![Q3 - FY16 Results [Company Update]](https://static.fdocuments.in/doc/165x107/577ca4dc1a28abea748b4c27/q3-fy16-results-company-update.jpg)

Results update – Q4FY08

20

Results update – Q4FY08 April 28, 2008

Transcript of Results update – Q4FY08

Results update – Q4FY08April 28, 2008

2

• Performance highlights- Q4 FY08

• Business review

• Future plans and strategy

• Corporate overview

• Industry overview

Presentation structure

Unless otherwise mentioned, facts and figures in this presentation refer to those for the India Infoline group (consolidated)

Financial performance highlights

Highlights

Dividend proposed- Rs6 per share, up 100% over previous yearStock split proposed- 1 share of Rs10 into 5 shares of Rs2 eachFull year Income crosses Rs10 billion mark, up 140% yoyFull year net profit (prior to exceptional items) at Rs1.89bn, up 150% yoyQuarterly Income at Rs3.84 billion, up 169% yoyQuarterly post tax net profit at Rs0.66 billion, up 168% yoyEBIDTA margin for the year was 39.3% compared to 33.2% in the previous yearAverage daily equity trading turnover in FY08, up 190% to Rs 24.3 bnMarket share on NSE up to 3.4% in FY08 compared to 2.2% in FY07 Insurance mobilization Rs 4.47 bn up 24% y-yCommodities average daily volumes up 44% to Rs 1.8 bn. Market share up to 1.4% from 1.1% in FY07Mutual Funds income up 27% to Rs 1.9 bn due to higher focus on equity MFsSignificant growth in lending business and financing income tripled qoq.

