Resource Planning Advisory Group Workshop - FortisBC · RPAG Wor kshop Feb 2013 RPAG Wor kshop Jan...

51

Resource Planning Advisory Group Workshop February 9 th , 2012

Transcript of Resource Planning Advisory Group Workshop - FortisBC · RPAG Wor kshop Feb 2013 RPAG Wor kshop Jan...

Resource Planning Advisory Group

Workshop

February 9th, 2012

Agenda

8:30 a.m. –9:00 a.m. Sign In

Breakfast

9:00 a.m. –9:15 a.m. Introduction

Welcome & LTRP Update

9:15 a.m. – 9:30 a.m. Board bus for site visit and travel to Waste Management site

9:30 a.m. – 10:30 a.m. Tour of the Waste Management CNG Fueling Station

10:30 a.m. – 10:45 a.m. Board bus and travel back to Executive Plaza Hotel

10:45 a.m. – 11:00 a.m. Settle back into meeting room – finish discussion on Transportation

11:00 a.m. – 12:00 p.m. Planning Environment

Energy Policy Environment

12:00 p.m. – 1:00 p.m. Lunch

1:00 p.m. – 2:00 p.m. Gas Supply and Regional Infrastructure

Overview of industry projections for supply, demand, and price

2:00 p.m. – 2:15 p.m. Break

2:15 p.m. – 3:15 p.m. Review FortisBC’s Scenario Development work

Summary of Jan. 10 workshop and approach to incorporating RPAG feedback

3:15 p.m. – 3:30 p.m. Wrap Up & Next Steps

2

Natural Gas for Transportation

Jason Wolfe, Manager, Market Development

February 9th, 2012

Natural Gas for Transportation Largest opportunity for natural gas load growth

and GHG emissions reductions

• Challenges: • Up-front vehicle cost differential

• Awareness of technological improvements in NGV

• Lack of fuelling infrastructure for return-to-base fleets

• EEC incentives in flux

• Key elements: • “Anchor-tenant” fueling model

• ‘User-pay’ vs. public refueling

• Monthly ‘take-or-pay’ volumes

• Cost recovery over term of contract

• Mitigation of stranded assets

4

BC’s GHG Emissions by Sector

Source: LiveSmart BC website

5

Transportation sector is

BC’s largest GHG

source

5

NG is less carbon intensive than conventional fuels

Source: LCFRR Intentions Paper

•Conventional CNG has a net carbon intensity value that is 38% lower than

reformulated gasoline and 28% lower than ultra-low sulphur diesel.

• Conventional LNG has comparable reductions in net carbon intensity

6

Historical Diesel Pricing vs. NG (DLE)

Prices shown for NGT (DLE) are current market retail

prices in BC; contract prices would be lower

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

1.80

Av

g V

an

co

uv

er

Reta

il P

rices

CA

D $

.00 P

er

Lit

re

Calendar Years

NGT & Diesel Vancouver Pump Prices

Diesel

NGT DLE

7

Waste Management Project – 20 NG Trucks

• Will displace 468,000 litres per year of diesel

• GHGs reduced by 213 tonnes per year

• Equivalent to taking 41 passenger cars off the road

• Fuel savings ~50%

• Plan to ramp up to 100 vehicles

8

Vedder Transport Project – 50 NG Trucks

• Will displace 3.6 million litres per year of diesel

• GHGs reduced by 3,754 tonnes per year

• Equivalent to taking 722 passenger cars off the road

• Fuel savings ~50%

9

Purpose of Today’s Workshop:

Discuss and Developing a Better Understanding of

FortisBC’s Current Planning Environment

2013 LTRP Timeline

Jan 2012 Mar 2013

Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar

2013

LTRP Submission

Oct 2012

RPAG WorkshopFeb 2013

RPAG Workshop

Jan

Resource Plan Stakeholder Forum

· Forecast Update

· Asset Management

· Technology Discussion

· Forecast Results

· Resource Analysis

· Draft Outcomes

· LTRP Outcomes & Summary

· Action Plan

Jan 2012

RPAG Scenario Workshop

Feb 2012

RPAG Workshop

· Planning Environment· Energy Policy Environment· Gas Supply and Regional

Infrastructure

Sep - Nov

Resource PlanCommunity Consultation

Mar - Apr

Resource PlanCommunity Consultation

May 2012

RPAG Workshop

Objectives and Topics

• Familiarize RPAG members with aspects of the energy

planning environment.

