Ensuring Customer Satisfaction in Banking Sector through ...

8/6/2019 Retial Banking-customer Satisfaction

http://slidepdf.com/reader/full/retial-banking-customer-satisfaction 1/19

Relational benefits and customersatisfaction in retail banking

Arturo Molina Department of Marketing, University of Castilla-La Mancha,

Cobertizo San Pedro Ma rtir, Toledo, Spain

David Martın-Consuegra Department of Marketing, University of Castilla-La Mancha, Ronda de Toledo,

Ciudad Real, Spain, and

Agueda Esteban Department of Marketing, University of Castilla-La Mancha,

Cobertizo San Pedro Ma rtir, Toledo, Spain

Abstract

Purpose – The purpose of this paper is to investigate the impact of relational benefits on customersatisfaction in retail banking. This paper presents a causal model that identifies a connection betweenthe relational benefits achieved through a stable and long-term relationship with a given bank andcustomer satisfaction with retail banking.

Design/methodology/approach – Based on a theoretical framework regarding the relationshipbetween relational benefits and customer satisfaction, an empirical study using a sample of 204 bankcustomers was conducted, and the theoretical model is tested. Multi-item indicators from prior studieswere employed to measure the constructs of interest, and the proposed relationships were tested usingstructural equations modeling methods.

Findings – The results show that confidence benefits have a direct, positive effect on the satisfactionof customers with their bank. However, special treatment benefits and social benefits did not have any

significant effects on satisfaction in a retail banking environment.Research limitations/implications – This study was conducted in a retail banking setting, andmay not be generalized in other service sectors. It has also focused on the relationship betweenrelational benefits and satisfaction, while other factors that may have an influence on consumersatisfaction have not been considered.

Practical implications – The findings suggest that banks can create customer satisfaction throughrelational strategies that focus on building customer confidence. Therefore, frontline employees shouldbe committed to establishing and maintaining confidence benefits for customers.

Originality/value – Interest in the subjects of relational benefits and customer satisfaction has beengrowing among marketing researchers and practitioners. The present study provides usefulinformation on the relationship between customer satisfaction and specific relational benefits in retailbanking.

Keywords Customer satisfaction, Banking, Relationship marketing, Spain

Paper type Research paper

IntroductionMany innovations have recently modified the concept of retail banking, due to newforms of commercialization and distribution of financial services, as well as to theevolution of twenty-first century consumers (Verhoef et al., 2002; Sweeney andMorrison, 2004).

The current issue and full text archive of this journal is available at

www.emeraldinsight.com/0265-2323.htm

Customersatisfaction inretail banking

253

International Journal of Bank

Marketing

Vol. 25 No. 4, 2007

pp. 253-271

q Emerald Group Publishing Limited

0265-2323

DOI 10.1108/02652320710754033

8/6/2019 Retial Banking-customer Satisfaction

http://slidepdf.com/reader/full/retial-banking-customer-satisfaction 2/19

The importance of this study is based on relationship marketing, service qualityand consumer satisfaction as key elements for the success of financial businessesfacing increasing competition and recent market changes. Although past studiesprovide knowledge regarding the nature and importance of banking relationships from

a customer viewpoint (O’Loughlin et al., 2004), some questions remain unanswered.Nowadays, most financial service providers trust that a conscientious customer servicewill be more important for consumer satisfaction than lower prices in those activitieswhere there is a direct rapport between companies and consumers in particular.

The marketing literature has recognized the importance of developing andmaintaining enduring relationships with customers of service businesses(Henning-Thurau et al., 2002). Also, a review of literature has revealed that studiesfocusing on relationship marketing, service and satisfaction already exist (e.g. Oliver,1981; Gronroos, 1990; Berry, 1995; Bitner, 1995; Bejou et al., 1998; Gwinner et al., 1998;Mittal et al., 1999; Henning-Thurau et al., 2002; Jamal and Naser, 2002; Aldlaigan andButtle, 2005; Pont and McQuilken, 2005; Leverin and Liljander, 2006). Nevertheless,there is a significant lack of practical and empirical works analyzing the actualconsequences for individual consumers of maintaining long-term relationships withservice providers. In addition, a review of the literature has also shown that there areonly a few studies which have dealt with business efforts to establish stable andlong-lasting relationships with consumers, as well as with the connection betweenrelational benefits and customer satisfaction which regular customers enjoy.Furthermore, while Gwinner et al. (1998) call for causal research in the area of relational benefits and in different contexts, there are but few empirical studies in retailbanking (Colgate et al., 2005; Martın-Consuegra et al., 2006). It is also remarkable thatthere is no research on the relationship between relational benefits and customersatisfaction in retail banking.

For these reasons, the central goals of this research are to empirically identify the

relational benefits customers receive as a result of engaging in long-term relationalexchanges with banks, to define the main components of satisfaction and to determinewhat is the relationship between relational benefits and satisfaction in retail banking.As a consequence, this paper describes the relationship between the two conceptsmentioned above: satisfaction and relational benefits. To be more precise, the purposeof this article is to integrate the lines of research on relational benefits and satisfactionin retail banking, the latter of which is conceived as a mediator between these relationalbenefits and the main relationship marketing outcomes. To be precise, a path model isproposed and tested. In order to do this, a previous analysis of the features of relationship marketing and satisfaction as fundamental factors in financial servicesexchanges is needed. In order to better understand the factors affecting the relationshipbetween relationship marketing and satisfaction, this research has analyzed it in a

concrete consumer sample. The relationship proposed has been tested applying amultivariate analysis, as indicated by the review of the literature on retail banking,relationship marketing and satisfaction.

Literature review Relational benefitsThe concept of relationship marketing has emerged within the field of servicesmarketing and industrial marketing in the last years of the twentieth century. One of

IJBM25,4

254

8/6/2019 Retial Banking-customer Satisfaction

http://slidepdf.com/reader/full/retial-banking-customer-satisfaction 3/19

the most important contributions was Hunt’s (1993) proposal, which established thatthe fundamental element in marketing is the management of interactions, although adecade earlier Berry (1983) had already proposed a formal definition of relationshipmarketing as a strategy to attract, maintain and enhance customer relationships.

According to this approach, organizations should be more interested in keeping stablerelationships with their customers than in accumulating occasional exchanges (Beattyet al., 1996). In addition, other research pointed out that companies can gain benefits bykeeping long-term customer relationships due to increased satisfaction (Parasuramanet al., 1991; Shani and Chalasani, 1992; Zeithaml et al., 1993).

Relationship marketing nowadays is in a leading position in many companystrategic plans, as well as in many marketing research areas, as a consequence of thetotal redefinition of the function of marketing, which many authors agree inconsidering as the superseding of the transactional paradigm. Nevertheless, there arefew empirical works which have explored the motivations and benefits consumers getfrom keeping a long-term relationship with a specific service provider (Sheth andParvatiyar, 1995; Bendapudi and Berry, 1997; Gwinner et al., 1998; Reynolds andBeatty, 1999; Henning-Thurau et al., 2002), even though it is obvious that, in practice,such benefits are interpreted as advantages by consumers and their analysis mayrender more efficient competitive strategies.

In recent decades, research into relationship marketing mainly concentrated on theanalysis of benefits gained by customer loyalty from the point of view of serviceproviders, and, in general, in the context of the relationships among companies. Thisline of work produced a group of studies which examine the benefits obtained byproviders who have developed a collection of loyal customers through relationshipmarketing. However, the revision of the literature on service marketing has facilitatedthe identification and characterization of the diverse relational advantages consumersobtain by being loyal to their providers, thus allowing for a classification of benefits

into three groups: confidence benefits, social benefits, and special treatment benefits(Henning-Thurau et al., 2002).

