Restricted 11 Challenges to implementing global regulatory reform in Asia Presentation at IADI-DICGC...

19

Restricted 1 Challenges to implementing global regulatory reform in Asia Presentation at IADI-DICGC Conference on Role of Deposit Insurance in Bank Resolution Framework – Lessons from the Financial Crisis Jodhpur, India, 15 November 2011 Ilhyock Shim Senior Economist Bank for International Settlements * The views expressed here are those of the presenter, and do not necessarily represent those of the Bank for International Settlements.

-

Upload

willa-beasley -

Category

Documents

-

view

220 -

download

1

Transcript of Restricted 11 Challenges to implementing global regulatory reform in Asia Presentation at IADI-DICGC...

Restricted

11

Challenges to implementingglobal regulatory reform in Asia

Presentation at IADI-DICGC Conference on Role of Deposit Insurance in Bank Resolution Framework –

Lessons from the Financial Crisis

Jodhpur, India, 15 November 2011

Ilhyock ShimSenior Economist

Bank for International Settlements

* The views expressed here are those of the presenter, and do not necessarily represent those of the Bank for International Settlements.

Restricted

2

Overview

I. Global regulatory reform and its impact on Asia

– Revised micro-prudential capital regulation

– Macro-prudential capital regulation

– New micro-prudential liquidity regulation

– Impact of global regulatory reform on Asian banks

II. Macroprudential policy framework and deposit insurance

– Macroprudential policy framework and the G20

– Macroprudential policy framework and financial safety net

– Macroprudential policy framework and deposit insurance

Restricted

3

I. Global regulatory reformand its impact on Asia

Restricted

4

The reform of bank capital regulation

Overview

Capital ratio = Capital

Risk-weighted assets

Enhancing risk coverage● Securitisation products● Trading book● Counterparty credit risk

New capital ratio● Common equity● Tier 1● Total Capital● Capital conservation buffer

Raising the quality of capital● Focus on common equity● Stricter criteria for Tier 1● Harmonised deductions from capital

Macroprudential overlay

Mitigating procyclicality● Countercyclical buffer

Leverage ratio

Mitigating systemic risk● Capital surcharges● Contingent capital● Bail-in debt● OTC derivatives

4

Restricted

5

Capital ratio: the new requirements

Increases under Basel III are even greater when one considers the stricter definition of capital and enhanced risk weighting

In percentage of risk-weighted assets

Capital requirements

Common equity Tier 1 capital Total capital

MinimumConservation

bufferRequired Minimum Required Minimum Required

Basel II 2 4 8

Memo: Equivalent to around 1% for an average

international bank under the new definition

Equivalent to around 2% for an average

international bank under the new definition

Basel IIINew definition and calibration

4.5 2.5 7.0 6 8.5 8 10.5

Restricted

6

Leverage ratio Objectives

– Supplement the risk-based framework with a simple measure of total assets and off-balance sheet exposures

– Contain the build-up of leverage during boom periods– Introduce safeguards against model risk, measurement error and

attempts to “game” risk-based requirements Implementation

– Supervisory monitoring from 01.01.2011– Parallel run 01.01.2013 – 01.01.2017 3.0% Tier 1 leverage ratio– View to migrate the requirement to Pillar 1 on 01.01.2018 after

appropriate review and calibration– Need to monitor closely the relationship between risk weighted

assets and total assets which varies across countries

Restricted

7

Countercyclical capital buffer

Objective– Create a buffer of capital to protect the banking sector from periods of

excess aggregate credit growth– Ensure that adequate capital is on hand to maintain flow of credit

during stress Buffer decisions and reciprocity

– Each jurisdiction responsible for determining the buffer size (0 - 2.5%)– Buffer size is based upon the location of the exposure

Buffer calibration– Buffer size is determined through use of a credit/GDP guide and

judgement The BCBS also issued on 16 December 2010 “Guidance for national

authorities operating the countercyclical capital buffer” as a supplement to the requirements set out in the Basel III rules text.

