Retirement is just the beginning The Best of America ® America’s INCOME Annuity ® IAM-0160AO...

21

Retirement is just the beginning The Best of America ® America’s INCOME Annuity ® IAM-0160AO (6/05) • Not a deposit • Not FDIC or NCUSIF insured • Not guaranteed by the institution • Not insured by any federal government agency • May lose value

-

Upload

caitlyn-daniel -

Category

Documents

-

view

214 -

download

1

Transcript of Retirement is just the beginning The Best of America ® America’s INCOME Annuity ® IAM-0160AO...

Retirement is just the beginning

The Best of America® America’s INCOME Annuity®

IAM-0160AO (6/05)

• Not a deposit • Not FDIC or NCUSIF insured • Not guaranteed by the institution• Not insured by any federal government agency • May lose value

Are you ready for what comes next?

IAM-0160AO (6/05)

Agenda

• Potential retirement pitfalls

– Retirement income sources

– Longevity risk

– Inflation risk

– Asset allocation risk

• Immediate variable annuities

• The Best of America® America’s INCOME Annuity®

• America’s INCOME Annuity Income FoundationSM

• Conclusion and next steps

IAM-0160AO (6/05)

Where will your retirement income come from?

Most people need approximately 70% of their current income to maintain their current standard of living in retirement

Most people need approximately 70% of their current income to maintain their current standard of living in retirement

Other 3%

Social Security39%

Pensions19%

Part-timework25%

Personal savings14%

Source: Income of the Aged Chartbook 2002, SSA Publication No. 13-11727, Social Security Administration (September 2004).

Potential retirement pitfalls: Income sources

IAM-0160AO (6/05)

Will your money last as long as you do?

Age Male Female Joint*70 93.9% 96.3% 99.8%

75 84.4% 90.3% 98.5%

80 70.7% 80.6% 94.3%

85 53.0% 65.3% 83.7%

90 33.5% 44.5% 63.0%

95 16.5% 23.0% 35.7%

100 5.9% 8.6% 14.0%

Probability of a 65-year-old living to age1:

*Probability that either husband or wife will reach that age. 1Based on individual annuity mortality rates from the Society of Actuaries Annuity 2000 Mortality table.

Potential retirement pitfalls: Longevity risk

IAM-0160AO (6/05)

Potential retirement pitfalls: Inflation risk

How will you be affected by inflation?

1990 2002

$122,900

$14,371

$187,600

$21,440

1Statistical Abstracts of the United States: 2003, U.S. Census Bureau (February 2004).

Average price increase over a 12-year period1

IAM-0160AO (6/05)

Potential retirement pitfalls: Asset allocation risk

Source: T. Rowe Price Form No. 05515-268 (June 2005).

Assumes a starting balance of $500,000 and an initial withdrawal rate of 7.89% increased by 3% each year for inflation. Withdrawals are made at the start of each year. Taxes and fees on any investments, and required minimum distributions for tax-deferred assets, are not considered in this illustration. For the years 1976–2004, portfolio performance is based on historical returns of a portfolio composed of 40% Standard and Poor’s 500 Stock Index (“S&P 500 Index”), 40% Lehman Brothers U.S. Aggregate Index, and 20% Lehman Brothers 1–3 Year Government Bond Index and a portfolio of 20% S&P 500 Index, 50% Lehman Brothers U.S. Aggregate Index, and 30% Lehman Brothers 1–3 Year Government Bond Index. For the year 1975, the intermediate-term bond performance is based on the Lehman Brothers Government/Credit Index, and the short-term bond performance is based on the U.S. 30-day Treasury bill. The S&P 500 Index tracks the stocks of 500 U.S. companies. Charts are shown for illustrative purposes only and are not intended to represent the performance of any specific security. Past performance cannot guarantee future results. Source: T. Rowe Price Associates. *The following allocations include short-term bonds: 40/60 is 40% stocks, 40% bonds, and 20% short-term bonds; and 20/80 is 20% stocks, 50% bonds, and 30% short-term bonds.

