Reunion Presentation 2008 Dwight Drake Federal Payroll Tax 15.3 % of first $102,000 of earned income...

40

Reunion Presentation 2008 Federal Payroll Tax 15.3 % of first $102,000 of earned income 2.9% of excess earned income

-

date post

21-Dec-2015 -

Category

Documents

-

view

213 -

download

0

Transcript of Reunion Presentation 2008 Dwight Drake Federal Payroll Tax 15.3 % of first $102,000 of earned income...

Reunion Presentation 2008

Dwight Drake

Federal Payroll Tax

15.3 % of first $102,000 of earned income

2.9% of excess earned income

Reunion Presentation 2008

Dwight Drake

Bottom Line for Middle- and Low-Income America

More Than One in Seven Earned Dollars Taken Off The Top to Feed the Gorilla

} Gorilla Tax

Reunion Presentation 2008

Dwight Drake

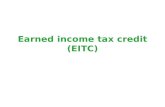

Rush Limbaugh Website - “Truth About Taxes”

Only the Rich Pay Taxes!

IRS Latest Data:

- Top 1% Pay More Than 39%

- Top 25% Pay Over 86%

- Top 50% Pay Over 97%

Reunion Presentation 2008

Dwight Drake

Rich vs. Non-Rich Non-Rich Rich

Self employment income 60,000 0

S Corp earnings 0 300,000

Dividends 0 150,000

Capital gains 0 150,000

Total Income 60,000 600,000 10 x

Income taxes 2,546 108,892 42.8 x

Taxes as % of income 4.24% 18.14%

Reunion Presentation 2008

Dwight Drake

Rich vs. Non-Rich Non-Rich Rich

Self employment income 60,000 0

S Corp earnings 0 300,000

Dividends 0 150,000

Capital gains 0 150,000

Total Income 60,000 600,000 10 x

Income taxes 2,546 108,892 42.8 x

Gorilla payroll taxes 9,180 0

Total taxes 11,726 108,892

Taxes as % of income 19.54% 18.14%

Reunion Presentation 2008

Dwight Drake

Savings As % of Household Disposable Income

0

2

4

6

8

10

12

France

Germany

Italy

Netherlands

Japan

U.K

U.S

Reunion Presentation 2008

Dwight Drake

80% of Americans:

Payroll Tax Hit Exceeds Income Tax Hit - Often By Many Times

Source: Congressional Budget Office (January 2002)

