Results Presentation 1Q 2013 - Bankia · Results Presentation 1Q 2013 April 2013 1Q 2013 April 2013...

28

Results Presentation 1Q 2013 April 2013 1Q 2013 April 2013

Transcript of Results Presentation 1Q 2013 - Bankia · Results Presentation 1Q 2013 April 2013 1Q 2013 April 2013...

Results Presentation 1Q 2013

April 2013 1Q 2013

April 2013

2 of 28 / April 2013

Disclaimer

This document has been prepared by Bankia, S.A. (“Bankia”) and is presented exclusively for information purposes. It is not a prospectus and does not constitute an offer or recommendation to invest.

This document does not constitute a commitment to subscribe, or an offer to finance, or an offer to sell, or a solicitation of offers to buy securities of Bankia, all of which are subject to internal approval by Bankia.

Bankia does not guarantee the accuracy or completeness of the information contained in this document. The information contained herein has been obtained from sources that Bankia considers reliable, but BANKIA does not represent or warrant that the information is complete or accurate, in particular with respect to data provided by third parties. This document may contain abridged or unaudited information and recipients are invited to consult the public documents and information submitted by Bankia to the financial market supervisory authorities. All opinions and estimates are given as of the date stated in the document and so may be subject to change. The value of any investment may fluctuate as a result of changes in the market. The information in this document is not intended to predict future results and no guarantee is given in that respect.

Distribution of this document in other jurisdictions may be prohibited, and therefore recipients of this document or any persons who may eventually obtain a copy of it are responsible for being aware of and complying with said restrictions. By accepting this document you accept the foregoing restrictions and warnings.

This document does not reveal all the risks or other material factors relating to investments in the securities/transactions of Bankia. Before entering into any transaction, potential investors must ensure that they fully understand the terms of the securities/transactions and the risks inherent in them. This document is not a prospectus for the securities described in it. Potential investors should only subscribe for securities of Bankia on the basis of the information published in the appropriate Bankia prospectus, not on the basis of the information contained in this document.

3 of 28 / April 2013

Contents

1. 1Q 2013 highlights

2. 1Q 2013 results

3. Asset quality and risk management

4. Liquidity and solvency

5. Conclusions

4 of 28 / April 2013

1Q 2013 highlights

Profit generation

FINANCIAL PERFORMANCE

Comfortable liquidity position

RESTRUCTURING PLAN PROGRESS

NPLs stabilisation

Cost reduction

1 2

Organic capital generation

Capital increase in progress

Workforce agreement (ERE)

Branch closure plan accelerated

IT integration completed

5 of 28 / April 2013

1Q 2013 highlights

FINANCIAL PERFORMANCE – BFA GROUP 1

Net profit generation: €213 million in BFA Group

Operating costs reduction: down 11.6% on 4Q 2012 Results

Asset quality

Liquidity and solvency

NPLs and NPL ratio stable

High provision coverage over credit portfolios

LTD ratio and commercial gap unchanged vs. Q4 2012.

