Retirement Planning Chapter 29 Tools & Techniques of Financial Planning Copyright 2009, The National...

64

Retirement Planning Chapter 29 Tools & Techniques of Financial Planning Copyright 2009, The National Underwriter Company 1 What is Retirement Planning? Retirement Planning is the process of insuring that there are sufficient financial resources to provide a desired lifestyle in the retirement years. It consists of several tasks: – Determining retirement financial needs. – Analyzing current resources to provide for retirement needs. – Working with retirement plan distributions and seeing that your client follows certain rules in a timely manner. For more detailed information on retirement planning, see the Tools & Techniques of Employee Benefit and Retirement Planning.

-

Upload

harriet-kelly -

Category

Documents

-

view

224 -

download

2

Transcript of Retirement Planning Chapter 29 Tools & Techniques of Financial Planning Copyright 2009, The National...

Retirement Planning Chapter 29Tools & Techniques of

Financial Planning

Copyright 2009, The National Underwriter Company 1

What is Retirement Planning?

Retirement Planning is the process of insuring that there are sufficient financial resources to provide a desired lifestyle in the retirement years. It consists of several tasks:

– Determining retirement financial needs.– Analyzing current resources to provide for

retirement needs.– Working with retirement plan distributions and seeing that your

client follows certain rules in a timely manner.

For more detailed information on retirement planning, see the Tools & Techniques of Employee Benefit and Retirement Planning.

Retirement Planning Chapter 29Tools & Techniques of

Financial Planning

Copyright 2009, The National Underwriter Company 2

Determining Financial Needs for Retirement

• Identifying client lifestyle expectations and quantifying income needs in retirement.

• Determining what resources are currently available to pay for retirement and whether they will be sufficient for the client’s desired lifestyle.

• Analyzing future income flow and sources of funds to meet future needs.

Retirement Planning Chapter 29Tools & Techniques of

Financial Planning

Copyright 2009, The National Underwriter Company 3

Determining Financial Needs for Retirement

• The process also includes obtaining information on qualified plan benefits, and recognition of the appropriate role of insurance in retirement planning.

• These steps, combined with TVM analysis, will determine what additional funds need to be saved and invested to meet client needs.

Retirement Planning Chapter 29Tools & Techniques of

Financial Planning

Copyright 2009, The National Underwriter Company 4

The Current Environment

Some of the factors you and your clients need to understand to successfully plan for wealth accumulation and retirement include the following:

– The magnitude of the financial requirements facing retirees during retirement.

– The impact of inflation on retirement.– The effect that financial well-being has on the quality of life.– The planning alternatives that are available for the purpose of

developing a plan that leads to financial self-sufficiency.

Retirement Planning Chapter 29Tools & Techniques of

Financial Planning

Copyright 2009, The National Underwriter Company 5

The Current Environment for Retirees

• 75% of elderly families cannot afford luxury items.

• Pension plans at best replace only about one-half of a person’s salary.

• An employer-sponsored retirement plan and Social Security together almost certainly will not provide adequate funds for maintaining the pre-retirement standard of living during retirement.

Retirement Planning Chapter 29Tools & Techniques of

Financial Planning

Copyright 2009, The National Underwriter Company 6

The Current Environment for Retirees

• Many people will have to deal with deteriorating health during retirement.

– Poor health creates the problem of increased medical bills.

– Increases purchases of services that retirees were once able to perform for themselves (for example, home maintenance).

• Even at what may appear to be low levels, ongoing inflation during the retirement years will erode the purchasing power of the retiree’s income.

Retirement Planning Chapter 29Tools & Techniques of

Financial Planning

Copyright 2009, The National Underwriter Company 7

Determining Financial Needs

• Tripod of Economic Security.

• Employer-Sponsored Plans.

• Crisis in Social Security.

• Combination Concerns.

• Inflation.

• Estimating the Inflation Rate.

• Personalizing the Inflation-Rate Assumption.

Retirement Planning Chapter 29Tools & Techniques of

Financial Planning

Copyright 2009, The National Underwriter Company 8

Factors Affecting Retirement Planning

• Retirement can be as long as one-third of a person’s lifespan.

• Most income is produced in the middle third of one’s life, so building up enough money to sustain a lifestyle for an equal time is a massive task.