• Discuss recent energy policy shifts

• Explain and discuss the Demand Side Management

Regulation amendments

• Describe and discuss current natural gas supply issues

• Discuss energy prices and competitiveness

• Provide an update on the Scenario Development work

Energy Policy Environment

Ken Ross, Integrated Resource Planning Manager

February 9th, 2012

• Abundant sources of energy (electricity and natural gas)

• Low electricity rates compared to other jurisdictions (Heritage Rates)

• GHG emissions output profile is different

• Transportation

• Fossil fuel production

• Little emission from electricity

• Energy policy until now promoting energy efficiency and use of electricity

and other green energy alternatives

• British Columbia’s Energy Objectives

• New Natural Gas Strategy

• Different type of new building stock being developed

BC’s Energy Environment Unique from other jurisdictions in Canada

14

Population Growth

0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

7,000,0001

98

6

19

89

19

92

19

95

19

98

20

01

20

04

20

07

20

10

20

13

20

16

20

19

20

22

20

25

20

28

20

31

20

34

Northeast

Nechako

North Coast

Cariboo

Kootenay

Thompson-Okanagan

Vancouver Island / Coast

Mainland / Southwest

Historic Projected

source: BC Stats

Sept. 2011

BC projected average annual growth = 1.4%

Current Regulation and Policies Environmental Focus

• BC Energy Plan

• Greenhouse Gas Reductions Targets Act

• 6% below 2007 levels by 2012

• 16% below the 2007 levels by 2016

• 33% below 2007 level by 2020

• 80% below 2007 level by 2050

• BC Climate Action Charter

• Carbon neutrality by 2012

• Offset Emissions Regulation

• Carbon Tax Act

• $30 per tonne as of July 1, 2012

• Clean Energy Act

• Amendments to the Utilities Commission Act

• Amendments to DSM Regulation

• New Natural Gas Strategy

2007

2012

16

Signals of Changing Energy Policy:

Review of BC Hydro June, 2011 (Report)

• Forecasted electricity rate increases over the next 10 years for BC Hydro give

rise to reevaluating energy policy

• “We recommend that BC Hydro and the province:

• Evaluate alternative definitions and timelines for government’s self-sufficiency policy that meet the

needs of the province and ratepayers in a way that is sustainable for the long term.

• Burrard Thermal Generation Station continue to be used as a source of back-up energy as well as

for voltage stabilization”

• Natural gas usage in BC currently not considered under the Clean Energy Act.

• BC Hydro - limited ability to leverage this resource beyond 7% of total

generation.

• Market analysis - natural gas price will continue to be low over at least the

medium term, - potentially a desirable and inexpensive generation choice

17

Natural Gas Supply Abundance

18

BC’s Natural Gas Strategy - Feb 3, 2012

• Natural Gas recognized by the provincial government as a

“Climate Solution”:

• Develop a revised Energy Efficient Buildings

Strategy in 2013.

Using natural gas efficiently in BC not only

reduces emissions; it also reduces the cost

of doing business, increases productivity and

improves the standard of living that British

Columbians have come to expect.

• Encourage biomethane opportunities

• Offering consumers low-carbon natural gas

19

BC’s Natural Gas Strategy (continued)

• Promote use of high efficiency natural gas electricity

generation in export markets, and in specific markets in

BC to meet the demand for capacity

• New and expanded uses of natural gas in BC, in the

transportation sector

• BC will work to introduce new regulation under CEA to advance

natural gas vehicle program

• framework for a planned five-year,

$62 million program to reduce

transportation emissions

20

Changing Situation

GHG Emissions

Reduction Targets

Cost Pressures

Energy Diversification

Socio-economic Issues

Regional Implications

21

• Revenue Requirement Application Decision Pending

• Amalgamation/Rate Design

• Suspended pending resubmission in March

• Biomethane

• Program up and running to residential and commercial customers

• Two supply contracts approved (Catalyst and Columbia Shuswap Regional District)

• Natural Gas for Transportation Fuelling

• Expenditures and contract approval for first CNG project (Waste Management)

• General Terms & Conditions for future projects (expecting endorsement)

• Thermal Energy Services

• First project offered under FEI – Delta School District - currently under regulatory

review

• Energy Efficiency and Conservation

• Sought approval of increased EEC expenditures in the 2012-2013 RRA, currently

awaiting Commission Decision

• AES Inquiry

• Role of utilities in new product and service offerings in a regulated environment