In relation to this in particular, Bendapudi and Berry (1997) suggest four factors(antecedents) that affect consumer receptivity when deciding whether to maintain theconnection with habitual providers: environmental, partner, customer, and interaction.The effects of these antecedent variables on constraint-based relationship maintenanceare mediated by dependence on the relationship partner. Dependence and trust in therelationship partner mediate the antecedent variables’ effects on dedication basedrelationship maintenance. In order to facilitate the application of these factors toservice companies, Berry (1983) delineates the five strategic elements that relationshipmarketing is based on: to develop a central element around which the stablerelationship with the customer is constructed, to personalize the relationship, to

increase the central element by offering extra benefits, to augment loyalty to theprovider through price fixation, and to make employees aware that they areimmediately responsible in front of customers. Moreover, the use of relationshipmarketing in retail banking activities may have some advantages, for instance:increased consumer loyalty, benefits for consumers as well as improved promotion of complementary services.

Following this line, Gwinner et al. (1998) point out that motivated consumers whomaintain long-term relationships with their providers expect not only to receive good

Customersatisfaction inretail banking

255

8/6/2019 Retial Banking-customer Satisfaction

http://slidepdf.com/reader/full/retial-banking-customer-satisfaction 4/19

service, but also additional benefits from maintaining that relationship (social benefits,confidence and special treatment). Academic literature terms these “relational benefits”(Bendapudi and Berry, 1997; Dwyer et al., 1997; Reynolds and Beatty, 1999). Gwinneret al. (1998) define them as those benefits customers are likely to receive as a result of

engaging in long-term relationships with a service provider. Special treatment benefitsconsist of an extensive range of benefits or economic advantages which come in theform of first-rate levels of service, preferential treatment, special operation conditionsand time saving. These types of benefits are the principal motivation for the customerto develop a long term relations with the service provider. Confidence benefits describea detailed combination of psychological benefits in relation to: trust in the marketer,reduction in perceived operation risks and a decrease in anxiety. Finally, social benefitsare defined by benefits of a social nature which adopt the form of personal recognitionby employees in direct dealings, or the forging of links and social relationships, whichare gratifying for the customer. These types of benefits are especially relevant in thoseservice banks where a high level of interpersonal contact exists between customers andemployees. The influence of these benefits causes the customer to manifest his/herloyalty more to the employee who provides the service rather than to the financialentity in itself. In addition, Beatty et al. (1996) affirmed that these benefits received byconsumers can be classified in two main categories: functional and social benefits.Functional benefits include confidence and special treatment benefits and socialbenefits consist of the Gwinner et al. (1998) social benefits.

Three elements increase relational benefits in the relationship between consumersand service providers: relationship with the trademark, interpersonal relationships,and company relationships (San Martin, 2005). First, consumers expect specifictrademark characteristics (trust) and project their feelings onto the trademark (loyalty).Second, in interpersonal relationships, it is important to consider the affective oremotional component, which may create influential variables such as trust and

commitment. Finally, the level of relationships with the company is less intense. It isparticularly difficult, for instance, to separate the different relationship levels in thecase of financial businesses, because the establishment, the staff, and the services ortrademarks are all integrated into one unit.

Relationship marketing outcomesIt is at any rate remarkable that, in recent years, relationship marketing activities arepreferably evaluated in relation to business profitability. However, as businessprofitability may be influenced by many other variables, it seems more appropriate todefine the concept of relationship marketing more specifically when attempting athorough approach. At least two key elements stand out in the literature of relationshipmarketing: customer loyalty and word-of-mouth (Henning-Thurau et al., 2002; Wong

and Zhou, 2006). Loyalty concerns itself with purchase reiteration behavior and isactivated by company marketing activities. Loyalty is one of the primary phases of relationship marketing and much research has focused on this concept, especially inrelation to profitability from a theoretical and empirical approach (Reichheld and EarlSasser, 1990; Payne and Rickard, 1997; Oliver, 1999). Positive word-of-mouthcommunication, defined as all informal communications between a customer andothers concerning evaluations of goods or services, includes “relating pleasant, vivid,or novel experiences; recommendations to others; and even conspicuous display”

IJBM25,4

256

8/6/2019 Retial Banking-customer Satisfaction

http://slidepdf.com/reader/full/retial-banking-customer-satisfaction 5/19

(Anderson, 1998). Word-of-mouth communication is a powerful force in influencingfuture buying decisions, particularly when the service delivered is of high risk for thecustomer; and it helps to attract new customers as relational partners to a company’sofferings. Attracting new customers has been interpreted as part of the relationship

marketing concept by many proponents (Berry, 1983; Gronroos, 1990; Morgan andHunt, 1994).

For that reason, a key challenge is to identify and understand how manageriallycontrolled antecedent variables influence relationship marketing outcomes. In thissense, Henning-Thurau et al. (2002) propose satisfaction as a mediator in therelationship between relational benefits and the two outcomes mentioned above(customer loyalty and word-of-mouth). Consumer satisfaction is a central element inthe marketing exchange process, because it undoubtedly contributes to serviceproviders’ success (Darian et al., 2001). Furthermore, satisfaction is one of the essentialfactors to predict consumer behavior and, more specifically, purchase repetition. Themore consumers fulfill their expectations during the purchase or service use, the higherthe probability that consumers will repeat purchase establishment (Wong and Sohal,2003). So, customer satisfaction is an essential factor in order to acquire loyalcustomers who would also recommend their regular establishment to other customers.The recognition that there are positive (although not perfect) links between satisfactionin general, relationship satisfaction in particular and loyalty and word-of-mouth andrepurchase highlight the importance of identifying and explaining the conditionsunder which satisfaction develops (Bejou et al., 1998). While the concept of customersatisfaction consists of many factors, relational benefits may be the most directlyinfluential.

Customer satisfactionDuring the last four decades, satisfaction has been considered as one of the most

important theoretical as well as practical issues for most marketers and customerresearchers (Jamal, 2004). However, no single definition of satisfaction has beenunanimously accepted by literature related to the matter. All definitions proposed,however, agree that the concept of satisfaction implies the necessary presence of a goalthe consumer wants to achieve. According to Homburg et al. (2006), previous researchhas recognized that both cognition (Oliver, 1980; Bearden and Teel, 1983; LaBarberaand Mazursky, 1983; Oliver and DeSarbo, 1988) and affect (Westbrook, 1987;Westbrook and Oliver, 1991; Mano and Oliver, 1993) significantly predict satisfaction

judgments.On one hand, within literature on services marketing, satisfaction has traditionally

been defined as a cognitive-based phenomenon (Westbrook, 1987). Cognition has beenstudied mainly in terms of the expectations/disconfirmation paradigm; also known as

the confirmation/disconfirmation paradigm, which states that expectations originatefrom the customer’s beliefs about the level of performance that a product/service wouldprovide (Oliver, 1980). Also, various models and theories that have been developed tothis end (Oliver, 1980; Swan and Trawick, 1980; Tse and Wilton, 1988; Anderson andSullivan, 1993; Patterson et al., 1997), indicate that customer satisfaction is related tothe size and direction of disconfirmation, which is defined as the difference between thepost-purchase and post-usage evaluation of the performance of the product/service andthe expectations held prior to the purchase (Sharma and Ojha, 2004).

Customersatisfaction inretail banking

257

8/6/2019 Retial Banking-customer Satisfaction

http://slidepdf.com/reader/full/retial-banking-customer-satisfaction 6/19

On the other hand, other studies have recognized that the affect experienced duringthe acquisition and consumption of the product or service can also have a significantinfluence on satisfaction judgments (Homburg et al., 2006). The role affectivedimension in establishment evaluation has not been overlooked by research (Burns and

Neisner, 2006). Liljander and Strandvik (1997) suggest that satisfaction cannot becompletely understood without the study of its affective dimension. Dube-Rioux (1990)points out that a consumer affective response can be used to predict satisfaction moreaccurately than cognitive evaluation. In addition, Westbrook (1987) identified theneglected role of affect in post-purchase satisfaction appraisals, which then resulted instudies of the role of affect in service encounters as well as for the overall evaluation of a service (e.g. Alford and Shrerell, 1996; Liljander and Strandvik, 1997; Matilla andWirtz, 2000; Schoefer and Ennew, 2005; Jiang and Wang, 2006).

