Revised Version of Risk Management - a conceptual framework

19

Risk Management: A Conceptual Framework B.V.Raghunandan, SVS College, Bantwal-Karnataka-India

-

Upload

svs-college -

Category

Economy & Finance

-

view

164 -

download

1

description

A more detailed account of the preliminaries of risk management

Transcript of Revised Version of Risk Management - a conceptual framework

Risk Management: A Conceptual Framework

B.V.Raghunandan,

SVS College,

Bantwal-Karnataka-India

Meaning of Risk• Risk is defined as possibility of loss• Lico Reis, ”Degree of uncertainty of return

on an asset”• Investopedia (www.invetopedia.com), ”

The chance that an investment's actual return will be different than expected”.

• Philippe Jorion, ”the volatility of unexpected outcomes, which can represent the value of assets, equity or earnings”

Classification of Risks

Risk

Pure Risk

Life Insurance General Insurance

Speculative Risk

Financial, Business,

Market and Interest Risk

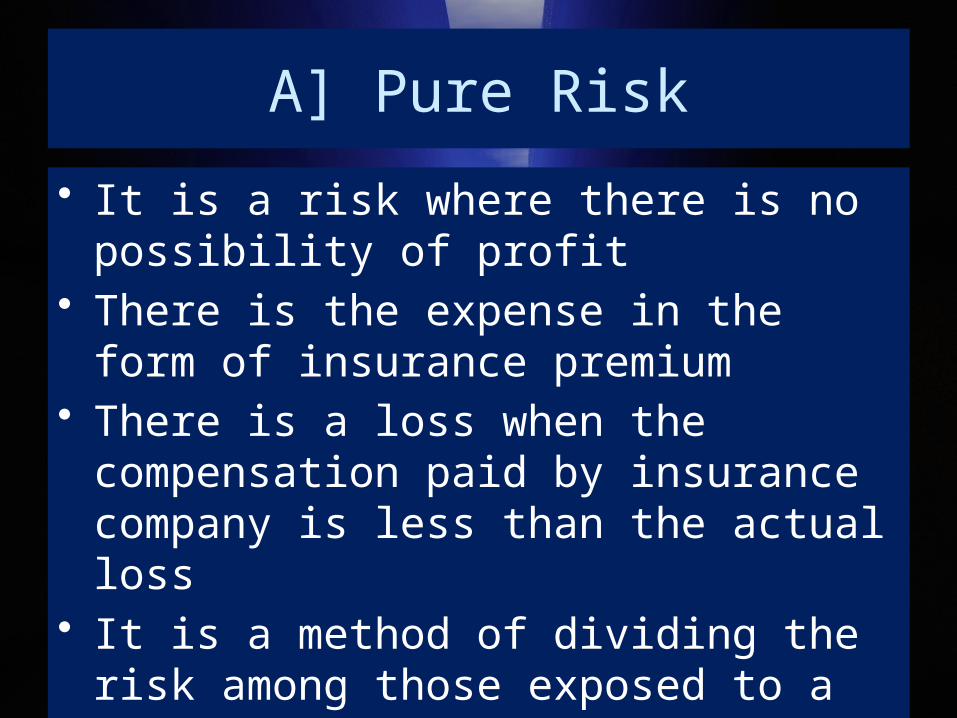

A] Pure Risk

• It is a risk where there is no possibility of profit

• There is the expense in the form of insurance premium

• There is a loss when the compensation paid by insurance company is less than the actual loss

• It is a method of dividing the risk among those exposed to a particular type of risk

B] Speculative Risk

• Speculative risk not only attempts to compensate for the loss, but may also bring in a profit

• Financial risk management tools may bring in profit apart from covering the risk

A] Pure Risk Management

• Life Insurance and General Insurance• Life Insurance Principles: Utmost Good

faith, and Insurable Interest• General Insurance Principles:

- Utmost Goodfaith

-Insurable Interest

-Indemnity

-Subrogation

-Contribution

Principle of Utmost Goodfaith

• Insured should reveal to the insurers all the material facts about the subject-matter

• This principle is applicable to all types of insurance contracts

• In life insurance, all the facts about the health of the insured person should be revealed to the insurers

• In case of any material facts concealed, the insurer can avoid his liability

Principle of Insurable Interest

• A person standing to gain from the existence of the subject matter or stands to lose by its destruction has insurable interest in the subject matter

• Everyone has insurable interest in his life, in the life of his spouse and in the lives of his children and vice versa

• In case properties, the owner has insurable interest and the lender on the security of the property

