Responsible Credit. The Portuguese Experience.

33

Regional Conference on Consumer Protection and Financial Literacy World Bank and Financial Sector Commission of Bulgaria 10 June 2014 Maria Lúcia Leitão • Head of the Banking Conduct Supervision Department RESPONSIBLE CREDIT The Portuguese Experience

-

Upload

financial-sector-advisory-centre-the-world-bank -

Category

Economy & Finance

-

view

96 -

download

0

Transcript of Responsible Credit. The Portuguese Experience.

Regional Conference on Consumer Protection and Financial Literacy World Bank and Financial Sector Commission of Bulgaria 10 June 2014

Maria Lúcia Leitão • Head of the Banking Conduct Supervision Department

RESPONSIBLE CREDIT

The Portuguese Experience

2 •

RESPONSIBLE CREDIT

Regional Conference on Consumer Protection and Financial Literacy

10 June 2014

RESPONSIBLE CREDIT: a comprehensive approach

• Responsible credit embraces:

Responsible lending

Responsible borrowing

Responsible management of pre-arrears and arrears

• Responsible credit shall cover all phases of the credit life cycle:

Prior to the conclusion of the credit agreement

During the lifetime of the credit agreement

In the renegotiation of credit agreements in pre-arrears or arrears

3 •

3. Equitable and Fair Treatment of Consumers

All financial consumers should be treated equitably, honestly and fairly at all stages of their relationship with financial service providers. (…)

5. Financial Education and Awareness

Financial education and awareness should be promoted by all relevant stakeholders and clear information on consumer protection, rights and responsibilities should be easily accessible by consumers. (…) The provision of broad based financial education and information to deepen consumer financial knowledge and capability should be promoted, especially for vulnerable groups. (…)

Regional Conference on Consumer Protection and Financial Literacy

RESPONSIBLE CREDIT

OECD G20 Principles on Financial Consumer Protection

10 June 2014

4 •

RESPONSIBLE CREDIT

Regional Conference on Consumer Protection and Financial Literacy

10 June 2014

RESPONSIBLE LENDING

• Credit institutions shall grant credit in a prudent, honest and transparent manner

• Responsible lending practices promote:

Credit risk control, thus contributing to reinforce credit institutions’ prudential soundness and the safeguard of financial stability

Consumer protection, by ensuring that the credit products offered are suitable to each customer’s needs and financial capacity

• Prudential supervision and conduct of business supervision pursue the same goal

5 •

RESPONSIBLE CREDIT

Regional Conference on Consumer Protection and Financial Literacy

10 June 2014

The principles of RESPONSIBLE LENDING

• Responsible lending is mostly based on the following principles

Non-misleading advertising

Provision of complete and accurate information to customers

Customer assistance

Suitability assessment

Creditworthiness assessment

“Fairness for consumers of financial services and products can be achieved through a range of

protection measures such as fair and clear advertising, improved transparency […],

standardised information, […] assessments of creditworthiness/suitability, sound and clear

advice […].”

6 •

RESPONSIBLE CREDIT

Regional Conference on Consumer Protection and Financial Literacy

10 June 2014

Implementation of RESPONSIBLE LENDING principles

• Advertisement: How to ensure effective oversight (ex-ante vs ex-post approach)?

• Provision of information: Standardised information sheet / Monthly statements Mystery shopping proves to be effective

• Customers’ assistance: Assistance vs counselling? Training of staff is a priority

• Suitability: Standard products should be offered to improve comparability Cross-selling

• Creditworthiness: Which level of Loan-to-value / Loan-to-income? How to assure creditworthiness

during the lifetime of the loan?

7 •

RESPONSIBLE CREDIT

Regional Conference on Consumer Protection and Financial Literacy

10 June 2014

RESPONSIBLE BORROWING

• Customers should make informed and responsible credit decisions

• For that purpose, customers should:

Be capable of interpreting and understanding information on the credit product

Assess if the credit product offered suits their needs and financial capacity

• Financial education is the key for responsible borrowing

“Through studies and research on behavioural economics, supervisors and

regulators can try to identify the capabilities of consumers, as well as the decision making pitfalls that result from

biases and heuristics.”