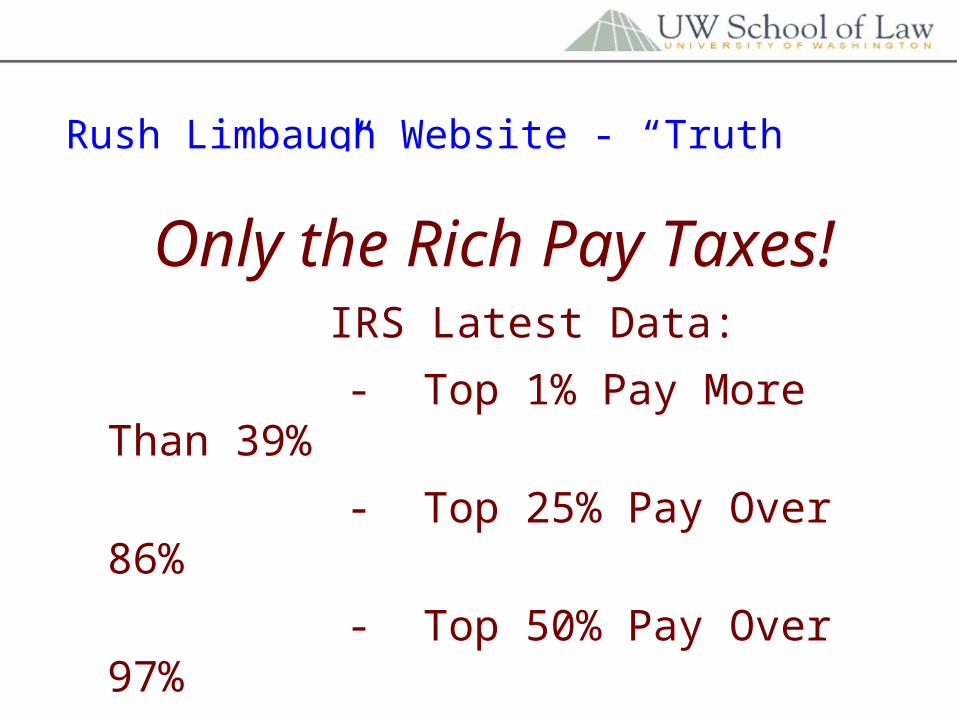

Corporate & Partnership Tax - Instructor: Dwight Drake

C Corp

Depr. Ded.

Tax Exemptor foreign

entity

Property

Lease

Sale-In Lease Out (‘SILO”) Corporate Tax Shelter

Debt Service

Lease Payments

Corporate & Partnership Tax - Instructor: Dwight Drake

SILO Simplified Hypothetical Numbers The Deal:

- Property Cost $60 million.

- 30 yr financing @ 5%. Annual debt service $3,840,000. Approx. $3,240,00 interest; 600k principal.

- Lease payments: $3,300,000 a year.

First Year Tax Impact if depreciation 10 yr 150% DDB:

C Corp: Lease income: 3,300,000.

Interest expense: (3,240,000)

Depreciation: (9,000,000)

Tax Loss (8,940,000)

Tax savings @ 35% 3,129,000

Exempt Org Dollar gain & C Corp dollar cost: $540,000 (3,840,000 less 3,300,000)

Corporate & Partnership Tax - Instructor: Dwight Drake

Domestic C Corp

Foreignentity

Foreign Income Corporate Tax Shelter Shift ala UPS

Common Owners

Independent Company

DeductiblePremiums Reinsurance

Premiums

Corporate & Partnership Tax - Instructor: Dwight Drake

C Corp Shelter Attacks1. New Section 470 Anti-SILO Provision: Protection fund less than 20% of basis; min. 20%

equity investment if lease over 5 yrs; lessee not bear risk of loss if lease over 5 yrs; if over 7 yr class life, any lessee option price must be FMV at time of exercise.

2. Expanded information reporting requirements under 6011.

3. Extended statute of limitations for listed transactions under 6501.

4. New failure to disclose penalty under 6707A.

5. New accuracy related penalty for listed and reportable transactions under 6662A.

6. Interest deduction denied on underpayments per redesigned 163(m).

7. New penalties for individuals failure to report, not maintaining investor lists, for tax shelter promoters, failure to report foreign accounts.

8. Expanded authority to enjoin material advisors.

9. Confidentiality exception for professionals on tax shelters.

10. Senate attempts at “non-business propose” and “changed economic position” standards. House has refused to play ball. Only a matter of time.

Corporate & Partnership Tax - Instructor: Dwight Drake

Check The Box GamePre – 1997

- Big fear was partnership or LLC taxable deemed

“association” taxable as C corp.

- Two Given Factors:

Associates

Business Objective

- Four Determinative Factors (Must Flunk Two):

Continuity of Life

Central Management

Limited Liability

Free Interest Transferability

Corporate & Partnership Tax - Instructor: Dwight Drake

Check The Box GamePost – 1996

- Corporate Characteristic Test Gone.

- Corporation is taxed as corp – C or S.

- Partnership or LLC taxes as partnership unless elect

to be taxed as C or S corp. Effective up to 75 days

before and 12 months after election.

- Sole owner non-corp is disregarded entity, taxed as

sole proprietorship.

- Pre-97 entities keep status, except for solos.

- No change for 60 months – unless IRS approval or

50% change in ownership.

