Result of Crisis Management Survey 2014 - Deloitte US · Result of Crisis Management Survey 2014...

31

Result of Crisis Management Survey 2014 Deloitte Touche Tohmatsu LLC Crisis Management Service

Transcript of Result of Crisis Management Survey 2014 - Deloitte US · Result of Crisis Management Survey 2014...

Result of Crisis Management Survey 2014

Deloitte Touche Tohmatsu LLCCrisis Management Service

Table of contents

Introduction 3

Executive Summary 7

Analysis of respondents 10

Analysis of domestic subsidiaries respondents 18

Analysis of foreign subsidiaries respondents 24

© 2015. For information, contact Deloitte Touche Tohmatsu LLC.

Introduction

3 Result of Crisis Management Survey 2014

© 2015. For information, contact Deloitte Touche Tohmatsu LLC.

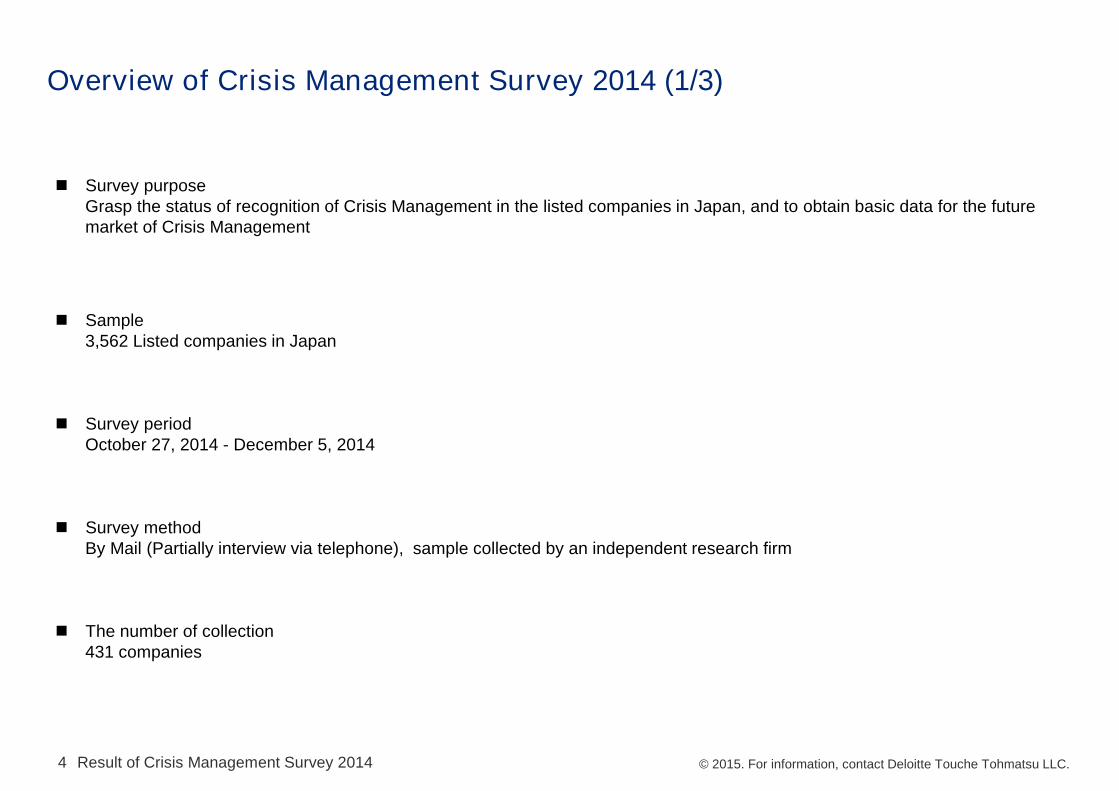

Overview of Crisis Management Survey 2014 (1/3)

Result of Crisis Management Survey 20144

Survey purposeGrasp the status of recognition of Crisis Management in the listed companies in Japan, and to obtain basic data for the future market of Crisis Management

Survey methodBy Mail (Partially interview via telephone), sample collected by an independent research firm

Survey periodOctober 27, 2014 - December 5, 2014

Sample3,562 Listed companies in Japan

The number of collection431 companies

© 2015. For information, contact Deloitte Touche Tohmatsu LLC.

Overview of Crisis Management Survey 2014 (2/3)

Result of Crisis Management Survey 20145

Definition of terms• Crisis

Crisis is a single large-scale or combination of events that could significantly damage organization’s strategic objectives, critical assets*, reputation or even the existence of the organization.e.g., natural disaster, cyber attack, political change, product recall, information leakage, accounting fraud, legal amendment*human resources, physical assets, intellectual property, information, etc.

• Cybercyber breach, info leakage, virus infection, etc.

• Fraudfinancial crime, fraud, violation of law, etc.

• Natural disasterearthquake, typhoon, pandemic, etc.

• Productsupply chain disruption, recall, quality failure, facility accident, etc.

• Finance / Legalfinancial crisis, litigation, financial distress, labor-management issue, intellectual property violation, regulatory, etc.

• Geopoliticalinternational conflict, terror, etc.

• Environmentpollution, etc.

• Reputationharmful rumor, boycott movement, decline of stock market price caused by harmful rumor, etc.

© 2015. For information, contact Deloitte Touche Tohmatsu LLC.

Overview of Crisis Management Survey 2014 (3/3)

Result of Crisis Management Survey 20146

*Japan Standard Industry Classification, Ministry of Internal Affairs and Communications

Industry* Number of respondents

Agriculture andForestry 1

Mining and Quarrying of stone and gravel 2

Construction 19

Manufacturing 175Electricity, Gas, Heat

supply and Water 3

Information andCommunications 24

Transport andPostal services 16

Wholesale andRetail trade 99

Finance andInsurance 23

Real estate andGoods rental and leasing 13

Services, N.E.C. 56

Total 431

Number of employee Number of respondents

More than 10,000 43More than 5,000 -Less than 10,000 31

More than 3,000 -Less than 5,000 30

More than 1,000 -Less than 3,000 86

More than 500 -Less than1,000 85

More than 300 -Less than 500 54

More than 100 -Less than 300 65

Less than 100 37

Total 431

Consolidated net sales Number of respondents

More than 1 trillion JPY 21

More than 500 billion -Less than 1 trillion JPY 15

More than 100 billion -Less than 500 billion JPY 82

More than 50 billion -Less than 100 billion JPY 46

More than 30 billion -Less than 50 billion JPY 63

More than 10 billion -Less than 30 billion JPY 102More than 5 billion - Less

than 10 billion JPY 46

Less than 5 billion JPY 56

Total 431

© 2015. For information, contact Deloitte Touche Tohmatsu LLC.