Organic capital generation: 57 bps, reaching 9.97% EBA Core Tier 1 pro

forma in BFA Group

6 of 28 / April 2013

1Q 2013 highlights

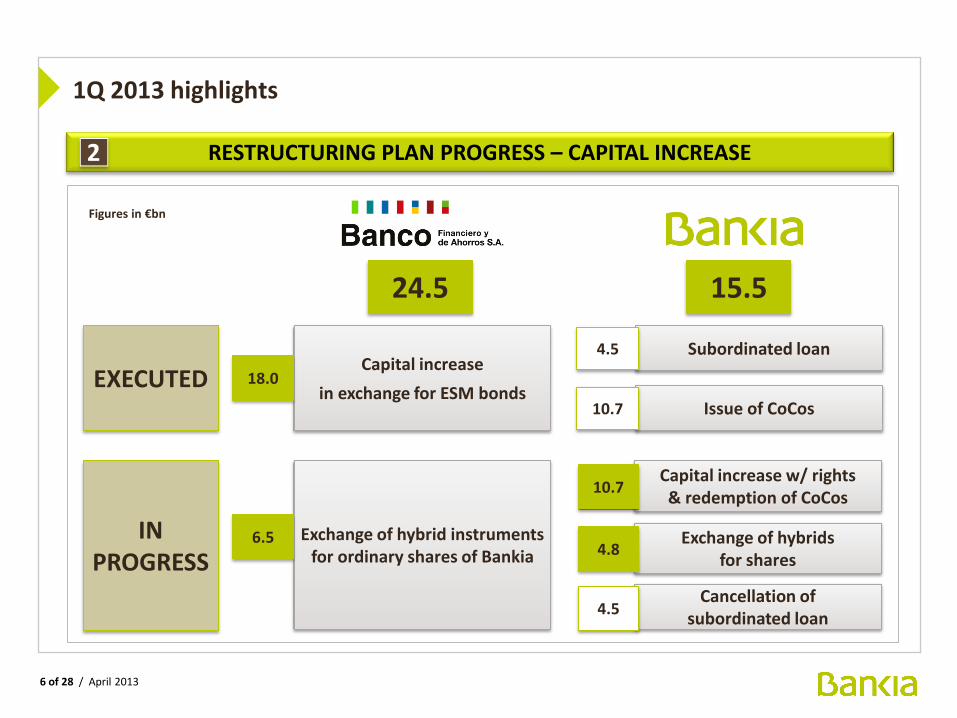

RESTRUCTURING PLAN PROGRESS – CAPITAL INCREASE 2

24.5

EXECUTED Capital increase

in exchange for ESM bonds

IN PROGRESS

18.0

Exchange of hybrid instruments for ordinary shares of Bankia

6.5

Issue of CoCos

Exchange of hybrids for shares

Capital increase w/ rights & redemption of CoCos

Cancellation of subordinated loan

Subordinated loan

15.5

10.7

4.5

10.7

4.5

4.8

Figures in €bn

7 of 28 / April 2013

1Q 2013 highlights

RESTRUCTURING PLAN PROGRESS – CAPITAL INCREASE 2

Reduction of par value from €2 to €0.01

1x100 reverse split

New par value: €1

COMPLETED

€10,700 million

Rights issue in Bankia

Capital increase in Bankia for up to €5,210

(1) million without subscription rights

(exchange of hybrids)

IN PROGRESS

CAPITAL INCREASE FIGURES AVERAGE HAIRCUT ON HYBRIDS EXCHANGE

Shares to be issued (million) 11,762

Subscription price (€)

Maximum amount (€m)

1.3527

15,910

Preferred shares

Perpetual subordinated debt

Dated subordinated debt

38%

36%

13% (1)

(1) Maximum amount of capital increase for exchange. In the baseline scenario the exchange of hybrids will generate €4,841 million of capital and therefore an estimated maximum amount of €15,541 million

8 of 28 / April 2013

1Q 2013 highlights

ESTIMATED TIMELINE (subject to supervision and register of the Issuance Prospectus and Securities Note by the CNMV)

FROB Steering Committee approves agreements for par value reduction, reverse split, capital increase w/ rights and hybrid conversion

16 April

Shares start trading after reverse split 22 April

Expected date for the Prospectus to be registered by CNMV 25/26 April (e)

New shares start trading Last week May(e)

Rights trading period

Senior debt exchange (LT2) offer period

26/28 April – 10/13 May (e)

21/24 May (e) Allotment of shares and exchange of hybrids

RESTRUCTURING PLAN PROGRESS – CAPITAL INCREASE 2

Redemption of CoCos

9 of 28 / April 2013

1Q 2013 highlights

BANKIA GROUP EXPECTED SHAREHOLDERS STRUCTURE

PRE-CAPITAL INCREASE POST-CAPITAL INCREASE AND EXCHANGE (e)

