Reverse Mortgages A Solution For Asset Rich/Cash Poor Retirees Strategic Ramifications & Planning...

37

Reverse Mortgages A Solution For Asset Rich/Cash Poor Retirees Strategic Ramifications & Planning Opportunities Speaker: Kate Anderson Company: Mariner Financial Date: Wednesday 22 November 2006

-

Upload

melissa-martin -

Category

Documents

-

view

216 -

download

2

Transcript of Reverse Mortgages A Solution For Asset Rich/Cash Poor Retirees Strategic Ramifications & Planning...

Reverse Mortgages

A Solution For Asset Rich/Cash Poor Retirees

Strategic Ramifications &

Planning Opportunities

Speaker: Kate Anderson

Company: Mariner Financial

Date: Wednesday 22 November 2006

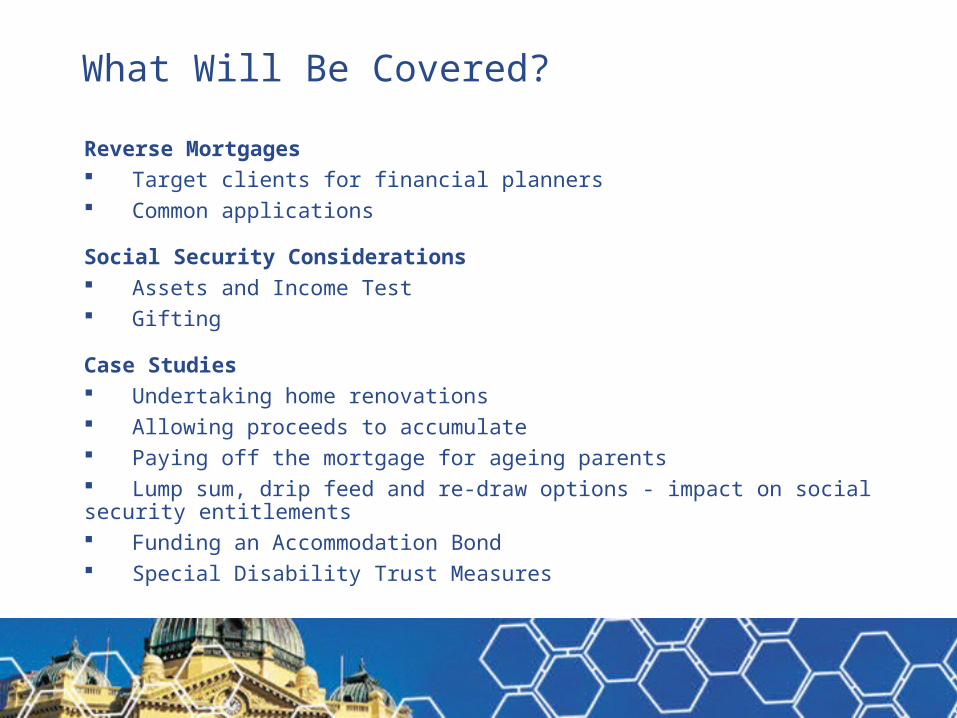

What Will Be Covered?

Reverse Mortgages Target clients for financial planners Common applications

Social Security Considerations Assets and Income Test Gifting

Case Studies Undertaking home renovations Allowing proceeds to accumulate Paying off the mortgage for ageing parents Lump sum, drip feed and re-draw options - impact on social security entitlements Funding an Accommodation Bond Special Disability Trust Measures

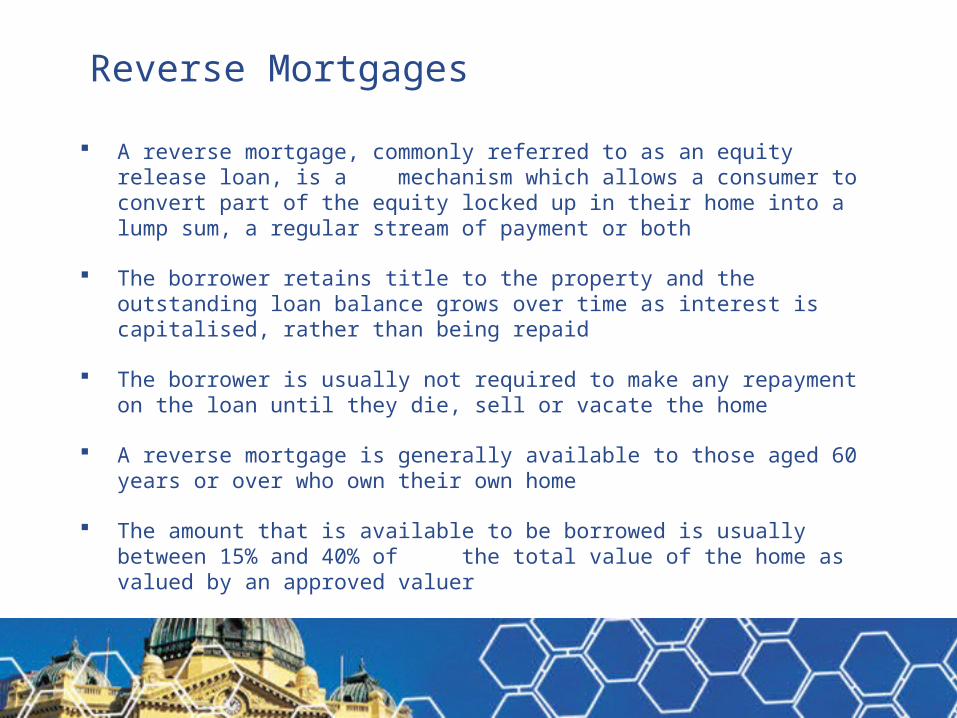

Reverse Mortgages

A reverse mortgage, commonly referred to as an equity release loan, is a mechanism which allows a consumer to convert part of the equity locked up in their home into a lump sum, a regular stream of payment or both