Executive Summary

7 Result of Crisis Management Survey 2014

© 2015. For information, contact Deloitte Touche Tohmatsu LLC.8 Result of Crisis Management Survey 2014

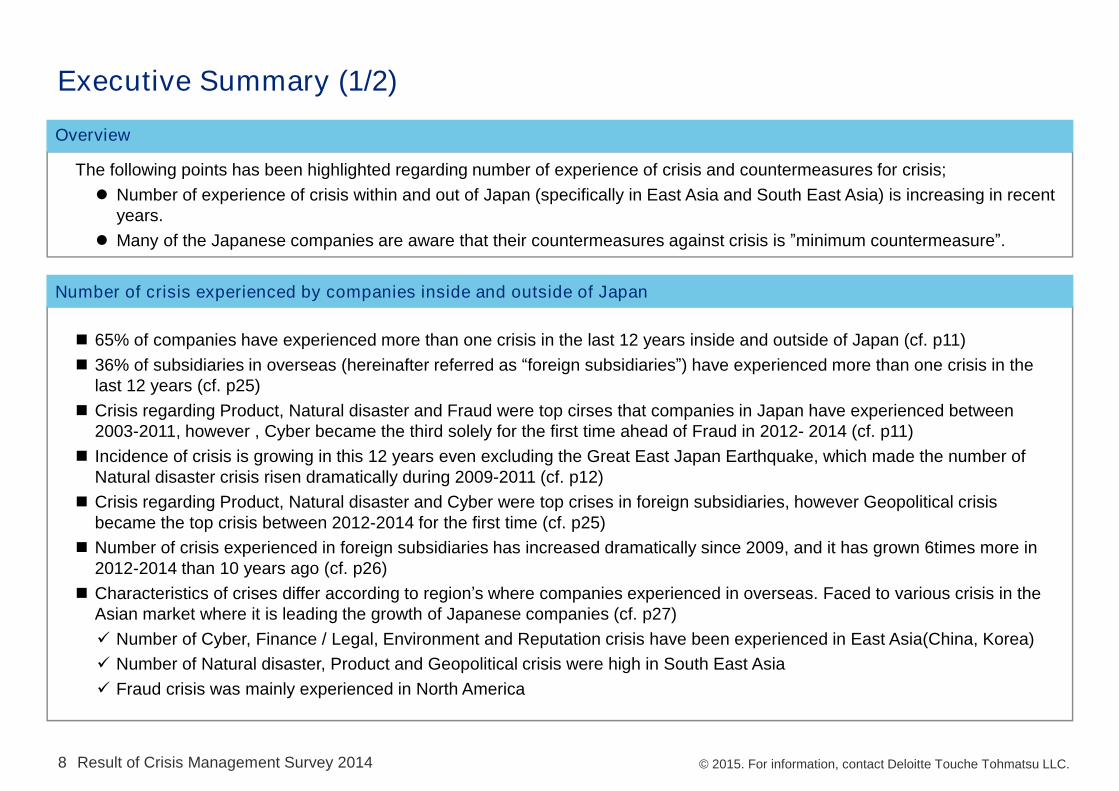

Executive Summary (1/2)

The following points has been highlighted regarding number of experience of crisis and countermeasures for crisis; Number of experience of crisis within and out of Japan (specifically in East Asia and South East Asia) is increasing in recent

years. Many of the Japanese companies are aware that their countermeasures against crisis is ”minimum countermeasure”.

Overview

65% of companies have experienced more than one crisis in the last 12 years inside and outside of Japan (cf. p11) 36% of subsidiaries in overseas (hereinafter referred as “foreign subsidiaries”) have experienced more than one crisis in the

last 12 years (cf. p25) Crisis regarding Product, Natural disaster and Fraud were top cirses that companies in Japan have experienced between

2003-2011, however , Cyber became the third solely for the first time ahead of Fraud in 2012- 2014 (cf. p11) Incidence of crisis is growing in this 12 years even excluding the Great East Japan Earthquake, which made the number of

Natural disaster crisis risen dramatically during 2009-2011 (cf. p12) Crisis regarding Product, Natural disaster and Cyber were top crises in foreign subsidiaries, however Geopolitical crisis

became the top crisis between 2012-2014 for the first time (cf. p25) Number of crisis experienced in foreign subsidiaries has increased dramatically since 2009, and it has grown 6times more in

2012-2014 than 10 years ago (cf. p26) Characteristics of crises differ according to region’s where companies experienced in overseas. Faced to various crisis in the

Asian market where it is leading the growth of Japanese companies (cf. p27) Number of Cyber, Finance / Legal, Environment and Reputation crisis have been experienced in East Asia(China, Korea) Number of Natural disaster, Product and Geopolitical crisis were high in South East Asia Fraud crisis was mainly experienced in North America

Number of crisis experienced by companies inside and outside of Japan

© 2015. For information, contact Deloitte Touche Tohmatsu LLC.9 Result of Crisis Management Survey 2014