To sum up, the review of the literature suggests that the most common component of evaluation is previous expectations of the purchase experience by the consumer(Andreassen and Lindestad, 1998). It can thus be stated that consumers are satisfiedwhen purchase results exceed their expectations, in accordance with the“disconfirmatory paradigm” (Oliver, 1980). Each experience leads to an evaluation,and an accompanying emotional reaction, by the customer. It is also necessary to pointout that consumer satisfaction can be attributed to various dimensions such assatisfaction with the frontline employees, the core service or the organization in general(Lewis and Soureli, 2006). This process may imply the construction of differentsatisfaction dimensions (Westbrook, 1981; Anselmsson, 2006). To be more precise,previous research in services directed at people and characterized by high customercontact with individually customized service solutions has identified several dimensionswhich effectively have a different influence on overall consumer satisfaction.

Customer satisfaction within the context of retail banking

Banking is one of the many service industries, characterized by high customer contactwith individually customized service solutions, where customer satisfaction has beenan increasing focus of research. Levesque and McDougall (1996) point out thatcustomer satisfaction and retention are critical for retail banks. They investigate themajor determinants of customer satisfaction (service quality, service features,customer complaint handling and situational factors), and future intentions in the retailbank sector. Bloemer et al. (1998) investigate how image, perceived service quality andsatisfaction determine loyalty in a retail bank. Armstrong and Seng (2000) analyze thedeterminants of customer satisfaction in the banking industry (transactionalparadigm, purchase intentions and fairness (equity). The study of Lassar et al.(2000) examines the effects of service quality on customer satisfaction from twodistinct methodological perspectives – SERVQUAL and technical/functional quality.

Jamal and Naser (2002) suggest that customer satisfaction is based not only on the judgment of customers towards the reliability of the delivered service, but also oncustomers’ experiences with the service delivery process. Hence, they reportdemographic differences (education and income levels) in the degree of customersatisfaction. Therefore, customer satisfaction with retail banking is composed of a widevariety of dimensions.

Overall consumer satisfaction thus reveals the general evaluation of the actionscarried out by a given business in relation to expectations accumulated after various

IJBM25,4

258

8/6/2019 Retial Banking-customer Satisfaction

http://slidepdf.com/reader/full/retial-banking-customer-satisfaction 7/19

contact between the consumer and business (Bitner and Hubber, 1994). If customersperceived that they are obtaining additional benefits from their relationship withestablishment employees, their satisfaction level with the service provider will increase(Beatty et al., 1996). Relational benefits can then be considered as an important factor

for satisfaction with financial businesses. Therefore, relational benefits meaningspecial treatment, confidence and social benefits, which were identified by Gwinneret al. (1998), would have a great influence on customer satisfaction with their habitualestablishments.

Likewise, research literature has considered trust as a factor with a great influenceon the degree of satisfaction at the level of the relationship between producers andconsumers through distribution channels (Anderson and Narus, 1990). Besides this, theanalysis of the role played by expectations in satisfaction evaluation leads to thededuction that there is a positive relationship between the confidence relational benefitand satisfaction (Szymanski and Henard, 2001). Whereas Henning-Thurau et al. (2002)found a non-significant relationship between special treatment and satisfaction, it islogical to expect that the benefit of special treatment will have a great influence onsatisfaction within retail banking. This is due to the fact that special treatmentprovided by a financial service provider can be perceived as a part of the overallservice, so that this benefit will increase customer satisfaction (Reynolds and Beatty,1999). Equally, while Henning-Thurau et al. (2002) could not find a positive relationshipbetween social benefits and satisfaction, it is reasonable to anticipate that socialbenefits could have a positive influence on satisfaction even though these benefits tendto focus more on relationships than results. This is due to the importance attributed bycustomers to social interaction with financial frontline employees more than to anyother relational benefits (Reynolds and Beatty, 1999). Consequently, the main researchquestion of the study is to verify if there is a direct and positive relationship betweenthe above mentioned relational benefits and consumer satisfaction.

MethodologyThe research process involved the following steps. First, a literature review wasundertaken to identify relational benefits and customer satisfaction dimensions inretail banking. Second, the population and sampling procedure was established. Third,a questionnaire was constructed. Finally, the methods of data collection and analyseswere determined.

Sample dataAn empirical study was conducted in Spain in 2004. The population of the study wasbank customers in three large Spanish cities located in central Spain. A representativesample was selected, taking into account the distribution of branches of the different

entities in each of the cities analyzed. Data was collected by using a conveniencesampling method. The questionnaire was administered by personal interview in bankbranches within normal banking hours. Respondents were asked to focus on the bankthey use most often, not necessarily the one in which the interview took place. A totalof 219 questionnaires were completed. However, in order to ensure that they werecustomers who had an ongoing relationship with a particular bank, the intervieweewas asked to offer an evaluation of the said relationship on a five-point scale whichranges between I have a very weak relationship with the bank to I have a very strong

Customersatisfaction inretail banking

259

8/6/2019 Retial Banking-customer Satisfaction

http://slidepdf.com/reader/full/retial-banking-customer-satisfaction 8/19

8/6/2019 Retial Banking-customer Satisfaction

http://slidepdf.com/reader/full/retial-banking-customer-satisfaction 9/19

Before the questionnaire was distributed it was proof-read by two marketingacademics and five professionals from the banking sector. Thus, the questionnaire waspre-tested and, based on the debriefing of the pre-test respondents; minor changes weremade to improve the clarity and visual layout of the questionnaire.

ResultsThis section will provide results of the analysis on the variables described. This will befollowed by subsequent analyses of the relationship between relational benefits andcustomer satisfaction with a bank. In addition to descriptive statistics, multivariateanalysis techniques were used in the data with the objective of contrasting therelationship proposed and verify the possible results, in agreement with the objectives.

Exploratory phaseBefore going deeper into the relationship between relation benefits and customersatisfaction in retail banking, the fit of the scales in relation to the data was analyzed.

Although the scales have been widely used, no previous study has used them in abanking context. Initially, the scales used in this study were factor analyzed to assesstheir psychometric properties. Exploratory factoring was based on a principalcomponents analysis with a varimax rotation of 14 and 20 items that describe thedifferent relational benefits and customer satisfaction dimensions suggested byliterature, respectively. Before conducting the exploratory factor analysis, a test wascarried out to establish whether variables correlated to each other with the end aim of finding out whether it was possible to carry out a factor analysis. According toBartlett’s Test of Sphericity (sig ¼ 0:000) relational benefits and satisfaction variablescorrelated with each other respectively, which meant it was possible to perform a factoranalysis. Furthermore, the Kaiser-Meyer-Olkin (KMO) measures of sampling adequacy(score 0.883 and 0.905 respectively) indicated a practical level of common variance and

therefore factoring was appropriate.The factors whose eigenvalues were greater than 1 were selected according to the

criteria developed by Kaiser (1958). In addition, only factor loadings greater than 0.5were included in the analysis (Hair et al., 1999) and items with extractions lower than0.5 were not included in the analysis.

The relational benefits principal components factor analysis showed the securingof three factors. The three diverse types of relational benefits, identified in previousliterature, were in the following terms: 29.99 per cent the first factor, 26.42 per centthe second and 18.18 per cent the third. In this way, 74.60 per cent of the variance isobtained. According to literature (Gwinner et al., 1998; Patterson and Smith, 2001;Henning-Thurau et al., 2002; Martın-Consuegra et al., 2006), the three dimensionsderived from the exploratory factor analysis were labeled “Special treatment

benefits” (STB), “Confidence benefits” (CB), and “Social benefits” (SB). Six itemswere loaded on the first dimension (STB), the second dimension (CB) consisted of four items, and four items were loaded on the third one (SB). Thereafter, one itemfrom the second factor with significant cross loadings across all three factors weredropped (Hair et al., 1999).