Regulatory Update

22

Demand Side Management Regulation

Amendments

Sarah Smith, Manager, Energy Efficiency &

Conservation

February 9th, 2012

Amended Demand Side Management

Regulation

• DSM Benefit/cost analysis

• Low gas cost environment

• Some worthwhile programs challenged by previous

iteration of DSM Regulation

• Especially residential and low-income

• Introduction of Modified Total Resource Cost Test

• Avoided cost based on Zero Emission Energy Alternative

• 15% adder for Non-Energy Benefits

• 33% portfolio impact cap

• Utilities Cost Test

• Specified DSM

• Standards Attribution

24

Natural Gas Supply

Mike Hopkins, Manager, Commodity and Price Risk

February 9th, 2012

The “Shale Gale” Has Taken Over

Technology and cost improvements have increased supply

certainty 26

Gas Prices Disconnected from Other Fuels

• NYMEX gas prices remain disconnected from other competing fuels

• NYMEX gas prices are lowest levels in almost 10 years 27

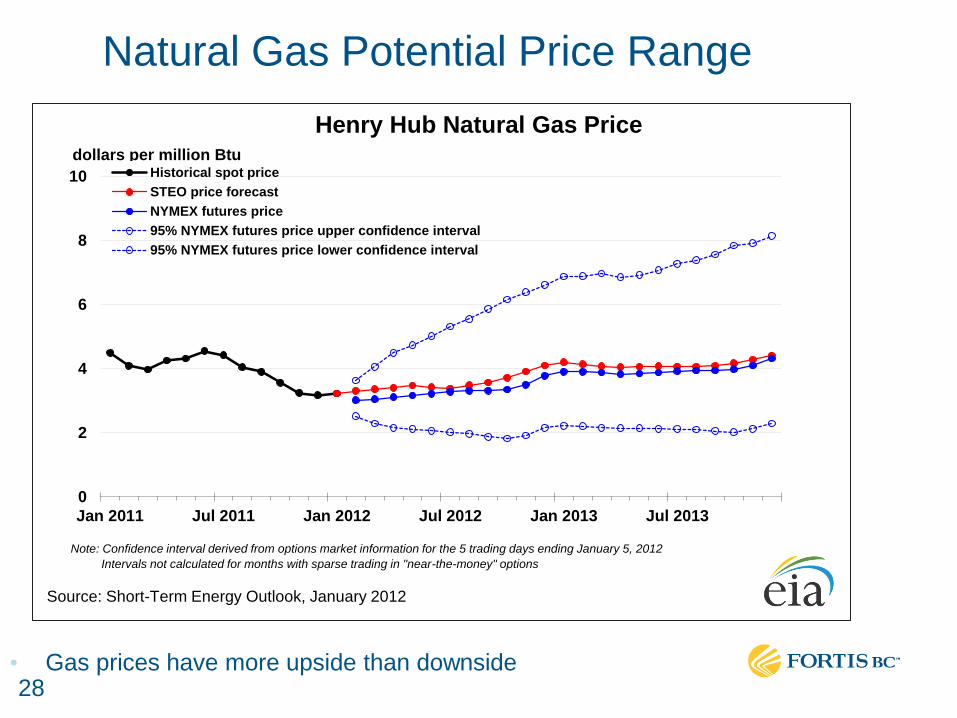

Natural Gas Potential Price Range

• Gas prices have more upside than downside

0

2

4

6

8

10

Jan 2011 Jul 2011 Jan 2012 Jul 2012 Jan 2013 Jul 2013

Henry Hub Natural Gas Price

Historical spot price

STEO price forecast

NYMEX futures price

95% NYMEX futures price upper confidence interval

95% NYMEX futures price lower confidence interval

Note: Confidence interval derived from options market information for the 5 trading days ending January 5, 2012

Intervals not calculated for months with sparse trading in "near-the-money" options

dollars per million Btu

Source: Short-Term Energy Outlook, January 2012

28

Why higher gas prices in the future ?

• Producers cutting back on gas drilling

• Increased demand for power generation

• Increased industrial demand

• Growth in natural gas vehicles (NGV’s)

• LNG exports

29

Coal Plant Retirements Increasing Gas Demand

30

Proposed LNG Export Facilities

• Multiple LNG export terminals proposed in the US

• Several facilities proposed for northern BC 31

Global LNG Spot Prices ($US/MMBtu)