Performance highlights – Q4FY08

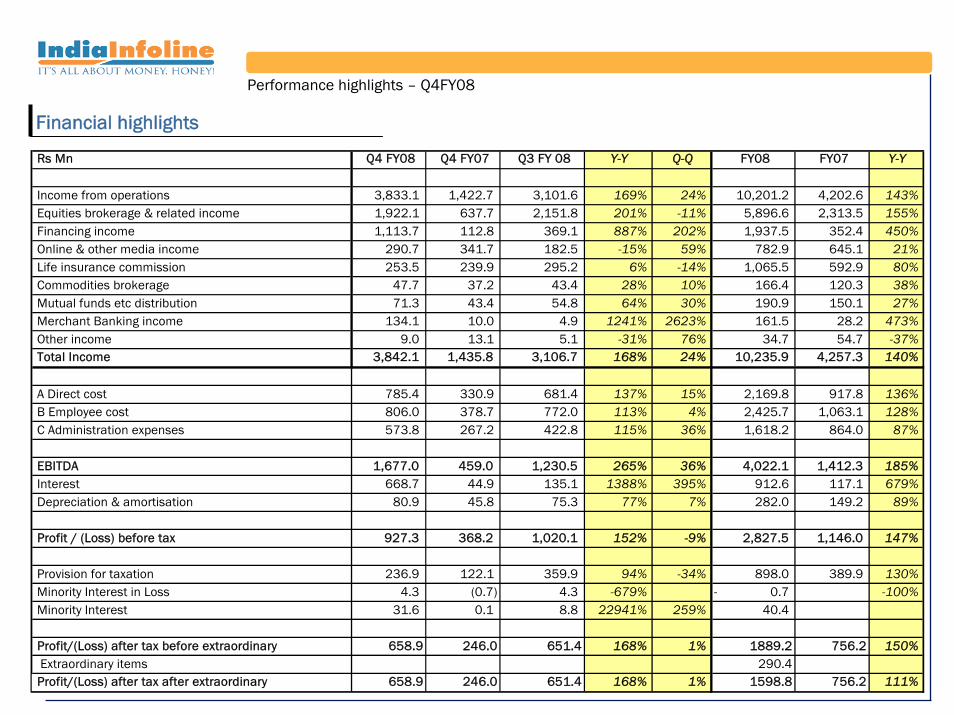

Financial highlights

Performance highlights – Q4FY08

Rs Mn Q4 FY08 Q4 FY07 Q3 FY 08 Y-Y Q-Q FY08 FY07 Y-Y

Income from operations 3,833.1 1,422.7 3,101.6 169% 24% 10,201.2 4,202.6 143%Equities brokerage & related income 1,922.1 637.7 2,151.8 201% -11% 5,896.6 2,313.5 155%Financing income 1,113.7 112.8 369.1 887% 202% 1,937.5 352.4 450%Online & other media income 290.7 341.7 182.5 -15% 59% 782.9 645.1 21%Life insurance commission 253.5 239.9 295.2 6% -14% 1,065.5 592.9 80%Commodities brokerage 47.7 37.2 43.4 28% 10% 166.4 120.3 38%Mutual funds etc distribution 71.3 43.4 54.8 64% 30% 190.9 150.1 27%Merchant Banking income 134.1 10.0 4.9 1241% 2623% 161.5 28.2 473%Other income 9.0 13.1 5.1 -31% 76% 34.7 54.7 -37%Total Income 3,842.1 1,435.8 3,106.7 168% 24% 10,235.9 4,257.3 140%

A Direct cost 785.4 330.9 681.4 137% 15% 2,169.8 917.8 136%B Employee cost 806.0 378.7 772.0 113% 4% 2,425.7 1,063.1 128%C Administration expenses 573.8 267.2 422.8 115% 36% 1,618.2 864.0 87%

EBITDA 1,677.0 459.0 1,230.5 265% 36% 4,022.1 1,412.3 185%Interest 668.7 44.9 135.1 1388% 395% 912.6 117.1 679%Depreciation & amortisation 80.9 45.8 75.3 77% 7% 282.0 149.2 89%

Profit / (Loss) before tax 927.3 368.2 1,020.1 152% -9% 2,827.5 1,146.0 147%

Provision for taxation 236.9 122.1 359.9 94% -34% 898.0 389.9 130%Minority Interest in Loss 4.3 (0.7) 4.3 -679% 0.7- -100%Minority Interest 31.6 0.1 8.8 22941% 259% 40.4

Profit/(Loss) after tax before extraordinary 658.9 246.0 651.4 168% 1% 1889.2 756.2 150% Extraordinary items 290.4

Profit/(Loss) after tax after extraordinary 658.9 246.0 651.4 168% 1% 1598.8 756.2 111%

Profit After Tax

Profit Before Tax

Revenues

EBIDTA margins

Performance in pictures

Performance highlights – Q4FY08

Profit After Tax (Rs Mn)

879

EBIDTA Margins(%)Profit Before Tax (Rs Mn)

Revenues (Rs Mn)

Mar-08Mar-06 Jun-06 Sep-06 Dec-06 Mar-07 Jun-07 Sep-07 Dec-070

1000

2000

3000

4000

0

100

200

300

400

500

600

700

Mar-08Mar-06 Jun-06 Sep-06 Dec-06 Mar-07 Jun-07 Sep-07 Dec-07

168187

133172

246

368 361

651 659

7881,136

1,436 1,334

1,953

3,107

3,842

857

0

200

400

600

800

1000

1200

Mar-08Mar-06 Jun-06 Sep-06 Dec-06 Mar-07 Jun-07 Sep-07 Dec-07

255298

201260

368 343

537

1020927

0

5

10

15

20

25

30

35

40

45

50

Mar-08Mar-06 Jun-06 Sep-06 Dec-06 Mar-07 Jun-07 Sep-07 Dec-07

3841

3129

32 33 34

4044

6

• Performance highlights- Q4 FY08

• Business review

• Future plans and strategy

• Corporate overview

• Industry overview

Presentation structure

Unless otherwise mentioned, facts and figures in this presentation refer to those for the India Infoline group (consolidated)

7

Downturn in the capital markets triggered by sub-prime woes and global inflationary pressuresMarket share on NSE at 3.6% in Q4Average daily turnover declines 29% QoQ to Rs 26.7 bn in line with marketWe will continue expansion of network and investment in technology, systems and processes

Equities broking (Cash & FAO)

