Retail Marketing Assignment 1 Tesco Fresh & Easy Group A2

21

Retail management Tesco/Fresh & Easy University of Groningen Faculty of Economics and Business Msc. Business Administration – Marketing Prof. L. Voerman December, 2011 Group A02 Harold Dijkstra S1455362 Joyce Gussenhoven S2032910 Perry Nauta S1774441 Robin Papa S1785613

Transcript of Retail Marketing Assignment 1 Tesco Fresh & Easy Group A2

Retail management Tesco/Fresh & Easy

University of Groningen Faculty of Economics and Business

Msc. Business Administration – Marketing

Prof. L. Voerman December, 2011

Group A02 Harold Dijkstra S1455362

Joyce Gussenhoven S2032910 Perry Nauta S1774441 Robin Papa S1785613

2

Abstract The purpose of this research was to investigate how Fresh & Easy can become a success. Tesco is a success in the United Kingdom, Europe and Asia, but since Tesco opened a Fresh & Easy store 2.25 years ago in the United States, this stores have had disappointing results. In this report we only look at the grocery retailing market in Arizona, California and Nevada, states in the southwest of the U.S. The research question is:

• How can our Fresh & Easy venture still become a success before the end of the original five-‐year plan?

Before looking forward to the future of Fresh & Easy, an important question we want to answer is:

• Are the disappointing results of Fresh & Easy in the past 2.25 years a consequence of the economic recession in the western U.S., a wrong strategy or bad implementation?

Finally, following from the external analysis, and in particular the consumer analysis, and previous implementation adjustments without the desired result, another sub question we identified is:

• How can Fresh & Easy adjust better to customer needs? To find answers on these questions, an internal and external analysis is done, followed by a confrontation matrix, options and the implementation. The results show that the disappointing results of Fresh & Easy are a consequence of some missing opportunities in the current strategy to gain a competitive advantage. To better meet the customer needs and to become a success, these opportunities need to be implemented in the current strategy. The opportunities are increase operating hours, reduce shelf stock outs, offer more familiar brands, location convenience and loyalty program. This way, Fresh & Easy becomes a success before the end of the five-‐year plan by implementing these five opportunities.

Key words: Fresh & Easy, Tesco, strategy, opportunities, implement Research theme: How can Fresh & Easy become a success? Seminar supervisor: L. Voerman

3

Table of contents 1. Introduction .......................................................................................................................... 4 1.1 Market definition ............................................................................................................ 4 1.2 Problem statement ......................................................................................................... 4

2. Strategic retail planning ....................................................................................................... 5 2.1 Business mission ............................................................................................................ 5

3. External analysis .................................................................................................................. 5 3.1 Customer analysis .......................................................................................................... 5 3.2 Competitive factors ........................................................................................................ 6 3.2.1 Competitive rivalry ................................................................................................. 6

3.3 Market factors ................................................................................................................ 7 3.3.1 Growth ..................................................................................................................... 7 3.3.2 Seasonality ............................................................................................................... 7 3.3.3 Business cycle .......................................................................................................... 8 3.3.4 Porters Five Forces model ...................................................................................... 8

3.4 Environmental factors ................................................................................................... 9 3.4.1 Technology ............................................................................................................... 9 3.4.2 Economic .................................................................................................................. 9 3.4.3 Regulatory ................................................................................................................ 9 3.4.4 Social ........................................................................................................................ 9

3.5 Conclusion ....................................................................................................................... 9 4. Analysis of strengths and weaknesses ............................................................................. 10 4.1 Financial resources ...................................................................................................... 10 4.2 Management capabilities ............................................................................................. 11 4.3 Locations ....................................................................................................................... 11 4.4 Operations .................................................................................................................... 11 4.5 Merchandising capabilities .......................................................................................... 11 4.6 Customer loyalty .......................................................................................................... 11 4.7 Conclusion ..................................................................................................................... 12

5. Issues ................................................................................................................................... 12 5.1 Consumer demands ..................................................................................................... 12 5.2 Awareness ..................................................................................................................... 12 5.3 Invest or divest? ........................................................................................................... 13

6. Strategic Options ................................................................................................................ 13 7. Evaluation of strategic options .......................................................................................... 14 8. Strategic opportunities ...................................................................................................... 15 8.1 Increase operating hours ............................................................................................. 16 8.2 Reduce shelf stockouts ................................................................................................ 16 8.3 Offer more familiar brands .......................................................................................... 16 8.4 Location convenience .................................................................................................. 17 8.5 Loyalty program ........................................................................................................... 17

9. Conclusion ........................................................................................................................... 17 10. References ......................................................................................................................... 19 Appendix I – SWOT matrix .................................................................................................... 20 Appendix II -‐ Confrontation matrix ...................................................................................... 21

4

1. Introduction Confident, because of the domestic success of Tesco in the United Kingdom and its successful international expansion to Europe and Asia, Tesco opened our first Fresh & Easy store in the United States about 2.25 years ago. Based on an ambitious five-‐year plan, Tesco intended to gain a significant market share in the states of California, Arizona and Nevada in the United States. However, results of the Fresh & Easy venture are disappointing. Targeted sales are not achieved, impact on the revenues of competitors is low and sales growth forecasts are marginal, even after corrections to the original plan during the past year. As the responsible management team of the Fresh & Easy venture in the U.S., our task is to inform the management of Tesco about the underlying reasons for the disappointing results and provide them with advice regarding the future of Fresh & Easy.

1.1 Market definition Since our Fresh & Easy stores in the U.S. are considered as a distinct venture of Tesco, although not mentioned as a distinct subsidiary, this analysis will be described from the perspective of the Fresh & Easy venture instead of Tesco. Consequently, strengths and weaknesses with regard to Tesco will only be included in the internal analysis when they are relevant to Fresh & Easy in the U.S. Our market can be defined as the grocery retailing industry in Arizona, California and Nevada, states in the south-‐west of the U.S. Since the five-‐year plan prepared in 2007 focused on these three states and there is no information available about other parts of the U.S., we will limit our analysis to this geographical market. Our market definition includes all grocery retailers, ranging from convenience stores to supercenters. Concerning the customer need dimension of a market definition (Abell, 1980) it can be found that other retailers also are increasingly offering groceries in addition to the typical supply in their stores. Although this is relevant as a market trend for Fresh & Easy, and therefore will be included in the market analysis, the core products these retailers sell are not relevant to Fresh & Easy in the current situation. Therefore, these retailers will not be included in the market definition and hence the market definition will only focus on the grocery retailing industry.