Restricted

8

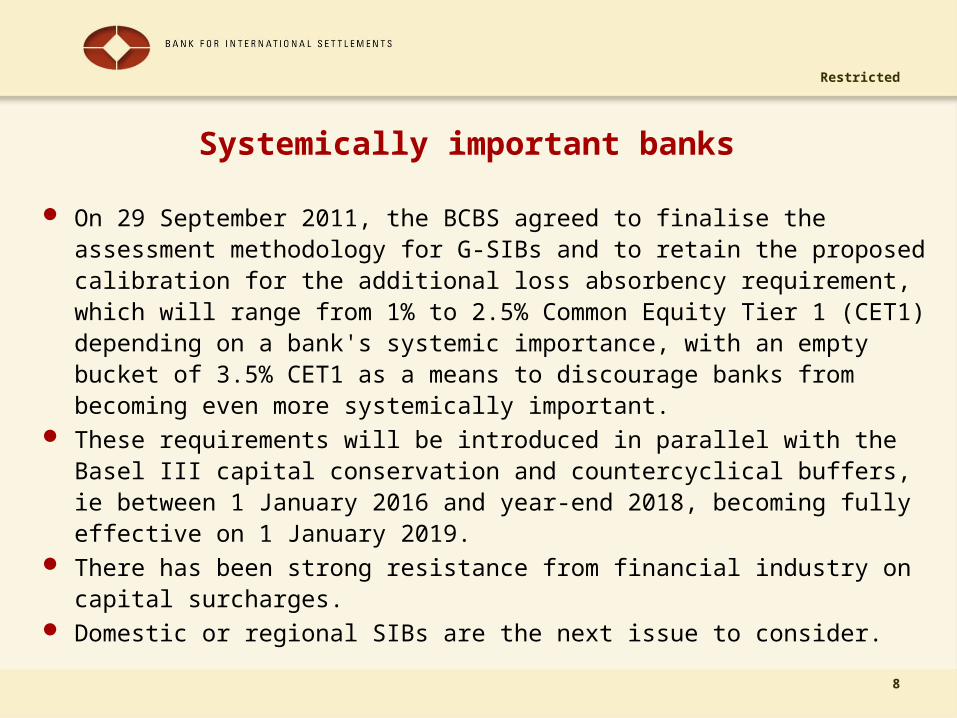

Systemically important banks

On 29 September 2011, the BCBS agreed to finalise the assessment methodology for G-SIBs and to retain the proposed calibration for the additional loss absorbency requirement, which will range from 1% to 2.5% Common Equity Tier 1 (CET1) depending on a bank's systemic importance, with an empty bucket of 3.5% CET1 as a means to discourage banks from becoming even more systemically important.

These requirements will be introduced in parallel with the Basel III capital conservation and countercyclical buffers, ie between 1 January 2016 and year-end 2018, becoming fully effective on 1 January 2019.

There has been strong resistance from financial industry on capital surcharges.

Domestic or regional SIBs are the next issue to consider.