In addition, with regard to customer satisfaction a principal axis factoring withVarimax-rotation was the extraction technique employed. The resulting factorstructure consisted of three factors. In this regard, only 57.58 per cent of the variance

Customersatisfaction inretail banking

261

8/6/2019 Retial Banking-customer Satisfaction

http://slidepdf.com/reader/full/retial-banking-customer-satisfaction 10/19

was obtained, although it allowed for the clear identification of three customersatisfaction dimensions. Eight items loaded on the first dimension with a variance of 24.22 per cent, the second dimension with seven items contributed a variance of 19.53per cent, and the third one with five items contributed 13.84 per cent variance. After

that, three items with marginally significant loadings and significant cross loadingsacross all three factors were dropped (Hair et al., 1999). According to a review of theliterature on this subject (e.g. Oliver, 1980; Westbrook, 1981; Levesque and McDougall,1996; Lassar et al., 2000; Anselmsson, 2006), the three dimensions derived from theexploratory factor analysis were labeled “Frontline employee satisfaction” (FES),“Accessibility” (A), and “Service policy satisfaction” (SPS).

Confirmatory phaseNext, an assessment of the relational benefits and consumer satisfaction scales forunidimensionality and internal consistency was conducted. Confirmatory factoranalyses were used to test relational benefits and consumer satisfaction dimensions

were identified respectively. The measures were then analyzed for reliability andvalidity following the main guidelines offered by Hair et al. (1999) At this point, itemsthat did not load at 0.4 or above on any factor were excluded.

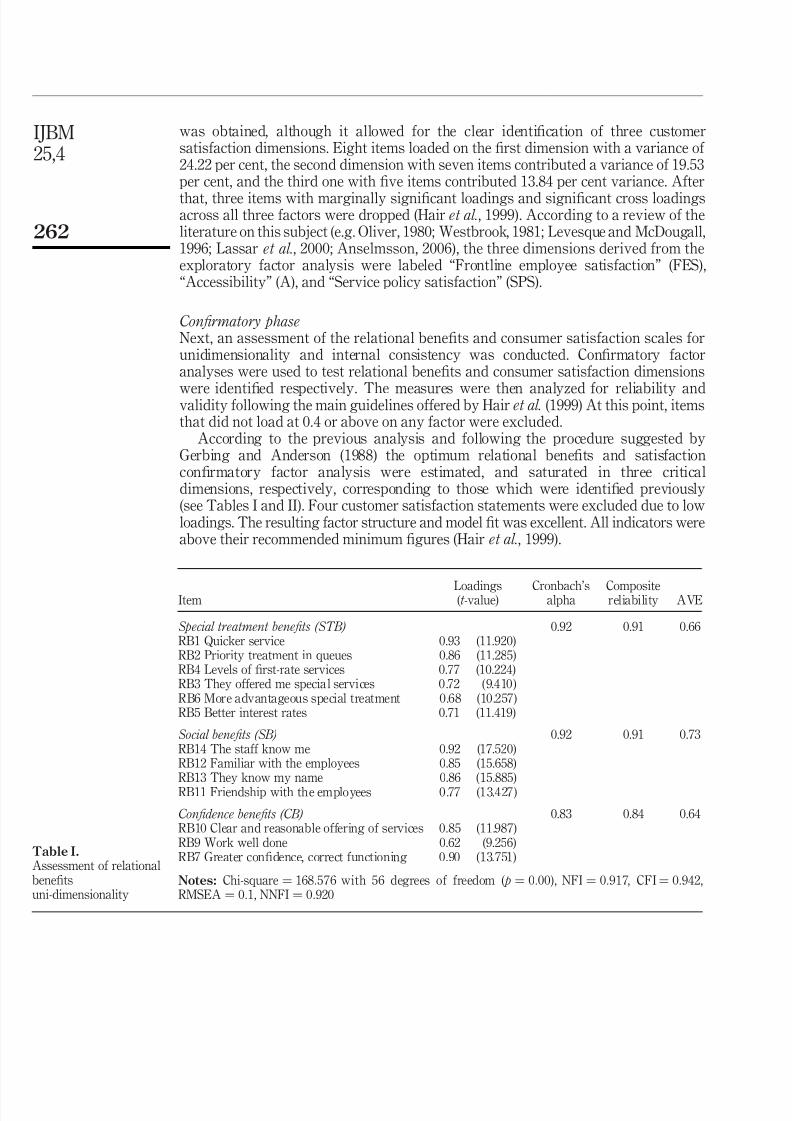

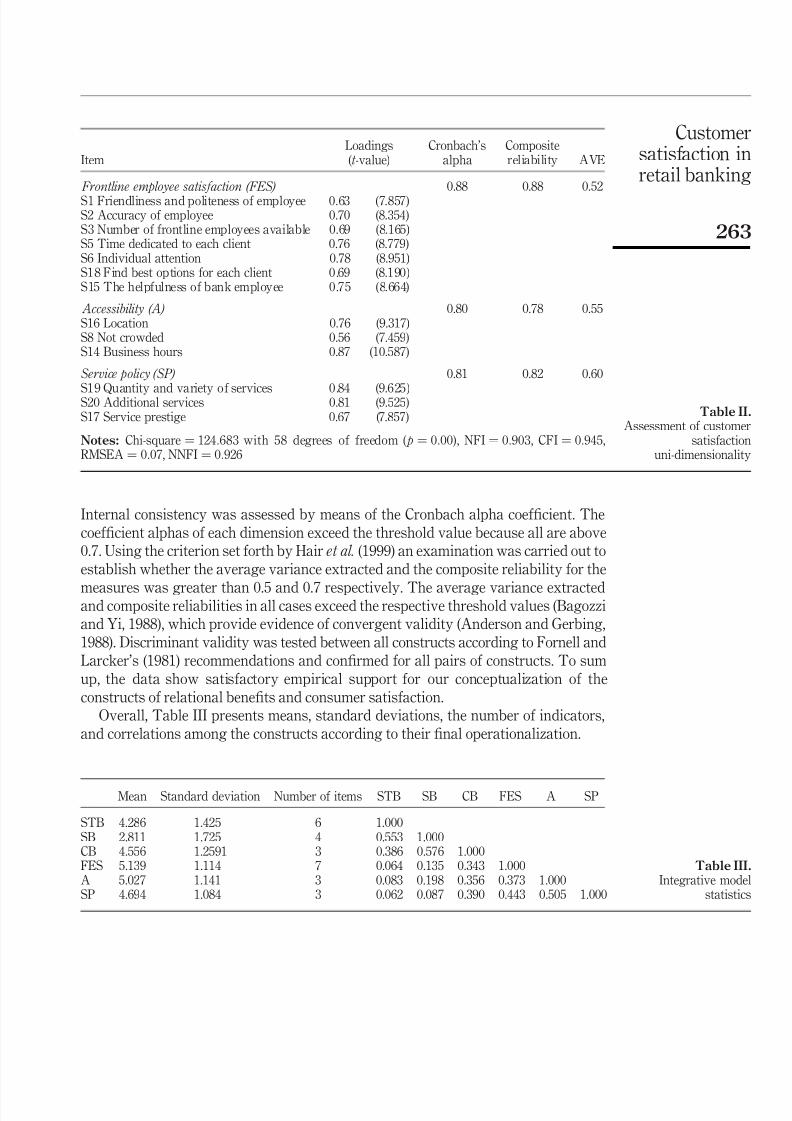

According to the previous analysis and following the procedure suggested byGerbing and Anderson (1988) the optimum relational benefits and satisfactionconfirmatory factor analysis were estimated, and saturated in three criticaldimensions, respectively, corresponding to those which were identified previously(see Tables I and II). Four customer satisfaction statements were excluded due to lowloadings. The resulting factor structure and model fit was excellent. All indicators wereabove their recommended minimum figures (Hair et al., 1999).