IAM-0160AO (6/05)

Immediate variable annuities

• Products that provide a guaranteed lifetime income, offering security and the ability to maintain your lifestyle

• The Best of America® America’s INCOME Annuity® an immediate variable annuity

IAM-0160AO (6/05)

Immediate variable annuities

• Long-term investment designed for retirement purposes

• Converts your retirement investment (like a 401k) into immediate income payments

• An insurance contract bought with a lump-sum payment

• Provides income payments that last for life or a specific number of years, guaranteed (subject to the claims-paying ability of the issuing insurance company)

• Payments increase or decrease based on market performance and asset allocation

IAM-0160AO (6/05)

Both the product prospectus and underlying subaccount prospectuses can be obtained from your investment professional or by writing to:

Nationwide Life Insurance CompanyP.O. Box 182021Columbus, OH 43218-2021

Before investing, carefully consider the subaccounts’ investment objectives, risks, charges and expenses. The product prospectus and underlying subaccount prospectuses contain this and other important information. Read the prospectus carefully before investing.

Immediate variable annuities are sold by prospectus.

Immediate variable annuities: Obtaining a prospectus

IAM-0160AO (6/05)

Immediate variable annuities

Keep in mind that this presentation is based on current interpretations of the law, neither the company nor its representatives give legal or tax advice.

IAM-0160AO (6/05)

• Receive guaranteed income payments to supplement other income sources

• Make minimum required distributions from traditional retirement plans, such as IRAs

• Avoid 10% IRS tax penalty for withdrawals made prior to age 59 ½ (only available with specific payment options; please consult your legal or tax advisor for details)

• Leave a legacy by utilizing wealth transfer strategies, funding a trust or contributing to a charity

• All annuities have limitations and investing involves risk, including possible loss of principal

• Guarantees are subject to the claims-paying ability of the issuing insurance company

– Depending on the payment option you choose, how long the annuitant lives and the performance of your investment options, you may get back less than you invested

• Underlying investment options are only available with variable annuity or life insurance products; they are not made directly available to the general public

• Early withdrawals from an annuity:

– May be subject to surrender charges and/or may incur a 10% tax penalty if taken prior to age 59½

– Will be subject to income taxes and will reduce the death benefit and contract value proportionately

Immediate variable annuities: Details to keep in mind

IAM-0160AO (6/05)

The Best of America® America’s INCOME Annuity®

• Variable and fixed investment options– These are only available as investment options in variable annuities or

variable life insurance products; they are not offered directly to the general public

• Multiple payment options – Many include a death benefit – The Single Life With Cash Refund option offers a return of principal

guarantee, less any applicable premium taxes

• Access to assets in case of emergency– May be subject to a surrender charge and may not be available in all states– Subject to income tax and, if taken before age 59½, may be subject to 10%

tax penalty– Will reduce any remaining payments in the term-certain period and will

reduce the death benefit, the living benefit or the cash surrender value

• Cost: 1.25%*(daily net assets in the variable account)

IAM-0160AO (6/05)

America’s INCOME Annuity Income FoundationSM Rider

With you every step of the way

America’s INCOME Annuity Income FoundationSM (AIA Income Foundation) Rider

• Potential — Growth potential and inflation protection

• Confidence — A long-term strategy that protects against loss of income

• Flexibility — Choice of Step-up Guarantee or Level Guarantee

IAM-0160AO (6/05)

America’s INCOME Annuity Income FoundationSM Rider

How does it work?

• Variable annuity payments are calculated according to the chosen income option and payment frequency and these payments fluctuate with market performance

• If the AIA Income Foundation rider is elected, you will receive a guarantee that when market declines cause your variable annuity payment amount to fall below the guaranteed floor amount, Nationwide® will make up the difference so that you will receive a guaranteed payment, regardless of poor market performance

• You can choose between two floor guarantee options, either the patent-pending Step-up Guarantee or the Level Guarantee option

IAM-0160AO (6/05)

Step-up Guarantee Option

Guarantees are subject to the claims-paying ability of Nationwide Life Insurance Company and will be reduced if the contract owner incurs a redemption fee, makes a variable-to-fixed transfer or takes an unscheduled withdrawal.

• The guaranteed variable payment amount will be equal to 75% of the first variable annuity payment calculated on the contract issue date

• On each income-start-date anniversary, your guaranteed variable annuity payment amount may increase, if 75% of the calculated variable annuity payment is greater than the previously guaranteed variable annuity payment amount

America’s INCOME Annuity Income FoundationSM Rider

IAM-0160AO (6/05)

Level Guarantee Option

• The guaranteed variable payment amount will be equal to 85% of the first variable annuity payment calculated on the contract issue date

• Once the guaranteed variable annuity amount is established it will not increase during life of the contract

Guarantees are subject to the claims-paying ability of Nationwide Life Insurance Company and will be reduced if the contract owner incurs a redemption fee, makes a variable-to-fixed transfer or takes an unscheduled withdrawal.