Corporate & Partnership Tax - Instructor: Dwight Drake

Check The Box Game

Tax consequences of change:

From partnership to C status: Deemed contribution of assets for stock, followed by liquidation with stock distributed to owners.

From C status to partnership: Deemed asset distribution by corp to shareholders (very expensive tax wise), followed by contribution of assets to new partnership.

Corporate & Partnership Tax - Instructor: Dwight Drake

Why Use C Corp? 1. Bracket racquet at low end: $13,750 corporate tax of first $75,000 of

earnings versus $26,250 individual (35%).

2. Tax-free employee benefits for shareholder employees.

3. Tax-free reorganization potential.

4. Corporate year flexibility.

5. § 1045 Rollover potential.

6. § 1202 capital gain exclusion (50%). Deceiving at 28% rate.

7. § 1244 ordinary loss treatment. (50k limit)

8. LTCG treatment on stock gain.

9. Consolidated return convenience.

10. True “Separateness” – “Don’t mess with my return” factor.

11. Auto control for majority.

Corporate & Partnership Tax - Instructor: Dwight Drake

Rate ComparisonsMarried Filing Jointly: C Corps (Inclusive Bubbles)

First 14,300 - 10% First 50k 15%

Excess to 58,100 15% Excess to 75k 25%

Excess to 117,250 25% Excess to 100k 34%

Excess to 178,650 28% Excess to 335k 39% (First Bubble)

Excess to 319,100 33% Excess to 10 mill 34%

Excess 35% Excess to 15 mill 35%

Capital Gain Max 15% Excess to 18.33 mill 38% (Second Bubble)

Dividend Max 15% Excess 35%

C Corp Income Split – 150k

C Corp Pass Thru Entity

C tax on 50k 7,500

Owner income tax on excess 14,236 27,140

Total Income tax 21,736 27,140

Savings of 19.9%

* Assumes payroll taxes a push, married couple with two exemptions, use of standard deduction, and year is 2005.

Copyright 2005 Dwight Drake. All Rights Reserved.Business Planning: Closely Held Enterpriseswww. drake-business-planning.com

Corporate & Partnership Tax - Instructor: Dwight Drake

Fringe Benefit Limitations

1. Three primary employee fringe benefits:

- Section 79 Group Term Life Insurance

- Medical and Dental Reimbursement Plans

- Section 125 Cafeteria Plans

2. C Corp employees get all even if shareholders

3. Partners of partnership may not participate

4. 2% or more shareholders of S Corp may not participate

Corporate & Partnership Tax - Instructor: Dwight Drake

Why Use Partnership-Taxed Entity? 1. Income pass thru – no double tax.

2. Loss pass thru – still have basis, at-risk and passive loss hurdles.

3. Passive income potential.

4. Special allocation potential.

5. Outside basis adjustments.

6. Easy cash and property bail-outs.

7. Inside basis adjustment – 754.

8. Tax-free profits interest.

9. Transfer-for-value exception.

Corporate & Partnership Tax - Instructor: Dwight Drake

S Corp Eligibility Requirements (§ 1361)

1. Eligible Corps – no banks or insurance companies, affiliated group member only if “Qualified Subchapter S Subsidiary” – 100% owned by S corp and election to disregard QSSS as tax entity.

2. Shareholder number: 100 max. Married couple count one. Families (6 generations deep) may count as one. If fiduciary holds, look thru to beneficiaries.

3. Eligible shareholders: No corps, partnerships, nonresident aliens, or ineligible trusts. Estate’s, qualified pension trusts and some charitable trusts OK.