• Most people don’t really have any idea what they want to do in retirement, making it difficult to quantify needs.

• Even at low levels, inflation can cause what appeared to be enough money to lose its purchasing power, causing retirement to be a time of anxiety and worry rather than a satisfying time of life.

Retirement Planning Chapter 29Tools & Techniques of

Financial Planning

Copyright 2009, The National Underwriter Company 9

Tripod of Economic Security

Traditionally, economic security in retire-ment was supported by three “legs”:

– Social Security.

– Employer pension plans.

– Personal savings and investment.

Recently, the long-term viability of the Social Security system has come into question, and employer pensions are becoming more rare, leaving the person’s savings the one leg left.

Retirement Planning Chapter 29Tools & Techniques of

Financial Planning

Copyright 2009, The National Underwriter Company 10

Employer-Sponsored Plans

• Not designed to replace all pre-retirement income. Best only replace about one-half.– Integration with Social Security reduces that to 20-25%.– Based on entire career, not the final working years.– Do not provide protection against pre-retirement inflation.

• Profit-sharing plans do not assure that a contribution will be made each year.

• Defined benefit pension plans are being replaced by 401(k) plans that put savings and investment burden on the employee.

• Many employers are terminating all pension and profit sharing plans.

Retirement Planning Chapter 29Tools & Techniques of

Financial Planning

Copyright 2009, The National Underwriter Company 11

Guaranteed Income for Life

• Most defined contribution plans do not guarantee an income for life.

• The responsibility for managing resources becomes the employee’s.

• There are no cost-of-living increases – the employee gets a lump-sum and must do the best he or she can.

• Many people are ill-equipped to manage a portfolio by inclination or education.

Retirement Planning Chapter 29Tools & Techniques of

Financial Planning

Copyright 2009, The National Underwriter Company 12

Crisis in Social Security

• Social Security is meant to be a safety net.

• However, it does not come anywhere near replacing pre-retirement income.

• Many observers question whether Social Security will be able to meet the demands for benefits after the year 2020.

Retirement Planning Chapter 29Tools & Techniques of

Financial Planning

Copyright 2009, The National Underwriter Company 13

Percentage of Pre-retirement Income Provided by Social Security

Retirement Planning Chapter 29Tools & Techniques of

Financial Planning

Copyright 2009, The National Underwriter Company 14

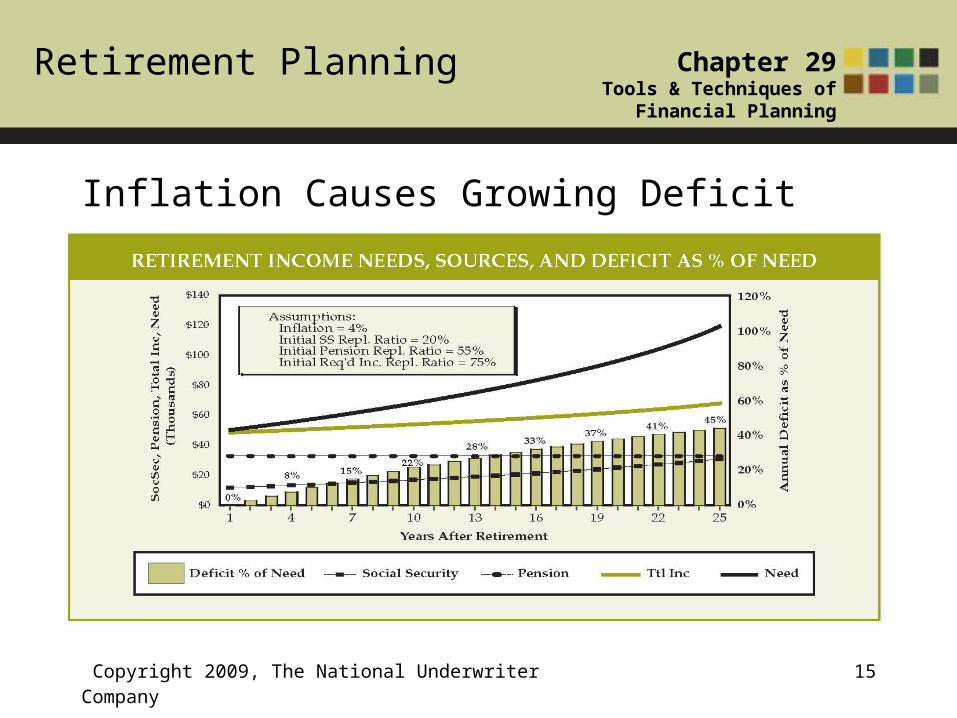

• Biggest threat to economic independence in retirement is inflation.