Restricted

9

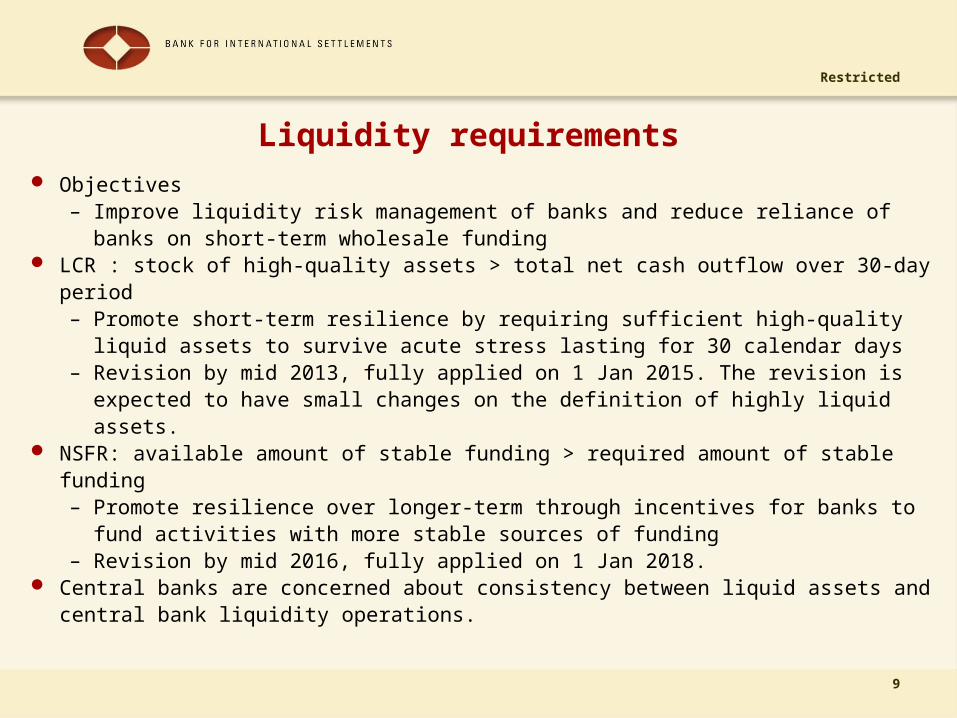

Liquidity requirements

Objectives– Improve liquidity risk management of banks and reduce reliance of banks

on short-term wholesale funding LCR : stock of high-quality assets > total net cash outflow over 30-day period

– Promote short-term resilience by requiring sufficient high-quality liquid assets to survive acute stress lasting for 30 calendar days

– Revision by mid 2013, fully applied on 1 Jan 2015. The revision is expected to have small changes on the definition of highly liquid assets.

NSFR: available amount of stable funding > required amount of stable funding– Promote resilience over longer-term through incentives for banks to fund

activities with more stable sources of funding– Revision by mid 2016, fully applied on 1 Jan 2018.

Central banks are concerned about consistency between liquid assets and central bank liquidity operations.

Restricted

10

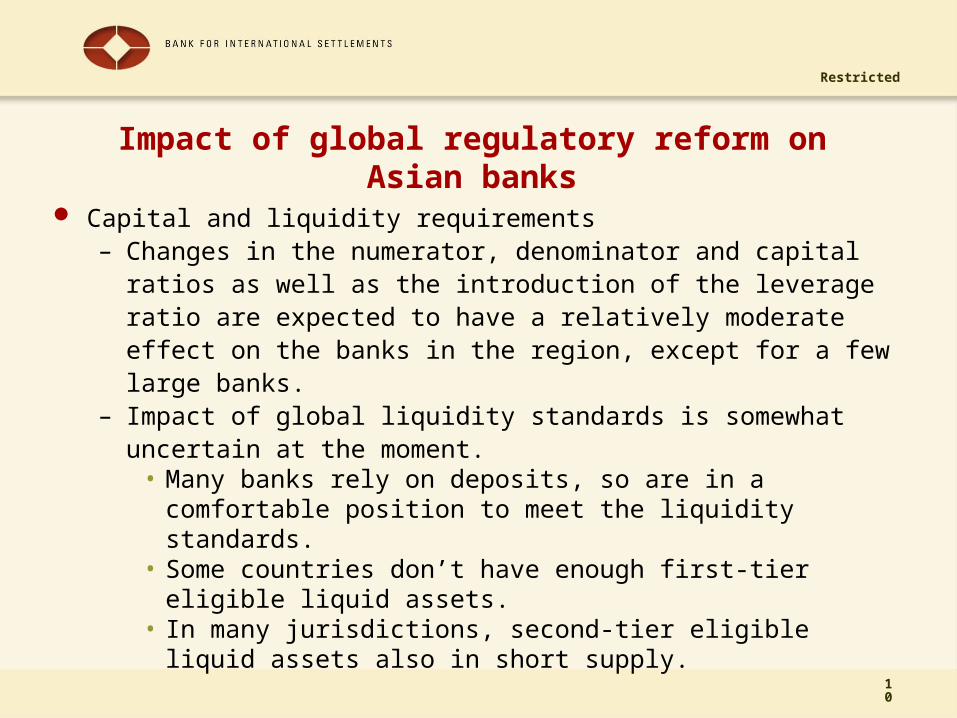

Impact of global regulatory reform on Asian banks

Capital and liquidity requirements – Changes in the numerator, denominator and capital ratios as well

as the introduction of the leverage ratio are expected to have a relatively moderate effect on the banks in the region, except for a few large banks.