The borrower retains title to the property and the outstanding loan balance grows over time as interest is capitalised, rather than being repaid

The borrower is usually not required to make any repayment on the loan until they die, sell or vacate the home

A reverse mortgage is generally available to those aged 60 years or over who own their own home

The amount that is available to be borrowed is usually between 15% and 40% of the total value of the home as valued by an approved valuer

Large and Rapidly Growing Community

Consumer needs in retirement is great

2.6 million retirees in Australia

2.1 million own their own home

80% of these are on the pension and retired with less than $70K

Retirement population is growing

2.1 million in 2004 = 11% of total Australian population

Expected to grow to 25% of Australian population

Over time we will see people approaching retirement, retiring on more than $70K as they have had more years in the superannuation market

Source: Australian Bureau of Statistics

Financial Pressure in the Household

Average weekly household income for Australians between 55 and 64 = $1,035

Reduces significantly >65 to $540 per week

68.4% rely on the government for primary income

80.2% own their own home with no mortgage

Highest projected Australian growth segment is >85 which is projected to grow

from 1% to 7-11% by 2010

Pension growth below cost of living

The average Australian pensioner has a gap to fill

Household final year income 55-59 =$62,376*

Pension = $12,711.40

$

Source: *HILDA Wave 2 Australian Bureau of Statistics

Australia’s Fastest Growing Segment is 65 yrs +

Population : 2004 vs 2014

2004 Population

Projected 2014

0

100000

200000

300000

400000

0 5 10 15 20 25 30 35 40 45 50 55 60 65 70 75 80

Population Growth by Age Band : 2004 vs 2014

-10%

0%

10%

20%

30%

40%

50%

60%

70%

5yr Age Band

Grow th in Period

Quinquennial Age Groups

All Ages

13% Australians > 65 (i.e. 2.6 million)

By 2020 - 19% > 65

By 2050 - 27% > 65

Children can maintain a higher standard of living than their parents

Many children would prefer their parents to utilise assets to maintain quality of life

Source: Trowbridge Deloitte

Clients Who Can Use a Reverse Mortgage

Target Clients for Financial Planners

People 60 years and over:

Current retiree clients with investment funds locked up and with short-term

cash needs

Lapsed retiree customers with some investment history but no investment

funds remaining (perhaps lapsed Allocated Pension clients); and

Non-clients who are retired with asset/income imbalance but no investment

history

Clients in accumulation phase who are currently supporting their parents

Common Applications

Supplementing existing funds with regular cash flow

Covering essential services such as medical costs

Undertaking home renovations

Paying out an existing mortgage

Generating an income stream

Funding ongoing home care

Paying an accommodation bond to an age care facility

Relieving the burden on the accumulator who is supporting a parent who owns

their own home

Making a contribution into superannuation

For wealthier retirees who wish to pass on their inheritance while they are alive by

borrowing funds against the value of their home and giving it to intended

beneficiaries

Issues That Should Be Considered

Projected movements in interest rates and property prices

Variations in consumer’s life expectancies and old-age caring and housing needs

Intergenerational tensions and conflict between the desire to leave an inheritance

and the need for money to live on in older age

How much care they may require both at home and perhaps in aged care facilities

and the costs of such needs

How much super they have and how much if any government benefits they may

be entitled to

If they receive regular payments from a provider, whether there will be sufficient

funds available to sustain these payments for the rest of their lives

Social Security Considerations

The Social Security Act has special rules covering home equity conversion

agreements, which means:

“…. an agreement under which the repayment of an amount paid to or on behalf of the person, or the person’s partner, is secured by a mortgage of the principal home of the person or person’s partner”

Implications for both the Income and Assets Tests

Note

The monies advanced from a loan are not income under the Income Test; and

The loan itself is not an asset under the Assets Test

The Assets Test

Under a reverse mortgage, where the amount borrowed is unspent:

The first $40,000 is not counted as an asset for 90 days; and

The amount over the first $40,000 is counted as an asset immediately

Where the amount borrowed is spent, depending on what the funds are used for,

further assessment may be necessary

If the amount is spent on non-assessable items (e.g. repairs or improvement to

the principal place of residence) no further assessment is necessary

If the amount is spent on assessable items (e.g. a motor car) the relevant

Income and Assets Test will apply

The Income Test

The amount advanced under a reverse mortgage is not income itself; rather any

additional income assessable under this Test depends on how the loan proceeds

are used

Where the unspent part of the loan is held as a financial asset (e.g. bank account,

shares, managed funds) it will be subject to deeming. Where the loan is spent on

consumer goods, no additional income is included under the Income Test

Financial investments under the deeming provisions of the Income Test are

‘deemed’ to earn a certain rate of income no matter what rate of income is actually

earned

Case Study 1 - Undertaking Home Renovations

Couple, both age 75

Asset rich – family home valued around $500,000

Income poor – full age pension only*

They do not want to sell their home

Tap into $30,000 home equity to renovate interior and exterior of home

$30,000 is spent immediately

No deemed income under the Income Test

$30,000 spent on home improvements (an exempt asset) and therefore does not

count towards assessable assets

Full age pension not affected*

*Based on social security rates effective 20 September 2006

Case Study 2 – Allowing Proceeds to Accumulate

Single pensioner aged 75

In receipt of the full age pension*

Tap into $90,000 home equity and allow loan proceeds to accumulate in bank

account

The $90,000 is being held as a financial asset (bank account)