1.2 Problem statement Stemming from the disappointing results in the first 2.25 years of our Fresh & Easy stores, the following main problem is identified:

• How can our Fresh & Easy venture still become a success before the end of the original five-‐year plan?

Before looking forward to the future of Fresh & Easy an important question we want to answer is:

• Are the disappointing results of Fresh & Easy in the past 2.25 years the result of a wrong strategy or bad implementation?

5

Finally, following from the external analysis, and in particular the consumer analysis, and previous implementation adjustments without the desired result, another sub question we identified is:

• How can Fresh & Easy adjust better to customer needs?

2. Strategic retail planning In order to provide an answer to the questions in the problem statement we employ the strategic retail planning process as described by Levy & Weitz (2009). In addition, we also include some elements of Aaker’s (2007) strategic market management model.

2.1 Business mission The Business mission of our Fresh & Easy venture is to become a considerable player in the grocery retailing in southwest U.S., in the states California, Arizona, Nevada. By selling fresh and wholesome food, providing high product quality and selling at low prices in our neighborhood markets we strive for average sales per store of $200.000.

3. External analysis Our external analysis provides insights in the market and trends of the U.S. grocery retail industry. This is based upon Levy & Weitz (2009) who argue that an external analysis exists of market factors, competitive factors and environmental factors. In additions, Aaker (2007) is used for some additional information, primarily for the customer analysis because in our opinion it is important to take a close look at your customers and we believe that this is not clear done in the strategy of Levy & Weitz (2009).

3.1 Customer analysis The information collected in the previous 2.25 years is minimal. What we know is that the U.S. customer can be described as not tolerant towards stock outs, because when they encounter stock outs they are more likely to shop elsewhere. There is also a low consumer demand and willingness to experiment with a new store brand in the U.S and they are also concerned about the lack of familiar brands at Fresh & Easy. Before opening our first shop, some extensive research was performed, for example by putting 50 senior managers to live with families in California for a month to experience how Americans ate, shop and spent their leisure time. However, conclusions from that initial research obvious are not sufficient, since actual sales figures are far below targeted sales. Therefore, we need more information about the lifestyle of the citizens of California, Arizona and Nevada, to better segment the market to fulfil their specific needs. However, we did find some important trends regarding these consumers already:

• Interest in wellness, health and conscious food choices • A continuing trend towards on-‐the-‐go consumption

Time-‐pressured consumers are interested in both fresh foods and ready-‐to-‐eat meals. These trends are particularly evident in California. In California there are 35million

6

people. In addition, customers regret that we do not offer a loyalty programs and therefore they might get loyal to competitors who do offer a loyalty program. After analysis, initial plans were to target an underserved niche in the marketplace, with our neighbourhood markets, to avoid the competition of large chains. It is believed that there is an unmet need between the convenience stores and the supermarkets. The convenience stores are small stores where people only buy some products like cigarettes, newspapers, etc. and supermarkets are big stores which people visit once a week and fill up there trolley. With Fresh & Easy our assortment is wider than convenience stores were we also sell fresh products and time-‐pressured consumers can buy their products easily. However, since customers of convenience stores typically shop for other product types than we offer, and demand and willingness to experiment with new store brands is low, consumers do not adopt our neighbourhood market concept very fast. To get a better insight in consumer demands and segments, more insight is needed in their shopping behaviours. Future research is recommended to reveal how consumers in California, Arizona and Nevada shop, and how that differs between different consumer groups. For example, more information regarding differences between customers of different ethnical origins or with different income levels could provide a better guideline for positioning our stores with regard to a target group.

3.2 Competitive factors Aaker (2007) described barriers to enter and the bargaining power of vendors in the market analysis and Levy & Weitz (2009) described this in the competitor analysis. As one of the forces of the five forces of Porter (Porter, 1979), we decided to put them in the market analysis, because in our opinion they are primarily relevant to the market instead of competitors. In the competitor analysis we only describe the competitive rivalry.

3.2.1 Competitive rivalry The grocery retailing industry in the U.S. includes many kind of formats from small convenience stores through supermarkets to big supercentres. In the U.S. there are about 35.000 supermarkets and almost every retailer sell some grocery items. Some analysts believe that the U.S. was over-‐stored. The result is intense price competition. But as described earlier, we noted a possible gap between convenience stores and supermarkets. The grocery retailing in California, Nevada and Arizona was not dominated by one chain. Important competitors groups for us are:

• Convenience stores: There are several thousand convenience stores in California (and Nevada and Arizona), including 1200 operated by 7-‐Eleven. Patrons of convenience stores were typically seeking out beer, cigarettes or a newspaper, rather than a salad.

• Supermarket chains: the most important supermarket chains in the U.S. are Kroger, Safeway and Supervalu, none of which commanded more than 15% of U.S. grocery sales. Kroger and Supervalu opened a lot of stores in 2009. An average supermarket has 47.000 items were families fill their trolley weekly.

7

• Other retailers: almost every retailer from drugstore to home improvement centres sold some grocery items.

Fresh & easy is closer in size to convenience stores that regular supermarkets. Some additional information about the leading players in grocery retailing in Southern California, where we want to launch Fresh & Easy, is:

• Ralph’s: a unit of Kroger with 263 supermarkets and 100 additional stores • Vons: a unit of Safeway with 260 stores • Albertsons: a unit of Supervalu with 135 stores • Stater Brothers: with 165 stores

Also important competitors are Whole Foods and Trader Joe’s. In California, Nevada and Arizona Wal-‐Mart has a lower penetration then in other states of the U.S. Most competitors in the U.S. depended on separate deliveries from multiple suppliers, but we decided to use our own truck fleet to receive deliveries from just a few sources. Wal-‐Mart, regarded as a logistic expert, employed a similar centralized model. Collecting more insight in the relative strengths and weaknesses is recommended in order to gat a better understanding of their competitive advantages. Concluded can be that Fresh & Easy has different kind of competitors to keep in mind when we position our stores in California, Arizona and Nevada to gain a competitive advantage. However, the reported impact of our stores on revenues of competitors so far is low.