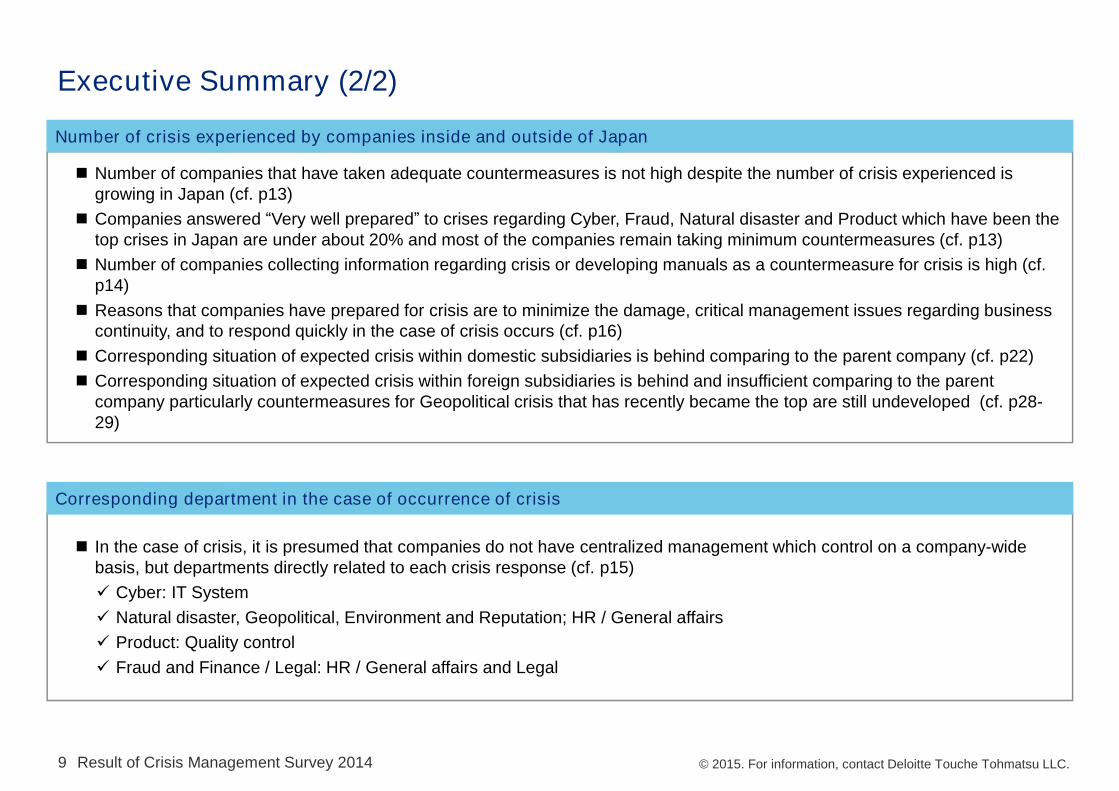

Executive Summary (2/2)

Number of companies that have taken adequate countermeasures is not high despite the number of crisis experienced is growing in Japan (cf. p13)

Companies answered “Very well prepared” to crises regarding Cyber, Fraud, Natural disaster and Product which have been the top crises in Japan are under about 20% and most of the companies remain taking minimum countermeasures (cf. p13)

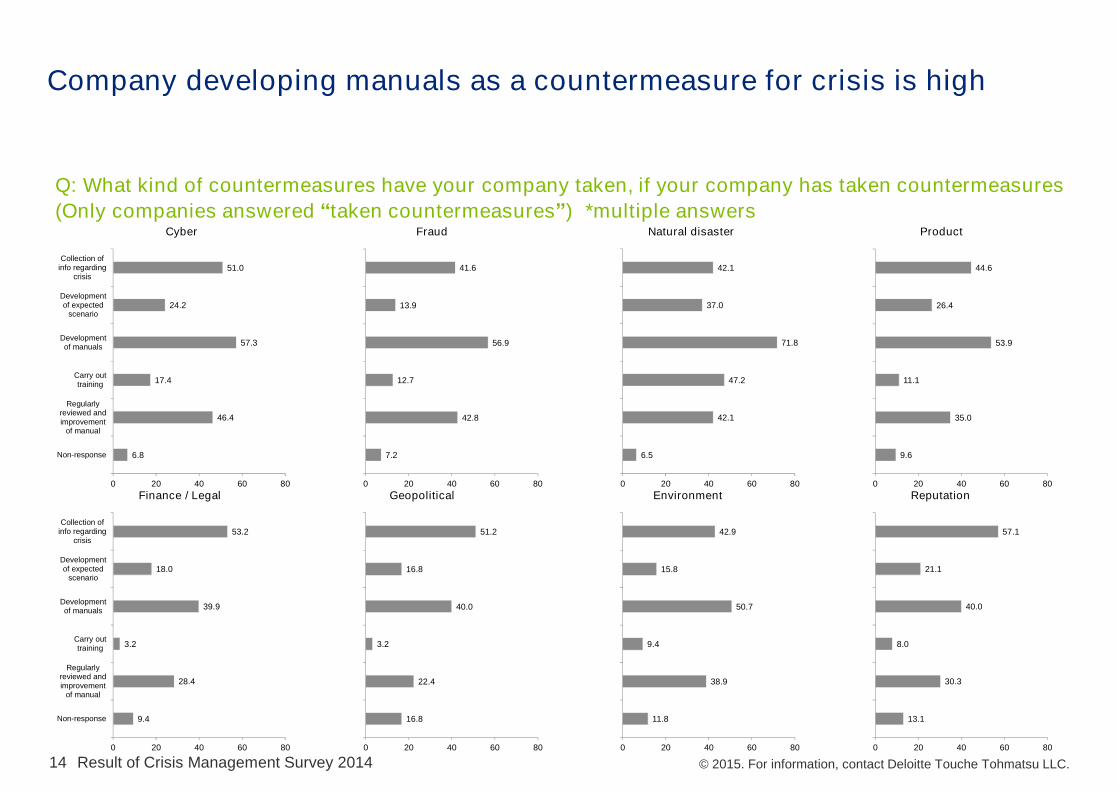

Number of companies collecting information regarding crisis or developing manuals as a countermeasure for crisis is high (cf. p14)