Deemed income on full amount immediately

Up to $3,732 p.a. ($144pf) counted as income

Could lead to a reduction in the age pension

Income free area $128pf*

$50,000 of the loan when held in bank account will count as an asset immediately

After 90 days, the remaining $40,000 will also count as an asset

*Based on social security rates effective 20 September 2006

Case Study 3 – Paying Off the Mortgage For Ageing Parents

45 year old accumulator

Paying mortgage for ageing parents

Siblings unable to contribute

Parent home worth $500,000

Outstanding loan worth $40,000

Parents tap into $60,000 home equity

Apply $40,000 to settle existing mortgage and $20,000 to renovate bathroom

Keep capital and investment plan intact

Burden of supporting parents carried by the estate and will be shared equally

by siblings

Case Study 4 – Impact on Social Security Entitlements

Rex and Bonny both aged 70 have paid off their family home now valued at

$900,000

Their only other assets are lifestyle assets of $30,000 and financial assets of

$40,000

They are in receipt of the full age pension*

They decide to borrow $225,000 (LVR 25%) against the value of their property

What options do Rex and Bonny have as to how they can receive the $225,000,

and how will this impact their social security entitlements?

Option 1: A single lump sum of cash

Option 2: A drip feed facility; allows Rex and Bonny to receive a regular cash

payment over a number of years ($1,250 each month)

Option 3: A re-draw facility; allows Rex and Bonny to request cash advance whenever needed ($2,000 each month); or

Option 4: A combination of the above * Social security rates and thresholds effective 20 September 2006

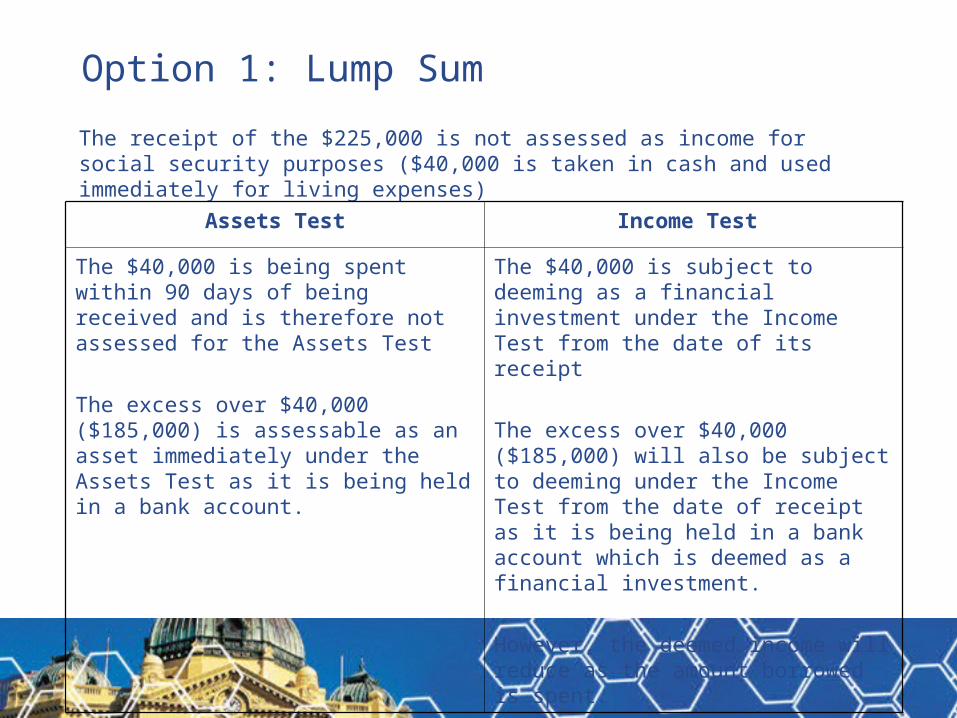

Option 1: Lump Sum

The receipt of the $225,000 is not assessed as income for social security purposes ($40,000 is taken in cash and used immediately for living expenses)

Assets Test Income Test

The $40,000 is being spent within 90 days of being received and is therefore not assessed for the Assets Test

The excess over $40,000 ($185,000) is assessable as an asset immediately under the Assets Test as it is being held in a bank account.

The $40,000 is subject to deeming as a financial investment under the Income Test from the date of its receipt

The excess over $40,000 ($185,000) will also be subject to deeming under the Income Test from the date of receipt as it is being held in a bank account which is deemed as a financial investment.

However, the deemed income will reduce as the amount borrowed is spent.