• As prices go up year by year, the retiree has to draw down more money to have the same amount of purchasing power.

• Even if Social Security keeps pace with inflation, at 4% inflation, in about 10 years, the combination of pension and Social Security will have only about 75% of the purchasing power that it had in the first year.

Retirement Planning Chapter 29Tools & Techniques of

Financial Planning

Copyright 2009, The National Underwriter Company 15

Inflation Causes Growing Deficit

Retirement Planning Chapter 29Tools & Techniques of

Financial Planning

Copyright 2009, The National Underwriter Company 16

Estimating the Inflation Rate

• No one can accurately project future inflation rates. • Over the period from December 1950 to December

1992 inclusive, the average compound increase in prices was 4.2%.

• Since 1992, however, it has been under 3% compounded.

• Many people may be comfortable with projecting a 3%-4% annual increase for long-term estimates of inflation. Others who are more cautious and conservative in their approach may want to choose a higher long-term inflation assumption.

Retirement Planning Chapter 29Tools & Techniques of

Financial Planning

Copyright 2009, The National Underwriter Company 17

Personalizing the Inflation-Rate Assumption

• Retirees typically consume more services than the national average, and services generally have a higher inflation rate than goods.

• There may be regional differences and personal habits that make your clients’ inflation rate different than the national average.

• CPI places great emphasis on housing prices, which may not change for retirees who have completely paid for homes.

• Biggest error as a planner is to underestimate inflation, since that will leave the client with a severe shortfall.

• Focus on long-term rates for your estimates, and do not let one or two years distract you from that reality.

Retirement Planning Chapter 29Tools & Techniques of

Financial Planning

Copyright 2009, The National Underwriter Company 18

Estimating the Length of the Retirement Income Need• Expected Starting Date for Retirement.• Longevity.• Individual Life Expectancies.• Special Consideration for Married Couples.• Second-to-Die Probabilities.• First-to-Die Probabilities.• Planning for Two Separate Income Streams.• Caution is Advised.• The Length of Retirement.• Estimating Retirement Income Needs.

Retirement Planning Chapter 29Tools & Techniques of

Financial Planning

Copyright 2009, The National Underwriter Company 19

Expected Starting Date for Retirement

• Because it was the age to collect full Social Security benefits, age 65 was the age most people used in planning. However, 67 may be more realistic now since that is the Normal Retirement Age under Social Security for individuals born in 1960 and later years.

• However, average age of retirement for American workers is 62. Some of this may have been caused by forced early retirement and some by the fact that one can draw reduced Social Security benefits at that age.

• Long-term commitments such as mortgages or college expenses may force a later retirement age.

Retirement Planning Chapter 29Tools & Techniques of

Financial Planning

Copyright 2009, The National Underwriter Company 20

Longevity

• Predicting how long a person will live is not easy.• If one’s relatives have lived well into their 80’s, then

genetically there could be an expectation that one will also have a long life-span.

• Others, whose relatives died young, may not expect to live that long.

• One of the biggest fears of retired persons is outliving their money.

• Even knowing the average life expectancy, since the proba-bility of a person living beyond the average life expectancy for someone their age is greater than 50%, it is clearly imprudent to base predictions on average life expectancy.

Retirement Planning Chapter 29Tools & Techniques of

Financial Planning

Copyright 2009, The National Underwriter Company 21

Individual Life Expectancies

• Consider John and Judy, age 65 and age 62.• The median age of death, where a person has exactly a 50/50

chance of surviving that long or longer, for them as single persons is 15.7 and 22 years, respectively.

• However, half the people will survive beyond their median ages of death, so it would be unwise to use the median ages of death.