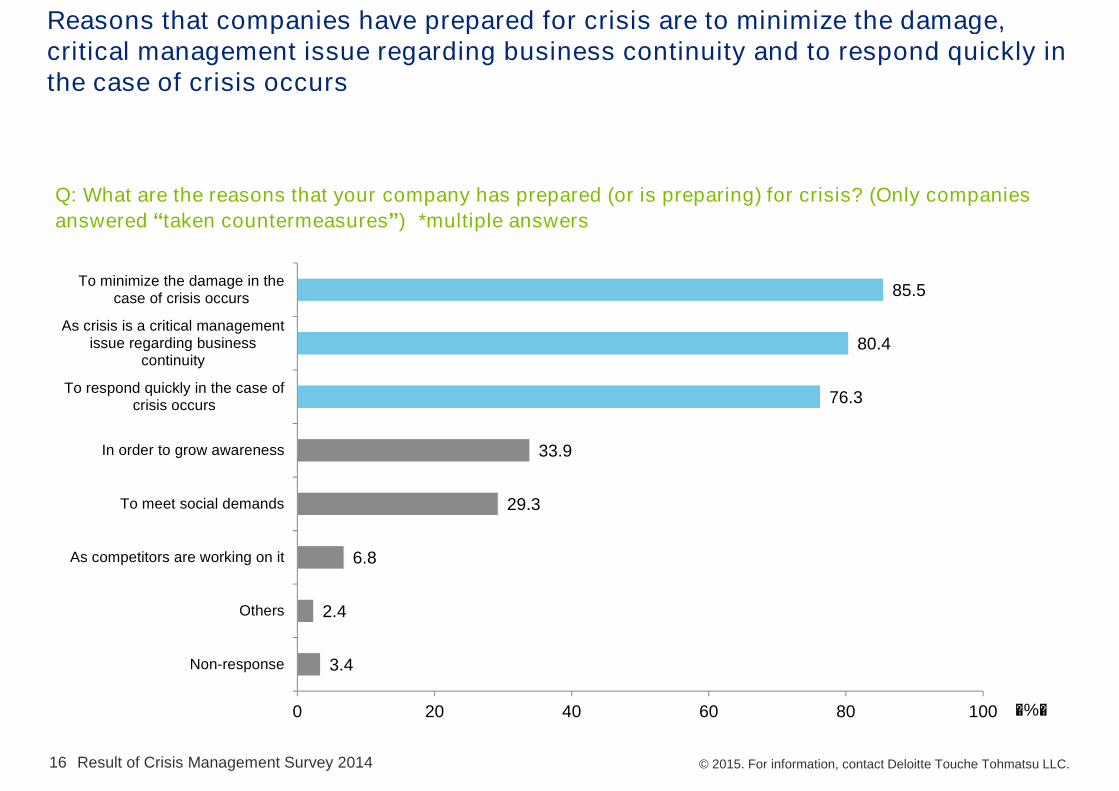

Reasons that companies have prepared for crisis are to minimize the damage, critical management issues regarding business continuity, and to respond quickly in the case of crisis occurs (cf. p16)

Corresponding situation of expected crisis within domestic subsidiaries is behind comparing to the parent company (cf. p22) Corresponding situation of expected crisis within foreign subsidiaries is behind and insufficient comparing to the parent

company particularly countermeasures for Geopolitical crisis that has recently became the top are still undeveloped (cf. p28-29)

Number of crisis experienced by companies inside and outside of Japan

In the case of crisis, it is presumed that companies do not have centralized management which control on a company-wide basis, but departments directly related to each crisis response (cf. p15) Cyber: IT System Natural disaster, Geopolitical, Environment and Reputation; HR / General affairs Product: Quality control Fraud and Finance / Legal: HR / General affairs and Legal

Corresponding department in the case of occurrence of crisis

© 2015. For information, contact Deloitte Touche Tohmatsu LLC.

Analysis of respondents*

10 Result of Crisis Management Survey 2014

*431 listed companies in Japan which responded the questionnaire

© 2015. For information, contact Deloitte Touche Tohmatsu LLC.11

*Summary of each sheet is written in this box, but we have erased it upon translating as it is summarized in the “Executive summary”

65% of companies have experienced crisis in the last 12 years. There is no significant change in the ranking of the experienced crisis

Q: Has your company ever experienced any crisis?

Yes65%

No34%

Non-response

1%

Q: When and what type of crisis did your company experienced? *multiple answers

Experience of crisis(Responded companies)

Ranking of experienced crisis(Responded companies)

2003-2005 2006-2008 2009-2011 2012-2014 2003-2014

1st Product Product Natural disaster Product Natural

disaster

2nd Natural disaster Fraud Product Natural

disaster Product

3rd Fraud Natural disasterCyber

Finance / Legal*

Fraud Cyber Fraud

4th Cyber Finance / Legal Fraud Cyber

5th Finance / Legal Cyber Finance / Legal Finance / Legal

6th Reputation Reputation Reputation Reputation Reputation

7th Geopolitical Environment Environment Geopolitical Geopolitical

8th Geopolitical Geopolitical Environment Environment* Same rank as same number

Result of Crisis Management Survey 2014

© 2015. For information, contact Deloitte Touche Tohmatsu LLC.12

Number of crisis experienced in companies has increased, and incidence of crisis is growing

Q: When and what type of crisis did your company has experienced? *multiple answerTransition of experienced crisis

(Responded companies)[Number]

7993

333

189

0

50

100

150

200

250

300

350

2003-2005 2006-2008 2009-2011 2012-2014

Cyber Fraud Natural disaster Product Finance / Legal Geopolitical Enviroment Reputation AllResult of Crisis Management Survey 2014

© 2015. For information, contact Deloitte Touche Tohmatsu LLC.Result of Crisis Management Survey 201413

Companies that have taken adequate countermeasures are not high

Q: What is the corresponding situation of each type of expected crisis?[Type of crisis] Corresponding situation of expected crisis (Responded companies)

6.5

10.2

3.0

8.4

14.6

19.3

18.8

21.6

34.1

36.9

26.0

56.1

50.3

62.9

58.2

59.9

7.9

3.9

5.3

6.0

6.5

7.2

6.0

7.0

14.6

8.1

10.0

11.1

9.0

4.2

6.5

3.0

20.0

9.3

16.0

9.0

6.5

2.8

3.5

3.7

13.9

26.9

36.2

6.0

9.3

1.6

3.5

2.1

3.0

4.7

3.5

3.4

3.8

2.0

3.5

2.7

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Reputation

Enviroment

Geopolitical

Finance /Legal

Product

Naturaldisaster

Fraud

Cyber

Very well prepared Prepared minimum countermeasures Under development of countermeasuresUnder consideration Not considered Not expected as crisisNon-response