Option 1: Lump Sum

Prior to reverse mortgage Subsequent to reverse mortgage

Lifestyle assets

Car/Home Contents

Assets

$30,000

Income

$0

Lifestyle assets

Car/Home Contents

Assets

$30,000

Income

$0

Financial assets

Cash/Bank Account

$40,000 $1,200

(deemed amt)

Financial assets

Cash/Bank Account

$225,000 $11,974

(deemed amt)

Social Security Age Pension

$22,391*

in yr 1

Social Security Age Pension

$19,973*

in yr 1

* Social security rates and thresholds effective 20 September 2006, includes Pharmaceutical Allowance

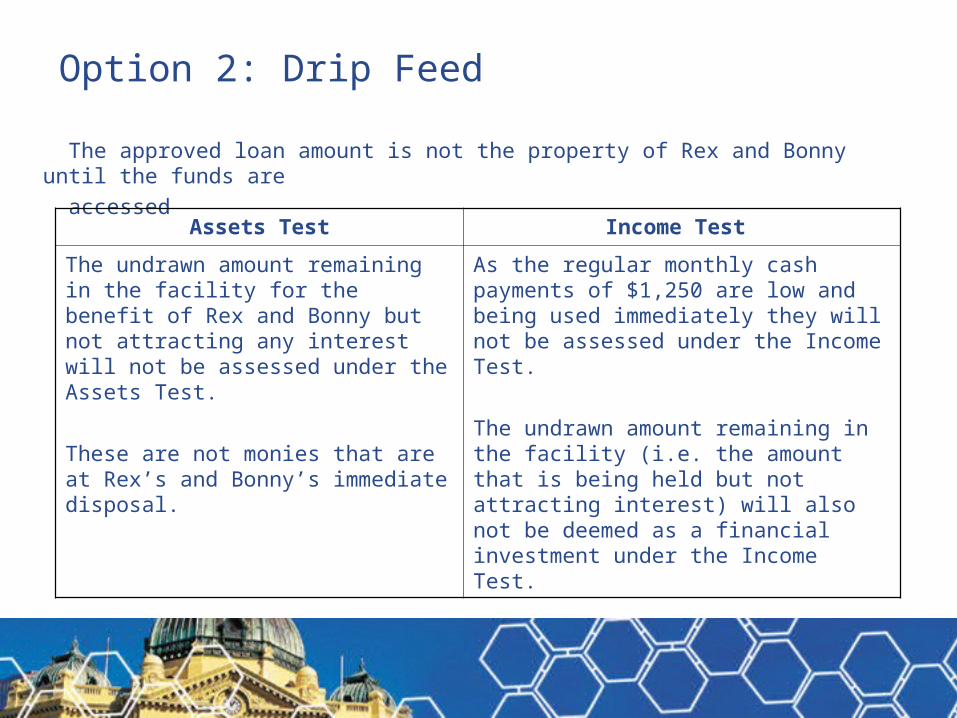

Option 2: Drip Feed

The approved loan amount is not the property of Rex and Bonny until the funds are

accessed

Assets Test Income Test

The undrawn amount remaining in the facility for the benefit of Rex and Bonny but not attracting any interest will not be assessed under the Assets Test.

These are not monies that are at Rex’s and Bonny’s immediate disposal.

As the regular monthly cash payments of $1,250 are low and being used immediately they will not be assessed under the Income Test.

The undrawn amount remaining in the facility (i.e. the amount that is being held but not attracting interest) will also not be deemed as a financial investment under the Income Test.

Option 2: Drip Feed

Prior to reverse mortgage Subsequent to reverse mortgage

Lifestyle assets

Car/Home Contents

Assets

$30,000

Income

$0

Lifestyle assets

Car/Home Contents

Assets

$30,000

Income

$0

Financial assets

Cash/Bank Account

$40,000 $1,200

(deemed amt)

Financial assets

Cash/Bank Account

$40,000 $1,200

(deemed amt)

Social Security Age Pension

$22,391*

in yr 1

Social Security Age Pension

$22,391*

in yr 1

* Social security rates and thresholds effective 20 September 2006, includes Pharmaceutical Allowance

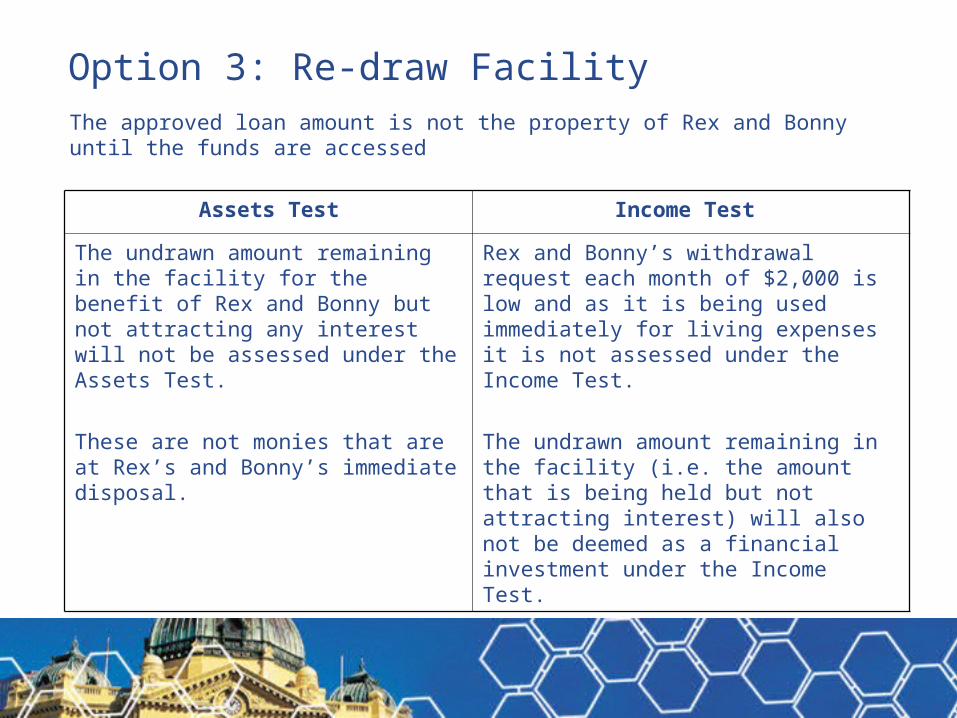

Option 3: Re-draw FacilityThe approved loan amount is not the property of Rex and Bonny until the funds are accessed

