REVIEW OF CAPITAL REQUIREMENTS FOR BANKS...

24

Directorate General (Internal Market and Financial Services) European Commission Av de Cortenberg 107 B-1049 Bruxelles 16 th October 2003 Association of Private Client Investment Managers and Stockbrokers Company limited by guarantee Registered in England and Wales No. 2991400 VAT Registration No. 675 1363 26 London Office 112 Middlesex Street London E1 7HY Tel: +44 (0) 20 7247 7080 Fax: +44 (0) 20 7377 0939 Email: [email protected] Brussels Office Rue des Colonies 56 B-1000 Brussels Tel: +32 2 227 6565 Fax: +32 2 227 6524 REVIEW OF CAPITAL REQUIREMENTS FOR BANKS AND INVESTMENT FIRMS COMMISSION SERVICES THIRD CONSULTATION PAPER – 1 st JULY 2003

Transcript of REVIEW OF CAPITAL REQUIREMENTS FOR BANKS...

Directorate General (Internal Market and Financial Services) European Commission Av de Cortenberg 107

B-1049 Bruxelles

16th October 2003 Association of Private Client Investment Managers and Stockbrokers

Company limited by guarantee Registered in England and Wales No. 2991400

VAT Registration No. 675 1363 26

London Office 112 Middlesex Street

London E1 7HY Tel: +44 (0) 20 7247 7080 Fax: +44 (0) 20 7377 0939 Email: [email protected]

Brussels Office

Rue des Colonies 56 B-1000 Brussels

Tel: +32 2 227 6565 Fax: +32 2 227 6524

REVIEW OF CAPITAL REQUIREMENTS FOR BANKS AND INVESTMENT FIRMS

COMMISSION SERVICES THIRD CONSULTATION PAPER – 1st JULY 2003

2

INDEX 1. Introduction ............................................................................................. 3 2. Competitive Issues ................................................................................... 5 3. Simpler Investment Firms....................................................................... 5 4. The More Complex 730k Investment Firms........................................ 7 5. The Need for Further Differentiation of the 730k Category............. 8 6. Articulation of Expenditure Based Requirement and Operational Risk 10 7. Unsettled Transactions ............................................................................ 10 8. Business Lines ........................................................................................... 11 9. Supervisory Convergence and Consistency .......................................... 12 10. The Role of Insurance ........................................................................... 13 11. Outsourcing.............................................................................................. 13 12. The Asset Management Firm Operating under the Description of “Private Bank”.......................................................................................... 13 13. Cost Benefit Analysis .............................................................................. 14 Annex 1: Proposed QIS Questions for Investment Firms..................... 15 Annex 2: Investment Firm Statistics ......................................................... 17 Annex 3: Model A and Model B Clearing ................................................ 20 Annex 4: Operational Losses ...................................................................... 24

3

1. Introduction 1.1 We are grateful to the Commission Services for continuing to consult on the proposed

Risk Based Capital Directive and for emphasising the need to appropriately differentiate the capital adequacy framework where necessary from the new Basel Accord, to take account of the range and type of financial institutions that will be covered by the EU requirements.

1.2 APCIMS-EASD is the trade association representing the private client investment

community in the UK. In addition, we have European members, following our takeover of the European Association of Securities Dealers (EASD) eighteen months ago. Our 221 members include all the UK eligible firms who offer financial services in equities to the private client.

1.3 Our members operate on more than 500 locations, they have in excess of €300 billion

under management and administration and are primarily involved in portfolio management and stockbroking services on behalf of individual investors, charities and trusts. The remarks that we make with respect to the Capital proposals are therefore drawn from this perspective. In addition, the majority of our members are medium and small sized specialist independent firms.

1.4 Our members are particularly concerned that the Risk Based Capital Directive as it is

currently framed will have an adverse impact on investment firms and will put them at a competitive disadvantage to banks who offer the same services. The Risk Based Capital Directive uses the model of operational risk, credit risk and market risk developed by Basel and a bank that has exposure in these three areas is required to allocate capital more appropriately according to the actual risks of its business. The result is that in some areas of a bank’s operation, there will be capital reductions and, in other areas, capital increases with the intention of achieving overall neutrality. However, an investment firm does not have exposure to credit risk, exposure to market risk is incidental and often the only risk that it runs is operational risk. For this reason the Directive as it stands is cost additive for investment firms so render them uncompetitive.

1.5 The key issues for our members are:-

i. Although we welcome the improvements made by the Commission Services to their original proposals for applying the Basel treatment to all investment firms and we support the proposition that 50k and 125k firms should be left on EBR, we are still concerned that the application of the risk based capital requirements to many 730k investment firms will put them at a competitive disadvantage to banks.

ii. The more complex 730k category is intended for the more complex investment firms and needs to be more closely defined so that it does not include firms who may hold a principal position, but do not operate a trading book.

iii. Further differentiation and clarification of the business lines for investment firms is required with the intention of developing a more appropriate capital treatment for those firms which, whilst classified as 730k, are neither of the size nor undertake the complexity of business of the large firms for whom this category is intended.

4

iv. The application of the requirements to high net worth asset management firms

that are categorised as private banks requires special consideration. v. The capital treatment for unsettled or failed transactions should not be applied to

trading for extended settlement. vi. Supervisors should be required to disclose information on their interpretation

application of the rules. vii. An impact study needs to be undertaken with the questions specifically tailored

for investment firms. viii. It is very important that the proposals do not result in firms ceasing offering

some services as a consequence of the Directive not being sufficiently developed and so resulting in an unjustified increase in capital requirements.