America’s INCOME Annuity Income FoundationSM Rider

IAM-0160AO (6/05)

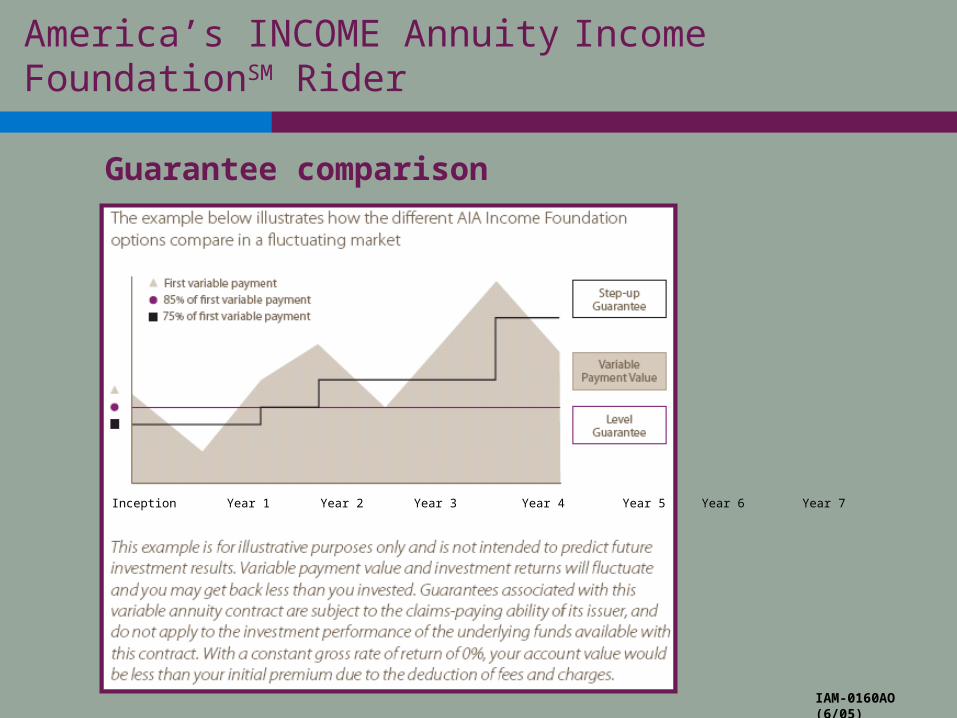

Guarantee comparison

America’s INCOME Annuity Income FoundationSM Rider

IAM-0160AO (6/05)

Inception Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7

On a finer note…

• The additional cost for this feature is 1.00% of the daily net assets of the variable account

• Guarantees associated with this rider are subject to the claims-paying ability of Nationwide Life Insurance Company

• Not all underlying investment options available at the contract level are available with this rider

• This rider is irrevocable and may not be available in all states

• A 3.0% assumed investment return (AIR) must be selected– This will result in a lower initial payment then the other

available AIRs

• Term-certain payment options of less then 10 years aren’t available

America’s INCOME Annuity Income FoundationSM Rider

IAM-0160AO (6/05)

Conclusion

IAM-0160AO (6/05)

• Potential retirement pitfalls– Retirement income sources

– Longevity risk

– Inflation risk

– Asset allocation risk

• Immediate variable annuities

• The Best of America® America’s INCOME Annuity®

• America’s INCOME Annuity Income FoundationSM

• Questions

Next Steps

For additional information or a personalized plan, please meet with your investment professional or logon to nationwidefinancial.com.

All individuals selling these products must be insurance-licensed registered representatives.

The Best of America® America’s Income Annuity® is issued by Nationwide Life Insurance Company, Columbus, Ohio; the general distributor of these products is Nationwide Investment Services, member NASD; in Michigan only: Nationwide Investment Svcs. Corporation.

Nationwide and the Nationwide Framemark are federally registered service marks of Nationwide Mutual Insurance Company. The Best of America and America’s INCOME Annuity are federally registered service marks of Nationwide Life Insurance Company. America’s INCOME Annuity Income Foundation is a service mark of Nationwide Life Insurance Company. On Your Side is a service mark of Nationwide Life Insurance Company.

Contracts/Riders: IAC-0100AO, IAC-0100OR, IAC-0100TX, IAR-0100AO, IAR-0100OR, IAR-0100TX; In Oklahoma: IAC-0100OK, IAR-0100AO

© 2005, Nationwide Financial Services, Inc. All rights reserved.

IAM-0160AO (6/05)