8 •

RESPONSIBLE CREDIT

Regional Conference on Consumer Protection and Financial Literacy

10 June 2014

RESPONSIBLE CREDIT in the Consumer Credit Directive (CCD)

• The CCD establishes principles and rules to promote responsible credit practices

Advertisement: standard information in advertisement of consumer credit products (representative example)

Information duties: provision of complete and accurate pre-contractual and contractual information - standardised information sheet (SIS)/annual percentage rate of charge (APR)

Customer assistance/suitability: provision of adequate explanations to customers /right of withdrawal (14 calendar days)

Creditworthiness assessment: obligation to consult credit registry databases

• Credit intermediaries shall also observe these rules

9 •

RESPONSIBLE CREDIT

Regional Conference on Consumer Protection and Financial Literacy

10 June 2014

RESPONSIBLE CREDIT in the Mortgage Credit Directive (MCD)

• The MCD extends the principles and rules laid down in the CCD to mortgage credit and sets out new rules on responsible credit

Customer assistance / suitability:

Requires relevant staff to have an adequate level of knowledge of the products Establishes rules for staff remuneration (sales incentives under scrutiny) Sets out rules on the provision of advisory services

Creditworthiness assessment: obligation to make a thorough and prospective assessment of the consumer’s creditworthiness

Responsible borrowing: measures to promote financial education of consumers

Management of pre-arrears and arrears : imposes measures to avoid foreclosure

• The MCD also establishes specific rules on credit intermediaries

10 •

RESPONSIBLE CREDIT

Regional Conference on Consumer Protection and Financial Literacy

10 June 2014

RESPONSIBLE CREDIT in the perspective of the European Banking Authority

• Opinion of the EBA on Good Practices for Responsible Mortgage Lending (2013):

Make reasonable inquiries to confirm customers’ financial capacity

Ensure a reasonable debt service coverage

Establish prudent loan-to-value ratios

Ensure that credit is refused when minimum requirements are not met

11 •

RESPONSIBLE CREDIT

Regional Conference on Consumer Protection and Financial Literacy

10 June 2014

RESPONSIBLE CREDIT in the perspective of the European Banking Authority

• Opinion of the EBA on Good Practices for the Treatment of Borrowers in Mortgage Payment Difficulties (2013):

Act honestly, fairly and professionally

Implement internal policies for dealing with distressed borrowers

Provide information and assistance to borrowers

When viable, offer renegotiation solutions to borrowers to avoid foreclosure

12 •

RESPONSIBLE CREDIT

Regional Conference on Consumer Protection and Financial Literacy

10 June 2014

RESPONSIBLE LENDING in Portugal: advertisement of credit products

• Advertising campaigns on all banking products and services must observe disclosure rules

• Banco de Portugal (2008) defined enforceable rules on accuracy and transparency of information; balanced information on advantages and access conditions and restrictions

• Main features of the supervisory model adopted:

Ex-post supervision (except ex-ante for structured deposits)

Mixed principle and ruled-based regulation

Risk-based approach

All the different means of communication are under scrutiny (TV, outdoors, mail shots, internet, booklets,…)

13 •

RESPONSIBLE CREDIT

Regional Conference on Consumer Protection and Financial Literacy

10 June 2014

RESPONSIBLE LENDING in Portugal: advertisement of credit products

Before After

It’s mine for only

€15/month

It’s mine for only

€15/month x 48m for every €500

APRC of 21.6% for a 48-month credit of €500 with an annual interest rate of 16%. Total amount payable

by the consumer of €724.50 APRC of 21.6% for a 48-month credit of €500 with an

annual interest rate of 16%

ABC Bank ABC Bank

14 •

RESPONSIBLE CREDIT

Regional Conference on Consumer Protection and Financial Literacy

10 June 2014

RESPONSIBLE LENDING in Portugal: price lists

• Banco de Portugal (2008) set forth requirements for the release of information on fees, expenses and interest rates regarding retail banking products and services