4. One Class of Stock. Voting differences only allowed.

Corporate & Partnership Tax - Instructor: Dwight Drake

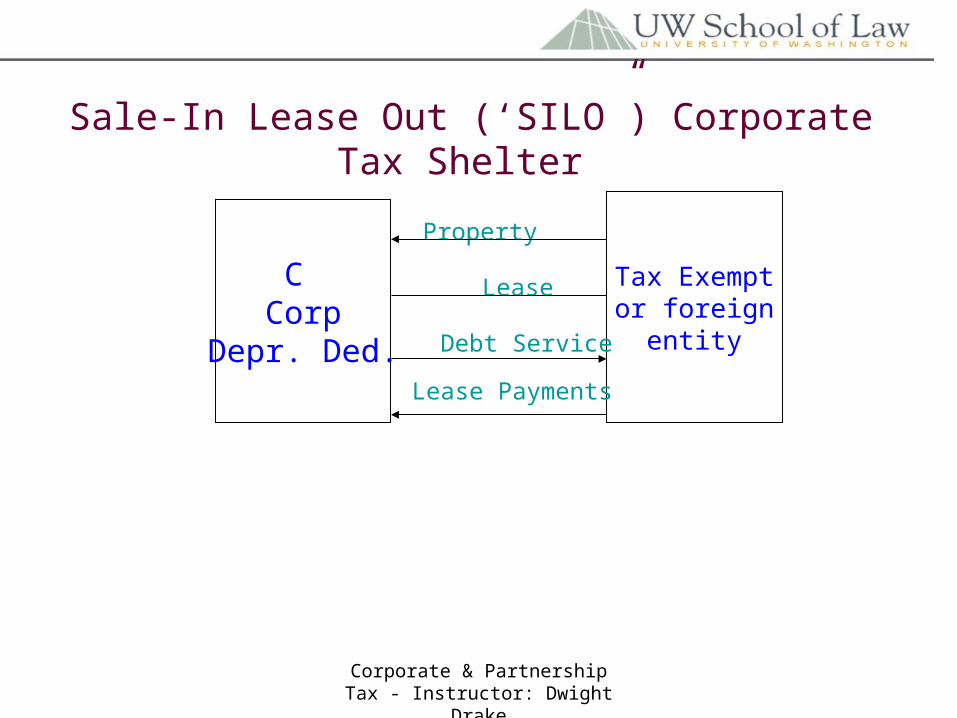

Trusts That Work With S Election

1. Voting trusts

2. Grantor trusts

3. Testamentary trusts that were grantor trusts – for 2 years following death of grantor.

4. Testamentary trusts that receive S corp stock under will – but only for 2 years following death.

5. “QSST” - Qualified Subchapter S Trusts. Requires: Only one beneficiary; all income distributed annually to US citizen or resident; Elect QSST status and treated as owner of S corp stock for tax purposes. QTIP Trust classic example.

6. “ESBT” – Electing Small Business Trust. Requires: All beneficiaries qualified S corp shareholders; all interests received by gift or bequest, not purchase; trust S corp income taxed at highest individual marginal rates. Advantage: allows multiple Bs and income sprinkling.

Corporate & Partnership Tax - Instructor: Dwight Drake

Straight Debt Huge Safe Harbor 1361(c)(5)

1. Unconditional promise to pay on demand or at specified time.

2. Interest rate and payments not contingent on profits or discretion.

3. No convertibility

4. Creditor actively and regularly engaged in lending money or is individual, estate or trust that would be eligible S corp shareholder.

Note: If safe harbor met, excess interest may still not be treated as interest for tax purposes.

Corporate & Partnership Tax - Instructor: Dwight Drake

Why Use S Corporation? 1. Income pass thru – no double tax.

2. Loss pass thru – still have basis, at-risk and passive loss hurdles. Basis hurdle tougher.

3. Passive income potential.

4. Outside basis adjustments.

5. Bail-outs – easier than C, harder than partnership.

6. Tax-free reorg potential.

7. Full capital gains benefit on stock sale.

8. Easier self employment tax planning.

9. Multiple entity consolidation with QSSS.

10. Auto majority control potential.

Corporate & Partnership Tax - Instructor: Dwight Drake

Problem 694(a)

Z Corp

99 Individuals

A & B Brothers JT

1 Share Each

21 Shares

Valid S Corp. 100 Shareholder Requirement Satisfied Per Family Provision of 1361(c)(1).