Assets Test Income Test

The undrawn amount remaining in the facility for the benefit of Rex and Bonny but not attracting any interest will not be assessed under the Assets Test.

These are not monies that are at Rex’s and Bonny’s immediate disposal.

Rex and Bonny’s withdrawal request each month of $2,000 is low and as it is being used immediately for living expenses it is not assessed under the Income Test.

The undrawn amount remaining in the facility (i.e. the amount that is being held but not attracting interest) will also not be deemed as a financial investment under the Income Test.

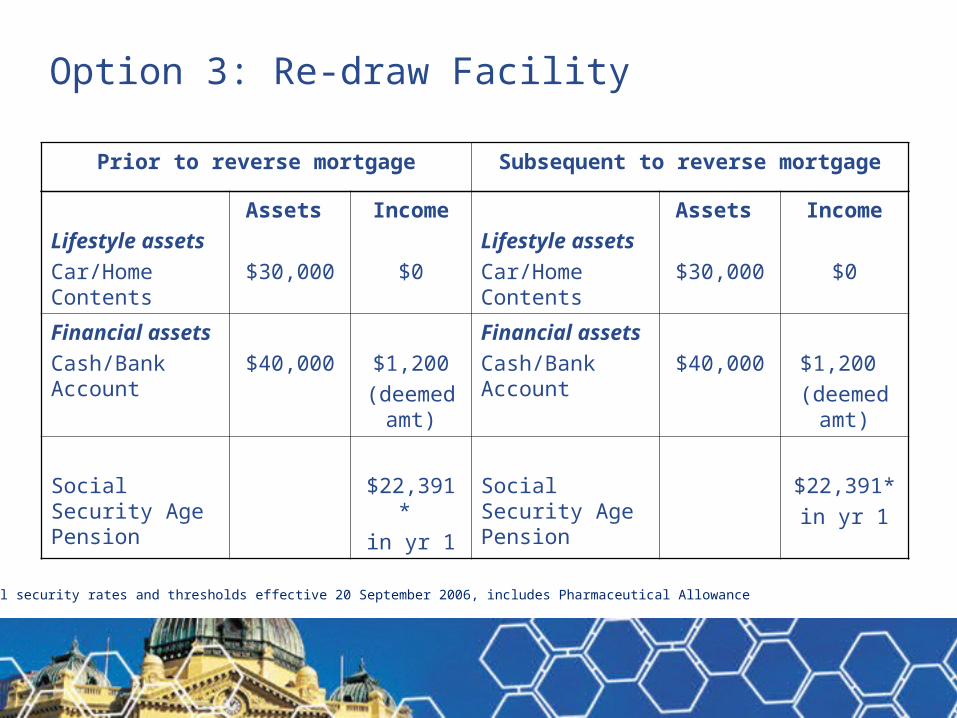

Option 3: Re-draw Facility

Prior to reverse mortgage Subsequent to reverse mortgage

Lifestyle assets

Car/Home Contents

Assets

$30,000

Income

$0

Lifestyle assets

Car/Home Contents

Assets

$30,000

Income

$0

Financial assets

Cash/Bank Account

$40,000 $1,200

(deemed amt)

Financial assets

Cash/Bank Account

$40,000 $1,200

(deemed amt)

Social Security Age Pension

$22,391*

in yr 1

Social Security Age Pension

$22,391*

in yr 1

* Social security rates and thresholds effective 20 September 2006, includes Pharmaceutical Allowance