• North America benefitting from abundant shale gas and depressed demand

32

FortisBC Regional Gas Market

British

Alberta

Columbia

Fort

Nelson

Niska

McMahon

Pine

River

TCPL

Northwest Pipeline

NWP

PNG

Rocky

Mountain

Basin

Western Canada

Sedimentary Basin British

Alberta

Columbia

Fort

Aitken

Creek

AECO

Jackson

Prairie

McMahon

Pine

River

Station 2

Northwest Pipeline

Kingsgate Sumas

NWP

PNG

Mist

Rocky

Mountain

Basin

Western Canada

Sedimentary Basin

SCP FEVI

WA

OR

Market Supply

Market

Storage

LNG

Storage

Mt.Hayes

Tilbury

33

Regional Peak Day Demand vs. Capacity

Mt. Hayes

LNG Storage

Winter

peak day

capacity is

constrained

in the I-5

region over

the long

term

34

BC Supply offsetting Alberta declines

35

Northeast BC Developments - TransCanada

TCPL Pipeline

expansions

into northeast

BC

36

Northeast BC Developments - Spectra

Spectra

pipeline and

plant

developments

37

Spectra T-South Enhanced Service

• Spectra utilizing part of FEI’s

Southern Crossing Pipeline

• Shippers have option to flow to

Huntingdon or Kingsgate

• 87 MMcf/d available in total

• May 1, 2010 - Oct 31, 2014

• $20 million to FEI Core customers

over contract period

38

Kingsvale-Oliver Reinforcement Project (KORP)

• Expansion of T-South Enhanced

Service

• 161 km of 24 inch looping from

Kingsvale-Oliver in BC

• Bi-directional using Southern

Crossing Pipeline

• Expected in-service 2015

• Optimizes existing infrastructure

in an integrated system with

Spectra T-South

KORP

39

Other Regional Developments

Cross Cascades

Ruby Pipeline

KORP

I-5 region

peak day

constraint

zone

40

Summary

• Low gas prices for now – due to strong supply and weak

demand

• BC supply growth - helping offset declines in Alberta

• Demand expected to increase in the future

• Pacific Northwest - expansion required now in the region to

meet future demand growth

• FortisBC - opportunities to encourage BC supply to our region

41

Electricity Prices

Ron Zeilstra, Resource Development Manager

February 9th, 2012

Price Forecasts Wholesale Market Curve vs. New Resources Market Curve for Energy

and Capacity

43

Scenario Update

Incorporating RPAG Feedback

Ken Ross, Integrated Resource Planning Manager

February 9th, 2012

A. Define

• Define the question and parameters

• Define a starting point or status quo

B. Explore

•Identify trends and forces •Identify uncertainties and importance •Rank uncertainties and importance •Select scenario themes

C. Build

• Flesh out scenario future worlds

• Write scenario stories

• Test the model

D. Use

• Develop and assess strategies

• Ongoing monitoring and assessment of scenarios and strategies

Steps in Scenario Planning - Background

Integrated Resource Planning

Stakeholder

Engagement Progress

45

Critical Uncertainties 1

46

Critical Uncertainties 2

47

RPAG Scenarios -

Visions of Future A. Define B. Explore C. Build D. Use

Decentralized Energy

Markets (Self Generation)

Centralized Energy

Markets (Grids)

Positive Perception of

Natural Gas Negative Perceptions

of Natural Gas

48

• High demand for

natural gas

• High demand for

renewables

• High fuel switching

capability

• Lowest natural gas

demand

• Highest demand for

renewables

• Policy driving

incentives for

alternatives &

energy efficiency

• Low natural gas

demand

• High natural gas

demand

• High industrial

demand for natural

gas

• Moderate gas price

Scenarios -

Visions of Future

Pricing Carbon

Doing More with Less

Demand Renaissance

Limited Choices

A. Define B. Explore C. Build D. Use

Rapid Technological

Advancement

Slow Technological

Advancement

Constricted Supply Abundant Supply

49

Incorporating RPAG Feedback

• List and note RPAG Critical Uncertainties and relative

placement on matrix

• Incorporate the critical uncertainties and issues identified

by the RPAG into FortisBC scenarios and analysis, and

report back to the RPAG as to how this was done.

• Examine each of the 48 factors identified by the RPAG,

addressing the long term directional impacts on

supply/demand, and outline how each factor fits into the

FortisBC scenarios, or how it will be considered in the

analysis

50

Next Steps

51

Jan 2012 Mar 2013

Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar

2013

LTRP Submission

Oct 2012

RPAG WorkshopFeb 2013

RPAG Workshop

Jan

Resource Plan Stakeholder Forum

· Forecast Update

· Asset Management

· Technology Discussion

· Forecast Results

· Resource Analysis

· Draft Outcomes

· LTRP Outcomes & Summary

· Action Plan

Jan 2012

RPAG Scenario Workshop

Feb 2012

RPAG Workshop

· Planning Environment· Energy Policy Environment· Gas Supply and Regional

Infrastructure

Sep - Nov

Resource PlanCommunity Consultation

Mar - Apr

Resource PlanCommunity Consultation

May 2012

RPAG Workshop

Other Discussion Topics?