• Price lists allow for a comparison of products while increasing competition

• Price lists are available at every counter and on credit institutions’ websites

• Banco de Portugal’s Bank Customer Website displays the price lists of all credit institutions

Bank Customer Website http://clientebancario.bportugal.pt)

Harmonised template

http://clientebancario.bportugal.pt/pt-PT/DireitosdosClientes/DireitoInformacao/Precarios/Paginas/Precarios.aspx

15 •

RESPONSIBLE CREDIT

Regional Conference on Consumer Protection and Financial Literacy

10 June 2014

RESPONSIBLE LENDING in Portugal: consumer credit

• Banco de Portugal (2009), following the transposition of the CCD, issued a notice on the provision of pre-contractual and contractual information (Standardised Information Sheet)

• A maximum interest rate regime for consumer credit has been in place in Portugal since January 2010

Banco de Portugal publishes the maximum interest rates for new credit agreements on a quarterly basis

• Banco de Portugal is now conducting a public consultation on a notice imposing the provision of regular information to customers during the lifetime of the credit agreement (Monthly statements)

Standardised Information Sheet

16 •

RESPONSIBLE CREDIT

Regional Conference on Consumer Protection and Financial Literacy

10 June 2014

RESPONSIBLE LENDING in Portugal: mortgage credit

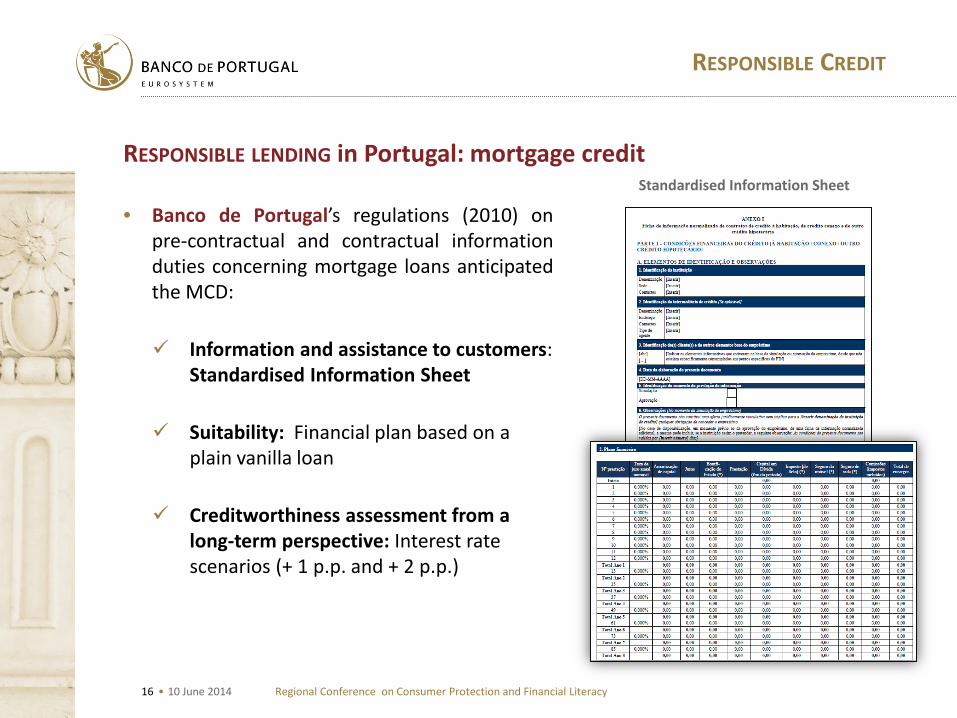

• Banco de Portugal’s regulations (2010) on pre-contractual and contractual information duties concerning mortgage loans anticipated the MCD:

Information and assistance to customers: Standardised Information Sheet

Suitability: Financial plan based on a plain vanilla loan

Creditworthiness assessment from a long-term perspective: Interest rate scenarios (+ 1 p.p. and + 2 p.p.)