Business review

Equities broking

IIL market share

IIL locations

4580

152

568

758

0

100

200

300

400

500

600

700

800

2004 2005 2006 2007 2008

Business locations (branches & sub-brokers)

Equities Brokerage Rs Mn (LHS)

Av. Daily Vol (Rs.Mn)

542 568 499606 641 693

1128

2152

1922

0

500

1000

1500

2000

2500

Mar-06 Jun-06 Sep-06 Dec-06 Mar-07 Jun-07 Sep-07 Dec-07 Mar-080

5000

10000

15000

20000

25000

30000

35000

40000

1.90%

3.6%

1.3%

1.9%

2.6%

3.2%

3.8%

Mar-06 Jun-06 Sep-06 Dec-06 Mar-07 Jun-07 Sep-07 Dec-07 Mar-08

NSE Market Share

Institutional equities

Rapid ramp-up: 60-strong institutional equities team Healthy gains in market share; have done some large block placements during the yearEmpanelled with most large global institutional investors, domestic institutionsInstitutional research team of 25 analysts, with a blend of industry and equity research experience Daily product, The Front Page, launched in October 2007More than 120 stocks under coverage“Inside India” – a differentiating product comprising a series of India maps, released in March 2008

Some of our research products

25 maps of opportunities and challengesBusiness review

9

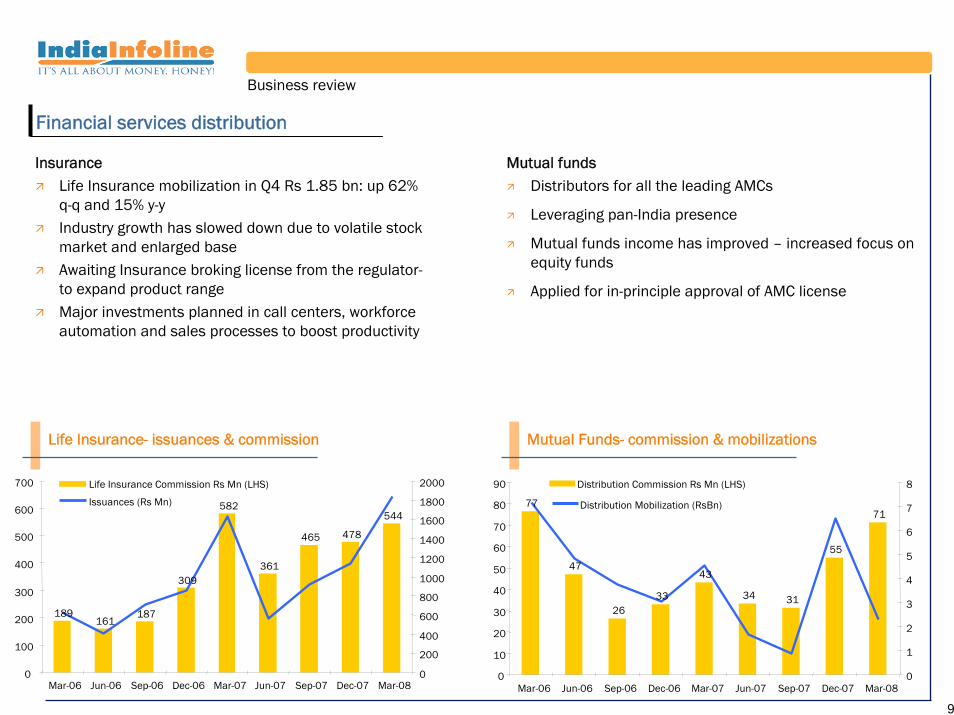

InsuranceLife Insurance mobilization in Q4 Rs 1.85 bn: up 62% q-q and 15% y-yIndustry growth has slowed down due to volatile stock market and enlarged baseAwaiting Insurance broking license from the regulator-to expand product range Major investments planned in call centers, workforce automation and sales processes to boost productivity