BFA 48%

Free Float 52% BFA

~69%

Free Float ~31%

0

FINAL NO. OF SHARES (MILL.) 11,509

RESTRUCTURING PLAN PROGRESS – CAPITAL INCREASE 2

(1)

(1) Estimate based on €4,841 million of capital generation

10 of 28 / April 2013

1Q 2013 highlights

BRANCH CLOSURES UP TO 1Q 2013

PLANNED CLOSURES BY 2015 1,143

CLOSURES COMPLETED BY 1Q 2013 197

% OF TARGET 17%

Branch closures envisaged in Strategic Plan to be accelerated

Madrid and Valencia networks (60% of total) to be fully restructured by June 2013

All planned closures are expected to have been completed by 1Q 2014

RESTRUCTURING PLAN PROGRESS – FASTER IMPLEMENTATION 2

PLANNED CUMULATIVE CLOSURES

1Q13 2Q13 1Q14

197

607

1,143

11 of 28 / April 2013

Contents

1. 1Q 2013 highlights

2. 1Q 2013 results

3. Asset quality and risk management

4. Liquidity and solvency

5. Conclusions

12 of 28 / April 2013

BFA and Bankia P&L – Key figures

1Q 2013 results

Net interest income

Gross income

Operating expenses

Pre-provision profit

587

1,027

(498)

529

Provisions and other expenses

Profit before tax

(266)

263

Profit after tax 213

Taxes (50)

Dividends

Other revenue

101

339

512

868

(494)

374

(272)

102

72

(30)

1

355

Figures in €m

13 of 28 / April 2013

Bankia pro forma P&L – Key figures

A

B

C

D

Mar 2013

Pro forma income statement excludes €89 million interest expense for the quarter from the subordinated loan granted by BFA to Bankia, to be cancelled after the capital increase.

1Q 2013 results

Bankia Group data. €m

Net interest income

Gross income

Operating expenses

Pre-provision profit

601

957

(494)

463

Provisions and other expenses

Profit before tax

(272)

191 E

14 of 28 / April 2013

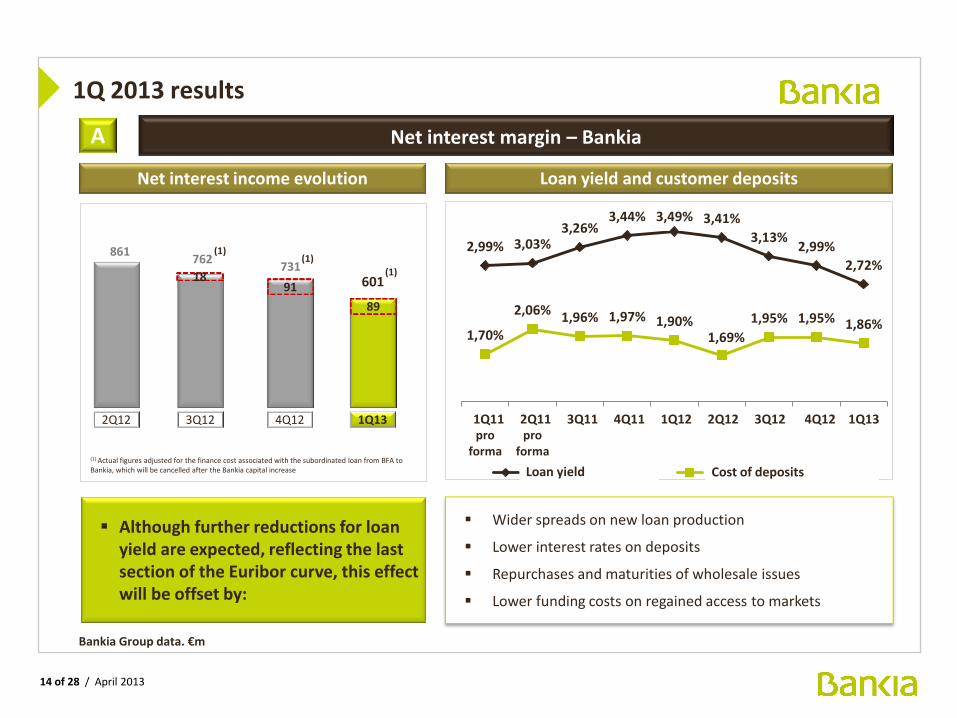

Net interest margin – Bankia

Bankia Group data. €m

Net interest income evolution

2Q12 3Q12 4Q12 1Q13

Although further reductions for loan yield are expected, reflecting the last section of the Euribor curve, this effect will be offset by:

