Responding to a fundamental shift in regulatory expectations · 1 Conduct risk for insurersR...

36

Conduct risk for insurers Responding to a fundamental shift in regulatory expectations

Transcript of Responding to a fundamental shift in regulatory expectations · 1 Conduct risk for insurersR...

Conduct risk for insurersResponding to a fundamental shift in regulatory expectations

1 Conduct risk for insurers: Responding to a fundamental shift in regulatory expectations

contentsContents3 Welcome

5 Executive Summary

7 1. The conduct era: more than just a risk type

8 2. Insurer perspectives and industry reaction

15 3. Moving beyond TCF

22 4. The response

30 5. The insurance industry working together

31 6. Conclusion

32 Appendix: List of participating firms

33 Who to contact

2 Conduct risk for insurers: Responding to a fundamental shift in regulatory expectations

This is a joint report from Oliver Wyman and the Chartered Insurance Institute.

AcknowledgementsTheauthorswouldliketothanktheCIIforitssupportandinputtothisreport.Theyare

alsogratefultonumerousindustryparticipantsfortheirtimeandthethoughtfulnessof

theircontributions.

3 Conduct risk for insurers: Responding to a fundamental shift in regulatory expectations

Message from Oliver Wyman

We interviewed twenty two CEOs and senior executives from across the UK insurance industry to understand their views on, and response to, the FCA’s Conduct Risk agenda. Participants covered a broad representation of the industry, including life insurers, general insurers, health insurers and composites.

Thisreportpresentsourfindingsfromtheresearchandoutlinestheactionswebelieveinsurersneedto

takeinordertorespondtotheFCA’smainareasofconcern.

Wehopethatyoufindthereportusefulforunderstandingtheimplicationsforinsurersofamoreopen,

transparentandaccountablemarket,andinconsideringyourapproachtomanagingConductRisk.

Sean McGuire Tim Kirk

Partner,OliverWyman Partner,OliverWyman

Richard Thornton James Bryan

Partner,OliverWyman Partner,OliverWyman

welcom

e

4

welcom

eMessage from the CII

Dr Sandy Scott

ChiefExecutive,CII

There is no doubt that both the Prudential Regulation Authority and the Financial Conduct Authority have put conduct, culture and public interest at the very heart of their approach following their formation back in April this year.

AsthelargestprofessionalbodyintheUKfinancialservicessector,theCharteredInsuranceInstitute

welcomesthisfocusonimprovingthecultureofthewholefinancialservicessectorandwebelievethat

howprofessionalsbehaveisasimportantaswhattheyknow.WeattheCIIhaveactivelypromoted

higherprofessionalstandardsacrossourmembershipandinitiativesincludingtheAldermanbury

DeclarationandCorporateCharteredInsurersandBrokersareexamplesofourdesirefortheinsurance

sectortoattempttomakeitsownweatherratherthanrelyonmeetingacompliancerequirementculture.

Asabodythatchampionshigherstandardswebelieveitisrightforustoofferchallengetoour

professionandtheinsurancesectoratlargeonconductissuesparticularlyontopicswherethepublic

andregulatoraredemandingmore.

Thisreport,producedbyOliverWyman,isdesignedtohelpraisethelevelofdebateonthekeyconduct

issuesemergingacrosstheinsurancesector,andwhilsttherewillbearangeofresponsestothe

analysisandrecommendations,itdoescapturethecurrentthinkingofleadingpractitionersoninsurance

conductrisk.Itshouldalsoactasastimulusforfuturethinkingandactionacrosstheinsurancesectors–

aswellassupportingthedialoguewithournewregulators.

Wehopeyoufindthisreportagoodstartingpointforadebatetheprofessionneedstohavewithinitself,

withtheregulatorsandultimatelypartofalargerconversationwiththewiderpublic.Letushopeitwill

leadtoabetterdialogueandultimatelybettersolutionstomeetthepublicinterest.

Conduct risk for insurers: Respondingtoafundamentalshiftinregulatoryexpectations

5 Conduct risk for insurers: Responding to a fundamental shift in regulatory expectations

Executive summaryMartinWheatley,ChiefExecutiveoftheFinancialConductAuthority(FCA),promisedattheABI’s2013

BiennialConferencethattheFCAwouldbe:“averydifferentanimaltotheFinancialServicesAuthority

(FSA).”Hesetoutapositivevisionofasuccessfulandcompetitivemarketwhereregulationisnotazero-

sumgame,andwherecustomersandthebestfirmscanbenefitfrommorecompetition,betterproducts

andbetterservice.

Initsfirstmonthsofexistence,theFCAhasundoubtedlybeenactive,withmarketstudiesandthematic

reviewsofinsuranceproductsandoperations.Andthereisnodoubtthatthereissomeanxietyamongst

insurersinrelationbothtotheworkloadcausedbythesereviews,andalsototheirpotentialimpact

onexistingwaysofdoingbusiness.However,itisalsotheFCA’sintentionthatthematicreviewsdo

notsimplyadduptoasuccessionofbadnewsstories;goodpracticeandimprovementshouldalsobe

recognisedandhighlighted.

InordertounderstandtheviewsoftheUKinsuranceindustrytowardsConductRiskmoreclearly,we

interviewed22CEOsandotherseniorinsuranceexecutives.Theseinterviewsprovedtobeinformative,

andexhibitedabroadrangeofviews.Insummary,wefoundthat:

• ThereisamismatchofexpectationsbetweeninsurersandtheFCA

• Therehasbeenaninconsistentresponsefrominsurersinbothpaceandcontent

• Therearefourkeyemergingissueswhichwillbeparticularlychallengingtoaddress.

“ a very different animal to the Financial Services Authority (FSA)

”

executive summ

ary

6 Conduct risk for insurers: Responding to a fundamental shift in regulatory expectations

Mismatch in expectationsOurinterviewsrevealedthat,forsomefirmsatleast,ashifttoamoretransparentandcompetitive

marketisregardedaspositive.However,ingeneralwefoundamismatchinexpectationsbetween

insurersandtheFCAinthreekeyareas:

1. Theroleoftheregulator,andlevelofregulatoryintervention,requiredtoaddressdeficiencies

inthemarket.

2. Thepracticalimplicationsofthenewregulatoryregimeforfirms,andtheextentofchange

requiredtocomply.

3. Thelevelofpreparednessandprogressbyinsurersinadaptingtothenewregime.

Emerging issuesAsweconsiderthespeedanddirectionofthejourneytowardsamuchmoreopen,transparentand

accountablemarket,weseefouremergingtrendsthatmaybecomeparticularlychallengingforinsurers:

1. Afocusongoodcustomeroutcomes,ratherthanonactionstakenbyregulatedentitiesto

influencethoseoutcomes.Followingtherulesisnotenough.

2. Definingandprovingthevalueformoneyofproducts.Bothpriceandvalueneedto

standuptointensepublicscrutiny.

3. Pressuretoensuregreaterequality.Thiswouldinvolvemanagingthetrade-offbetween

individualunderwritingandpoolingofriskstoensureuniversalaccesstoinsurance,andreducing

discriminationbetweengroupsortypesofcustomers.

4. Settingtheboundariesfortheuseandmanagementofcustomerdatatoensurethattechnological

progressdoesnotoutstripregulators’andcustomers’appetiteforintrusion.

Insurer responsesInordertorespond,wethinkthatinsurersshouldcarryoutthefollowingfivesteps:

1. Definetheirconductriskappetiteandobtainseniorstakeholderbuy-in.

2. Performaconductriskdiagnostictoidentifychangesrequired.

3. Strengthentools,processesandcontrols.

4. Realigntheirbusinessmodelwithgoodcustomeroutcomes.

5. Reinforcethroughleadershipactions,culture,trainingandincentives.

executive summ

ary

7

1. the conduct era: more than just a risk type

1. The conduct era: more than just a risk type

Consumerprotectionregulationisnotnewtothefinancialservicesindustry,andfewwouldargue

againstsomeformofregulationbeingbeneficialtobothconsumersandfirms.However,weconsider

thattheconductriskagendabeingpursuedbytheFinancialConductAuthority(FCA)representsa

majorchangeinexpectations,andismuchmorethanjustanewversionoftheTreatingCustomers

Fairly(TCF)principles.

Despitesignificantprogressandpositiveintentionsbymanyfirms,acontinuationofincidentsrelatedto

conductriskpointtowardsdeficienciesinthewaythefinancialservicesmarketoperatesandintheway

somefirmsmanagetheirproductsandcustomerrelationships.Theseinclude:

• Targetcustomermarketsandproductvaluepropositionscanbepoorlydefined,preventingfirms

frommonitoringgoodcustomeroutcomeseffectively.

• Thesuitabilityofindividualcustomersdoesnotalwaysreceivesufficientattention,asprocesses

tomatchproductsandclientsmaylackrigourandareinsufficientlysupportedbyevidence.

• Productcomplexityandbundlingremaincommon,makingitharderforcustomerstomake

decisionsintheirownbestinterestswithoutdetailed,structuredadvice.

• Toolsandinfrastructureareunderdeveloped.Withconductriskregulationmovingtheindustry

evenfurtherawayfromasimplecaveatemptorregime,evidenceofdueprocesswhichsucceeds

indeliveringgoodcustomeroutcomesisparamount.

• Employeeincentivesarenotalwaysalignedwithprovidingappropriatecustomersolutions.

Givenmulti-billionpoundtaxpayerbailoutsandsignificantpoliticalpressure,thesedeficienciesareno

longerbeingtolerated.RegulatorsinkeymarketssuchastheUS(ConsumerFinancialProtectionBureau

(CFPB))andtheUK(FCA)areconcentratingtheirconductoversightindedicatedteamsorseparate

agencies,whileenactingsweepingregulationthatcoversbothabroadarrayofconduct-relatedissues

andanewmodelforsupervision.

IntheUK,theFCAisheavilyfocusedonensuringthatcustomerinterestsareembeddedthroughout

allareasoffirms,andthatallcustomersexperiencegood–ifnotthebest–outcomes.Thisisamatter

ofstrategyandcultureformanagement,muchmorethansimplyanissueofprocessandcontrol.