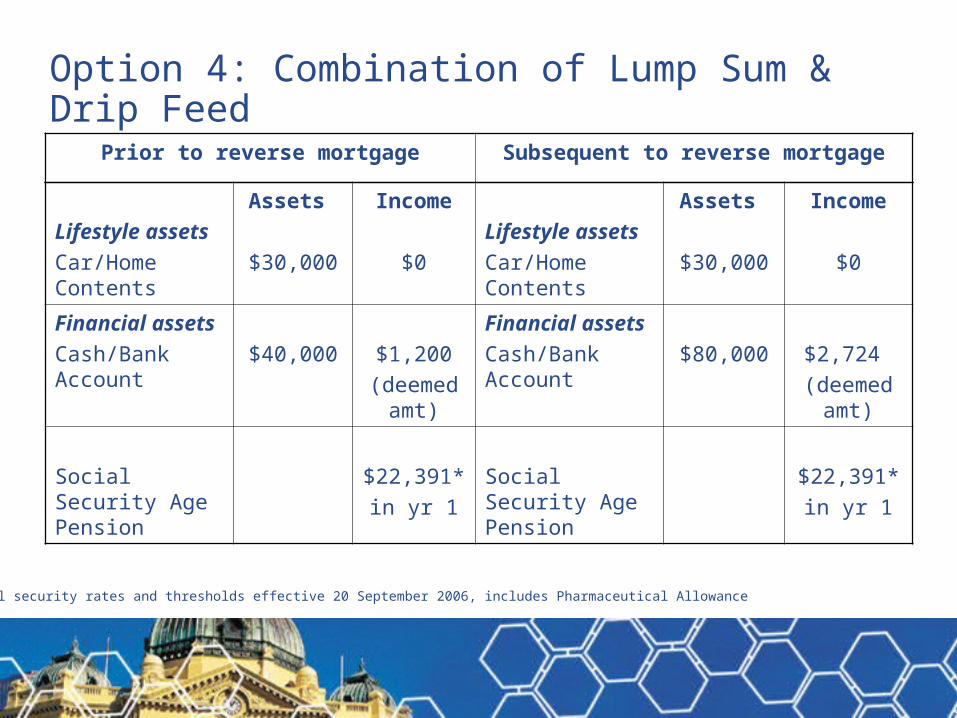

Option 4: Combination of Lump Sum & Drip Feed

The approved loan amount is not the property of Rex and Bonny until the funds are accessed ($40,000 is taken in cash and used immediately for living expenses)

Assets Test Income Test

The $40,000 is being spent within 90 days of being received and therefore is not assessed for the Assets Test.

The remaining loan amount that is being held and not attracting any interest for the benefit of Rex and Bonny will not be assessed under the Assets Test. These are not monies that are at Rex’s and Bonny’s immediate disposal.

The $40,000 is subject to deeming as a financial investment under the Income Test from the date of its receipt. However, the deemed income will be reduced as the amount borrowed is spent. As the regular monthly cash payments of $1,250 are low and being used immediately they will not be assessed under the Income Test.

The undrawn amount remaining in the facility will also not be deemed as a financial investment under the Income Test.

Option 4: Combination of Lump Sum & Drip Feed

Prior to reverse mortgage Subsequent to reverse mortgage

Lifestyle assets

Car/Home Contents

Assets

$30,000

Income

$0

Lifestyle assets

Car/Home Contents

Assets

$30,000

Income

$0

Financial assets

Cash/Bank Account

$40,000 $1,200

(deemed amt)

Financial assets

Cash/Bank Account

$80,000 $2,724

(deemed amt)

Social Security Age Pension

$22,391*

in yr 1

Social Security Age Pension

$22,391*

in yr 1

* Social security rates and thresholds effective 20 September 2006, includes Pharmaceutical Allowance

Gifting

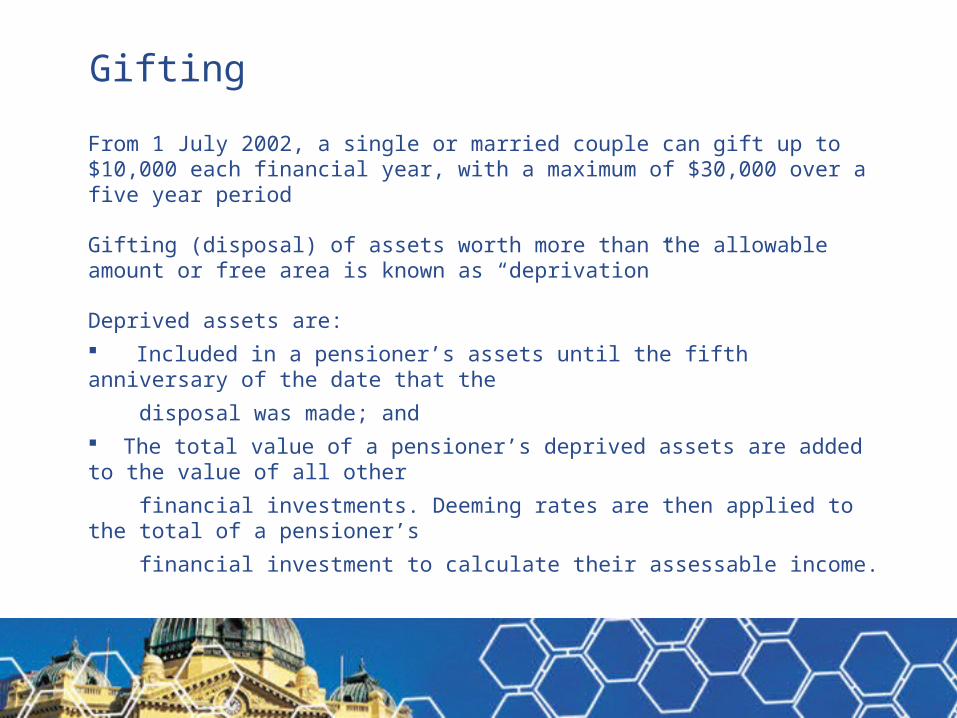

From 1 July 2002, a single or married couple can gift up to $10,000 each financial year, with a maximum of $30,000 over a five year period

Gifting (disposal) of assets worth more than the allowable amount or free area is known as “deprivation”

Deprived assets are:

Included in a pensioner’s assets until the fifth anniversary of the date that the

disposal was made; and

The total value of a pensioner’s deprived assets are added to the value of all other

financial investments. Deeming rates are then applied to the total of a pensioner’s

financial investment to calculate their assessable income.