Standardised Information Sheet

17 •

RESPONSIBLE CREDIT

Regional Conference on Consumer Protection and Financial Literacy

10 June 2014

RESPONSIBLE BORROWING in Portugal: financial information

• Banco de Portugal actively participates in courses and seminars on legal and regulatory developments in the retail banking market

Leaflets on consumer credit

Leaflet on mortgage credit

• Banco de Portugal disseminates information to consumers and to the industry on banking products and services, through the publication of leaflets and flyers and through the Bank Customer Website

18 •

RESPONSIBLE CREDIT

Regional Conference on Consumer Protection and Financial Literacy

10 June 2014

RESPONSIBLE BORROWING in Portugal: financial information

• The Bank Customer Website (www.clientebancario.bportugal.pt) was created by Banco de Portugal in 2007

19 •

RESPONSIBLE CREDIT

Regional Conference on Consumer Protection and Financial Literacy

10 June 2014

RESPONSIBLE BORROWING in Portugal: financial education

• Banco de Portugal participates actively in the Portuguese National Plan for Financial Education managed by the National Council of Financial Supervisors (Banco de Portugal, Insurance and Pension Funds Supervisory Authority and Securities Market Commission).

• The National Plan for Financial Education:

Was launched in 2011 as a framework for financial education projects

Has adopted high-level principles for financial education initiatives (e.g. to prevent conflicts of interest)

Follows the best international practices of the International Network on Financial Education (INFE)

Supports the implementation and coordination of financial education initiatives targeted at various population groups

20 •

RESPONSIBLE CREDIT

Regional Conference on Consumer Protection and Financial Literacy

10 June 2014

RESPONSIBLE BORROWING in Portugal: financial education

• The “Todos Contam” Website (www.todoscontam.pt) was created in 2012 and is the dedicated website of the National Plan for Financial Education

21 •

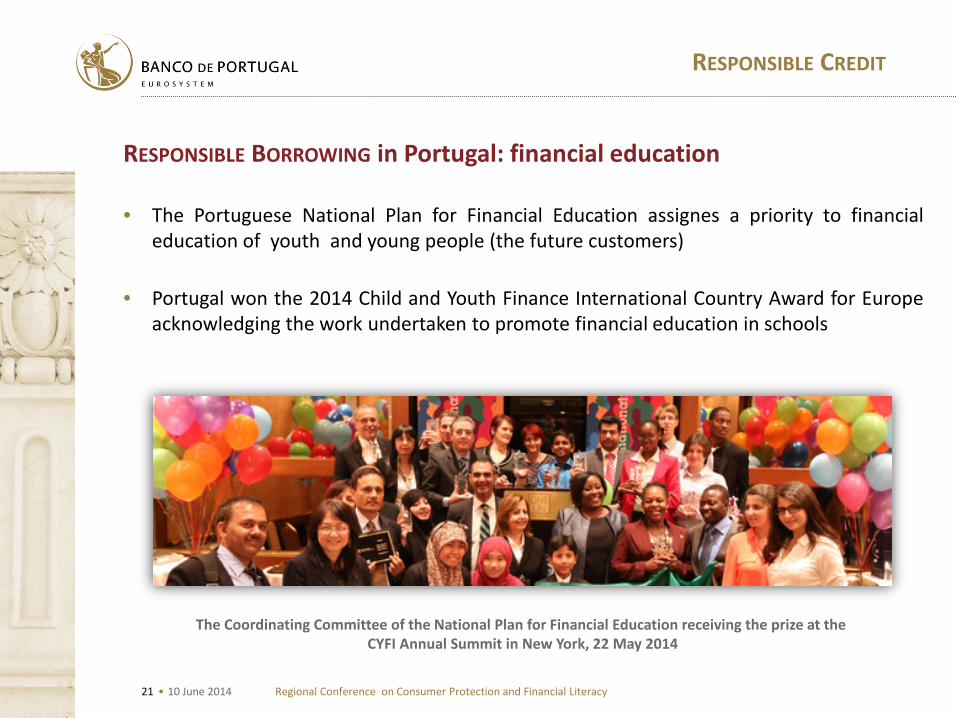

• The Portuguese National Plan for Financial Education assignes a priority to financial education of youth and young people (the future customers)