1.6 In addition, we seek further clarification in two particular areas:-

• the continuation of the Expenditure Based Requirement; • the particular circumstance in the UK where for historical structural reasons we

have trading for non standard settlement, primarily involving small value retail sales.

1.7 In asking for an expansion of business lines to reflect the different nature of business

activities carried out by investment firms, it is important to note that the current proposals give the banking sector of the industry a competitive advantage over non banks. Investment firms are asking for equality of treatment in order that their particular business risks are properly assessed and capital charges can be calibrated accordingly.

5

2. Competitive Issues 2.1 APCIMS is seriously concerned that the current proposals for applying the Risk Based

Capital Directive to investment firms will result in placing those firms at a competitive disadvantage to banks who offer the same services. Banks (including investment banks) have credit risk which attracts a reduced capital requirement under the new proposals. Investment firms do not have credit risk and few of them have market risk, which means that most investment firms only have operational risk. Therefore a system which is designed to reallocate capital across the range of risks run by a bank has an adverse impact on entities who neither offer that range of services nor do they offer the service for which a capital reduction is offered.

2.2 If the new regime is applied in its current form, the net consequence to smaller 730k

investment firms who hold no banking licence and do not have credit risk will be very serious indeed.

Recommendation We urge the Commission to provide an additional category or categories between the current 125k and the current 730k definitions so that professional firms do not find themselves at a competitive disadvantage to those who hold a banking licence. 3. Simpler Investment Firms 3.1 During the structured dialogue and in our responses to date to the Commission, we have

stressed strongly that investment firms do not fall easily within the Basel framework, which has been designed for the banking sector and specifically for internationally active banks.

3.2 We note that in the Quantitative Impact Study QIS3, attention was mainly paid to banks

and indeed this is referred to within the explanatory document to this Consultation Paper. This explanatory document also states that in order to assess the impact of the proposals for investment firms, the Commission Services have co-ordinated a data sharing exercise in co-operation with national authorities.

3.3 It is noticeable that the studies undertaken to date, whilst no doubt addressing the issues

sensibly from the perspective of banking, ask questions which are inappropriate for non credit institutions with the consequence that there has been varying interpretation of the questions, which will not have helped in terms of interpretation of the responses.

3.4 We remain concerned that credit institutions and investment firms tend to be bracketed

together within the consultation, on the assumption that both types of institution operate and compete in many of the same markets and on the same product lines. We accept that this may be the case in some countries, but it is certainly not the same in all countries and is certainly not in the UK.

6

3.5 In addition, the consultation also overlooks the fact that all investment firms in the UK

are required to hold their client assets and cash separate from that of the firms, both in terms of separate accounts and also in terms of holding them within a separate legal entity such as a nominee account or in “trust”. In this context trust is a legal concept, not simply one of understanding. However client assets or cash are recognised by banks as part of their own assets or liabilities.

3.6 The result of a UK study undertaken by the Financial Services Authority to assess the

application of the new capital proposals to investment firms is well known. That study showed that the amount of capital that such entities would have to hold without modification of the new provisions would be hugely increased, and that the increase was not justifiable against the risks that such entities run. This increase was directly as a result of the application of the operational risk charge. Whilst we agree that capital should be applied in accordance with the risk the firm faces, we believe that the EBR already provides a sound basis for the calculation of regulatory capital for investment firms.

3.7 We are therefore pleased to see that the Commission is proposing to exempt 50k and

125k firms from the operational risk charge, leaving them subject to the Expenditure Based Requirement. We would urge that this approach is adopted and we emphasise that this would not give such firms any advantage in the marketplace, rather they would be severely disadvantaged if such a pragmatic decision is not ultimately taken and banking standards are applied to this type of entity.

3.8 It is also important to note that most of the firms who would be covered by this

proposal would be small, both in comparative terms and in absolute terms. Also, as these firms operate in the retail space, the quantum with which they are involved is small compared to that of institutional firms, whether considered on a segregated basis or as a total of funds under management or in terms of the size of trades they undertake.

3.9 We remain concerned, however, that there are many other types of firms which are also

low risk and low impact who, as a consequence of their lines of business, will be required to use either the BIA or the Standardised Approach. It is therefore essential to ensure that the calibrations of business lines are a match with the business that investment firms are undertaking, if anomalous results and unreasonable increases in capital requirements are to be avoided.

Recommendations We would urge the Commission Services to develop a set of questions specifically designed for investment firms in order to assess with a greater degree of certainty and accuracy the impact on them of these proposed changes. We attach some suggested questions for an impact study on investment firms at Annex 1. In all instances capital requirements should be reduced for firms where client assets, including cash, are held entirely separate from the assets of the firm. All low risk firms including 50k, 125k including asset management firms must be exempt from the proposals for the Operational Risk Charge.

7

Further work should be undertaken to ensure that the calibration of business lines match the business that investment firms are undertaking. This point is amplified on page 5 of this response. The Commission Services should take existing control and risk management standards applied by home state regulators into account when assessing what further requirements are needed in this Directive. 4. The More Complex 730k Investment Firms 4.1 Many of our member firms are concerned that they may fall within the definition of 730k

only because of specific situations that may arise, which are incidental to the primary business they undertake. A firm may find itself holding principal positions for structural reasons rather than as a consequence of running a trade book. One example is where the firm is acting as in an agency capacity dealing in options on behalf of its clients, where it has to trade in the firm’s name in the market. A second, and perhaps more common example, occurs where a firm deals directly on the Stock Exchange Trading System (SETS): such a trade passes automatically through to the London Clearing House (LCH) which acts as the central counterparty, but in order to use the LCH the firm has to trade as principal, even though it is trading on behalf of a client.