• According to the survival probabilities, John has a 25% chance of surviving almost 22 years to age 86.9 and a 10% chance of surviving almost 27 years to age 91.8. Judy has a 25% chance of surviving almost 28 years to age 90.9 and a 10% chance of surviving about 34 years to age 96.2.

• How much risk can you take that you will run out of income?

Retirement Planning Chapter 29Tools & Techniques of

Financial Planning

Copyright 2009, The National Underwriter Company 22

Single Life Expectancy

Retirement Planning Chapter 29Tools & Techniques of

Financial Planning

Copyright 2009, The National Underwriter Company 23

Special Consideration for Married Couples

• For couples, simply using the longest life expectancy will underestimate the length of time expected until the second spouse dies.

• For a couple both aged 65, the difference is about 4 years.

• Therefore, using second-to-die tables in estimating retirement needwill be more accurate for couples.

Retirement Planning Chapter 29Tools & Techniques of

Financial Planning

Copyright 2009, The National Underwriter Company 24

Retirement Planning Chapter 29Tools & Techniques of

Financial Planning

Copyright 2009, The National Underwriter Company 25

Retirement Planning Chapter 29Tools & Techniques of

Financial Planning

Copyright 2009, The National Underwriter Company 26

Second-to-Die Probabilities & First-to-Die Probabilities• It is rarely a good idea to assume less than 30 years in

retirement for a couple. However, the chance of BOTH living that long is usually fairly small.

• For second to die, the probability is that one of the two will live longer than either of their life expectancies. For first to die, the probability is that one of the two will die sooner than either of their life expectancies.

Retirement Planning Chapter 29Tools & Techniques of

Financial Planning

Copyright 2009, The National Underwriter Company 27

Second-to-Die Probabilities & First-to-Die Probabilities (cont’d)• Thus, the period of time for which one needs to plan

to have sufficient retirement income for two people together is less than the period of time one would need to plan to have that same total income for two people considered separately.

• However, the period of time beyond the first death for which one needs to plan to have the lesser required survivor income is longer than the greater of the two people’s life expectancies.

Retirement Planning Chapter 29Tools & Techniques of

Financial Planning

Copyright 2009, The National Underwriter Company 28

Planning for Two Separate Income Streams

• Typically, one person can live on about two-thirds the income needed for two people.

• When planning for a couple’s retirement funding, you can break the planning into two separate income periods or income streams.

• The first income stream is the amount necessary to meet the survivor-income requirement with the period of need based upon second-death probabilities.

• The second income stream is the additional income (in addition to the survivor-income provided in the first income stream) required to meet the joint-income need with the period of need based upon first-death probabilities.

Retirement Planning Chapter 29Tools & Techniques of

Financial Planning

Copyright 2009, The National Underwriter Company 29

Retirement Planning Chapter 29Tools & Techniques of

Financial Planning

Copyright 2009, The National Underwriter Company 30

Caution is Advised

• Longevity trends have averaged 2% - 6% increase every 10 years for the past five decades.

• This means that using today’s tables for computing retirement needs for people decades away from retirement age could severely understate the need.

• In addition, financial planning clients tend to be better educated, be in better health and be more affluent than average, all factors leading to greater longevity.

• Never forget that average life expectancy tables mean that there is at least a 50-50 chance that the person will live longer than the average age.

Retirement Planning Chapter 29Tools & Techniques of

Financial Planning

Copyright 2009, The National Underwriter Company 31

The Length of Retirement

• Overestimating the length of retirement is less serious than underestimating it.

• No one is going to complain about being better off in retirement than expected, but the fear of running out of money is constant and can be debilitating for the retiree.

• The monitoring of the financial plan over the years will keep the retirement plan on track.

Retirement Planning Chapter 29Tools & Techniques of

Financial Planning

Copyright 2009, The National Underwriter Company 32

Estimating Retirement Income Needs

• Set up a budget as if the person were retiring today. Compute the lump sum needed at retirement, using conservative estimates of longevity, inflation and investment return.

• Project the future value of retirement assets the client already has to retirement age.

• If present assets are sufficient, fine, but if not, compute a savings and investment schedule to meet the need.

• As always, monitor progress toward goals.

Retirement Planning Chapter 29Tools & Techniques of

Financial Planning

Copyright 2009, The National Underwriter Company 33

Obtaining Information on Qualified Plan Benefits

• Annual Benefit of Statements.