• Portugal won the 2014 Child and Youth Finance International Country Award for Europe acknowledging the work undertaken to promote financial education in schools

RESPONSIBLE CREDIT

Regional Conference on Consumer Protection and Financial Literacy

10 June 2014

RESPONSIBLE BORROWING in Portugal: financial education

The Coordinating Committee of the National Plan for Financial Education receiving the prize at the CYFI Annual Summit in New York, 22 May 2014

22 •

RESPONSIBLE CREDIT

Regional Conference on Consumer Protection and Financial Literacy

10 June 2014

MANAGEMENT OF PRE-ARREARS AND ARREARS SITUATIONS

• Responsible credit also entails responsible management of pre-arrears and arrears situations

• As important as granting credit in a responsible manner is ensuring that the existing loans are repaid, despite of unexpected events

• Portugal now has a comprehensive legal and regulatory framework to deal with pre-arrears and arrears on credit agreements with household customers, which already covers:

The rules set out in the MCD on the management of arrears

The EBA Opinion on Good Practices for the Treatment of Borrowers in Mortgage Payment Difficulties

23 •

RESPONSIBLE CREDIT

Regional Conference on Consumer Protection and Financial Literacy

10 June 2014

• The Portuguese model is applicable to all credit agreements signed with household customers

• The General Regime adopted a non-intrusive approach, focused on the procedures credit institutions should follow when dealing with pre-arrears and arrears situations…

• … complemented with specific rules for arrears on housing loan agreements

• Based on the negotiation between the credit institution and the customer, with the support of an Assistance Network for Indebted Consumers

• Subject to permanent and systematic oversight and assessment by Banco de Portugal

Brochure on the prevention and settlement of arrears

MANAGEMENT OF PRE-ARREARS AND ARREARS in Portugal

http://clientebancario.bportugal.pt/SiteCollectionDocuments/Prevention%20and%20settlement%20of%20arrears%20on%20credit%20agreements%20with%20private%