3.3 Market factors In this section we will give an overview of the market factors, growth, seasonality and business cycle used by Levy & Weitz (2009) and the five forces of Porter described by Aaker (2007).

3.3.1 Growth The grocery market of the United States was estimated to be worth $600 billion in 2005 and was still growing. There is no specific information about the growth, but because of the rapidly growing population and the relative price inelasticity of this market, it seems reasonable to assume that the grocery retailing market grew right along with the population. Due to a lack of information about the states Nevada, Arizona and California, we have to assume that the same trend of growth also takes place there. Based on the size of the population of the United States and of the three states of Arizona, California and Nevada in 2005 and 2011, we value the grocery market of these states around $94 billion.

3.3.2 Seasonality Since we focus primarily on fresh produce, seasonality may be an issue for some products. Although we build upon a relationship between Tesco and two of its established U.K. suppliers, we should account for this seasonality factor particularly with

8

regard to local supply. Therefore, more insight is required in the seasonality effects of the different product groups.

3.3.3 Business cycle The grocery retailing market in its whole, does not suffer a lot from the economic recession. Economic analysts even believe that food retailers are relatively immune to economic conditions. However, a shift within the market from the premium to the discount stores can be observed. Extreme discount retailers benefited significantly from the new sense of frugality among American shoppers. Chains like Dollar General, Dollar Tree and Family Dollar were planning ambitious store openings for 2010.

3.3.4 Porters Five Forces model The Market profitability is analyzed using Porter’s Five Forces model (Porter, 1979):

• The threat of the entry of new competitors is rated as moderate. While entry barriers are high for complete chains, because of the enormous initial investment costs and high amount of required capital, they are relatively low for a single convenience store.

• The threat of substitute products is low. Almost all companies who are active on the grocery retail market are within the market definition. Only stores like gasoline retailers and drug stores are not part of our defined market, but their market share is relatively low.

• The bargaining power of customers is low. As said, there are no real alternatives to the grocery retail market and customers are relatively price insensitive: They need groceries.

• The bargaining power of suppliers is moderate. Since we use two established U.K. suppliers that have a good relationship with Tesco, their bargaining power is higher than the power of local suppliers in the current situation.

• The intensity of competition is high. A huge number of different types of stores and companies compete on this market and there are almost no sustainable advantages, because the current concepts can be copied easily.

Overall, the market profitability is relatively low. The average operating profit a U.S. supermarket realized was 2% to 3%. Looking at the analysis of Porter’s Five Forces in the grocery retail market, both low-‐cost structures and higher cost-‐structures can be successful. The distribution channels in the grocery retail market are the stores. There are a number of different types of stores, as is mentioned in the competitor analysis. These are convenience stores, supermarket chains and other retailers. In this market a number of trends can be recognized:

• The market is growing rapidly • Due to economic recession, customers change from premium chains to discount

chains, like Dollar General, Dollar Tree and Family Dollar • Intense price competition going on

9

3.4 Environmental factors Levy & Weitz (2009) give four environmental factors, which are used in the environmental analysis:

3.4.1 Technology There are no relevant technological developments in the current situation.

3.4.2 Economic In the beginning of 2010 the economic recession continued to hit the western U.S. hard. There is a lot of unemployment and most retailers were hurting in the economic downturn of 2008 and 2009. Only food retailers should be relatively immune for the recession. The recession might have decreased consumer demand and willingness to experiment with a new store brand. Retail spending was only increasing in 2010 among wealthier Americans. Besides this, the recession also reduced the cost of site leases and new stores construction.

3.4.3 Regulatory WIC vouchers (Women, Infants and Children’s government nutrition program) could Influence the choice of consumers for a specific chain, where these vouchers are accepted.

3.4.4 Social The population of California, Nevada and Arizona is rapidly growing and diverse, as demonstrated in the following demographic figures of the population in California of over 35 million people:

o Caucasians: 40 % o Hispanic-‐Americans: 37% o Asian-‐Americans: 12% o African-‐Americans: 6%

These three groups have a median household income well above the average income in the U.S.

3.5 Conclusion Some important opportunities derived from the external analysis are:

• There is an increasing consumer interest in wellness, health and conscious food choices.

• There is a growing diverse population with a trend towards on-‐the-‐go consumption.

• We target an underserved niche with Fresh & Easy to avoid the competition. • In these three states, California, Nevada and Arizona, there is no dominance by

any one chain and the Wal-‐Mart penetration is lower in these states than in other states of the U.S.

• Relatively low cost of site leases and new store construction and easy to obtain sites and planning permits for Fresh & Easy format stores.

10

Important threats are: • Intense price competition in U.S. because of large amount of stores • Economic recession in U.S. • Relatively low consumer demand and willingness to experiment with a new store

brand and customers are concerned about the lack of familiar brands at Fresh & Easy.

• U.S. shoppers are not very tolerant to stock outs and do not perceive prepackaged products a very fresh.