Item Loadings( t -value) Cronbach’salpha Compositereliability AVE

Special treatment benefits (STB) 0.92 0.91 0.66RB1 Quicker service 0.93 (11.920)RB2 Priority treatment in queues 0.86 (11.285)RB4 Levels of first-rate services 0.77 (10.224)RB3 They offered me special services 0.72 (9.410)RB6 More advantageous special treatment 0.68 (10.257)RB5 Better interest rates 0.71 (11.419)

Social benefits (SB) 0.92 0.91 0.73RB14 The staff know me 0.92 (17.520)RB12 Familiar with the employees 0.85 (15.658)RB13 They know my name 0.86 (15.885)RB11 Friendship with the employees 0.77 (13.427)

Confidence benefits (CB) 0.83 0.84 0.64RB10 Clear and reasonable offering of services 0.85 (11.987)RB9 Work well done 0.62 (9.256)RB7 Greater confidence, correct functioning 0.90 (13.751)

Notes: Chi-square ¼ 168:576 with 56 degrees of freedom ( p ¼ 0:00), NFI ¼ 0:917, CFI ¼ 0:942,RMSEA ¼ 0:1, NNFI ¼ 0:920

Table I.Assessment of relationalbenefitsuni-dimensionality

IJBM25,4

262

8/6/2019 Retial Banking-customer Satisfaction

http://slidepdf.com/reader/full/retial-banking-customer-satisfaction 11/19

Internal consistency was assessed by means of the Cronbach alpha coefficient. The

coefficient alphas of each dimension exceed the threshold value because all are above

0.7. Using the criterion set forth by Hair et al. (1999) an examination was carried out to

establish whether the average variance extracted and the composite reliability for the

measures was greater than 0.5 and 0.7 respectively. The average variance extractedand composite reliabilities in all cases exceed the respective threshold values (Bagozzi

and Yi, 1988), which provide evidence of convergent validity (Anderson and Gerbing,

1988). Discriminant validity was tested between all constructs according to Fornell and

Larcker’s (1981) recommendations and confirmed for all pairs of constructs. To sum

up, the data show satisfactory empirical support for our conceptualization of the

constructs of relational benefits and consumer satisfaction.

Overall, Table III presents means, standard deviations, the number of indicators,

and correlations among the constructs according to their final operationalization.

ItemLoadings( t -value)

Cronbach’salpha

Compositereliability AVE

Frontline employee satisfaction (FES) 0.88 0.88 0.52

S1 Friendliness and politeness of employee 0.63 (7.857)S2 Accuracy of employee 0.70 (8.354)S3 Number of frontline employees available 0.69 (8.165)S5 Time dedicated to each client 0.76 (8.779)S6 Individual attention 0.78 (8.951)S18 Find best options for each client 0.69 (8.190)S15 The helpfulness of bank employee 0.75 (8.664)

Accessibility (A) 0.80 0.78 0.55S16 Location 0.76 (9.317)S8 Not crowded 0.56 (7.459)S14 Business hours 0.87 (10.587)

Service policy (SP) 0.81 0.82 0.60

S19 Quantity and variety of services 0.84 (9.625)S20 Additional services 0.81 (9.525)S17 Service prestige 0.67 (7.857)

Notes: Chi-square ¼ 124:683 with 58 degrees of freedom ( p ¼ 0:00), NFI ¼ 0:903, CFI ¼ 0:945,RMSEA ¼ 0:07, NNFI ¼ 0:926

Table II.Assessment of customer

satisfactionuni-dimensionality

Mean Standard deviation Number of items STB SB CB FES A SP

STB 4.286 1.425 6 1.000SB 2.811 1.725 4 0.553 1.000CB 4.556 1.2591 3 0.386 0.576 1.000FES 5.139 1.114 7 0.064 0.135 0.343 1.000A 5.027 1.141 3 0.083 0.198 0.356 0.373 1.000SP 4.694 1.084 3 0.062 0.087 0.390 0.443 0.505 1.000

Table III.Integrative model

statistics

Customersatisfaction inretail banking

263

8/6/2019 Retial Banking-customer Satisfaction

http://slidepdf.com/reader/full/retial-banking-customer-satisfaction 12/19

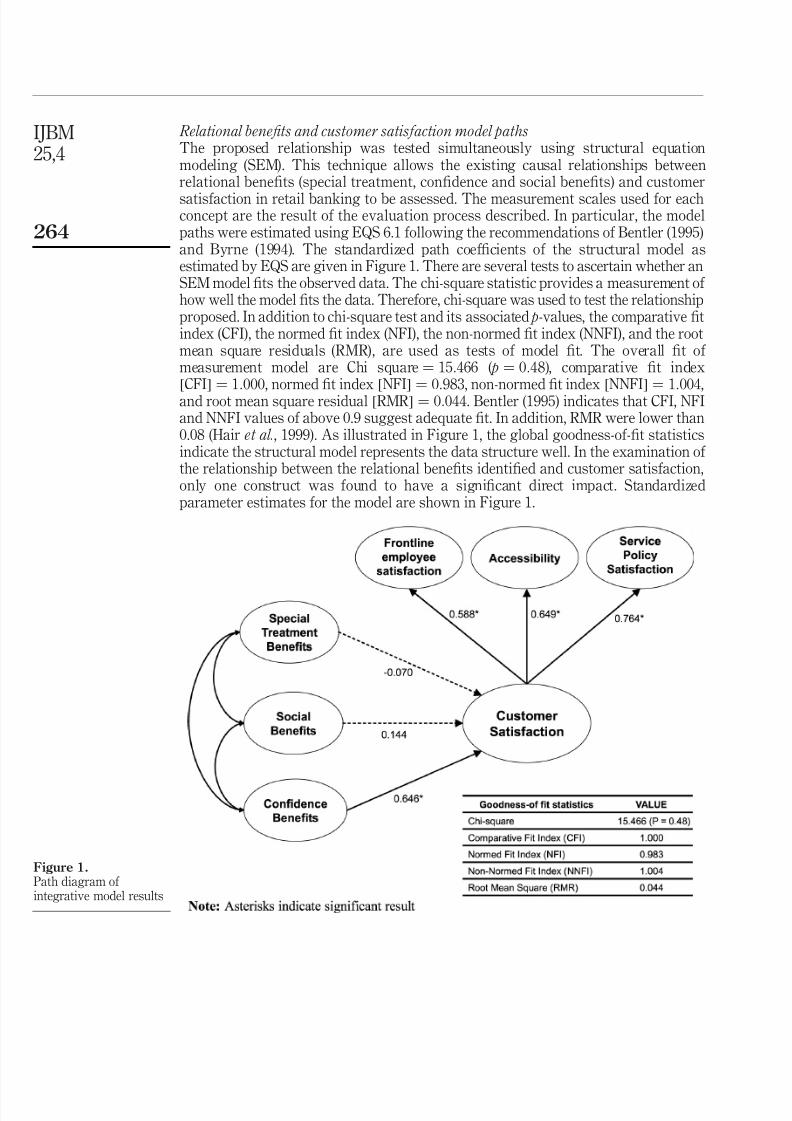

Relational benefits and customer satisfaction model pathsThe proposed relationship was tested simultaneously using structural equationmodeling (SEM). This technique allows the existing causal relationships betweenrelational benefits (special treatment, confidence and social benefits) and customer

satisfaction in retail banking to be assessed. The measurement scales used for eachconcept are the result of the evaluation process described. In particular, the modelpaths were estimated using EQS 6.1 following the recommendations of Bentler (1995)and Byrne (1994). The standardized path coefficients of the structural model asestimated by EQS are given in Figure 1. There are several tests to ascertain whether anSEM model fits the observed data. The chi-square statistic provides a measurement of how well the model fits the data. Therefore, chi-square was used to test the relationshipproposed. In addition to chi-square test and its associated p-values, the comparative fitindex (CFI), the normed fit index (NFI), the non-normed fit index (NNFI), and the rootmean square residuals (RMR), are used as tests of model fit. The overall fit of measurement model are Chi square ¼ 15:466 ( p ¼ 0:48), comparative fit index½CFI� ¼ 1:000, normed fit index ½NFI� ¼ 0:983, non-normed fit index ½NNFI� ¼ 1:004,and root mean square residual ½RMR� ¼ 0

:044. Bentler (1995) indicates that CFI, NFI

and NNFI values of above 0.9 suggest adequate fit. In addition, RMR were lower than0.08 (Hair et al., 1999). As illustrated in Figure 1, the global goodness-of-fit statisticsindicate the structural model represents the data structure well. In the examination of the relationship between the relational benefits identified and customer satisfaction,only one construct was found to have a significant direct impact. Standardizedparameter estimates for the model are shown in Figure 1.