20bank%20customers.pdf

24 •

RESPONSIBLE CREDIT

Regional Conference on Consumer Protection and Financial Literacy

10 June 2014

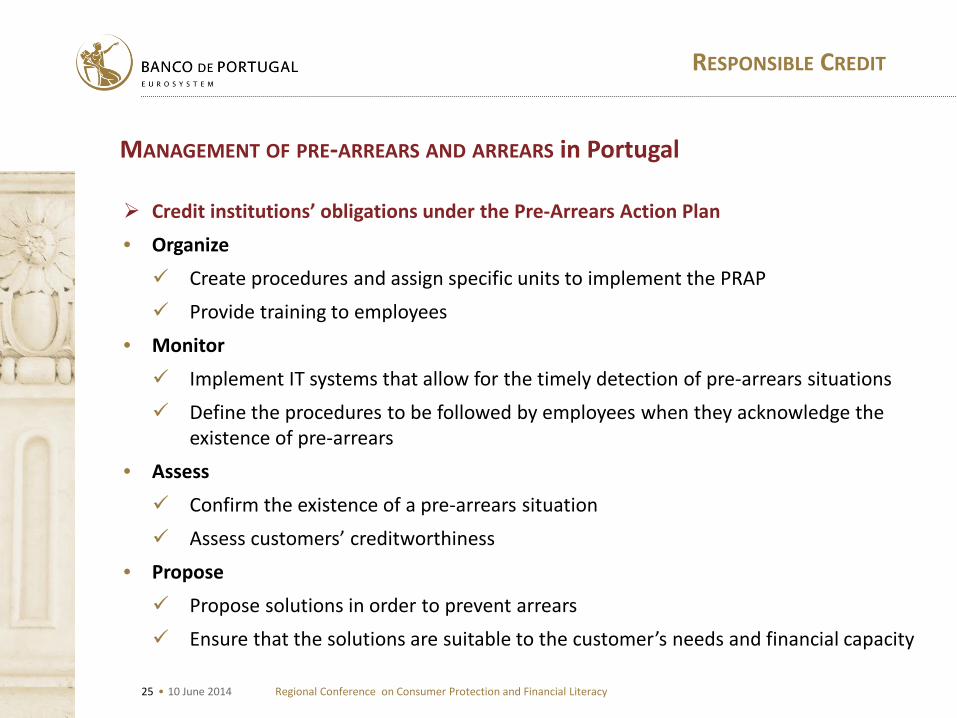

• The General Regime requires credit institutions to implement a Pre-arrears Action Plan (PRAP), describing the procedures adopted to monitor credit agreements and manage pre-arrears situations

• Sets out a negotiation model for the out-of-court settlement of arrears situations – the Out-of-court Arrears Settlement Procedure (OASP)

• Credit institutions are obliged to assess customers’ creditworthiness and, when viable, negotiate suitable debt restructuring solutions

• Household customers have the right to be informed on their situation and benefit from a series of guarantees, but are required to cooperate during the negotiation process

Arrears prevention

Pre-arrears Action Plan

Arrears resolution Out-of-court Arrears

Settlement Procedure

MANAGEMENT OF PRE-ARREARS AND ARREARS in Portugal

25 •

RESPONSIBLE CREDIT

Regional Conference on Consumer Protection and Financial Literacy

10 June 2014

Credit institutions’ obligations under the Pre-Arrears Action Plan • Organize Create procedures and assign specific units to implement the PRAP Provide training to employees

• Monitor Implement IT systems that allow for the timely detection of pre-arrears situations Define the procedures to be followed by employees when they acknowledge the

existence of pre-arrears • Assess Confirm the existence of a pre-arrears situation Assess customers’ creditworthiness

• Propose Propose solutions in order to prevent arrears Ensure that the solutions are suitable to the customer’s needs and financial capacity