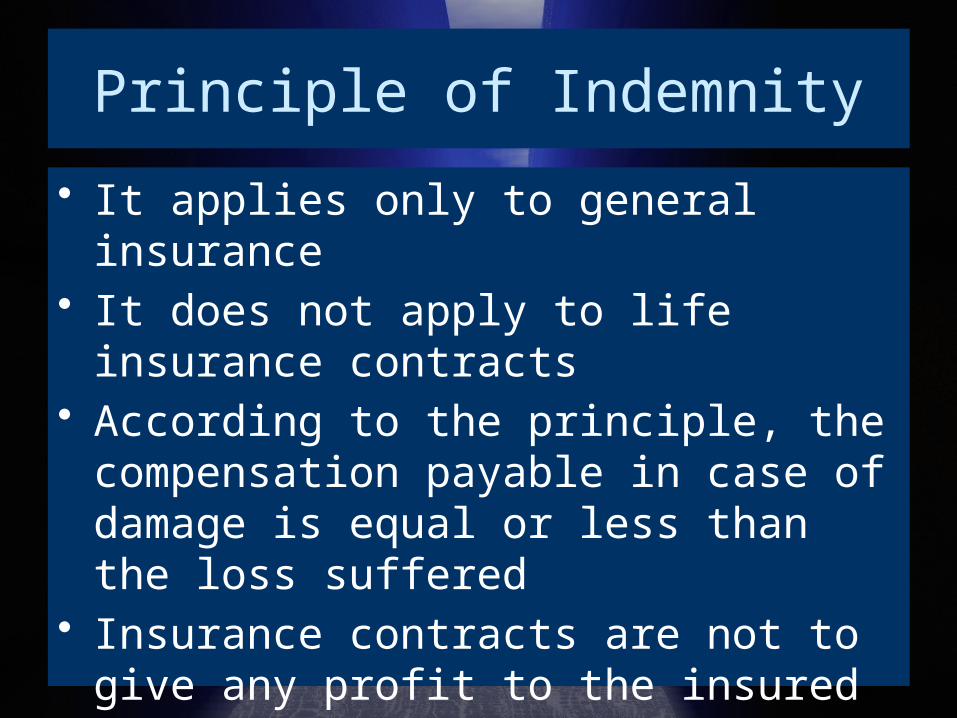

Principle of Indemnity

• It applies only to general insurance• It does not apply to life insurance contracts• According to the principle, the

compensation payable in case of damage is equal or less than the loss suffered

• Insurance contracts are not to give any profit to the insured

• Under no circumstance, the compensation will exceed the loss incurred

Principle of Subrogation

• It is an extension of the principle of indemnity

• Applicable to general insurance contracts and not to life insurance contracts

• Once the compensation is paid for the total loss of the subject matter, the insurers get the ownership of the damaged subject-matter

Principle of Contribution

• It is also an extension of principle of indemnity

• Applicable only to general insurance contracts and not to life insurance contracts

• In case of double insurance, both the insurers put together will contribute towards the compensation proportionately

• Both the insurers will give a compensation that will not exceed the loss

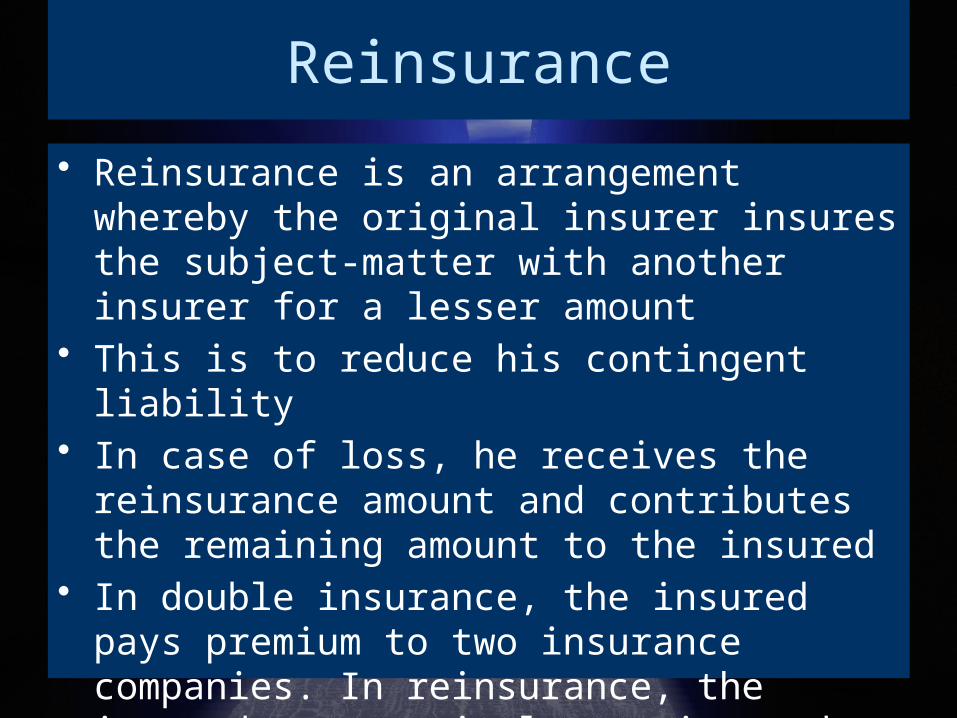

Reinsurance

• Reinsurance is an arrangement whereby the original insurer insures the subject-matter with another insurer for a lesser amount

• This is to reduce his contingent liability• In case of loss, he receives the reinsurance

amount and contributes the remaining amount to the insured

• In double insurance, the insured pays premium to two insurance companies. In reinsurance, the insured pays a single premium and the insurer pays a lesser premium to another insurer

Types of Pure Risks

• Risks relating to physical assets• Risks relating to human assets• Risks relating to liability

B] Speculative Risks

• Business Risk• Default Risk• Market Risk• Liquidity Risk• Credit Risk• Exchange Risk

• Financial Risk• External Environment

Risk• Environment Risk• Attrition Risk• Manufacturing Risk• Risk of Natural

Calamity

Handling the Risk

• Risk Management

• Risk Retention

Risk Management: Action

• Risk Avoidance• Diversification• Spin-off• Risk Transfer• Risk Sharing• Fighting Fire with

Fire

Risk Retention: Acceptance

• Rationale:

1. When it can not be avoided

2. High cost of management of risk

3. Risk management may increase loss

4. Where control is difficult

5. Where risk management is too complex

Risk Management Process: Steps Involved

1) Identification of Objectives: competition, stability in earnings, meeting customer expectation, treasury management, cost control, protecting foreign markets

2) Identification of Risks

3) Evaluation of Risk

4) Selection of Policy

5) Developing Strategy

6) Organisational Authority

7) Organisational Control & Corrective Action

THANK YOU