• Defined Contribution Type Plans.

• Defined Benefit Plans.

• Vesting.

• Summary Plan Descriptions.

• Tax Forms.

• Plan Administrator.

Retirement Planning Chapter 29Tools & Techniques of

Financial Planning

Copyright 2009, The National Underwriter Company 34

Annual Benefit Statements

• An employee in an ERISA plan must be provided with annual benefit statements, a summary plan description, appropriate tax forms and access to a plan administrator.

• The benefit statement must show the accrued benefits and vesting status.

• It may show projected Social Security benefits, family death benefits, and value of any contributions the employee has made to the plan.

Retirement Planning Chapter 29Tools & Techniques of

Financial Planning

Copyright 2009, The National Underwriter Company 35

Defined Contribution Type Plans

• Benefit consists of accumulated account balance.

• Balance includes contributions by the employer, contributions by the employee and investment earnings, plus in some cases, forfeitures by non-vested employees who have left the plan.

• Value may go down if investment return is negative.

Retirement Planning Chapter 29Tools & Techniques of

Financial Planning

Copyright 2009, The National Underwriter Company 36

Types of Defined Contribution Plans

• Profit-sharing plans.• IRC Section 401(k) plans (also

called cash or deferred plans).• Money-purchase plans.• Employer stock-ownership

plans (generally referred to as ESOPs).

• IRC Section 403(b) plans (also called tax-sheltered annuity plans or tax-deferred annuity plans).

• Simplified employee pension plans (also called SEPs).

• Salary-reduction simplified employee pension plans (also called SARSEPs).

• Stock bonus plans.• Thrift plans.• Savings plans.• Target benefit plans.• Cash balance plans.• SIMPLE IRAs.• SIMPLE 401(k) plans.

Retirement Planning Chapter 29Tools & Techniques of

Financial Planning

Copyright 2009, The National Underwriter Company 37

Defined Benefit Plan

• A defined benefit plan defines the benefit the employee will receive at retirement, usually based on earnings and years of service.

• The benefit may be based on the final salary and the number of years worked for the employer. In these plans, the accrued benefit is the current value of the funds the employee has earned to date that will be used to buy the pension benefit.

• When reading the annual benefit statement:– Note whether the benefit is the current or projected benefit.– Are benefits stated in current or future dollars?

Retirement Planning Chapter 29Tools & Techniques of

Financial Planning

Copyright 2009, The National Underwriter Company 38

Vesting

• To receive a benefit, the plan participant may have to be in the plan for a specified number of years.

• This waiting period is called the “vesting period” and benefits that the employee will receive even if he leaves the company are “vested.”

• There are two kinds of vesting schedules:– Cliff vesting: The employee is not vested at all until a certain

date, then is 100% vested.– Graded vesting: A certain percentage of the employee’s

accrued benefit is vested per year over a period of years. Five year vesting is very common.

Retirement Planning Chapter 29Tools & Techniques of

Financial Planning

Copyright 2009, The National Underwriter Company 39

Summary Plan Descriptions

The summary plan description gives more detail and may include explanations of:

– Early retirement provisions.– Normal retirement age.– Deferred retirement provisions.– Payout options available at retirement.– Potential pitfalls.– Claims procedures.– In addition, the Summary Plan Description will usually

explain how benefits are computed.

Retirement Planning Chapter 29Tools & Techniques of

Financial Planning

Copyright 2009, The National Underwriter Company 40

Tax Forms & Administrator

• Tax Forms– In addition to the annual benefit statement and summary plan

description, employees will also be supplied with a variety of retirement-related federal tax forms. Chief among these is Form 1099R. This form is sent whenever a person receives a lump-sum distribution from the retirement plan or whenever a person is receiving annuity payments or periodic payments.

• Plan Administrator– In addition to all the written information employees receive

about their plans, they also have access to a plan administrator, benefits adviser, or human-resources representative. In some cases, the same person may wear all three hats; in others, a team of experts is available to advise employees.

Retirement Planning Chapter 29Tools & Techniques of

Financial Planning

Copyright 2009, The National Underwriter Company 41

Role of Insurance in Retirement Planning

• Insurance in General.