Corporate & Partnership Tax - Instructor: Dwight Drake

Problem 694(b)

Z Corp

99 Individuals

A & B Spouses

1 Share Each

21 Shares

Valid S Corp. 100 Shareholder Requirement Satisfied Per Family Provision of 1361(c)(1).

Corporate & Partnership Tax - Instructor: Dwight Drake

Problem 694(c)

Z Corp

99 Individuals

A & B Spouses

1 Share Each 21 Shares

S election good so long as shares held in A’s estate. Once transferred to F, 100 shareholder requirement flunked. S election ends, with short S year and short C year.

F Friend

A Dies, SharesTransferred

Corporate & Partnership Tax - Instructor: Dwight Drake

Problem 694(d)

Z Corp

99 Individuals

Voting Trust

1 Share Each 21 Shares

Voting trust permissible S shareholder, but 100 shareholder requirement flunked because now have 102 shareholders.

3Beneficiaries

Corporate & Partnership Tax - Instructor: Dwight Drake

Problem 694(e)

Z Corp

99 Individuals

Revocable Living Trust

1 Share Each 21 Shares

Grantor trust permissible S shareholder, and 100 shareholder requirement not flunked because only one beneficiary.

OneBeneficiary

Corporate & Partnership Tax - Instructor: Dwight Drake

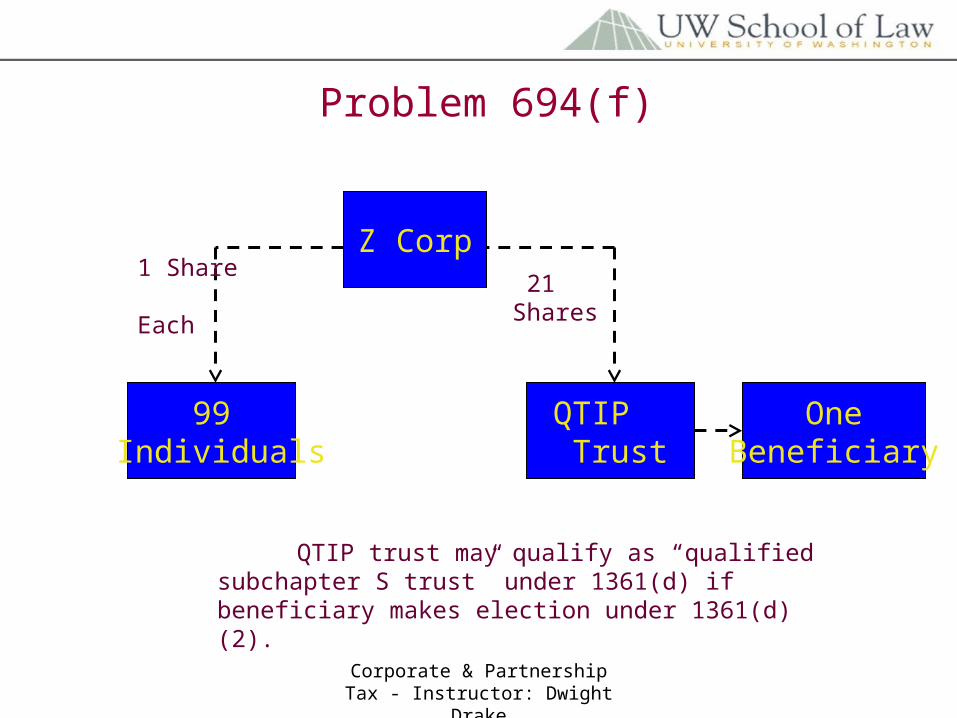

Problem 694(f)

Z Corp

99 Individuals

QTIP Trust

1 Share Each 21 Shares

QTIP trust may qualify as “qualified subchapter S trust” under 1361(d) if beneficiary makes election under 1361(d)(2).