Yetwestillseethattoomanyfirmsarepreoccupiedwiththedefensivecontrolsrequiredtomanage

theregulatoryrisk(ratherthancustomerdetriment),andwithseekingtocomplywiththenarrowest

interpretationoftherules.

TheFCAispresentingmuchmorethananewrisktype.Boardsandexecutiveteamsmustgraspthe

scopeandextentoftheregulator’sagenda,andthesocialandpoliticalexpectationsthatdriveit.If

theydonot,theyruntheriskofmissingthestrategicimplications,andthepotentialforsignificant

disruptionsinthemarket,astheFCA’sinterventionsstarttochangethenatureofcompetition,andnew

businessmodelsevolve.

Conduct risk for insurers: Respondingtoafundamentalshiftinregulatoryexpectations

8 Conduct risk for insurers: Responding to a fundamental shift in regulatory expectations

2. insurer perspectives and industry reaction2. Insurer perspectives and industry reaction

TherequirementtoTreatCustomersFairly(TCF)wasenshrinedintheFSA’soriginalPrinciplesfor

Businesswithwhichallfirmswererequiredtocomply.Overtheyears,theconceptoftreatingcustomers

fairlywasenhancedandcodifiedbytheFSA,culminatinginfirmsbeingrequiredtodemonstrate

evidencethattheyhadembedded“fairness”before31stDecember2008.

Afteraslowstart,managementteamsinvestedheavilyinrespondingtotheregulator’sagenda.

However,lookingbackoverthepastdecade,twothingsareclear:

1. Theregulator’sexpectationshavecontinuouslyevolvedandincreased,leadingtonewareasof

regulatoryfocusandintervention.

2. Ateachstage,whileprogresshasindeedbeenmade,theindustry’sresponsehaslaggedbehindthe

regulator’sexpectations.

FollowingthecreationoftheFCAinApril2013,weareseeinganewwaveofconductscrutiny.While

thesixconsumeroutcomesexplainingwhattheFSAwantedTCFtoachieveforconsumersarestill

applicable,weviewtheFCAagendaasbeingsubstantiallymorethansimplyafewtweakstotheTCF

regime.

TheFCAhasannounceditsintenttomovetoanewandmorefocusedsupervisorymodel.

Thisentails:

•Movingfromareactiveapproachtoapre-emptiveandjudgement-basedapproach.

•Movingfromdealingwithsymptomstoaddressingunderlyingcauses.

•Movingfromanapproachfocusedonlyonensuringcompliancewithrules,toanapproachthat

encouragesfirmstodotherightthinginrespectoftheircustomersandthemarketstheyoperatein.

Againstthisbackground,theoverwhelmingconclusionfromoursurveyisthatthereisasignificant

mismatchbetweenFCAexpectationsandtheviewsofmanyinsurerswithregardto:

1. Theroleoftheregulator,andthelevelofregulatoryinterventionrequiredtoaddressanydeficiencies

inthemarket.

2. Thepracticalimplicationsofthenewregulatoryregimeforfirms,andtheextentofthechanges

requiredtocomply.

3. Thelevelofpreparednessandprogressmadebyfirmsinadaptingtothenewregime.

Theseissuesareexploredonthefollowingpages.

“ The FCA will continue to focus on how firms are managed and structured so that every decision they make is in the best interests of their customers

”FCARiskOutlook2013

“ Our approach to risk will enable us to become more proactive and intervene earlier, focusing on the sources of detriment such as product design, governance and incentives

”MartinWheatley,FCA,ChiefExecutive

9 Conduct risk for insurers: Responding to a fundamental shift in regulatory expectations

2.1. The role of the regulator

UptotheendofNovember2013,theFCAhaspublisheditsfindingsfromseventhematicreviewswhich

affectinsurers.

Someinsurersarguethatthisistoomuch,toosoonfromtheFCA,andthatincreasedregulationmay

resultinalossofinnovation,greaterfinancialexclusionandcustomerdetriment.Asevidence,they

pointtotheimpactoftheRetailDistributionReviewprogramme(RDR)andtheresultinglossofaccess

tofinancialadviceforlowandmiddleincomeearners.Somearguethatastheregulatoryburdenrisesin

otherareasofinsurance(suchasgeneralinsuranceproducts)wewillseeasimilarimpact.

TheFCA’sobjectivesoncompetitionandvalueformoneyrepresentamajorareaofconcernformany

insurers.SomeworrythattheFCAmaypotentiallytrytobecomeapriceregulator,andarguestrongly

thatthisisunlikelytoimprovemarketefficiencyorleadtobettercustomeroutcomes.

TheFCAhaspreviouslymadeitsstanceclearinthisregardbysayingexplicitlythatitdoesnotwantto

becomea de jurepriceregulatorofinsuranceproducts.

However,recentUKGovernmentproposalssuggestingthattheFCAshouldsetacaponthecostof

paydayloanshavethepotentialtochangethelandscape.TheFCAhasgenuineconcernsoverthe

valueformoneyofferedbysomeproductsonthemarket.Mobilephoneinsuranceandlegalexpenses

insurancehavecomeunderthespotlight,andpressureismountingontheannuitiesarea.

AstheFCAtakesactiontoimprovecompetition(whichwebelievewillmeanmuchmoretransparencyin

howproductsperformforcustomers)andvalueformoney,thereisariskofde factopriceregulationof

insuranceproductsasjudgementsaboutproductdesignandvalueplayagreaterroleintheregulator’s

supervisionoffirms.Wealsoenvisagemoredirectpoliticalpressuretoregulatepricingin

theinsurancesector.

WhiletheFCA’sconductriskmanagementapproachhasbeendistilledintoasetofforward-looking

priorities,clarityisstillrequiredinsomeareas.Forexample,howisvalueformoneytobedefined?

Whatpreciselyaretheresponsibilitiesofinsurersanddistributorsinensuringgoodcustomeroutcomes?

Whiletheregulatormayprovidefurtherguidanceinsomeareas,thisisunlikelytobedetailedor

prescriptive.Itwillbeuptoeachinsurertosetoutwhat“goodconduct”meansfortheirbusiness.

Webelievethisprocessneedstostartwithdebateattheverytopoftheorganisationabouthow

itwishestocompeteinthemarketplace,andtherelationshipitwantstohavewithitscustomers,

distributorsandtheregulator.

“ Conduct risk should be a “top 3” issue for all UK insurers

”CEO,UKLifeInsurer

“ The current situation of “pseudo regulation of price” is very confusing for consumers and firms generally

”CEO,UKGeneralInsurer

2. insurer perspectives and industry reaction

10 Conduct risk for insurers: Responding to a fundamental shift in regulatory expectations

2. insurer perspectives and industry reaction

“ Important that regulation does not become a barrier to entry into markets and that it does not cause firms to withdraw from markets, reducing competition and customer choice.

”CEO,GeneralInsurer

2.2. Practical implications and extent of changes required

Inadditiontodifferingviewsontheextentofregulationandinterventionrequired,webelievethereisa

disparitybetweentheFCAandmanyinsurersonthepracticalimplicationsofthenewconductagenda,

andontheextentofthechangesthataregoingtoberequired.Manyinsurersviewthechangestobe

relativelyminoradjustmentstotheirexistingbusinessandoperatingmodels.

IfwecomparetheresultsofourUKinsurersurveytoasimilarsurveyweconductedwithUKretailbanks,

weseethatthebanksaremuchmorealerttotheneedforchangeandtotheextentofchangesrequired.

Insurancecompanyexecutivesarekeentopointoutthatthebanksareverydifferenttoinsurers,and

thatconductriskisthereforelessofanissueforinsurers’customersthanitisforbanks’customers.

Whileweagreethatinsurersareverydifferenttobanks,wedonotbelievethatinsurersaregoingto

getofflightly.Indeed,manyexecutiveswespeaktoareabletopointoutwherecurrentproducts,orthe

market,donotperformwellforconsumers.Wethereforeexpectsignificantchangestoinsurerbusiness

andoperatingmodelswillberequired,albeitwithdifferentareasoffocusfromthebanks.

OneofoursurveyquestionsaskedinsuranceCEOswheretheythinkthemostsignificantimpactwillbe

feltacrosstheoverallinsuranceindustry.Thetopthreeareashighlightedwere:

1. Productofferingsanddesign

2. Incentivestructures(atpointofsale)

3. Organisationalculture.

“ The main difference is that insurers have long recognised a duty of care to policyholders that does not seem to have a cultural equivalent in banking.

”CEO,UKLifeInsurer

11 Conduct risk for insurers: Responding to a fundamental shift in regulatory expectations

Figure 1. FCA and conduct impact on insurance industry – responses from survey recipients

Onproduct offerings and design,manyinsurershaverecognisedtheneedtoreviewtheirexisting

businessandplannedproductlaunchestoidentifypotentialhighriskproductsfromaconduct

perspective(thosethatposemostriskofcustomerdetriment),andthentaketheappropriateaction.

Suchreviewsareexpectedtoresultinchangestoproductdesign(suchastermsandconditionsand

policyexclusions),salesandtargeting,supportprocesses(suchasclaimsmanagement),

andgovernance.Insomecases,thereviewislikelytoleadtothewithdrawalofproducts,eitherthrough

thefirm’schoice,orwiththeactiveencouragementoftheFCA.Wehavealreadywitnessedsignificant

changesinthebankingsector,andarestartingtoseemoresignsofthisininsurancetoo.Inmostcases,

wefeelinsuranceproductscouldbeadapted,andwithdrawalwillbeunnecessary.

InsurersbelievethatIncentive Structureswillalsobeaffected,butthatanychangeswillbemainly

limitedtofront-linesalesstaff.Insurerswillneedtotrytoachieveabalancebetweenmeetingsales

targetswhilealsoensuringgoodcustomeroutcomes.Wehavealreadystartedtoseethisinpractice,

withseveralinsurersremovingsalesvolumecommissionsfortheirfront-linesalesstaff,andinstead

givingcreditforqualityofcustomerserviceandforensuringthatcustomers’needsaremet.

Weagreethatfront-linesalesincentivestructureswillneedtobereviewedandalignedwithgood

customeroutcomes,althoughwedonotconsiderthatremunerationstructuresthatincludecommission

areinappropriateperse.However,theywillneedstrongcontrolsanddifferentstructures,suchasthe

removalofcommissionpaymentsifqualitytargetsarenotachieved.