• Since customers value loyalty programs, they might get loyal to competitors offering a loyalty program

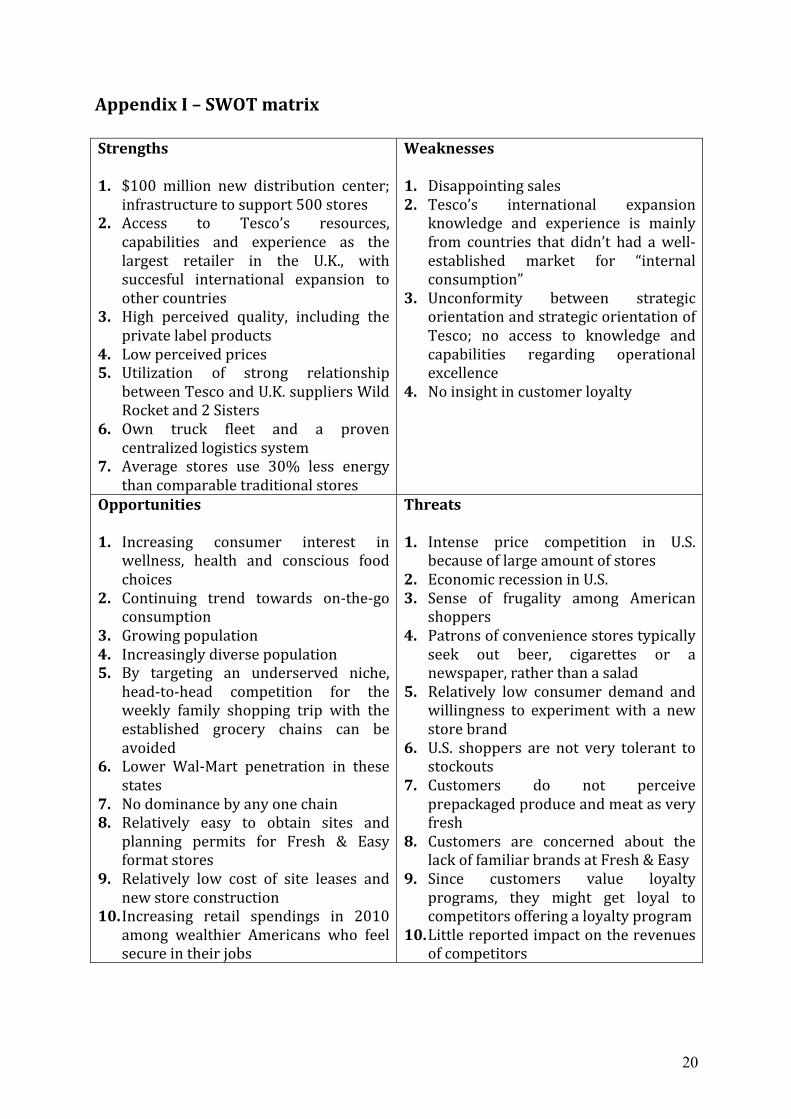

See appendix 1 for a complete overview of the opportunities and threats in the SWOT matrix.

4. Analysis of strengths and weaknesses When considering the internal situation of our venture, we revealed more insight in the strengths and weaknesses we are currently facing. Since our venture is part of Tesco, and we can use their resources, capabilities and experiences, we consider these aspects of Tesco as relevant for the internal situation at our Fresh & Easy venture.

4.1 Financial resources Our 2010 annual report, accounting our financial data for the fiscal year ending February 2010, states revenues of £349 million and a trading loss of £165 million, whereas an average U.S. supermarket has an operating profit of 2% to 3% of sales per year. However, we believe these losses are currently at their peak amount and will decrease in the future. Currently we are in the middle of a $2 billion plan for 5 years, with a short-‐term goal to open 200 stores throughout Arizona, California and Nevada before February 2009. This goal has not been achieved as at the time of writing only 126 stores have been opened. It seems important to maximize sales, but this is difficult because although the amount of visits projected for customers at Fresh & Easy is 75 as opposed to 59 visits per year for a typical U.S. supermarket, the projected spending per visit for a Fresh & Easy is on average $26 below the average spending of $41 at a supermarket. The revenue of one customer at Fresh & Easy is $1,125 per year, for a customer at a typical U.S. supermarket this amount is $2,419 per year. The prospected sales per week for each store are $200,000. Currently these sales per week per store come to an amount of $50,000 to $60,000, which is 75% below the prospected amount. Sales increase was estimated only 6% for the year 2011-‐2012. Because past investments are already spend and cannot be reversed, we have to consider them as sunk costs at should not account for these sunk costs with regard to our future decisions. Since we have access to the resource of Tesco, we still have access to sufficient resources. Although we are currently facing a recession in the U.S., economic analysts believe that our limited range of food products make us relatively immune for economic distress.

11

4.2 Management capabilities In addition to access to Tesco’s resources, we also have access to the capabilities and experience at Tesco. Following from their experience as a market leader in the U.K. and from successful international expansion to other countries, their capabilities and experience can be considered as a strength to our venture as well.

4.3 Locations With 126 stores, an ambitious plan to open more stores and a new a $100 million, state-‐of-‐the-‐art, distribution center that is able to supply 500 stores in the three states, location is an import aspect with regard to our future plans. However, more insight is needed to reveal customer perceptions of the locations of our stores.

4.4 Operations Regarding the operations of our stores, it can be considered as a strength that the average Fresh & Easy store uses 30% less energy than a comparable traditional store. We also can build on a centralized logistics model, with an own truck fleet, that is believed to be state of the art since logistic expert Wal-‐Mart uses a similar model. In addition, since we focus on a “ready to sell approach”, with prepackaged produce and meat, and shelf-‐ready container, this will result in smooth operations. However, since our orientation is focused more towards operational excellence and capabilities and experience at Tesco are more based on an emphasis on market leadership, there is incongruity between our strategic orientation and the strategic orientation of Tesco. This means that we cannot readily adopt Tesco’s management philosophy at our stores and may eventually lead to friction with regard to our internal organization.

4.5 Merchandising capabilities We did get positive customers reactions on our product quality and low prices, also for our private labels. Our assortment has a strong emphasis on private labels, fresh produce and prepared meals. In addition, we build on the good relationship between Tesco and U.K. suppliers Wild Rocket and 2 Sisters for a large part of our supplies.

4.6 Customer loyalty Customers of the Fresh & Easy mention that the stores have a “hospital-‐look”, because of the stark décor, the polished cement floors and white walls. Furthermore, we could not accept American Express and we have no customer loyalty program, something our customers disliked. Since we do not invested in information technology in our stores we currently have no insight in customer loyalty figures. When employing information technology such as a loyalty program we will likely be able to get better insight in consumer behavior. We already responded to some feedback received and for example adjusted store interior during last year. Moreover, we started promotions and displays in the stores and advertised on billboards, buses and radio programs, so we are putting effort in enhancing awareness already.