– Impact of global liquidity standards is somewhat uncertain at the moment.

• Many banks rely on deposits, so are in a comfortable position to meet the liquidity standards.

• Some countries don’t have enough first-tier eligible liquid assets.

• In many jurisdictions, second-tier eligible liquid assets also in short supply.

Restricted

11

Impact of global regulatory reform on Asian banks

Capital flows and FX liquidity risk– The recent crisis clearly showed that dependence on short-

term, wholesale and cross-border lending corresponded to increased vulnerabilities.

– Current liquidity regulation does not have specific provisions for FX funding liquidity risk or maturity mismatches for each currency.

• At a minimum, aggregated across transferable and convertible currencies.

• Currency composition of LCR buffer should broadly match the currency composition of net cash outflows.

Restricted

12

Impact of global regulatory reform on Asian banks

Macroprudential perspective

– Many authorities in the region have built up invaluable experience over the past two decades in using monetary, prudential and fiscal measures to address procyclicality.

– However, risk management systems at the firm level are still relatively weak

• Micro and macro stress testing

• Data requirement

• Analytical capacity

Restricted

13

Impact of global regulatory reform on Asian banks

Credit provision to support growth– In some countries, strong demand for bank loans exists to

support strong growth and upgrade standards of living• Infrastructure and real estate loans

– Can Basel III support these loans effectively? • In particular, given that it is relatively more difficult for banks

to raise capital in the market in Asia, any expansion of bank balance sheets may not be easily supported by increases in bank equity unless banks have strong profits.

• Also, new liquidity regulation such as NSFR may hinder investment in long-term risky projects.

– Overall, the long-term benefit of higher and stronger capital base will outweigh the potential short-term cost in Asia and the Pacific.

Restricted

14

Impact of global regulatory reform on Asian banks Treatment of trade finance under Basel capital framework

– G20 leaders at the 2011 Seoul Summit decided to “evaluate the impact of regulatory regimes on trade finance”.

– The BCBS established Trade Finance Group, had consultations with the World Bank, WTO and the International Chamber of Commerce.

– 100% Credit Conversion Factor in calculating the leverage ratio for contingent trade finance exposures: need exception for trade finance?

• CCF is determined by the likelihood of off-b/s position becoming an on-b/s item, and whether commitments are unconditionally cancellable.

– 20% Credit Conversion Factor for short-term self-liquidating trade letters of credit under the risk-based measure: need to lower it?

• CCF is determined by the likelihood of off-b/s position becoming an on-b/s item, not by the probability of default of a trade finance instrument

– One-year maturity floor when calculating RWAs under the Advanced IRB: inappropriate for short-term self-liquidating letters of credit?

• The BCBS agree to waive the floor and use a maturity less than one year.– Sovereign floor of risk weighting for to short-term self-liquidating letters of credit

• The BCBS decided to waive it: for low-income countries, the risk-weighting decreases from 100% to 50% or even 20%.

Restricted

15

II. Macroprudential policy framework and deposit insurance

Restricted

1616

2010 G20 SEOUL SUMMIT DOCUMENT, Paragraph 41, first bullet

“Further work on macro-prudential policy frameworks: In order to deal with systemic risks in the financial sector in a comprehensive manner and on an ongoing basis, we called on the FSB, IMF and BIS to do further work on macro-prudential policy frameworks, including tools to mitigate the impact of excessive capital flows, and update our Finance Ministers and Central Bank Governors at their next meeting.”