Wethinkthatconduct(andcustomer-focusedperformance,moregenerally)couldalsoplayamuch

strongerroleinthedeterminationofexecutivebonuses.Forexample,whiledeferralofbonusesisnow

mandatoryinbanks,wenotethatitisnotyetcommonpracticeforinsurers.Thiscouldleaveinsurers

exposedtothepossibilitythatstaffchaseshort-termprofitswithouttakingintoaccounttheriskof

subsequentcostsinregulatoryfinesorcompensation.

Amongtheexecutivesweinterviewed,organisational culturewasconsideredtobethethirdmost

significantareaforchange.Thistallieswithourownexperiencethatcultureandleadershiphavenot

yetreceivedsufficientattentionfromfirmsseekingtomeettheexpectationsofconsumersandthe

regulator.

Insurersneedtosetoutatonefromthetopthatmovesbeyondbroadcorporateaspirations,and

isbroughttolifethroughleadershipactions,decisionmaking,businesspracticesandstandards,

recruitment,rewardsandclearcommunicationtostaffaboutwhatconstitutesacceptableand

unacceptablebehaviour.Aboveall,thetonearticulatedbyleaderstotherestoftheorganisation

needstobeseenasauthentictostaff(aswellastocustomersandtheregulator)andhastobeapplied

rigorously,ortheunwrittengroundrulesthatexistintoday’smarketwillpersist.

TheFCAarticulatedthisconceptinadifferentway,askingcompaniestoconsider“shouldwe”carryout

acertainactivityorbehaveinacertainway,aswellas“couldwe”.

Least significant change Most significant change

Distributionmodels

Governance&controls

Organisationalculture

Incentivestructure

Productofferings/design

Organisationdesign

2. insurer perspectives and industry reaction

12 Conduct risk for insurers: Responding to a fundamental shift in regulatory expectations

2. insurer perspectives and industry reaction2.3. Level of preparedness and progress in

adapting to the new regime

Inouropinion,theregulatorwillexpectfirmstore-examineand,ifrequired,realigntheirbusinessand

operatingmodels,includingstrategy,systemsandcontrols,skillsets,cultureandincentives.TheFCA

haspubliclystatedthatfromtheboardrightthroughtofrontlinesalesstaff,firmbehaviour,attitudes

andmotivationsmustchangetoembracegoodconductandensurethatcustomerexperiencesand

outcomesmeetexpectations.

Whilesomeinsurersarestartingtotakeaction,webelievethattheinsuranceindustryasawholeisstill

somewayfromdefiningandembeddingasetofcommongoodconductpractices.Inourexperience,

manyinsurersdonotyethaveaclearviewonwhatgoodconductlookslikefortheirorganisation.Even

incaseswheretheydo,insurerssometimesfacecommercialchallengesinachievingrelevantgoals,and

feelthattheycannotmoveforwardbythemselvesinsomeareas.Forexample,pricingnewandexisting

motorinsurancecustomersatthesameprofitmarginwouldresultinmassivefirstmoverdisadvantage.

Althoughthevastmajorityofinsurershavealreadycommencedpreparationsforthenewregulatory

environment,manystilldonotyetrecognisethelarge-scalechangesrequiredtomeettheFCAagenda

onconductrisk.Oursurveysuggeststhatveryfewinsurerscurrentlyhaveinplacesuchacomprehensive

approachtoconduct.Fewhaveintroduceddedicatedconductriskprogrammesorteamstodevelop

robustprocessesforidentifying,monitoringandmanagingconductrisk.Thisisincontrasttotheir

bankingcounterparts,whichhaveinvestedheavilyinaligningtheirbusinessmodelsanddemonstrating

evidenceofgoodcustomeroutcomes.

Weaskedinsurerswheretheyfelttheir companycurrentlyhadgoodconductriskcapabilities,and

wheretheyneededtodothemostworkoverthecomingmonths.Figure2,below,summarisesthe

answerstothisquestion.

Figure 2. Assessment of current conduct risk capabilities vs. priority area of focus for the next

12 months – responses from survey participants

Averagecurrentconductriskcapabilities

Aver

age

prio

rity

are

aof

focu

sov

ern

ext1

2m

onth

s

Veryhigh

High

Med

LowNot

developedInitiativestarted

Partiallycomplete,notyetembedded

Fullyembedded

Largely under control

• Board and Executive MI

• Conduct risk mangement strategy

• Risk appetite statements

Fair value exchange • • Evidence of customer

suitability

Ability to identify risks •• Seller incentives

• Conduct risk definition

Complaints handling •

Executive compensation •

Product development process •

Key areas of focus

13 Conduct risk for insurers: Responding to a fundamental shift in regulatory expectations

Accordingtotheinsurerswespoketo,thefollowingareaswerethoughttobebroadlyundercontroland

requiringlimitedadditionalfocus:

•Executivecompensation

•Complaintshandling

•Definitionofconductrisk

• Abilitytoidentifyconductrisks

• Sellerincentives.

PerhapssurprisinglygivenwhatweseeandhearfromtheFCA,almostallinsurersinoursurveyfeltthat

conductriskmanagementwasalmostfullyembeddedinexecutive compensation,andthatthisareadid

notrequireanyadditionalfocus.TheFCAisveryclearthatgoodconductstartswiththe“tonefromthe

top”.Indeed,experienceteachesusthatoneofthemosteffectivetoolsforincreasingexecutivefocuson

aparticularareaistoalignincentiveswiththatgoal.Insurersshouldthinkcarefullyabouthowconduct

influencesexecutivecompensation,ensuringthatexecutivesarerewardedforgoodconductwhilealso

introducingothermeasures,suchastheabilitytoclawbackbonusesinfutureyearsforpoorconduct.

Complaints handlingwasanotherareawhereinsurersfeltcomfortablethattheywerebroadlywhere

theyneededtobe,andthatlittlefurtherattentionwasrequired.Twokeyreasonsexplainthisfinding.

Firstly,insurershavealreadyplacedastrongfocusonthisareaforanumberofyearsundertheTCF

regime.Secondly,complaintsandcomplaintshandlingperformanceistypicallytrackedasaKey

PerformanceIndicator.Whilesomefirms’complaintshandlingprocessesmaynotneedtobeoverhauled

(althoughFinancialOmbudsmanService(FOS)upholdratesindicatethatissuesremaininsomeareas),

insurerscouldreassesswhethertheircomplaintsfeedbackprocessesareeffective.Complaintscanbea

greatearlywarningindicatorofpotentialfutureconductrisks.Oursenseisthatmanyinsurersdonotdo

asmuchastheycouldtounderstandtherootcausesofcomplaintsandremedythem.

Onthedefinition of conduct risksandtheability to identify conduct risks,mostinsurersfeelthey

haveagoodunderstandingofwhatconductriskis,andhavecarriedoutsomeworktosingleoutwhat

theybelievetobetheirmostmaterialconductrisks.However,inourview,theinterpretationandfocus

ofconductriskisevolving.Aswediscussinthefollowingchapter,webelievethatfourareaswillbe

prioritisedinthenextwaveofconductrisk.Fromourresearch,manyinsurersareatpresentpoorly

preparedtorespondtothesefutureareasoffocus,andhavenotadequatelythoughtthroughwherethey

standoneachissue.

Insurersrecognisethatseller incentivesrequirecarefulrealignmentwithgoodcustomeroutcomes,

althoughmostfeelthattheirfirmhasalreadytackledthisissue.Someinsurersareremoving,orhave

removed,incentivesforsalesvolumeorvaluefromthefrontline.Thiscontrastswiththeindustry-wide

viewdepictedinfigure1whichindicatesthatexecutivesconsiderincentivestobeanareathatwill

requiremajorchange.

2. insurer perspectives and industry reaction

14 Conduct risk for insurers: Responding to a fundamental shift in regulatory expectations

2. insurer perspectives and industry reactionInsurersidentifiedthefollowingareasasthoserequiringmostatttentiontoaddressandembedfully:

• Developingboard and executive managementinformationspecifictoconductrisk.

• Developaholisticconduct risk managementstrategyandapproach.

• Updaterisk appetite statementstoincludemoreofaconductriskfocus,includingthedevelopmentof

conductriskappetitestatementsandappropriateintegrationwithexistingriskappetite.

• Demonstratea‘fair value exchange’betweentheinsurerandthepolicyholder(webelievethatthis

needstobeahigherprioritythanourresearchindicatesitcurrentlyis).

• Demonstrateevidence of customer suitabilityandunderstanding(althoughsomeparticipantsdidnot

believethiswasapplicabletotheirbusiness).

Almostallinsurersstatedthattheyneedtodomoreworktoimprovethereportingofconduct-related

measuresinboard and executive management information.Weagreethatmanagementinformation

doeshelpinhighlightingwheretheremaybeconduct-relatedissues.However,itisjustonepartofthe

solution.Conductmanagementinformationcanassistinidentifyingwheretherearealreadyconduct

issues,butcanalsobeforward-looking,helpingtoidentifywherepotentialconductissuesmayemerge

inthefuture.

Conduct risk management strategyincludesdefiningwhatconductriskisfortheinsurer,andtheir

overallapproachtomanagingconductrisk.Mostinsurersthinkofconductriskasbeingembeddedin

everythingtheydoasabusiness,cuttingacrossalldepartmentsandprocesses.Assuch,itislessabout

havingasinglestrategyonhowtomanageconductrisk,butmoreaboutembeddinggoodconductin

thepolicies,processes,businesspracticesandculturerightacrosstheorganisation.Giventheall-

encompassingnatureofconductriskmanagement,thisisanareawheremanyfeeltheyhavesomework

todo.