12

4.7 Conclusion Following from this internal focused analysis of the retail planning process, we derived the following key findings with regard to our strengths and weaknesses. A complete overview of the strengths and weaknesses can be found in the SWOT matrix in Appendix I. Key strengths:

• Access to Tesco’s resources, capabilities and experiences and relationship with U.K. suppliers

• Advanced distribution center, own truck fleet and a proven logistics model • High perceived quality and low perceived prices

Key weaknesses

• Disappointing sales • No alignment between strategic orientation of our venture and the strategic

orientation of Tesco • No insight in customer loyalty

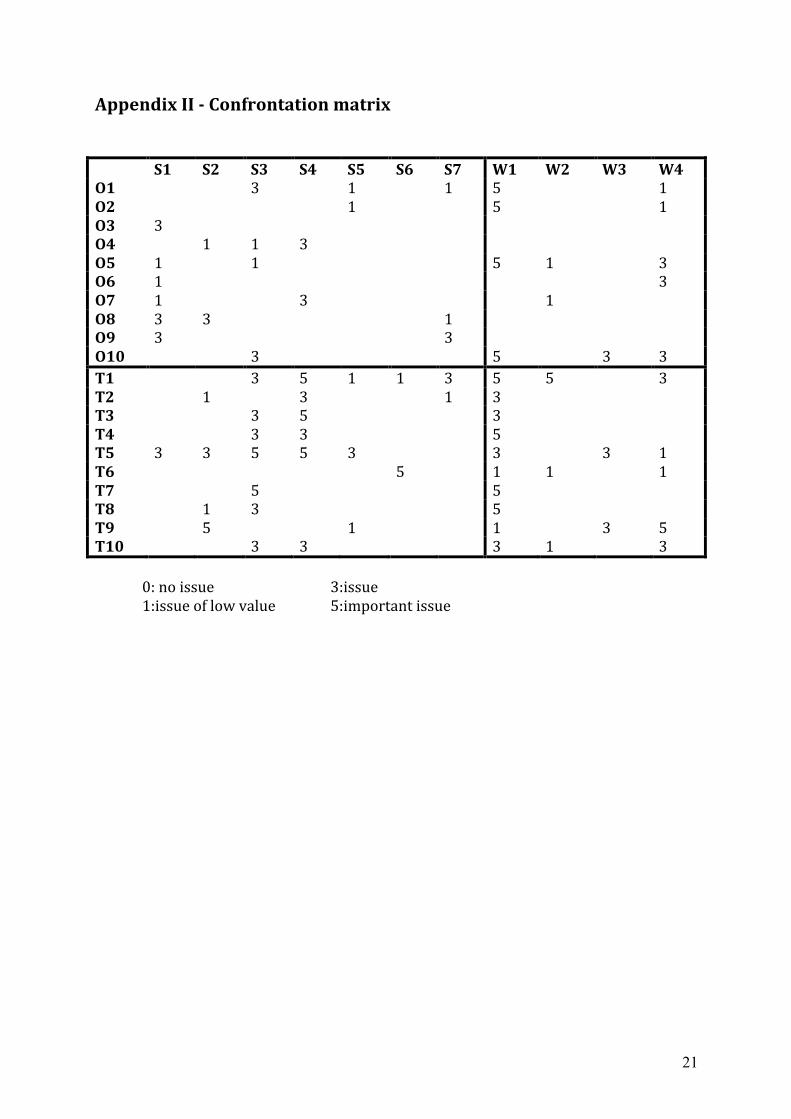

5. Issues The issues described here are based on our current position and the trends we found in regarding the external factors of our analysis. Following from our analysis, a SWOT matrix and a confrontation matrix are used in order to reveal what are relevant issues. These matrices can be found in Appendix I and II.

5.1 Consumer demands Before opening our first store, Tesco did some comprehensive field research and pre-‐testing in California. However, now more than 2 years later, we found that we do not sufficiently meet consumer demands which results in sales figures far below targeted sales. Even after our corrections during 2009, our stores still have only a small negative effect on the revenues of competitors. Customers, for example, are not very satisfied with our limited operating hours, whereas a lot of other U.S. retailers are opened 24-‐hours a day. Better meeting customer demands will in more favorability of our stores in the perception of customers and therefore in higher revenues. In addition, more insight in the positioning is also relevant with regard to this issue in order to see how they position themselves with regard to customer demands.

5.2 Awareness In order to increase revenues, people have to become more aware of our Fresh & Easy neighborhood markets. Although advertising was already increased during 2009, customers are likely still not very aware of our concept. Since customers are not that inclined to experiment with new store brands because of the recession, growing awareness of our Fresh & Easy will likely take some time. In addition, whereas

13

customers of convenience stores usually shop for beer, cigarettes and newspapers, they do not very fast adopt the concept of fresh food in our convenience-‐like neighborhood markets. Moreover, with our strong focus on our high quality private-‐label products, customers are concerned about familiar brands in our stores.

5.3 Invest or divest? Since sales are disappointing and the planned number of operating stores is not achieved, the question is whether to continue our Fresh & Easy venture or try to sell it. Earlier attempts by British competitors of Tesco to enter the U.S. market did not succeed, and they sold their U.S. subsidiaries. On the other hand, since California, Arizona and Nevada are growing markets, which are not dominated by a large supermarket chain, our Fresh & Easy venture may still be an opportunity to improve our current situation.