© 2015. For information, contact Deloitte Touche Tohmatsu LLC.Result of Crisis Management Survey 201414

Company developing manuals as a countermeasure for crisis is high

Q: What kind of countermeasures have your company taken, if your company has taken countermeasures(Only companies answered “taken countermeasures”) *multiple answers

9.6

35.0

11.1

53.9

26.4

44.6

0 20 40 60 80

6.5

42.1

47.2

71.8

37.0

42.1

0 20 40 60 80

ProductNatural disaster

11.8

38.9

9.4

50.7

15.8

42.9

0 20 40 60 80

13.1

30.3

8.0

40.0

21.1

57.1

0 20 40 60 80

ReputationEnvironment

7.2

42.8

12.7

56.9

13.9

41.6

0 20 40 60 80

6.8

46.4

17.4

57.3

24.2

51.0

0 20 40 60 80

Non-response

Regularlyreviewed andimprovement

of manual

Carry outtraining

Developmentof manuals

Developmentof expected

scenario

Collection ofinfo regarding

crisis

FraudCyber

9.4

28.4

3.2

39.9

18.0

53.2

0 20 40 60 80

Non-response

Regularlyreviewed andimprovement

of manual

Carry outtraining

Developmentof manuals

Developmentof expected

scenario

Collection ofinfo regarding

crisis

Finance / Legal Geopolitical

16.8

22.4

3.2

40.0

16.8

51.2

0 20 40 60 80

© 2015. For information, contact Deloitte Touche Tohmatsu LLC.Result of Crisis Management Survey 201415

[Type of crisis]

23.0

8.6

18.8

13.1

5.5

9.3

11.1

4.5

12.5

6.1

2.6

26.8

26.0

37.1

36.9

49.1

36.3

13.2

62.8

33.2

6.3

0.6

46.3

2.3

79.8

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Reputation

Enviroment

Geopolitical

Finance /Legal

Product

Naturaldisaster

Fraud

Cyber

Corporate planning Finance / Accounting Legal HR / General affairs Quality control IT System Other admin

HR/General affairs in the case of Natural disaster, Geopolitical, Environment and Reputation, IT system in the case of Cyber, and Quality control in the case of Product crisis will lead in the case of occurrence of crisis

Q: Which department will lead in the case of occurrence of crisis? (Only the companies answered “taken countermeasures”)

© 2015. For information, contact Deloitte Touche Tohmatsu LLC.Result of Crisis Management Survey 201416

Reasons that companies have prepared for crisis are to minimize the damage, critical management issue regarding business continuity and to respond quickly in the case of crisis occurs

[%]

Q: What are the reasons that your company has prepared (or is preparing) for crisis? (Only companies answered “taken countermeasures”) *multiple answers

3.4

2.4

6.8

29.3

33.9

76.3

80.4

85.5

0 20 40 60 80 100

Non-response

Others

As competitors are working on it

To meet social demands

In order to grow awareness

To respond quickly in the case ofcrisis occurs

As crisis is a critical managementissue regarding business

continuity

To minimize the damage in thecase of crisis occurs

© 2015. For information, contact Deloitte Touche Tohmatsu LLC.Result of Crisis Management Survey 201417

Uncertain whether crisis occurs is a high numbered answer for a reason not to consider countermeasures for crisis

Q: What are the reasons of not considered countermeasures for crisis? (Only companies answered “not considered countermeasures”) *multiple answers

7.7

10.3

59.0

10.3

7.7

20.5

0 20 40 60 80

40.0

8.6

31.4

17.1

11.4

17.1

0 20 40 60 80

ProductNatural disaster

10.4

13.5

58.3

29.2

10.4

11.5

0 20 40 60 80

Reputation

18.2

9.1

54.5

23.6

7.3

10.9

0 20 40 60 80

Environment

26.7

6.7

50.0

13.3

13.3

23.3

0 20 40 60 80

22.2

7.4

33.3

25.9

14.8

22.2

0 20 40 60 80

Non-response

Others

Uncertain whethercrisis occurs

Unnecessary sincethe effect isuncertain

No know-how ofdeveloping

countermeasures

Shortage ofresources; human

resources andbudget

FraudCyber

15.6

13.3

48.9

15.6

8.9

11.1

0 20 40 60 80

Non-response

Others

Uncertain whethercrisis occurs

Unnecessary sincethe effect isuncertain

No know-how ofdeveloping

countermeasures

Shortage ofresources; human

resources andbudget

Finance / Legal

15.1

9.3

51.2

26.7

15.1

10.5

0 20 40 60 80

Geopolitical

© 2015. For information, contact Deloitte Touche Tohmatsu LLC.