15 Conduct risk for insurers: Responding to a fundamental shift in regulatory expectations

3. moving beyond TCF

3. Moving beyond TCF

ImportantdifferenceshavealreadyemergedbetweentheFCA’scurrentagendaandexpectations

andthoseundertheFSA’sTCFregime.Whenweconsidertheoveralldirectioninwhichthemarket

andregulationaremoving,weseethefuturetobecharacterisedbysignificantlymoreopenness,

transparencyandaccountability.Thiscreatesfouremergingissuesthatmaybecomeparticularly

challengingforinsurers.Theseare:

1. Followingtherulesisnotenough.Therewillbeamuchgreaterfocusoncustomersgettinggood

outcomes,ratherthanontheactionstakenbyregulatedentitiestoinfluencethoseoutcomes.

2. Ultra-transparencymeansthatallproductsandserviceswillneedtostanduptogreaterpublic

scrutinytoprovethattheyoffer value for money.

3. Therewillbemorepressuretobalancecommercialdecisionswithsatisfyingdemandsfor

equalityofaccesstoinsuranceandfortheremovalofdiscriminationinpricing.

4. Companieswillneedtoensurethatthepotentialadvantagesfromrapidadvancesintechnologyand

BigDataarenotjeopardisedbytheinappropriateuseandmanagementofcustomer data

andinformation.

3.1. A focus on customer outcomes

TheFCAhassaidveryclearlythatanimportantelementof“goodcustomeroutcomes”isthatproducts

shouldbesuitablefortherelevantcustomers,whoshouldinturnunderstandwhattheyhavebought.

Whilenoinsurerislikelytodisputethatthisistherightaim,thekeydebatenowconcernshowfaran

individualinsurerneedstogotoensurethatthegoalisrealised.Thereareanumberofinteresting

questionsrelatingtothistheme:

•Whataretheinsurers’responsibilitiesinensuringthatitscustomersunderstandtheproductstheyare

buying,andthattheseproductsaresuitable?

•Atwhatpointdoesthecustomerhavetotakeresponsibilityforensuringthattheyunderstandthe

products,andthattheproductsaresuitable?

•Whataretheinsurer’sresponsibilitieswhentheproductisbeingsoldbyathird-partydistributor,and

towhatextentdoestheinsurerneedtoensurethatdistributorsarealsodemonstratinggoodconduct

andachievinggoodcustomeroutcomes?

•Towhatextentdoinsurershaveadutytoensuregoodconductwithregardtocompetitors’customers

(suchasontheissueofreferralfees)?

Manyinsurerswillalreadytestcustomercommunicationstoensurethattheyareunderstandableforthe

targetaudience,butistherearesponsibilitytocheckthatthecommunicationisbeingread,andthatitis

beingusedtomakeareasonabledecision?

16 Conduct risk for insurers: Responding to a fundamental shift in regulatory expectations

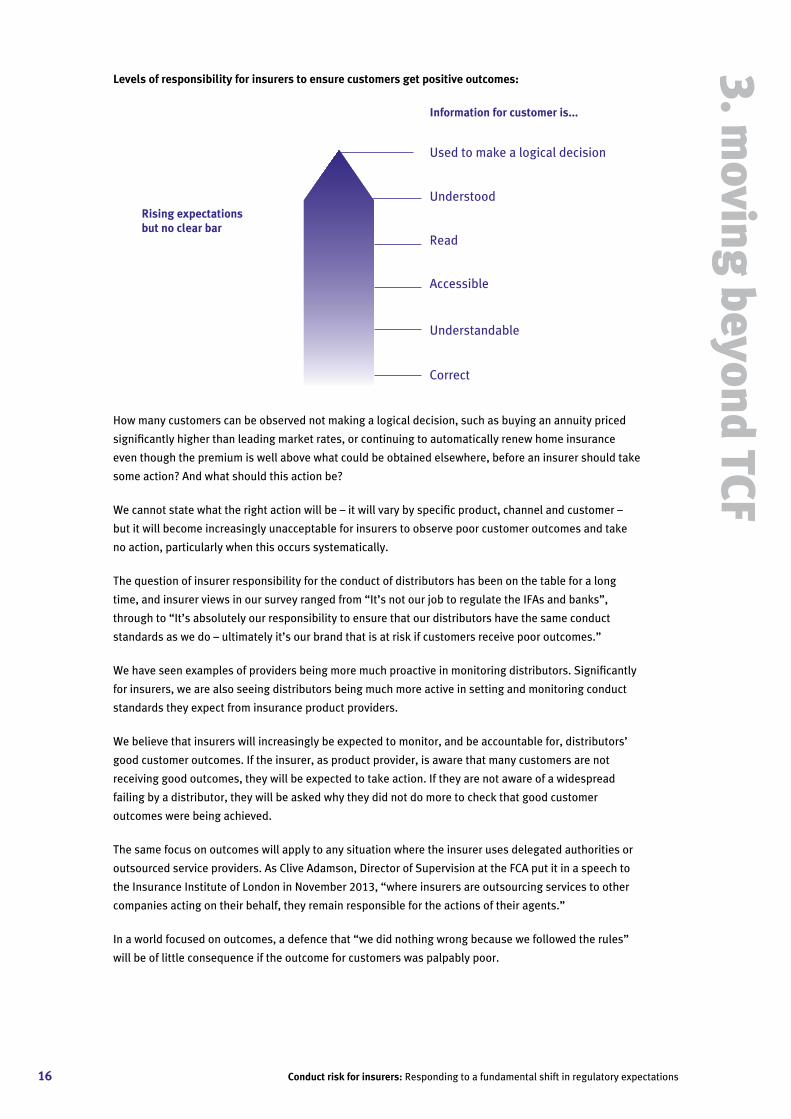

Howmanycustomerscanbeobservednotmakingalogicaldecision,suchasbuyinganannuitypriced

significantlyhigherthanleadingmarketrates,orcontinuingtoautomaticallyrenewhomeinsurance

eventhoughthepremiumiswellabovewhatcouldbeobtainedelsewhere,beforeaninsurershouldtake

someaction?Andwhatshouldthisactionbe?

Wecannotstatewhattherightactionwillbe–itwillvarybyspecificproduct,channelandcustomer–

butitwillbecomeincreasinglyunacceptableforinsurerstoobservepoorcustomeroutcomesandtake

noaction,particularlywhenthisoccurssystematically.

Thequestionofinsurerresponsibilityfortheconductofdistributorshasbeenonthetableforalong

time,andinsurerviewsinoursurveyrangedfrom“It’snotourjobtoregulatetheIFAsandbanks”,

throughto“It’sabsolutelyourresponsibilitytoensurethatourdistributorshavethesameconduct

standardsaswedo–ultimatelyit’sourbrandthatisatriskifcustomersreceivepooroutcomes.”

Wehaveseenexamplesofprovidersbeingmoremuchproactiveinmonitoringdistributors.Significantly

forinsurers,wearealsoseeingdistributorsbeingmuchmoreactiveinsettingandmonitoringconduct

standardstheyexpectfrominsuranceproductproviders.

Webelievethatinsurerswillincreasinglybeexpectedtomonitor,andbeaccountablefor,distributors’

goodcustomeroutcomes.Iftheinsurer,asproductprovider,isawarethatmanycustomersarenot

receivinggoodoutcomes,theywillbeexpectedtotakeaction.Iftheyarenotawareofawidespread

failingbyadistributor,theywillbeaskedwhytheydidnotdomoretocheckthatgoodcustomer

outcomeswerebeingachieved.

Thesamefocusonoutcomeswillapplytoanysituationwheretheinsurerusesdelegatedauthoritiesor

outsourcedserviceproviders.AsCliveAdamson,DirectorofSupervisionattheFCAputitinaspeechto

theInsuranceInstituteofLondoninNovember2013,“whereinsurersareoutsourcingservicestoother

companiesactingontheirbehalf,theyremainresponsiblefortheactionsoftheiragents.”

Inaworldfocusedonoutcomes,adefencethat“wedidnothingwrongbecausewefollowedtherules”

willbeoflittleconsequenceiftheoutcomeforcustomerswaspalpablypoor.

Levels of responsibility for insurers to ensure customers get positive outcomes:

Rising expectations but no clear bar

Information for customer is...

Correct

Understandable

Accessible

Read

Understood

Usedtomakealogicaldecision

3. moving beyond TCF

17 Conduct risk for insurers: Responding to a fundamental shift in regulatory expectations

3. moving beyond TCF

3.2. Value for money

Thiswasoneofthemostkeenlydebatedtopicsinourinterviews.Therewasageneralconsensusthat

productsshouldbefairlypricedandoffervalueformoney.However,wealsosawthelesscommon

opinionthatifpriceandtermsandconditionsarefullyexplained,anypriceormarginisacceptable.

Accordingtothisview,itisuptothecustomertodecideforthemselveswhatrepresentsvaluefor

money.Forexample,apricepremiumcouldbejustifiedbythetimesavedinnotshoppingaround,orby

thepeaceofmindobtainedthroughbuyingfromaknownbrand.

Whenweexploredhowvalueformoneycouldbeassessed,therewasmuchlessclarityandno

agreementaboutwhetherhighpricesormarginsnecessarilymeanthatthecustomerhasgotpoorvalue

formoney.

Inourview,thevalueformoneyissueisgoingtobecomeincreasinglyimportanttotheregulator.

TheFCAwillseektoimprovecompetitionandtransparency,andwillintervenedirectlyonbehalfof

consumerswhoareunabletodetermineifapolicyrepresentsagooddeal.

Significantly,ourresearchshowedthatthisisnotseenasbadnewsbyallinsurers.Wesawaspectrum

ofattitudesonhowfirmsshouldcompeteandbehaveinthemarket,includinginsurerswhobelievethat

boththeyandtheircustomerswillbenefitfrommoretransparencyandfromeffortstomakevaluefor

moneyeasiertoassess.ThisconformswiththeFCA’sviewthatamorecompetitivemarketwhichtreats

itscustomersbetterisgoodfortheindustry.

Itisthereforeessentialthatinsurersputthemselvesonthefrontfootbyreviewingtheirproducts,and

bymakingsuretheycanjustifythevaluethatproductsoffer.Inmakingthisassessment,valuefor

moneyisnotjustaboutpriceorinsurermargin;itisunrealistictosaythataspecificmarginorclaims

levelisunfairtocustomers.However,whereprofitisunusuallyhigh,thiswillneedtobejustified.This

maybe,forexample,becauseitisanewproductwheretheriskinvolvesgreateruncertainty,orthat

claimsarevolatileoverthemedium-to-long-term,meaningthatashort-termassessmentofmarginis

inappropriate.