6. Strategic Options Following from the issues, we derived three strategic options as described in this section. Option 1: Stop Fresh & Easy

• W1, W2, W3, T1, T2, T4, T5, T10 The first option is that we stop our operations, and try to sell our venture. Of course, the ultimate decision with regard to whether to continue or quit is the responsibility of Tesco’s management. When they decide to leave the U.S., Tesco could use the resources now allocated to our venture for other projects. British competitors of Tesco previously failed to get a sustainable share in the U.S. market, and since the disappointing results of our stores we now should consider it as an option that Tesco should stop this attempt as well. Although we are nowadays faced with a recession, food retailers are believed to be relatively immune for these economic conditions. However, our targeted sales are not achieved and we have little impact on the sales of competitors. Adoption of our neighborhood markets concept and awareness are low. In addition, the U.S. retailing market, including the local grocery retailing market we operate in, is characterized by fierce price competition. Moreover, our format requires a different strategic orientation than Tesco’s market leadership orientation, which might be inconvenient for Tesco. Option 2: Continue with the Fresh & Easy-‐formula and introduce further improvements

• S1-‐S7, W4, O1-‐O3, O8, O9, T5-‐T9 The Fresh & Easy-‐formula has a number of great strengths, knowingly the high quality products, the low prices and the state-‐of-‐the-‐art distribution center. On first sight, these strengths should lead to a successful entry into the U.S. market. In reality, Fresh & Easy’s entry was not that successful, but by gathering customer feedback, a number of problems stood out: limited opening hours, the frequency of shelf stock outs, the lack of a customer reward program and low perceived freshness of prepackaged produce and meat. When better meeting customer demands, we are likely to better exploit our

14

strengths. Since we have access to the resources, capabilities and experience of Tesco, we could use for example its information technology in order to start a loyalty program at our stores to increase customer loyalty and to collect consumer purchase data to improve even more on meeting customer demands. Regarding consumer trends showing an increasing interest in wellness, health, conscious food and on-‐the-‐go-‐consumption, we should invest in convincing consumers that we offer what they want. Therefore, we should improve our concept to better suit customer needs, for example by obtaining new stores on convenient locations for customers. In addition, we should also increase our advertising budget in order to grow awareness of our store brand. Moreover, it is recommended that we establish a loyalty program to increase customer loyalty and gain more insights in customer behavior. Option 3: Change our formula

• S2, W1, W3, O3, O4, O6, O7, O10, T4, T5, T10 The last option is to stay active on the U.S. market, but with a new formula. Our Fresh & Easy-‐name has been out there for almost two and a half years and its brand image might have been negatively affected because of disappointing sales and customer complaints. Also, the gap between convenience stores and supermarkets that we intend to fill is likely not as large as expected earlier, which is also mentioned by analysts in the market. There is relatively low consumer demand and willingness to experiment with a new store brand and customers of convenience stores showed to be mainly interested in beer, cigarettes and newspapers instead of fresh food. Although perceived quality and low prices are positive among customers, our stores only had a small effect on competitors’ revenues. Therefore it can be concluded that the current concept did not had the expected effect. In addition, the strategic orientation of our formula does not match the strategic orientation of Tesco. Possibly there will be better synergy between our stores in the U.S. and Tesco when our strategic orientation is better aligned to the general orientation of Tesco. Moreover, forecasts show increasing retail spending in 2010 only among wealthier American, indicating an opportunity to change gears and approach the grocery retailing market in California, Arizona and Nevada from another perspective. Regarding the relatively low Wal-‐Mart population and lack of a dominant chain in this geographic market, this market may be still attractive for a new concept. Finally, the fast growing population in these states is becoming increasingly diverse, providing even more opportunities for other formulas that might work. Having access to Tesco’s resources, changing our concept to a different formula is feasible.

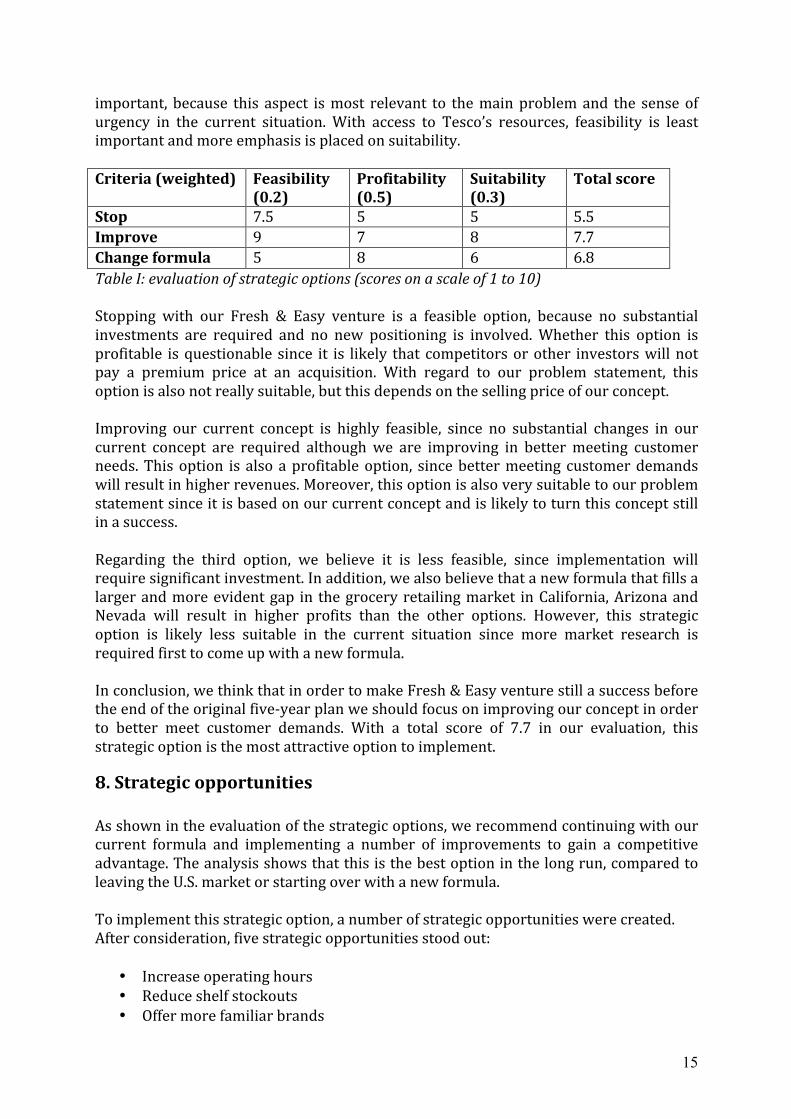

7. Evaluation of strategic options In order to evaluate which strategic option will be the best solution to the current situation we will consider our main problem statement first: How can our Fresh & Easy venture still become a success before the end of the original five-‐year plan? To get an answer on this question, we evaluated our strategic options with regard to their feasibility, profitability and their suitability. The weights assigned are respectively 0.2 for feasibility, 0.5 for profitability and 0.3 for suitability. Profitability scores are most