OneBeneficiary

Corporate & Partnership Tax - Instructor: Dwight Drake

Problem 694(g)

Partnership

S Corp 100 Shr’s

S Corp 100 Shr’s

Partner Partner

S election permitted per Rev. Rule 94-43. Rationale: 100 limit was for administrative simplicity, which is not adversely effected by partnership.

S Corp100 Shr’s

Partner

Corporate & Partnership Tax - Instructor: Dwight Drake

Problem 694(h)

S Corp

Shareholder

VotingCommon

NonvotingCommon

S election works. Voting and nonvoting still considered one class per 1361(c)(4). Preferred would kill S if issued, but no effect if unissued.

UnissuedPreferred

Shareholder

Corporate & Partnership Tax - Instructor: Dwight Drake

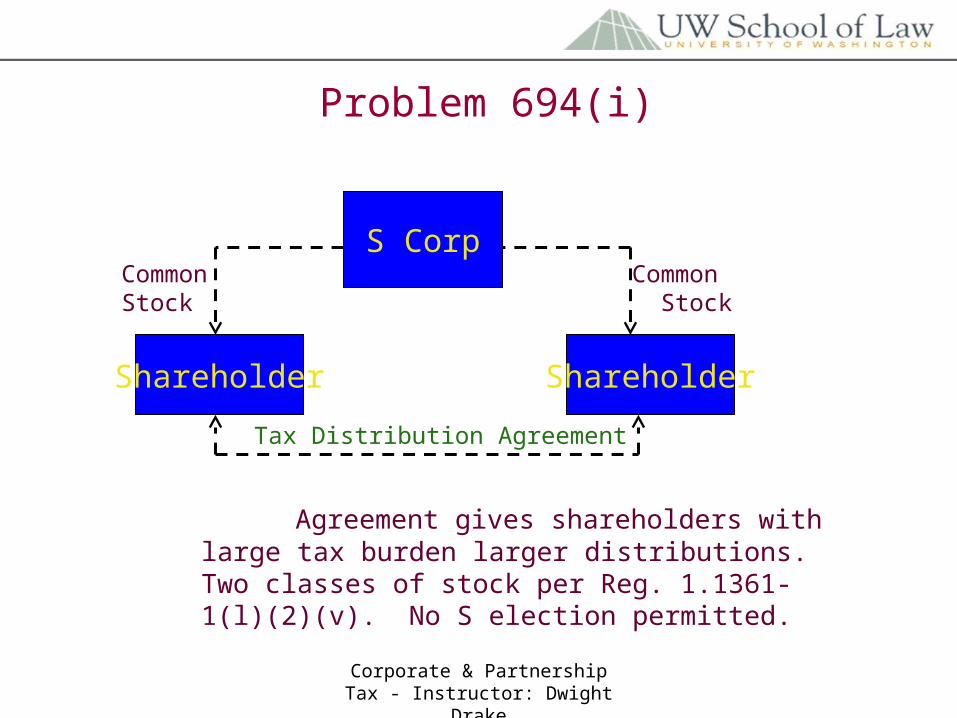

Problem 694(i)

S Corp

Shareholder

CommonStock

Common Stock

Agreement gives shareholders with large tax burden larger distributions. Two classes of stock per Reg. 1.1361-1(l)(2)(v). No S election permitted.

Shareholder

Tax Distribution Agreement

Corporate & Partnership Tax - Instructor: Dwight Drake

Problem 694(j)

S Corp

Shareholder

Debt & Stock 25 to 1 Ratio

Shareholder

Debt & Stock 25 to 1 Ratio

Clearly bonds may be equity, but not kill S if “straight debt”

per 1361(c)(5)(A). Neither subordination nor high rate

prevent “straight debt”, but excess interest may not be

deductible as interest.