Inouropinion,eachmanagementteamneedstodevelopclearguidancewhichwillalertthemto

productsthatmayofferpoorvalueformoneyandwhereefficacymayneedtobereassessed.This

guidancecouldincludefactorssuchas:

• Whatvalueformoneymeansforcustomers.

• Thetimeframeneededtomakearealisticassessmentoftheproduct’sriskandmargin.

• Thedistributionofpremiumsandfeestoeachplayerinthevaluechain–distributorpaymentsand

commission,insurerprofit,andclaimspayouts.

• Policyconditionsthatreducethevalueoftheproduct,suchashighexcesses,exclusions,triggersfor

premiumincreases.

• Theimpactof“hiddencharges”thatincreasethetotalcostoftheproductforcustomers.

• Theimpactontotalcostandvaluewhensellingbundledproductsandadd-onstoimprovereturnson

low-margincoreproducts.

18 Conduct risk for insurers: Responding to a fundamental shift in regulatory expectations

Itisapparentthatmanyotherfactorsinfluencetheperceptionofvalueformoney.Thesemayinclude

thebrandoftheprovideranddistributor,thequestionofwhethertheproductmeetsthecustomer’s

needs,ortheservicelevelcustomersreceivebothduringandafterthesale,andwhethertheycould

haveobtainedanidentical(ornearlyidentical)productatasignificantlylowercost.Thereisalsoa

simplequestionofwhetheronecompany’sproductischeaperbecauseitoffersbettervalueformoney,

orbecauseithasmisunderstoodtherisk.

Societyismovingtooneofultra-transparencyandaccountability.Unlessafirmisconfidentitcanstand

uptopublicscrutiny,itisatrisk.Thetestforinsurersistoaskhowtheregulator,mediaandcustomers

wouldreactifallthedetailsofaproductwerefullytransparentandinthepublicdomain:charges,

commissions,claimslevels,margin,andsoon.Iftheanswertothisquestionfeelsuncomfortable,then

actionisprobablyrequired.

3.3. Equality

Infuture,weconsiderthattherewillbeincreasingpressureoninsurerstoensurethatthereisgreater

“equality”betweencustomers.Todate,thispressurehasarguablybeenexertedmorethroughpolitical

channels(andsubsequentapplicationsthroughthejudicialroute)thanthroughregulatoryinterventions,

suchasgenderneutralpricing.Weexpectoverallpressuretocontinue.

Whileinsurerscanacceptthatsomecustomergroupsarepricedoutofthemarketorareotherwise

disadvantagedduetothenatureoftheirrisk,thislogicisunattractivefromtheperspectiveofpublic

policy,whereinsuranceisviewedasasocialgood.Andaswehaveseeninrelationtogender-neutral

pricingandfloodinsurance,governmentwilldirectlyinterveneinthemarketundertheguiseof

promotingequality.

Giventhistrend,insurersneedtoconsiderwhethercurrentapproachestopricinganddistributionare

atriskfromregulatorsorlegislatorswhoarekeentoensureequalityandremoveanysensethatcertain

customergroupsarebeingdisadvantaged.

Oneareawhichmayneedtobereconsideredisthepricingofnewversusexistingcustomers.While

almostallinsurerswespeaktosaythattheywouldliketorewardloyalcustomers,itiscommonpractice

acrossmanyproductlinestoofferbetterratestonewcustomersthantoexistingcustomers.Thishas

beeninsurers’responsetomarketandconsumerbehaviour,andtheyappearfearfulofamassive

first-moverdisadvantageshouldtheytrytochangetack.Meanwhile,collectiveactionisconstrainedby

competitionissues.

Wedonotbelievethatregulatorsshouldprohibitdifferentialpricingasawayofinsurersgrowingmarket

share(orrewardingloyalty).Norshouldallcustomersberequiredtobeofferedanequalprice;lower-risk

customersshouldreasonablyexpecttopayless.

Inourview,itshouldbeacceptableforaninsurertotakeasmall,ornegative,marginintheearlyyears

ofacustomerrelationshipintheexpectationofahighermarginovertime.However,thereisclearly

aspectrumbetweenrecoveringinitialinvestmentinacquiringacustomeranddeliberatelyexploiting

customerinertiaoverthelongertermofacontract.Wesuggestthatinsurersneedtobeclearabout

wheretheirownriskappetitelies.Factorstheymaywanttoconsiderinclude:

3. moving beyond TCF

19 Conduct risk for insurers: Responding to a fundamental shift in regulatory expectations

3. moving beyond TCF

• Theextenttowhichthemarginprofileistransparenttocustomersatthepointofacquisition(e.g.by

advertisinganexplicitfirstyeardiscount).

• Theprofileofcustomermarginsovertime(forexample,whethermarginscontinuetoriseafterthe

pointatwhichtheoriginalinvestmenthasbeenrecouped).

• Themagnitudeofthegapbetweenthepriceofferedtoseasonedcustomersandthenewbusiness

pricetheywouldbeofferediftheyshoppedafresh.

• Theextenttowhichvulnerablesubgroupsareofferedvalueformoney(e.g.theelderly,andother

groupslessabletoshoparound).

Thereareotherpracticesthat,althoughlessobvious,couldalsobereviewedinordertodeterminehow

toensuretheyareappropriatefrombothanequalityandconductriskperspective.Forexample,ifa

customercallsamotorinsurer,theymighthaveaoneinahundredchanceofreceivingaquotethatis

5%higherthannormal,andaoneinahundredchanceofreceivingaquotethatis5%lowerthannormal.

Thisisacommonapproachtotestingpriceelasticity,butitisclearlyunequal.Whetherthisshouldbe

asourceofconcernisnotyetclear,andrepresentsanexampleofthedifficultjudgementsthatinsurers

needtomake.

Manypeopleinthebankingsectoraresayingthatitistimetoreturntowhattheyterm“old-fashioned”

banking.Insurersmaywishtoconsiderwhatthismaymeanforthem,andtheextenttowhichthe

originalpurposeofinsurance–thesharedpoolingofrisk–isstillrelevantandhowtobalancethiswith

theneedforpeopletopayafairpremiumcommensuratewiththerisktheycontributetothepool.

Eachinsurerwillneedtoadjusttheirowncomfortlevel,andensurethatanappropriatebalanceis

achievedbetweenindividualunderwriting,poolingofcustomersandtheprincipleofaccesstoinsurance

forallsectionsofsociety.Evenwheredecisionsmakesenseintheworldofunderwritingandcommercial

logic,managementneedstoconsiderwhatchallengesmayemergeinthenameofequality.

20 Conduct risk for insurers: Responding to a fundamental shift in regulatory expectations

3.4. Use of customer data and information

TheadvanceoftechnologyandBigDataopensupinnovationopportunitiesforinsurersinproduct

design,pricing,customertargeting,servicingandclaimsmanagement.However,evenwhileoperating

withintheboundariesofthelaw,therearestillquestionsaboutthelimitsofwhatisacceptableand

unacceptableuseofcustomerdata.ThereisbotharegulatoryandreputationalriskforinsurersifBig

Dataopportunitiesareexploitedfasterthancustomerswant.

Toensuretheadvancesintechnologyarenotjeopardisedbyinappropriatesourcing,usageand

managementofdata,insurersneedtodevelopclearguidanceandprinciplesontheuseofcustomer

information.

Forexample,itiscommonpracticeintheannuitymarkettoaskcustomersabouttheirhealthand

lifestyleinordertodeterminewhethertheyareeligibleforanenhancedannuity.Thisisacceptableifthe

customervoluntarilyprovidestheinformationdirectlytotheinsureraspartofthequotationprocess,

butisitacceptablefortheinsurertoobtainthisinformationthroughothersources?Isitappropriatefor

asupermarkettouseloyaltycarddataoncigarettepurchasestobeusedinpricingannuitiesfortheir

customers?Whatifaninsurercanseefromthecustomer’sFacebookpagethattheysmoke?

Onecouldarguethatthereisnoproblemiftheuseofthisinformationisdeliveringabetteroutcomefor

thecustomer(forexample,intheformofabetterannuityrate,ortodetectfraud),andtheinformation

isavailablewithinthepublicdomain(andaFacebookpostingisarguablyputtinginformationinthe

publicdomain).Butwhatiftheinsurerusesinformationthatislegallyavailable,butisobtainedwithout

customers’explicitconsent,inordertopriceaprotectionproduct,andthisadditionalinformationresults

inahigherpriceforthecustomerorcoverbeingdeclined?

Anotherinterestingareaistheuseofbehaviouraldata.Someinsurersareexperimentingwithusing

informationabouthowthecustomerbehavesontheirwebsiteasaninputintothequotationsgiven.

Forexample,theymaytakeintoaccounttheproductswhichcustomersview,andhowmanydifferent

combinationsofproductfeaturestheytryout.Acustomerwhotriesseveralalternativeamountsforan

excessonanonlinemotorinsurancepolicyquotationformisconsideredtobemoresensitivetoprice

thansomeonewhojustrequestsaquotewiththestandardexcess.

Otherexamplesofthisdilemmaincludewhetheritisfairtoloadthepremiumforonecustomerifthey

happentosharethesameaddressassomeoneonafrauddatabase.

Insurersneedtobeconfidentthatnotonlyaretheyoperatingwithintheletterandspiritofallrelevant

lawsandregulations,butthat,astheycaptureandmakeuseofnewsourcesofcustomerdata,theyare

happytodefendwhattheydotocustomerswhenasked.TheABIguideontelematicsmaybeauseful

exampleofhowtheseconcernscanbeaddressedinanopenway.

3. moving beyond TCF

21 Conduct risk for insurers: Responding to a fundamental shift in regulatory expectations

3. moving beyond TCF

Aswellasconsideringhowtheyusecustomerdata,insurersalsoneedtothinkabouthowtheystoreand

manageit.Forexample,

• Ifrelyingoninformationnotknowinglyordirectlyprovidedbythecustomer,howtoensurethat

itisverified?

• Howisdatakeptuptodatesothatonlythemostrecentinformationaboutacustomerisusedto

makeadecision?