15

important, because this aspect is most relevant to the main problem and the sense of urgency in the current situation. With access to Tesco’s resources, feasibility is least important and more emphasis is placed on suitability. Criteria (weighted) Feasibility

(0.2) Profitability (0.5)

Suitability (0.3)

Total score

Stop 7.5 5 5 5.5 Improve 9 7 8 7.7 Change formula 5 8 6 6.8 Table I: evaluation of strategic options (scores on a scale of 1 to 10) Stopping with our Fresh & Easy venture is a feasible option, because no substantial investments are required and no new positioning is involved. Whether this option is profitable is questionable since it is likely that competitors or other investors will not pay a premium price at an acquisition. With regard to our problem statement, this option is also not really suitable, but this depends on the selling price of our concept. Improving our current concept is highly feasible, since no substantial changes in our current concept are required although we are improving in better meeting customer needs. This option is also a profitable option, since better meeting customer demands will result in higher revenues. Moreover, this option is also very suitable to our problem statement since it is based on our current concept and is likely to turn this concept still in a success. Regarding the third option, we believe it is less feasible, since implementation will require significant investment. In addition, we also believe that a new formula that fills a larger and more evident gap in the grocery retailing market in California, Arizona and Nevada will result in higher profits than the other options. However, this strategic option is likely less suitable in the current situation since more market research is required first to come up with a new formula. In conclusion, we think that in order to make Fresh & Easy venture still a success before the end of the original five-‐year plan we should focus on improving our concept in order to better meet customer demands. With a total score of 7.7 in our evaluation, this strategic option is the most attractive option to implement.

8. Strategic opportunities As shown in the evaluation of the strategic options, we recommend continuing with our current formula and implementing a number of improvements to gain a competitive advantage. The analysis shows that this is the best option in the long run, compared to leaving the U.S. market or starting over with a new formula. To implement this strategic option, a number of strategic opportunities were created. After consideration, five strategic opportunities stood out:

• Increase operating hours • Reduce shelf stockouts • Offer more familiar brands

16

• Location convenience • Loyalty program

8.1 Increase operating hours Consumers mentioned the limited opening hours of Fresh & Easy as a reason not to shop at Fresh & Easy. Fresh & Easy-‐stores are typically open from 8 a.m. to 9 p.m., while most U.S. retailers are open 24 hours a day. This opportunity is relatively easy to implement and can persuade consumers to do their shopping at Fresh & Easy. The current staff has to be convinced to work during these hours and new staff has to be found. Also, the distribution of goods has to be altered, which will be described next. The objective of this opportunity is to get more customers into the store and increase sales. We can measure this by looking if the amount of customers and the amount of sales is increasing when we are open for 24 hours instead of 13 hours a day. The investment we have to do for this opportunity is mainly for employees. We can introduce this opportunity within one month when we have arranged it with the employees. When we are open for 24 hours a day, we can directly start with the measurement and look at the results after one month.

8.2 Reduce shelf stockouts Another disadvantage of the current Fresh & Easy-‐stores are the relative high frequency of shelf stockouts. This follows from the ‘British’ way of doing, where the store is restocked after opening hours. British customers accept this and go back a day later to get their products, but U.S. shoppers don’t. As mentioned before, Fresh & Easy should also change their opening hours and be open 24 hours a day. This has important implications for the way and time of restocking. Goods should be coming in from the distribution centre and be put on the shelves all day long, not just at night. This way, the frequency of shelf stockouts should be reduced significantly. Because Tesco persuaded one of its U.K. suppliers, Wild Rocket, to set up a distribution centre near our stores, and Tesco has strong ties of with this supplier, it should be possible to change the way and times of distribution from Wild Rocket to our distribution centre. We have our own truck fleet, which makes it easier to deliver goods to the stores at the right times. Possibly, a JIT-‐strategy could be implemented, thereby reducing both shelf stockouts and storage costs. At first, the implementation of this opportunity might not have a great effect, but in time it will persuade customers who left because of the frequency of shelf stockouts, to come back to the Fresh & Easy-‐stores. The objective is to reduce shelf stockouts and this keeps customers. Some solutions for this problem are already given, but this takes some time to solve this opportunity. We would like to achieve this as soon as possible.

8.3 Offer more familiar brands Research has shown that consumers long for a fit of products with personal preferences (Clemons & Nunes, 2011). A supermarket with a long tail, in other words a high variety of produce, has a greater chance of attracting a customer looking for a certain brand of

17

produce. We believe that when we increase brands that are more familiar at our Fresh & Easy stores, and thus increase the long tail of our assortment; we will be able to sell more of our private-‐label and fresh produce. We do not believe that the assortment should be increased in a way that all focus moves away from our own brand, but an expansion of the assortment with brands that are often sought for in competitor’s stores can help to bring customers in. Also Ailawadi (2004) stated that it is important for retailers to retain a balance between store brands and national brands to attract and retain the most profitable customers. We want to offer more familiar brands within six months, but a lot of investments need to be done. For example, familiar brands need to be bought, but more important are the promotion cost. When more familiar brands are in the shop, we can measure if this influences the amount of customers and their spending.

8.4 Location convenience ‘What are the three most important things in retailing? Location, location, location’ (Levy & Weitz, 2009). To be successful, the location of a store is of great importance. To make Fresh & Easy a success, we have to put a lot of effort in choosing the right locations for our stores. Previously, in some cases, Fresh & Easy took over vacant pre-‐existing drugstore locations, because it was convenient and relatively cheap. However, it’s reasonable to doubt if these locations really fitted our strategy. In the future, Fresh & Easy should choose specific locations that fit the strategy. Research should be done, by using geodemographic data, to see which locations perform best on factors like accessibility, traffic flow, distance to consumers and quality of the environment (Campo & Gijsbrechts, 2004; Levy & Weitz, 2009). This opportunity does not need extra investments only some extra costs in doing research about where to open a new store. When we want to buy new sites to open Fresh & Easy stores, we have to do research about what is a good place. This will take some time, but can be used for other times, when we want to open a new store.