Figure 1.Path diagram of integrative model results

IJBM25,4

264

8/6/2019 Retial Banking-customer Satisfaction

http://slidepdf.com/reader/full/retial-banking-customer-satisfaction 13/19

The results are quite similar to those obtained from a wide variety of service providersby Henning-Thurau et al. (2002). As predicted in the proposed relationship, confidentbenefits had positive and significant influences on satisfaction ( b ¼ 0:646, p , 0:01).Contrary to the proposed relationship, the influences of special treatment ( b ¼ 20:070)

and social benefits ( b ¼ 0:

144) on satisfaction are not significant. The results supportconfidence benefits having a significant and strong impact on customer satisfaction,whereas satisfaction is not significantly influenced by either social or special treatmentbenefits. For this reason, the results presented in Figure 1 attest to the significance of confidence benefits as one of the retail banking customer satisfaction antecedents. Themagnitude of the significant positive correlation confidence benefits coefficient shownin Figure 1, offers partial support for the relationship proposed. Overall, it can besuggested that only the confidence benefits derived from maintaining a stablerelationship with a bank have an important and positive effect on retail bankingcustomer satisfaction. In this regard, it could therefore be assumed that the efforts of financial institutions to discover and offer to consumers adequate confidence benefits,and even social benefits, generate a higher value to the relationship with the bank,which directly affects customer satisfaction.

Discussion and implicationsThe main objective of this paper was to analyze the relationship between relationalbenefits and consumer satisfaction after a service has been rendered through retailbanking. To be more precise, the analysis has focused on the relationship betweencustomers and their regular banks. Since relational benefits, as an overall relationshipvalue provision system, influence expectations, the considerable impact of those oncustomer satisfaction is logical. Also, the theoretical approach to each of these conceptsand their empirical application to financial business thereafter have proved thisobjective.

Results in this research lead to some relevant conclusions. First of all, the results of the study of relational benefits confirm those obtained by Gwinner et al. (1998) in avariety of services, and Martın-Consuegra et al. (2006) in retail banking. In addition,they are similar to those yielded by other research, although such works have generallycentred on a wide variety of services (Patterson and Smith, 2001; Henning-Thurau et al.,2002). The relational benefits identified in these works for the service sector can also beapplied to retail banking, as this paper has demonstrated. Consequently, due to thecurrent situation of retail banking and to the importance of relationship marketing forits development, it is essential to include a consumer perspective in the analysis of thisrelationship. Also, the results from the empirical analysis suggest three dimensions of the construct of customer satisfaction in retail banking. Its components are based onthe evaluation of experiences by the consumers in the bank. Consequently, customer

satisfaction in financial businesses depends on the service policy satisfaction, onaccessibility, and on the frontline employee satisfaction.

The use of a causal model has facilitated information about the relationship betweenrelational benefits and satisfaction. This research has empirically validated therelationship between relational benefits and the satisfaction of a customer with his/herregular bank. Even though some previous works had centered on relational benefits,only the studies by Reynolds and Beatty (1999) in retailing, Henning-Thurau et al.(2002) in a wide variety of services and Marzo et al. (2004) in retail clothing store

Customersatisfaction inretail banking

265

8/6/2019 Retial Banking-customer Satisfaction

http://slidepdf.com/reader/full/retial-banking-customer-satisfaction 14/19

establishments, had tried to prove the relationship between relational benefits andsatisfaction. These studies had focused on one kind of business establishment or awide variety of services. Contrarily, the present research has promoted the analysis of this relationship in retail banking.

This study has established, however, that, even if special treatment, confidence andsocial benefits are all present in retail banking, only bank confidence seems to be of definitive importance. In this sense, this paper coincides with the results from reviewedresearch (Henning-Thurau et al., 2002), so it reinforces the premise that trust andconfidence in good service rendered by a given bank is the key to a good long-termrelationship between this establishment and its customers.

Considering the results obtained here, it is possible to affirm that relational benefitsare a predicting element of satisfaction when a service is rendered directly by thefinancial service provider to the final consumer. Consequently, this research presents atheoretical contribution because it proposes a conceptual model for the analysis of theinfluence of relational benefits on satisfaction. In this theoretical framework, this modelintegrates three kinds of relational benefits which could affect the dimensions of consumer satisfaction.

In interpreting the results of this study, a number of limitations must be considered.From a theoretical point of view, the framework of this research is restricted to its ownobjectives. This study has pondered the relationship between relational benefits andsatisfaction, while other antecedents or consequences of consumer satisfaction have notbeen considered. This research and the model it proposes have been devised as a basis forfuture studies. From a methodological perspective, the results from this study can only begeneralized for banks and financial services providers, due to the fact that it has only beenapplied to these businesses. Furthermore, different segments of customers might existwith regard to their relational preferences (Reynolds and Beatty, 1999; Henning-Thurauet al., 2002). Future researches may wish to explore the moderating relationship of

consumer relational preferences. In developing a more extensive framework, a model thatincorporates the consequences of customer satisfaction in retail banking, that is, loyaltyand word-of-mouth, will also provide timely and important contributions to marketingknowledge. In addition, larger sample size may get significant results for those proposedrelationships that were non-significant. It is probable that the non-significant results forsome of the path coefficients may be due to the sample size.

Some suggestions can be made after considering the results from this study. Anindication as to how bank management can gain direction from this study becomesevident when the findings are considered in conjunction with the competitiveadvantage concept. First, financial businesses are advised to apply relationshipmarketing in order to enhance the number of regular and satisfied customers. Second,it is necessary for top managers to establish the most important dimensions of

customer satisfaction in retail banking. Third, the relatively strong relationshipdemonstrated between confidence benefits and customer satisfaction may lead themanagement of a financial service to think that it is more beneficial to focus on trust orconfidence than it is on special treatment benefits (better interest rates). Finally, due tothe fact that financial businesses are heterogeneous, presenting a wide variety of sizesand forms, it is desirable that further research should be made and that it concentrateson analyzing the relationship between the two concepts used in this study, and thedegree or intensity of this relationship.

IJBM25,4

266

8/6/2019 Retial Banking-customer Satisfaction

http://slidepdf.com/reader/full/retial-banking-customer-satisfaction 15/19

To conclude, the information provided by this research can be better used whendesigning marketing strategies for financial businesses. Banks need to continue theirbasic strategy of maintaining a stable and close relationship with their customers inorder to improve customer satisfaction.

References

Aldlaigan, A. and Buttle, F. (2005), “Beyond satisfaction: customer attachment to retail banks”, International Journal of Bank Marketing , Vol. 23 No. 4, pp. 349-59.

Alford, B.L. and Shrerell, D.L. (1996), “The role of affect in consumer satisfaction judgments of credence-based services”, Journal of Business Research, Vol. 37 No. 1, pp. 71-84.

Anderson, E.W. (1998), “Customer satisfaction and word of mouth”, Journal of Service Research,Vol. 1, May, pp. 5-17.

Anderson, E.W. and Narus, J.A. (1990), “A model of distributor firm and manufacturer firmworking partnerships”, Journal of Marketing , Vol. 54, January, pp. 42-58.

Anderson, E.W. and Sullivan, M.W. (1993), “The antecedents and consequences of customer

satisfaction for firms”, Marketing Science, Vol. 12 No. 2, pp. 125-43.Anderson, J.C. and Gerbing, D.W. (1988), “Structural equation modeling in practice: a review and

recommended two-step approach”, Psychological Bulletin, Vol. 103 No. 3, pp. 411-23.

Andreassen, T.W. and Lindestad, B. (1998), “Customer loyalty and complex services: the impactof corporate image on quality, customer satisfaction and loyalty for customer with varyingdegrees of service expertise”, International journal of Service Industry Management , Vol. 9No. 1, pp. 7-23.