MANAGEMENT OF PRE-ARREARS AND ARREARS in Portugal

26 •

RESPONSIBLE CREDIT

Regional Conference on Consumer Protection and Financial Literacy

10 June 2014

The Out-of-Court Arrears Settlement Procedure

Negotiation

Default

Beginning of the OASP

Credit institution informs the

customer of the beginning of the

OASP

Assessment and presentation of

proposals

First contact with the customer

15 days

31 –

60

days

5 days

30 days

90 days

MANAGEMENT OF PRE-ARREARS AND ARREARS in Portugal

27 •

RESPONSIBLE CREDIT

Regional Conference on Consumer Protection and Financial Literacy

10 June 2014

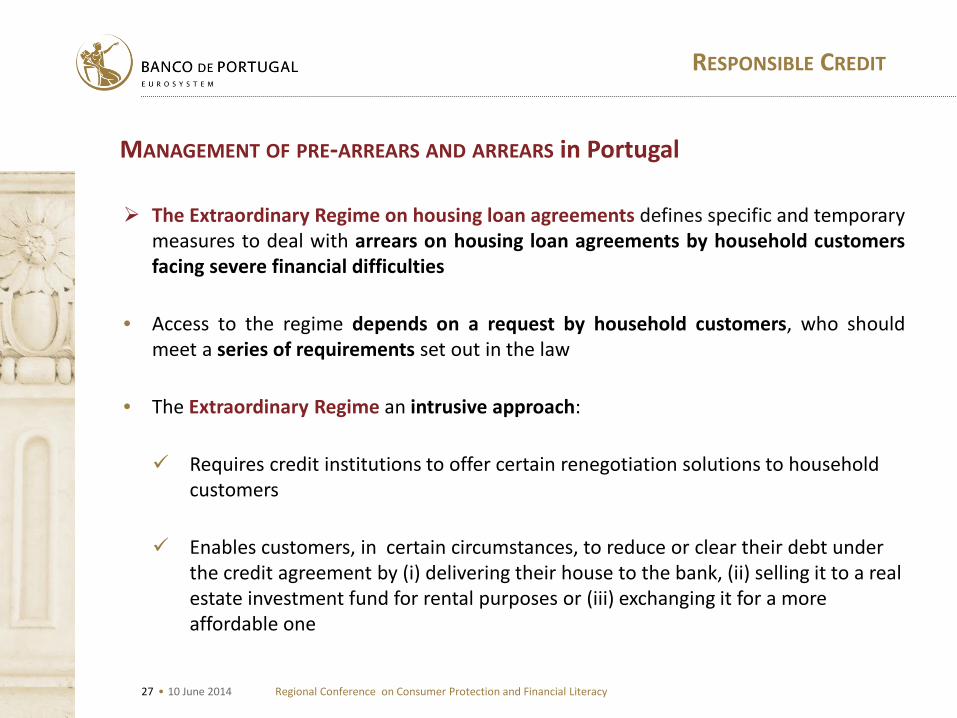

The Extraordinary Regime on housing loan agreements defines specific and temporary measures to deal with arrears on housing loan agreements by household customers facing severe financial difficulties

• Access to the regime depends on a request by household customers, who should meet a series of requirements set out in the law

• The Extraordinary Regime an intrusive approach:

Requires credit institutions to offer certain renegotiation solutions to household customers

Enables customers, in certain circumstances, to reduce or clear their debt under the credit agreement by (i) delivering their house to the bank, (ii) selling it to a real estate investment fund for rental purposes or (iii) exchanging it for a more affordable one

MANAGEMENT OF PRE-ARREARS AND ARREARS in Portugal

28 •

RESPONSIBLE CREDIT

Regional Conference on Consumer Protection and Financial Literacy

10 June 2014

• The success of a negotiation approach to deal with pre-arrears and arrears situations requires the creation of mechanisms to assist and inform indebted customers

• The Assistance Network for Indebted Consumers comprises private and public legal entities fulfilling a set of requirements and accredited by the General Directorate for Consumers, following an opinion of Banco de Portugal

• Indebted consumers may apply to the network to obtain, on a free-of-charge basis, information, advice and assistance

• Banco de Portugal has been involved in several initiatives across the country to train the network’s entities

MANAGEMENT OF PRE-ARREARS AND ARREARS in Portugal

29 •

RESPONSIBLE CREDIT

Regional Conference on Consumer Protection and Financial Literacy

10 June 2014

THE ASSISTANCE NETWORK FOR INDEBTED CONSUMERS in Portugal www.todoscontam.pt

30 •

RESPONSIBLE CREDIT

Regional Conference on Consumer Protection and Financial Literacy

10 June 2014

• Credit institutions have improved their internal procedures and information systems to ensure comprehensive and centralised management of pre-arrears and arrears situations and the provision of information to Banco de Portugal

• Faster intervention by credit institutions allowed for the settlement of a large number of arrears situations, either through the payment of overdue amounts or debt restructuring

Overdue period at the beginning of the OASP

0%10%20%30%40%50%60%70%80%90%

100%

Regular or arrears up to 60 days

Arrears between 61 and 90 days

Arrears between 91 and 365 days

Arrears for more than 365 days

ASSESSING THE MANAGEMENT OF PRE-ARREARS AND ARREARS in Portugal

31 •

RESPONSIBLE CREDIT

Regional Conference on Consumer Protection and Financial Literacy

10 June 2014

• A non-intrusive approach to deal with pre-arrears and arrears, based on the credit institutions’ procedures, may not have an immediate impact on the reduction of credit default rates, especially in a context of economic and financial constraints