• Assessing Risks.

• Life Insurance.

• Disability Income.

• Medical Insurance.

Retirement Planning Chapter 29Tools & Techniques of

Financial Planning

Copyright 2009, The National Underwriter Company 42

Insurance in General

• Any wealth accumulation plan assumes a continuation of the ability to earn money and that assets, once acquired, will stay intact.

• One of the major tasks of retirement planning is to assure that risks in the client’s life do not derail their retirement plans.

• Loss of earning power through death or disability or loss of assets through property damage or malfeasance can destroy the best-laid plans.

• Insurance is the method of handling risk most often used for retirement planning.

Retirement Planning Chapter 29Tools & Techniques of

Financial Planning

Copyright 2009, The National Underwriter Company 43

Assessing Risks

• Some risks will be retained because the premium cost to use insurance is great compared to the risk involved.

• Insurance is the best value when the risk is unlikely (meaning a low premium) but the risk could be devastating to the insured.

• For example, it is highly unlikely that the average home-owner is going to face a negligence suit for millions of dollars. However, if he or she did, it would be crushing. So an umbrella policy for $2 million, which is typically only about $250 per year, would be a great buy.

Retirement Planning Chapter 29Tools & Techniques of

Financial Planning

Copyright 2009, The National Underwriter Company 44

Life Insurance

• Life insurance protects a family against the loss of income or increased expenses due to the death of the insured.

• The amount of life insurance needed is the remaining amount in the projected wealth accumulation plan.

Retirement Planning Chapter 29Tools & Techniques of

Financial Planning

Copyright 2009, The National Underwriter Company 45

Disability Income

• A client has a greater chance of suffering a disability than of dying, yet the impact on the wealth accumulation plan might even be worse with the medical expenses needed to treat the disability.

• Disability income insurance can replace the income from a job or keep a business afloat during the disability of the client.

• Since an elimination period of 90 days or more will cost much less than a shorter period, the financial planner must assure that the client keeps an emergency fund of 3 to 6 months living expenses.

Retirement Planning Chapter 29Tools & Techniques of

Financial Planning

Copyright 2009, The National Underwriter Company 46

Medical Insurance

• Medical costs have spiraled up much faster than have other costs in the economy.

• An unexpected illness or accident could costhundreds of thousands of dollars in medical bills.

• Although most medical insurance is obtained through the employer, self-employed clients will need assistance in obtaining medical insurance at a reasonable price.

• The most reasonably priced medical insurance isthe HMO, however, there are a number of other variations of medical insurance. Employees rarely have much choice: Self-employed can make the decision of what kind of insurance they want. Choosing a high-deductible plan can provide insurance against devastating loss with a lower premium cost.

Retirement Planning Chapter 29Tools & Techniques of

Financial Planning

Copyright 2009, The National Underwriter Company 47

Retirement Plan Distribution Planning

• What options does the plan provide?• Defined Benefit Plan Distribution Provisions.• Tax Implications.• Nontaxable and Taxable Amounts.• Taxation of Annuity Payment.• Lump Sum Distributions.• Taxation of Death Benefits.• Federal Estate Tax on Distributions.• Lump Sum vs. Deferred Payments: The Tradeoff.• Penalty Taxes.• Penalty for Distributions too soon.• Penalty for Distributions too late or not enough.

Retirement Planning Chapter 29Tools & Techniques of

Financial Planning

Copyright 2009, The National Underwriter Company 48

What Options does the Plan Provide?

• Found in Summary Plan Description.

• Some plans may have several choices on distributions, while others may only allow a lump sum.

Retirement Planning Chapter 29Tools & Techniques of

Financial Planning

Copyright 2009, The National Underwriter Company 49

Defined Benefit Plan Distribution Provisions

• Must provide a joint and survivor annuity.

• For single participant, benefit is usually a life annuity.

• Any option that the plan offers that eliminates the participant’s spouse must be agreed to in writing by the spouse.

• Other common options are a period certain annuity or a lump sum distribution.

Retirement Planning Chapter 29Tools & Techniques of

Financial Planning

Copyright 2009, The National Underwriter Company 50

Defined Contribution Plan Distribution Provisions

• Sometimes will provide annuity benefits, but most often offer lump sum.