Mutual Funds- commission & mobilizationsLife Insurance- issuances & commission

Financial services distribution

Mutual fundsDistributors for all the leading AMCs

Leveraging pan-India presence

Mutual funds income has improved – increased focus on equity funds

Applied for in-principle approval of AMC license

Business review

Distribution Commission Rs Mn (LHS)

Distribution Mobilization (RsBn)

Life Insurance Commission Rs Mn (LHS)

Issuances (Rs Mn)

189161

187

309

582

361

465 478

544

0

100

200

300

400

500

600

700

Mar-06 Jun-06 Sep-06 Dec-06 Mar-07 Jun-07 Sep-07 Dec-07 Mar-080

200

400

600

800

1000

1200

1400

1600

1800

2000

77

47

2633

43

34 31

55

71

0

10

20

30

40

50

60

70

80

90

Mar-06 Jun-06 Sep-06 Dec-06 Mar-07 Jun-07 Sep-07 Dec-07 Mar-080

1

2

3

4

5

6

7

8

10

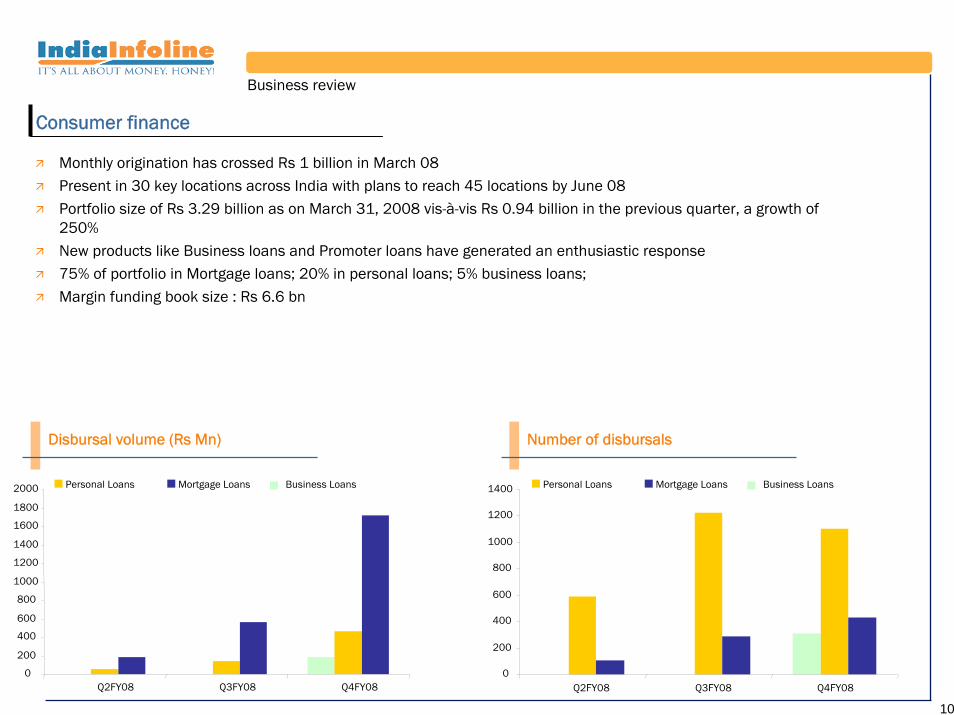

Monthly origination has crossed Rs 1 billion in March 08 Present in 30 key locations across India with plans to reach 45 locations by June 08Portfolio size of Rs 3.29 billion as on March 31, 2008 vis-à-vis Rs 0.94 billion in the previous quarter, a growth of 250%New products like Business loans and Promoter loans have generated an enthusiastic response75% of portfolio in Mortgage loans; 20% in personal loans; 5% business loans; Margin funding book size : Rs 6.6 bn

Consumer finance

Business review

Number of disbursalsDisbursal volume (Rs Mn)

Personal Loans Mortgage Loans

0

200

400

600

800

1000

1200

1400

1600

1800

2000

Q2FY08 Q3FY08 Q4FY08

Business Loans

0

200

400

600

800

1000

1200

1400

Q2FY08 Q3FY08 Q4FY08

Personal Loans Mortgage Loans Business Loans

11

• Performance highlights- Q4 FY08

• Business review

• Future plans and strategy

• Corporate overview

• Industry overview

Presentation structure

Unless otherwise mentioned, facts and figures in this presentation refer to those for the India Infoline group (consolidated)