• The impact of the General Regime will be mainly reflected on the effectiveness of credit institutions’ procedures and systems to manage pre-arrears and arrears situations and therefore should be assessed from a medium/long-term perspective

• The limited impact of the Extraordinary Regime suggests that:

A model based on the customers’ initiative is likely to be less effective than one based on the credit institutions’ initiative

The definition of access requirements should be well balanced, in order to (i) ensure the effectiveness of the regime and (ii) prevent moral hazard

ASSESSING THE MANAGEMENT OF PRE-ARREARS AND ARREARS in Portugal

32 •

RESPONSIBLE CREDIT

Regional Conference on Consumer Protection and Financial Literacy

10 June 2014

Active oversight to ensure RESPONSIBLE CREDIT

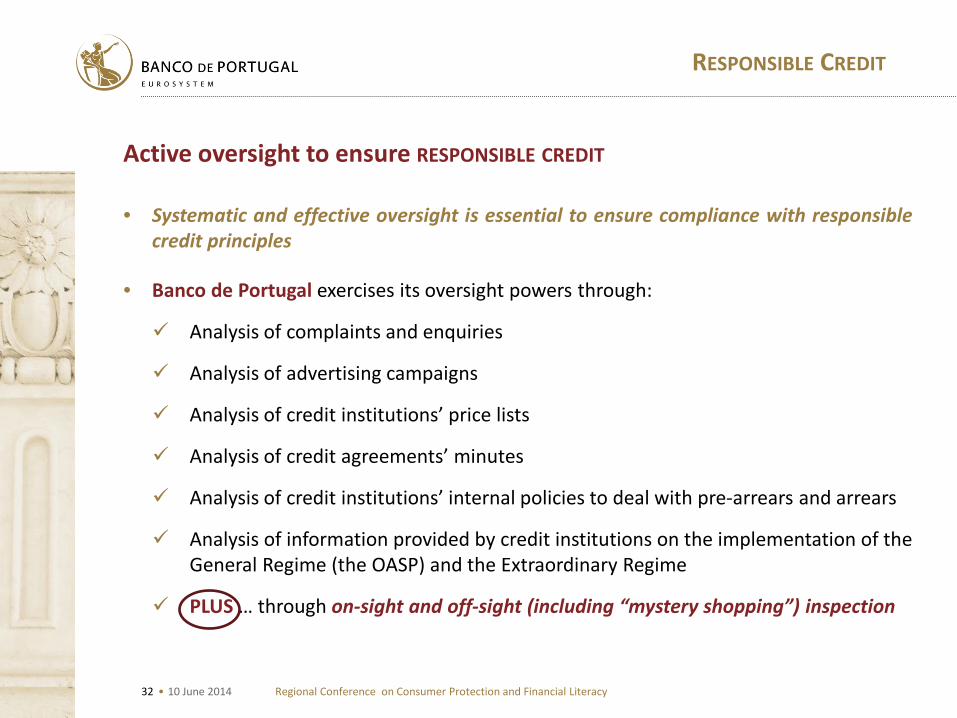

• Systematic and effective oversight is essential to ensure compliance with responsible credit principles

• Banco de Portugal exercises its oversight powers through:

Analysis of complaints and enquiries

Analysis of advertising campaigns

Analysis of credit institutions’ price lists

Analysis of credit agreements’ minutes

Analysis of credit institutions’ internal policies to deal with pre-arrears and arrears

Analysis of information provided by credit institutions on the implementation of the General Regime (the OASP) and the Extraordinary Regime

PLUS … through on-sight and off-sight (including “mystery shopping”) inspection

Regional Conference on Consumer Protection and Financial Literacy World Bank and Financial Sector Commission of Bulgaria 10 June 2014

Maria Lúcia Leitão • Head of the Banking Conduct Supervision Department

RESPONSIBLE CREDIT

The Portuguese Experience