Limit of 2 years shall beyreckoned from the order sought tobe revised

CIT Vs. Allagendran FinanceLtd.(2007) 293 ITR 1 (SC)◦ Reassessment made u/s. 147◦ CIT sought to revise the issues dealt in the original

assessment◦ Time Limit to be reckoned from original order

Rectification order u/s. 154

03/12/2015 40

Appeal can be filed to ITAT against the orderf th CIT / 263of the CIT u/s. 263

AO will pass an order u/s. 143(3) r.w.s. 263of the Act as per the directions given in theof the Act as per the directions given in theorder u/s. 263

Time Limit for AO : Section 153 (2A) – Withinf th d f th fi i lone year from the end of the financial year

from the date of order u/s. 263

03/12/2015 41

Can assessee seek a new benefit in such assessment◦ Section 263 applies to only order which are prejudicial toSection 263 applies to only order which are prejudicial to

revenue◦ Alternate remedies are available to assessee for the areas

where it is aggrievedHindu Bank Karur Ltd Vs Addl CIT (1976) 103 ITR 553◦ Hindu Bank Karur Ltd. Vs. Addl. CIT (1976) 103 ITR 553(Mad)

◦ Asst. CIT Vs. ITW India (P) Ltd. (2010) 40 SOT 348 (Hyd)

No appeal filed against Revision order – Whether appealcan be filed against order u/s. 143(3) r.w.s. 263

C B O S P d t Ltd V ACIT (2012) 138 ITD 542◦ Crew B.O.S. Products Ltd. Vs. ACIT (2012) 138 ITD 542(Del.)

03/12/2015 42

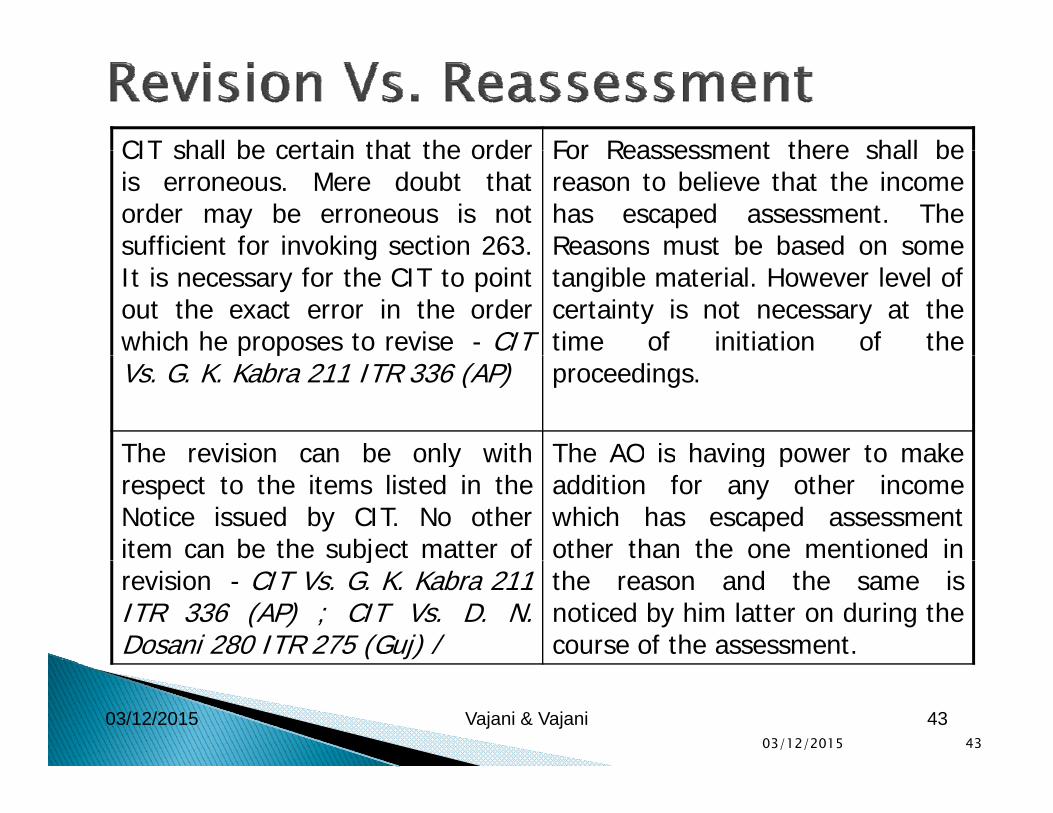

CIT shall be certain that the order For Reassessment there shall beCIT shall be certain that the orderis erroneous. Mere doubt thatorder may be erroneous is notsufficient for invoking section 263.

For Reassessment there shall bereason to believe that the incomehas escaped assessment. TheReasons must be based on somesufficient for invoking section 263.