Anselmsson, J. (2006), “Sources of customer satisfaction with shopping malls: a comparativestudy of different customer segments”, International Review of Retailing, Distribution and Consumer Research, Vol. 16 No. 1, pp. 115-38.

Armstrong, R.W. and Seng, T.B. (2000), “Corporate-customer satisfaction in the bankingindustry of Singapore”, International Journal of Bank Marketing , Vol. 18 No. 3, pp. 97-111.

Bagozzi, R.P. and Yi, Y. (1988), “On the evaluation of structural equation models”, Journal of the Academy of Marketing Science, Vol. 16, Spring, pp. 74-94.

Bearden, W.O. and Teel, J.E. (1983), “Selected determinants of consumer satisfaction andcomplaints reports”, Journal of Marketing Research, Vol. 20, February, pp. 21-8.

Beatty, S.E., Mayer, M., Coleman, J.E., Reynolds, K.E. and Lee, J. (1996), “Customer-salesassociate retail relationships”, Journal of Retailing , Vol. 72 No. 3, pp. 223-47.

Bejou, D., Ennew, C.T. and Palmer, A. (1998), “Trust, ethics and relationship satisfaction”, International Journal of Bank Marketing , Vol. 16 No. 4, pp. 170-5.

Bendapudi, N. and Berry, L.L. (1997), “Customers’ motivations for maintaining relationships withservice providers”, Journal of Retailing , Vol. 73 No. 1, pp. 15-37.

Bentler, P.M. (1995), EQS: Structural Equations Program Manual , BMDP Statistical Software,

Los Angeles.

Berry, L.L. (1983), “Relationship marketing”, in Berry, L.L., Shostack, G.L. and Upah, G. (Eds), Emerging Perspectives Services Marketing , American Marketing Association, Chicago, IL,pp. 25-8.

Berry, L.L. (1995), “Relationship marketing of services-growing interest, emerging perspectives”, Journal of the Academy of Marketing Science, Vol. 23 No. 4, pp. 236-45.

Bitner, M.J. (1995), “Building service relationships: it’s all about promises”, Journal of the Academy of Marketing Science, Vol. 23 No. 4, pp. 246-51.

Customersatisfaction inretail banking

267

8/6/2019 Retial Banking-customer Satisfaction

http://slidepdf.com/reader/full/retial-banking-customer-satisfaction 16/19

Bitner, M.J. and Hubber, A.R. (1994), “Encounter satisfaction versus overall satisfaction versus

quality”, in Rust, R.R. and Oliver, R.L. (Eds), Service Quality: New Directions in Theory and

Practice, Sage Publications, Thousand Oaks, CA, pp. 311-29.

Bloemer, J., De Ruyter, K. and Peeters, P. (1998), “Investigating drivers of bank loyalty: the

complex relationship between image, service quality and satisfaction”, International Journal of Bank Marketing , Vol. 16 No. 7, pp. 276-86.

Burns, D.J. and Neisner, L. (2006), “Customer satisfaction in a retail setting: the contribution of

emotion”, International Journal of Retail & Distribution Management , Vol. 34 No. 1,

pp. 49-56.

Byrne, B.M. (1994), Structural Equations Modeling with EQS and EQS/Windows, Sage

Publications, Newbury Park, CA.

Colgate, M., Buchanan-Oliver, M. and Elmsly, R. (2005), “Relationship benefits in an internet

environment”, Managing Service Quality, Vol. 15 No. 5, pp. 426-36.

Darian, J.C., Tucci, L.A. and Wiman, A.R. (2001), “Perceived salesperson service attributes and

retail patronage intentions”, International Journal of Retail & Distribution Management ,

Vol. 29 Nos 4/5, pp. 205-13.Dube-Rioux, L. (1990), “Power of affective reports in predicting satisfaction judgments”,

in Goldberg, M., Gorn, G. and Pollay, R. (Eds), Advances in Consumer Research,Vol. 17,

pp. 571-6.

Dwyer, F.R., Schurr, P.H. and Oh, S. (1997), “Developing buyer-seller relationships”, Journal of

Marketing , Vol. 51, April, pp. 11-27.

Fornell, C. and Larcker, D.F. (1981), “Evaluating structural equation models unobservable

variables and measurement error”, Journal of Marketing Research, Vol. 18 No. 1, pp. 39-51.

Gerbing, D.W. and Anderson, J.C. (1988), “An updated paradigm for scale development

incorporating unidimensionality and its assessment”, Journal of Marketing Research,

Vol. 25, May, pp. 186-92.

Gronroos, C. (1990), “Relationship approach to marketing in service context: the marketing andorganizational behaviour interface”, Journal of Business Research, Vol. 20, January,

pp. 3-11.

Gwinner, K.P., Gremler, D.D. and Bitner, M.J. (1998), “Relational benefits in services industries:

the customer’s perspective”, Journal of the Academy of Marketing Science, Vol. 26 No. 2,

pp. 101-14.

Hair, J.F., Anderson, R.E., Tatham, R.L. and Black, W.C. (1999), Multivariate Analysis, Prentice

Hall, New York, NY.

Henning-Thurau, T., Gwinner, K.P. and Gremler, D.D. (2002), “Understanding relationship

marketing outcomes: an integration of relational benefits and relationship quality”,

Journal of Service Research, Vol. 4 No. 3, pp. 230-47.

Homburg, C., Koschate, N. and Hoyer, W.D. (2006), “The role of cognition and affect in theformation of customer satisfaction: a dynamic perspective”, Journal of Marketing , Vol. 70,

July, pp. 21-31.

Hunt, S.D. (1993), “General theories and the fundamental explananda of marketing”, Journal of

Marketing , Vol. 47, fall, pp. 9-17.

Jamal, A. (2004), “Retail banking and customer behaviour: a study of self concept, satisfaction

and technology usage”, International Review of Retailing, Distribution and Consumer

Research, Vol. 14 No. 3, pp. 357-79.

IJBM25,4

268

8/6/2019 Retial Banking-customer Satisfaction

http://slidepdf.com/reader/full/retial-banking-customer-satisfaction 17/19

Jamal, A. and Naser, K. (2002), “Customer satisfaction and retail banking: an assessment of someof the key antecedents of customer satisfaction in retail banking”, International Journal of

Bank Marketing , Vol. 20 No. 4, pp. 146-60.

Jiang, Y. and Wang, C.L. (2006), “The impact of affect on service quality and satisfaction:

the moderation of service contexts”, The Journal of Service Marketing , Vol. 20 No. 4,pp. 211-8.

Kaiser, H.F. (1958), “The varimax criterion for analytic rotation in factor analysis”, Psychometrika, No. 23, pp. 187-200.

LaBarbera, P.A. and Mazursky, D. (1983), “A longitudinal assessment of consumersatisfaction/dissatisfaction: the dynamic aspect of the cognitive process”, Journal of

Marketing Research, Vol. 20 No. 4, pp. 393-404.

Lassar, W.M., Manolis, C. and Winsor, R.D. (2000), “Service quality perspectives and satisfactionin private banking”, Journal of Services Marketing , Vol. 14 No. 3, pp. 244-71.

Leverin, A. and Liljander, V. (2006), “Does relationship marketing improve customer relationshipsatisfaction and loyalty?”, International Journal of Bank Marketing , Vol. 24 No. 4,pp. 232-51.

Levesque, T. and McDougall, G.H.G. (1996), “Determinants of customer satisfaction in retailbanking”, International Journal of Bank Marketing , Vol. 14 No. 7, pp. 12-20.

Lewis, B.R. and Soureli, M. (2006), “The antecedents of consumer loyalty in retail banking”, Journal of Consumer Behaviour , Vol. 5, February, pp. 15-31.

Liljander, V. and Strandvik, T. (1997), “Emotions in service satisfaction”, International Journal of Service Industry Management , Vol. 8 No. 2, pp. 148-69.

Mano, H. and Oliver, R.L. (1993), “Assessing the dimensionality and structure of the consumptionexperience: evaluation, feeling and satisfaction”, Journal of Consumer Research, Vol. 20,pp. 451-67.