4.2 Agency firms route much of their business through specialist market makers, known in

the UK as Retail Service Providers (or RSPs). Nevertheless an agency firm will still use SETS and therefore the firm may under these circumstances have to trade as principal, though it does not have a principal trading book. We believe that similar situations arise in other European countries.

4.3 It is surely not the intention of the Commission to incorporate into the definition of

730k firms, an entity which, in order to have access to a particular market or to particular clearing systems, may find itself taking temporarily a principal position for such structural reasons. We propose that the Commission only include in the definition of 730K firms those entities which actually run a trading book.

4.4 We would like to highlight another practical issue which is relevant to the description of

a firm’s business and could determine whether or not it should fall into the 730k category. Sometimes a firm is unable to match an investor’s order precisely and as a result finds itself having taken a principal position which is incidental and provisional in nature, and is strictly limited to the time required to carry out the transaction relating to that investor’s order. This is a situation which 125k firms can find themselves in; it is understood from the regulatory perspective, and to date would not be one which, in the UK, would necessarily result in the firm being classified as dealing as principal or dealing on its own account. Clearly this is an ongoing commercial necessity and highlights another reason why the 730k category should be defined more tightly, so that it includes only those firms which run a trading book.

4.5 A firm can find itself holding a principal position for structural reasons rather than as a

consequence of running a trading book. For example:-

(i) A firm acting in an agency capacity dealing in options on behalf of its clients, has to trade in the firm’s name on the market.

8

(ii) A firm that deals directly on the Stock Exchange Trading System (SETS) has to

use the London Clearing House which acts as the central counterparty but in order to use the LCH, the firm has to either trade as principal or use a general clearing member of the London Clearing House. Both aspects add to the cost of a trade. We understand that there are similar examples in other jurisdictions.

(iii) It is possible that a firm is unable to match an investor’s order precisely and, as a

result, finds itself having to take a principal position which is incidental and provisional in nature and is strictly limited to the time required to carry out the transaction relating to that order.

4.6 We seek confirmation that in these situations firms would not find themselves identified

as 730k and that it is not the intention of the Commission to incorporate into this definition a firm which, in order to have access to a particular market or a particular clearing system, may find itself taking temporarily a principal position for structural reasons rather than running a trading book.

Recommendation Where a firm takes a principal position which does not fall into the trading book (because a firm does not have the trading intent as set out in Annex G-1 to CAD III) then taking those positions should not constitute “dealing for their own account” and so should not result in a firm being categorised as 730k. 5. The Need for Further Differentiation of the 730k Category 5.1 The Commission has undertaken to ensure that it pays particular attention to small and

medium sized enterprises (SMEs) and we welcome this. In addition, the Commission also seeks to be flexible with regard to the future capital requirements of the diverse European financial industry. It is our understanding that there is widespread recognition that the business undertaken by an investment bank is noticeably different in quantum and risk than that of, for example, a small stockbroking investment management firm. However, both can fall into the same 730k category.

5.2 At Annex 2 are some statistics of the APCIMS community, taken from the 2002 issue of

the annual detailed statistical analysis that is undertaken of their member firms. Whilst markets have improved in 2003 which will have increased some of the portfolio sizes, nevertheless it provides a good picture of these independent investment firms for which we are concerned. These firms are described in this Annex as advisory and discretionary market firms. That is, they are members of the Stock Exchange and they undertake advice based business on behalf of their clients.

5.3 It can be seen that these 103 market firms have just over 700000 clients and a total of

nearly £92 billion of funds under management. This averages at nearly 7000 clients per firm and £130000 of fund under management per client. Although not all these firms will be classified as 730k, none are materially different in terms of either numbers of clients or the value of the funds managed from those who will be designated 125k.

9

5.4 These firms are clearly SMEs and of a much smaller size than, for example, investment banks. It is our understanding that the Basel proposals were never intended for this type of firm.

5.5 It is important to note these firms provide a variety of services according to the needs of

their customers. For example, these firms may well undertake placing activities. A placing activity would mean that a firms would agree to purchase a specific quantity of a new issuer but importantly only when it had an agreement to allocate the onward sale. That is, the firm acts as an intermediary between the issuer and the end investor.

5.6 A second example is when firms may well be involved is advice with respect to an IPO

but not with the finance. Such advice carries a lower risk to that of the corporate finance provision and therefore should be treated accordingly.

5.7 As a general point, where activities are generally described as corporate finance but are

not underwriting or placing on a firm commitment basis, then the required capital should be modulated accordingly.

Recommendations In summary, the 730k categorisation should be developed further to cater for these types of firms, applying to them a capital requirement that is not as aggressive as that of a large multi-discipline 730k firm. We would define the firms that should fall into this developed or reduced category as ones that have the following characteristics:- (i) the firm is defined as a SME with respect to the industry in their country or

countries of operation; (ii) the size of the client fund managed and administered by the firm is of a retail

quantum; (iii) the firm does not have a credit risk exposure; (iv) the firm may find itself holding a principal position but does not operate a trading

book, other than in support of its other activites; (v) the firm may offer some corporate activities such as corporate advice and placing

but is not underwriting on a firm commitment basis nor engaged in corporate finance.