Gifting

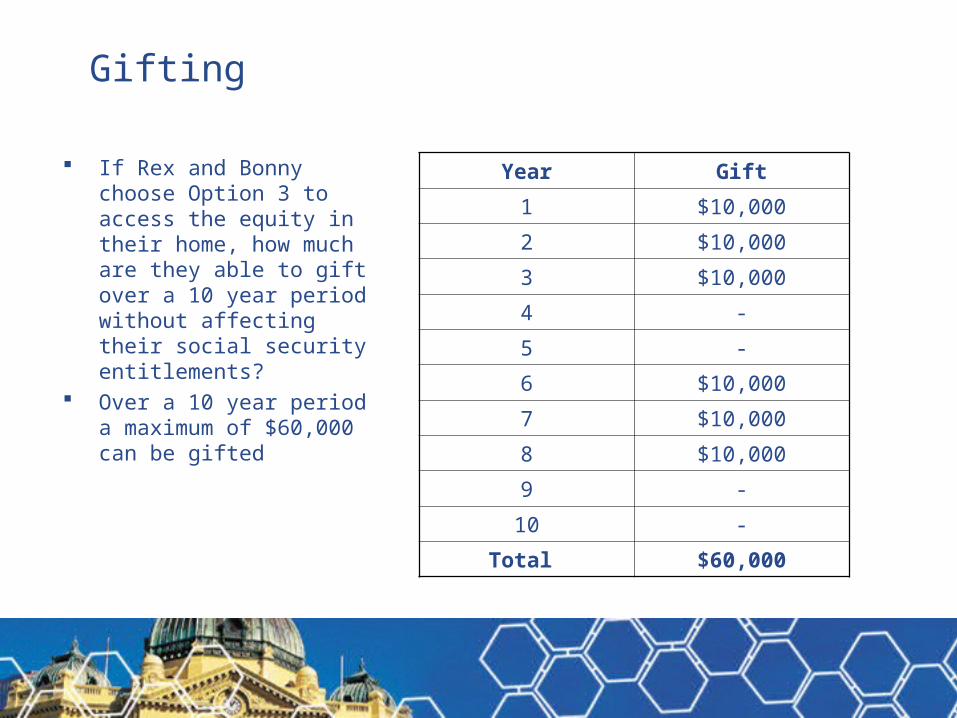

If Rex and Bonny choose Option 3 to access the equity in their home, how much are they able to gift over a 10 year period without affecting their social security entitlements?

Over a 10 year period a maximum of $60,000 can be gifted

Year Gift

1 $10,000

2 $10,000

3 $10,000

4 -

5 -

6 $10,000

7 $10,000

8 $10,000

9 -

10 -

Total $60,000

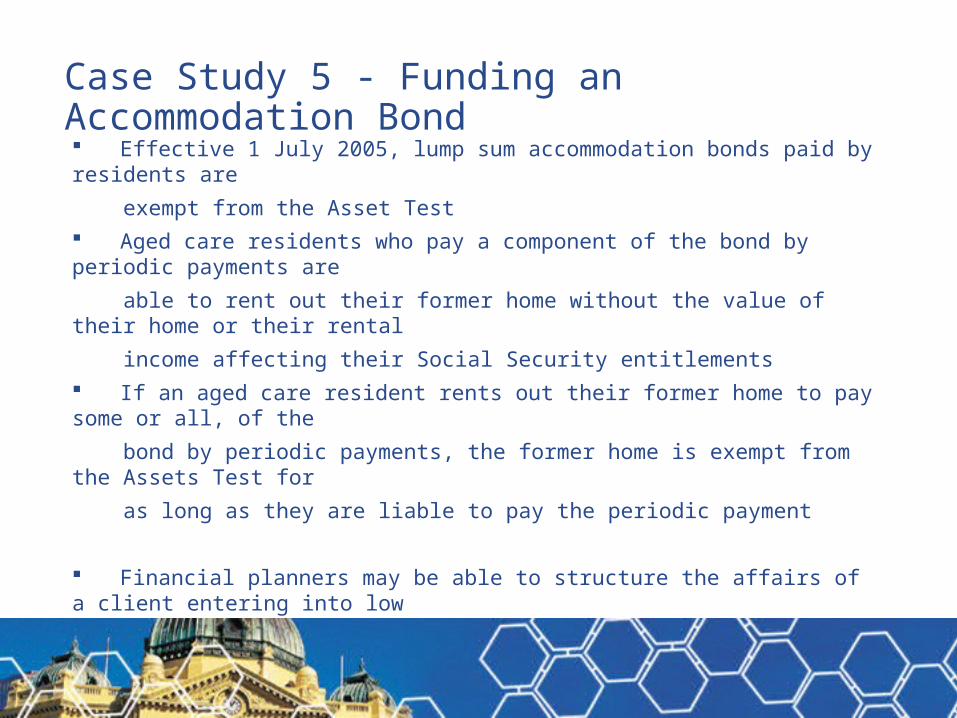

Case Study 5 - Funding an Accommodation Bond

Effective 1 July 2005, lump sum accommodation bonds paid by residents are

exempt from the Asset Test

Aged care residents who pay a component of the bond by periodic payments are

able to rent out their former home without the value of their home or their rental

income affecting their Social Security entitlements

If an aged care resident rents out their former home to pay some or all, of the

bond by periodic payments, the former home is exempt from the Assets Test for

as long as they are liable to pay the periodic payment

Financial planners may be able to structure the affairs of a client entering into low

level care so as to keep the age pension as well as the family home

The rental income from their home can then be used to fund some of the costs of

a residential age care facility

Case Study 5 - Funding an Accommodation Bond

Single pensioner aged 75

In receipt of the full age pension*

About to enter into low level (hostel) care and asked to pay an accommodation

bond of $135,000, however they do not wish to sell their family home

Decides to pay the accommodation bond in periodic payments, which is made up

of two components, the amount the service provider can deduct annually for up to

five years, and also the interest that the provider would normally earn on the lump

sum

*Based on social security rates effective 20 September 2006

Case Study 5 - Funding an Accommodation Bond

Residential aged care costs

Basic daily care fee

Bond is greater than $125,500 and therefore the non-pension basic daily care fee applies

$13,644* p.a.