Analysis of domestic subsidiaries respondents*

18 Result of Crisis Management Survey 2014

*222 listed companies that owns domestic subsidiaries

© 2015. For information, contact Deloitte Touche Tohmatsu LLC.19

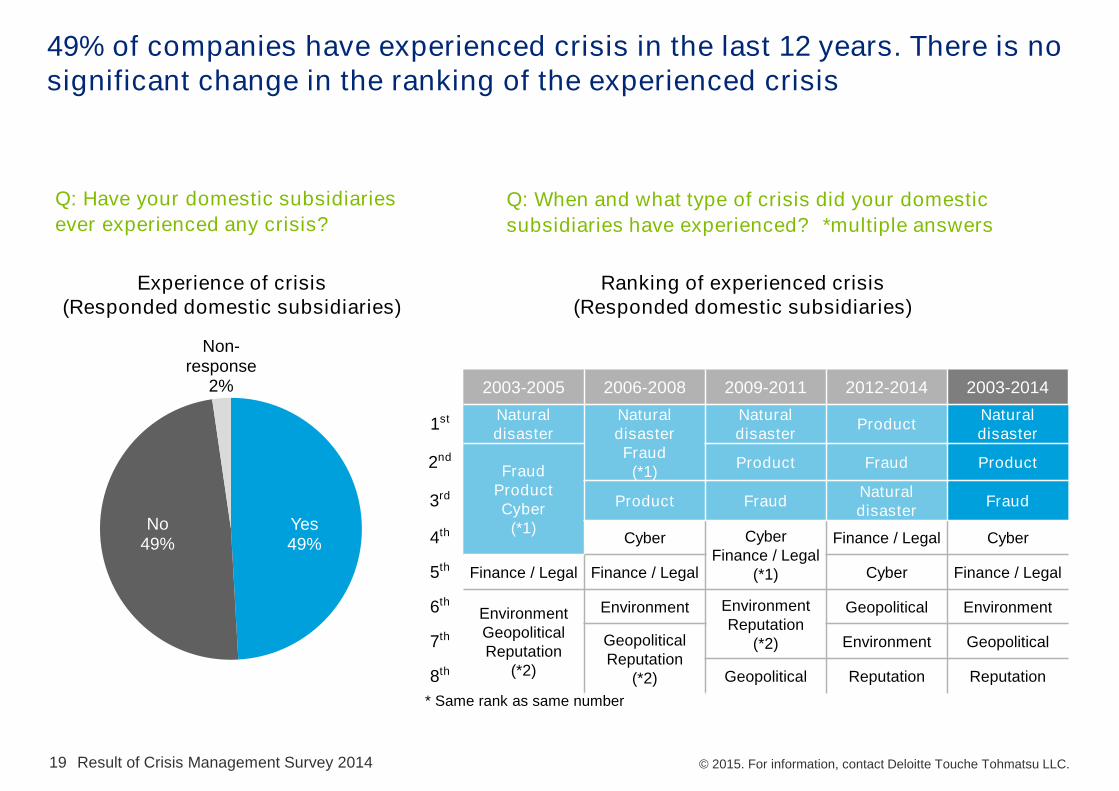

49% of companies have experienced crisis in the last 12 years. There is no significant change in the ranking of the experienced crisis

Q: Have your domestic subsidiaries ever experienced any crisis?

Yes49%

No49%

Non-response

2%

Experience of crisis(Responded domestic subsidiaries)

Ranking of experienced crisis(Responded domestic subsidiaries)

Q: When and what type of crisis did your domestic subsidiaries have experienced? *multiple answers

2003-2005 2006-2008 2009-2011 2012-2014 2003-2014

1st Natural disaster

Natural disasterFraud

(*1)

Natural disaster Product Natural

disaster

2ndFraud

ProductCyber

(*1)

Product Fraud Product

3rd Product Fraud Natural disaster Fraud

4th Cyber CyberFinance / Legal

(*1)

Finance / Legal Cyber

5th Finance / Legal Finance / Legal Cyber Finance / Legal

6thEnvironmentGeopoliticalReputation

(*2)

Environment EnvironmentReputation

(*2)

Geopolitical Environment

7th GeopoliticalReputation

(*2)

Environment Geopolitical

8th Geopolitical Reputation Reputation* Same rank as same number

Result of Crisis Management Survey 2014

© 2015. For information, contact Deloitte Touche Tohmatsu LLC.20

Number of crisis experienced in domestic subsidiaries have increased, and incidence of crisis is growing

Transition of experienced crisis(Responded domestic subsidiaries)

Q: When and what type of crisis did your domestic subsidiaries have experienced? *multiple answers

[Number]

17

25

126

70

0

50

100

150

2003-2005 2006-2008 2009-2011 2012-2014Cyber Fraud Natural disaster Product Finance / Legal Geopolitical Enviroment Reputation All

Result of Crisis Management Survey 2014

© 2015. For information, contact Deloitte Touche Tohmatsu LLC.21

Domestic subsidiaries that have taken adequate countermeasures are not high

[Type of crisis] Corresponding situation of expected crisis (Responded domestic subsidiaries)

5.9

8.1

1.8

7.2

11.7

15.8

14.4

15.8

33.3

35.1

22.5

46.4

42.8

57.7

50.9

58.1

7.7

5.9

6.3

6.3

7.7

9.9

7.2

8.1

16.2

9.9

10.4

16.2

11.3

4.1

10.4

6.3

14.4

10.8

21.2

6.8

7.2

4.5

5.4

3.2

18.9

25.2

33.8

14.0

14.9

5.4

9.0

5.4

3.6

5.0

4.1

3.2

4.5

2.7

2.7

3.2

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Reputation

Enviroment

Geopolitical

Finance /Legal

Product

Naturaldisaster

Fraud

Cyber

Very well prepared Prepared minimum countermeasures Under development of countermeasuresUnder consideration Not considered Not expected as crisisNon-response

Result of Crisis Management Survey 2014

Q: What is the corresponding situation of each type of expected crisis?

© 2015. For information, contact Deloitte Touche Tohmatsu LLC.22

Corresponding situation of expected crisis within domestic subsidiaries is behind comparing to the parent company

Q: What is the corresponding situation of each type of expected crisis? (Comparing with the parent company)Corresponding situation of expected crisis (Responded companies and domestic subsidiaries)

5.9

8.1

1.8

7.2

11.7

15.8

14.4

15.8

33.3

35.1

22.5

46.4

42.8

57.7

50.9

58.1

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Reputation

Enviroment

Geopolitical

Finance /Legal

Product

Naturaldisaster

Fraud

Cyber

Very well prepared Prepared minimum countermeasures Under development of countermeasuresUnder consideration Not considered Not expected as crisisNon-response

[Type of crisis]

Total number of “Very well prepared” and “Prepared minimum countermeasure” of parent companyResult of Crisis Management Survey 2014

© 2015. For information, contact Deloitte Touche Tohmatsu LLC.23

Countermeasures are remained collection of info regarding crisis within domestic subsidiaries

Q: What kind of countermeasures has your domestic subsidiaries taken? (Only domestic subsidiaries answered “not considered countermeasures”) *multiple answers

Result of Crisis Management Survey 2014

5.8

48.8

7.4

47.9

31.4

57.9

0 20 40 60 80

4.9

50.3

47.2

66.3

38.7

57.1

0 20 40 60 80

ProductNatural disaster

6.9

27.6

4.6

33.3

17.2

69.0

0 20 40 60 80

11.5

47.9

7.3

44.8

18.8

58.3

0 20 40 60 80

ReputationEnvironment

5.5

46.9

2.8

46.2

13.8

61.4

0 20 40 60 80

8.0

48.8

14.6

53.0

29.3

62.2

0 20 40 60 80

Non-response

Regularlyreviewed andimprovement

of manual

Carry outtraining

Developmentof manuals

Developmentof expected

scenario

Collection ofinfo regarding

crisis

FraudCyber

6.7

36.1

3.4

31.1

18.5

69.7

0 20 40 60 80

Non-response

Regularlyreviewed andimprovement

of manual

Carry outtraining

Developmentof manuals

Developmentof expected

scenario

Collection ofinfo regarding

crisis

Finance / Legal

16.7

29.6

3.7

29.6

13.0

61.1

0 20 40 60 80

Geopolitical

© 2015. For information, contact Deloitte Touche Tohmatsu LLC.