Corporate & Partnership Tax - Instructor: Dwight Drake

Problem 699(a)

S Corp

A B C D

300 Shrs 100 Shrs 100 Shrs 100 Shrs

Operations began October 3

(a) Who must consent to S? All shareholders, including nonvoting. 1362(a)(2).

If B sold to G, both B & G would need to consent because both shareholders during

first year. If B refused, then election good for second year.

If B partnership which transfer to individual, election not good for first year because

B (ineligible shareholder) owned for part of first year. Election good for year 2.

Corporate & Partnership Tax - Instructor: Dwight Drake

Problem 699(b)

S Corp

A B C D

300 Shrs 100 Shrs 100 Shrs 100 Shrs

Operations began October 3

(b) When election required? By 15th day of third month. 1362(b)(1)(B). Begin

Oct 3, so election due by Dec 17. New corp year begins when corp has shareholders,

acquires assets or begins business, whichever is first.

Corporate & Partnership Tax - Instructor: Dwight Drake

Problem 699(c)

S Corp

A B C D

300 Shrs 100 Shrs 100 Shrs 100 Shrs

Operations began October 3

(c) What taxable year allowed? “Permitted year” is calendar year or natural

business year. 25% last two month gross reciepts test of Rev. Proc. 87-32. Also,

444 election and 7519 deposit game allowed. Since ski resort, should meet 25% test.

Corporate & Partnership Tax - Instructor: Dwight Drake

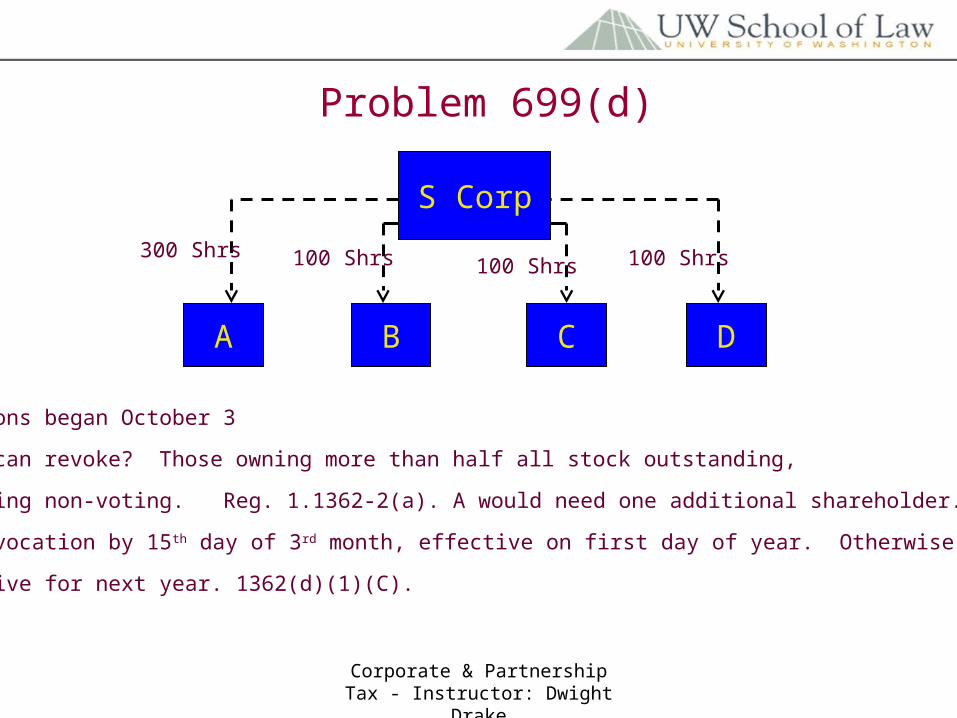

Problem 699(d)

S Corp

A B C D

300 Shrs 100 Shrs 100 Shrs 100 Shrs

Operations began October 3

(d) Who can revoke? Those owning more than half all stock outstanding,

including non-voting. Reg. 1.1362-2(a). A would need one additional shareholder.