It is necessary for the CIT to pointout the exact error in the orderwhich he proposes to revise - CIT

Reasons must be based on sometangible material. However level ofcertainty is not necessary at thetime of initiation of thep p

Vs. G. K. Kabra 211 ITR 336 (AP) proceedings.

The revision can be only with The AO is having power to makeThe revision can be only withrespect to the items listed in theNotice issued by CIT. No otheritem can be the subject matter of

The AO is having power to makeaddition for any other incomewhich has escaped assessmentother than the one mentioned inj

revision - CIT Vs. G. K. Kabra 211ITR 336 (AP) ; CIT Vs. D. N.Dosani 280 ITR 275 (Guj) /

the reason and the same isnoticed by him latter on during thecourse of the assessment.

03/12/2015 4303/12/2015 Vajani & Vajani 43

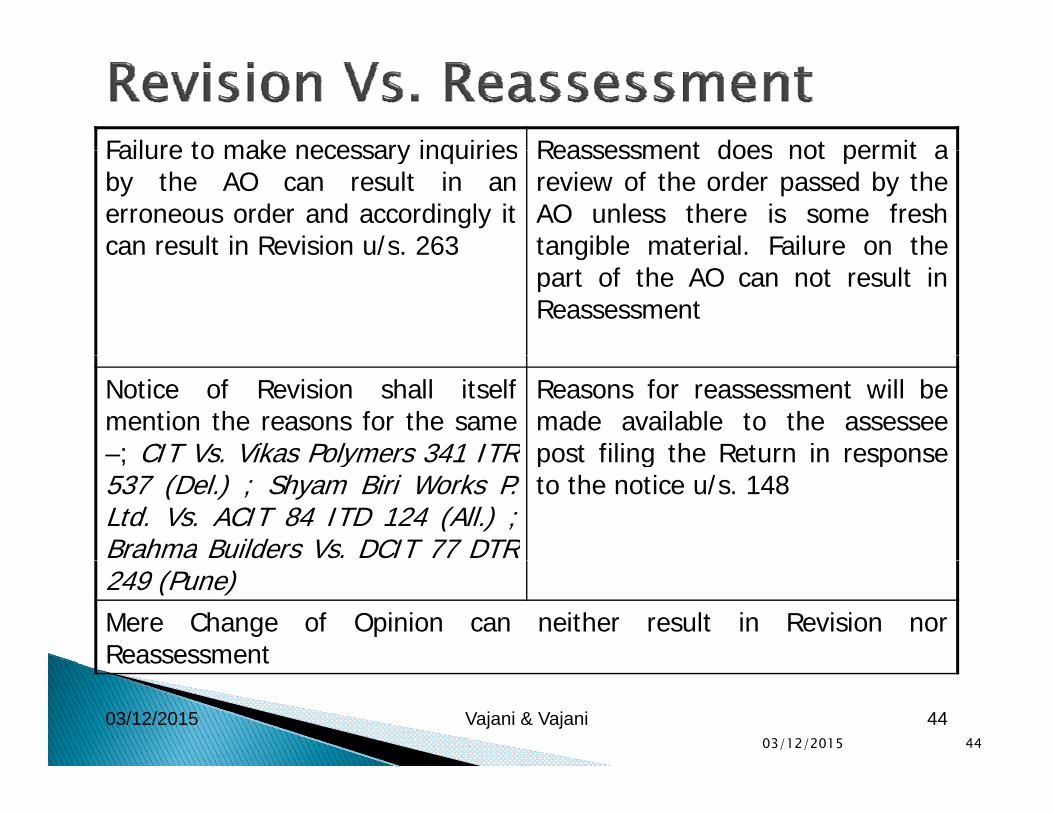

Failure to make necessary inquiries Reassessment does not permit aFailure to make necessary inquiriesby the AO can result in anerroneous order and accordingly itcan result in Revision u/s. 263

Reassessment does not permit areview of the order passed by theAO unless there is some freshtangible material. Failure on thecan result in Revision u/s. 263 tangible material. Failure on thepart of the AO can not result inReassessment

Notice of Revision shall itselfmention the reasons for the same–; CIT Vs Vikas Polymers 341 ITR

Reasons for reassessment will bemade available to the assesseepost filing the Return in response; CIT Vs. Vikas Polymers 341 ITR

537 (Del.) ; Shyam Biri Works P.Ltd. Vs. ACIT 84 ITD 124 (All.) ;Brahma Builders Vs. DCIT 77 DTR

post filing the Return in responseto the notice u/s. 148

249 (Pune)Mere Change of Opinion can neither result in Revision norReassessment

03/12/2015 4403/12/2015 Vajani & Vajani 44

Reassessment

Vajani & VajaniVajani & VajaniChartered AccountantsPhone : 2375 9876 / 2374 0792Phone : 2375 9876 / 2374 0792Handphone : 98205 25972Email:[email protected]