($37.38 x 365 days)

Income tested fee

In receipt of the full age pension

$0.00 p.a.

Retention amount $3,282.00 p.a.

($273.50 x 12 months)

Periodic payments

10% is the maximum interest rate (July – Sept 2006)

$13,500* p.a.

(10% x $135,000)

Total $30,426 p.a.

* Social security rates and thresholds effective 20 September 2006

Case Study 5 - Funding an Accommodation Bond

Total income

Social security age pension

Paying bond by periodic payments and therefore able to rent former home without the value of the home or the rental income affecting the age pension. Former home will be exempt from the Assets Test for as long as the periodic payment is paid

$13,315* p.a.

Rental income $13,000 p.a.

($250 x 52)

Total $26,315 p.a.

* Social security rates and thresholds effective 20 September 2006

Case Study 5 - Funding an Accommodation Bond

$4,111 shortfall!

Accessing the equity in his home may enable a person entering into low level

(hostel) care to bridge the gap between the residential fees they have to pay and

the total income they receive from the combined age pension and rental income

Certain issues must be considered if the payment of an accommodation bond via

periodic payments is funded through a reverse mortgage

Tax issues - CGT exemption

Insurance on the home

Cost of financial plan initially and ongoing

Ongoing management issues of residential home being let

Case Study 6 - Special Disability Trust Measures

Effective 20 September 2006

The measure will assist families to make private financial provision, through a

special disability trust, for the future care and accommodation needs of their

children and close relatives with severe disabilities

The trust must be established solely in order to provide for current and future care

and accommodation needs of the beneficiary

The assessable assets of the trust will be exempt from the means test to

$500,000 (indexed annually)

Under the Assets Test, where the assessable assets of the trust are in excess of

the $500,000 limit, the balance is to be assessed as the beneficiary’s assets

Under the Income Test, the income derived by the trust and income received from

the trust by the beneficiary are exempt from the Income Test

Case Study 6 - Special Disability Trust Measures

Couple, both age 70

Daughter, aged 19 is severely disabled – in receipt of the full disability support

pension

Asset rich – family home valued at $550,000

Income poor – full age pension only*

They don’t want to sell their home, however they are unable to provide their

daughter with the extra financial support she needs for the ongoing care now and

after they have passed away

Tap into $225,000 home equity and contribute into a special disability trust with

their daughter as the principal beneficiary to provide for her current and future

accommodation and ongoing care

Full social security pensions (age pension and disability support pension) not

affected*

* Social security rates and thresholds effective 20 September 2006

Social Security Implications – Wrap Up

Be aware of the social security rules

How the proceeds from a reverse mortgage are used may affect social

security benefits

Careful advance planning as to how and when the funds are spent may help

borrowers to retain benefits

Why borrow money and let it sit in the client’s bank account for 90 days?

Why borrow the money in the first place if it is not needed?

Important to remember that periodic payments:

Are a return of capital and are not taxable

If spent and not accumulated, do not count under the Income Test

Are backed by a 100% Assets Test exempt asset (family home)

2006 Federal Budget AnnouncementsImpact on reverse mortgage strategies

Undeducted contributions

Personal after-tax contributions will be limited to $150,000 p.a. (three times

the limit for concessional contributions). A higher cap of $1 million will apply

for the transitional period from 10 May 2006 to 30 June 2007

Nearing or approaching retirement – strategy involving selling investment

property and contributing proceeds into super

Option – reverse mortgage on investment property

Pension Assets Test

The Assets Test taper rate for pensions will be halved. Pension recipients will

only lose $1.50 (not $3.000 per fortnight)

For example, based on current pension rates and thresholds, the proposed

changes mean the pension will not cut out until a single homeowner’s assets

exceed approximately $494,000 (currently $325,500). A homeowner couple will

receive part pension if their assets are under $783,500 (currently $503,200)

Action Plan

Review Existing Client Database:

Retiree customers with investment funds locked up and short term cash needs

Lapsed retiree customers with no investment funds remaining

Current accumulation customers who are supporting their parents

Current retiree customer with asset/income imbalance

Due to the implications a reverse mortgage may have on a client’s personal

circumstances financial advice should be a mandatory requirement for the product

providers to release funds

Log on to www.marinerretirement.com.au to access reference material, quick

reference and technical guides

Disclaimer

The information contained in this presentation is for financial advisers only and is not to be passed on to retail clients, unless it forms part of the financial adviser’s own advice to the client. The information is not a securities recommendation. It is a guide only and based on legislation current as at September 2006. We believe the information contained in this update has been obtained from reliable sources but we cannot be responsible for any errors, omission or inaccuracies.