2011 G20 Cannes SUMMIT DOCUMENT

“ tbc ”

Macroprudential policy in the G20 process

Restricted

1717

Macroprudential policy and financial safety nets

Three lines of defence to minimise the impact of a systemic distress

(1) ex-ante regulation and supervision to provide the right incentive to discourage excessive risk-taking at an institutional level and in a system

(2) buffers maintained by financial institutions or by the financial system against realized losses and liquidity shocks

(3) financial safety nets provided by national authorities. Important to maintain consistency between the macroprudential policy

framework and financial safety net arrangements. – If financial safety net is strong, the moral hazard problem is likely to

occur. Thus, we need to introduce strict regulation to avoid risk-taking by financial institutions.

– If financial safety net is weak, financial institutions need to maintain more buffers to reduce the probability and extent of relying on the safety net.

Restricted

1818

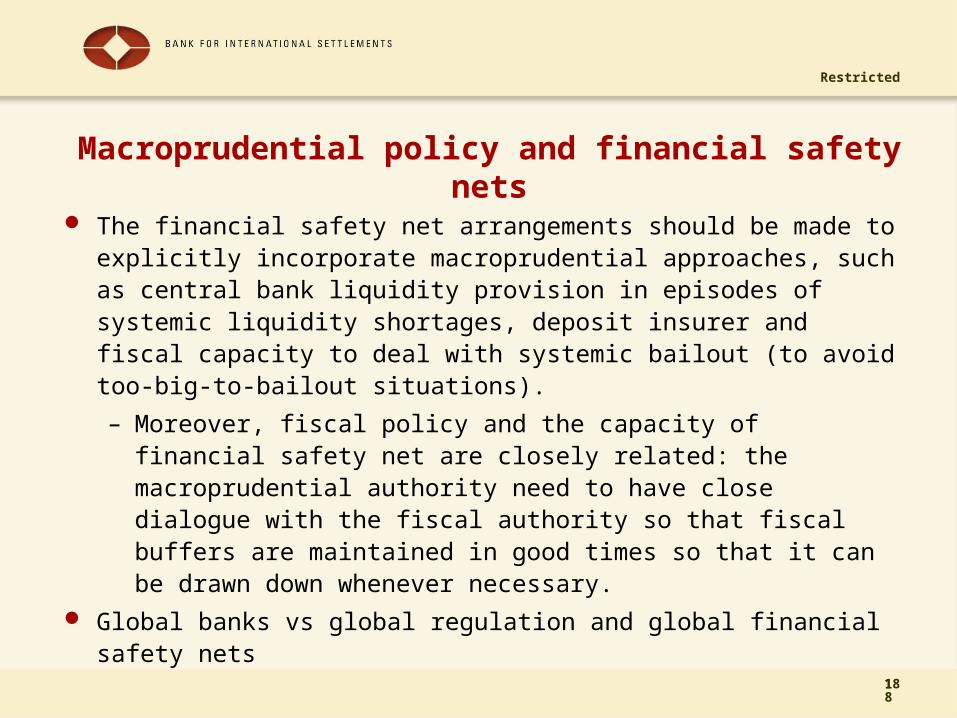

Macroprudential policy and financial safety nets

The financial safety net arrangements should be made to explicitly incorporate macroprudential approaches, such as central bank liquidity provision in episodes of systemic liquidity shortages, deposit insurer and fiscal capacity to deal with systemic bailout (to avoid too-big-to-bailout situations).

– Moreover, fiscal policy and the capacity of financial safety net are closely related: the macroprudential authority need to have close dialogue with the fiscal authority so that fiscal buffers are maintained in good times so that it can be drawn down whenever necessary.

Global banks vs global regulation and global financial safety nets

Restricted

1919

Macroprudential policy and deposit insurance

Do deposit insurers need to have a macroprudential perspective (systemic risk and procyclicality)?

Did micro-prudential Prompt Corrective Action work during the recent international financial crisis? How about systemic risk exception?– If not, why? How to revise it?

Since the crisis, a lot of progress has been made in designing regulation to mitigate both procyclicality and systemic risk.

What are the roles deposit insurers play in the macro-prudential policy framework? – What specific roles deposit insurers should play in financial

stability or macroprudential council?– What funding arrangements, deposit insurance premium,

coverage, and cross-border coordination of deposit insurance?