8.5 Loyalty program A good opportunity to develop a competitive advantage is to start a loyalty program. Loyalty programs are part of an overall customer relationship management program. Members of loyalty programs are identified when they buy, because they use some type of loyalty card. The purchase information of these customers is stored in a huge database and from this database we can analyze what types of merchandise and services certain groups of customers are buying. With this information we can better meet the needs of our customers (Levi & Weitz, 2009). It will be costly to introduce a loyalty program and it will take some time to develop this program. The goal is to have a loyalty program within eight months.

9. Conclusion Our first Fresh & Easy store in the United States was opened about 2.25 years ago. Unfortunately the results of the Fresh & Easy venture are disappointing. Targeted sales are not achieved, impact on the revenues of competitors is low and sales growth forecasts are marginal, even after corrections to the original plan during the past year. In

18

order to find an answer on these disappointing results we developed the following problem statement:

• How can our Fresh & Easy venture still become a success before the end of the original five-‐year plan?

To find an answer on this question we first did an internal and external analysis. During the analysis, we found an answer on the following question.

• Are the disappointing results of Fresh & Easy in the past 2.25 years a consequence of the economic recession in the western U.S., a wrong strategy or bad implementation?

The answer we found is that the disappointing results is not a consequence of the economic recession, but we miss some important opportunities in the current strategy in the retail industry in the U.S to gain a competitive advantage. The analysis resulted in a confrontation matrix and three options; stop with Fresh & Easy, continue with Fresh & Easy, but improve some points, or start another formula. It is recommended to continue with Fresh & Easy, but we have to implement the opportunities that will gain a competitive advantage. This gives us an answer on the third question.

• How can Fresh & Easy adjust better to customer needs?

The five opportunities we have to implement to better meet the needs of the customers and gain a competitive advantage are; increase operating hours, reduce shelf stock outs, offer more familiar brands, location and loyalty program. So, Fresh & Easy becomes a success before the end of the five-‐year plan by implementing these five opportunities.

19

10. References Aaker, D.A. & McLoughlin, D. (2007), “Strategic Market Management”, Chichester: Wiley

& Sons. Abell, Derek F. (1980), “Defining the business: the starting point of strategic planning”,

New Jersey: Prentice Hall. Ailawadi, K & Harlam, B. (2004) An emperical analysis of the determinants of the retail

margins: the role of store-‐brand share, Journal of marketing, 68:147-‐165 Campo, K., & Gijsbrechts, E. (2004). Should retailers adjust their micromarketing

strategies to type of outlet? An application to location-‐based store space allocation in limited and full-‐service grocery stores. Journal of Retailing and Consumer Services, 11: 369-‐383.

Clemons, E.K., Nunes, P.F., 2011. Carrying your long tail: Delighting your consumers and

managing your operations. Decision Support Systems, 51(4): 884-‐893. Levy, M. & Weitz, B.A. (2009), “Retailing management”, New York: Mc Graw Hill. Porter, Michael. E. (1979), ‘How competitive forces shape strategy’, Harvard Business

Review, 57(2): 137-‐145.

20

Appendix I – SWOT matrix Strengths 1. $100 million new distribution center;

infrastructure to support 500 stores 2. Access to Tesco’s resources,

capabilities and experience as the largest retailer in the U.K., with succesful international expansion to other countries

3. High perceived quality, including the private label products

4. Low perceived prices 5. Utilization of strong relationship

between Tesco and U.K. suppliers Wild Rocket and 2 Sisters

6. Own truck fleet and a proven centralized logistics system

7. Average stores use 30% less energy than comparable traditional stores

Weaknesses 1. Disappointing sales 2. Tesco’s international expansion

knowledge and experience is mainly from countries that didn’t had a well-‐established market for “internal consumption”

3. Unconformity between strategic orientation and strategic orientation of Tesco; no access to knowledge and capabilities regarding operational excellence

4. No insight in customer loyalty

Opportunities 1. Increasing consumer interest in

wellness, health and conscious food choices

2. Continuing trend towards on-‐the-‐go consumption

3. Growing population 4. Increasingly diverse population 5. By targeting an underserved niche,

head-‐to-‐head competition for the weekly family shopping trip with the established grocery chains can be avoided

6. Lower Wal-‐Mart penetration in these states

7. No dominance by any one chain 8. Relatively easy to obtain sites and

planning permits for Fresh & Easy format stores

9. Relatively low cost of site leases and new store construction

10. Increasing retail spendings in 2010 among wealthier Americans who feel secure in their jobs

Threats 1. Intense price competition in U.S.

because of large amount of stores 2. Economic recession in U.S. 3. Sense of frugality among American

shoppers 4. Patrons of convenience stores typically

seek out beer, cigarettes or a newspaper, rather than a salad

5. Relatively low consumer demand and willingness to experiment with a new store brand

6. U.S. shoppers are not very tolerant to stockouts

7. Customers do not perceive prepackaged produce and meat as very fresh

8. Customers are concerned about the lack of familiar brands at Fresh & Easy

9. Since customers value loyalty programs, they might get loyal to competitors offering a loyalty program

10. Little reported impact on the revenues of competitors

21

Appendix II -‐ Confrontation matrix S1 S2 S3 S4 S5 S6 S7 W1 W2 W3 W4 O1 3 1 1 5 1 O2 1 5 1 O3 3 O4 1 1 3 O5 1 1 5 1 3 O6 1 3 O7 1 3 1 O8 3 3 1 O9 3 3 O10 3 5 3 3 T1 3 5 1 1 3 5 5 3 T2 1 3 1 3 T3 3 5 3 T4 3 3 5 T5 3 3 5 5 3 3 3 1 T6 5 1 1 1 T7 5 5 T8 1 3 5 T9 5 1 1 3 5 T10 3 3 3 1 3

0: no issue 3:issue 1:issue of low value 5:important issue