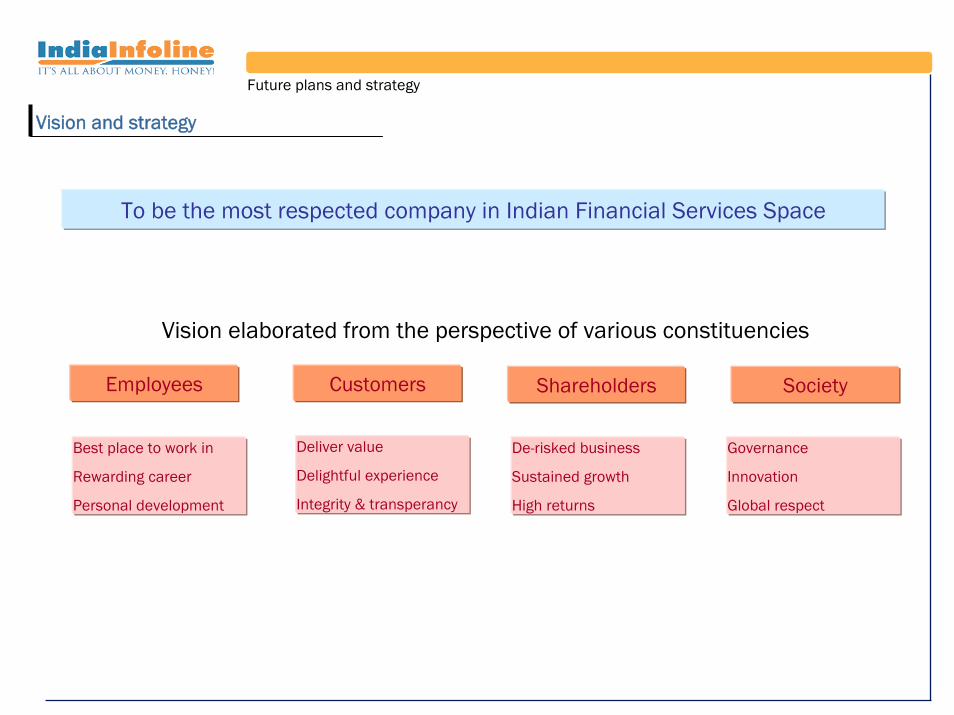

Vision and strategy

Future plans and strategy

To be the most respected company in Indian Financial Services Space

Employees Customers Shareholders Society

Best place to work in

Rewarding career

Personal development

Deliver value

Delightful experience

Integrity & transperancy

De-risked business

Sustained growth

High returns

Governance

Innovation

Global respect

Vision elaborated from the perspective of various constituencies

Business plan

One stop shop for all financial services productsDe-risking business model but not drifting from the coreCritical mass in all key businesses

Strong focus on risk management and complianceBetting on people with proven credentialsFocus on efficient use of capital

Future plans and strategy

Assetmanagement

Investmentbanking

Consumerfinance

Wealthmanagement

Institutionalequities

Life insurance

Retail broking

Financial Services

14

• Performance highlights- Q4 FY08

• Business review

• Future plans and strategy

• Corporate overview

• Industry overview

Presentation structure

Unless otherwise mentioned, facts and figures in this presentation refer to those for the India Infoline group (consolidated)

1995 Incorporated as an Equity Research & Consulting firm

1999Changed business model to embrace the Internet and launch www.indiainfoline.com

2000Started distribution of personal financial products

Launched online equity trading through www.5paisa.com

Started life insurance distribution as Corporate Agent

2005

2004Acquired Commodities broking license

Launched Portfolio Management Service

Debuted on the Indian stock marketsLaunched proprietary trading platform Trader Terminal