• Sometimes the employee can just take withdrawals as needed.

• If an annuity option is desired, but not offered by the plan, the employee can always roll the lump sum distribution over to an IRA at a life insurance company and take it in the form of an annuity.

• Lump sums can also be rolled over into IRAs at investment firms, mutual fund companies or banks.

Retirement Planning Chapter 29Tools & Techniques of

Financial Planning

Copyright 2009, The National Underwriter Company 51

Tax Implications

• Some participants just want the highest income possible in retirement, and do not want to think about taxes.

• The planner must consider:1. the direct income tax on the lump sum or periodic distribution.2. penalty taxes.3. estate taxes.4. generation skipping transfer taxes.

• A qualified plan distribution may be subject to federal, state, and local taxes, in whole or in part.

• This section will focus only on the federal tax treatment. Federal tax is usually higher than state or local and many states exempt retirement distributions.

Retirement Planning Chapter 29Tools & Techniques of

Financial Planning

Copyright 2009, The National Underwriter Company 52

Nontaxable and Taxable Amounts

• While the bulk of most retirement plan distributions will be taxed as ordinary income, some will include a tax-free return of the employee’s own money.

• If an annuity is taken, payments will be proportionally taxable and tax-free according to the ratio of the employee’s cost basis in the plan.

• An exception for after-tax contributions made prior to 1987 for certain plans is that those will be treated as non-taxable until the entire pre-1987 contribution has been recovered.

Retirement Planning Chapter 29Tools & Techniques of

Financial Planning

Copyright 2009, The National Underwriter Company 53

Determining Tax on a Distribution

• The first step is to determine the participant’s cost basis in the plan benefit. The participant’s cost basis can include:1. The total after-tax contributions made by the employee to a

contributory plan.2. The total cost of life insurance reported as taxable income by

the participant if the plan distribution is received under the same contract that provided the life insurance protection.

3. Any employer contributions previously taxed to the employee – for example, where a nonqualified plan later becomes qualified.

4. Certain employer contributions attributable to foreign services performed before 1963.

5. Amounts paid by the employee in repayment of loans that were treated as distributions.

Retirement Planning Chapter 29Tools & Techniques of

Financial Planning

Copyright 2009, The National Underwriter Company 54

Taxation of Annuity Payments

• The annuity rules of IRC Section 72 apply to periodic plan distributions made over more than one taxable year of the employee in a systematic liquidation of the participant’s benefit.

• Amounts distributed are taxable in the year received, except for a proportionate recovery of the cost basis.

• The method used for recovery of the cost basis depends on the participant’s annuity starting date.

Retirement Planning Chapter 29Tools & Techniques of

Financial Planning

Copyright 2009, The National Underwriter Company 55

Taxation of Annuity Payments

If the annuity starting date is after December 31, 1997 and the annuity is payable over two or more lives, the excludable portion of each monthly payment is determined by dividing the employee’s cost basis by the number of payments shown in the table below:

If the combined ages Number ofOf the annuitants are: PaymentsNot more than 110 410More than 110 but not more than 120 360More than 120 but not more than 130 310More than 130 but not more than 140 260More than 140 210

Retirement Planning Chapter 29Tools & Techniques of

Financial Planning

Copyright 2009, The National Underwriter Company 56

Taxation of Annuity Payments

If (a) the annuity starting date was after November 18, 1996 and before January 1, 1998 and the annuity is payable over two or more lives, or (b) the annuity starting date is after November 18, 1996 and the annuity is payable over one life, the excludable portion of each monthly payment is determined by dividing the employee’s cost basis by the number of payments shown in the table below:

Number ofAge PaymentsNot more than 55 360More than 55 but not more than 60 310More than 60 but not more than 65 260More than 65 but not more than 70 210More than 70 160

Retirement Planning Chapter 29Tools & Techniques of

Financial Planning

Copyright 2009, The National Underwriter Company 57

Lump Sum Distributions

• A lump sum distribution may be desirable for retirement planning purposes, but the distribution may be large enough to push most of it into the highest tax bracket.

• In determining the tax on a lump sum distribution, the first step is to calculate the taxable amount of the distribution.