• Howisdatakeptsecuresothatitisnotlostorstolen?

Astheamountofavailablepersonaldatabeingcapturedandstoredgrows,thechallengeincreases.

Weexpecttoseetheregulatorbeingmuchmorevigilant,andlesstolerant,inthisarea.

Todate,mostofthedebatehasbeendictatedbywhatistechnologicallypossibleandcommercially

useful.Thepotentialforsignificantreputationalandregulatoryriskassociatedwithcustomerdata

meansthatmorediscussionisrequiredaboutwhatisacceptable.

22 Conduct risk for insurers: Responding to a fundamental shift in regulatory expectations

4. the response4. The response

Aseachwaveofconsumerprotectionregulationhasbeenbroughtforward,theindustryhaslagged

behindtheregulator’sexpectations.Thisremainsthecasedespitethefactthatinsurershavemade

significantprogress,devotingconsiderableattentiontoensuringgoodcustomeroutcomes.

Itisclear,however,thatanyfirmswhichbelievethattheycancontinuetotakeanarrowcompliance

approachwillfinditincreasinglydifficulttoprovidetheevidencerequiredbytheFCA.Thismayleave

themexposedtosignificantregulatoryandreputationaldamage.Ultimately,someofthechanges

envisagedbytheFCA(resultingfromanincreasinglyconsumeristsociety,andaninterventionist

politicalbody)maymakesomebusinessmodelsobsolete.Iftheyeverwere,conductriskandconsumer

protectioncertainlynolongerrepresentabox-tickingcomplianceexercise.

Inordertomanageandembedconductandcustomer-relatedriskacrossthebusiness,insurersmust

ensuretheyhaveaclearandwell-definedapproachwhichisalignedtogoodconductandtheFCA’s

broaderrequirements.Thismustoriginatefromboardlevel,andthenbeclearlycommunicatedto

internalandexternalstakeholders.

Webelievethatastrongconductriskapproachembeddedintotheorganisationisacriticalsuccess

factorinthelonger-termviabilityofinsurancebusinesses.Inoursurvey,manyinsurerscitedother

industrieswheretheybelievecertaincompanieshavedemonstratedbetterconductthanmanyinsurers.

TheexamplesmostfrequentlyprovidedwereJohnLewisandAmazon.comintheretailsector,andVirgin

Atlanticintheairlineindustry.Theexecutiveswespoketobelievedthatthesecompaniespossessone

commontrait–theyhaveputcustomersattheheartoftheirstrategyandbusinessmodel,andthishas

beenanimportantfactorintheirprofitabilityandgrowth.Insurerswerealsokeentopointoutthatthere

arealsoplentyofexamplesofpoorconductinbothoftheseindustriestoo!

Someinsurershavealreadybeentakingboldactionoverthelastyearorso,forexamplebyremoving

allsalesincentivesforfront-linegeneralinsurancestaff,whileothershavetakenmoreofa“waitand

see”approach.Nowthatexpectationsongoodconductarebecomingclearer,andregulatoryscrutinyis

increasing,thesefirmswillhavetocatchup.Throughourworkonconductrisk,wehavecometoview

fivestepsascriticalinachievinglastingprogressinthisarea:

1. Defineyourconductriskappetite,andobtainseniorstakeholderbuy-in.

2. Performaconductriskdiagnostictoidentifychangesrequired.

3. Strengthentools,processesandcontrols.

4. Realignthebusinessmodelwithgoodcustomeroutcomes.

5. Reinforcethroughleadershipbehaviour,culture,trainingandincentives.

23 Conduct risk for insurers: Responding to a fundamental shift in regulatory expectations

Step 1.

Define your conduct risk appetite and obtain senior stakeholder buy-in

Theconductissueisnotblackandwhite.Eachinsurerneedstodecideitsownappetiteortolerancefor

conductriskandcommunicateitsconclusionsbroadlyacrossthefirminordertoinfluencebehaviour.

Indefiningriskappetite,managementneedstodefinehowfartheirfirmshouldgointermsofboth

knowing,andbeingabletodemonstrateevidencethat:

• Customersunderstandwhattheyarebuying.

• Productsaresuitableforthecustomerbuyingthem.

• Customersarereceivingacceptablelevelsofservice.

Insurersalsoneedtodefinewhatconductriskappetitemeansinpractice.Forexample:

• Towhatextentshouldallcustomersbeofferedthelowestpossibleprice?

• Howcanloyalcustomersberewarded?

• Towhatextentdoesconductriskappetiteextendtoincludethebehaviourofyourdistributors?

• Towhatextentdoesitincludetheoutcomesofotherinsurers’customers(suchasinrelationto

referralfeesinmotorinsurance)?

Thesearediscussionsthatshouldbeledbytheboard.

Oncetheconductriskappetitehasbeendefined,strongseniorstakeholderbuy-infortheriskappetite

hastobeobtained.Suchstakeholdersalsoneedtoaccepttheneedtochangetoalignwiththestated

appetite.Itisimportantthatseniorstakeholdersrecognisetheimportanceofgettingconductriskright.

Theymustalsounderstandthepotentialimplicationsofgettingitwrong,withpossiblefinesand

compensationpayments,aswellaspotentiallonger-termdamagefromtheimpactonthecompany’s

reputation.Insurersthathavebeenthemostsuccessfulatobtainingseniorstakeholdersupporthave

tendedtobethosewhereboardmembersfirmlybelievethatensuringtheirbusinessmodelisaligned

withachievinggoodcustomeroutcomesisnotonlytherightthingtodo,butisalsocommerciallythe

bestthingtodointhemedium-to-longerterm.

Accountabilitiesneedtobeagreedforconductriskmanagementandoversight,balancingthe

responsibilitiesofbusinessunitsandriskandcompliancedepartments.Oursurveyshowedthatthose

insurerswhichhadmademostprogressinimplementingaconductriskstrategyhadinvolvedboth

entitiesinabalancedway.Firmsmaywishtoidentifyanexecutivetotakeformalresponsibility.Indeed,

somefirmshaveappointedaHeadofConductRisk,orformallyincludedconductriskwithinthemandate

ofanexistingexecutive,suchastheRegulatoryRiskDirector.Responsibilitiesformanagingconduct

riskonaneverydaybasiscanthenbeintegratedintoexistinggovernancestructures,alwaysensuring

significantfront-lineinvolvementandaccountability.

4. the response

24 Conduct risk for insurers: Responding to a fundamental shift in regulatory expectations

4. the responseStep 2.

Perform a conduct risk ‘diagnostic’ to identify changes required

Intheshortterm,firmsshouldhaveacredibleandeffectiveresponseforconductriskinplaceasa

matterofpriority.Someinstitutions’instinctiveresponsehasbeentoviewconductriskjustasyet

anothersalesprocesscomplianceprogramme.However,wefeelthatthisresponsefailstounderstand

thescaleofchangethatisrequiredacrosstheirvaluechains,astheindustrymovesintothenew

Conductera.

Inourwork,weregularlycarryoutriskidentificationusinga“follow-the-money”approach,exposing

potentialareasofcustomerdetrimentbylookingatthoseareasoftheinsurer’sbusinesswhere

significantrevenuesandprofitsaregenerated.Thishasprovedtobeausefulapproach,andconduct

regulatorssuchastheUKFCAarelookingtofollowsuit.Itisimportanttonote,ofcourse,thatstrong

profitabilitydoesnotnecessarilyindicatethatthereisaconductissue.Itmerelyservesasanindicator

(oneofmany)thattheremaybeconductissuesthatshouldbeinvestigatedfurther.

Thereareanumberofpotentialcontributingfactorstopoorcustomerconduct.Itmaybehelpfulfor

insurerstogothroughthesetohelpthemidentifypotentialconductissueswithintheirportfolio.Key

factorscaninclude:

• Complexityofproduct,andtherelativesophisticationofthecustomer.

• Pricetransparencyandeaseofswitching.

• Whetherthepolicyistheactivelysoughtproductoranancillary,add-onorpolicy.

• Universalityoftheproductandsizeofthesuitablemarket.

• Irreversibility:theeasewithwhichacustomerandtheinsurercanwithdrawfromthecontract

withoutnegativeimpact.

• Thequantumofthedownsideriskforthecustomerandinsurerasaresultofpoorconduct.

• Importanceoftheproducttotheinsurer’soverallbusiness.

• Levelofcommissionbeingpaid.

• Levelofcompetitionwithintheproductline,andprofitability.

Inadditiontoachievingclarityonthecustomersegmentsandproductclassesatrisk,sixmajor

processesalongthevaluechainneedtobereviewed:

1. Product development and governance: Integrationofconductriskcriteriaintonewproductapproval

andgovernanceprocesses,includingthedefinitionofpositiveoutcomesandcorrespondingmetrics,

aswellasongoingmonitoringoftheproduct’sperformanceandindicatorsofemergingrisks.

2. Customer segmentation: Upgradingofsegmentationandprofilingtoolstocoverneeds,riskappetite,

financialexperience,eligibilityandlosstolerance.

3. Customer proposition:Increasingthedetailandsophisticationofproduct/customermatching,and

aligningcommercialtermsmorecloselytotheconceptofapositiveoutcome.

25 Conduct risk for insurers: Responding to a fundamental shift in regulatory expectations

4. Sales: Formalisationandupgradeofsalesforcestandardsandtraining,linkingqualification

levelstoproductsalesauthority,bothinternallyandatdistributors.Upgradingofsalesprocess

documentationtodemonstrateevidenceofsuitability.Developmentofoutcometestingprocedures,

suchasmysteryshopping.

5. Post sales, including claims and complaints: Activemonitoringofproductperformancetoidentify

customerdetriment.Upgradingofcustomerreportingtoincorporateriskcontent,andincreasing

dynamicreportingfrequencytoreflectrisklevels.

Muchoftheaboverelatestofront-linetoolsandprocesses,andindeedtheonusshouldbeonthefront

linetoensureitsalignmentwiththeprinciplesofgoodconductofbusiness.Ontheonehand,thisis

goodnewstothoseinstitutionsaspiringtogreaterefficiencyinriskandcompliance.Ontheotherhand,

suchfront-lineactivityrequiresoversightandmonitoring.Forthistobeeffective,firmsshouldensure

thatconductriskbecomespartoftheiroverallrisktaxonomy,andisthusfullyintegratedintorisk

identification,assessmentandmanagementprocesses.