2006Acquired membership of DGCXLaunched Wealth Advisory Services

2007CLSA Institutional equities team joins

Formed Singapore subsidiary IIFL (Asia) Pte Ltd

Client base included leading FIIs, Banks, Consulting firms & Corporates

First round of capital raising from reputed Private Equity investors

Evolution

Equity dilution in parent and subsidiaries to raise about USD268Mn

2008Wealth Management launched under the IIFL Wealth brand

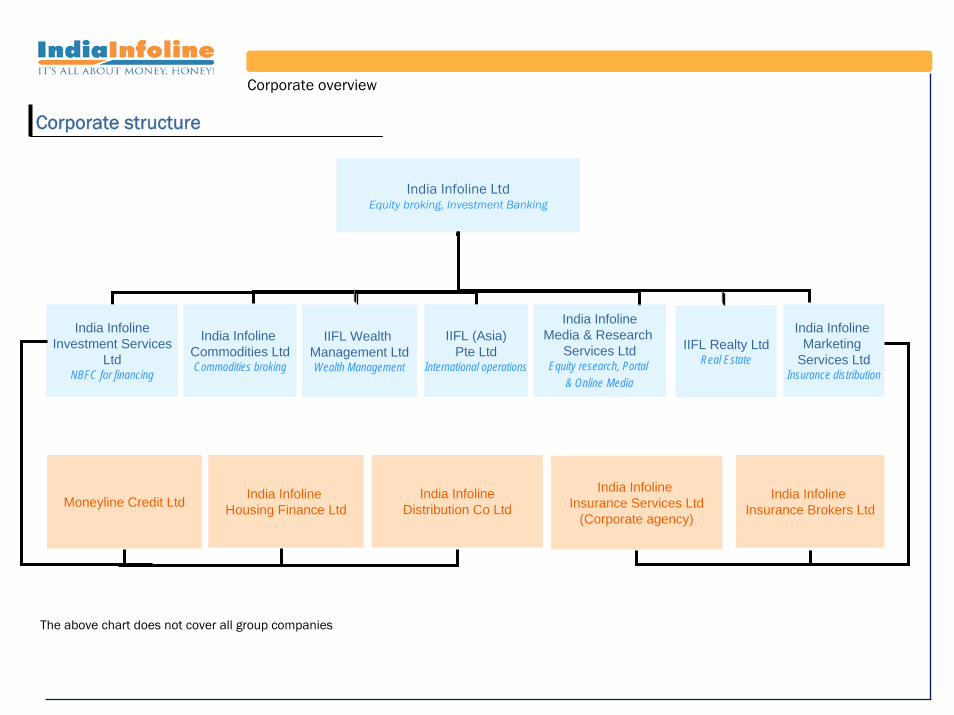

Corporate overview

India Infoline LtdEquity broking, Investment Banking

India InfolineInvestment Services

LtdNBFC for financing

India Infoline Commodities LtdCommodities broking

IIFL (Asia)Pte Ltd

International operations

India InfolineMedia & Research

Services LtdEquity research, Portal

& Online Media

India Infoline Marketing

Services LtdInsurance distribution

India Infoline Housing Finance LtdMoneyline Credit Ltd India Infoline

Distribution Co LtdIndia Infoline

Insurance Brokers Ltd

India Infoline Insurance Services Ltd

(Corporate agency)

IIFL Wealth Management LtdWealth Management

IIFL Realty LtdReal Estate

The above chart does not cover all group companies

Corporate structure

Corporate overview

17

• Performance highlights- Q4 FY08

• Business review

• Future plans and strategy

• Corporate overview

• Industry overview

Presentation structure

Unless otherwise mentioned, facts and figures in this presentation refer to those for the India Infoline group (consolidated)