10

6. Articulation of Expenditure Based Requirement and Operational Risk 6.1 The proposals currently appear to imply that any investment firm that applies the Basic

Indicator Approach or the Advanced Measurement Approach will have to add the operational risk charge to their existing expenditure based requirement. This concerns us as we do not believe that the two charges should be additive, although we appreciate that the Commission wishes to see a floor set at the EBR requirement.

Recommendation The Expenditure Based Requirement should be seen as a fall back charge and should not be additive with any operational risk charges. 7. Unsettled Transactions 7.1 We note in paragraph 302 the affirmation that under the current CAD requirements,

firms benefit from a five day’s grace period after the settlement date, during which they can resolve unsettled transactions without receiving a specific capital charge. The Commission Services are now proposing two alternative changes to this requirement. However, no reference has been made to the particular UK situation relating to certificated trading and the consequences of the proposals in terms of costs both to firms who are prepared to act for individuals who hold certificates and consequently to the customers for whom they act.

7.2 Most of the 12 million UK shareholders still hold one or more share certificates which

they received as a result of either the privatisations of the 1980s or the demutualisations of the 1990s. UK law still requires all companies to offer shares in certificated form and, in spite of intensive lobbying by the industry, UK Company Law only gives shareholders rights of attendance at AGMs, of voting and of receiving information if their name is on the share register. Full shareholder rights are therefore only conferred on those who hold share certificates.

7.3 We do not expect the European Commission to resolve these local issues, but for these

reasons we see no early reduction in the number of certificates held by UK shareholders. Evidently it is slower to move paper around the settlement system and those brokers who are prepared to handle certificated trades (and primarly these are on a sale only basis) usually deal for T+10 settlement.

7.4 Should changes be made to regulatory capital, such that this type of trading results in

additional capital having to be held from the moment of dealing, then clearly the cost of such a transaction to the firm and the individual investor would rise accordingly. It is important to note that certificated trades tend to be low value and less than the average private investor bargain, which currently stands at just under £7,000.

7.5 We understand that the Commission Services are seeking to apply a capital charge to

unsettled or failed transactions. However, at present it appears that trading for extended settlement is being treated the same as unsettled or failed transactions, yet the risk is clearly different between the two issues.

11

Recommendation Additional capital should only be required if settlement does not take place 5 days after the agreed settlement date. Such an arrangement would cater for both extended settlement trading, where the settlement date is set at the time of trading and for standard settlement currently set at T+3. 8. Business Lines 8.1 Annex H provides information on business lines and we welcome the introduction of the

improved mapping of investment services by the use of the finer business line approach. Nevertheless, we retain a significant number of concerns relating to both the category to which business lines have been placed and the beta factors allocated.

8.2 Underwriting and placing under the ISD – Underwriting and placing are bracketed

together, both attracting the same corporate finance beta factor of 18%. However, it is also the case that some firms may undertake the placing activity, but without the underwriting activity. This is a particularly important matter for the smaller specialist stockbroking firms who can be extensively involved in undertaking such activities on behalf of small and medium sized companies.

8.3 Retail brokerage – This operation attracts a beta factor of 12%, the same as that for

retail banking. However, retail banking includes the taking of deposits and the advancing of credit, including retail lending, private lending and card services. Meanwhile retail brokerage does not include the two major risk issues of lending and deposit taking and, in addition, the data shows that the losses are small. In an execution only trade, the suitability requirements remain with the client and are not passed to the firm (see the ISD). This again points to the need to reduce the beta factor for this category.

8.4 Asset Management under the ISD – The arguments for this particular activity are the

same as 7.3 and the beta factor assigned to it needs further consideration. Private client investment management or portfolio management, is the major undertaking of our membership and has the following characteristics:-

i. The assets of the client are held by a third party, separate from these of the firm. ii. Client money is held separately in an account segregated from the firm’s account. iii. The amounts are retail in terms of client size. iv. Loss data shows that losses tend to be small and are usually the consequence of

mistakes. v. The activity is tightly regulated and already subject to stringent regulatory

requirements, systems and controls. 8.5 Incidental Activities – Firms seek to meet the requirements of their customers by

offering additional services and developing these services accordingly. This is part of the dynamic market place and one which we would seek to encourage rather than to constrain. As firms develop their range of services many will be considered to be incidental activities and as such the regulatory capital framework must be sufficiently flexible to allow such developments to take place without causing an immediate capital impact. This needs to be recognised within the new Directive.

12

8.6 Payment and Settlement Services – It is surprising that firms responsible for payment and settlement services should be considered to have the same operational risk profile of proprietary trading firms or firms underwriting institutional deals. Again payment and settlement services are significantly lower risk activity and should be recognised accordingly.

Recommendations Placing is clearly a significantly lower risk activity than underwriting, as it does not attract the same exposure to risk from the firm. We therefore consider that placing should be allocated a lower beta factor than that of underwriting. As the risk associated with retail brokerage is significantly less than retail banking, the beta factor should also be significantly less than the 12% currently assigned to both. Whilst we welcome the special attention given to asset management, nevertheless a 12% beta factor, which therefore rates portfolio management as risky as retail banking, is significantly higher than this activity warrants. A de minimis regime should be developed in order than an activity which is not the main business of the firm, or is a peripheral activity, does not result in an immediate adverse capital impact. 9. Supervisory Convergence and Consistency 9.1 Firms in different countries are not necessarily identical, and there is also likely to be

some difference in application of requirements by supervisors from country to country. However, we are concerned that there should be as much consistency as possible. If the practical application and requirements in one jurisdiction are significantly different to those in another jurisdiction, this can result in some firms being impacted by substantial additional costs, while others should be significantly favoured. This consultation paper highlights a number of potential undue burdens that could arise as a consequence of differential interpretation. To these we would also add home state interpretation of what should be in the Expenditure Based Requirement and the attributing of investment firms to the different categories of 50k, 125k and 730k.