Oversightrequiresinformationthatcansupportmanagementdecision-making.Suchinformation

shouldbebasedonmetricswhichfocusoncustomeroutcomesaswellasoninputstotheconduct

riskmanagementprocess.Asboardsincreasinglyseekoversightofconductriskperformance,we

havefoundthatindicatorssuchasmysteryshoppingresults,customeroutcometesting,profitability

metrics,customersatisfactionandadvocacy,andproductperformancestatisticscanallbeusefulin

substantiatingthecontentofreportstoboardlevel.

Incarryingouttheconductriskdiagnostic,insurersmustquantifyandprioritisethegapsidentified,for

examplebyemployingameasureofcustomervaluedetriment.Theyshouldalsoclassifyeachgapinto

oneofthreecategories:

• Gapsthatshouldbeaddressedassoonaspossible,duetoashort-termriskofFCAactionagainstthe

firm,significantconsumerdetrimentorreputationaldamage.

• Othergapsthattheinsurerisabletoaddressbyactingalone,despitethefree-riderriskandpotential

forfirstmoverdisadvantage.

• Gapsthatcanonlybeaddressedifotherinsurersdosoatthesametime(althoughiftheindustry

waitstoolongforacollectiveresponse,itmayfindthatithasalessattractivesolutionforceduponit).

Havingagreedthethrustoftheapproachanditsprincipalcomponents,firmscanthendetailthe

initiativesthattheywillpursuetoembedgoodconductofbusinessintotheirproductsandprocesses.

Theensuingworkwillinvolvetwoelements.Firstly,tools,processesandcontrolsarelikelytoneed

strengtheningtoprovideassuranceandevidencethatthoseoutcomesarebeingachieved.Secondly,

businessmodelswillneedtobereviewedtoensuretheyarefundamentallyalignedwiththeconceptof

ensuringgoodcustomeroutcomes.

4. the response

26 Conduct risk for insurers: Responding to a fundamental shift in regulatory expectations

4. the responseCase study – A life insurer has implemented a dedicated conduct programme

Alifeinsurerhasestablishedadedicatedconductriskprogrammewithaclearobjectivetoidentify

andreduceanypoorcustomeroutcomesacrosstheirbusiness.Theprogrammeissponsoredbythe

CEOandinvolvesthe1stand2ndlinesofthebusinessworkingcloselytogether.Theprogramme

hasstrongseniorstakeholdersupportandhasbeenupandrunningforthelast6months.

TheInsurerbroadlyfollowedafivestepprocess:

1. Definedconductriskstrategyandwhat‘good’lookslikefortheorganisation,includingaclear

definitionofa‘customerdetriment’measurewhichconsiderscustomeroutcomesrather

thanjustbusinessprocesses.

2. Establishedaconductprogramme,includingaformalprogrammestructure,dedicated1stand

2ndlineresourcesandaclearsetofobjectivesandmeasuresofsuccess

3. Carriedoutareviewacrossthebusinesstoidentifythemostmaterialareaswherecustomers

–generallyasaresultoftheirbehaviourorunderstanding–maynotbegettingwhatinformed

professionalsmightdeemappropriateoutcomes.

4. Foreacharea,identifiedtheleversrequiredtoreducethequantumofcustomerdetriment,

developedabusinesscaseformakingthechangesrequiredtoaddresstheissueandsetclear

targetsforreducingthisoverthenextthreeyears.

5. Implementedtheidentifiedchanges,trackedtheimpactonthevalueofcustomerdetrimentand

nowregularlyreportonprogresstotheboard.

Bywayofexample,withinitsannuitiesbusinesstheInsurerestimatedthat20%byvalueof

itsDefinedContributionpensioncustomerflowswerepurchasingastandardannuity,whena

proportionwouldhavebeeneligibletopurchaseanenhancedannuitywhichthefirmdoesnot

offer.Whilsttheannuityratesofferedwereverygoodwhenmeasuredagainstconventionalrates

inthemarketfortheOpenMarketOption,anddisclosuresincustomercommunicationsarefully

compliant,effectivelyasmallproportionofthesecustomersweremakingapotentiallyuninformed

choiceandthiswasleadingtocustomerdetriment.Thefirmestimatethatthevalueofthelossto

impactedcustomerswasgreaterthan£5mperannum.

Theleversforaddressingthiswereidentifiedandaprojecthasbeensetuptoclosethegapin

aphasedmanner.Thebenefitsincludedwithinthebusinesscaseincludeelementsforboththe

companyandthecustomer.

TheCEOfeelsverystrongly(andhastheboard’ssupport)thatthevastmajorityoftheseissuescan

beaddressedinwaysthatare‘NetPresentValue(NPV)positive’oratleastclosetoNPVneutral

intermsofprofitstotheinsureroverthemediumterm.So,notonlyisfindingwaysofimproving

customeroutcomestherightthingtodo,theyalsobelieveitiscommerciallyattractivetodoit.

27 Conduct risk for insurers: Responding to a fundamental shift in regulatory expectations

Step 3.

Strengthen tools, processes and controls

Insurersneedtodeveloptheirmanagementinformationanddevelopkeymonitoringmetricstobe

abletodemonstrateevidenceofstrongcustomerserviceandgoodcustomeroutcomes.Someinsurers

haveintroduceda“conductrisktolerancescore”,whichislinkedtotheirstatedconductriskappetite

andisregularlyreportedtotheboard.Thescoreincludesmetricsrelatedtofeaturessuchasproduct

characteristics,customerexperience,customeroutcomes,salesincentivesandstaffcapabilities.While

theexistenceofthismetricinitselfwillnotnecessarilyimproveconduct,itcanbeausefultoolin

promptingdebateonconductamongtheexecutiveteamandtheboard.

“ Insurers need to find business models that really reward customer loyalty

”CEO,CompositeInsurer

4. the response

28 Conduct risk for insurers: Responding to a fundamental shift in regulatory expectations

4. the responseStep 4.

Realign business model with good customer outcomes

Themoredefensivemovesoutlinedabovearethenecessaryactionsrequiredtoavoidfines,litigation

andreducecustomercomplaints.Butacontrolframeworkisdesignedtocurtailactivityinareasdeemed

risky,notsuggestwaysinwhichtosustaintherevenuestreamsfromthoseactivities.Thereisthusarisk

thatfocusingondefensivemovesleavesastrategicvacuumatatimewheninsurerscanexpecttosee

significantdisruptionsinthemarketwithConductofBusinessprinciplesbecomingfullyembedded.

Insurersshouldthereforeprepareforthestrategicimplicationsofabusinessmodelmoreclosely

alignedwithconductriskconcerns.Webelievethatthesestrategicimplicationswillbefeltinatleast

threeareas:

• Ensuringsuitabilityandappropriatetargeting.

• Deliveringvalueformoney.

• Respondingtoagrowingagendaforequality.

• Harnessingtechnologicalinnovationatapaceacceptabletoconsumers.

ItislikelythatabusinessmodelmorecloselyalignedwithgoodConductofBusinesswillinvolvea

simplerandmoretransparentlypricedproductrange,andanarguablyfairerdistributionofinsurers’

costsandrevenuesacrosstheircustomerbaseasaresult.Suchchangescanresultinsignificantshifts

ofmarketsharebetweenfirmswhicharewellpreparedforchangeandhaverelevantplansinplace(such

asthroughusingcustomeranalyticstogainabetterunderstandingoftheirneeds),andfirmswhichare

merelyreactive,remainingresistanttochangebeforedeliveringanuncoordinatedresponse.

Onespecificexampleconcernsgeneralinsurers.Currentlythestrategyofmostgeneralinsurersinvolves

offeringlowerpremiumstonewcustomers,assumingtheycanmakeprofitsonthisbusinessinlater

yearsaspremiumsincreaseforthosecustomerswhoremain.

Likewise,itisclaimedthatmanyannuitycustomersfailtogetagooddealastheydonotshoparound,

andprovidersknowinglyexploitthisinertia.

Inboththese,andother,examples,theremustbeariskthatthesepracticeswillnotbesustainable,and

thereforethatbusinessmodelsbasedonthesepracticeswillnotbesustainable.

Webelievethatboards,andspecificallynon-executivedirectors,havearoletoplayinchallenging

existingmodelsandunderstandingthesensitivityofthebusinesstosignificantchangestothestatus

quo.Forexample,whatwouldhappenifpricedifferentialsbetweennewandexistingcustomerswere

projectedtoshrinksignificantlyordisappearwithinthenextfiveyears?Oriftherewasasignificant

increaseinconsumerstakingadvantageoftheopenmarketandshoppingaroundforthebestannuity

solution?Wouldtheboardbewillingtocontinuetowritebusinessinthesameway?Wouldtheinsurer’s

operatingmodelbecost-effective?

29 Conduct risk for insurers: Responding to a fundamental shift in regulatory expectations

Step 5.

Reinforce through leadership behaviour, culture, training and incentives

Conductriskmanagementwillfailifthetoneatthetopandthemessagesgiventostaffthroughhiring,

trainingandperformancemanagementdonotreinforcethestrategicpositioningonconductrisk.

Organisationsneedtoformarealisticviewofthecultureintheirorganisation,andseektounderstand

theunwrittengroundrulesandrelationshipswhichinfluencethewaydecisionsaretakenthroughoutthe

organisation.Ahelpfulstartingpointcanbea“culturalthermometer”testtounderstandtheunderlying

cultureofthefirm,comprisingsurveys,interviewsandfocusgroupswhichinvolveseniormanagement,

thefrontline,themiddleandbackofficeandclients.

Aseriesofactionscanthenbeidentifiedrelatingtoleadershipdevelopment,incentives,trainingand

development,recruitmentandrewards,toolsandprocesses,allseekingtoembedandreinforcethe

desiredculturalvalues.Theseactionswillhelptoensurethatpeopledowhatisrighteveninsituations

thatarenotforeseenbypolicyandprocess,therebyreducingexposuretoconductrisk.Theywillalso

servetokeepoverallriskandcontrolspendingincheck.