Analysis of foreign subsidiaries respondents*

24 Result of Crisis Management Survey 2014

*173 listed companies that owns foreign subsidiaries

© 2015. For information, contact Deloitte Touche Tohmatsu LLC.Result of Crisis Management Survey 201425

36% of foreign subsidiaries have experienced crisis in the last 12 years. Most recently Geopolitical at the top

Q:Have your foreign subsidiaries ever experienced any crisis?

Yes36%

No55%

Non-response

9%

Experience of crisis(Responded foreign subsidiaries)

Ranking of experienced crisis(Responded foreign subsidiaries)

Q: When and what type of crisis did your foreign subsidiaries have experienced? *multiple answers

2003-2005 2006-2008 2009-2011 2012-2014 2003-2014

1st Product Product Natural disaster Geopolitical Natural

disaster

2nd Natural disaster Natural

disasterCyber*

Product Natural disaster Product

3rd Finance / Legal Cyber ProductCyber*

CyberGeopolitical*4th

CyberGeopolitical

Environment*

Finance / Legal Finance / Legal

5th

GeopoliticalEnvironment

Fraud*

GeopoliticalFraud*

Finance / Legal Finance / Legal

6thEnvironmentReputation*

Environment

7thEnvironmentReputation*

Reputation

8th Fraud Fraud* Same rank as same number

© 2015. For information, contact Deloitte Touche Tohmatsu LLC.Result of Crisis Management Survey 201426

Number of crisis experienced in foreign subsidiaries has increased, and incidence of crisis is growing

Transition of experienced crisis(Responded foreign subsidiaries)

Q: When and what type of crisis did your foreign subsidiaries have experienced? *multiple answers

[Number]

12

19

48

75

0

20

40

60

80

100

2003-2005 2006-2008 2009-2011 2012-2014Cyber Fraud Natural disaster Product Finance / Legal Geopolitical Enviroment Reputation All

© 2015. For information, contact Deloitte Touche Tohmatsu LLC.Result of Crisis Management Survey 201427

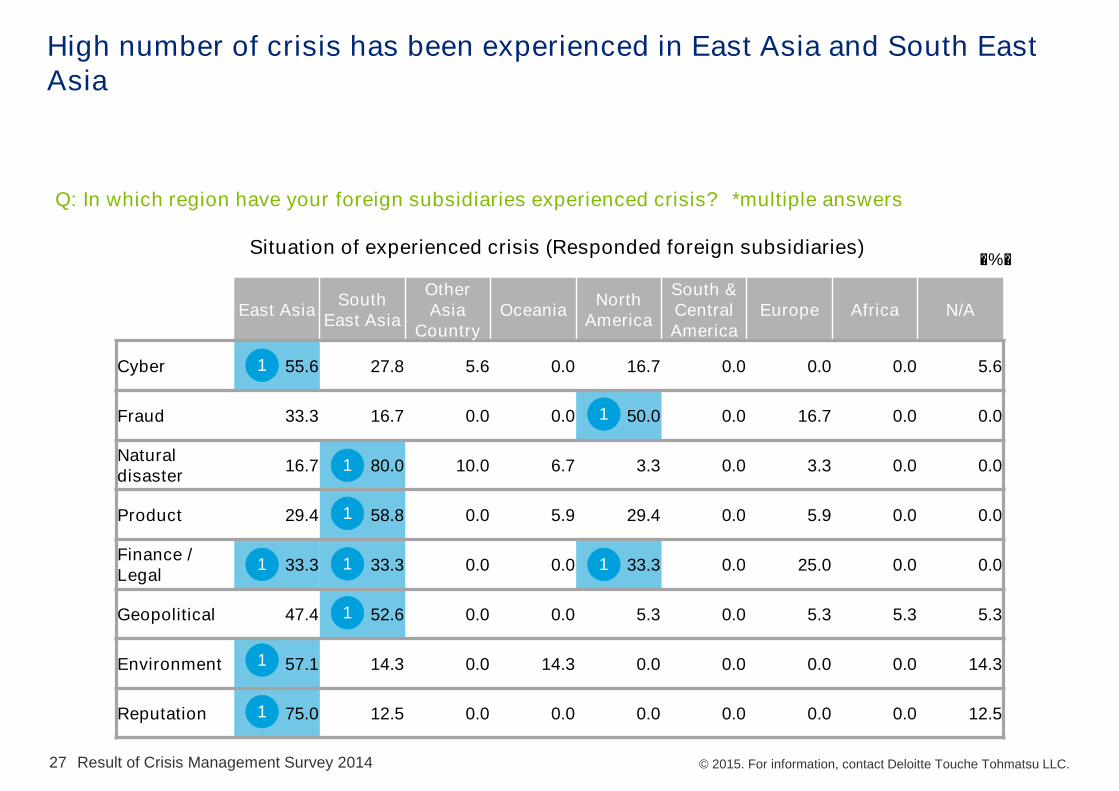

High number of crisis has been experienced in East Asia and South East Asia

Q: In which region have your foreign subsidiaries experienced crisis? *multiple answers

East Asia South East Asia

Other Asia

CountryOceania North

America

South & Central America

Europe Africa N/A

Cyber 55.6 27.8 5.6 0.0 16.7 0.0 0.0 0.0 5.6

Fraud 33.3 16.7 0.0 0.0 50.0 0.0 16.7 0.0 0.0

Naturaldisaster 16.7 80.0 10.0 6.7 3.3 0.0 3.3 0.0 0.0

Product 29.4 58.8 0.0 5.9 29.4 0.0 5.9 0.0 0.0

Finance / Legal 33.3 33.3 0.0 0.0 33.3 0.0 25.0 0.0 0.0

Geopolitical 47.4 52.6 0.0 0.0 5.3 0.0 5.3 5.3 5.3

Environment 57.1 14.3 0.0 14.3 0.0 0.0 0.0 0.0 14.3

Reputation 75.0 12.5 0.0 0.0 0.0 0.0 0.0 0.0 12.5

[%]

1

1

1

1

1

1

1

1

Situation of experienced crisis (Responded foreign subsidiaries)

1

1

© 2015. For information, contact Deloitte Touche Tohmatsu LLC.Result of Crisis Management Survey 201428

Foreign subsidiaries that have taken adequate countermeasures are not high

Q: What is the corresponding situation of each type of expected crisis?