Recommendation In the interests of transparency, we consider it essential that supervisors are required to disclose information on their intepretation and application of the rules. We note that the Commission Services are considering how the requirements for supervisory co-operation might be enhanced. We consider that supervisors need to make public the way that they are interpreting and applying the requirements to the various types of firms, that this information should be disseminated widely and summarised by, for example, a group attached to CESR and that there should be an independent committee of “appeal”.

13

10. The Role of Insurance 10.1 We note and concur with the concerns raised by Commission Services on the complexity

of recognising insurance as a risk mitigator. In particular, the Commission Services state they believe that the recognition of insurance for capital adequacy purposes should be limited only to the Advanced Measurement Approach. The reason given for this is that it is difficult to find a way to apply insurance mitigation to simpler approaches.

Recommendation From a practical perspective, a firm with insurance is less exposed to risk than a firm without insurance, and therefore regardless of how difficult it is to implement, all firms with insurance should be allowed to obtain at least some relief from the operational risk charge. As a result we do not agree that insurance should be disregarded except for those on the AMA. 11. Outsourcing 11.1 A number of firms outsource functions such as custody of assets or settlement and

clearing of transactions. While we acknowledge that outsourcing does not necessarily transfer responsibility or the risk attached to the outsourced activity, there is one particular instance where such a transfer does take place. The arrangement is referred to in the UK as ‘Model B clearing’ (Annex 3).

11.2 The term ‘Model B clearing’ describes a contractual arrangement, recognised by the

regulator, whereby the market risk and the operational risk is transferred to a fully regulated third party. That third party is also within the capital adequacy regime, is subject to conduct of business rules and holds insurance covering risk.

Recommendation The new capital requirements should recognise the transfer of risk by allowing some reduction in the capital requirement of a firm which has outsourced certain functions provided there is in place a sound legal agreement and that the arrangement has been approved by the home state regulator. This should apply to Model B clearing arrangements as well as the other outsourcing arrangements. 12. The Asset Management Firm operating under the description of “Private Bank” 12.1 Private banks are a particular type of firm that offer tailored portfolio management

services to high net worth clients. They do not operate a retail banking function nor corporate banking. They take their client money in the form of deposits but in other respects are to an asset management firm.

12.2 Where a private bank offers deposit taking to its customers, it is on a much more

restricted basis than is the case, for example, a retail bank. Meanwhile it does not undertake wholesale banking services. As a consequence we consider further consideration should be given to the treatment of a private bank.

14

Recommendation Where the private bank offers restricted deposit services to its high net worth customers only, then this is a reduced exposure and so warrants a beta factor less than that currently applied to retail banking. 13. Cost Benefit Analysis 13.1 Firms are operating in difficult market conditions and have been doing so for some

years. The future is uncertain and clearly steps are being taken to minimise non-essential expenditures and reduce costs. Whilst we do not suggest that inefficient firms should be artificially supported, we are concerned that all requirements that result in firms of all types having to change current methods of operation are subject to an in-depth cost benefit analysis.

13.2 The Commission is required to give specific consideration to adverse effects of any

regulation on SMEs, but doesn’t appear to have done this for the small and medium sized investment firms covered by this directive.

Recommendation We urge the Commission Services to conduct a cost benefit analysis of their proposals. It is essential that all those with responsibilities in this area, including the Commission, CESR, regulators and supervisors, keep the cost of change to the industry to the minimum.