18 91

861 762

731 601

89

1Q 2013 results

(1) Actual figures adjusted for the finance cost associated with the subordinated loan from BFA to Bankia, which will be cancelled after the Bankia capital increase

A

Loan yield and customer deposits

Wider spreads on new loan production

Lower interest rates on deposits

Repurchases and maturities of wholesale issues

Lower funding costs on regained access to markets

(1) (1)

(1)

2,99% 3,03% 3,26%

3,44% 3,49% 3,41%

3,13% 2,99%

2,72%

1,70%

2,06% 1,96% 1,97% 1,90% 1,69%

1,95% 1,95% 1,86%

1T 2011pro

forma

2T 2011pro

forma

3T 2011 4T 2011 1T 2012 2T 2012 3T 2012 4T 2012 1T 2013

Rendimiento créditos Coste depósitos de clientes Loan yield Cost of deposits

1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12 4Q12 1Q13

15 of 28 / April 2013

Net interest margin – Bankia A

Non-developer SMEs and

corporates

1Q13

4.00

Spreads on new production

+32 bps

Third-party mortgages

Loans and advances to customers Customer deposits

Wider LOAN SPREADS

1Q 2013 results

NEW PRODUCTION

Lower DEPOSIT INTEREST

RATES

2012

3.68

1Q13

2.81

+66 bps

2012

2.15

Sight deposits

1Q13

0.34

-9 bps

2012

0.43

Time deposits

1Q13 2012

2.43

-46 bps

2.89

IMPROVEMENT IN SPREADS

Bankia Group data. bps

16 of 28 / April 2013

Gross Income in 1Q 2013 reflects the low interest rate environment and slowdown in banking activity

Gross income – Bankia

Composition and growth of Gross Income

B

Bankia Group data. €m

1Q 2013 results

(1) Actual figures adjusted for the funding cost associated with the subordinated loan from BFA to Bankia, which will be cancelled after Bankia’s capital increase

GROSS INCOME 1Q 2013

957 (1)

1,020

GROSS INCOME 2Q 2012

884 (1)

GROSS INCOME 3Q 2012

904 (1)

GROSS INCOME 4Q 2012

601 (1)

Net interest income

225

161

16 (45)

Net fees Trading

income & exch. diffs.

Dividends and eq. method

Other

(DGF)

GROSS INCOME 1Q 2013

957 (1)

89

17 of 28 / April 2013

Operating expenses – Bankia

Quarterly operating expenses evolution

C

Despite the fall in interest income, cost reduction has kept the basic cost-to-income ratio down (1)

Q2 2012

592

1Q 2013

494

Bankia Group data. €m

1Q 2013 results

Q4 2012

553

Q3 2012

560 - 10.7%

(1) Cost-to-income ratio excluding trading income and exchange differences

Q2 2012 1Q 2013 Q4 2012 Q3 2012

59.5%

62.1% 63.3% 62.1%

Operating expenses/Gross income (ex tr. income)

18 of 28 / April 2013

1Q 2013 results

Pre-provision profit D

Bankia Group data. €m

2Q12 3Q12 4Q12 1Q13

428 324 351 463

Pre-provision profit up compared to three previous quarters

(1) (1)

(1) Actual figures adjusted for the funding cost associated with the subordinated loan from BFA to Bankia, which will be cancelled after Bankia’s capital increase

18 91

89

306 260

374

(1)