2.9

4.6

1.7

4.6

8.1

5.8

7.5

10.4

28.3

31.8

33.5

35.8

34.7

39.3

43.4

40.5

9.2

5.8

8.1

11.0

9.8

11.0

11.6

8.7

17.9

16.2

16.8

20.8

17.9

15.6

13.9

15.0

13.3

9.8

16.2

7.5

7.5

11.6

5.8

6.4

15.6

17.3

9.8

7.5

8.1

4.6

5.8

5.8

12.8

14.5

13.9

12.8

13.9

12.1

12.0

13.2

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Reputation

Enviroment

Geopolitical

Finance /Legal

Product

Naturaldisaster

Fraud

Cyber

Very well prepared Prepared minimum countermeasures Under development of countermeasuresUnder consideration Not considered Not expected as crisisNon-response

Corresponding situation of expected crisis (Responded foreign subsidiaries)[Type of crisis]

© 2015. For information, contact Deloitte Touche Tohmatsu LLC.Result of Crisis Management Survey 201429

Corresponding situation of expected crisis within foreign subsidiaries is behind comparing to the parent company

Q: What is the corresponding situation of each type of expected crisis? (Comparing with the parent company)

2.9

4.6

1.7

4.6

8.1

5.8

7.5

10.4

28.3

31.8

33.5

35.8

34.7

39.3

43.4

40.5

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Reputation

Enviroment

Geopolitical

Finance /Legal

Product

Naturaldisaster

Fraud

Cyber

Very well prepared Prepared minimum countermeasures Under development of countermeasuresUnder consideration Not considered Not expected as crisisNon-response

Corresponding situation of expected crisis (Responded companies and foreign subsidiaries)[Type of crisis]

Total number of “Very well prepared” and “Prepared minimum countermeasure” of parent company

© 2015. For information, contact Deloitte Touche Tohmatsu LLC.Result of Crisis Management Survey 201430

Countermeasures are remained collection of info regarding crisis within foreign subsidiaries

Q: What kind of countermeasures has your foreign subsidiaries taken? (Only foreign subsidiaries answered “not considered countermeasures”) *multiple answers

5.4

40.5

5.4

41.9

17.6

55.4

0 20 40 60 80

5.1

30.8

17.9

47.4

23.1

53.8

0 20 40 60 80

ProductNatural disaster

5.6

31.5

0.0

29.6

13.0

66.7

0 20 40 60 80

9.5

41.3

6.3

38.1

12.7

55.6

0 20 40 60 80

ReputationEnvironment

5.7

38.6

2.3

39.8

11.4

56.8

0 20 40 60 80

8.0

36.4

6.8

37.5

17.0

63.6

0 20 40 60 80

Non-response

Regularlyreviewed andimprovement

of manual

Carry outtraining

Developmentof manuals

Developmentof expected

scenario

Collection ofinfo regarding

crisis

FraudCyber

8.2

24.6

1.6

27.9

13.1

67.2

0 20 40 60 80

7.1

35.7

0.0

31.4

14.3

61.4

0 20 40 60 80

Non-response

Regularlyreviewed andimprovement

of manual

Carry outtraining

Developmentof manuals

Developmentof expected

scenario

Collection ofinfo regarding

crisis

Geopolitical Finance / Legal

Member ofDeloitte Touche Tohmatsu Limited

Deloitte Touche Tohmatsu (Japan Group) is the name of the group consisting of member firms in Japan of Deloitte Touche Tohmatsu Limited (DTTL), a UK private company limited by guarantee, and Deloitte Touche Tohmatsu (Japan Group) provides services in Japan through Deloitte Touche Tohmatsu LLC, Deloitte Tohmatsu Consulting Co., Ltd., Deloitte Tohmatsu Financial Advisory Co., Ltd., Deloitte Tohmatsu Tax Co., and all of their respective subsidiaries and affiliates. Deloitte Touche Tohmatsu (Japan Group) is among the nation's leading professional services firms and each entity in Deloitte Touche Tohmatsu (Japan Group) provides services in accordance with applicable laws and regulations. The services include audit, tax, consulting, and financial advisory services which are delivered to many clients including multi-national enterprises and major Japanese business entities through nearly 7,900 professionals in almost 40 cities of Japan. For more information, please visit Deloitte Touche Tohmatsu (Japan Group)’s website at www.deloitte.com/jp/en.

Deloitte provides audit, consulting, financial advisory, risk management, tax and related services to public and private clients spanning multiple industries. With a globally connected network of member firms in more than 150 countries and territories, Deloitte brings world-class capabilities and high-quality service to clients, delivering the insights they need to address their most complex businesschallenges. Deloitte’s more than 210,000 professionals are committed to becoming the standard of excellence.

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee (“DTTL”), its network of member firms, and their related entities. DTTL and each of its member firms are legally separate and independent entities. DTTL (also referred to as “Deloitte Global”) does not provide services to clients. Please see www.deloitte.com/about for a more detailed description of DTTL and its member firms.

This communication contains general information only, and none of Deloitte Touche Tohmatsu Limited, its member firms, or their related entities (collectively, the “Deloitte Network”) is, by means of this communication, rendering professional advice or services. No entity in the Deloitte Network shall be responsible for any loss whatsoever sustained by any person who relies on this communication.

© 2015. For information, contact Deloitte Touche Tohmatsu LLC.