15

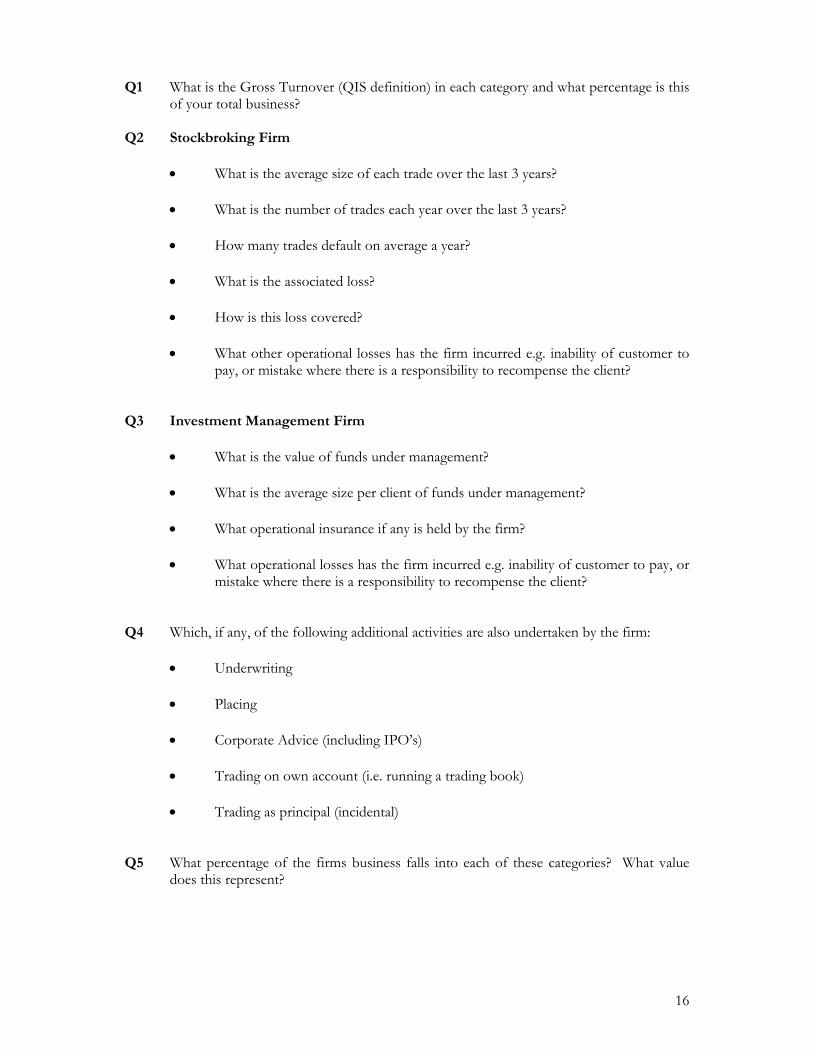

ANNEX 1

Quantitative Impact Study

Questions designed for Investment Firms

The intention of these questions is to identify, firstly, the specific activities which investment firms undertake, secondly, the limited risk to which they are exposed and, thirdly, the extent and value of additional activities undertaken. Such questions should be part of the quantitative impact study specifically designed for such entities. It is important to note that the list is not designed for investment banks. The following list identifies the main categories of Investment firm (excluding investment banks). Execution only brokerage No advice; undertaking clearing and settlement;

holding client money; custody of client assets Execution only brokerage As above, but with the activities of clearing,

settlement, holding client money and custody of client assets contracted out under Model B arrangements.

Advice based stockbroking services Advice; portfolio management, undertaking (both discretionary and advisory) clearing and settlement, holding client money;

custody of client assets Advice based stockbroking services As above, but with Model B arrangements (both discretionary and advisory) Portfolio Management Advice; holding client money; custody client assets Portfolio Management Advice; not holding client money; no custody

client assets Private Bank (1) An Asset Management; does not take deposits or

advance credit; has a banking license Private Bank (2) Asset Management; offers deposit and credit

services to limited client base Independent Financial Adviser Advice only

16

Q1 What is the Gross Turnover (QIS definition) in each category and what percentage is this of your total business?

Q2 Stockbroking Firm

• What is the average size of each trade over the last 3 years?

• What is the number of trades each year over the last 3 years?

• How many trades default on average a year?

• What is the associated loss?

• How is this loss covered?

• What other operational losses has the firm incurred e.g. inability of customer to pay, or mistake where there is a responsibility to recompense the client?

Q3 Investment Management Firm

• What is the value of funds under management?

• What is the average size per client of funds under management?

• What operational insurance if any is held by the firm?

• What operational losses has the firm incurred e.g. inability of customer to pay, or mistake where there is a responsibility to recompense the client?

Q4 Which, if any, of the following additional activities are also undertaken by the firm:

• Underwriting • Placing

• Corporate Advice (including IPO’s)

• Trading on own account (i.e. running a trading book) • Trading as principal (incidental)

Q5 What percentage of the firms business falls into each of these categories? What value

does this represent?

17

ANNEX 2

Investment Firm Statistics Year on Year Comparison of Client Trades by Peer Group Table 22.0 provides a year on year analysis of LSE-routed client trades for each client category, by firm type. It includes both Market and Non-Market Firms. Table 22.0

Trading volumes

Mainly XO firms

Advisory & discretionary

Non Market fund

managers

by client type within business group

Calendar 2001

Calendar 2002

Calendar 2001

Calendar 2002

Calendar 2001

Calendar 2002

Own name XO

3,142,690 1,618,801 305,053 149,101 229 393

Administered XO

5,003,840 3,781,991 369,310 233,164 20,517 15,553

Internal indirect XO

2,033,321 2,180,746 0 0 0 0

Advisory dealing

27,435 44,653 611,573 521,370 655 1,814

Advisory portfolio

62,968 68,248 2,175,508 2,194,726 93,631 78,054

Discretionary

59,998 122,799 1,949,073 2,073,739 6,213,585 5,121,542

Total LSE Trades

10,330,252 7,817,238 5,410,517 5,172,100 6,328,617 5,217,356

18

Fund1 Values by Portfolio Band in each Peer Group (Data extrapolated for 103 market and 98 Non-Market Firms)

This section provides estimates of funds segmented by portfolio band for (1) administered XO clients of Market Firms, (2) advisory and discretionary clients of Market Firms and (3) clients of Non-Market fund managers (almost exclusively discretionary).

Administered xo market firms Table 30.0 is consistent with the known low net worth profile of most XO investors with 69% of all funds in the lowest band. The <£50K group is subject to considerable double counting. We believe that double counting is less likely for higher net worth investors. This latter category is important to firms as it includes a high proportion of active traders.

Advisory & discretionary market firms Funds managed by non XO Market Firms are fairly evenly distributed across a wide range from low to high net worth. However, a surprisingly high percentage of clients (58%) fall into the lowest net worth category, although they account for only 5% of the funds.

non-market firms Funds managed by Non-Market Firms are all discretionary holdings and are tilted slightly towards the high net worth end. Relatively few clients (31%), with 3% of funds, fall into the lowest < £50K band. Most clients (about 55%) fall into the two medium net worth bands (£50-£150K and £150K-£250K).

1 The client numbers are likely to be overstated as we are unable to assess the extent of double counting arising from investors holding accounts with two or more brokers. On the other hand, the portfolio value is probably understated because it does not include certain PEPs and Unit Trust funds which are not considered to be an integral part of the participant’s business and are managed elsewhere. The definition does not include “own name” execution only and advisory dealing investors. These funds are in the custody of the client and have been discussed earlier.