19 of 28 / April 2013

Profit before tax

Pre-provision profit

Financial asset impairment and provisions

Non-financial asset impairment

463 (1)

-218

-3

Provision for real estate assets -51

1Q 2013

1Q 2013 results

Profit/(loss) before tax 191

(1) Including €89m of net interest income due to the impact of the subordinated loan

E

Risk management covered and financeable by pre-provision profit

Bankia Group data. €m

20 of 28 / April 2013

Contents

1. 1Q 2013 highlights

2. 1Q 2013 results

3. Asset quality and risk management

4. Liquidity and solvency

5. Conclusions

21 of 28 / April 2013

Asset quality and risk management

Portfolios

Retail

Corporates and SMEs

87.6

43.0

Gross amount

Developers 4.8

Credit quality

Bankia Group data. €bn

Total loan portfolio 145.8

Provisions as % gross loans

3.3%

14.8%

44.8%

8.0%

High portfolio coverage ratios maintained

Dec 2012

Loans and coverage ratios on loan portfolios

86.4

41.8

Gross amount

4.8

142.6

Mar 2013

Provisions as % gross loans

3.2%

15.0%

46.7%

8.1%

Total without developers 141.0 6.7% 137.8 6.7%

22 of 28 / April 2013

Asset quality and risk management

Credit quality

Bankia Group data. €bn

Dec 2012

Total gross assets 152.5

NPLs 19.8

NPL ratio

NPL coverage

13.0%

61.8%

Stable NPL ratio and coverage

NPLs and coverage NPLs evolution

Mar 2013

149.6

19.6

13.1%

61.9%

NPLs Dec 2012

+ Gross additions

- Recoveries

19.8

- Written-off

NPLs 1Q 2013

+ 0.7

- 0.8

-0.1

19.6

Net additions - 0.1

23 of 28 / April 2013

Contents

1. 1Q 2013 highlights

2. 1Q 2013 results

3. Asset quality and risk management

4. Liquidity and solvency

5. Conclusions

24 of 28 / April 2013

Main liquidity indicators - Bankia

Commercial gap

LTD stable around 120%

Liquidity and solvency

Commercial gap: Net credit – mediation loans – retail commercial paper – strict customer deposits

LTD ratio: (Net credit / (retail commercial paper + strict customer deposits + ICO/EIB deposits + single-certificate covered bonds))

2Q 2012

60.2

1Q 2013

32.8

4Q 2012

33.3

3Q 2012

60.4

Bankia Group data. €bn

Transfer of deposits to investment funds seeking higher returns

Acceleration of branch closures

Change in policy on deposit interest rates

Continued reduction in the Commercial gap in the following context:

25 of 28 / April 2013

Liquidity and solvency

Organic capital generation

Self-sustaining capital generation

Bankia Group – EBA CORE TIER 1

5.67%

9.44% 10.3

BFA Group – EBA CORE TIER 1

DEC 2012

+ 19 bps

MAR 2013

+ 38 bps 9.40% 9.97%

Actual December 2012

Capital increase(1)

Generated organically

+ 7 bps + 36 bps 9.63%

10.06%

DEC 2012 MAR 2013 ↑Prof. ↓RWAs ↑Prof. ↓RWAs

3.52 %

5.88%

3.52 %

5.88%

0,57%

4.94 %

4.69%

4.94 %

4.69%

0.43%

(1) Estimate based on €4,841 million of exchange of hybrid instruments into new Bankia shares

26 of 28 / April 2013

Contents

1. 1Q 2013 highlights

2. 1Q 2013 results

3. Asset quality and risk management

4. Liquidity and solvency

5. Conclusions

27 of 28 / April 2013

Conclusions

Income statement getting “back to normality”

1

3

4

Pressure on net interest income (as we expected)

2

Intensive Group restructuring: process completed in 4 quarters

Pricing and business policies focused on margin and fee management

Reinforced NPL monitoring and management

Results Presentation 1Q 2013

April 2013 1Q 2013

April 2013