• The taxable amount consists of (a) the total value of the distribution less (b) after-tax contributions and other items constituting the employee’s cost basis.

• If employer securities are included in the distribution, the net unrealized appreciation of the stock is generally subtracted from the value of a lump sum distribution.

Retirement Planning Chapter 29Tools & Techniques of

Financial Planning

Copyright 2009, The National Underwriter Company 58

Taxation of Death Benefits

• In general, the income tax treatment that applies to death benefits paid to beneficiaries is very similar to that of lifetime benefits payable to participants; however, more favorable treatment applies to spouse beneficiaries than to other beneficiaries.

• Either the annuity rules or the lump sum special tax provisions may be available to the beneficiary receiving a death benefit.

• However, an additional income tax benefit is available, in that if the death benefit is payable under a life insurance contract held by the qualified plan, the pure insurance amount of the death benefit (Total life insurance benefit – Cash Value) is excludable from income taxation.

Retirement Planning Chapter 29Tools & Techniques of

Financial Planning

Copyright 2009, The National Underwriter Company 59

Federal Estate Tax on Distributions

• Generally, the value of a death benefit payable from a retirement plan is includable in the estate of participant.

• There have been attempts to manipulate “incidents of ownership” in such a way as to keep from playing estate tax by using life insurance.

Retirement Planning Chapter 29Tools & Techniques of

Financial Planning

Copyright 2009, The National Underwriter Company 60

Lump Sum vs. Deferred Payments : The Tradeoff

• Advantages of a lump sum distribution include– The ability to roll over certain distributions.– 10-year averaging tax treatment (limited to certain distributions

to individuals who reached age 50 before 1986).– freedom to invest plan proceeds at the participant’s – not the

plan administrator’s – discretion.• The contrasting advantages of a deferred payout are:

– deferral of taxes until money is actually distributed (however, such deferral can also be obtained in the case of a rollover).

– continued sheltering of income on the plan account from taxes while money remains in the plan.

– security of retirement income.

Retirement Planning Chapter 29Tools & Techniques of

Financial Planning

Copyright 2009, The National Underwriter Company 61

Penalty Taxes for Taking Distributions Too SoonEarly distributions from qualified plans, 403(b) tax-deferred annuity plans, IRAs and SEPs are subject to a penalty of 10% of the taxable amount of the distribution, except for distributions:

– Made on or after age 59½.– Made to the plan participant’s beneficiary or estate on or after

the participant’s death.– Attributable to the participant’s disability.– That are part of a series of substantially equal periodic

payments made at least annually over the life or life expectancy of the participant, or of the participant and beneficiary (separa-tion from the employer’s service is required, except for IRAs).

Retirement Planning Chapter 29Tools & Techniques of

Financial Planning

Copyright 2009, The National Underwriter Company 62

– Made following separation from service after attainment of age 55 (not applicable to IRAs).

– That are certain tax credit ESOP dividend payments, or– To the extent of medical expenses deductible for the year

under Code Section 213, whether or not actually deducted.– In addition, certain distributions made from IRAs for the

payment of health insurance premiums by unemployed individuals, and certain distributions used for higher education expenses or first-time home purchases may be exempt from the penalty.

Penalty Taxes for Taking Distributions Too Soon (cont’d)

Retirement Planning Chapter 29Tools & Techniques of

Financial Planning

Copyright 2009, The National Underwriter Company 63

Penalty for Distributions Too Late or Not Enough• Distributions from qualified plans, 403(b) tax-deferred

annuity plans, IRAs, SEPs, and 457 governmental deferred compensation plans must begin by April 1 of the calendar year after the participant attains age 70½.

• There is an annual minimum distribution required; if distribution is less than the minimum, the penalty is 50% of the amount that should have been distributed but was not.

Retirement Planning Chapter 29Tools & Techniques of

Financial Planning

Copyright 2009, The National Underwriter Company 64

Penalty for Distributions Too Late or Not Enough (cont’d)• The minimum distribution is determined by dividing the

participant’s account balance (generally as of December 31 of the preceding year) by the participant’s life expectancy, determined under a “Uniform Lifetime Table.” set forth in regulations.

• Following the death of the participant, the remaining benefit may generally be distributed over the life expectancy of the beneficiary, determined under tables set forth in the regulations.