Table 30.0

Value band

Number of execution only clients

Value of funds (£m)

(% oftotal

funds)

Up to £50K 3,050,729 13,366 (69%)

£50-150K 32,396 2,749 (14%)

£150-250K 4,813 927 (5%)

£250-500K 2,569 879 (5%)

£500K-£1m 833 586 (3%)

£1-3m 310 506 (3%)

£3-10m 44 242 (1%)

£10-25m 0 0 (0%)

Over £25m 0 0 (0%)

Totals 3,091,694 19,255

Table 31.0

Value band

Number of advisory/discr-etionary

clients

Value of funds (£m)

(% oftotal

funds)

Up to £50K 408,543 4,455 (5%)

£50-150K 149,292 12,965 (14%)

£150-250K 61,249 10,874 (12%)

£250-500K 50,198 16,627 (18%)

£500K-£1m 21,604 14,462 (16%)

£1-3m 8,969 15,101 (16%)

£3-10m 1,870 9,733 (11%)

£10-25m 269 4,210 (5%)

Over £25m 65 3,141 (3%)

Totals 702,059 91,568

Table 32.0

Value band

Number of portfolio clients

Value of funds (£m)

(% oftotal

funds)

Up to £50K 95,732 2,562 (3%)

£50-150K 129,127 15,108 (19%)

£150-250K 42,213 10,304 (13%)

£250-500K 27,430 12,121 (16%)

£500K-£1m 10,096 9,192 (12%)

£1-3m 4,442 9,643 (13%)

£3-10m 1,204 8,886 (12%)

£10-25m 306 6,012 (8%)

Over £25m 55 2,981 (4%)

Totals 310,605 76,809

19

Analysis of all Private Client Funds (Data extrapolated for 103 Market Firms and 98 Non-Market Firms)

Analysis of client numbers by portfolio values The analyses of private client funds on the two preceding pages relate to those funds administered or managed by stockbrokers and fund managers. This section takes into account all private client funds, both administered/managed funds and funds in clients’ own custody. Chart 50.0 provides estimates showing a breakdown of clients and funds into values of over and under £50K, for each of the three main types of firm.

Clients with portfolios exceeding £50,000 generate most business for stockbrokers (whether execution only or full service advisory/discretionary firms) and Non-Market fund managers. We estimate that this category numbers 48,000 clients of execution only firms, 370,000 clients of advisory/discretionary stockbrokers and 215,000 clients of Non-Market Firms, 633,000 in total.

Chart 50.0

48

370

215

3,609

524

96

XO

Adv/Discret

Non market

Number of Clients (000's)

Clients with funds in portfolios under £50KClients with funds in portfolios over £50K

figures not adjusted for double counting

20

ANNEX 3

Outsourcing Introduction Model A and Model B clearing are arrangements whereby firms outsource part or all of their back office to a fully regulated third party. With Model A clearing the clearing firm performs a series of administrative functions such as the movement of stock and cash for settlement purposes, the reconciliation of bank and stock accounts, and the processing of corporate actions and dividends. However, the correspondent firm retains full responsibilities for the functions carried out by the clearing entity from a regulatory basis. With Model B clearing, the Model B clearing firm becomes the legal counterparty to all trades and adopts the primary settlement risk until the transactions are fulfilled. Correspondent firm records are transferred to the clearing firm’s system and a standard suite of dedicated accounts is established specifically for each co-respondent. The clearing firm will still undertake functions such as the settlement of transactions, the movement of stock and cash, the reconciliation of bank, trading and custody accounts and the process of corporate actions and dividends. The clearing firm is also responsible for ensuring that the client money calculation and segregation requirements are fulfilled on an ongoing basis and the relevant aspects of the financial resources requirements are fully calculated. These capital calculations have an impact on the regulatory capital of the clearing firm. Approximately 40 of our member firms use the full Model B service and about 10 of our firms use Model A. APCIMS contends that there is transference of risk in both instances with clearly a greater transference of risk by those use firms who use the full Model B service. We therefore believe that the Commission should recognise outsourcing as a risk mitigator. The detail of Model A and Model B clearing is set out on the following pages.