If revocation by 15th day of 3rd month, effective on first day of year. Otherwise,

effective for next year. 1362(d)(1)(C).

Corporate & Partnership Tax - Instructor: Dwight Drake

Problem 699(e)

S Corp

A B C D

300 Shrs 100 Shrs 100 Shrs 100 Shrs

Operations began October 3

(e) C sells to nonresident alien? S termination immediately. 1362(b)(1)(C).

Current year divided into short S year and short C year. 1362(d)(2)(B) & 1362(e).

Corporate & Partnership Tax - Instructor: Dwight Drake

Problem 699(f)

S Corp

A B C D

300 Shrs 100 Shrs 100 Shrs 100 Shrs

Operations began October 3

(f) Only 5 shares to Olga and C had no knowledge? 1362(f) permits

cure for inadvertent termination. Olga’s sale would need to be rescinded

and C recognizes income otherwise allocable to Olga. “Inadvertent” burden

of proof on corporation. Fact that corp had no knowledge of sale “tends to

establish” proof of “inadvertence”. Reg. 1.1362-4(b) and -5.

Corporate & Partnership Tax - Instructor: Dwight Drake

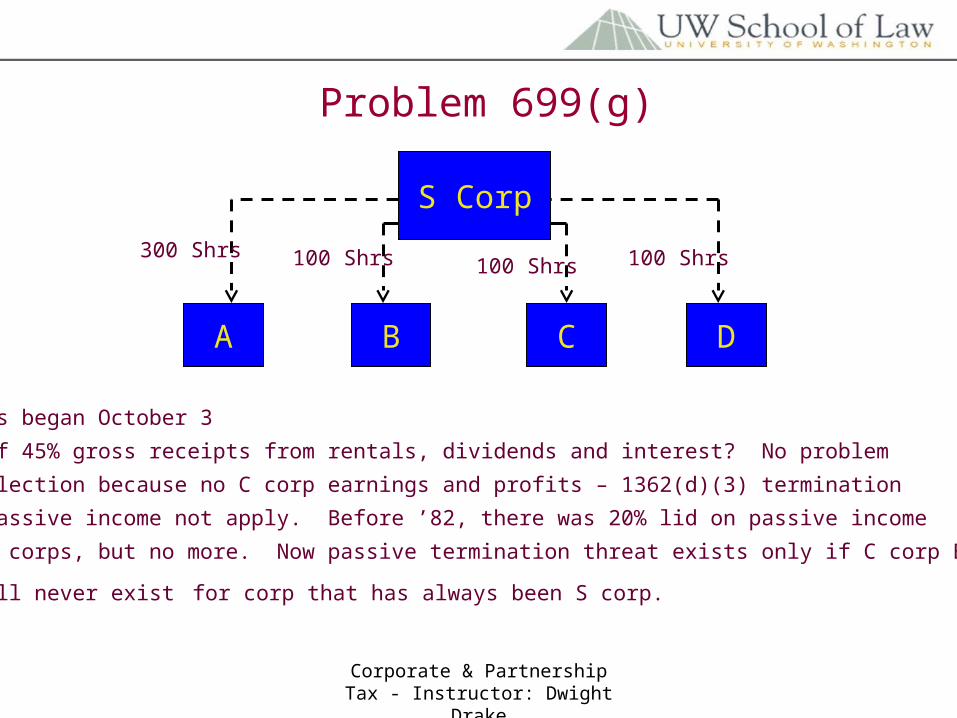

Problem 699(g)

S Corp

A B C D

300 Shrs 100 Shrs 100 Shrs 100 Shrs

Operations began October 3

(g) What if 45% gross receipts from rentals, dividends and interest? No problem

with S election because no C corp earnings and profits – 1362(d)(3) termination

for 25% passive income not apply. Before ’82, there was 20% lid on passive income

for all S corps, but no more. Now passive termination threat exists only if C corp E & P,

which will never exist for corp that has always been S corp.