Martın-Consuegra, D., Molina, A. and Esteban, A. (2006), “The customer’s perspective onrelational benefits in banking activities”, Journal of Financial Services Marketing , Vol. 10

No. 4, pp. 98-108.Marzo, M., Pedraja, M. and Rivera, M.P. (2004), “The benefits of relationship marketing for the

consumer and for the fashion retailers”, Journal of Fashion Marketing and Management ,Vol. 8 No. 4, pp. 425-36.

Matilla, A. and Wirtz, J. (2000), “The role of preconsumption affect in post-purchase evaluation of services”, Psychology & Marketing , Vol. 17 No. 7, pp. 587-605.

Mittal, V., Kumar, P. and Tsiros, M. (1999), “Attribute-level performance, satisfaction, andbehavioral intentions over time: a consumption system approach”, Journal of Marketing ,Vol. 63 No. 2, pp. 88-101.

Morgan, R.M. and Hunt, S.D. (1994), “The commitment-trust theory of relationship marketing”, Journal of Marketing , Vol. 58, July, pp. 20-38.

Ndubisi, N.O. and Wah, C.K. (2005), “Factorial and discriminant analyses of the underpinnings of

relationship marketing and customer satisfaction”, International Journal of Bank Marketing , Vol. 23 No. 7, pp. 542-57.

Oliver, R.L. (1980), “A cognitive model of the antecedents and consequences of satisfactiondecisions”, Journal of Marketing Research, Vol. 17 No. 4, pp. 460-9.

Oliver, R.L. (1981), “Measurement and evaluation of satisfaction processes in retail setting”, Journal of Retailing , Vol. 57 No. 3, pp. 25-49.

Oliver, R.L. (1999), “Whence consumer loyalty?”, Journal of Marketing , Vol. 63, Special issue,pp. 33-44.

Customersatisfaction inretail banking

269

8/6/2019 Retial Banking-customer Satisfaction

http://slidepdf.com/reader/full/retial-banking-customer-satisfaction 18/19

Oliver, R.L. and DeSarbo, W.S. (1988), “Response determinants in satisfaction judgments”,

Journal of Consumer Research, Vol. 14, pp. 495-507.

O’Loughlin, D., Szmigin, I. and Turnbull, P. (2004), “From relationships to experiences in retail

financial services”, International Journal of Bank Marketing , Vol. 22 No. 7, pp. 522-39.

Parasuraman, A., Berry, L.L. and Zeithaml, V.A. (1991), “Understanding customer expectations

of service”, Sloan Management Review, Vol. 32, spring, pp. 39-48.

Patterson, P.G. and Smith, T. (2001), “Realationship benefits in service industries: a replication in

a Southeast Asian Context”, Journal of Services Marketing , Vol. 15 No. 6, pp. 425-33.

Patterson, P.G., Johnson, L.W. and Spreng, R.A. (1997), “Modelling the determinants of customer

satisfaction for business-to-business professional services”, Journal of the Academy of Marketing Science, Vol. 25 No. 1, pp. 4-17.

Payne, A. and Rickard, J. (1997), “Relationship marketing, customer retention and firm

profitability”, Working Paper, Cranfield School of Management, Bedford.

Pont, M. and McQuilken, L. (2005), “An empirical investigation of customer satisfaction and

loyalty across two divergent bank segments”, Journal of Financial Services Marketing ,

Vol. 9 No. 4, pp. 344-59.Reichheld, F.F. and Earl Sasser, W. Jr (1990), “Zero defections: quality comes to services”,

Harvard Business Review, Vol. 68, September-October, pp. 105-11.

Reynolds, K.E. and Beatty, S. (1999), “Customer benefits and company consequences of

customer-salesperson relationships in retailing”, Journal of Retailing , Vol. 75 No. 1,

pp. 11-32.

San Martin, S. (2005), “Consumer-retailer from a multi-level perspective”, Journal of International Consumer Marketing , Vol. 17 Nos 2/3, pp. 93-116.

Schoefer, K. and Ennew, C. (2005), “The impact of perceived justice on consumers’ emotional

responses to service complaint experiences”, The Journal of Services Marketing , Vol. 19

No. 5, pp. 261-70.

Shani, D. and Chalasani, S. (1992), “Exploiting niches using relationship marketing”, Journal of Service Marketing , Vol. 6, pp. 43-52.

Sharma, N. and Ojha, S. (2004), “Measuring service performance in mobile communication”,The Service Industries Journal , Vol. 24 No. 6, pp. 109-28.

Sheth, J.N. and Parvatiyar, A. (1995), “Relationship marketing in consumer markets: antecedentsand consequences”, Journal of the Academy of Marketing Science, Vol. 23 No. 4, pp. 255-71.

Swan, J.E. and Trawick, I.F. (1980), “Inferred and perceived disconfirmation in consumersatisfaction”, Advances in Consumer Research, pp. 97-100.

Sweeney, A. and Morrison, M. (2004), “Clicks vs bricks: internet-facilitated relationships in

financial services”, International Journal of Internet Marketing and Advertising , Vol. 1

No. 4, pp. 350-70.

Szymanski, D.A. and Henard, D.H. (2001), “Customer satisfaction: a meta-analysis of theempirical evidence”, Journal of the Academy of Marketing Science, Vol. 29 No. 1, pp. 16-35.

Tse, D.K. and Wilton, P.C. (1988), “Models of customer satisfaction formation: an extension”,

Journal of Marketing Research, Vol. 25 No. 2, pp. 204-12.

Verhoef, P.C., Franses, P.H. and Donkers, B. (2002), “Changing perceptions and changing

behavior in customer relationships”, Marketing Letters, Vol. 13 No. 2, pp. 121-34.

Westbrook, R.A. (1981), “Sources of consumer satisfaction with retail outlets”, Journal of Retailing , Vol. 57 No. 3, pp. 68-85.

IJBM25,4

270

8/6/2019 Retial Banking-customer Satisfaction

http://slidepdf.com/reader/full/retial-banking-customer-satisfaction 19/19

Westbrook, R.A. (1987), “Product/consumption-based affective responses and post-purchaseprocesses”, Journal of Marketing Research, Vol. 24 No. 3, pp. 258-70.

Westbrook, R.A. and Oliver, R.L. (1991), “The dimensionality of consumption emotion patternsand customer satisfaction”, Journal of Consumer Research, Vol. 18, pp. 84-91.

Wong, A. and Sohal, A. (2003), “A critical incident approach to the examination of customerrelationship management in a retail chain: an exploratory study”, Qualitative Market

Research: An International Journal , Vol. 6 No. 4, pp. 248-62.

Wong, A. and Zhou, L. (2006), “Determinants and outcomes of relationship quality: a conceptualmodel and empirical investigation”, Journal of International Consumer Marketing , Vol. 18No. 3, pp. 81-96.

Zeithaml, V.A., Berry, L.L. and Parasuraman, A. (1993), “The nature and determinants of customer expectations of service”, Journal of the Academy of Marketing Science, Vol. 21No. 1, pp. 1-12.

About the authorsArturo Molina is an Associate Professor in the Marketing Department. His research interests arefocused on services, retailing, relationship marketing and image tourism. He has publishedseveral journal articles and papers for international and national conferences. He has spentseveral research periods at European, North American and Canadian Universities. Arturo Molinais the corresponding author and can be contacted at: [email protected]

David Martın-Consuegra is an Associate Professor in the Marketing Department. Hisresearch interests are centered on market orientation, customer relationship, financial servicesand tourism. He has published several journal articles and papers for international and nationalconferences. He has spent several research periods at European and North AmericanUniversities.

Agueda Esteban is a Professor of Marketing. She is head of the Marketing Department. Shehas a particular research interest in the marketing of the tourist services. She has publishednumerous journal articles, conference papers and books, including Principios de Marketing ( Marketing Principles ) and La Investigacio n de Marketing en Espan a ( Marketing Research inSpain ).

Customersatisfaction inretail banking

271

To purchase reprints of this article please e-mail: [email protected] visit our web site for further details: www.emeraldinsight.com/reprints