21

Model A Clearing This service is effectively a “back office for hire” service, with the Clearing Firm performing a series of administrative functions on behalf of the correspondents. The correspondents transfer their records onto the Clearing Firm’s system, into a suite of ledgers established specifically for the individual correspondent. The Clearing Firm undertakes many of the settlement and control processes, such as the movement of stock and cash for settlement purposes, the reconciliation of bank and stock accounts, and processing of corporate actions and dividends. The accounts established at central clearing services, such as CREST, are in the name of the correspondent, as are all bank accounts and settlement accounts at custodians in other jurisdictions. The nominee companies used to register clients’ assets are also wholly owned by the correspondent. The accounts established within the Clearing Firm’s system are only used for processing business for the particular correspondent. There is no utilisation of the accounts for the business of other correspondents. Therefore, from a legal perspective, the Clearing Firm has no ownership of the accounts of the correspondent, as these are all accounts of the broker. The Clearing Firm’s role is to administer and operate these accounts on behalf of the broker, and it does so under specific mandates. Therefore members of staff at the Clearing Firm will act as authorised signatories over the accounts. In relation to trading activities under the model A clearing service, the Clearing Firm takes no legal responsibility for the trades executed by the correspondent. The correspondent trades in its own name, and has the direct relationship with the market counterparty. The correspondents require memberships of the relevant exchanges in order to undertake trading activities. All transactions are reported to the relevant exchange or regulator in the name of the correspondent, although this could be achieved by using the systems of the Clearing Firm, rather than those of the correspondent. The Clearing Firm is not a counterparty to the trade in any way. In terms of the relationship with the underlying client, this exists only between the client and the correspondent. The Clearing Firm plays no part in the relationship with the underlying client. Whilst information for accounting to clients for investment and other activities are usually generated from the Clearing Firm’s system, the contract notes, activity statements, valuations and custody statements are issued in the name of the correspondent, and there is no reference to the Clearing Firm. If a custody service if offered, the correspondent retains all custodian responsibilities to the underlying clients. Clients are likely to be aware of the involvement of the Clearing Firm in the operation of their account, as they would probably be required to send stock and cash to the Clearing Firm’s offices, although cheques and stock transfers are in the name of the correspondent. A key aspect of the model A relationship is that the correspondent must retain full authorisation from the regulator. The correspondent must be authorised to undertake dealing (receipt and transmission of orders, and execution of orders), as well as to hold client money and to offer safe custody services. The correspondent retains full responsibilities for the functions carried out by the Clearing Firm on a model A basis from a regulatory perspective, including ensuring that the reconciliations of their bank, trading and custody accounts are undertaken in accordance with regulatory requirements, that the client money calculation and segregation requirements are fulfilled on an ongoing basis, and the relevant aspects of the financial resources requirements, such as counterparty risk requirement, large exposures requirements, foreign exchange requirement and position risk requirements are correctly calculated.

22

Model B Clearing The key difference between model A and model B clearing services is that the Clearing Firm becomes the legal counterparty to all trades and adopts the primary settlement risk until the transactions are fulfilled. Correspondents records are transferred to the Clearing Firm’s system, and a standard suite of dedicated accounts is established specifically for each correspondent. Under this model, the Clearing Firm would still undertake functions such as the settlement of transactions, the movement of stock and cash, the reconciliation of bank, trading and custody accounts and the processing of corporate actions and dividends. In terms of accounts, under a model B arrangement, all bank, settlement and custody accounts are established in the name of the Clearing Firm. Similarly, the nominee companies used to register client assets for safe keeping purposes would be wholly owned by the Clearing Firm. The accounts are likely to be pooled accounts, and would be used to process business across all model B correspondents. It is unlikely that any bank, trading or custody accounts would be set up specifically for individual model B correspondents. The nominee companies used for the custody service are also likely to be pooled, although they may be designated to a certain extent, in order to distinguish the various different activity types for each broker. Under a model B arrangement, it is possible for either the correspondent or the Clearing Firm to execute transactions. Where the correspondent executes transactions, these are done either in the name of the correspondent, but are simultaneously “given up” to the Clearing Firm, or are executed by the correspondent in the name of the Clearing Firm. This means that the Clearing Firm takes full responsibility for the executed trades and becomes the counterparty to the transaction with the market. The correspondent bears none of the risks associated with the transactions, although would have regulatory responsibilities in connection with the execution of the transactions, if these are executed in the name of the correspondent. The open exposures reside on the Clearing Firm’s balance sheet and not that of the correspondent, and are thus funded by the Clearing Firm. Therefore, the Clearing Firm carries the credit and market risks of the open exposures until they are fulfilled at settlement. The Clearing Firm will have to calculate the counterparty risk requirement, large exposures requirement, and any foreign exchange requirement or position risk as appropriate. All transactions are reported to the relevant exchanges and regulators in the name of the Clearing Firm, although it should be possible to identify which correspondent has originated the trade. From a legal perspective, both the Clearing Firm and the model B correspondent have a relationship with the underlying client. The correspondent is responsible for the initiation of the relationship, as well as for the execution of transactions arising and any advisory or investment management services, dependant upon the arrangements in place. As the transactions are adopted by the Clearing Firm, clients have to pay the Clearing Firm directly. Payments are made to the Clearing Firm in its name, and not to the model B correspondent. Contract notes, activity statements, valuations etc should make clear the dual relationship that the client has with the correspondent and the Clearing Firm. Under a model B arrangement, the correspondent may not be required to maintain such a broad authorisation, as the key risks and liabilities are taken on by the Clearing Firm. Therefore, the correspondent only requires authorisation to deal and manage/give advice as required. There is no requirement to maintain any authorisation for holding client money or for safe keeping services (except for arranging safe keeping), as these become the responsibility of the Clearing Firm. As a result, a lesser authorised category could be sought by the correspondent. The Clearing Firm, however, is required to maintain full authorisation for dealing, holding client

23

money and offering a safe keeping service. Responsibility for the reconciliation of bank, trading and settlement accounts is the responsibility of the Clearing Firm, and not the correspondent, as all such accounts are in the name of, and owned by the Clearing Firm. The Clearing Firm is also responsible for ensuring that the client money calculation and segregation requirements are fulfilled on an ongoing basis, and the relevant aspects of the financial resources requirements, such as counterparty risk requirement, large exposures requirements, foreign exchange requirement and position risk requirements are fully calculated. These capital calculations have an impact on the regulatory capital of the Clearing Firm.

24

ANNEX 4

Operational Losses A recent survey of some APCIMS member firms has yielded the following figures: • Average total dealing errors 0.2% of turnover • Maximum total dealing errors 0.8% of turnover • Average portfolio management losses 0 • Average number of customer complaints

per year for which recompense is required 5 • Average size of each claim less than GBP4000