Inthesalesarena,incentivesareoneofthemostcriticaldeterminantsofbehaviourandhavebeen

identifiedasasignificantcontributortopastfailings.Wecontinuetofindthroughourworkthat

incentives,intheirsimplestform,canleadtogoodstaffbehaviours,encouragingstafftounderstand

customerneedsandtodirectcustomerstosuitableproducts.Forexample,conductcouldbemanaged

byonlygivingcreditforhigh-qualitysaleswherecustomerneedsandsuitabilityhavebeenclearly

demonstrated,andbyensuringrewardsarebasedonabalancedsetofmetrics(forexample,through

meetingneeds,anddisplayinggoodserviceandgoodcolleaguebehaviours).

Notwithstandingtheabove,however,itistheseniorleadersofthefirmandhowtheybehave,act,

makedecisionsandcommunicatethatwillhavethemostimpactoncreatingandreinforcingthe

cultureofthefirm.

4. the response

30 Conduct risk for insurers: Responding to a fundamental shift in regulatory expectations

5. the insurance industry working together

5. The insurance industry working together

Whileeachindividualinsurermustdevelopitsownresponsetothemarketconditionscreatedby

theFCA,thereisscopeforcollectiveactiontohelpcreatetherightregulation,andhelpensuregood

customeroutcomes.

Overtheyears,collectiveaction,ledbytheAssociationofBritishInsurers(ABI),hassoughttopush

throughimprovementstocustomeroutcomes.Forexample,theRaisingStandardsprogrammeandthe

CustomerImpactScheme,whicheachenjoyedbroad,ifnotfull,participationfrominsurers,wereright

fortheirtime,andcouldpointtorealimprovementsintheirwake.

Weconsiderthatindustry-drivencollectiveactionthereforeremainsbeneficialinthefollowingareas:

1. Scrutinisingproposedregulationtoensurethatmarketreformsarenotagainsttheinterestsof

competitionandcustomers,forexamplethroughidentifyingthepotentiallosersaswellasthe

potentialwinnersfromregulatoryproposals.

2. CreatingCodesofConductthatactasaguidetoensurethatinsurersdelivergood

customeroutcomes.

3. Providingaforumtodiscusshowtoaddressissueswhichinsurerswillnottackleontheir

ownduetotheriskoffirst-moverdisadvantage.

WeacknowledgethattheABIisamemberorganisationandnotanaccreditingbodyorsupervisorand

thatCompetitionLawlimitscollectiveactioninsensitiveareassuchasduelpricing.However,theFCA

hasclearlysetoutthatitwillintervenetoimprovetheoperationofthemarket,anditislikelythatany

responseoutlinedandpromotedbytheregulatorwouldbelesswelcometotheindustrythansomething

itwasabletodesignitself.

31 Conduct risk for insurers: Responding to a fundamental shift in regulatory expectations

6. conclusion6. Conclusion

OurdiscussionswithCEOsandseniorexecutivesfromacrosstheinsuranceindustrywereopenand

informative.Theyrevealedthatmostinsurershavemadesignificantinvestmentstoimprovecustomer

outcomes,butalsothatinsurersdonotgenerallysharethesameviewsastheFCAabouttheextentof

customerdetrimentandthescaleofchangerequired.Indeed,thereisarealconcernintheindustrythat

toomuchregulationcouldreducecompetitionandinnovationtothedetrimentofconsumers.

Itisimportantforinsurerstoidentifythesignificanttrendsofopenness,transparencyandaccountability

thatwillshapethenatureofconductregulation.Eachinsurer,withtheactiveinvolvementoftheirboard,

willneedtodecidewhatimpactthesetrendsmayhaveontheirbusinessmodel,howtheywantto

respondandtheirappetiteforregulatoryandreputationalrisk.

Inourexperience,thisexerciserequiresastructuredapproachtoassesstheviabilityofcurrentbusiness

models,andtoidentifywhatbusinesspracticesandoperationsneedtochange.Allofthismustbe

supportedbyastrongfocusonensuringthefirm’sleadersandculturesettherighttoneforthebusiness.

InsurerswhoconsiderthatconductriskisnomorethananevolutionofTCFarelikelytofindthemselves

onthewrongsideoftheFCA.Theywillalsofallbehindasotherinsurersdevelopbusinessmodels,

productsandculturesmoreattunedtotoday’smarket.

32 Conduct risk for insurers: Responding to a fundamental shift in regulatory expectations

appendix: list of participating firm

sAppendix: List of participating firms

Wearegratefultothefollowingfirmsfortheirparticipatinginourresearch.

• AegonUK

• AgeasUK

• AllianzUK

• Amlin

• AvivaUK&IrelandGI

• AvivaUK&IrelandLife

• AXAUK

• BUPA

• Catlin

• DirectLineGroup

• FriendsLife

• Hiscox

• LegalandGeneral

• LVGI

• LVLife

• PartnershipAssurance

• PrudentialUKandEurope

• ReAssure

• RoyalLondonGroup

• StandardLife

• ZurichUKGI

• ZurichUKLife

33 Conduct risk for insurers: Responding to a fundamental shift in regulatory expectations

who to contactCIIDavid Ross

DirectorofCommunications

CharteredInsuranceInstitute

20Aldermanbury

LondonEC2V7HY

Email:[email protected]

About the Chartered Insurance Institute (CII)

Professionalism in practiceTheCIIistheworld’sleadingprofessionalorganisationforinsuranceandfinancialservices,withover110,000membersin150countries.

Wearecommittedtomaintainingthehigheststandardsoftechnicalexpertiseandethicalconductintheprofessionthroughresearch,educationandaccreditation.

www.cii.co.uk

Who to contact

About Oliver Wyman

OliverWymanisagloballeaderinmanagementconsultingthatcombinesdeepindustryknowledgewithspecialisedexpertiseinstrategy,operations,riskmanagement,operationaltransformation,andleadershipdevelopment.

Formoreinformation,pleasecontactthemarketingdepartmentbyemailatinfo-FS@oliverwyman.comorbyphoneatoneofthefollowinglocations:

EUROPE,MIDDLEEAST,AFRICA:+442073338333

NORTHAMERICA:+12125418100

ASIAPACIFIC:+6565109700

Oliver WymanTim Kirk, Partner

Sean McGuire, Partner

OliverWyman

55BakerStreet

LondonW1U8EW

Email:[email protected]

34 Conduct risk for insurers: Responding to a fundamental shift in regulatory expectations

About the authors

Sean McGuire, Tim Kirk, Richard Thornton andJames Bryan areLondon-basedPartnersin

OliverWyman’sFinancialServicespractice.

Copyright © 2013 Oliver Wyman. All rights reserved.

Thisreportmaynotbereproducedorredistributed,inwholeorinpart,withoutthewrittenpermission

ofOliverWymanandOliverWymanacceptsnoliabilitywhatsoeverfortheactionsofthirdpartiesin

thisrespect.

about the authors

ReportQualifications/AssumptionsandLimitingConditions

Thisreportisintendedtobereadandusedasawholeandnotinparts.Separationoralterationofanysectionorpagefromthemainbodyofthisreportisexpresslyforbiddenandinvalidatesthisreport.

Thisreportisnottobeused,reproduced,quotedordistributedforanypurposeotherthanthosethatmaybesetforthhereinwithoutthepriorwrittenpermissionofOliverWymanandtheCharteredInsuranceInstitute.Noattemptshallbemade,bycorrelationofdataorotherwise,toascertaintheidentityofanyparticipanttowhichany“blind”dataisattributable.Ifsuchidentificationisinadvertentlymade,itshallbekeptconfidentialandnotusedforanypurposewhatsoever.Furthermorethereportmaynotbeusedasameansforcompetingcompaniesorfirmstoreachanyunderstanding,expressorimplied,whichrestrictscompetitionorinanywayimpairstheabilityofanycompanyorfirmtoexerciseindependentbusinessjudgmentregardingmattersaffectingcompetition.

Informationfurnishedbyothers,uponwhichallorportionsofthisreportarebased,isbelievedtobereliablebuthasnotbeenverified.Nowarrantyisgivenastotheaccuracyofsuchinformation.Publicinformationandindustryandstatisticaldata,arefromsourceswedeemtobereliable;however,wemakenorepresentationastotheaccuracyorcompletenessofsuchinformationandhaveacceptedtheinformationwithoutfurtherverification.

Thefindingscontainedinthisreportmaycontainpredictionsbasedoncurrentdataandhistoricaltrends.Anysuchpredictionsaresubjecttoinherentrisksanduncertainties.Inparticular,actualresultscouldbeimpactedbyfutureeventswhichcannotbepredictedorcontrolled,including,withoutlimitation,changesinbusinessstrategies,thedevelopmentoffutureproductsandservices,changesinmarketandindustryconditions,theoutcomeofcontingencies,changesinmanagement,changesinlaworregulations.OliverWymanandtheCharteredInsuranceInstituteacceptnoresponsibilityforactualresultsorfutureevents.

Theopinionsexpressedinthisreportarevalidonlyforthepurposestatedhereinandasofthedateofthisreport.Noobligationisassumedtorevisethisreporttoreflectchanges,eventsorconditions,whichoccursubsequenttothedatehereof.

Thisreportdoesnotrepresentinvestmentadvicenordoesitprovideanopinionregardingthefairnessofanytransactiontoanyandallparties.

Therearenothirdpartybeneficiarieswithrespecttothisreport,andOliverWymanandtheCharteredInsuranceInstitutedonotacceptanyliabilitytoanythirdparty.Inparticular,neitherOliverWymannortheCharteredInsuranceInstituteshallhaveanyliabilitytoanythirdpartyinrespectofthecontentsofthisreportoranyactionstakenordecisionsmadeasaconsequenceoftheresults,adviceorrecommendationssetforthherein.

Ref:CII_conductrisk(12/13)CI3J_8420

©TheCharteredInsuranceInstitute2013

The Chartered Insurance Institute 42–48HighRoad,SouthWoodford,LondonE182JPtel:+44 (0)20 8989 8464email:[email protected]:www.cii.co.uk

@CIIGroup Chartered Insurance Institute