Industry overview

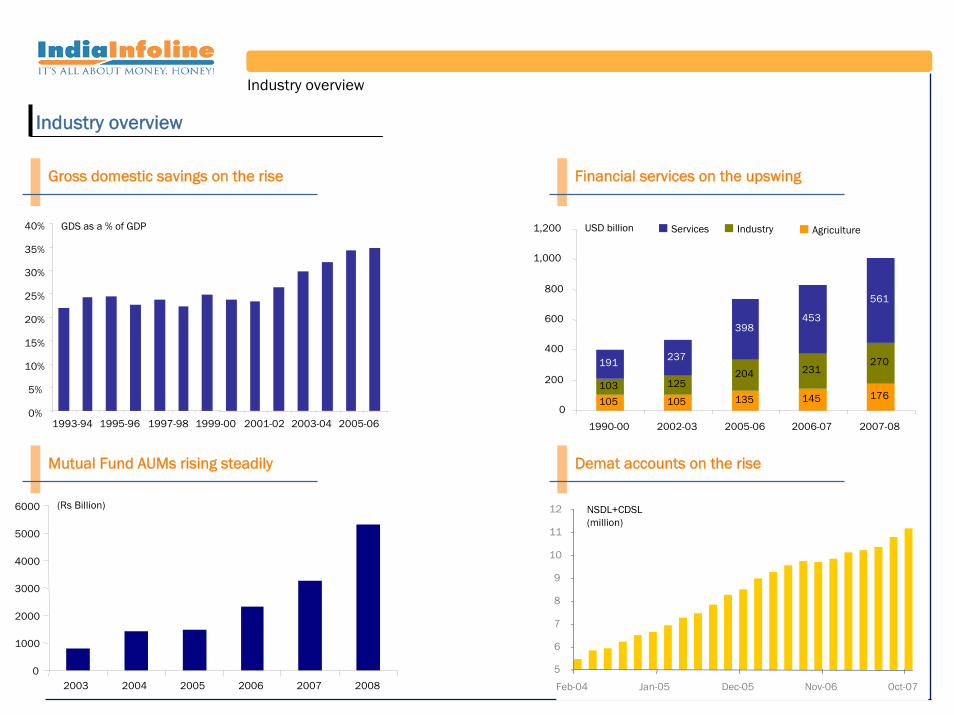

Industry overview

Gross domestic savings on the rise

Mutual Fund AUMs rising steadily

Financial services on the upswing

105 105 135 145 176103 125

204 231270191 237

398453

561

0

200

400

600

800

1,000

1,200

1990-00 2002-03 2005-06 2006-07 2007-08

Services Industry Agriculture

0

1000

2000

3000

4000

5000

6000

2003 2004 2005 2006 2007 2008

(Rs Billion)

0%

5%

10%

15%

20%

25%

30%

35%

40%

1993-94 1995-96 1997-98 1999-00 2001-02 2003-04 2005-06

GDS as a % of GDP USD billion

Demat accounts on the rise

5

6

7

8

9

10

11

12

Feb-04 Jan-05 Dec-05 Nov-06 Oct-07

NSDL+CDSL (million)

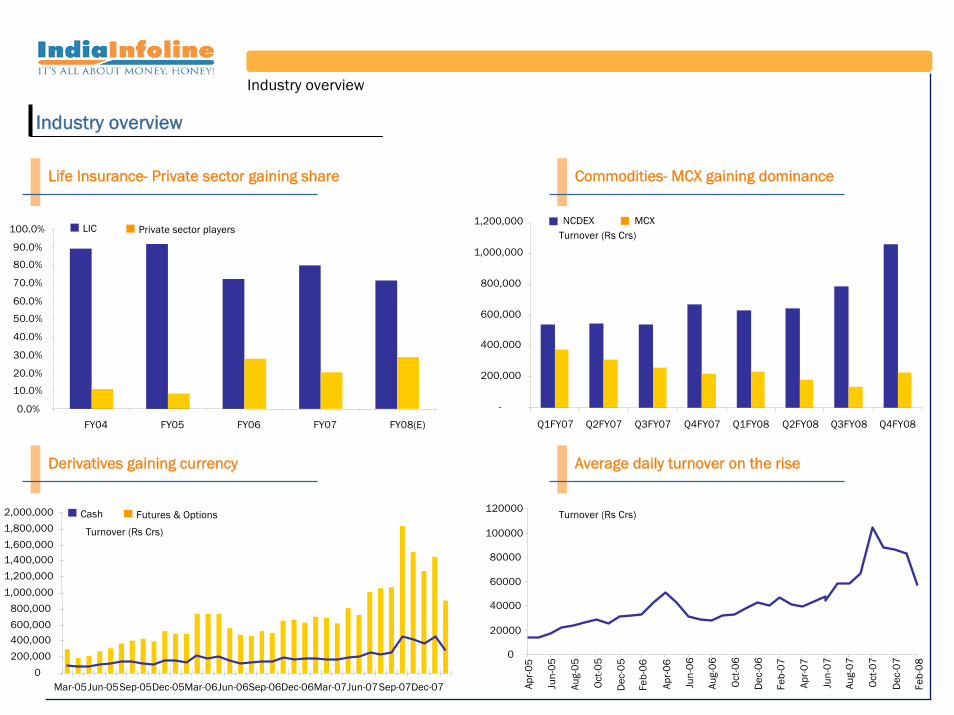

Life Insurance- Private sector gaining share

Derivatives gaining currency

Commodities- MCX gaining dominance

Average daily turnover on the rise

Industry overview

Industry overview

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

100.0%

FY04 FY05 FY06 FY07 FY08(E)

LIC Private sector players

-

200,000

400,000

600,000

800,000

1,000,000

1,200,000

Q1FY07 Q2FY07 Q3FY07 Q4FY07 Q1FY08 Q2FY08 Q3FY08 Q4FY08

NCDEX MCXTurnover (Rs Crs)

0

200,000

400,000600,000

800,000

1,000,000

1,200,000

1,400,0001,600,000

1,800,000

2,000,000

Mar-05Jun-05Sep-05Dec-05Mar-06Jun-06Sep-06Dec-06Mar-07Jun-07Sep-07Dec-07

Cash Futures & Options

Turnover (Rs Crs)

0

20000

40000

60000

80000

100000

120000

Apr-0

5

Jun-

05

Aug-

05

Oct

-05

Dec

-05

Feb-

06

Apr-0

6

Jun-

06

Aug-

06

Oct

-06

Dec

-06

Feb-

07

Apr-0

7

Jun-

07

Aug-

07

Oct

-07

Dec

-07

Feb-

08

Turnover (Rs Crs)

20

Thank you

Published in April 2008. © India Infoline Ltd 2008-09.

India Infoline Ltd. All rights reserved. Regd. Off: 75, Nirlon Complex, Off W E Highway, Goregaon (E) Mumbai-400 063. Tel.: +(91 22)6677 5900 Fax: 2685 0451.

This report is for information purposes only and does not construe to be any investment, legal or taxation advice. It is not intended as an offer or solicitation for the purchase and sale of any financial instrument. Any action taken by you on the basis of the information contained herein is your responsibility alone and India Infoline Ltd (hereinafter referred as IIL) and its subsidiaries or its employees or directors, associates will not be liable in any manner for the consequences of such action taken by you. We have exercised due diligence in checking the correctness and authenticity of the information contained herein, but do not represent that it is accurate or complete. IIL or any of its subsidiaries or associates or employees shall not be in any way responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this publication. The recipients of this report should rely on their own investigations. IIL and/or its subsidiaries and/or directors, employees or associates may have interests or positions, financial or otherwise in the securities mentioned in this report.

![Financial Results with Results Press Release, Investor Update & Limited Review Report for June 30, 2015 [Company Update]](https://static.fdocuments.in/doc/165x107/577cb40d1a28aba7118c46c3/financial-results-with-results-press-release-investor-update-limited-review.jpg)

![Results Press Release [Company Update]](https://static.fdocuments.in/doc/165x107/5695cedc1a28ab9b028b8547/results-press-release-company-update-56a6ce492878c.jpg)

![Results of EGM [Company Update]](https://static.fdocuments.in/doc/165x107/577c7f4b1a28abe054a3ef19/results-of-egm-company-update.jpg)

![Results Presentation [Company Update]](https://static.fdocuments.in/doc/165x107/577cb4341a28aba7118c5b10/results-presentation-company-update.jpg)